Middle East Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

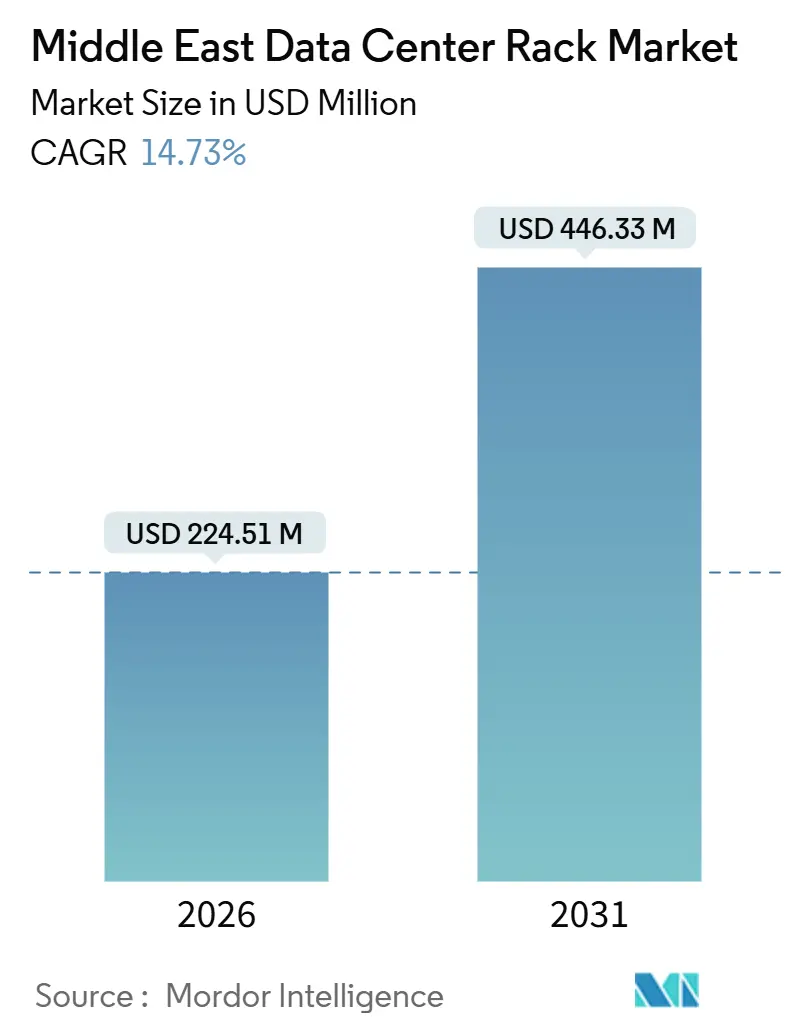

| Market Size (2026) | USD 224.51 Million |

| Market Size (2031) | USD 446.33 Million |

| Growth Rate (2026 - 2031) | 14.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Data Center Rack Market Analysis by Mordor Intelligence

The Middle East Data Center Rack Market size is estimated at USD 224.51 million in 2026, and is expected to reach USD 446.33 million by 2031, at a CAGR of 14.73% during the forecast period (2026-2031). Demand is accelerating because hyperscale clouds are localizing capacity, sovereign-AI mandates require on-shore computing, and operators are standardizing on high-density, enclosed cabinets that support liquid or rear-door cooling. Full-length 42U racks remain dominant, yet edge rollouts tied to 5G and micro-modules are lifting shipments of half-height enclosures. Saudi Arabia and the United Arab Emirates account for the bulk of new deployments, but Oman and Jordan are emerging with specialized edge and colocation projects. Supply chains are in flux as local-content rules reward knock-down kits and regional fabrication, while heat-intensive GPU clusters are pushing designers toward liquid cooling.

Key Report Takeaways

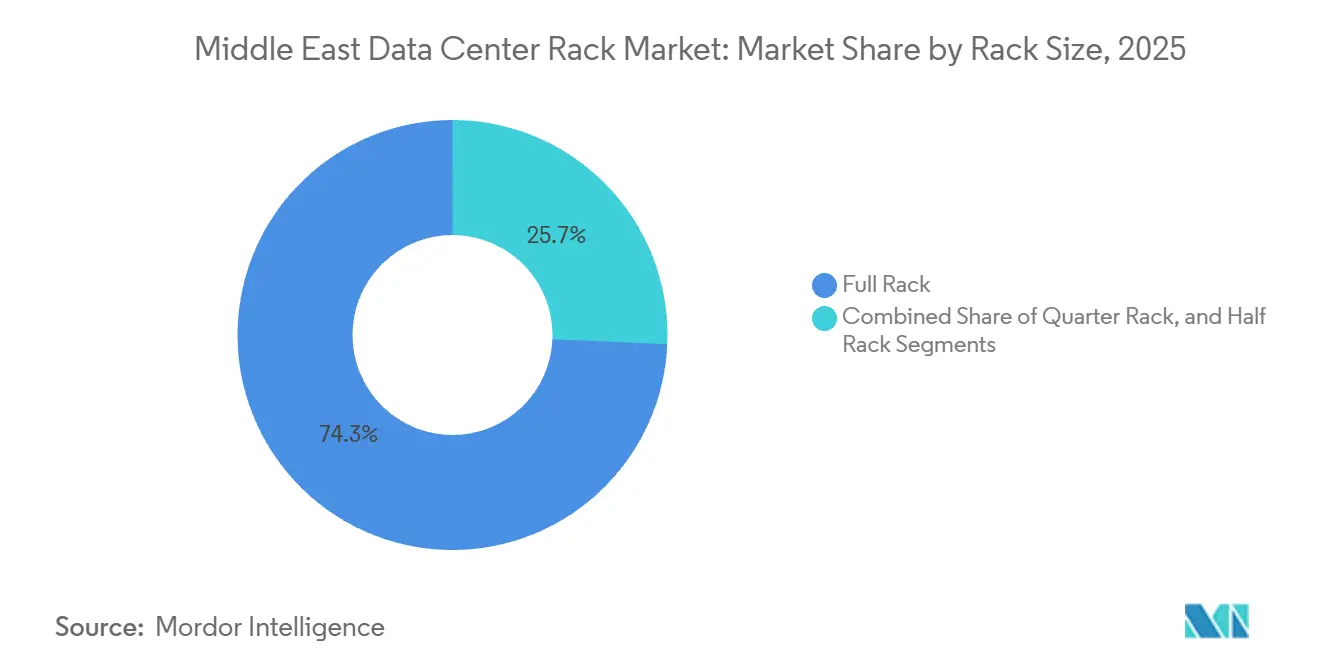

- By rack size, full racks held 74.32% of Middle East data center rack market share in 2025, while half racks are projected to expand at 15.53% CAGR through 2031.

- By rack type, enclosed cabinets captured 79.33% revenue share in 2025, and this format is forecast to grow at 15.67% CAGR to 2031.

- By tier classification, Tier 3 led with 56.21% share in 2025, whereas Tier 4 racks show the highest projected CAGR at 16.12% over 2026-2031.

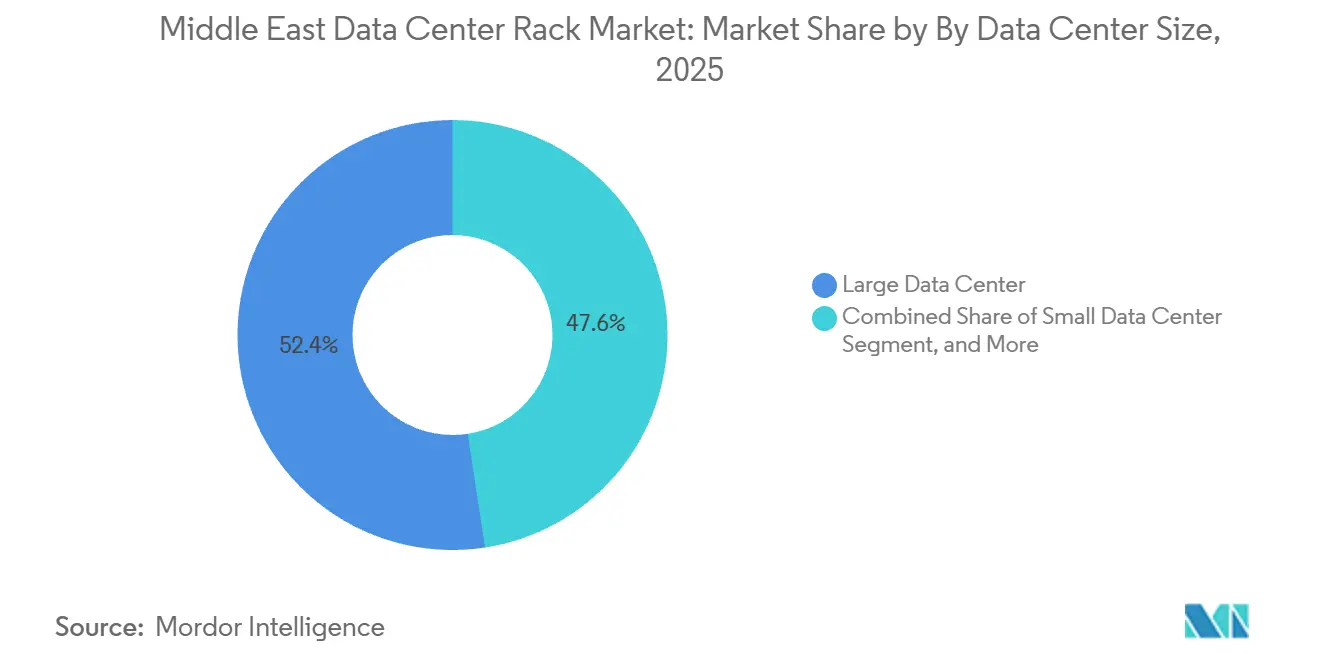

- By data center size, large facilities represented 52.42% of shipments in 2025, yet hyperscale sites are expected to rise at 15.71% CAGR during the outlook.

- By data center ownership, colocation providers commanded 51.53% share in 2025, while hyperscalers and cloud service operators are set to advance at 15.82% CAGR over the forecast window.

- By country, Saudi Arabia led with 39.35% revenue share in 2025, while the United Arab Emirates is forecast to expand at 16.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

The conditions observed in Middle east are shaped as much by international forces as by domestic ones. Mordor Intelligence’s data center rack market research places those conditions within the broader global frame.

Middle East Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale Build-Outs by Cloud Majors in Saudi Arabia and UAE | +3.8% | Saudi Arabia, UAE, spillover to Oman | Medium term (2-4 years) |

| Accelerated Local-Content Requirements Driving On-Shore Colocation Demand | +2.9% | Saudi Arabia, UAE, Jordan | Short term (≤ 2 years) |

| 5G-Led Edge Sites Requiring Micro-Module Racks | +2.4% | UAE, Saudi Arabia, Oman | Medium term (2-4 years) |

| Sovereign-AI and HPC Investments in Gulf States | +3.2% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Renewable-Energy PPA Incentives Lowering Opex for Rack Densification | +1.6% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Micro-Climate Resistant Enclosures for Desert Environments | +1.4% | GCC-wide with focus on Saudi Arabia and UAE | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscale Build-Outs by Cloud Majors in Saudi Arabia and UAE

Cloud platforms are rolling out multi-region footprints inside the Gulf to satisfy data-sovereignty rules, and every new availability zone translates into thousands of high-density, enclosed cabinets engineered for 20 kilowatt or higher loads. Racks must integrate cable-routing, rear-door heat exchangers, and sensor-driven airflow because AI training clusters intensify thermal output. Modular pod layouts that scale from 5 megawatts to 50 megawatts are shortening construction schedules, giving rack vendors that deliver pre-assembled kits an edge.

Accelerated Local-Content Requirements Driving On-Shore Colocation Demand

Saudi Arabia’s IKTVA and the UAE’s ICV frameworks impose 30%-40% domestic-value thresholds on technology projects, so global vendors now ship knock-down racks for final assembly in-country or partner with regional steel fabricators.[1]Saudi Arabian Government, “In-Kingdom Total Value Add (IKTVA) Program,” my.gov.sa Certification under these schemes commands price premiums yet ensures priority in bid evaluations. As local compliance expands to Jordan, the supply chain is moving from import-centric to hybrid models that split fabrication, powder coating, and final integration across multiple Gulf plants.

5G-Led Edge Sites Requiring Micro-Module Racks

Standalone 5G cores and network slicing push compute toward radio sites, retail branches, and industrial yards, and each node needs a half rack or wall-mount enclosure that tolerates temperature swings while dissipating 5-10 kilowatts. Half-height cabinets embed power distribution, closed-loop cooling, and fire suppression inside a single form factor, slashing on-site labor. Telecom operators now standardize on sealed, IP55-rated steel to protect baseband units from dust, and this requirement accelerates demand for compact racks.

Sovereign-AI and HPC Investments in Gulf States

National AI blueprints in Saudi Arabia and the UAE allocate hundreds of megawatts for large language model training, and these GPU clusters need liquid-cooled racks that handle 50 kilowatt loads or higher.[2]Qualcomm, “Qualcomm and Saudi SDAIA Partner on 200MW AI Compute Infrastructure,” qualcomm.com Vendors that integrate manifold distribution units, leak detection, and redundant pumps inside the cabinet capture premium pricing even as overall volumes stay modest. This development splits the Middle East data center rack market into a commodity air-cooled tier and a high-margin liquid-cooled tier aimed at HPC workloads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Tariffs on Steel Enclosures in Non-FTA Countries | -1.8% | Jordan, Oman | Short term (≤ 2 years) |

| Limited Availability of Tier-IV Colocation Floor Space Outside GCC | -1.2% | Jordan, Rest of Middle East | Medium term (2-4 years) |

| Growing Preference for Blade and Sled Servers Reduces Rack Count | -1.4% | GCC-wide with early adoption in UAE and Saudi Arabia | Medium term (2-4 years) |

| Water-Scarcity Regulations Limiting Liquid-Cooling Retrofits | -1.1% | UAE, Saudi Arabia, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs on Steel Enclosures in Non-FTA Countries

Jordan and some secondary Gulf states levy 5%-15% duties on finished steel products, and fully assembled racks often fall into higher tariff bands, raising landed costs. Buyers respond by sourcing local fabrication or importing flat-pack kits for final assembly, which splinters quality assurance and prolongs project timelines. To preserve margins, multinational suppliers are opening bonded warehouses in Dubai free zones, but this adds logistics complexity.

Water-Scarcity Regulations Limiting Liquid-Cooling Retrofits

Freshwater conservation policies in the UAE and Saudi Arabia limit evaporative cooling, discouraging retrofit liquid-cooling loops that rely on chilled water. Closed-loop immersion and direct-to-chip systems avoid water draw yet raise rack costs by 20%-30%, slowing adoption in legacy halls. Consequently, older data centers stay on air-cooled racks, while new hyperscale builds integrate liquid designs from day one, deepening the technology gap between facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Edge Proliferation Drives Compact Formats

Full racks command 74.32% of Middle East data center rack market share in 2025, underscoring the historical dominance of 42U footprints for colocation and enterprise halls. Yet half racks expand at a 15.53% CAGR through 2031, propelled by 5G edge rollouts that install compute in small shelters. Nokia’s 2025 Cloud RAN build in Abu Dhabi used 12U and 18U weatherized enclosures, proving how radio access networks shift away from centralized halls toward distributed nodes. Quarter racks see niche uptake for remote offices, but bulk demand will continue to cluster around the two leading sizes.

Operators favor dual portfolios, one for hyperscale halls that absorb thousands of identical 42U cabinets and another for half-height enclosures that ship fully integrated with power, cooling, and security. The approach simplifies procurement while meeting divergent thermals, with GPU clusters leaning on full racks that support 20 kilowatt power and half racks targeting edge applications running at 5 kilowatt or lower. Vendors that span both ends capture the widest wallet share, but must juggle distinct supply chains and pricing models.

By Rack Type: Enclosed Cabinets Dominate Desert Deployments

Enclosed cabinets held 79.33% of Middle East data center rack market share in 2025 and are projected to grow 15.67% through 2031. Dust ingress protection drives the preference, as IP54-rated doors shield servers from desert particulates while positive-pressure airflow improves reliability.[3]IEC, “IEC 60529 IP Rating Standards for Enclosures,” iec.ch Open-frame racks linger in test labs or Tier 1 halls, yet their share is eroding because operators pair uptime targets with stricter environmental controls.

Thermal strategies also tilt the field. Rear-door heat exchangers and in-row chillers retrofit smoothly onto sealed cabinets, letting facilities step up power density without replacing chilled-water plants. The Moro Hub solar data center in Dubai completed in 2025 and adopted sealed enclosures with rear-door exchangers to manage daytime heat using passive energy.[4]Moro Hub, “Moro Hub Completes Phase 2 of Solar-Powered Data Center,” morohub.com As AI drives 30-50 kilowatt loads, the enclosed format cements its edge, sustaining premium ASPs despite hyperscaler price pressure.

By Tier Type: Tier 4 Gains as Sovereign-AI Demands Five-Nines Uptime

Tier 3 halls accounted for 56.21% of racks in 2025, a legacy from enterprise colocation contracts that permit planned downtime for maintenance. Yet Tier 4 deployments expand at 16.12% CAGR because sovereign-AI projects and financial workloads require uninterrupted runtime. Saudi Arabia’s 200 megawatt AI compute estate, announced in 2026, mandates 2N+1 redundancy in power and cooling, pushing rack orders toward cabinets with dual PDUs and intelligent monitoring.

Higher tiering raises capital cost per rack by about 25%, but downtime costs for GPU clusters exceed USD 100,000 per hour, making Tier 4 cost-effective. Vendors that embed environmental sensors and predictive analytics into their frames help operators hit service-level objectives, creating a feature race that differentiates premium suppliers from commodity-only brands.

By Data Center Size: Hyperscale Facilities Outpace Legacy Segments

Large data centers formed 52.42% of shipments in 2025, yet hyperscale campuses will grow at 15.71% CAGR through 2031 as cloud majors deploy multi-region capacity. A single hyperscale hall can house 20,000 racks, dwarfing the 500-rack footprint typical of a large colocation site. Microsoft’s three Saudi availability zones adopted standardized 42U cabinets with 20 kilowatt thresholds, revealing the scale effect that hyperscale deals have on volume.

Standardization compresses margins because price negotiations hinge on massive unit counts, but vendors gain predictability and longer forecast horizons. Conversely, medium sites from 100-500 racks and small sites under 100 racks retain higher margins through customization. Suppliers must balance portfolio mix, channel policy, and production scheduling to optimize profitability during the hyperscale build wave.

By Data Center Type: Hyperscalers Gain Share from Colocation Providers

Colocation operators held 51.53% share in 2025, but hyperscalers and cloud service providers will pick up speed with a 15.82% CAGR, reflecting a pivot toward owned-and-operated estates. AWS and Oracle both chose captive facilities for their 2025-2026 expansions, bypassing third-party halls and negotiating directly with manufacturers. Direct procurement rewards vendors that can offer just-in-time logistics and global spares programs, but payment terms lengthen to 90 days.

Colocation providers retain a role because enterprises prefer opex renting over capex builds. They order smaller batches and require flexible rack widths, deeper cable trays, and variable PDU configurations to support mixed tenants. The divergent needs keep both segments relevant, yet growth momentum clearly favors hyperscaler footprints.

Geography Analysis

Saudi Arabia held 39.35% of Middle East data center rack market share in 2025. Vision 2030 digital policy, on-shore data mandates, and a USD 5.3 billion hyperscale commitment by AWS collectively drive demand. The Saudi Data and Artificial Intelligence Authority joined Qualcomm in 2026 for a 200 megawatt AI estate requiring liquid-cooled, 50 kilowatt racks. Local-content clauses under IKTVA incentivize assembly plants inside the Kingdom, welcoming regional manufacturers that partner with domestic steel mills.

The United Arab Emirates is forecast to grow at 16.08% CAGR from 2026 to 2031, the fastest in the region. Dubai’s role as a submarine-cable crossroads and Abu Dhabi’s sovereign-AI investments spur rack orders. Khazna’s planned 5 gigawatt AI campus and the Stargate UAE project target 1 gigawatt of GPU capacity, both specifying enclosed, liquid-ready cabinets. The UAE’s ICV scorecard pushes suppliers to localize, and the DEWA D33 efficiency mandate makes high-density racks critical to reduce cooling energy per megawatt.

Oman, Jordan, and other Middle East states represent emerging opportunities. Oman focuses on 5G edge shelters and rust-resistant enclosures for coastal humidity. Jordan courts colocation deals by offering lower power tariffs, but higher import duties on finished steel reduce competitiveness. Iraq, Lebanon, and Yemen remain hampered by infrastructure gaps, limiting rack deployments to opportunistic contracts with international agencies or telcos. Vendors must tailor go-to-market models, pairing direct sales in core Gulf markets with channel distribution and project-based bids in frontier states.

The data center rack market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as South America, Europe, and North America, along with detailed country-level analysis for Saudi Arabia, Chile, Poland, Norway, Italy, and Germany.

Competitive Landscape

The Middle East data center rack market is moderately concentrated, with global vendors like Schneider Electric, Vertiv, and Rittal maintaining strong positions through partnerships with colocation providers and hyperscale operators. Local-content mandates in Saudi Arabia and the UAE are creating opportunities for regional manufacturers offering faster, customized solutions. Competitive strategies focus on liquid-cooling, intelligent rack systems, localization, and vertical integration. Chinese manufacturers are entering the Gulf with cost advantages but face quality concerns and longer customization lead times.

Technology adoption is driving change, with pre-integrated rack solutions reducing installation time and winning hyperscale contracts. Schneider Electric’s EcoStruxure platform uses IoT and analytics to differentiate. Opportunities lie in liquid-cooled AI racks, micro-modules for 5G, and modular systems that meet IEC 60529 standards. The market is splitting into low-margin air-cooled racks and premium liquid-cooled enclosures, pressuring mid-tier suppliers to localize or integrate.

Private equity-backed manufacturers are partnering with global brands to ensure cost efficiency, while Gulf sovereign funds invest to meet localization quotas. Vertiv’s 2025 joint venture in King Abdullah Economic City highlights a shift to local assembly. Abu Dhabi’s AIQ is integrating anomaly detection into rack controllers, and Dubai partnerships are cutting replenishment cycles to ten days. Startups like Submer and Iceotope are licensing designs to vendors, accelerating market entry. Consolidation is expected as global firms acquire smaller assemblers to scale and meet warranty demands.

Middle East Data Center Rack Industry Leaders

Schneider Electric SE

Vertiv Group Corp.

Rittal GmbH & Co. KG

Eaton Corporation plc

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft and G42 broadened their UAE partnership to add several hundred megawatts of AI-ready capacity.

- January 2026: AWS commenced commercial operations of its Saudi region, fulfilling a USD 5.3 billion build plan.

- November 2025: Microsoft completed three availability zones in Saudi Arabia, deploying thousands of standardized 42U cabinets.

- October 2025: du and Microsoft opened a USD 544 million hyperscale facility in Dubai, featuring modular rack pods.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Middle East data center rack market as revenue from the sale of new, factory-built enclosures (open-frame or cabinet) that house servers, storage, and networking gear inside commercial, colocation, and hyperscale facilities across Saudi Arabia, United Arab Emirates, Israel, Qatar, Kuwait, Bahrain, Oman, Jordan, and the wider region. We count first-installation shipments only, while replacement racks are tracked as part of yearly demand.

Scope exclusion: We exclude edge micro-cabinets below 6U that go to telecom towers or retail kiosks.

Segmentation Overview

- By Rack Size

- Quarter Rack (Below 11U)

- Half Rack (12 to 22U)

- Full Rack (Above 42U)

- By Rack Type

- Enclosed Cabinet

- Open-Frame

- Wall-Mount and Micro-Edge Enclosure

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Size

- Small Data Center

- Medium Data Center

- Large Data Center

- Hyperscale Data Center

- By Data Center Type

- Colocation Data Center

- Hyperscalers Data Center/CSPs

- Enterprise and Edge Data Center

- By Country

- Saudi Arabia

- United Arab Emirates

- Oman

- Jordan

- Rest of Middle East

Detailed Research Methodology and Data Validation

Primary Research

We interviewed colocation operations managers in Riyadh and Dubai, procurement leads at two hyperscalers, facility design consultants, and regional distributors, which let us validate average selling prices, replacement cycles, and shipment lead times that are seldom captured in public sources.

Desk Research

We gathered public data from UN Comtrade HS codes 940320 and 847330, Gulf Cooperation Council customs bulletins, the UAE Telecommunications and Digital Government Regulatory Authority's traffic indexes, IEA data center energy dashboards, and peer-reviewed papers in IEEE Xplore that benchmark rack density. Company 10-Ks, investor decks, and articles on DataCenterKnowledge helped us map near-term facility pipelines. Paid resources include D&B Hoovers for vendor splits, Volza shipment trackers for import volumes, and Dow Jones Factiva for deal flow; they round out the desk model. The list is illustrative; many additional references were reviewed for data checks and clarification.

Market-Sizing & Forecasting

We employ a top-down model that converts announced IT-load additions, existing white space, and historical racks-per-megawatt ratios into annual rack demand. We then corroborate results through sampled ASP × volume roll-ups from leading suppliers. Key inputs include new megawatt capacity, median rack power density, the shift toward ≥48U heights, steel cost indexes, and import tariff schedules. Multivariate regression on these drivers projects the forecast horizon, while scenario analysis tests upside cases seeded by sovereign AI campuses. Gaps in shipment data are bridged by triangulating distributor interviews with customs manifests.

Data Validation & Update Cycle

Model outputs pass anomaly filters, peer review, and senior analyst sign-off before publication. We refresh every twelve months, with interim updates triggered when hyperscale build schedules, tariff rules, or material currency swings alter the outlook.

Why Mordor's Middle East Data Center Rack Baseline Stands Firm

We recognize that published values can differ, and we preview the usual reasons: scope, pricing assumptions, and refresh timing before detailing our stance.

Because our team locks definitions first and revisits them annually, the baseline remains steady even as market noise grows.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 197.31 million (2025) | Mordor Intelligence | |

| USD 175.61 million (2024) | Regional Consultancy A | GCC-only scope; limited validation of hyperscale retrofits |

| USD 221.57 million (2024) | Global Consultancy B | Ancillary hardware bundled; shorter upgrade-cycle assumption |

These contrasts show that Mordor's disciplined scope selection, variable tracking, and multi-layer verification yield a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

How large is the Middle East data center rack market in 2026 and what growth is expected?

The market is valued at USD 224.51 million in 2026 and is projected to reach USD 446.33 million by 2031, registering a 14.73% CAGR.

Which rack size is growing fastest in the region?

Half-height racks from 12U to 22U show the fastest expansion at 15.53% CAGR, driven by 5G edge deployments.

Why are enclosed cabinets preferred over open-frame racks in Gulf data centers?

Desert dust, temperature extremes, and the need for rear-door or liquid cooling make sealed, IP-rated cabinets more reliable and more efficient.

What role do local-content programs play in rack procurement?

Saudi IKTVA and UAE ICV requirements favor suppliers that assemble or source components domestically, impacting vendor selection and pricing.

How is liquid cooling affecting rack design in the Gulf?

AI and HPC clusters demand 50 kilowatt heat removal per rack, prompting designs that integrate manifolds, pumps, and sensors for immersion or direct-to-chip cooling.

Which countries contribute most to regional rack demand?

Saudi Arabia leads with 39.35% share, while the United Arab Emirates is the fastest growing at 16.08% CAGR through 2031.

Page last updated on: