Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

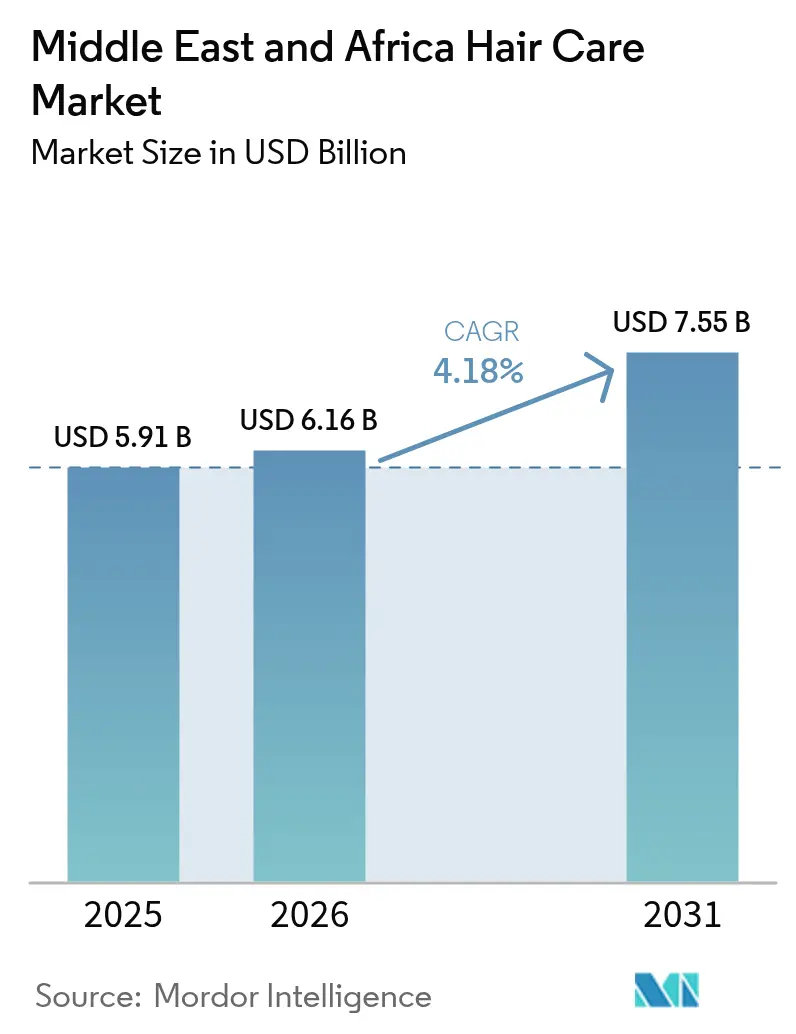

| Base Year Market Size (2025) | USD 5.91 Billion |

| Market Size (2026) | USD 6.16 Billion |

| Market Size (2031) | USD 7.55 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Hair Care Market Analysis by Mordor Intelligence

The Middle East and Africa hair care market size in 2026 is estimated at USD 6.16 billion, growing from 2025 value of USD 5.91 billion with 2031 projections showing USD 7.55 billion, growing at 4.18% CAGR over 2026-2031. Key growth drivers include demographic advantages, halal-focused regulations, and a shift toward premium products among Gen Z consumers. The region's diverse population, with varying hair care needs, is driving demand for tailored products. The increasing influence of social media is expanding male grooming routines, while government incentives are supporting the establishment of local production hubs. Synthetic formulations still dominate, yet natural alternatives are carving measurable volume as COSMOS and other certification schemes gain traction[1]Source: ChemLinked Team. "Indonesian Halal Cosmetics Regulations Explained at PCHi 2024." cosmetic.chemlinked.com. Digital retail is experiencing significant growth, driven by national e-commerce strategies, despite challenges posed by gray-market activities impacting authorized sales channels.

Key Report Takeaways

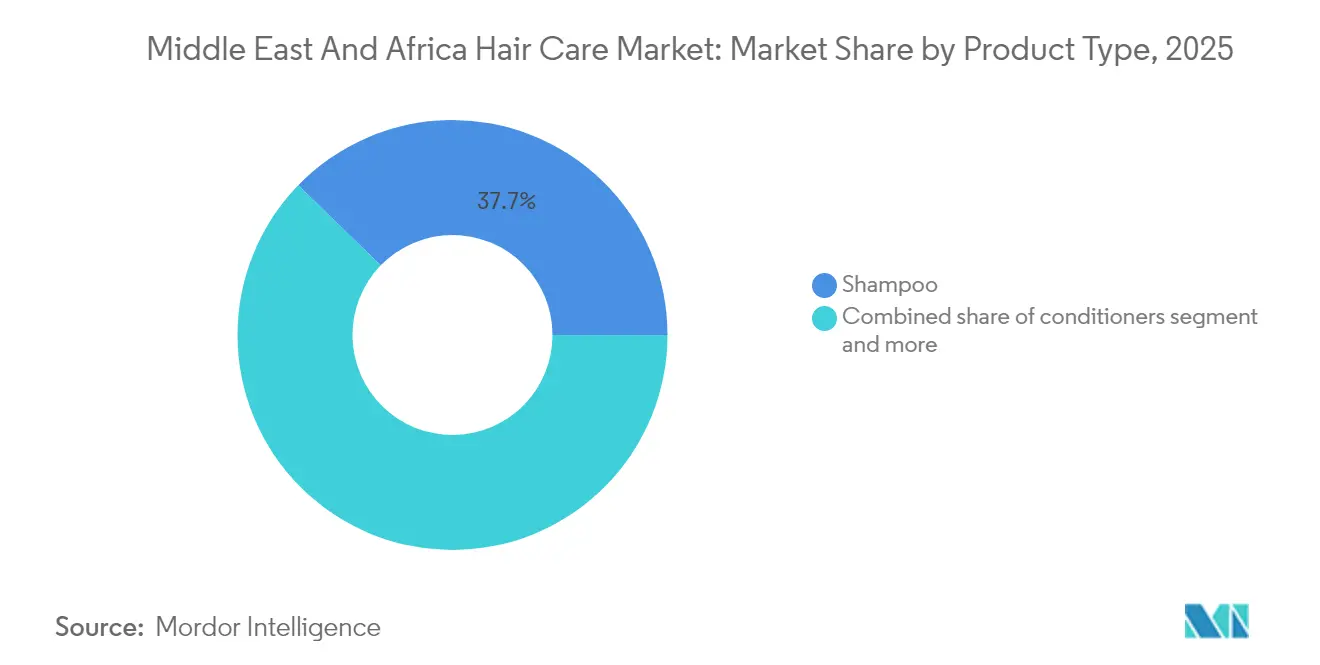

- By product type, shampoos led with 37.74% revenue share in 2025; hair styling products are forecast to expand at a 5.07% CAGR through 2031.

- By category, the mass segment held 72.58% revenue share in 2025, while premium is projected to grow at a 5.87% CAGR through 2031.

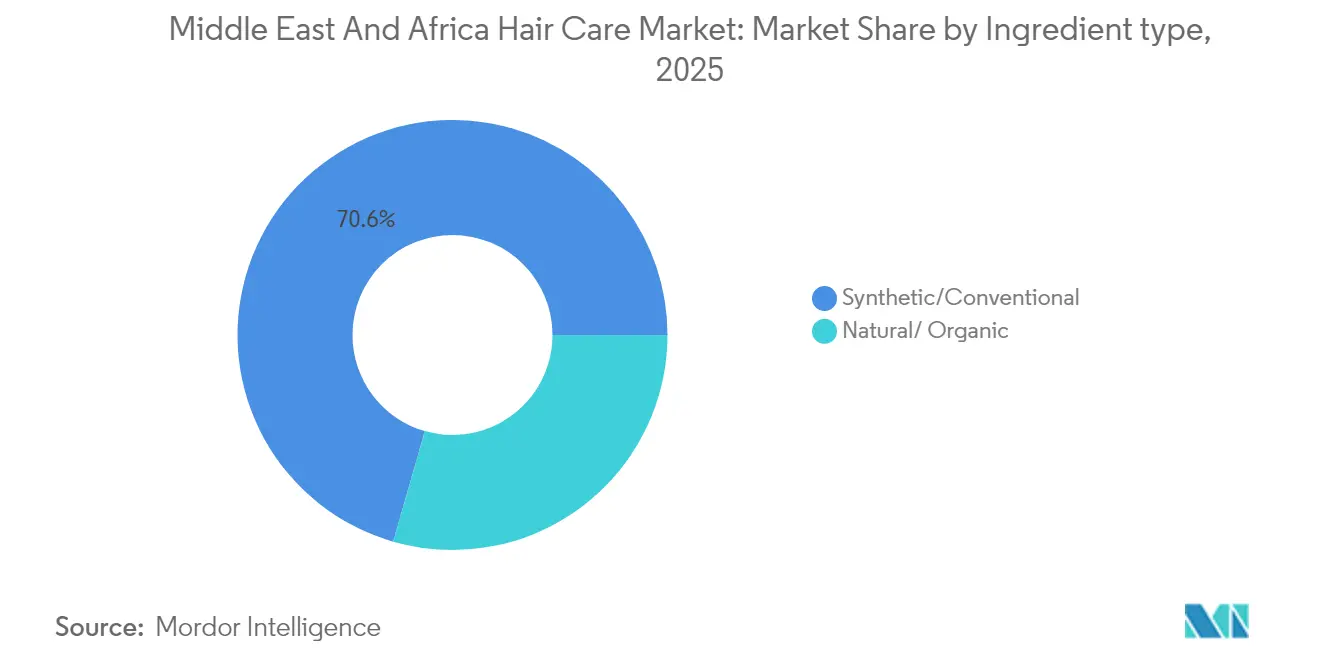

- By ingredient type, synthetic formulations commanded 70.55% revenue share in 2025; natural and organic are advancing at a 5.84% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for a 39.88% share of the Middle East and Africa hair care market size in 2025, and online channels are expected to expand at a 5.68% CAGR through 2031.

- By geography, Saudi Arabia held a 22.94% share of the Middle East and Africa hair care market size in 2025; South Africa is forecast to expand at a 6.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium halal-certified product launches | +0.8% | Global, concentrated in GCC and North Africa | |

| Rising male-grooming spend influenced by social media | +0.6% | Saudi Arabia, United Arab Emirates, Egypt with spillover to broader MENA | |

| Growing demand for natural and sulfate-free formulations | +0.7% | Global, early adoption in GCC and South Africa | |

| Government incentives for local cosmetics manufacturing | +0.5% | United Arab Emirates, Saudi Arabia, Egypt with expansion to other MEA markets | |

| High vitamin-D deficiency driving hair-loss remedies | +0.4% | Saudi Arabia, United Arab Emirates, Qatar, Kuwait | |

| Technological advancements in manufacturing | +0.3% | Regional manufacturing hubs: United Arab Emirates, Egypt, South Africa | |

| Source: Mordor Intelligence | |||

Premium halal-certified product launches

Premium halal certification is evolving from regulatory compliance to strategic differentiation, with brands leveraging certification to command price premiums while accessing broader Muslim consumer segments. The Standards and Metrology Institute for Islamic Countries (SMIIC) operates technical committees specifically for halal cosmetic issues, with Saudi Arabia's SFDA participating as a member organization to harmonize regional standards[2]Source: Standards and Metrology Institute for Islamic Countries. "SMIIC — Saudi Food and Drug Authority." smiic.org. Indonesia's mandatory halal certification framework, requiring BPJPH-issued certificates from October 2026, establishes operational precedents that MEA manufacturers are adopting proactively to maintain export competitiveness. This regulatory evolution creates first-mover advantages for brands that integrate halal compliance into product development rather than retrofitting existing formulations. The certification process demands segregated production lines, halal-compliant ingredient sourcing, and comprehensive supply chain traceability, effectively raising barriers to entry while rewarding established players with robust quality systems. Premium positioning becomes sustainable when halal certification combines with performance claims, enabling brands to capture both religious compliance and efficacy-driven purchase decisions across diverse consumer segments.

Rising male-grooming spend influenced by social media

Male grooming expenditure is accelerating across MEA markets, driven by social media influence and changing cultural attitudes toward male personal care investment. Saudi Arabia's demographic profile, with 63% of the population under 30 years and 82% social media penetration, creates concentrated demand for male-targeted hair care products influenced by digital content creators and grooming tutorials[3]Source: BeautyMatter Studio. "Gen Z Redefining The Middle East Consumer Landscape." BeautyMatter, beautymatter.com. This trend extends beyond traditional markets, with Marico's MENA operations delivering 47% growth in 2024, partly attributed to expanding male consumer segments and premiumization strategies targeting younger demographics. Social media platforms are reshaping purchase journeys, with approximately 90% of UAE and Saudi consumers influenced by online content, creating opportunities for brands that develop authentic influencer partnerships and educational content around male hair care routines. The shift represents a fundamental change in male consumer behavior, moving from functional hair care to lifestyle-driven grooming regimens that incorporate multiple products and premium price points. Brands that successfully navigate cultural sensitivities while delivering social media-worthy results are capturing disproportionate market share growth in this emerging segment.

Growing demand for natural and sulfate-free formulations

Natural and sulfate-free formulations are gaining traction as consumers increasingly prioritize ingredient transparency and scalp health, supported by regulatory frameworks that facilitate innovation in botanical actives. African ethnobotanical research identifies 68 plant species from 39 families used traditionally for hair treatment, with 30 species demonstrating clinical evidence for hair growth and scalp care applications. This scientific validation of traditional ingredients creates opportunities for brands to develop culturally relevant formulations that combine heritage knowledge with modern efficacy standards. Ecocert's COSMOS certification framework, operating in 130+ countries, provides credible natural and organic claims validation that enables premium positioning and export market access. The trend toward sulfate-free formulations aligns with increasing consumer awareness of scalp sensitivity and hair damage, particularly relevant in MEA markets where climate conditions and water quality create additional hair care challenges. Regulatory support for natural ingredients, combined with supply chain development for botanical actives, positions natural formulations as a sustainable growth driver rather than a niche segment.

Government incentives for local cosmetics manufacturing

Government-backed manufacturing incentives are reshaping supply chain strategies, with MEA countries offering comprehensive packages to attract cosmetics production investment and reduce import dependence. The UAE's "Make it in the Emirates" initiative provides access to competitively priced raw materials, world-class logistics infrastructure connecting 80% of the global population within an 8-hour flight radius, and 100% foreign ownership policies that eliminate traditional partnership requirements. Saudi Arabia's Vision 2030 localization targets, combined with premium residency programs launched in 2024 and Investment Promotion Authority facilitation, create attractive conditions for establishing regional manufacturing hubs. Egypt's 2024 legislation allowing foreign ownership of land for investment projects, coupled with tax exemptions, significantly reduces greenfield entry costs for international manufacturers. These incentives extend beyond traditional tax benefits to include infrastructure development, regulatory streamlining, and market access facilitation that collectively reduce the total cost of ownership for local production. The strategic imperative intensifies as supply chain resilience becomes critical, with companies like Himalaya Wellness investing AED 200 million in UAE manufacturing facilities to serve global markets through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity and grey-market imports | -0.9% | Nigeria, Egypt, Kenya with spillover effects across Sub-Saharan Africa | Short term (≤ 2 years) |

| Regulatory approval delays for new cosmetic actives | -0.5% | Saudi Arabia, United Arab Emirates, Egypt with regional harmonization effects | Medium term (2-4 years) |

| Water-scarcity driven sustainability pressures on factories | -0.4% | United Arab Emirates, Saudi Arabia, South Africa, Morocco | Medium term (2-4 years) |

| Cultural preference for DIY herbal remedies | -0.3% | Nigeria, Kenya, Morocco, Egypt with traditional medicine prevalence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price sensitivity and grey-market imports

Price sensitivity remains a fundamental constraint across MEA markets, exacerbated by grey-market imports that undermine authorized distribution channels and erode brand equity through counterfeit proliferation. Nigeria's beauty and cosmetics industry faces significant counterfeiting challenges, with consumers identifying fake products primarily through packaging quality (28.1%), product performance (17.6%), and suspiciously low pricing (12.6%), indicating sophisticated counterfeit operations that exploit price-conscious consumer segments. The UAE's position as a major trade hub creates both opportunities and risks, with Dubai Customs reporting 2,147 seizures and 388 intellectual property disputes in 2022, including significant volumes of counterfeit cosmetics entering regional supply chains through physical markets and e-commerce platforms. Currency devaluations compound pricing pressures, with companies like Godrej Consumer Products experiencing a 25% revenue decline in their Africa, United States and Middle East operations due to Naira devaluation and currency impacts, despite margin improvements through mix optimization. The challenge intensifies as grey-market operators leverage accessible packaging technology and e-commerce platforms to distribute counterfeit products at scale, requiring brands to invest heavily in authentication technologies, consumer education, and enforcement partnerships with customs authorities.

Water-scarcity driven sustainability pressures on factories

Water scarcity is driving fundamental shifts in manufacturing processes, with companies investing in waterless formulations and closed-loop systems to maintain operational sustainability in resource-constrained environments. The emergence of waterless beauty formulations addresses both environmental concerns and operational efficiency, with products removing up to 70% of traditional water content while delivering concentrated actives and extended shelf life. This trend is particularly relevant in MEA markets where water stress affects manufacturing costs and regulatory compliance, forcing companies to redesign production processes around water conservation principles. Regulatory frameworks are evolving to incorporate sustainability requirements, with Dubai Municipality's cosmetics guidelines emphasizing environmental protection and resource management as compliance factors. Manufacturing facilities are implementing advanced water recycling systems, with projects like Himalaya Wellness's Dubai facility incorporating solar energy and water recycling technologies to achieve operational sustainability targets. The constraint creates competitive advantages for companies that successfully transition to water-efficient manufacturing, while penalizing traditional producers that fail to adapt to resource scarcity realities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoos Dominate Despite Styling Surge

Shampoos maintain market leadership with 37.74% share in 2025, reflecting their essential role in daily hair care routines across diverse MEA consumer segments. The category's dominance stems from universal usage patterns and frequent repurchase cycles that create stable revenue streams for manufacturers. Hair styling products emerge as the fastest-growing segment with a 5.07% CAGR through 2031, driven by urbanization trends and social media influence on grooming standards. Conditioners occupy the second-largest position, benefiting from increased consumer awareness of hair damage caused by harsh climate conditions prevalent across MEA regions. Hair colorants represent a specialized segment with growth potential tied to cultural acceptance and regulatory approvals for specific ingredients.

L'Oréal's product innovation demonstrates category evolution, with the company unveiling AirLight Pro at CES 2024, a professional-grade hair dryer incorporating infrared-light technology that delivers up to 33% more hydrated hair while consuming 31% less energy than premium competitors. This technological advancement reflects the industry's shift toward multifunctional products that combine styling efficiency with hair health benefits. The Others category, encompassing treatments and specialized products, shows promise as consumers become more sophisticated in their hair care routines and seek targeted solutions for specific concerns like hair loss and scalp health.

By Category: Mass Market Leads While Premium Accelerates

Premium segments are experiencing rapid expansion at 5.87% CAGR through 2031, despite mass-market products commanding 72.58% share in 2025. This growth differential reflects evolving consumer preferences toward quality and efficacy over price sensitivity, particularly among younger demographics who prioritize product performance and brand authenticity. The premium segment's acceleration is supported by increasing disposable incomes in key markets and the influence of social media on beauty standards and product awareness.

Unilever's strategic focus on premium positioning exemplifies this trend, with the company launching its high-end Nexxus Promend collection in Shanghai in February 2025, targeting the premium sector that is growing approximately 12% annually. The mass-market segment's continued dominance reflects the region's diverse economic landscape, where price accessibility remains crucial for market penetration. However, the gap between mass and premium growth rates suggests a gradual market evolution toward higher-value products as economic development progresses across MEA countries.

By Ingredient Type: Synthetic Dominance Faces Natural Challenge

Natural and organic formulations are advancing at a 5.84% CAGR through 2031, challenging the synthetic segment's 70.55% market share in 2025. This growth trajectory reflects increasing consumer awareness of ingredient safety and environmental impact, supported by regulatory frameworks that facilitate natural ingredient innovation. The synthetic segment's current dominance stems from established supply chains, cost advantages, and proven efficacy in addressing specific hair care concerns.

Scientific research validates the natural ingredient opportunity, with studies identifying 68 African plant species used traditionally for hair treatment, of which 30 species demonstrate clinical evidence for hair growth and scalp care applications. This ethnobotanical foundation provides formulation opportunities that combine cultural relevance with scientific validation. The transition toward natural ingredients is supported by certification frameworks like COSMOS standards and regulatory acceptance of botanical actives, creating pathways for premium positioning and export market access.

By Distribution Channel: Digital Disruption Accelerates

Supermarkets and hypermarkets held a dominant 39.88% share of the Middle East and Africa hair care market in 2025.This digital acceleration reflects changing consumer shopping behaviors, particularly among younger demographics who research products online before purchasing. The growth is supported by improving logistics infrastructure, digital payment adoption, and government initiatives promoting e-commerce development across MEA markets.

Egypt's e-commerce evolution illustrates this transformation, with the market projected to grow from USD 9.05 billion in 2024 to USD 18.04 billion by 2029 at a 14.8% CAGR, supported by the National E-Commerce Strategy and Regulated E-Commerce framework launched in December 2024. Convenience and grocery stores, specialty beauty stores, and pharmacies maintain significant shares through their accessibility and personal service advantages. The channel evolution creates opportunities for brands that develop omnichannel strategies combining digital discovery with physical experience, particularly in markets where consumer trust in online purchases is still developing.

Geography Analysis

In 2025, Saudi Arabia holds a leading 22.94% market share, driven by its Vision 2030 economic diversification initiatives and strong consumer spending in urban centers like Riyadh and Jeddah. Government support through investment incentives and premium residency programs introduced in 2024 has attracted international brands to establish regional operations. Regulatory frameworks by the Saudi Food and Drug Authority ensure clear product registration pathways and uphold safety standards, with updates to prohibited and restricted substances lists made in 2025. The UAE follows as a strategic hub, leveraging its "Make it in the Emirates" initiative, which offers 100% foreign ownership and access to competitively priced raw materials. Smaller but affluent markets like Kuwait, Qatar, Oman, and Bahrain benefit from high per-capita consumption, premium product preferences, and growing e-commerce adoption.

South Africa is the fastest-growing market, with a projected CAGR of 6.01% through 2031, supported by a growing middle class and increasing beauty consciousness. Stable economic conditions and established retail infrastructure facilitate product distribution and brand building. Despite health concerns in other regions, hair relaxer sales remain strong in South Africa and other African markets, reflecting cultural preferences and beauty standards. Nigeria, while offering significant population-driven opportunities, faces challenges like currency devaluation and economic volatility, prompting cautious strategies by companies like Procter & Gamble. Meanwhile, Kenya, Egypt, and Morocco present balanced growth opportunities with improving regulatory environments and expanding retail channels, while smaller markets in the region offer niche opportunities for premium and specialized products.

Travel retail is emerging as a key distribution channel across MEA markets, with Dubai Duty Free achieving record revenue of USD 2.16 billion in 2023, including USD 374 million from perfume sales. Airport expansions, such as Saudi Arabia's King Fahd expansions and Dubai's USD 35 billion Al Maktoum International terminal, create significant retail opportunities for hair care brands. High passenger volumes in 2023—approximately 90 million in Dubai, 46 million in Doha, and 42.7 million in Jeddah—provide access to diverse international consumer segments, enabling brand discovery among travelers from key markets like India and China.

Regulatory Landscape

Hair care products across the Middle East and Africa are regulated under national cosmetics frameworks that require pre-market notification or registration, labeling controls, and ingredient and safety documentation. In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) governs cosmetics (including shampoos, conditioners, dyes, and relaxers) through its implementing regulation and product classification guidance, and it also issued updated guidance in 2025 covering cosmetic product notification and conditions for clearance and raw materials used in manufacturing.

In the UAE, cosmetic products are subject to conformity assessment requirements administered by the Ministry of Industry and Advanced Technology (MoIAT) through the Emirates Conformity Assessment Scheme (ECAS) under Cabinet Resolution No. 18 of 2014. Dubai Municipality requires cosmetics to be registered before being placed on the Dubai market through the Montaji system under Local Order No. 11 of 2003 and related technical guidelines. Across GCC markets, the movement of finished products and packaging practices is shaped by regional standards (via GSO/GCC alignment), which increases the need for consistent technical files, ingredient disclosure, and compliant claims management for cross-border distribution.

Value Chain Analysis

The value chain covers ingredient and packaging inputs (surfactants, preservatives, fragrances or essential oils, and primary packaging), formulation and filling, quality and regulatory compliance, and multi-channel distribution across modern trade, pharmacies, specialty beauty retail, and e-commerce. Multinational brand owners (such as L'Oréal, Unilever, Procter & Gamble, Henkel, and Dabur) work alongside regional and local manufacturers and contract producers, with the UAE serving as a key hub for GCC-oriented production and re-export, supported by logistics and compliance infrastructure.

Regulatory gates affect multiple points in the chain beyond market entry. Product notification and registration systems (for example, Dubai Municipality Montaji and SFDA notification or clearance requirements) raise the demand for documentation-ready formulations, ingredient traceability, and compliant labeling. GCC-wide standardization also increases the importance of harmonized packaging and safety practices. Grey-market leakage and counterfeiting pressure authorized distribution, so brand owners and distributors increasingly emphasize tighter channel control, authentication, and closer coordination with importers, retailers, and e-commerce platforms.

Competitive Landscape

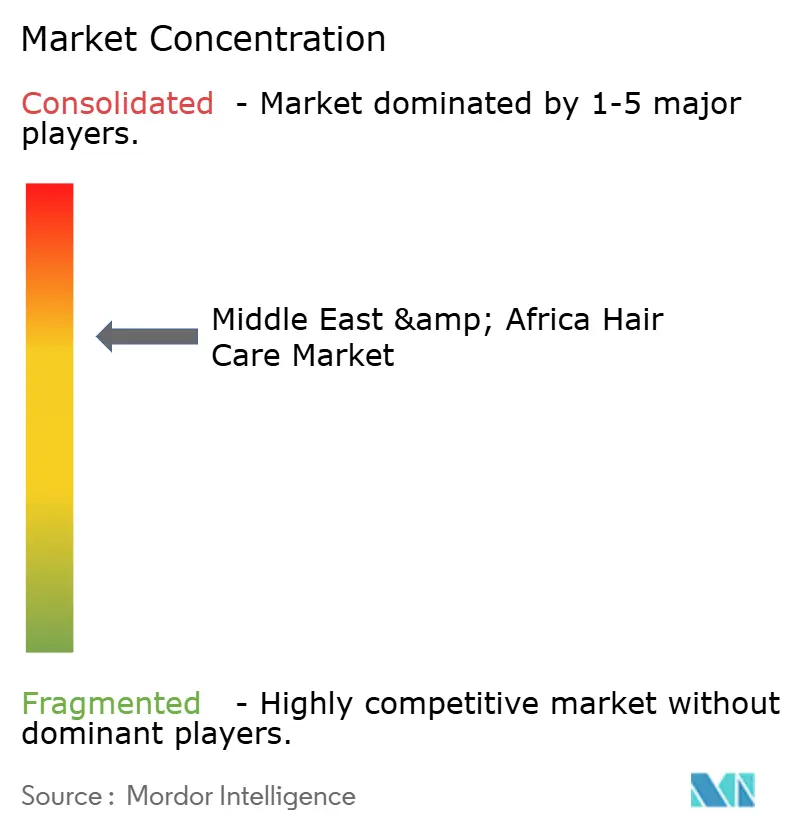

The Middle East and Africa hair care market is highly concentrated, with a score of 7 out of 10, dominated by multinational players such as L'Oréal, Unilever, Procter & Gamble, Henkel, and Dabur International. Significant barriers to entry, including regulatory compliance costs, distribution network requirements, and brand-building investments, limit competition in this diverse market. In 2024, L'Oréal's SAPMENA-SSA zone reported EUR 3.86 billion in sales, reflecting 12.0% growth, highlighting the scale advantages of established players with regional infrastructure and market expertise. Localization strategies, such as manufacturing investments, halal certification adoption, and premium segment development, are increasingly targeting younger demographics prioritizing sustainability and ingredient transparency.

Technology adoption is emerging as a critical competitive factor, with companies investing in beauty tech innovations, digital distribution platforms, and sustainable manufacturing processes to enhance market share. L'Oréal's AirLight Pro launch exemplifies this trend, integrating infrared-light technology with energy efficiency to address both performance and environmental concerns. Untapped opportunities exist in natural and organic formulations, male grooming, and specialized treatments for hair loss and scalp health, where traditional players have limited presence.

Emerging disruptors, such as UAE-based Mony Beauty, are addressing market gaps. Launched in June 2024, Mony Beauty focuses on natural curly hair extensions sourced from South Indian temple donations, catering to the demand for textured-hair products in Middle Eastern markets. Companies with established quality systems and regulatory expertise gain operational advantages in navigating frameworks like Dubai Municipality's cosmetics guidelines and SFDA requirements, further strengthening their market position.

Middle East And Africa Hair Care Industry Leaders

-

L'Oréal Group

-

Henkel AG & Co. KGaA

-

Procter & Gamble

-

Unilever PLC

-

Dabur International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ongoing standard-setting and manufacturing compliance programs create room for companies that can localize production and scale quality systems across multiple MEA markets. In 2026, Egypt adopted ISO 22716 alignment for cosmetics production through updated licensing requirements (with implementation starting April 16, 2026 and a grace period), while Kenya introduced new harmonized cosmetic standards via the Kenya Bureau of Standards, including standards covering hair sprays and oils. These moves tend to favor manufacturers and brand owners with GMP-aligned plants, strong QA processes, and export-ready labeling and technical files.

Alongside compliance-driven shifts, the market is seeing investment in professionalization and localized capability building in major demand centers. L'Oréal opened a new office in Jeddah in May 2026, positioning it as a hub for growth activities and professional training through its hairdressing academy footprint, supporting salon-linked portfolios, education-led sell-through, and professional-grade product ecosystems. Localized manufacturing capacity additions, including Henkel’s Riyadh beauty care facility producing Pert shampoos and conditioners, also help shorten replenishment cycles and improve responsiveness to local preferences, reducing reliance on long import lead times in markets where pricing pressure and gray-market activity distort traditional trade dynamics.

Recent Industry Developments

- May 2026: L'Oréal inaugurated a new office in Jeddah, strengthening its Saudi operating base and linking the site to professional training capacity through its L'Oréal Professionnel academy network. The move improves the company’s on-the-ground execution in a market where salon influence and premiumization are increasingly tied to brand education and certification.

- June 2025: Henkel Consumer Brands launched the Schwarzkopf Gliss hair care range across GCC markets with a Dubai-centered rollout. The regional debut expands Henkel’s premium and masstige shelf presence and highlights how influencer-led activations are accelerating awareness and trial in Gulf retail and e-commerce channels.

- July 2024: Henkel opened a beauty care production facility in Riyadh to manufacture Pert-branded products, including shampoos and conditioners. Local production supports faster servicing of Saudi demand and aligns supply with national localization priorities, while reducing exposure to cross-border logistics and import clearance frictions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers retail and professional sales of hair care products across the Middle East and Africa, measured in value terms. It includes everyday cleansing and care items, plus targeted products that support styling, coloring, and hair and scalp treatment.

Scope exclusions: We exclude salon services, hair tools and appliances, and non-hair personal care items that sit outside packaged hair care product sales.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Others

-

By Category

- Mass

- Premium

-

By Ingredient Type

- Synthetic

- Natural / Organic

-

By Distribution Channel

- Hypermarkets / Supermarkets

- Convenience and Grocery Stores

- Specialty Beauty Stores

- Pharmacies / Drug Stores

- Online Channels

- Others

-

By Geography

- Saudi Arabia

- United Arab Emirates

- Kuwait

- Qatar

- Oman

- Bahrain

- South Africa

- Nigeria

- Kenya

- Egypt

- Morocco

- Rest of Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us anchor the size of the consumer goods backdrop and align country-level demand signals before any modeling choices were locked. We referred to public sources such as national statistics offices in key MEA countries, customs and trade portals, World Bank indicators, and UN Comtrade series to understand import reliance and category momentum.

To keep assumptions practical, we also reviewed company annual reports, investor presentations, retailer communications, and association websites discussing beauty and personal care trends. A paid subscription focused on company financials and another on shipment-level trade flows were used selectively to cross-check revenue direction and trade mix for hair care categories. These sources are illustrative only, and many other references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to test what the desk research could not confirm cleanly, especially price tiers, channel split, and category substitution between basic care and treatment products. We spoke with manufacturers, distributors, large retailers, pharmacists, and salon-linked sellers across the Middle East and Africa so the model reflects local buying patterns and currency realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | |

| Mid tier: 58% | Functional/Unit leaders: 29% | |

| Smaller Players: 14% | Managers: 58% |

Market-Sizing & Forecasting

Sizing started from a top-down demand pool build that links hair care spend to population, urban mix, and beauty and personal care consumption signals across the covered countries, and then it is allocated into hair care based on observed category shares and channel weights. Where data gaps existed, the split was inferred using proxy indicators such as import intensity, modern retail penetration, and product availability across pharmacies and supermarkets.

To keep the totals realistic, the output was then corroborated with selective bottom-up checks like sampled average selling price by category multiplied by estimated volumes in key channels, followed by distributor and retailer sense checks on annual sell-through. The model uses practical inputs that can be refreshed each year, such as inflation-driven price movement, premiumization rate, e-commerce share shift, hair colorant adoption, and the mix between basic shampoo and conditioner versus treatment and hair loss products. Forecasts lean on scenario analysis, where macro conditions and pricing pressure are adjusted in line with expert feedback, and then reviewed country by country before consolidating the region.

Data Validation & Update Cycle

Validation is done through triangulation across country totals, category splits, and channel math so the final number matches more than one independent signal. If a country output moves too far from expected import trends, consumer spend indicators, or price progression, we recheck assumptions and reconnect with sources to understand what changed.

Before sign-off, the model and written insights go through a multi-step analyst review where variances are challenged and calculations are replayed for common failure points like double counting across channels. Reports are refreshed annually, and interim updates are triggered when material events occur, such as tax changes, sharp currency moves, or major channel disruptions. Right before delivery, a final scan is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Middle East and Africa Hair Care Market Market Size Compared Against Other Published Estimates

Published market sizes for MEA hair care often do not match because scope choices and year definitions are not always aligned. Differences also show up when one source uses a short forecast window and another uses a longer horizon where pricing and currency shifts compound.

In practice, the biggest gap drivers are what gets counted as hair care (for example, whether hair oils and hair loss treatments are included consistently), how retail versus salon-linked product sales are treated, and how prices are normalized across countries with different inflation paths. Another reason is currency handling, where the timing of FX conversion and the use of nominal versus adjusted pricing can move the final USD value. When the model is tied to country demand indicators and then checked against channel and category reality, the estimate stays traceable to repeatable inputs, which is the discipline applied here by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.91 B (2025) | |

| Trade Portal Summary A | USD 5.46 B (2025) | This estimate appears to use a different base definition and forecast frame, which can understate value when treatment and broader channel coverage are not fully reflected in the same way. |

| Regional Consultancy B | USD 13.49 B (2024) | The much higher figure likely reflects a wider basket and different year and currency assumptions, where adjacent beauty items and broader consumer splits can be rolled into hair care totals. |

The spread in published numbers is mainly explained by scope, year choice, and how pricing and FX are handled across different country conditions. By keeping the category basket consistent, validating channel splits with field feedback, and updating key price and currency assumptions on a clear cadence, the approach produces a balanced figure that can be rechecked and refreshed without guesswork.

Key Questions Answered in the Report

What is the current value of the Middle East and Africa hair care market?

The market is valued at USD 6.16 billion in 2026 and is projected to reach USD 7.55 billion by 2031.

Which country holds the largest share in regional hair care sales?

Saudi Arabia leads with 22.94% share of 2025 revenue.

Which product category is growing fastest across the region?

Hair styling products are advancing at a 5.07% CAGR through 2031.

How rapidly are online channels expanding for hair-care purchases?

E-commerce sales are increasing at a 5.68% CAGR, driven by government digital-trade strategies.

Page last updated on: