Microbial Fermentation Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

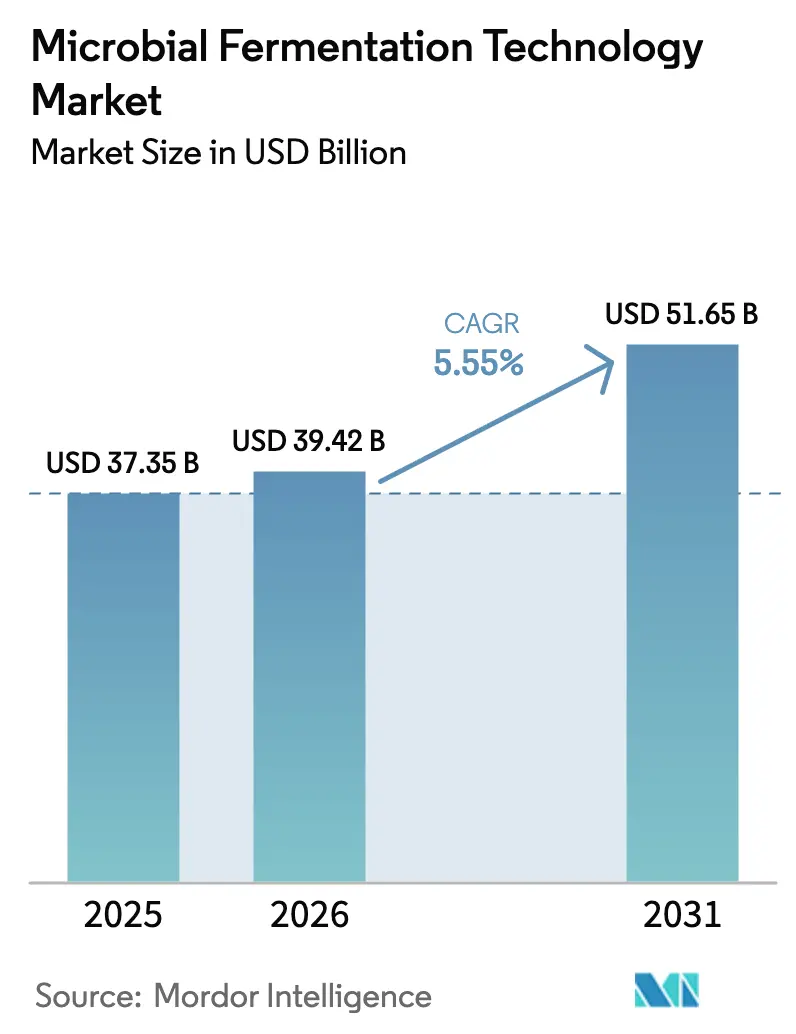

| Market Size (2026) | USD 39.42 Billion |

| Market Size (2031) | USD 51.65 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microbial Fermentation Technology Market Analysis by Mordor Intelligence

The microbial fermentation technology market size is expected to grow from USD 37.35 billion in 2025 to USD 39.42 billion in 2026 and is forecast to reach USD 51.65 billion by 2031 at 5.55% CAGR over 2026-2031. Rising demand for greener production pathways, government incentives for domestic biomanufacturing, and record levels of venture investment are aligning to expand capacity across pharmaceuticals, food proteins, and sustainable chemicals. Intensifying interest in precision fermentation, cell-free enzymatic platforms, and engineered microbial consortia is reshaping competitive strategies, while advances in AI-based strain engineering shorten development timelines and lower risk. Continuous processing and modular facilities are unlocking new operating models that cut contamination events and reduce capital intensity. Together, these factors are sustaining balanced, mid-single-digit growth even as legacy antibiotic revenues plateau.

Key Report Takeaways

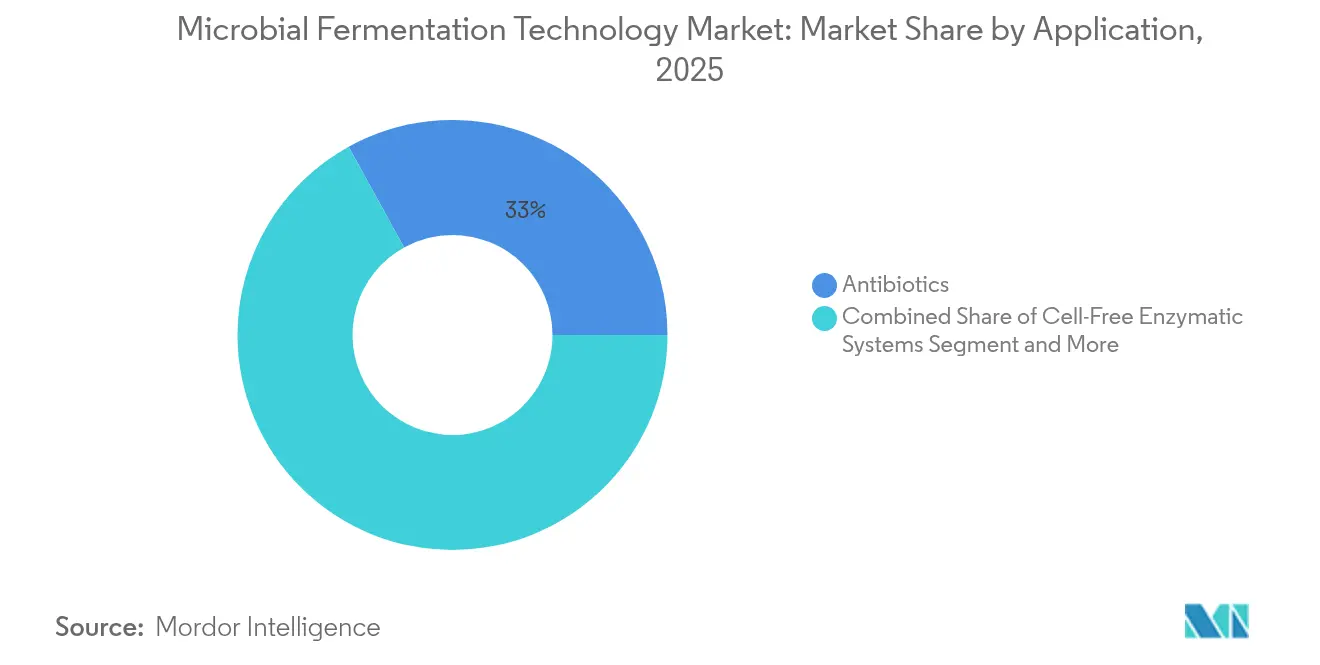

- By application, antibiotics held the largest 33.02% microbial fermentation technology market share in 2025, whereas cell-free enzymatic systems are forecast to expand at a 11.78% CAGR to 2031.

- By microorganism type, bacteria led with 46.41% share of the microbial fermentation technology market in 2025, while engineered synthetic consortia are poised for the fastest 13.1% CAGR through 2031.

- By mode of fermentation, fed-batch processes commanded 55.05% share of the microbial fermentation technology market in 2025; continuous systems show the highest 12.31% CAGR outlook.

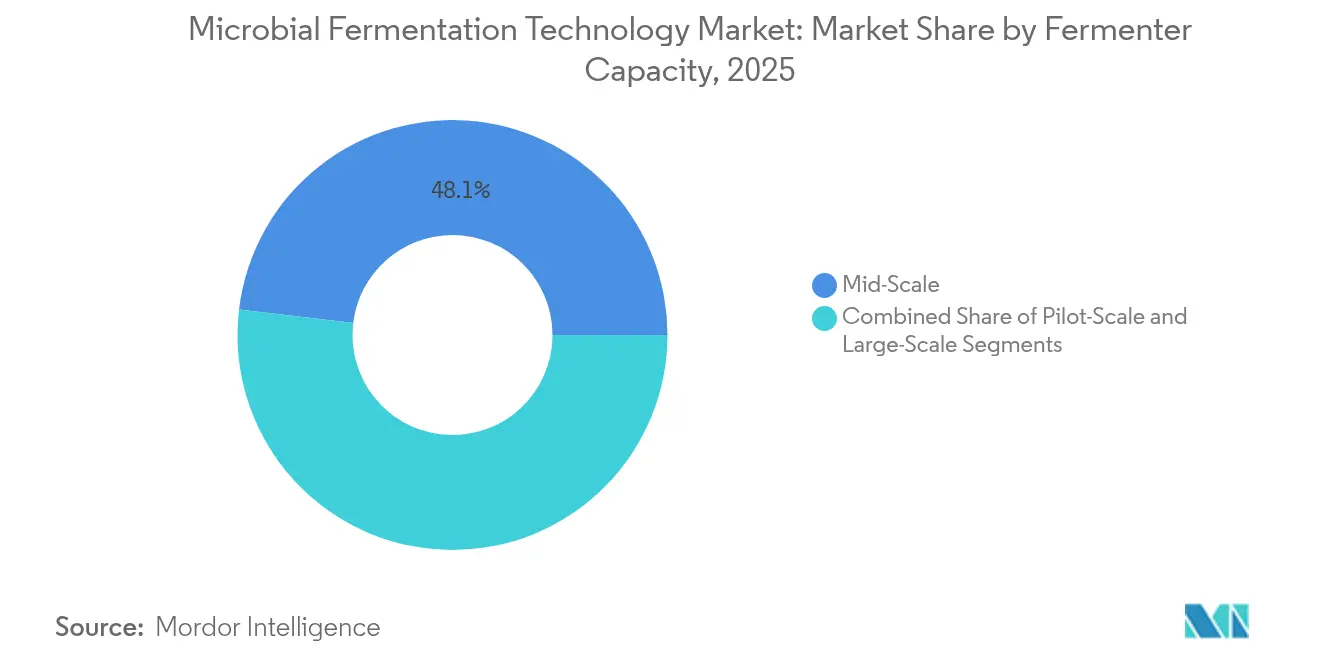

- By fermenter capacity, mid-scale vessels (1,000-20,000 L) captured 48.10% revenue in 2025, yet pilot-scale systems are growing at 12.18% CAGR.

- By end user, biopharmaceutical companies controlled 41.90% of the market size in 2025; food & beverage manufacturers post the fastest 12.89% CAGR through 2031.

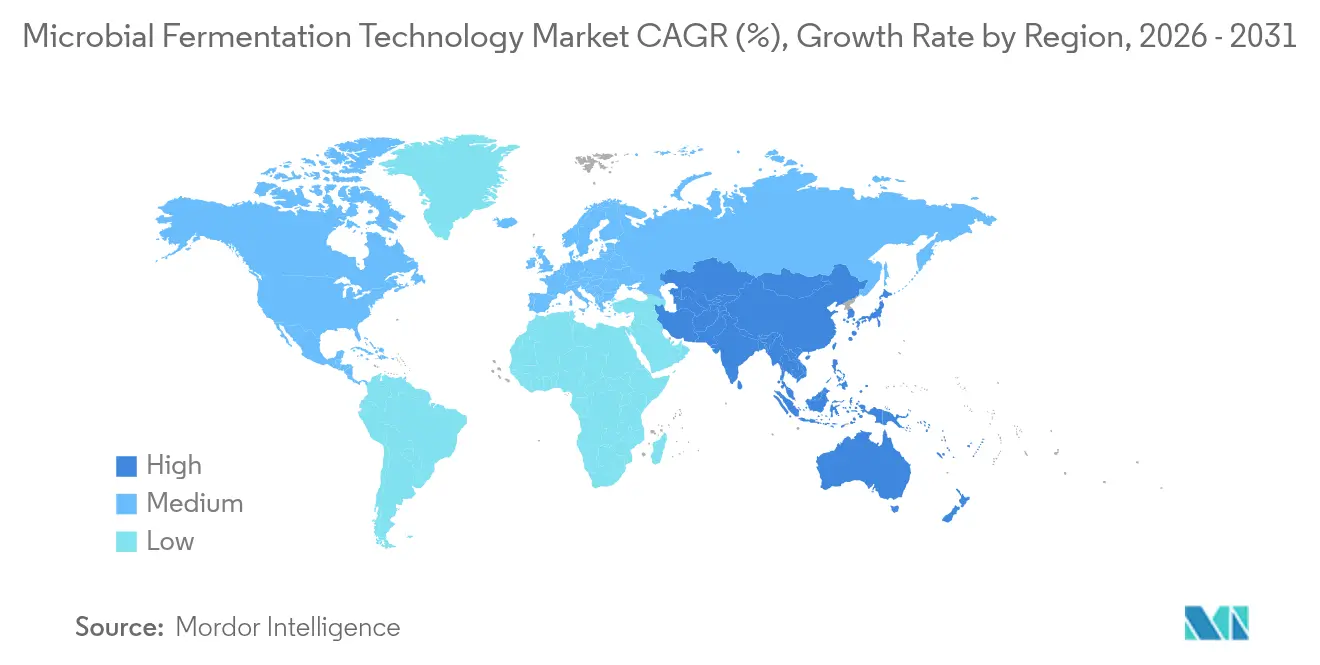

- By geography, North America accounted for 38.05% of the microbial fermentation technology market in 2025, whereas Asia-Pacific is projected to register a 12.12% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microbial Fermentation Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Microbial Capacity For RNA Vaccines | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Growing Demand For Recombinant Enzymes In Sustainable Chemicals | +1.8% | Global, strongest in APAC and North America | Long term (≥ 4 years) |

| Government Incentives For Biomanufacturing Resilience | +0.9% | North America, EU, with spillover to allied nations | Short term (≤ 2 years) |

| Rapid Adoption Of Continuous Fermentation Skid Systems | +1.1% | Global, led by developed markets | Medium term (2-4 years) |

| AI-Based Strain-Engineering Success Rates | +1.3% | Global, concentrated in tech-advanced regions | Long term (≥ 4 years) |

| Venture Funding Surge For Precision Fermentation Food Proteins | +0.8% | Global, with emphasis on North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand For Recombinant Enzymes In Sustainable Chemicals

Recombinant enzymes are displacing petrochemical catalysts as producers target lower emissions and tighter process specificity. Solugen’s USD 120 million Minnesota facility illustrates the shift, slashing 18 million kg of CO₂ each year while supplying low-carbon organic acids. High-throughput screening and AI-guided protein design compress discovery cycles from months to weeks. Emerging immobilization methods such as magnetic cross-linked cell aggregates extend enzyme lifespan, curbing consumable cost and waste. Expanding circular-economy policies in Europe and selective-waste mandates in China are amplifying demand for bio-based plastics, biofuels, and specialty chemicals generated with recombinant enzymes. This trajectory positions enzyme fermentation as a foundational pillar for large-scale decarbonization.

AI-Based Strain-Engineering Success Rates

Artificial intelligence now predicts gene edits that maximize pathway flux, cutting wet-lab iterations by up to 70% and boosting the probability of reaching commercial titers. The TUNEYALI biosensor toolkit enables real-time metabolic feedback during fermentation, shortening design–build–test–learn cycles. Ginkgo Bioworks and Novo Nordisk have extended their collaboration to deploy automated strain-engineering platforms in metabolic disease drug R&D. These integrated workflows feed directly into pilot-scale fermenters, accelerating scale-up while reducing uncertainty. As AI models train on expanding multi-omics datasets, predictive accuracy improves, enabling the rapid construction of synthetic consortia capable of complex, multistep conversions.

Government Incentives For Biomanufacturing Resilience

National security objectives are channeling unprecedented public funds into domestic microbial capacity. The US Department of Defense earmarked USD 2 billion for biotechnology under DARPA’s Biological Technologies Office[1]DARPA, “DARPA Announces $2 Billion Investment in Biotechnology Research,” darpa.mil. Simultaneously, the National Biotechnology and Biomanufacturing Initiative offers tax credits and grants for retrofitting legacy plants. China’s USD 4.17 billion synthetic biology strategy intensifies global competition, underwriting infrastructure for pharmaceuticals and industrial biotech. Harmonized regulatory fast-tracks for precision-fermented foods and cell-free therapeutics in the United States and Europe reduce market entry barriers. Preference for local supply bolsters order visibility for contract development and manufacturing organizations (CDMOs).

Rapid Adoption Of Continuous Fermentation Skid Systems

To cut downtime and contamination risk, producers are deploying modular continuous systems that integrate real-time analytics and closed-transfer operations. Skid-mounted platforms lower capital outlay and simplify line relocation, aligning with distributed manufacturing strategies in both pharmaceuticals and alternative proteins. Continuous upstream with batch downstream hybrids deliver higher volumetric productivity without disrupting established purification sequences. AI-enabled control loops stabilize residence time and nutrient feed, elevating batch-to-batch consistency. As single-use technology scales, disposable flow-paths support multiproduct flexibility while limiting clean-in-place expenses, accelerating adoption across developed markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strain Genetic-Stability Breakdown At High Cell Density | -0.7% | Global, particularly affecting large-scale operations | Medium term (2-4 years) |

| Scarcity Of Single-Use Reactors ≥5,000 L | -0.5% | Global, with acute shortages in APAC | Short term (≤ 2 years) |

| Upstream–Downstream Scale-Mismatch Bottlenecks | -0.4% | Global, most severe in emerging markets | Medium term (2-4 years) |

| Limited Global cGMP Talent Pool | -0.3% | Global, with critical gaps in APAC and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strain Genetic-Stability Breakdown At High Cell Density

As titers climb, metabolic stress accelerates mutation rates, triggering plasmid loss that can erode yields by 15-30% in industrial lines. Novel genetic circuits promise improved stability but often trade productivity for robustness. Early-warning analytics monitor copy-number variance and metabolite drift, yet the industry still calibrates the optimal balance between density and durability. Multi-batch campaigns and extended fermentations present cumulative risks, complicating cost calculations for high-value biologics. Reinforced selection mechanisms and synthetic auxotrophies are under evaluation, though commercial deployment remains limited.

Scarcity Of Single-Use Reactors ≥5,000 L

Demand for large-format disposable bioreactors surged alongside mRNA vaccines and precision fermentation proteins, overwhelming the specialized supply base. Lead times beyond 18 months force manufacturers to lock in orders early or revert to stainless steel, undermining the agility advantage of single-use systems. Raw material shortages for multilayer films and embedded sensors compound the challenge. Contract negotiations increasingly include volume guarantees, but smaller entrants struggle to secure allocation. Some producers deploy parallel 2,000 L trains to replicate 10,000 L capacity, adding operational complexity yet preserving contamination control benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cell-Free Systems Drive Innovation

Antibiotics posted a commanding 33.02% revenue in 2025, but cell-free enzymatic platforms are projected for the highest 11.78% CAGR, underscoring a pivot toward next-generation production that bypasses cellular constraints. Monoclonal antibodies and recombinant proteins still anchor revenue flows due to existing infrastructure and reimbursement pathways. Enhanced mRNA production lanes, initialized during the pandemic, now broaden vaccine pipelines. The microbial fermentation technology market benefits from the synergy between AI-assisted design and rapid prototyping offered by cell-free reactions, enabling on-demand therapeutics validated in the Journal of Biological Engineering’s programmable vesicle systems.

Cell-free synthesis also accelerates small-molecule diversification, allowing faster iteration on enzyme cascades critical for novel specialty chemicals. The modularity of reactions reduces facility retrofits, positioning contract manufacturers to offer multipurpose suites. The microbial fermentation technology market size for vaccines and enzymes is forecast to widen as governments fund pandemic preparedness stockpiles. Biosimilars face intensifying competition, yet cell-free transcriptomic approaches promise cost reductions that could restore margins. Collectively, application diversification stabilizes revenue streams even amid antibiotic commoditization.

By Microorganism Type: Synthetic Consortia Emerge

Bacteria supplied 46.41% of 2025 revenue owing to decades of optimization, but engineered synthetic consortia will expand at 13.1% CAGR, reflecting breakthroughs in division-of-labor metabolic engineering. Yeast keeps strong traction in glycosylated biologics, and filamentous fungi retain niche dominance in complex enzyme cocktails. Algae and cyanobacteria gain attention for photosynthetic chemical routes that bypass sugar feedstocks, while acetogenic bacteria valorize C1 gases into fuels.

Synthetic consortia enable sequential reactions across specialized strains, raising total pathway efficiency and tolerance thresholds. The microbial fermentation technology market size for these advanced communities is expected to grow as regulatory agencies clarify approval pathways. Discoveries in quorum-sensing control and orthogonal auxotrophies mitigate cross-contamination risk, enhancing commercial confidence. Coupling consortia with continuous processing may unlock sizeable cost reductions, especially in multi-step natural-product synthesis.

By Mode of Fermentation: Continuous Gains Momentum

Fed-batch processes controlled 55.05% of revenue in 2025 owing to entrenched pharmaceutical standards, yet continuous systems are predicted to climb at 12.31% CAGR as real-time analytics mature. Continuous reactors reduce downtime, improve footprint efficiency, and lower media use, making them attractive for commodity biomaterials. Hybrid schemes that integrate continuous upstream with batch downstream give operators the comfort of established purification requirements while capturing upstream intensification gains.

The microbial fermentation technology market appreciates the cost benefits of smaller vessel volumes achieving comparable productivity under perfusion. AI-driven adaptive control stabilizes residence time and metabolite levels, limiting contamination risk cited by Nature Catalysis in synthetic methylotroph platforms. Equipment vendors now offer skid-mounted modules suitable for rapid deployment and relocation, encouraging adoption among emerging-market producers where capital budgets are constrained.

By Fermenter Capacity: Pilot-Scale Flexibility

Vessels in the 1,000-20,000 L range delivered 48.10% revenue during 2025, the practical sweet spot for blockbuster biologics and precision proteins. Pilot-scale units below 1,000 L register the strongest 12.18% CAGR as companies embrace decentralized production. Lonza’s acquisition of the Vacaville site and concurrent modular retrofits illustrate this shift toward scalable sub-20,000 L suites.

Process-intensification advances boost titers, making small systems viable for commercial volumes. Single-use assemblies in pilot formats cut cleaning validation and support multi-product schedules, suited to startups scaling novel food proteins. The microbial fermentation technology market thrives on incremental capacity that matches uncertain demand curves, avoiding stranded mega-plants. Large-scale stainless systems remain essential for high-volume antibiotics but face competition from intensified midsize lines.

By End User: Food Manufacturers Accelerate Adoption

Biopharma firms captured 41.90% of 2025 spending, backed by entrenched cGMP expertise. Food and beverage producers, however, are forecast for the fastest 12.89% CAGR as precision fermentation replaces animal-derived proteins. Perfect Day’s whey warrants and Nestlé’s animal-free dairy pilot reflect mainstream momentum. CDMOs secure upside by providing capacity without fixed commitments, and CROs expand service lines in process characterization.

Academic centers and consortia support technology transfer to industry, exemplified by university-spinout alliances with contract producers for alternative lipids. The microbial fermentation technology industry sees cross-sector talent migration as food technologists converge with bioprocess engineers, harmonizing safety and labeling regulations. These collaborations shorten commercialization timelines, especially where consumer familiarity with fermentation accelerates acceptance.

Geography Analysis

North America led with 38.05% revenue in 2025 driven by USD 2 billion DARPA funding, a suite of tax incentives, and multiple private capacity additions. Fujifilm’s USD 1.6 billion expansion in North Carolina and Novo Nordisk’s USD 4.1 billion program anchor new facilities, while the BioSecure Act channels government contracts to domestic suppliers. Lonza’s USD 1.2 billion Vacaville acquisition and Agilent’s BIOVECTRA deal underscore consolidation that boosts regional expertise. A robust venture ecosystem funds AI-enabled startups, reinforcing the knowledge loop between academia and industry.

Asia-Pacific is forecast for the highest 12.12% CAGR, propelled by China’s USD 4.17 billion synthetic biology plan and India’s alignment with US supply-chain security requirements. WuXi Biologics continues regional capacity additions, while Singapore’s economic-development agency funds pilot plants for precision-fermentation milk proteins. South Korea invests in marine algae programs that tap offshore CO₂-to-chemical routes. Local governments streamline permitting to compete for foreign direct investment, creating fertile ground for small and midsize firms.

Europe remains a mature stronghold emphasizing sustainability. Germany’s bioeconomy framework incentivizes microbial production of biopolymers, and the Netherlands accelerates precision-fermentation cheese ventures. The United Kingdom leverages its synthetic biology clusters to commercialize cell-free therapeutics and advanced enzyme platforms, supported by dedicated regulatory guidance. The microbial fermentation technology market benefits from consistent quality standards and export-oriented CDMOs.

Middle East and Africa represent nascent but strategic growth vectors. Saudi Arabia’s NEOM Investment Fund anchors a precision-fermentation complex operated by Liberation Labs, targeting dairy and egg protein self-sufficiency. The region’s abundant renewable-energy resources enable competitive green-hydrogen-based feedstocks for C1 fermentations. Governments rush to establish biosafety regulations and workforce training to attract global partners.

Competitive Landscape

The microbial fermentation technology market balances established pharmaceutical giants with agile precision-fermentation entrants. Lonza, Fujifilm, and Novo Nordisk invest billions in facility expansions to secure large-volume biologics and mRNA capacity, exemplifying scale-driven defense strategies. Mid-tier CDMOs diversify into cell-free platforms and continuous production to differentiate service portfolios, while smaller innovators hone proprietary microbes for high-margin niches.

AI-centric platforms such as Ginkgo Bioworks automate strain construction, positioning themselves as design houses that license IP or partner for manufacturing. Perfect Day, Standing Ovation, and Liberation Labs extend food-protein pipelines through contract manufacturing alliances, blending branding strengths with operational depth. The microbial fermentation technology market witnesses cross-sector partnerships: BASF with synthetic-biology startups for sustainable pigments and pharma majors licensing enzyme pathways from industrial biotech firms.

Patent filings covering data-driven bioprocess optimization grew sharply in 2024, reflecting a race to secure algorithmic methods that tune fermentation on the fly. Talent scarcity remains a gating factor; leading firms launch internal training academies and collaborate with universities to widen cGMP-ready workforce pools. Supply-chain resilience influences strategy: several companies diversify resin and film vendors to mitigate single-use component constraints. As capacity scales, environmental-impact metrics emerge as bidding criteria for CDMO contracts, rewarding operators who can document low-carbon footprints.

Microbial Fermentation Technology Industry Leaders

Lonza Group AG

Novozymes

AbbVie Inc

Thermo Fisher Scientific

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Standing Ovation partnered with Tetra Pak to boost industrial production of alternative caseins via precision fermentation, targeting enhanced scalability and cost efficiency in protein manufacturing.

- April 2025: Liberation Labs secured a partnership with Saudi Arabia's NEOM Investment Fund to build a precision-fermentation facility, addressing regional food-security needs through local dairy and egg protein output.

Global Microbial Fermentation Technology Market Report Scope

As per the scope of the report, microbial fermentation technology refers to the use of microorganisms to convert substrates into valuable products through biochemical processes, typically in anaerobic conditions. This technology plays a crucial role in various industries, including pharmaceuticals and biotechnology.

The microbial fermentation technology is segmented by application, end user, and geography. By application, the market is segmented into antibiotics, monoclonal antibodies, recombinant proteins, biosimilars, vaccines, enzymes, small molecules, and other applications (hormones and vitamins, among others). By end user, the market is segmented into bio-pharmaceutical companies, contract research organizations (CROs), CMOs and CDMOs, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in value terms (USD) for the above segments.

| Antibiotics |

| Monoclonal Antibodies |

| Recombinant Proteins |

| Biosimilars |

| Vaccines |

| Enzymes |

| Small Molecules |

| Cell-Free Enzymatic Systems |

| Other Applications |

| Bacteria |

| Yeast |

| Filamentous Fungi |

| Algae & Cyanobacteria |

| Engineered Synthetic Consortia |

| Batch |

| Fed-Batch |

| Continuous |

| Pilot-Scale (<1,000 L) |

| Mid-Scale (1,000-20,000 L) |

| Large-Scale (>20,000 L) |

| Biopharmaceutical Companies |

| Contract Manufacturing Organizations (CMOs/CDMOs) |

| Contract Research Organizations (CROs) |

| Academic & Research Institutes |

| Food & Beverage Manufacturers |

| Industrial Biotechnology Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Antibiotics | |

| Monoclonal Antibodies | ||

| Recombinant Proteins | ||

| Biosimilars | ||

| Vaccines | ||

| Enzymes | ||

| Small Molecules | ||

| Cell-Free Enzymatic Systems | ||

| Other Applications | ||

| By Microorganism Type | Bacteria | |

| Yeast | ||

| Filamentous Fungi | ||

| Algae & Cyanobacteria | ||

| Engineered Synthetic Consortia | ||

| By Mode of Fermentation | Batch | |

| Fed-Batch | ||

| Continuous | ||

| By Fermenter Capacity | Pilot-Scale (<1,000 L) | |

| Mid-Scale (1,000-20,000 L) | ||

| Large-Scale (>20,000 L) | ||

| By End User | Biopharmaceutical Companies | |

| Contract Manufacturing Organizations (CMOs/CDMOs) | ||

| Contract Research Organizations (CROs) | ||

| Academic & Research Institutes | ||

| Food & Beverage Manufacturers | ||

| Industrial Biotechnology Firms | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the microbial fermentation technology market?

The microbial fermentation technology market size stands at USD 39.42 billion in 2026 and is forecast to reach USD 51.65 billion by 2031.

Which application is growing fastest within microbial fermentation?

Cell-free enzymatic systems are projected to grow at a 11.78% CAGR through 2031, reflecting heightened interest in production without cellular constraints.

Why are engineered synthetic consortia important?

They distribute metabolic tasks across multiple strains, delivering higher yields and enabling complex bioconversions, supporting a 13.1% CAGR for this microorganism segment.

How are government policies influencing market growth?

Programs such as the US National Biotechnology and Biomanufacturing Initiative and China’s synthetic biology plan provide funding and regulatory support, accelerating capacity expansion.

What limits faster capacity deployment today?

Scarcity of large single-use bioreactors and challenges maintaining genetic stability at high cell densities restrain rapid scaling, trimming the overall growth rate by roughly 1.2 percentage points.

Page last updated on: