Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

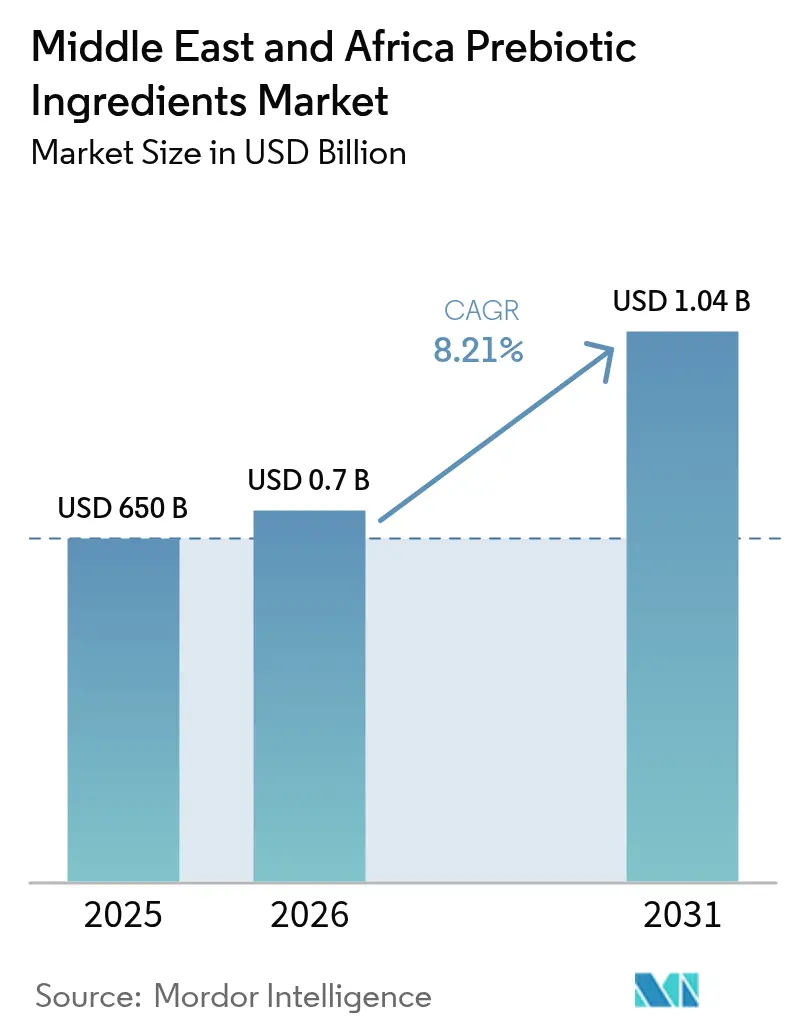

| Base Year Market Size (2025) | USD 650 Billion |

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Prebiotic Ingredients Market Analysis by Mordor Intelligence

The prebiotic ingredients market size in the Middle East and Africa was valued at USD 650 million in 2025 and estimated to grow from USD 703.37 million in 2026 to reach USD 1.04 billion by 2031, at a CAGR of 8.21% during the forecast period (2026-2031). The market is driven by the growing prevalence of non-communicable diseases, prompting consumers to seek gut-health solutions incorporated into everyday foods. Also, governments in various regions are addressing malnutrition and supporting the prebiotic ingredients market by integrating dietary fibers into subsidized staples through national fortification programs. Premium brands in the GCC are reformulating products to reduce sugar content while preserving taste, frequently combining low-calorie sweeteners with soluble fibers to deliver both functional and sensory advantages. Additionally, ingredient suppliers are increasing regional production capacities to address shipping disruptions and fertilizer-related chicory-root price fluctuations, ensuring a reliable supply and expanding applications in both food and animal feed industries.

Key Report Takeaways

- By ingredient type, inulin captured 45.83% of the Middle East and Africa prebiotic ingredients market share in 2025, while galacto-oligosaccharides (GOS) are forecast to expand at a 9.98% CAGR through 2031.

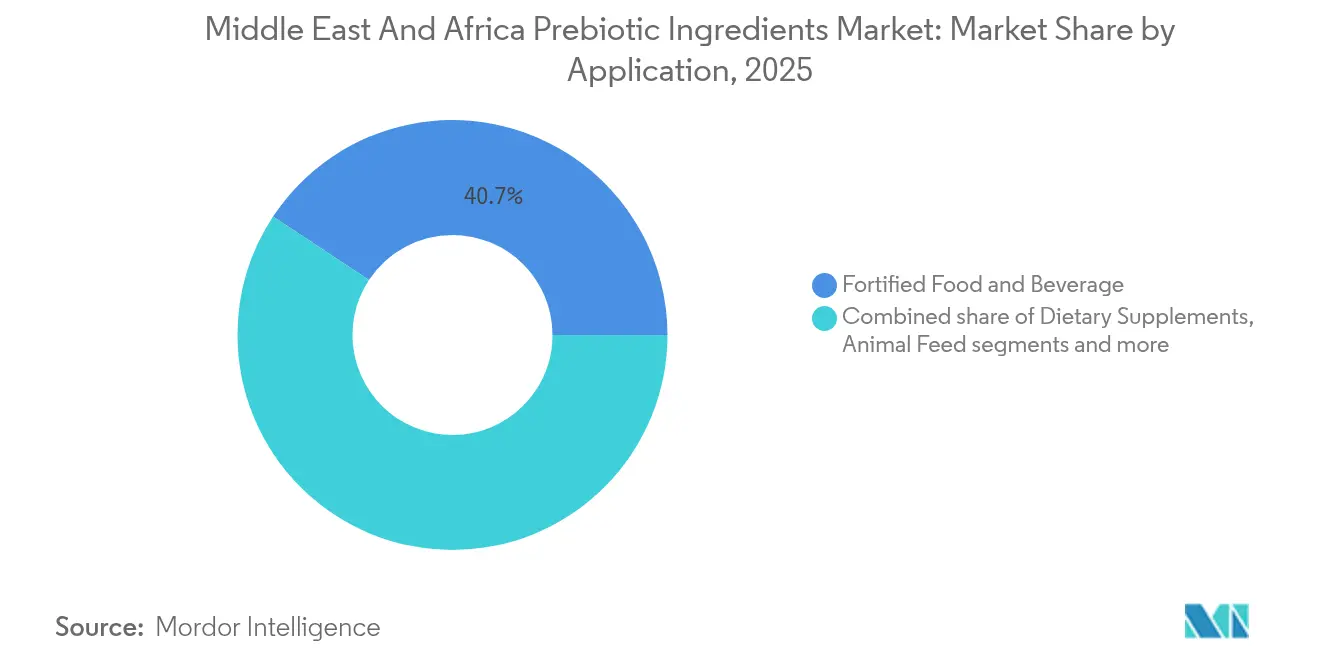

- By application, fortified food and beverage products accounted for a 40.72% share of the Middle East and Africa prebiotic ingredients market size in 2025; animal feed is projected to grow fastest at a 9.57% CAGR to 2031.

- By country, South Africa contributed 27.15% of regional demand in 2025, whereas Nigeria is expected to register the highest 8.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Prebiotic Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising gut health awareness and digestive issues | +2.1% | Saudi Arabia, United Arab Emirates, South Africa; spillover to Egypt, Nigeria | Medium term (2-4 years) |

| Expansion of functional foods and beverages | +1.8% | GCC countries, South Africa, Egypt; urban centers across United Arab Emirates | Short term (≤ 2 years) |

| Focus on infant and early-life nutrition | +1.5% | Nigeria, Egypt, Saudi Arabia; expanding to Morocco, Kenya | Medium term (2-4 years) |

| Government nutrition and fortification programmes | +1.3% | Egypt, Nigeria, Morocco; regional UN Nutrition Collaboration Framework (MENA) | Long term (≥ 4 years) |

| Product reformulation for sugar and calorie reduction | +1.0% | United Arab Emirates, Saudi Arabia, Turkey; premium segments in South Africa | Short term (≤ 2 years) |

| Growing focus on gut health drives use of prebiotic fibers in pet foods and feed additives | +0.9% | South Africa, GCC (Saudi Arabia, United Arab Emirates); poultry-intensive Egypt, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising gut health awareness and digestive issues

The increasing awareness of gut health and the prevalence of digestive issues are driving the demand for prebiotic ingredients in the region. Consumers are recognizing the strong connection between immune function and gut health. Digestive disorders have seen a significant rise, with a 2025 study titled "Socioeconomic and Demographic Disparities in the Impact of Digestive Diseases in the Middle East and North Africa (MENA) Region" reporting that total cases of digestive diseases in MENA increased from 19.7 million to 45.4 million, as per the National Library of Medicine [1]Source: National Library of Medicine, "Socioeconomic and Demographic Disparities in the Impact of Digestive Diseases in the Middle East and North Africa (MENA) Region", pubmed.ncbi.nlm.nih.gov. This sharp rise highlights the growing health burden and the increasing demand for products that support digestive health and immunity. Consumers are becoming more aware that maintaining gut health can enhance immune resilience, driving interest in functional foods and supplements containing prebiotic fibers. In response to this trend, brands like Danone are addressing the demand with fortified dairy and infant nutrition products that include prebiotic ingredients aimed at optimizing gut microbiota. This focus on health is also fostering innovation in product development, particularly in infant nutrition and adult digestive health supplements, contributing to the growth of the prebiotic ingredients market in the Middle East and Africa, where gut health is a prominent health concern. The combination of rising digestive disease rates and increasing healthcare awareness continues to support growth opportunities for prebiotic ingredients in the region. This dynamic is shaping consumer education, brand strategies, and product portfolio expansions, all aligned with the emphasis on gut-mediated immune health in the Middle East and Africa markets.

Expansion of functional foods and beverages

The reformulation of functional food and beverages is advancing across urban areas in the Middle East and Africa, driven by rising incomes, a growing expatriate population, and rapid retail modernization, which are increasing the demand for healthier product options. For instance, Tate & Lyle highlighted this trend by showcasing its EUOLIGO fructo-oligosaccharides (FOS) and TASTEVA M stevia at Gulfood Manufacturing in November 2024, targeting beverage and confectionery manufacturers in the region seeking to reduce sugar content while maintaining sweetness and taste. Also, Euoligo Fos supports sugar reduction and fiber fortification, addressing important health concerns such as digestive health and overall nutritional quality. This innovation aligns with consumer preferences for natural, reduced-sugar ingredients, reflecting growing health awareness and regulatory pressures to lower sugar consumption. These reformulations address the demand for functional benefits, such as improved digestive health supported by prebiotic fibers, while also responding to broader cultural shifts toward wellness and preventive health among increasingly health-conscious and cosmopolitan urban populations. The combination of evolving consumer preferences and advancements in ingredient technology, as demonstrated by Tate & Lyle's offerings, is driving growth in the prebiotic ingredients segment of the functional foods and beverages market. Furthermore, these products enable manufacturers to differentiate themselves in a competitive retail environment that is increasingly focused on premiumization and clean-label trends, fostering sustained innovation and market expansion driven by consumer demand for products that deliver both health benefits and sensory quality in everyday foods and beverages.

Product reformulation for sugar and calorie reduction

The increasing focus on sugar reduction is reshaping ingredient specifications in premium food and beverage segments across the Middle East and Africa, driven by regulatory scrutiny and heightened consumer health awareness. This shift is particularly critical due to the high prevalence of metabolic diseases in the region. According to the International Diabetes Federation, Saudi Arabia recorded an adult diabetes prevalence of 23.1% in 2024 (approximately 5.34 million adults), while the United Arab Emirates reported 20.7% (around 1.27 million adults) [2]Source: International Diabetes Federation, "Diabetes in Saudi Arabia (2024)", idf.org . These statistics underscore the need for reduced sugar and calorie content in product formulations. Prebiotic fibers such as inulin and Fructo‑oligosaccharides (FOS) are gaining traction as partial sugar replacers and bulking agents, offering sweetness and texture with lower sugar content while delivering digestive health benefits. These fibers enable clean-label claims and align with wellness-oriented consumer preferences in urban premium markets. Manufacturers are increasingly combining non-nutritive sweeteners with prebiotic fibers to maintain taste and mouthfeel while achieving calorie reduction targets. This reformulation strategy is being applied across categories such as dairy, beverages, and confectionery, where incremental sugar reductions per serving contribute to significant calorie savings. As retailers refine product assortments and regulators enforce sugar thresholds, procurement specifications now frequently include fiber functionality alongside sweetness targets, driving demand for prebiotic ingredient suppliers offering application support for stability, solubility, and sensory performance in heat-treated and shelf-stable products. This trend highlights the structural link between metabolic health concerns, regulatory focus, and the adoption of prebiotic ingredients, reinforcing steady market demand for functional fibers in reformulated premium products.

Growing focus on gut health drives use of prebiotic fibers in pet foods and feed additives

The growing emphasis on gut health is driving the adoption of prebiotic fibers in pet foods and feed additives across the Middle East and Africa, supported by a significant rise in pet ownership, particularly in urban areas. USDA data indicates that the pet population in the United Arab Emirates increased from 588,700 in 2014 to 938,000 in 2024, spurring demand for premium pet food products enriched with functional ingredients [3]Source: United States Department of Agriculture (USDA), "'Pawsperity' in the Pet Food Market", apps.fas.usda.gov. This trend highlights pet owners' increasing focus on providing nutrition that enhances digestive health, immunity, and overall well-being, reflecting broader human health trends. Prebiotic fibers such as inulin, Fructo‑oligosaccharides (FOS), and Galacto‑oligosaccharides (GOS) are being integrated into formulations to support gut microbiota balance, improve nutrient absorption, and enhance digestive comfort in companion animals. Leading brands like Royal Canin and Hill’s Science Diet are leveraging these benefits in their product offerings for the region, targeting health-conscious consumers seeking advanced pet care solutions. Technological advancements in extrusion and dehydration processes are further enabling the preservation of ingredient efficacy and palatability, even under the region's challenging climate and logistical conditions. Additionally, regulatory requirements emphasizing ingredient transparency and halal compliance are driving demand for high-quality, traceable prebiotic-enhanced pet foods. South Africa has emerged as a key manufacturing hub in the region, benefiting from a strong agricultural base to serve Middle East and African markets. The combination of a growing pet population and rising awareness among pet owners is creating a strong growth trajectory for prebiotic ingredient adoption in animal nutrition, a critical component of the regional market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import dependency and chicory-inulin price volatility | -1.2% | Egypt, Nigeria, Morocco, GCC; all net-importing Middle East and Africa markets | Short term (≤ 2 years) |

| Price sensitivity at manufacturer level | -0.8% | Nigeria, Egypt, Morocco; price-conscious mass-market segments | Medium term (2-4 years) |

| Limited consumer awareness in many developing markets | -0.6% | Rural Nigeria, Egypt, Morocco; lagging 40% behind urban Saudi Arabia | Long term (≥ 4 years) |

| Regulatory ambiguity on "prebiotic" label claims | -0.5% | Saudi Arabia (SFDA delays ~25% launches), fragmented Middle East and Africa regulatory landscape | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High import dependency and chicory-inulin price volatility

Reliance on imports and price volatility of chicory-inulin pose significant challenges for the prebiotic ingredients market in the Middle East and Africa (MEA). The region depends heavily on imported chicory-derived inulin and fructooligosaccharides (FOS) from Europe and Asia due to limited local production of essential raw materials like chicory roots. This dependency increases exposure to global supply chain disruptions, rising logistics costs, and fluctuating freight rates, which amplify procurement risks given the region's distance from primary production hubs. Chicory-inulin prices are particularly volatile, influenced by weather conditions affecting European harvests, currency fluctuations, and competing demands from larger markets, creating uncertainty in formulation budgets and long-term contracts. For instance, periodic price adjustments for BENEO's Orafti inulin, a leading branded chicory prebiotic, impact MEA supply chains, forcing food and supplement producers to either absorb higher costs or seek alternatives. This situation discourages consistent inclusion rates, especially in cost-sensitive applications such as dairy, bakery, and infant nutrition, where profit margins are tight. Additionally, regional manufacturers face challenges in negotiating favorable terms with distant suppliers, often resulting in higher landed costs compared to domestic alternatives in more self-sufficient markets. While efforts to explore local blending or alternative fibers like acacia are underway, these measures are insufficient to offset chicory-inulin's dominance in premium prebiotic formulations. Consequently, market growth remains constrained, emphasizing the need for diversified sourcing strategies and regional production investments to mitigate these challenges.

Limited consumer awareness in many developing markets

Consumer awareness remains a significant challenge in developing markets, particularly in the Middle East and Africa (MEA), where education levels vary widely between urban and rural areas. Urban centers such as Dubai and Johannesburg benefit from growing health literacy, supporting the adoption of premium fortified products. However, rural regions, including large parts of Nigeria, Egypt, and sub-Saharan Africa, prioritize basic nutrition over specialized gut health benefits, limiting the demand for prebiotic ingredients. Misconceptions about prebiotics, often conflated with generic fiber or overshadowed by probiotics, further hinder market growth. A 2024 study in Saudi Arabia revealed that only 21.9% of adults had high awareness of prebiotics, while 51.8% reported low familiarity, reflecting a broader regional trend of limited public understanding due to insufficient targeted campaigns, as per the National Library of Medicine. This urban-rural divide complicates efforts to justify premium pricing for prebiotic-enriched foods and supplements, as retailers in less-developed areas stock fewer functional products, reducing visibility and consumer access. Manufacturers are reluctant to invest in rural distribution, given the uncertain returns from education initiatives, perpetuating low market penetration. Categories such as bakery, dairy, and mass-market beverages face particular challenges, as low consumer literacy impedes impulse purchases. Simplified communication strategies linking prebiotics to everyday digestive health are essential, yet current efforts remain urban-focused, restricting overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Galacto‑oligosaccharides (GOS) Gains on Inulin's Dominance

Inulin held 45.83% of the ingredient-type share in 2025, driven by its cost-effectiveness, clean-label appeal, and decades of clinical validation that reinforce its role in digestive health and satiety applications across dairy, bakery, and supplements. Its versatility and established supply chains position inulin as the preferred fiber for manufacturers aiming to balance efficacy with affordability in premium formulations. Meanwhile, galacto-oligosaccharides (GOS) are projected to grow at a 9.98% CAGR through 2031, the fastest among ingredient types. This growth is attributed to their potent bifidogenic effects, which selectively nourish beneficial gut bacteria, and strong regulatory acceptance, particularly in infant formula, where GOS mimics human milk oligosaccharides for immune and digestive support. The increasing demand in urban markets is challenging inulin's lead as GOS adoption rises in early-life nutrition.

Fructo-oligosaccharides (FOS) maintain a balanced position in the market, valued for their neutral taste profile that enables seamless integration into beverage and confectionery applications without altering sensory qualities. For example, Tate & Lyle's EUOLIGO FOS, showcased at Gulfood Manufacturing in November 2024, supports sugar reduction efforts in the Middle East. Additionally, other ingredients like mannan-oligosaccharides (MOS) and functional fibers such as resistant starch and pectin are steadily gaining traction in animal feed and specialized human nutrition. These alternatives, despite having less robust clinical evidence compared to inulin and GOS, address niche applications such as pet nutrition and metabolic health, contributing to diversified portfolio strategies in the evolving prebiotic ingredients market.

By Application: Animal Feed Outpaces Fortified Food Growth

Fortified food and beverage applications accounted for 40.72% of the 2025 revenue, driven by the integration of prebiotics into everyday staples such as bread, dairy products, juices, and confectionery. These products resonate with urban consumers seeking digestive health benefits without compromising familiar tastes. Manufacturers have effectively leveraged prebiotics for clean-label claims, ensuring volume stability through broad accessibility across retail channels. Meanwhile, animal feed is projected to grow at a 9.57% CAGR through 2031, fueled by increasing livestock production demands, poultry export goals, and stringent feed-efficiency requirements. Research in Saudi Arabia demonstrates that combining plant fiber with organic acids enhances gut integrity and feed conversion ratios, particularly under the heat stress prevalent in the region's arid climates. This trend underscores the growing importance of prebiotics in protein-rich animal nutrition.

Aquaculture is emerging as a promising niche within the animal feed segment, with Egyptian researchers emphasizing the benefits of functional additives such as MOS, FOS, GOS, and β-glucans in improving disease resistance and growth in fish farming. This complements the gains seen in poultry feed by addressing the need for protein diversification in coastal markets. Additionally, the infant formula segment, though smaller in revenue, leads in innovation as formulators focus on GOS and FOS to mimic the microbiome, aligning with parental preferences for immune-supporting, premium early-life products. Dietary supplements are also experiencing growth, supported by the rise of e-commerce, where a significant portion of regional sales now occurs online. Emerging applications, including pharmaceuticals, personal care, and pet food, are attracting venture capital due to their high-margin potential, extending the versatility of prebiotics into specialized wellness areas. This diversification strengthens the foundation of fortified foods while the rapid growth of the animal feed segment reshapes application dynamics, emphasizing nutrition efficiency.

Geography Analysis

South Africa is projected to hold a 27.15% market share in 2025, positioning itself as a key player in the regional prebiotic ingredients market. This leadership is supported by advanced retail infrastructure that facilitates the distribution of premium functional products and the presence of established dairy and bakery sectors, where prebiotics like inulin are incorporated into staple products. The introduction of front-of-pack Warning Labels in 2023 has accelerated product reformulation efforts, focusing on reducing sugar content and increasing fiber levels. This shift has driven demand for cost-effective fibers, such as Ingredion's NUTRAFLORA scFOS, particularly in urban markets. While the country's relatively affluent urban population is receptive to global food trends and prebiotic ingredients, rural areas remain underserved, limiting full market penetration.

Saudi Arabia complements South Africa's volume leadership with high consumer awareness of the link between gut health and immune function, alongside a high prevalence of digestive disorders. This has driven the adoption of prebiotics in supplements and fortified dairy products, with innovation evident in categories such as beverages, where FOS (fructooligosaccharides) supports clean-label claims, aligning with regulatory initiatives promoting wellness. The market's premium health positioning further strengthens its role in driving demand for prebiotic ingredients.

Nigeria is expected to achieve a 8.89% compound annual growth rate (CAGR) through 2031, the highest among countries such as the United Arab Emirates, Saudi Arabia, South Africa, Morocco, Egypt, and Turkey. This growth is driven by a youthful demographic that boosts long-term demand, large-scale fortification programs targeting staple foods, and rapid urbanization that channels rural migrants toward gut health products. Nigeria's growth trajectory complements South Africa's infrastructure advantages, while Morocco and Egypt contribute through steady dairy fortification efforts. Additionally, the United Arab Emirates supports the market with premium imports, and Turkey strengthens regional dynamics with functional exports, ensuring a balanced growth outlook for the region.

Competitive Landscape

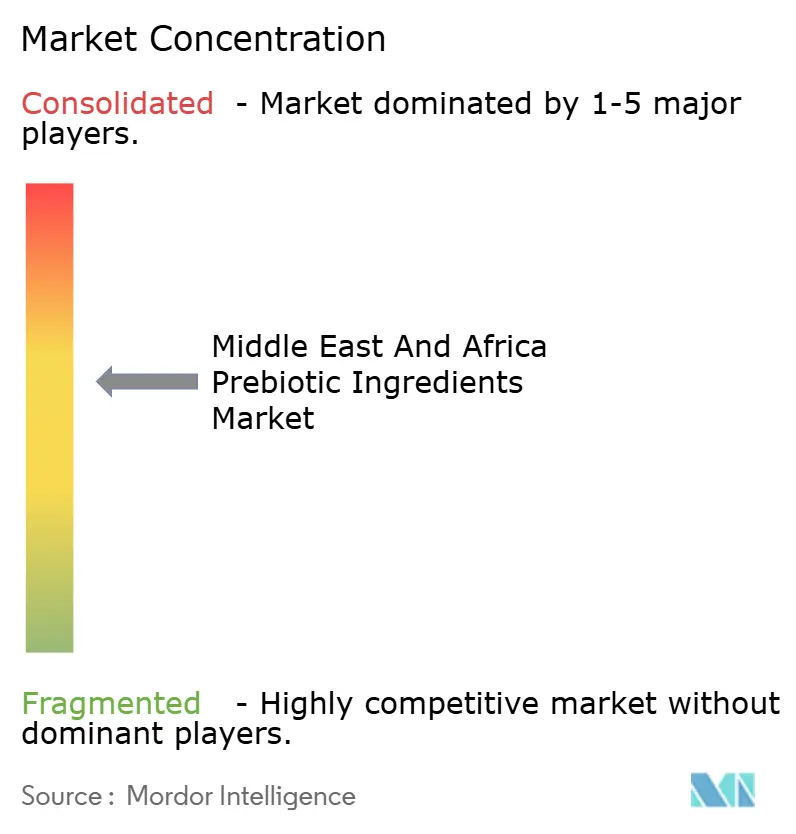

The prebiotic ingredients market in the Middle East and Africa exhibits moderate consolidation, with European chicory-root processors such as Beneo (Südzucker Group), Sensus (Cosun), and Cosucra maintaining a strong presence. These companies cater to the dairy sectors in South Africa and the United Arab Emirates, leveraging their extensive expertise in inulin production. Their dominance in fortified bakery and beverage markets is particularly evident in urban centers such as Johannesburg and Dubai, where consumer demand for clean-label products aligns with their cost-efficient offerings. Regional distributors play a pivotal role in ensuring consistent product availability, especially in import-dependent markets like Saudi Arabia and Egypt.

The influence of these European processors extends further to Morocco and Turkey, where chicory-based solutions, such as Beneo's Orafti inulin, are utilized in confectionery reformulations to achieve sugar reduction without compromising sensory quality. This strategy has bolstered their position in premium applications across the United Arab Emirates and South Africa. While moderate market consolidation provides opportunities for smaller players to explore niche segments, such as Nigeria's growing supplements market, European processors maintain a competitive edge. Their technical support, clinical validation, and focus on ensuring product stability under arid storage conditions have secured their loyalty among large-scale formulators in key markets like Egypt and Saudi Arabia.

Despite the stronghold of European processors, regional dynamics introduce competitive challenges. Companies such as Fonterra and Ingredion are gaining traction in the galacto-oligosaccharides (GOS) segment for infant formula in South Africa, the United Arab Emirates, and Morocco. Additionally, Olygose is targeting aquaculture feed applications in Egypt and Turkey. In Nigeria and Saudi Arabia, partnerships between these players and local processors are diluting the dominance of European suppliers, fostering innovation in heat-stable blends tailored to poultry feed applications. The market continues to reward scale in chicory supply while also valuing agility in addressing high-growth applications, resulting in a moderately concentrated competitive landscape across the region.

Middle East And Africa Prebiotic Ingredients Industry Leaders

-

Südzucker Group

-

Coöperatie Koninklijke Cosun U.A.

-

Ingredion Incorporated

-

Royal FrieslandCampina N.V.

-

Cosucra Groupe Warcoing SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Tate & Lyle introduced a range of sweetener and stabilizer solutions designed for the Middle Eastern market. This initiative aimed to meet the increasing demand for healthier product formulations in the region while improving taste and texture. The introduced ingredients included Euoligo Fos, a non-GMO dietary fiber, and Tasteva M, a stevia-based sweetener. Euoligo Fos also supported sugar reduction and fiber fortification, addressing critical health concerns such as digestive health and overall nutritional quality.

- October 2024: Future Food Foundry (3F), a UAE-based agri-food tech investor, invested USD 5 million in Greeneration (Dubai), a vertical farming operator specializing in edible flowers, microgreens, and specialty leaves. This investment was intended to support Greeneration's expansion beyond premium culinary ingredients into health- and sustainability-focused product lines. These offerings included superfoods such as spirulina, chia, and goji; adaptogens like ashwagandha and rhodiola; medicinal herbs such as turmeric and ginger; probiotic-containing functional foods; and sustainable plant-based proteins.

- September 2024: DSM-Firmenich Animal Nutrition and Health opened a new premix and additives manufacturing facility in Sadat City, Egypt, with an annual production capacity of 10,000 tons. The plant was equipped with Bühler technology and an integrated plant control system featuring barcoding. It was designed to serve customers in Egypt, the Middle East, Southern Europe, and Africa, addressing the increasing demand from mid-sized and large livestock farms as well as feed millers for premixes and advanced feed additives.

Middle East And Africa Prebiotic Ingredients Market Report Scope

The Middle East and Africa prebiotic ingredient market is segmented by ingredient type into inulin, FOS (fructo-oligosaccharide), GOS (galacto-oligosaccharide), and other ingredients; and by application into infant formula, fortified food and beverage, dietary supplements, animal feed, and others. Also, the study provides an analysis of the prebiotic ingredient market in the emerging and established markets across Middle East and Africa, including South Africa, Saudi Arabia, United Arab Emirates, Nigeria, Egypt, Morocco, Turkey, and the Rest of the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

By Ingredient Type

| Inulin |

| Fructo‑oligosaccharides (FOS) |

| Galacto‑oligosaccharides (GOS) |

| Other Ingredients (MOS and Other Functional Fibres) |

By Application

| Infant Formula |

| Fortified Food and Beverage |

| Dietary Supplements |

| Animal Feed |

| Other Applications |

By Country

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Ingredient Type | Inulin |

| Fructo‑oligosaccharides (FOS) | |

| Galacto‑oligosaccharides (GOS) | |

| Other Ingredients (MOS and Other Functional Fibres) | |

| By Application | Infant Formula |

| Fortified Food and Beverage | |

| Dietary Supplements | |

| Animal Feed | |

| Other Applications | |

| By Country | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is driving sustained growth of prebiotic ingredients across Middle East and Africa?

Government-backed fortification mandates, rising gut-health awareness, and localized production investments underpin an 8.21% CAGR through 2031.

Which ingredient type is gaining fastest?

Galacto-oligosaccharides are projected at a 9.98% CAGR, benefiting from regulatory acceptance in infant-formula applications.

How large will animal feed usage become?

Animal feed exhibits the highest 9.57% application CAGR, positioning it as the next frontier for volume growth.

Which country offers the strongest near-term upside?

Nigeria, expanding at a 8.89% CAGR, combines fortification programs with a rapidly urbanizing, youthful population.

Page last updated on: