Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

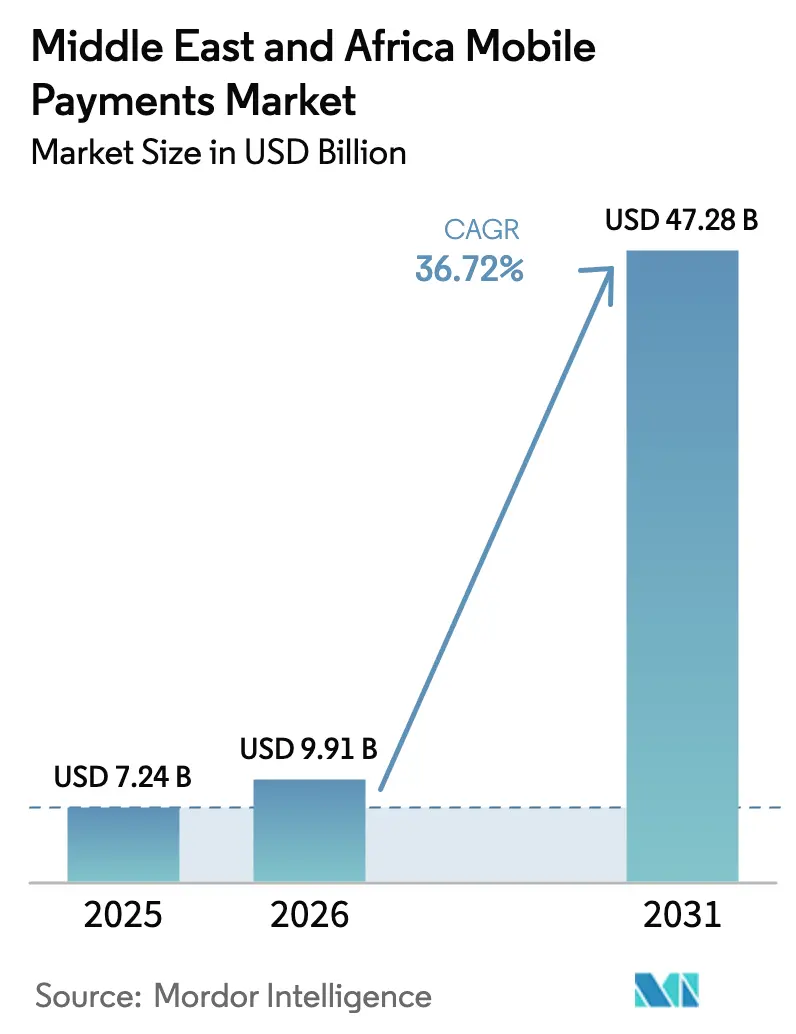

| Base Year Market Size (2025) | USD 7.24 Billion |

| Market Size (2026) | USD 9.91 Billion |

| Market Size (2031) | USD 47.28 Billion |

| Growth Rate (2026 - 2031) | 36.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Mobile Payments Market Analysis by Mordor Intelligence

The Middle East And Africa Mobile Payments Market size was valued at USD 7.24 billion in 2025 and estimated to grow from USD 9.91 billion in 2026 to reach USD 47.28 billion by 2031, at a CAGR of 36.72% during the forecast period (2026-2031).

Explosive growth is rooted in three structural shifts: deeper smartphone penetration, widespread 4G/5G coverage and the convergence of telco wallets with bank-grade rails.[1]Rishi Raithatha, “The State of the Industry Report on Mobile Money 2025,” GSMA, gsma.com Government cash-to-digital agendas, real-time payment rails and cross-border corridors are compressing adoption cycles, while super-app ecosystems reshape customer acquisition economics. Merchant acceptance costs continue to fall as SoftPOS-enabled smartphones replace traditional terminals, enabling micro-merchants to join the formal digital economy. Intense competition among telcos, banks and fintechs is translating into product innovation around Buy Now Pay Later (BNPL), QR codes and wage-linked wallets, creating sticky user engagement and larger addressable volumes for the Middle East and Africa mobile payments market.

Key Report Takeaways

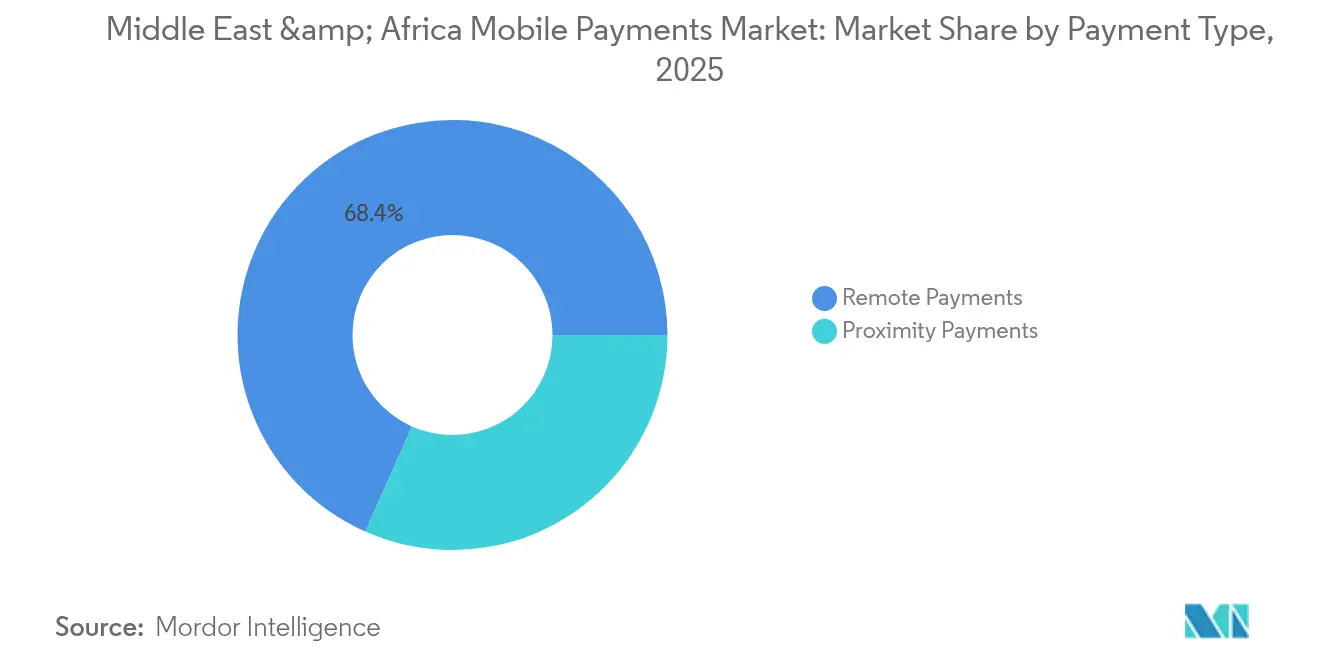

- By payment type: Remote payments held 68.35% of the Middle East and Africa mobile payments market share in 2025, while proximity payments are projected to expand at a 30.05% CAGR through 2031.

- By transaction type: In-store POS led with 40.55% revenue share in 2025; P2P transactions are growing fastest at a 32.1% CAGR to 2031.

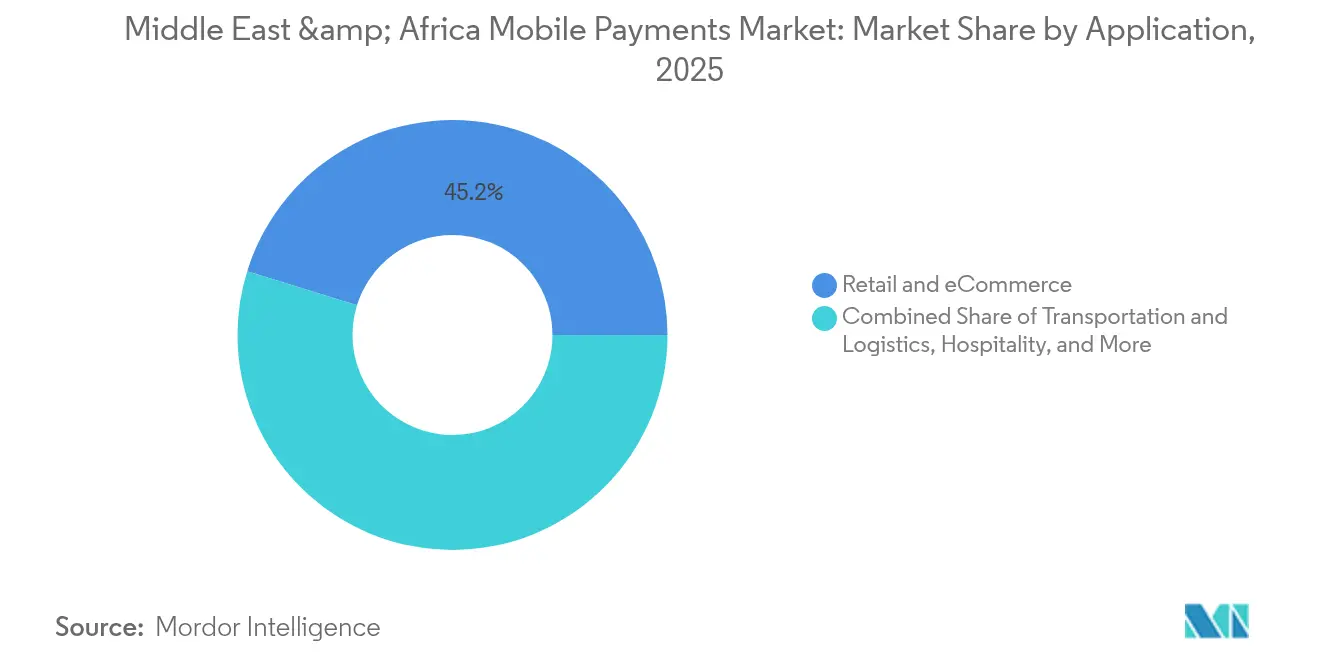

- By application: Retail & e-commerce dominated with 45.20% share in 2025; the government & public sector segment is forecast to rise at a 40.35% CAGR through 2031.

- By end-user: Personal transactions accounted for 77.30% of the Middle East and Africa mobile payments market size in 2025, while business transactions are advancing at a 28.4% CAGR to 2031.

- By geography: Africa captured 56.65% of the Middle East and Africa mobile payments market share in 2025; the Middle East region is projected to deliver the fastest growth with a 39.9% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC Wage-Protection-System (WPS) Mandates Accelerating Cash-to-Digital Migration | +7.8% | GCC countries (UAE, Saudi Arabia, Qatar, Kuwait, Oman, Bahrain) | Medium term (2-4 years) |

| BNPL-Enabled Wallet Loyalty Programs Boosting Transaction Frequency in UAE & KSA | +5.2% | UAE, Saudi Arabia, with spillover to other GCC states | Short term (≤ 2 years) |

| Telco-Super-App Race Unlocking Rural USSD Adoption in Sub-Saharan Africa | +9.5% | Nigeria, Kenya, South Africa, Ghana, with expansion to other Sub-Saharan countries | Medium term (2-4 years) |

| SoftPOS Roll-outs Among Micro-Merchants (Visa Tap-to-Phone Pilots) | +6.3% | South Africa, Egypt, UAE, Saudi Arabia, with expansion to other urban centers | Short term (≤ 2 years) |

| Wallet-to-Wallet GCC–Africa Remittance Corridors Cutting Transfer Fees | +4.1% | UAE-Nigeria, Saudi Arabia-Egypt, Qatar-Kenya corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GCC Wage-Protection-System (WPS) Mandates Accelerating Cash-to-Digital Migration

WPS compliance reached 99.8% in the UAE and 92% in Saudi Arabia in 2024, onboarding 5.8 million formerly cash-paid workers into digital channels.[2]White & Case LLP, “Unlocking Potential: GCC FinTech Trends, Regulations and Funding Outlook,” White & Case, whitecase.com Mandatory wage digitisation funnels recurring salary inflows into mobile wallets, boosting average non-salary transaction frequency by 3.2 times for providers such as STC Pay. The programme is expanding across Bahrain, Qatar and Oman, standardising payroll rails and lowering customer-acquisition costs. Banks benefit from float balances while telco wallets monetise fees on remittances and bill-pay. The initiative embeds financial inclusion at scale, cementing long-term volume upside for the Middle East and Africa mobile payments market.

BNPL-Enabled Wallet Loyalty Programs Boosting Transaction Frequency in UAE & KSA

Tabby’s integration with STC Pay lifted wallet transaction frequency by 42% in 2024, underscoring BNPL’s ability to extend consumer credit within existing digital wallets.[3]Visa Inc., “Visa Tap to Phone Adoption Soars: 200% Year over Year Growth Worldwide,” Visa Newsroom, visa.com BNPL adoption has reached 39% in the UAE and 42% in Saudi Arabia, driving USD 10 billion in annual wallet volumes and generating 2.7-times higher average ticket sizes versus traditional cards. Merchants gain higher conversion rates, consumers obtain deferred payments, and wallet operators capture interchange and late-fee income. Rapid scaling of BNPL-wallet hybrids is likely to deepen user stickiness and sharpen competitive differentiation in the Middle East and Africa mobile payments market.

Telco Super-App Race Unlocking Rural USSD Adoption in Sub-Saharan Africa

Orange’s Max it targets 45 million active users by 2025, leveraging USSD to reach low-end feature phones.[4]Jie Wang, “EM 2.0: A Road for the Digital Intelligent Transformation of African Carriers,” Huawei, huawei.com Telebirr in Ethiopia already services 40 million users, processing USD 3 billion in monthly transactions—roughly 30% of national GDP. Super-app positioning lets telcos bundle payments, micro-credit and insurance, extracting multi-line revenue while lowering churn. USSD resilience in low-bandwidth regions broadens addressable volumes and entrenches telcos as dominant players across the Middle East and Africa mobile payments market.

SoftPOS Roll-outs Among Micro-Merchants (Visa Tap-to-Phone Pilots)

Visa’s Tap-to-Phone recorded 200% year-over-year global growth in 2025, with strong momentum in South Africa, Egypt, UAE and Saudi Arabia. Converting Android phones into acceptance devices slashes hardware costs and formalises previously cash-only merchants—30% of new users were entirely new to digital payments. The technology supports contactless consumer preferences (61% of shoppers now prefer tap-and-go), enhances data capture for loyalty programmes and accelerates merchant onboarding. Widescale SoftPOS uptake is expected to rebalance transaction mix toward proximity payments and expand addressable GDP for the Middle East and Africa mobile payments market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Licensing Across 45+ African Regulators Delays Market Entry | -4.3% | Pan-African, with particular impact on cross-border payment initiatives | Long term (≥ 4 years) |

| Mobile-Money Transaction Caps in Nigeria & Egypt Reduce Ticket Size | -3.1% | Nigeria, Egypt, with spillover effects to neighboring countries | Medium term (2-4 years) |

| High USSD Fraud Rates Trigger Bank-Imposed PIN-Retry Limits | -2.7% | Sub-Saharan Africa, particularly Uganda, Zambia, and Kenya | Short term (≤ 2 years) |

| PAPSS Funding Gaps Slow Real-time Rail Deployment in Francophone Africa | -2.1% | West and Central African Economic and Monetary Union (WAEMU) countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Licensing Across 45+ African Regulators Delays Market Entry

Payment providers allocate 18-24% of their operating budgets to compliance as they navigate divergent licence classes and fee structures. Approval timelines range from three months to over one year, dampening time-to-market for cross-border propositions. Activity-based licensing models in Kenya and Ghana offer promising templates, but broad harmonisation remains a long-term agenda. The resulting friction restricts capital inflows, stifles innovation and clips growth for the Middle East and Africa mobile payments market.

Mobile-Money Transaction Caps in Nigeria & Egypt Reduce Ticket Size

Tiered KYC ceilings in Nigeria cap daily wallet transfers at NGN 5 million (USD 3,275), while Egypt enforces similar ceilings to curb money-laundering risk. Consequently, average mobile-money ticket sizes remain 62% lower than bank transfers, forcing providers to prioritise frequency over value. Although regulators aim to safeguard stability, the caps limit use cases such as B2B settlements and large remittances, tempering overall wallet revenue in the Middle East and Africa mobile payments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Proximity Surge Reshapes Transaction Landscape

Remote payments accounted for 68.35% of the Middle East and Africa mobile payments market in 2025, driven by bill-pay and e-commerce transfers. Visa’s Tap-to-Phone and widespread NFC handsets are now nudging proximity adoption upward with a projected 30.05% CAGR, especially in GCC urban centres where contactless initiatives led to a 47% uptick in 2024. Retailers gain higher throughput at checkout, while consumers benefit from tap-and-go convenience. Transaction data mined from proximity events enables hyper-local offers, boosting merchant sales and deepening ecosystem engagement.

The rapid diffusion of SoftPOS among micro-merchants lowers acceptance costs and targets previously cash-only outlets, expanding addressable volumes for the Middle East and Africa mobile payments market. Proximity payments also facilitate offline authentication, a vital feature in intermittent-connectivity environments. As infrastructure scales, the proximity share is expected to close the gap with remote transactions, shifting provider focus toward in-store experiences and embedded commerce offerings.

By Transaction Type: P2P Growth Drives Financial Inclusion

POS transactions led with a 40.55% share in 2025, reflecting high smartphone penetration and merchant digitisation across GCC states. P2P transfers, however, are projected to outpace other flows at a 32.1% CAGR, buoyed by remittance needs and limited branch networks. First-time mobile money users in Africa initiate 78% of their journeys through P2P, making it a critical acquisition funnel for the Middle East and Africa mobile payments market size.

International mobile-money remittances reached USD 34 billion in 2024. Providers are layering value-added services such as savings pots, micro-loans and insurance to monetise rising wallet balances. As regulators progress toward real-time-gross settlement interoperability, P2P corridors will deepen liquidity and reinforce the ecosystem’s role in economic integration.

By Application: Government Sector Emerges as Growth Engine

Retail & e-commerce captured 45.20% of the Middle East and Africa mobile payments market in 2025, fuelled by mobile-first checkout journeys and QR-enabled pop-up stores. Seamless purchasing improves conversion rates and basket sizes, compelling merchants to integrate multiple wallet options.

Public-sector adoption is accelerating at a 40.35% CAGR as digital identities and e-government portals gain traction under Saudi Vision 2030 and UAE Digital Government Strategy 2025. Digital disbursement of subsidies, fines and licence fees anchors volumes, lowers cash-handling costs and enhances transparency. Large-scale use cases catalyse ecosystem effects, bringing under-banked citizens into repeated digital interactions and expanding the Middle East and Africa mobile payments market.

By End-user: Business Segment Accelerates Digital Transformation

Personal wallets held a commanding 77.30% share in 2025, underscoring the pivotal role of mobile money in everyday financial lives. This dominance stems from salary deposits, bill payments and small-value retail transactions that together form the backbone of the Middle East and Africa mobile payments market share.

Business usage is forecast to expand at a 28.4% CAGR as enterprises digitise supplier settlements, payroll and B2B marketplaces. In Uganda, mobile-money transaction value exceeded UGX 100 trillion (USD 26 billion) in 2023. Digital workflows streamline reconciliation and improve liquidity, while higher transaction limits and API connectivity unlock embedded-finance propositions tailored for SMEs.

Geography Analysis

Africa held 56.65% of the Middle East and Africa mobile payments market in 2025, anchored by Kenya’s mobile-money transactions that equalled 59% of national GDP. Sub-Saharan smartphone adoption is expected to reach 44% by 2025, expanding the addressable base for USSD and app-based wallets. Despite chronic infrastructure gaps, telco innovation around offline authentication mitigates session failures caused by rural latency of 250 ms, which drives an 18% USSD drop-off rate.

The Middle East is on a faster growth curve with a projected 39.9% CAGR through 2031. Saudi Arabia’s target of 70% cashless transactions by 2025 and the UAE’s cash share already down to 17% of POS in 2023 illustrate the policy-led pivot toward digital money. Real-time payment systems processed USD 230 billion in 2023 and are forecast to surpass USD 903 billion by 2028 across the six GCC states.

Cross-regional wallet-to-wallet remittance corridors connect GCC migrant wage earners with African recipients, trimming fees and accelerating settlement. The Pan-African Payment and Settlement System is a potential game-changer, though funding gaps are delaying its rollout in Francophone blocs. These converging factors suggest a complementary rather than competitive dynamic, with Africa’s user scale and the Middle East’s infrastructure sophistication jointly propelling the Middle East and Africa mobile payments market.

Competitive Landscape

The competitive structure is bifurcated: telco-backed platforms command over 60% of active mobile-money accounts in Africa, while Middle Eastern markets showcase a mix of bank wallets and independent fintechs. East Africa is highly concentrated around M-Pesa, whereas Nigeria, Egypt and the UAE exhibit more fragmented shares. Global card networks are partnering instead of competing head-on—Mastercard’s alliance with Orange Money opens digital acceptance across seven African countries.

Strategic thrusts focus on ecosystem breadth. Super-app ambitions from Orange, MTN and STC co-locate payments with ride-hailing, micro-loans and insurance, creating multi-line monetisation. SoftPOS and biometric authentication differentiate challengers targeting micro-merchant acquisition in urban corridors. Cross-border remittance corridors, merchant aggregation in underserved segments and vertical-specific solutions such as healthcare payments represent whitespace opportunities that could reshape competitive standings within the Middle East and Africa mobile payments industry.

Incumbents are responding with accelerated M&A and minority stake investments. Recent funding rounds and partnerships—such as PayPal with TerraPay and Visa with Emirates NBD—signal a pivot toward embedded cross-border capabilities and tailored SME propositions. As regulatory sandboxes open and open-banking APIs mature, data analytics and AI-driven fraud modules will become decisive assets in earning consumer trust and scaling volumes across the Middle East and Africa mobile payments market.

Middle East And Africa Mobile Payments Industry Leaders

Orange S.A. (Orange Money)

Fawry (MyFawry)

Careem (CareemPay)

Vodafone Group

HyperPay Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vanstone Electronic showcased A99 smart POS terminals at Seamless Middle East, signalling a push to localise hardware for micro-merchants and capture SoftPOS spill-over demand.

- April 2025: PayPal partnered with TerraPay to weave its global network into Africa–GCC remittance corridors, expanding reach while TerraPay gains brand credibility among migrants.

- March 2025: Flydubai and Network International introduced mobile money payments for ancillary airline services in East Africa, creating incremental wallet use cases in travel.

- March 2025: Klaim secured USD 26 million to streamline healthcare claim settlements, leveraging embedded payments to shorten billing cycles for providers and insurers.

- March 2025: Checkout.com’s alliance with Tabby scales BNPL acceptance for UAE and Saudi retailers, locking in high-value millennial shoppers who favour instalment plans.

- January 2025: Sumitomo Corporation invested in Zension Technologies to bundle device subscriptions with in-wallet warranty payments, addressing rising smartphone demand in GCC.

- October 2024: Orange MEA partnered with Mastercard to extend Orange Money wallet acceptance across seven countries, reinforcing cross-border utility and card-scheme rails.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Middle East & Africa mobile payments market as the total value of proximity and remote transactions that are initiated on a handset via smartphone apps, USSD mobile money menus, QR or NFC taps, and settled in real time or near real time through wallet or mobile-money rails.

Scope Exclusions: Loads to prepaid cards, card-present POS swipes where no handset is involved, and desktop-only bank transfers are not counted.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

- Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Turkey

- Oman

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Morocco

- Rest of Africa

- Middle East

Detailed Research Methodology and Data Validation

Primary Research

Interviews with regulators, telco wallet managers, fintech founders, and merchant acquirers across Gulf states plus key African corridors helped us validate daily active metrics, user churn, and unreported cash-to-digital migration speeds. Structured surveys with small retailers and ride-hailing drivers further clarified typical ticket sizes and acceptance pain points.

Desk Research

We began with macro anchors from the World Bank, IMF, and national statistics offices to size household consumption, remittance inflows, and smartphone penetration. Central bank payment dashboards in Saudi Arabia, Nigeria, the UAE, South Africa, and Kenya provided annual wallet volumes, while GSMA Mobile Money reports supplied active account ratios and fee averages. Trade groups such as the Payments Association of South Africa and peer-reviewed journals offered elasticity insights. For company-level checks, our analysts accessed D&B Hoovers and Dow Jones Factiva to extract operator filings, funding rounds, and tariff changes. The sources listed are illustrative; many additional regulatory, press, and proprietary datasets fed the evidence base.

Market-Sizing & Forecasting

A blended top-down model converts consumer spending, migrant remittances, and formal retail turnover into a potential payment pool, then applies mobile wallet penetration, active user share, and ticket frequency factors. Select bottom-up validations, such as merchant roll-ups in Kenya and POS token counts in the UAE, tune country totals before regional aggregation. Key variables include smartphone data costs, QR acceptance density, interchange caps, BNPL wallet adoption, and agent network reach. Forecasts deploy multivariate regression linking wallet activity to GDP per capita, mobile data price, and regulatory openness; three scenarios are stress tested with senior interviewees.

Data Validation & Update Cycle

Outputs are reconciled against GSMA tallies, central bank settlement totals, and sampled operator revenues. An internal peer review and supervisor sign-off precede release. We refresh every twelve months, issuing interim updates if policy shocks, major funding rounds, or merger events materially shift trajectories.

Why Mordor's Middle East and Africa Mobile Payments Baseline Stands Firm

Published estimates often diverge because studies broaden or narrow the instruments, geographies, or revenue lenses they capture.

Mordor's framework sticks to handset initiated spend and revisits core drivers annually, thereby reducing drift and hindsight bias. Key gap drivers among other publishers include counting prepaid card loads, quoting processor fee revenue rather than gross payment value, or focusing solely on Gulf states while omitting populous African markets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 7.24 B USD (2025) | Mordor Intelligence | |

| 20.52 B USD (2023) | Regional Consultancy A | Includes digital wallet and card-based payments plus prepaid reloads, inflating totals. |

| 44 B USD (2025) | Industry Databook B | Focuses only on the Middle East and mixes prepaid card value with wallet spend. |

| 6 B USD (2025) | Global Aggregator C | Reports processor fee revenue, not transaction value, thereby understating market size. |

Taken together, the comparison shows that Mordor's disciplined scope selection, dual path modeling, and frequent refreshes deliver a balanced, transparent baseline that decision makers can track and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Middle East and Africa mobile payments market?

The market is valued at USD 9.91 billion in 2026 and is projected to climb to USD 47.28 billion by 2031 at a 36.72% CAGR.

Why are proximity payments growing so quickly in the region?

SoftPOS roll-outs, NFC handset penetration and government cashless agendas are simplifying acceptance for merchants and driving consumer demand for tap-and-go convenience.

How do Wage-Protection-System mandates affect mobile payments growth?

WPS rules push salaries into digital accounts, onboarding millions of low-income workers who then use wallets for everyday purchases, remittances and bill pay.

Which application segment is expanding fastest?

Government and public-sector payments are expected to grow at a 40.35% CAGR as digital IDs and e-government services embed mobile payment rails into public service delivery.

What are the main regulatory barriers facing providers?

Fragmented licensing across over 45 African regulators and transaction caps in Nigeria and Egypt increase compliance costs and limit high-ticket transactions.

How concentrated is the competitive landscape?

Roughly 70% of active users are with the top five platforms, indicating moderate concentration and ongoing room for new entrants that can differentiate on cross-border, SME or vertical-specific solutions.

Page last updated on: