Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

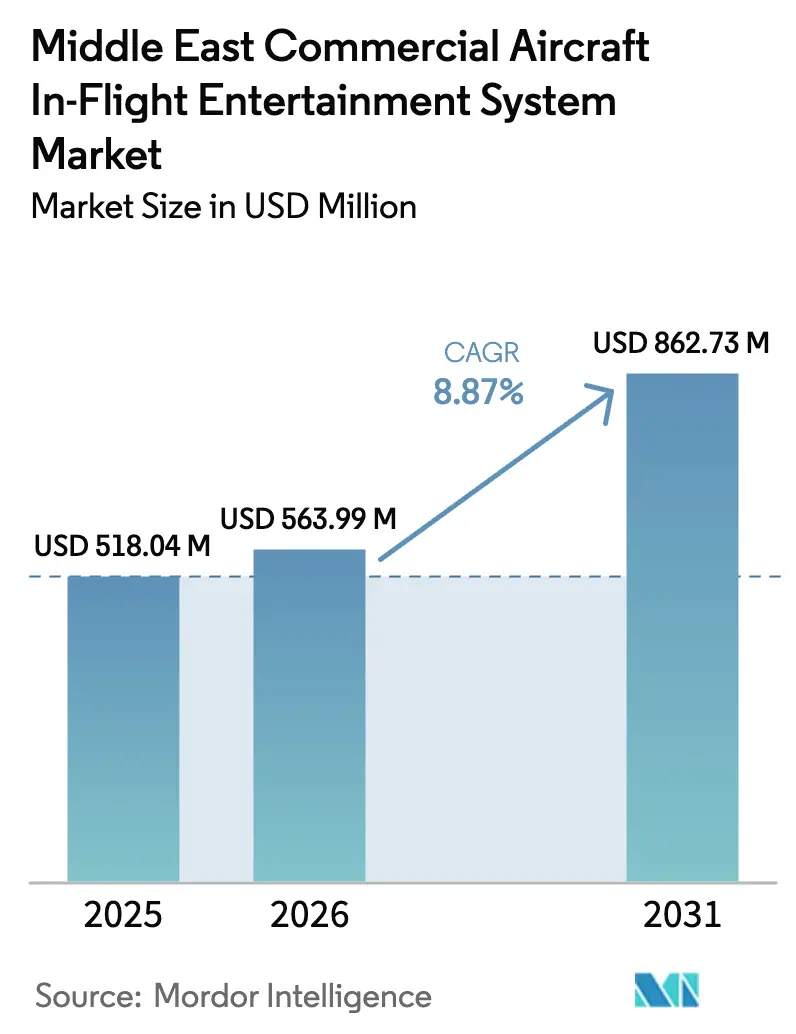

| Base Year Market Size (2025) | USD 518.04 Million |

| Market Size (2026) | USD 563.99 Million |

| Market Size (2031) | USD 862.73 Million |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Commercial Aircraft In-Flight Entertainment System Market Analysis by Mordor Intelligence

The Middle East commercial aircraft in-flight entertainment (IFE) system market size is expected to grow from USD 518.04 million in 2025 to USD 563.99 million in 2026 and is forecast to reach USD 862.73 million by 2031 at 8.87% CAGR over 2026-2031. Rising long-haul passenger volumes, aggressive wide-body renewal cycles, and government-backed aviation megaprojects anchor this momentum. Carriers pair significant cabin investments with hybrid seat-back + wireless architectures to sustain premium yields while cutting operating weight. Saudi Arabia’s localization mandates and the UAE’s hub strategy intensify regional competition, prompting suppliers to develop in-country MRO capabilities and expedite retrofit lines. Supply-chain normalization is easing monument delays, encouraging airlines to accelerate cabin refresh decisions deferred during the pandemic recovery period. Hardware revenues dominate, yet advertising, e-commerce, and tiered connectivity subscriptions are scaling rapidly as airlines monetize passenger engagement beyond the ticket.

Key Report Takeaways

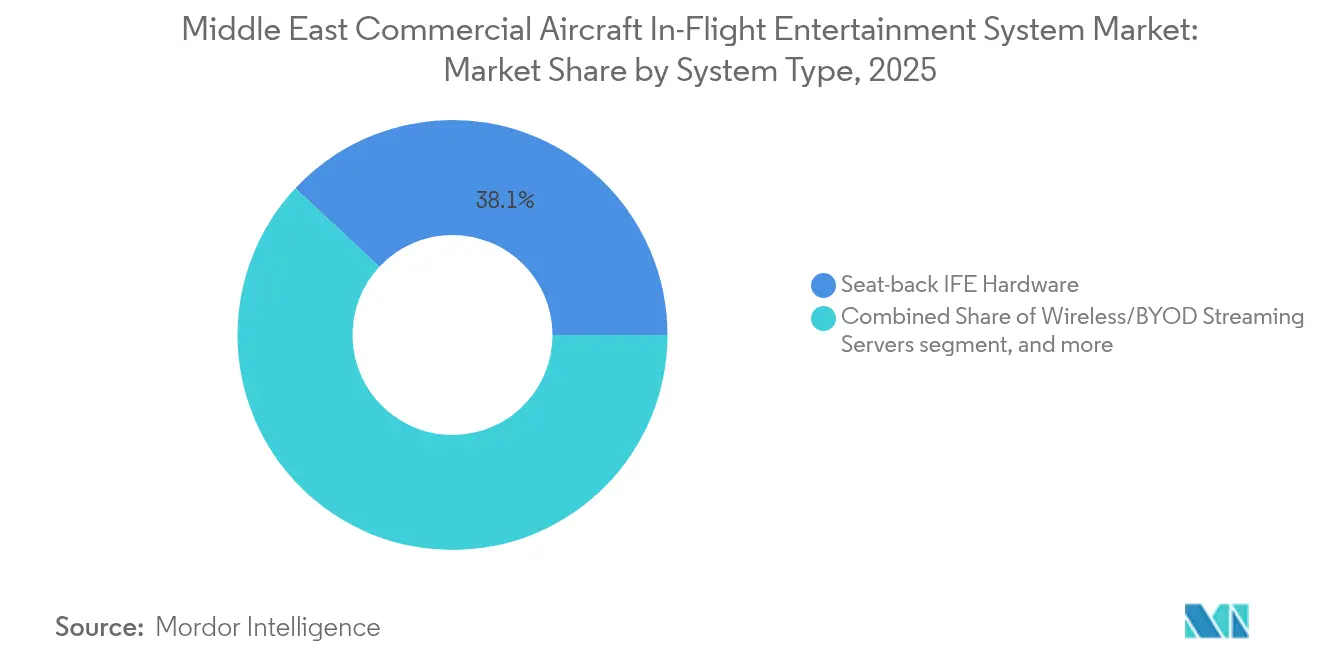

- By system type, seat-back hardware led with 38.05% revenue in 2025; cabin connectivity solutions recorded the quickest 9.96% CAGR to 2031.\

- By aircraft type, narrowbodies held 49.02% of the Middle East commercial aircraft IFE system market share in 2025, while widebodies are forecasted to post the fastest 9.04% CAGR through 2031.

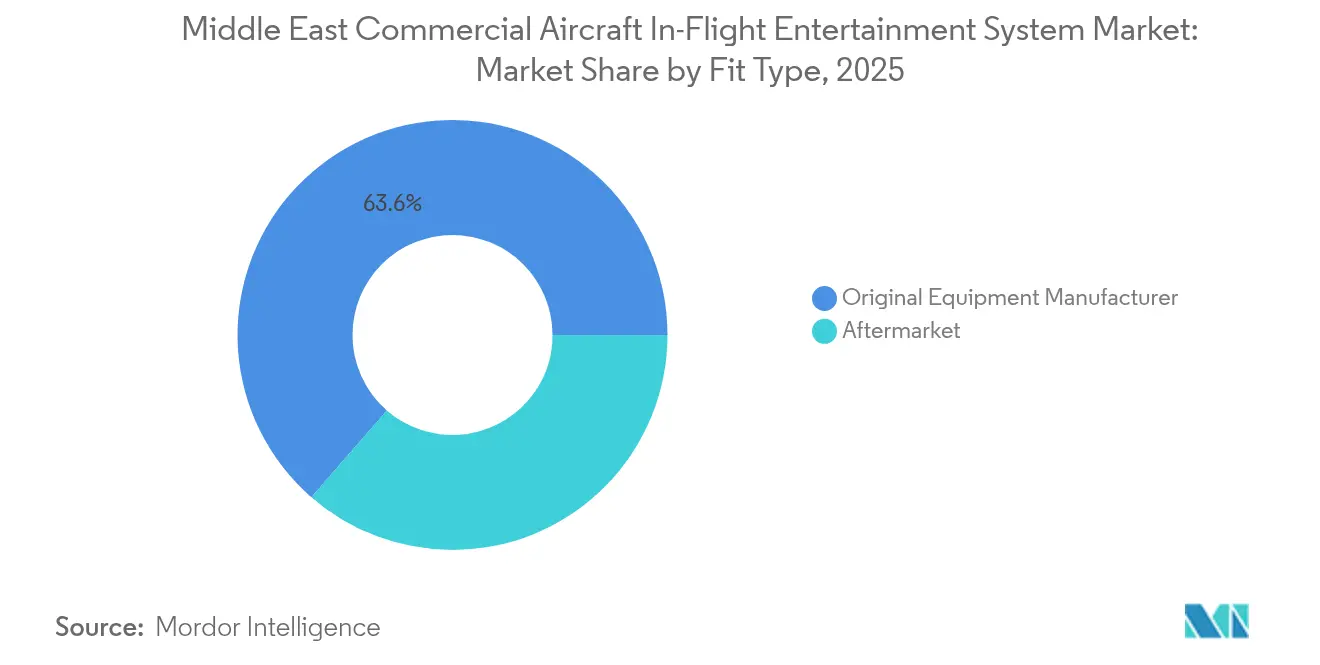

- By fitment, OEM installations accounted for 63.60% of revenue in 2025, whereas aftermarket retrofits advanced at a 8.89% CAGR as carriers upgraded in-service fleets.

- By revenue channel, hardware sales represented 75.70% in 2025, yet advertising and e-commerce rose at an 11.32% CAGR, the fastest among all streams.

- By geography, Saudi Arabia led with a 32.74% share in 2025 and is projected to grow the quickest at a 8.98% CAGR to 2031, reflecting Vision 2030 fleet expansion targets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Commercial Aircraft In-Flight Entertainment System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued rebound of Middle East passenger traffic | +1.80% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| Record widebody fleet renewal cycles announced by Middle Eastern carriers | +2.10% | Gulf states | Medium term (2-4 years) |

| Seat-back IFE as anchor for high-yield long-haul differentiation | +1.50% | Premium long-haul routes | Long term (≥ 4 years) |

| Introduction of premium-economy cabins across Gulf mega-carriers | +1.20% | Saudi Arabia | Long term (≥ 4 years) |

| Growth of point-to-point narrowbody services to Central Asia and Africa | +0.90% | Emerging routes | Medium term (2-4 years) |

| Localization mandates in Saudi/UAE MRO clusters | +0.80% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued Rebound of Middle East Passenger Traffic

Regional airports are forecasted to handle 310 million passengers in 2025, fully matching pre-pandemic volumes and renewing airlines’ focus on differentiated onboard experiences.[1] International Air Transport Association, “Air Passenger Forecast,” iata.org Emirates carried 58.5 million passengers in fiscal 2024, while Qatar Airways and Saudia opened new routes to tap pent-up leisure and business flows. Long-haul sectors see the most significant lift, amplifying demand for robust entertainment ecosystems that support advertising and premium content licensing. Air Arabia’s 172-aircraft wireless IFE agreement with Panasonic demonstrates how low-cost carriers now view digital engagement as a core component. IATA projects regional traffic to climb 5.8% annually through 2030, sustaining a healthy backlog for IFE suppliers.

Record Widebody Fleet Renewal Cycles Announced by ME Carriers

Emirates ordered 90 B777X jets and Qatar Airways booked 25 B777-8 freighters in 2024, signaling the most concentrated widebody refresh in the region’s history.[2]Boeing, “Orders & Deliveries 2024,” boeing.com New frames are specified with 4K seat-back displays, high-capacity servers, and gate-to-gate connectivity to protect yields on flights of 12-16 hours. Replacement timing dovetails with leases expiring from the 2010-2015 super-cycle, clustering demand, and favoring vendors with proven certification pipelines. Hybrid seat-back + wireless architectures dominate RFPs as airlines seek differentiation and weight savings.

Seat-Back IFE as Anchor for High-Yield Long-Haul Differentiation

Contrary to a wireless-only narrative, 73% of travelers still prefer built-in screens on flights over 6 hours.[3]Panasonic Avionics, “Passenger Preferences for IFE,” panasonic.aero Emirates outfits its newest cabins with 4K monitors, and Qatar Airways integrates privacy doors with personalized infotainment in QSuite. Airlines monetize seat-back real estate through targeted ads, which yield USD 2-4 per passenger per flight, while also serving as the primary interface for streaming and e-commerce. The commitment underscores that hardware and connectivity evolve together in the Middle East commercial aircraft IFE system market rather than as substitutes in the market.

Introduction of Premium-Economy Cabins Across Gulf Mega-Carriers

Emirates and Qatar Airways now offer premium economy on their A380 and B777 fleets, featuring display sizes that fall between economy and business norms, wider seat-row power budgets, and tiered digital perks. Suppliers must provide modular software that unlocks exclusive games, offers higher Wi-Fi speeds, and integrates loyalty programs for mid-tier fares. Revenue-management teams already bundle premium-economy tickets with priority bandwidth, converting IFE from sunk cost to an upsell lever.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent supply-chain bottlenecks for composite monuments | -1.40% | Global | Short term (≤ 2 years) |

| Cabin weight-reduction targets vs. in-flight connectivity power draw | -0.80% | Wide-body fleet focus | Medium term (2-4 years) |

| Skills shortage in regional completion centers | -0.60% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Slow retrofit cycles due to prolonged lease terms post-COVID | -0.90% | Older fleet segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Supply-Chain Bottlenecks for Composite Monuments

Lead times for premium cabin monuments now stretch to 12-18 months, which is double the pre-pandemic norm, delaying IFE integration and aircraft deliveries. Boeing and Airbus prioritize structural handover, leaving interior houses to clear backlogs. Gulf airlines accept provisional cabins with simplified entertainment pending retrofit slots, creating a secondary spike in demand once supply stabilizes. Regional composite capacity remains limited, motivating Saudi and UAE industrial funds to back local production lines.

Cabin Weight-Reduction Targets vs. In-Flight Connectivity Power Draw

Ultra-long-haul operators target aggressive fuel-burn reductions, yet 4K displays and high-speed routers can demand 150-200 watts per seat, compared to 50-75 watts for legacy systems. Carriers explore lighter wiring, rear-mounted processors, and USB-C power with energy-efficient regulation to reconcile fuel economics with passenger expectations. Hybrid layouts place full-power suites in premium zones, while the economy adopts BYOD streaming to cut costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Connectivity Outpaces Traditional Hardware

Seat-back hardware retained 38.05% of 2025 turnover, yet connectivity platforms will post the fastest 9.96% CAGR backed by LEO satellite rollouts. Travelers increasingly board with multiple devices, pushing airlines to install high-bandwidth routers and secure servers. The Middle East commercial aircraft IFE system market share of connectivity is set to expand as Starlink and OneWeb gain approvals for aviation use. Hybrid programs are prevalent: premium seats still feature 4K screens, while economy relies on browser-based portals. In-seat power upgrades trail this change, rising in parallel to support larger battery devices.

Suppliers position modular architectures that allow carriers to swap out SSDs, antennas, or displays as technology advances. This future-proofing lowers life-cycle cost and supports retrofits on mature airframes. Airlines value the revenue upside of gate-to-gate internet: paid tiers, e-commerce, and partner ads flow directly into ancillary lines.

By Aircraft Type: Widebodies Accelerate Premium Growth

The narrowbody fleet commanded 49.02% of 2025 revenue, yet the widebody sub-sector will log the highest 9.04% CAGR through 2031. Widebodies benefit from carriers refreshing high-density hub-and-spoke operations with 4K screens, multi-band antennas, and immersive audio. The Middle East commercial aircraft IFE system market size tied to widebodies is forecast to climb sharply as B777X and A350 backlogs enter service. Narrowbodies pivot toward wireless streaming, illustrated by Air Arabia’s fleetwide Panasonic deployment that cuts seat weight and maintenance. Mixed fleets let airlines tailor capex: premium long-haul receives seat-back displays, while regional jets rely on BYOD models for cost control.

Fleet planning reflects route economics. Gulf carriers rely on widebodies for 12-hour sectors where IFE drives ancillary revenue and Net Promoter Scores, whereas low-cost operators need quick-turn aircraft that avoid heavy monuments. As a result, growth divides along service model lines, but both streams add volume to the Middle East commercial aircraft IFE system market.

By Fit Type: Aftermarket Retrofits Narrow the Gap

OEM linefit accounted for 63.60% of 2025 spending because new deliveries commonly integrate entertainment at source. Delivery delays and extended leases now elevate retrofit demand, generating a 8.89% CAGR for the aftermarket. Carriers schedule cabin refreshes to align with heavy-check slots, installing lighter screens, faster servers, and higher-gain antennas. Modular kits cut downtime, letting airlines return aircraft to service within weeks. Localization policies push more retrofit work into Saudi and UAE MRO clusters, accelerating domestic capability growth and supporting the Middle East commercial aircraft IFE system industry’s supply resilience.

By Revenue Channel: Advertising and E-Commerce Scale Fast

Hardware still captured 75.70% of 2025 revenue, but digital advertising and e-commerce are rising at 11.32% CAGR. United’s Kinective Media success showed airlines can earn USD 2-4 per passenger per flight via personalized campaigns. Gulf carriers adapt this model, pairing Arabic language portals with duty-free, destination booking, and last-mile mobility offers. Connectivity subscriptions add a predictable stream, offsetting bandwidth charges. As platforms mature, margins from digital channels are poised to dilute the share of hardware in the total Middle East commercial aircraft IFE system market revenue.

Geography Analysis

Saudi Arabia commands the Middle East commercial aircraft IFE system market with a 32.74% slice in 2025 and the fastest 8.98% CAGR outlook. Vision 2030 pledges, new mega-airports, and premium giga-project traffic combine to keep demand robust. IFE suppliers gain from localization deals that tie certification and MRO work into Riyadh’s emerging aerospace corridor, but must navigate strict Saudization quotas. The uplift in the market size of the Middle East commercial aircraft IFE system also reflects Saudia’s 100+ aircraft acquisition plan, including wide-body variants outfitted with luxury 4K suites.

The United Arab Emirates ranks second, powered by Emirates’ and Etihad’s long-haul dominance and Dubai’s transit hub. Emirates’ order for 90 B777X jets carries next-generation 4K screens and real-time advertising capabilities that enlarge vendor pipelines. Dubai’s advanced regulatory regime speeds IFE certifications, making it an ideal proving ground for hybrid hardware-connectivity rollouts. Qatar holds a solid position after its World Cup capacity build-up. Qatar Airways maintains premium market standards, updating its A350 fleet with Thales AVANT 4K systems and integrated Wi-Fi that logs high attach rates on 16-hour sectors. Kuwait, Oman, and Bahrain represent niche markets focused on regional business routes. They typically select wireless streaming and USB-C power rather than full seat-back suites to limit weight and acquisition cost. Political stability and open-skies agreements influence procurement timing: when oil prices firm, these carriers accelerate cabin upgrades to match Gulf rivals. The Rest of the Middle East, including Jordan and Lebanon, shows modest upgrades as airlines vie for transit traffic feeding into larger hubs. Harmonized safety standards promoted by the UAE GCAA and Saudi GACA help smooth cross-border retrofit approvals, while pan-GCC recognition of STC certificates shortens market lead-times.

Competitive Landscape

The Middle East commercial aircraft IFE system market remains moderately fragmented. Panasonic Avionics, Thales, Collins Aerospace, and Safran hold the lion’s share but face agile challengers in connectivity and advertising tech. Panasonic leverages its early wireless IFE momentum, winning Air Arabia’s 172-aircraft deal, while Thales deploys AVANT 4K on Qatar Airways’ A350s. Collins invests USD 75 million to grow Dubai MRO capability, underscoring localization pressure. Safran packages lightweight seats with embedded screens to cut mass without reducing screen size.

Disruptors include Starlink Aviation and OneWeb, which aim to provide low-latency, high-throughput connectivity that favors BYOD models. Local industrial funds back joint ventures like JAMCO-PIF for monument production, gradually reducing reliance on imported interiors and altering supplier calculus. Airlines demand modular, agnostic platforms to swap displays, antennas, and servers mid-life to capture new revenue streams. Providers that master regional certification and offset rules gain an edge, as Gulf regulators increasingly link cabin approvals to local job creation.

White-space opportunities grow in digital advertising and e-commerce orchestration. United’s Kinective Media proof resets revenue expectations, prompting Gulf carriers to request similar plug-ins. Vendors that can integrate payment gateways, ad servers, and real-time analytics stand to capture high-margin service contracts. The competitive stakes, therefore, extend beyond hardware into data ownership and monetization strategies, redefining value pools inside the Middle East commercial aircraft IFE system market.

Middle East Commercial Aircraft In-Flight Entertainment System Industry Leaders

Collins Aerospace (RTX Corporation)

Safran SA

Diehl Stiftung & Co. KG

Panasonic Holdings Corporation

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Panasonic Avionics Corporation launched its cutting-edge, cloud-native Wi-Fi Portal platform, empowering airlines to take complete control of their in-flight connectivity experience. With this new Wi-Fi Portal, airlines can effortlessly customize their portal design, eliminating the need for formal change requests or ATPs. Utilizing self-service tools, airlines can seamlessly align their connectivity offerings with their brand identity, onboard strategy, and overarching commercial goals.

- June 2024: Panasonic Avionics Corporation inked a deal with Air Arabia to roll out its eXW wireless IFE solution on 172 aircraft. This new agreement builds upon an existing collaboration, which saw six A321LRs already equipped with Panasonic's eXW solution. Now, the deal expands to encompass Air Arabia's fleets, including the Airbus A320neo, A321neo, and A321XLR. Out of the total, 120 aircraft will receive the eXW solution directly from the OEM, while an additional 52 will undergo retrofitting.

Middle East Commercial Aircraft In-Flight Entertainment System Market Report Scope

By System Type

| Seat-back IFE Hardware |

| Wireless/BYOD Streaming Servers |

| In-seat Power and Peripherals |

| Cabin Connectivity (Ku/Ka/LEO) |

By Aircraft Type

| NarrowBody Aircraft |

| WideBody Aircraft |

| Regional Jets |

By Fit Type

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Revenue Channel

| Hardware Sales |

| Connectivity Service Subscriptions |

| Advertising and E-commerce |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Rest of Middle East |

| By System Type | Seat-back IFE Hardware |

| Wireless/BYOD Streaming Servers | |

| In-seat Power and Peripherals | |

| Cabin Connectivity (Ku/Ka/LEO) | |

| By Aircraft Type | NarrowBody Aircraft |

| WideBody Aircraft | |

| Regional Jets | |

| By Fit Type | Original Equipment Manufacturer (OEM) |

| Aftermarket | |

| By Revenue Channel | Hardware Sales |

| Connectivity Service Subscriptions | |

| Advertising and E-commerce | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East |

Market Definition

- Product Type - Entertainment provided to aircraft passengers during a flight refers to In-flight entertainment. The seatback screens which are used to provide entertainment are included under the IFE system product type.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms