Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

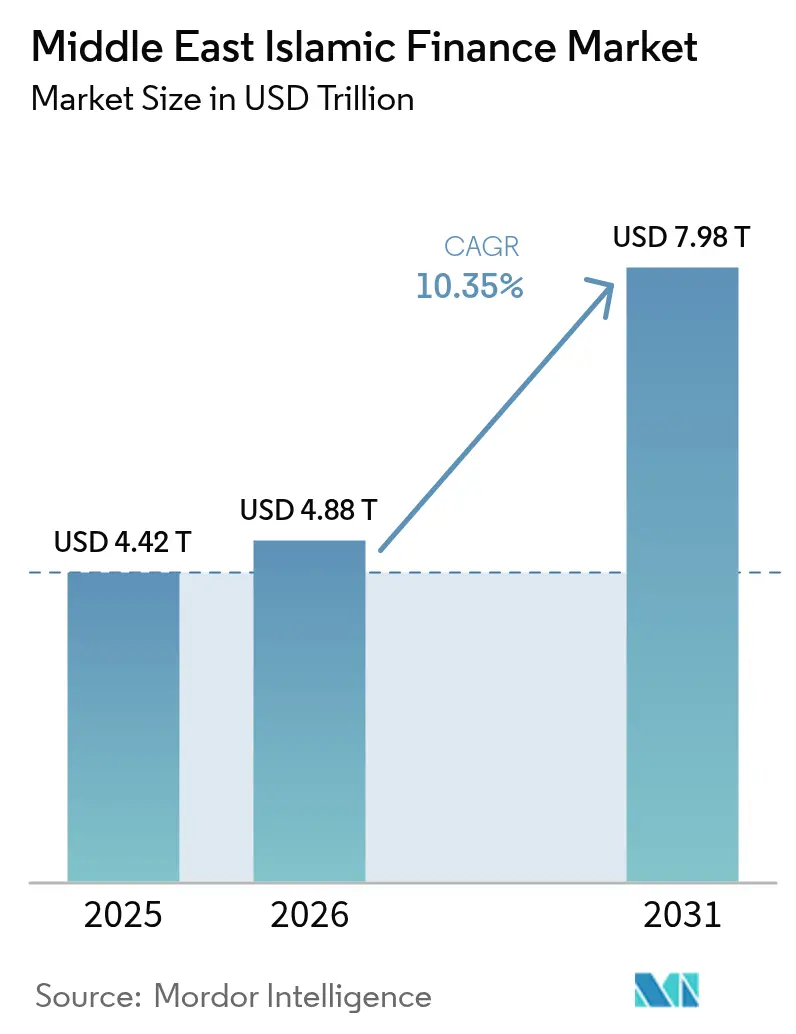

| Base Year Market Size (2025) | USD 4.42 Trillion |

| Market Size (2026) | USD 4.88 Trillion |

| Market Size (2031) | USD 7.98 Trillion |

| Growth Rate (2026 - 2031) | 10.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Islamic Finance Market Analysis by Mordor Intelligence

Middle East Islamic finance market size in 2026 is estimated at USD 4.88 trillion, growing from 2025 value of USD 4.42 trillion with 2031 projections showing USD 7.98 trillion, growing at 10.35% CAGR over 2026-2031. Ongoing government giga-projects, expanding sovereign wealth-fund commitments, and aggressive sukuk issuance pipelines continue to anchor funding demand, while regulatory harmonization within the Gulf Cooperation Council (GCC) is lowering cross-border friction and elevating regional liquidity standards[1]Saudi Vision 2030, “Vision 2030 Strategic Objectives,” VISION2030.GOV.SA. Digital-first entrants are compressing customer-acquisition costs by up to 40%, pushing legacy banks toward mobile-centric operating models, robo-advisory wealth tools, and open-finance architectures that meet AAOIFI guidance[2]UAE Central Bank, “Digital Currency and Open Finance Regulations,” CENTRALBANK.AE. At the same time, green and sustainability-linked sukuk structures are unlocking discounted pricing for both sovereign and corporate issuers, broadening the investor base and reinforcing the Middle East Islamic finance market’s role in global ESG capital flows.

Key Report Takeaways

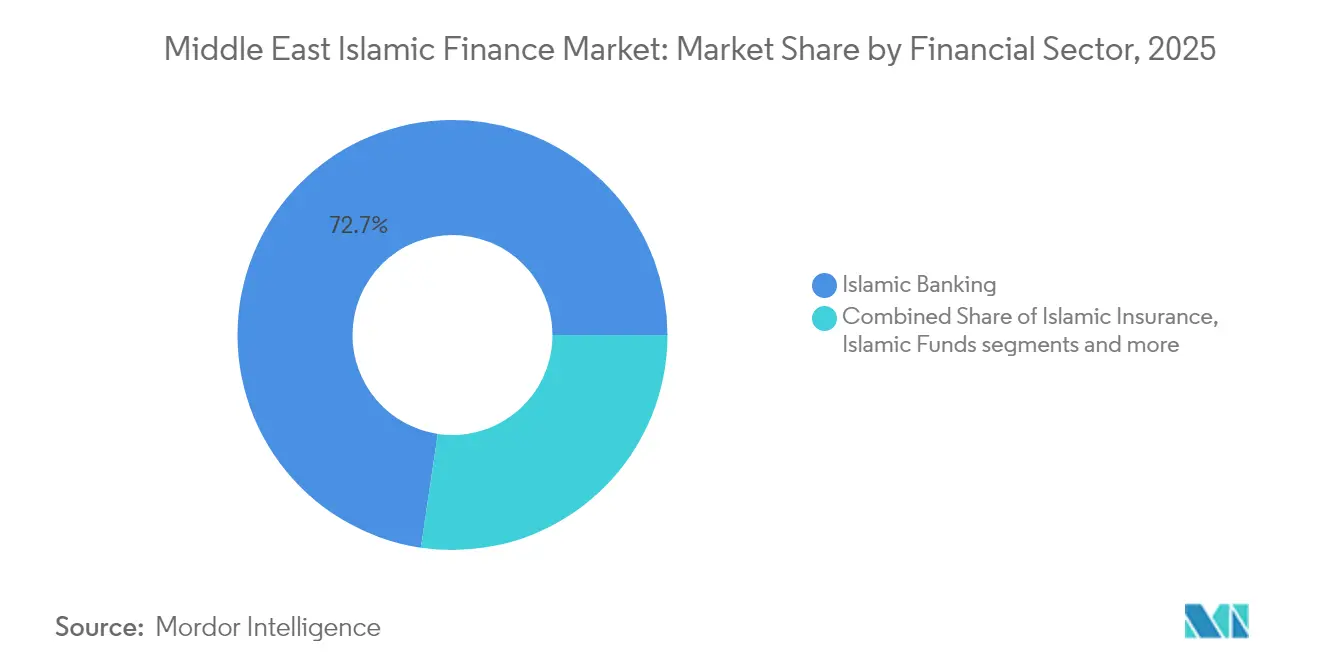

- By financial sector, Islamic banking led with 72.65% of the Middle East Islamic finance market share in 2025; digital-only Islamic banking platforms are projected to expand at 18.05% CAGR through 2031.

- By customer type, business clients accounted for 56.25% of the Middle East Islamic finance market share in 2025, while consumer segments are advancing at a 13.75% CAGR to 2031.

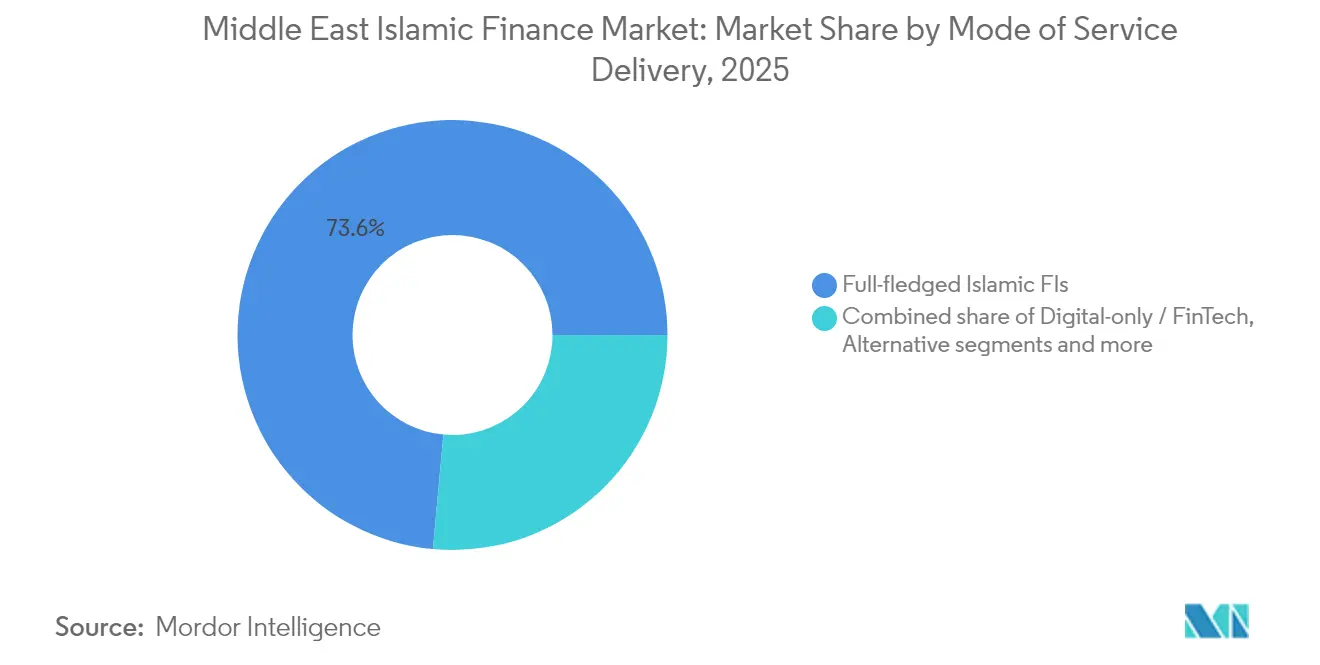

- By mode of service delivery, full-fledged Islamic financial institutions held 73.55% of the Middle East Islamic finance market size in 2025; digital-only and fintech platforms record the fastest projected CAGR at 21.25% between 2026-2031.

- By geography, Saudi Arabia captured a 49.05% of the Middle East Islamic finance market share in 2025; the United Arab Emirates is the fastest-growing geography at 16.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Islamic Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led giga-projects fuelling Islamic credit demand | +2.8% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Sovereign & corporate push for ESG/green sukuk issuance | +1.9% | GCC-wide, Egypt | Medium term (2-4 years) |

| Regulatory harmonization across GCC is enhancing cross-border liquidity | +1.4% | GCC states | Medium term (2-4 years) |

| Mandatory health-insurance laws accelerating takaful penetration | +1.2% | UAE, Saudi Arabia, Kuwait | Short term (≤ 2 years) |

| Rise of Sharia-compliant digital wealth platforms lowering customer-acquisition cost | +1.6% | UAE, Saudi Arabia, Bahrain | Short term (≤ 2 years) |

| Central-bank CBDC pilots unlocking Sharia-compliant liquidity tools | +1.7% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-led Giga-projects Fueling Islamic Credit Demand

Major infrastructure projects, including Saudi Arabia's USD 500 billion NEOM city, Dubai's 2040 Urban Master Plan, and Qatar's transport and healthcare initiatives, are significantly contributing to the long-term growth of Sharia-compliant project financing demand[3]NEOM Company, “Project Financing and Development Updates,” NEOM.COM . The initial sukuk tranches for NEOM have demonstrated the viability of innovative profit-and-loss sharing mechanisms, while also securing participation from global investors. This development has effectively broadened the capital base available to contractors and suppliers. The predictable funding schedules tied to these projects allow Islamic banks to lock in longer-duration assets, improving asset-liability matching and earnings visibility over the forecast horizon. Supply-chain participants now require Islamic working-capital facilities and trade-finance solutions, deepening credit penetration beyond the primary sponsors. Collectively, these projects add long-term loan origination pipelines that underpin the expansion of the Middle East Islamic finance market.

Sovereign & Corporate Push for ESG/Green Sukuk Issuance

In 2024, green sukuk volumes experienced significant growth, reflecting the increasing integration of ESG considerations with Sharia compliance. Saudi Arabia entered the market with its inaugural green sukuk issuance, while ADNOC issued a sustainability-linked sukuk. Both issuances achieved pricing below conventional equivalents, demonstrating a measurable reduction in the cost of capital. Egypt's planned program is set to expand the issuer base beyond the GCC, contributing to greater geographic diversification and enhanced secondary-market activity. Investor interest, driven by ethical and religious considerations, is broadening the buyer base, thereby improving liquidity and facilitating more efficient price discovery for sukuk. The alignment of ESG policy objectives with Islamic finance principles is positioning sukuk as a prominent asset class, supporting the continued expansion of the Middle East Islamic finance market.

Regulatory Harmonization Across GCC: Enhancing Cross-border Liquidity

In 2024, the implementation of unified Sharia governance frameworks by GCC central banks has streamlined compliance processes, reducing redundancies and lowering transaction costs for banks operating across multiple jurisdictions. The AFAQ payment rail, which facilitates significant monthly Islamic-compliant settlements, has enhanced cross-border transaction efficiency and strengthened intraregional trade finance capabilities. Bahrain’s adoption of AAOIFI standards as a standardized rulebook has simplified sukuk documentation procedures and shortened issuance timelines. Additionally, the UAE’s open-finance regulations mandating API interoperability have driven fintech innovation and enabled seamless cross-border data portability. These advancements have minimized structural inefficiencies, unlocking regional economies of scale, expanding balance sheets, and fostering competitive pricing, thereby accelerating the growth of the Middle East Islamic finance market.

Mandatory Health-insurance Laws Accelerating Takaful Penetration

Mandatory medical-insurance schemes in Saudi Arabia, UAE, and Kuwait are adding millions of new policyholders to takaful operators, translating into premium pools projected to double in some markets by 2027. Saudi Arabia alone issued over 15 million new takaful policies since 2024, representing the steepest annual jump on record. UAE’s expansion of compulsory coverage to the Northern Emirates is expected to inject USD 1.2 billion in additional annual premiums by 2026, with family takaful products showing outsized momentum among expatriates. Compulsory frameworks create predictable risk pools that permit 10-15% premium discounts through scale efficiencies without compromising profitability. The statutory nature of coverage ensures steady cash-flow streams and underpins the insurance leg of the Middle East Islamic finance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thin secondary-market liquidity for sukuk instruments | -1.8% | GCC-wide, Malaysia spillover | Medium term (2-4 years) |

| Shortage of Sharia/tech hybrid talent in Middle East markets | -1.3% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Potential balance-sheet impact from forthcoming AAOIFI Std 62 on sukuk risk-transfer | -2.1% | Global Islamic banks | Short term (≤ 2 years) |

| Cyber-security & data-sovereignty risks in open-banking APIs | -1.4% | GCC digital leaders | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thin Secondary-market Liquidity for Sukuk Instruments

Daily sukuk turnover remains substantially lower compared to equivalent bond markets, with corporate bid-ask spreads expanding due to insufficient market-making infrastructure. The preference of Islamic banks and takaful firms for buy-and-hold strategies results in a concentrated float, restricting free-float supply and impeding efficient price discovery. Smaller sukuk issuances often experience prolonged periods of inactivity, complicating portfolio adjustments and necessitating concessions during monetary tightening phases. Furthermore, regulatory constraints that discourage conventional investors from participating in secondary markets further diminish the depth of the order book. These liquidity constraints increase refinancing risks and moderate the growth trajectory of the Middle East Islamic finance market.

Shortage of Sharia/Tech Hybrid Talent in Middle East Markets

Industry associations report a critical shortage of professionals with expertise in both Islamic jurisprudence and fintech architecture. This talent gap has driven significant increases in salary premiums over recent years. The extensive timeline required to achieve dual qualifications serves as a barrier to entry for many, while the rapid evolution of fintech continues to expand the scope of required expertise. Consequently, financial institutions encounter operational challenges in deploying products that integrate real-time Sharia audits within their coding frameworks. Although educational programs are being developed to address this issue, the output of qualified graduates remains insufficient to meet market demand, a trend projected to persist through 2030. This talent deficit is inflating project costs, prolonging time-to-market, and constraining the growth trajectory of the Islamic Finance market in the Middle East.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Financial Sector: Digital Banking Drives Islamic Finance Evolution

Islamic banking accounted for 72.65% of the Middle East Islamic finance market in 2025, underscoring its role as the sector’s anchor franchise. Within that base, digital-only Islamic challengers are expanding at a 18.05% CAGR, compared with mid-single-digit growth for legacy branch networks. The divergence reflects superior unit economics, customer-acquisition costs fall, and the appeal of streamlined onboarding compliant with AAOIFI standards. Islamic insurance, or takaful, is the fastest-growing traditional vertical, buoyed by compulsory health-coverage laws that double premium pools in markets like Kuwait by 2027. Sukuk issuance continues diversifying into ESG formats as sovereign and corporate issuers exploit cost-of-capital advantages, while specialized Other Islamic Financial Institutions deliver niche trade-finance and commodity-murabaha services that complement core banking.

Digitalization also drives product-development velocity: banks deploy AI screeners to filter Sharia-compliant equities, and blockchain pilots promise instantaneous sukuk settlement. Green sukuk’s success demonstrates the compatibility of Islamic structures with sustainability imperatives, inviting larger allocations from global ESG funds and reinforcing market depth. Islamic funds are witnessing renewed institutional appetite, especially among pension and endowment allocators seeking both faith-based and ESG alignment. Al Rajhi Bank’s digital suite exemplifies the hybrid model wherein incumbent scale meets fintech agility, ensuring incumbents retain relevance while new entrants broaden market access. Together, these trends consolidate momentum for the Middle East Islamic finance market while diversifying revenue drivers across sub-sectors.

By Customer Type: Consumer Segment Momentum Builds

Business clients held 56.25% of the Middle East Islamic finance market share in 2025, reflecting a historical bias toward corporate lending and trade finance. Nevertheless, retail consumers are forecast to compound at 13.75% through 2031. Mandatory takaful requirements and mobile-first banking solutions, such as Sarwa’s Sharia-compliant investment platform, are driving growth. Vision 2030 initiatives have simplified account-opening KYC processes, enabling banks to target younger, digitally savvy Saudi consumers who demand integrated savings, payments, and micro-takaful services within a single application. The integration of embedded finance into e-commerce platforms facilitates instant Sharia-compliant payment options, further deepening market penetration into everyday consumer activities. Alinma Bank's profit growth underscores the potential for retail scale to enhance earnings performance.

Cross-sell opportunities multiply as consumers transition from basic current accounts to wealth, mortgage, and family-takaful products. Gig-economy workers blur the conventional corporate-retail divide, necessitating hybrid packages that combine business payment acceptance with personal savings modules. Governments also sponsor financial literacy drives aimed at expatriate populations, widening addressable demand pools. Digital KYC completes within minutes via biometric ID verification, reinforcing customer acquisition velocity. Consequently, consumer banking emerges as a primary growth engine underpinning the Middle East Islamic finance market’s expansion narrative.

By Mode of Service Delivery: Fintech Disruption Accelerates

Full-service Islamic institutions still dominate with 73.55% share of the Middle East Islamic finance market size, but digital-only competitors capture mindshare via sleek apps and fee-transparent models. Their 21.25% projected CAGR reflects technology-driven margin advantages and regulatory sandboxes that ease initial licensing. Islamic windows in conventional banks serve as gateways for mixed customer bases, although their growth trails dedicated fintechs due to slower decision cycles. Alternative platforms, crowdfunding, peer-to-peer, and supply-chain finance, are winning legal recognition, closing SME credit gaps through Sharia-compliant structures.

Digital rails such as the UAE’s Digital Dirham and Qatar’s Fawran system unlock instant settlement, letting fintechs guarantee near-real-time fund disbursements while remaining within Sharia bounds. Open-API ecosystems create composable banking stacks where specialized providers plug in compliant modules for identity, risk scoring, or payment orchestration. Incumbents respond by launching neo-bank offshoots, thereby cannibalizing their own branches before new entrants do. Consumers reward speed and transparency, propelling app-download metrics and transactional throughput. As adoption scales, cost-to-income ratios compress, and the Middle East Islamic finance market realizes productivity gains previously unreachable in branch-centric models.

Geography Analysis

Saudi Arabia controlled 49.05% of the Middle East Islamic finance market in 2025, fuelled by Vision 2030’s mandate for Sharia-aligned project financing and an expansive domestic retail base. NEOM, the Red Sea Project, and Riyadh Metro collectively generate multi-decade sukuk and syndicated-Murabaha pipelines that anchor domestic asset growth. The Saudi Central Bank continually refines governance codes, balancing fintech innovation with doctrinal rigor, which facilitates digital challenger launches without diluting religious legitimacy. Takaful premiums swell on mandatory employer coverage, and the kingdom’s banks register double-digit profit upticks, demonstrating balance-sheet resiliency and margin vitality.

The United Arab Emirates is the fastest-growing geography at 16.95% CAGR, leveraging Dubai’s cosmopolitan capital-market infrastructure and Abu Dhabi’s energy-sector depth. The world’s first open-finance framework tailored to Islamic institutions enables interoperable data flows that slash onboarding friction for both domestic and cross-border clients. ADNOC’s sustainability-linked sukuk underscores the UAE’s ESG leadership, while the Digital Dirham pilot embeds Sharia-compliant logic into CBDC rails, foreshadowing a regional paradigm shift in liquidity management. Mandatory insurance expansion in Northern Emirates injects new takaful volumes, and fintech hubs in DIFC and ADGM incubate Islamic robo-advisers that broaden retail engagement.

Qatar, Kuwait, Bahrain, and Oman together comprise a meaningful 20-plus-percent slice of the Middle East Islamic finance market and offer differentiated catalysts. Qatar’s Fawran-CBDC integration signals a forward-leaning payment architecture that lowers transaction costs for SMEs and fosters trade-finance innovations. Kuwait Finance House’s cross-border footprint and pending takaful boom illustrate how smaller markets leverage niche specialization. Bahrain hosts AAOIFI and operates a flexible regulatory sandbox, positioning itself as the region’s standard-setting lab. Oman and North African extensions provide untapped demographic pools, albeit with macro-stability challenges that dictate cautious entry sequencing. Collectively, regional heterogeneity diversifies growth sources, de-risking aggregate variance in the Middle East Islamic Finance market.

Regulatory Landscape

Regulation in the Middle East Islamic finance market is anchored by national central banks and free-zone regulators, with cross-border alignment supported by standard setters including AAOIFI and the Islamic Financial Services Board (IFSB). In the UAE, Federal Decree-Law No. (6) of 2025 strengthened statutory oversight through the Higher Shari'ah Authority and reinforced expectations for internal Shari'ah supervisory committees, while the Central Bank of the UAE maintains a Shari'ah governance standard in its rulebook and extends supervision into digital and open-finance use cases.

Across the GCC, supervisory emphasis has shifted toward governance and conduct clarity for Islamic products and distribution. The Dubai Financial Services Authority (DFSA) has been consulting on enhancements to Islamic Finance Rules in the DIFC, including sharper disclosures for takaful sales and clearer requirements around endorsements for authorised persons. Regionally, IFSB-31 (issued July 2025) sets guiding principles for the effective supervision of Shari'ah governance, with a recommended implementation by January 2027, and in May 2026 the IFSB highlighted emerging hybrid risks in Islamic banking, supporting tighter prudential interpretation for products that replicate conventional risk profiles.

Value Chain Analysis

The value chain covers product origination and structuring (Islamic banks, takaful operators, fund managers, and specialist arrangers), then Shari'ah governance and assurance (internal Shari'ah boards, national higher Shari'ah authorities where applicable, and standards alignment to AAOIFI and IFSB). Distribution then runs through branches, digital channels, and embedded-finance partnerships. For sukuk, the chain extends from structurers and legal counsel to rating and listing venues, primary dealers and investors, and post-issuance servicing and settlement, with secondary-market liquidity and market-making depth remaining a key bottleneck for price discovery.

Operational enablement has expanded through fintech and platform layers that digitize onboarding, compliance, and working-capital flows, particularly for SMEs and supply-chain ecosystems. Shari'ah-compliant supply chain finance platforms and modules (for example, Tawreeq and bank-led digital SCF offerings such as Emirates Islamic smartSCF, and bank integrations such as Abu Dhabi Islamic Bank working with QUALCO) use structures such as wakala to support vendor liquidity and early invoice settlement. The absence of a GCC-wide supervisor keeps cross-border compliance stacks fragmented, increasing documentation and governance overhead for institutions operating across multiple jurisdictions, even as AAOIFI/IFSB standards provide a common reference point.

Competitive Landscape

The top banks, Al Rajhi, Dubai Islamic, Kuwait Finance House, Qatar Islamic, and Emirates Islamic, command a significant share of market assets, producing a moderate concentration that encourages both scale and specialized niching. Incumbents employ digital overhauls, chatbot servicing, biometric authentication, and blockchain pilots to defend their share against nimble fintechs. White-space pursuits include green sukuk structuring, embedded gig-worker takaful, and AI-powered Sharia compliance, each requiring capex and specialist talent that only some players can marshal. Norton Rose Fulbright’s decade-long crafting of Sharia-tech legal talent illustrates growing advisory ecosystems that support product complexity.

Fintech challengers, agile in their approach, present fee-transparent models and gamified savings journeys, striking a chord with Gen-Z and millennial Muslims. However, regulatory capital mandates and adherence to AAOIFI Standard 62 create challenges, naturally filtering entrants to those boasting strong governance frameworks. Open-banking frameworks dismantle distribution barriers, enabling startups to leverage established incumbents' platforms, while allowing these incumbents to tap into third-party innovations through API integrations.

Strategic mergers and acquisitions, exemplified by Al Salam Bank's takeover of KFH-Bahrain's operations, highlight a trend towards consolidation, as players pursue cost optimization in an environment of tightening margins. As a result, the competitive landscape evolves into a hybrid ecosystem, where collaboration and competition intertwine, invigorating the Islamic finance market in the Middle East.

Middle East Islamic Finance Industry Leaders

Al Rajhi Bank

Kuwait Finance House

Dubai Islamic Bank

Qatar Islamic Bank

Alinma Bank

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Green, sustainability-linked, and transition-themed sukuk have broadened the opportunity set for sovereign and corporate funding pipelines, backed by demonstrated issuer activity in the region, such as Saudi Arabia's inaugural green sukuk and ADNOC's sustainability-linked sukuk issuance in 2024. A parallel opportunity is visible in local-currency depth and government-curve building, illustrated by the UAE Ministry of Finance listing AED 1.1 billion of Islamic Treasury Sukuk (T-Sukuk) taps on Nasdaq Dubai in April 2026, which strengthens reference pricing and expands instrument availability for Islamic banks, takaful operators, and asset managers.

Digitization is also creating whitespace in compliant retail and SME propositions, where automated governance and open-finance rails reduce unit costs without diluting Shari'ah oversight. In the UAE and wider GCC, regulators and standards bodies have moved from experimentation to codified expectations for AI and digital compliance. This includes AAOIFI's February 2026 consultation on AI-assisted Shari'ah compliance, with requirements around human scholar oversight and auditability, and the Central Bank of the UAE's March 2026 guidance requiring documented model-risk management frameworks for AI systems used in Shari'ah compliance by licensed Islamic banks. Together, these steps support scalable product screening, faster time-to-market for compliant portfolios, and new distribution models, including digital-only Islamic banking platforms, while keeping governance controls explicit.

Recent Industry Developments

- May 2026: Mal received in-principle approval from the Central Bank of the UAE (CBUAE) to establish an AI-native Islamic digital bank following a reported USD 230 million seed round. The approval broadens the UAE pipeline of digital-only Islamic banking entrants and raises the bar for automated, audit-ready Shari'ah compliance capabilities.

- October 2025: Emirates Islamic launched Islamic smartSCF, a fully digital, Shari'ah-compliant supply chain finance solution focused on vendor liquidity through early invoice settlement. The product expands Shari'ah-compliant working-capital distribution beyond traditional bilateral bank credit and strengthens the platform layer supporting SME and corporate ecosystems.

- May 2024: Al Salam Bank acquired Kuwait Finance House Bahrain (KFH-Bahrain), consolidating Islamic banking operations in Bahrain. The transaction increased scale in a standards-forward jurisdiction that hosts AAOIFI, supporting product standardization and operating leverage for regional expansion.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of Sharia-compliant financial assets and related activity generated through Islamic banking, sukuk, takaful, and other Islamic financial institutions operating across the Middle East.

Scope exclusions: Conventional (non-Sharia-compliant) financial assets, informal lending, and non-financial Islamic economy activities are excluded from this market.

Segmentation Overview

- By Financial Sector

- Islamic Banking

- Islamic Insurance (Takaful)

- Islamic Bonds (Sukuk)

- Other Islamic Financial Institutions (OIFLs)

- Islamic Funds

- By Customer Type

- Business

- Consumer

- By Mode of Service Delivery

- Full-fledged Islamic FIs

- Islamic Windows in Conventional FIs

- Digital-only / FinTech Platforms

- Alternative Platforms (Crowdfunding, P2P)

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Bahrain

- Oman

- Levant & Iraq

- Egypt & North Africa

Data Sources, Market Sizing, and Validation

Desk Research

We started with public, auditable sources to set the country boundaries and to understand how Islamic assets are reported and classified. This included central bank and regulator statistical releases in GCC markets, the Islamic Financial Services Board (IFSB), AAOIFI guidance notes for accounting treatment, and Islamic Development Bank Group publications that track regional Islamic finance themes.

Next, the desk phase was used to ground the market model in observable financial system signals, not just narrative trends. We reviewed annual reports, investor presentations, and audited financial statements of Islamic banks, takaful operators, and exchanges that list sukuk, followed by reputed financial press coverage for major sukuk issuance and policy shifts. Where needed, we also used paid subscriptions for company financials and intelligence, news and financials, patent databases, and global contracts and tenders to verify timelines and fill gaps on announced programs. These desk sources are illustrative, and other public and paid references were also consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on structured interviews and short surveys with Islamic banks, takaful providers, sukuk arrangers, Sharia boards and advisors, and institutional buyers, so desk assumptions could be corrected where market practice differs by country. We also checked views across major sub-regions, since reporting depth and product mix differ between GCC markets and the rest of the Middle East, and the final totals were aligned only after these differences were reconciled.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | |

| Mid tier: 56% | Functional/Unit leaders: 37% | |

| Smaller Players: 17% | Managers: 47% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build where country-level Islamic finance asset pools are reconstructed from regulator and industry reporting, then split into Islamic banking, sukuk, takaful, and other Islamic financial institutions using consistent classification rules. To keep the totals realistic, we corroborate the results with selective bottom-up checks, such as rolling up sampled balance sheet items from leading institutions, cross-checking sukuk outstanding against issuance patterns, and validating takaful asset growth against premium and investment income trends.

The model uses a short set of market fingerprints that can be verified each year, including Islamic banking asset growth rates, sukuk outstanding and new issuance flows, takaful gross contributions and investment returns, policy changes that affect Sharia governance and reporting, and local currency to USD conversion timing for the base year. Where direct splits are not available for smaller markets, we use proxy ratios from comparable neighboring markets and then adjust them after interview feedback on product mix and Islamic window penetration.

For forecasting, we rely on scenario analysis anchored to macro and policy drivers that typically move Islamic asset growth, then sanity-check the trend using simple time series behavior of asset growth where history is consistent. The forward view is finalized only after the primary inputs confirm whether growth is expected to be led by banking balance sheets, sukuk activity, or takaful expansion, since each sub-sector responds differently to rates, liquidity conditions, and sovereign funding needs.

Data Validation & Update Cycle

Validation is done through multiple passes of variance checks so the output does not drift away from real financial system signals. We compare the modeled totals against independent indicators such as reported Islamic asset shares, sukuk market activity, and publicly disclosed balance sheet movements, then re-check any country or sub-sector that shows an unusual jump.

Before sign-off, the assumptions, currency handling, and split logic are reviewed by another analyst, followed by targeted follow-ups when an input looks inconsistent with market practice. Reports are refreshed annually, with interim updates when material events occur, such as major regulatory revisions, large sovereign sukuk programs, or sudden changes in reporting standards. Right before delivery, a final sweep is done so clients receive the latest updated view aligned to the most recent public releases.

Mordor Intelligence's Middle East Islamic Finance Market Estimate Compared With Other Published Estimates

Published market sizes for Middle East Islamic finance can differ quite a bit, mainly because analysts do not always count the same asset classes, and they also vary on whether they use outstanding assets or annual flows as the core value. Differences also show up when some sources treat Islamic windows as fully Islamic assets, or when they apply different currency conversion timing in volatile periods.

By tracking asset-outstanding totals by financial sector and refreshing the country splits through primary checks, Mordor Intelligence keeps the estimate tied to what is actually reported by regulators and institutions, rather than blending in adjacent conventional pools. The remaining gaps usually come from scope choices, such as including wider MENA markets beyond the core Gulf focus, counting newer digital-only Islamic platforms, and using more aggressive or conservative assumptions on sukuk growth and takaful investment performance during the forecast window.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.42 T (2025) | |

| Industry Association A | USD 4.10 T (2025) | Uses a narrower country set focused on core GCC reporting and applies conservative inclusion rules for Islamic windows, which can reduce counted assets versus broader Middle East coverage. |

| Global Consultancy B | USD 4.95 T (2026) | Anchors the estimate on faster asset growth assumptions and forward currency translation, and it appears to blend some flow-based sukuk measures with asset totals, which can lift the headline value. |

Across the table, the spread is mainly explained by what is counted as Islamic assets (full-fledged versus windows), which countries are included, and whether the value is anchored to outstanding assets or activity flows. When these choices are made explicit and checked against regulator reporting and interview feedback, the resulting market size becomes easier to trace and repeat year to year.

Key Questions Answered in the Report

How large is the Middle East Islamic Finance market in 2026?

It is valued at USD 4.88 trillion and is projected to reach USD 7.98 trillion by 2031, reflecting a 10.35% CAGR.

Which country is the largest contributor to Islamic finance in the region?

Saudi Arabia holds 49.05% of regional assets, benefiting from Vision 2030 mega-projects and mandatory takaful laws.

What is driving green sukuk momentum in the GCC?

Sovereign and corporate issuers are pursuing ESG objectives, securing pricing advantages of 15-25 basis points over conventional bonds.

Why are digital-only Islamic banks growing faster than traditional banks?

Companies achieve notable reductions in customer-acquisition costs while offering mobile-first solutions that comply with AAOIFI standards.

How will CBDCs affect Islamic banks in the Middle East?

Digital currencies, including the UAE’s Digital Dirham, are positioned to enhance cost efficiency by reducing operational expenses while simultaneously providing Sharia-compliant liquidity solutions.

What risks could slow market growth?

Key challenges include thin sukuk secondary-market liquidity, a shortage of Sharia-tech talent, and cybersecurity vulnerabilities in open-banking APIs.

Page last updated on: