Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

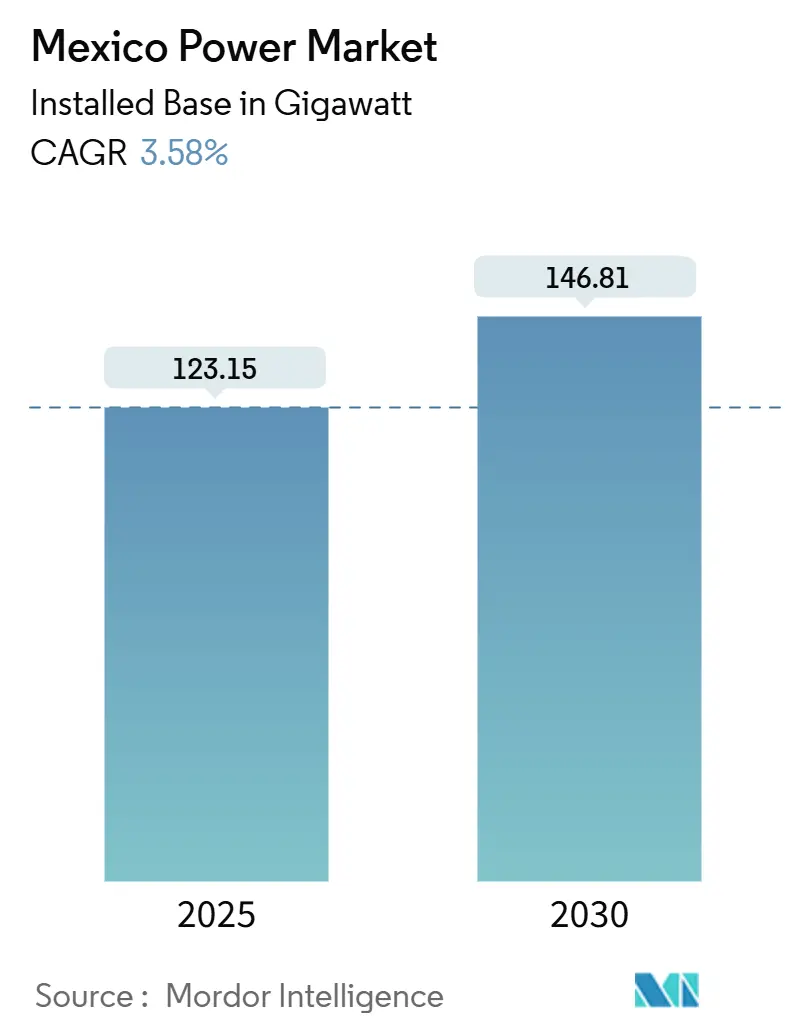

| Market Volume (2025) | 123.15 gigawatt |

| Market Volume (2030) | 146.81 gigawatt |

| Growth Rate (2025 - 2030) | 3.58% CAGR |

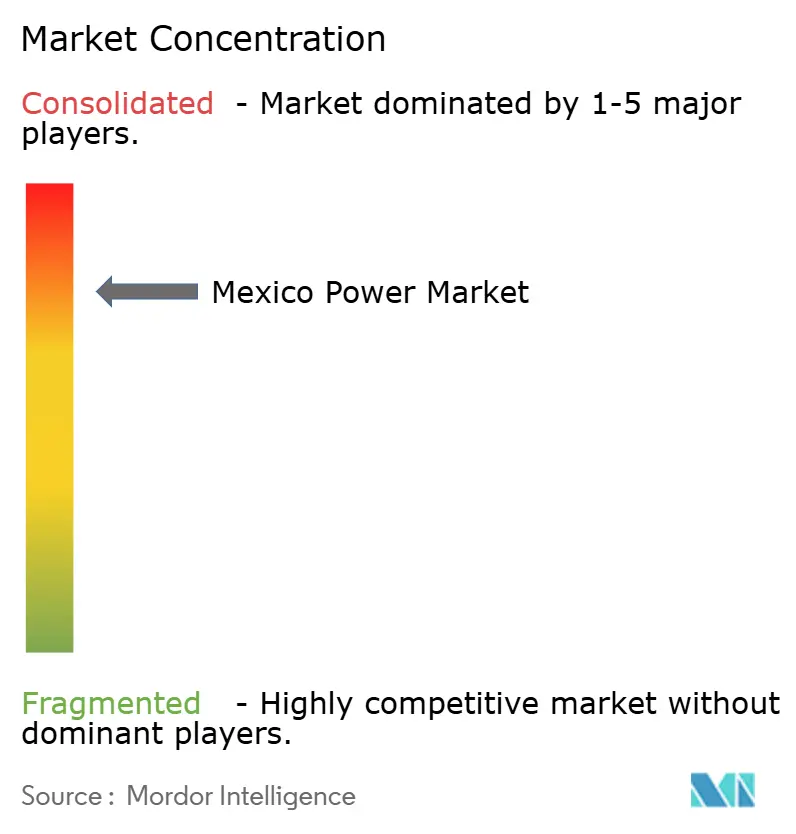

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Power Market Analysis by Mordor Intelligence

The Mexico Power Market size in terms of installed base is expected to grow from 123.15 gigawatt in 2025 to 146.81 gigawatt by 2030, at a CAGR of 3.58% during the forecast period (2025-2030).

Sustained nearshoring inflows, the Sheinbaum administration’s USD 23.4 billion investment plan, and a 27 GW capacity addition pledge position the Mexican power market as the region’s most critical growth platform. Natural gas–fired plants continue to anchor baseload reliability, yet a 35% clean-energy mandate extended to 2030 channels capital toward solar and wind parks that already exceed 10.6 GW capacity. High-voltage transmission upgrades, cross-border ties with ERCOT and WECC, and green bond financing accelerate grid modernization, while industrial consumers increasingly procure behind-the-meter supply to hedge reliability risk. However, policy shifts granting the Comisión Federal de Electricidad (CFE) at least 54% generation control and the dissolution of independent regulators create a more centralized governance model, which raises questions about permitting transparency.[1]Comisión Federal de Electricidad, “Informe Anual 2025,” cfe.mx

Key Report Takeaways

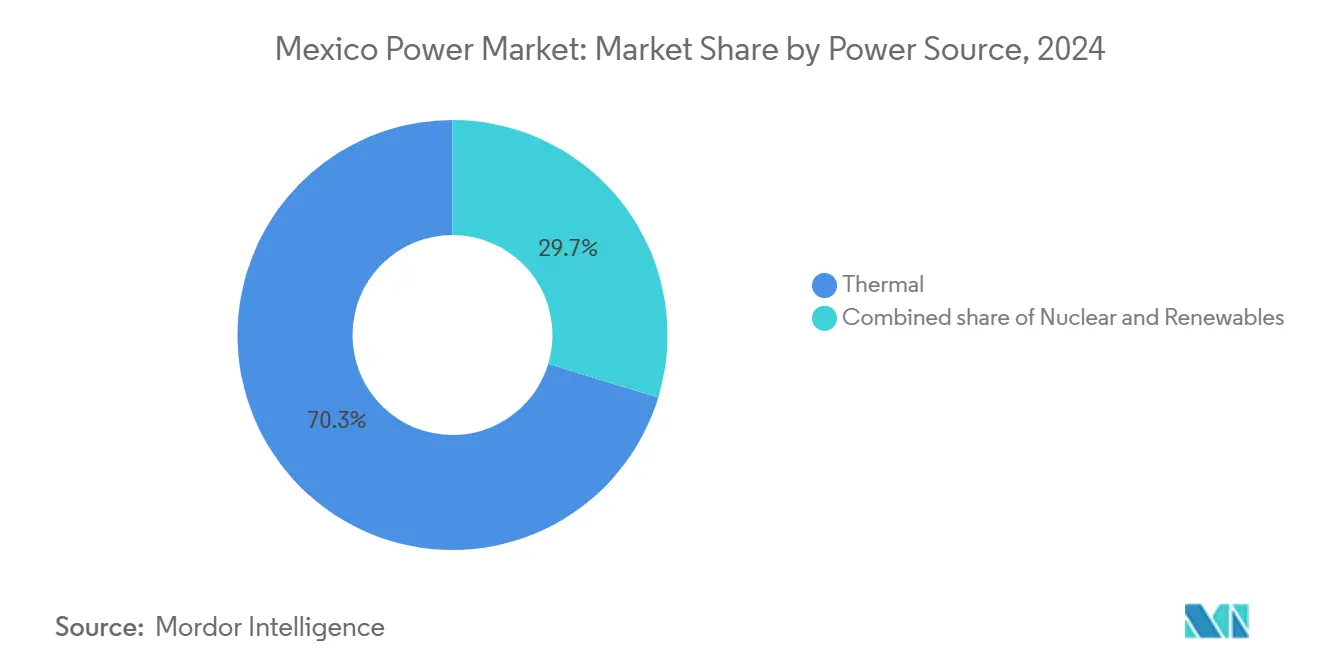

- By power source, thermal plants held 70.3% of the Mexico power market share in 2024; renewables are projected to expand at a 10.3% CAGR through 2030.

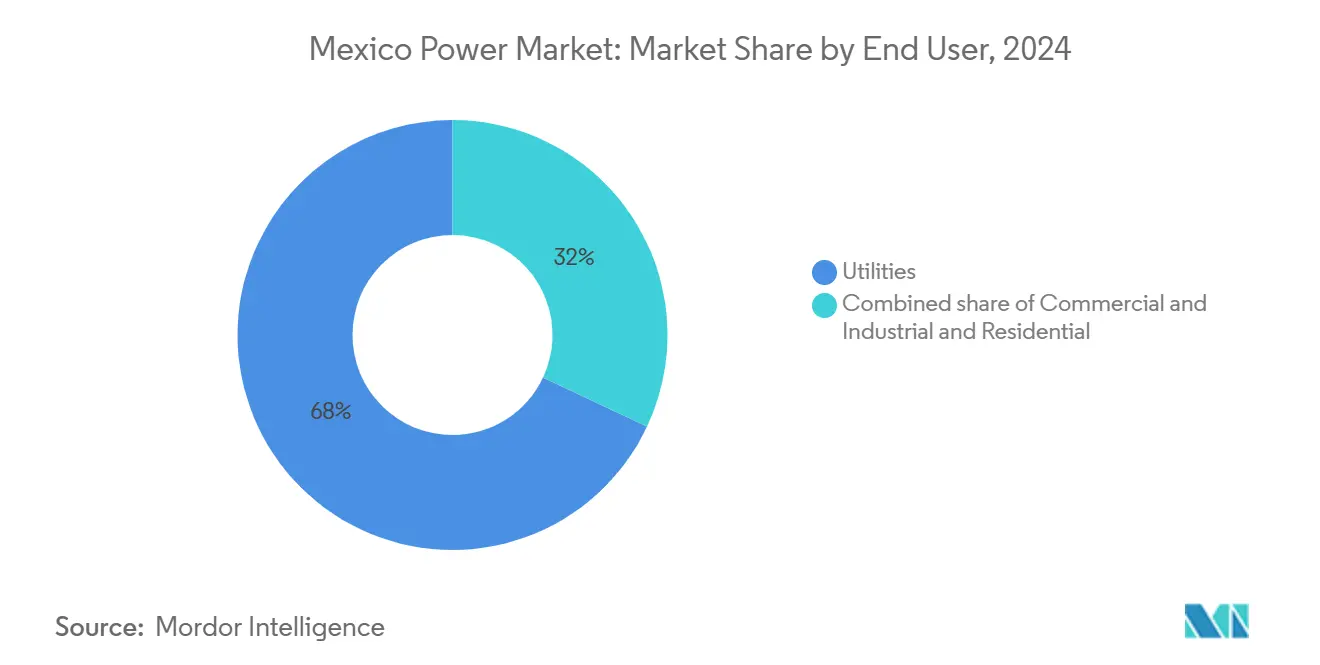

- By end user, industrial facilities accounted for 68% of the Mexican power market size in 2024, whereas commercial and service demand recorded the fastest rise at a 7.5% CAGR.

- CFE, Iberdrola, Enel, Acciona, and Sempra Infrastructure collectively control a major share of installed generation, underscoring a moderately concentrated arena.

Mexico Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring-led industrial load growth | +1.8% | Northern border states, Bajío region | Medium term (2-4 years) |

| 35% renewables target by 2024 extended to 2030 | +1.2% | National, concentrated in northern states | Long term (≥ 4 years) |

| Surge in utility-scale solar & on-site PV PPAs | +0.9% | Northern Mexico, Sonora, Chihuahua | Medium term (2-4 years) |

| Cross-border export potential to ERCOT & WECC | +0.6% | Border regions, Baja California, Tamaulipas | Long term (≥ 4 years) |

| Data-center & AI compute clusters (≥500 MW pipeline) | +0.4% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Grid-modernisation funds via green bonds (2025-2028) | +0.3% | National transmission network | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-shoring-led Industrial Load Growth

Rapid relocation of manufacturing from Asia is expected to boost electricity demand by 30% through 2030, driven by USMCA tariff advantages and proximity to US consumer markets. Nuevo León, Guanajuato, and Chihuahua register the steepest increases in load, prompting firms to purchase dedicated generation assets to secure supply continuity. Industrial power tariffs remain competitive relative to Texas, sustaining investment momentum despite higher capacity-reserve charges. CFE’s pipeline of 15 new combined-cycle plants will add 10.1 GW to meet nearshoring demand, equivalent to 810 MMcf/d of incremental gas burn. Grid planners nevertheless caution that sub-transmission backbones require parallel reinforcement to prevent regional bottlenecks.

35 % renewables target by 2024 extended to 2030

The federal clean-energy goal was pragmatically shifted from 2024 to 2030, offering developers a longer runway to close financing and interconnection milestones. Solar installations reached 10.67 GW in 2024 and are forecast to cross 27 GW by 2030, representing a 14.5% annual increase that keeps México among Latin America's top solar growth markets. Wind additions, led by Sempra Infrastructure's 320 MW Cimarron project, reinforce México's power market decarbonization while enhancing export headroom into California and Arizona grids.[2]Sempra Infrastructure, “Cimarron Wind Project Overview,” semprainfrastructure.com The Plan México framework allocates 6.4 GW of new renewables under the 54%-46% public-private split, confirming the state utility's central role as offtaker.

Surge in Utility-Scale Solar and On-Site PV PPAs

Corporate demand for traceable, clean electricity accelerates multi-gigawatt PPA signings, with industrial groups locking in 15- to 20-year solar offtakes to hedge against tariff volatility. Distributed generation surpassed 2,015 MW in 2024, aided by streamlined interconnection rules that now require less than 30 days for systems below 500 kW. Long-duration battery storage pilots emerge alongside PV arrays to comply with Grid Code 2.0 power-quality thresholds. International suppliers, such as Sungrow, partner with local developers to bundle inverters, storage, and digital monitoring, thereby lowering the levelized cost of electricity and enhancing Mexico's power market competitiveness.

Cross-Border Export Potential to ERCOT & WECC

Existing interties with California ISO and ERCOT currently trade marginal volumes, yet surplus solar and wind forecasts suggest up to 4 TWh of annual exports by 2030. Sempra’s high-voltage corridor linking Baja California to San Diego exemplifies how merchant projects can capitalize on production during peak California pricing. Coordinated planning between CENACE and US system operators harmonizes reserve-sharing protocols, though true scale-up hinges on incremental 400-kV pathways across Sonora and Tamaulipas. The export window also creates arbitrage that encourages hybrid gas-and-renewables dispatch, smoothing variability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Policy shifts curbing private-sector permits | -1.1% | National, affecting independent power producers | Short term (≤ 2 years) |

| Transmission congestion & curtailment on renewables | -0.8% | Northern states, renewable-rich regions | Medium term (2-4 years) |

| Water-stress constraints on thermal / hydro plants | -0.6% | Central and northern Mexico | Long term (≥ 4 years) |

| Cyber-security & AI-regulation gaps for smart grids | -0.3% | Urban centers, critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Policy Shifts Curbing Private-Sector Permits

Constitutional reform enacted in March 2025 dissolved the autonomous Energy Regulatory Commission and transferred oversight to the National Energy Commission within the Ministry of Energy. The new framework mandates that CFE retain a majority stake in generation, effectively capping private participation at 46% and subjecting new plants to heightened social-impact screening. International developers report that permit timelines are doubling, while banks apply higher risk premiums, inflating the weighted average cost of capital by up to 200 basis points. Industrial offtakers with signed PPAs confront uncertainty over dispatch priority, causing some to renegotiate tariffs or delay construction.

Transmission Congestion and Renewable Curtailment

Wind and solar hubs in Sonora, Chihuahua, and Tamaulipas routinely face curtailment rates exceeding 8% of their potential output during seasonal peaks, reflecting the lag between the build-out of generation and the reinforcement of transmission lines. CENACE’s suspension of emergency alerts complicates visibility into real-time bottlenecks, prompting developers to oversize projects or co-locate storage to secure deliverability. CFE’s USD 7.5 billion upgrade plan allocates 4,038 km of new 400 kV lines; however, the phased commissioning stretches over five years, prolonging the constraints. Limited export capacity further amplifies local congestion, prompting capital to shift to regions with spare thermal grid hosting capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Thermal Dominance Amid Renewable Acceleration

Renewables are the fastest-growing segment of the Mexican power market, advancing at a 10.3% CAGR to 2030. Solar PV already totals 10.67 GW and is projected to surpass 27 GW by 2030, keeping Mexico among Latin America’s most dynamic solar markets. Wind additions are also rising, led by Sempra Infrastructure’s 320 MW Cimarron farm backed by a 20-year PPA that signals deep market confidence. Plan México earmarks more than 6,400 MW of new clean capacity under a 54-46 public-private split that still grants CFE strategic control. Hydropower growth is limited by water stress, yet geothermal plants provide a steady baseload, and biomass-to-energy projects in farm belts extend electricity access to underserved communities.

Thermal sources retained 70.3% of the México power market share in 2024, underscoring continuing reliance on natural-gas infrastructure for grid stability. United States pipeline imports averaged 6.4 Bcf/d in December 2024, and the administration’s plan for 15 new combined-cycle plants will add 10.1 GW by 2030. Oil- and diesel-fired units remain critical in remote zones and during extreme-weather contingencies, while nuclear output stays flat as current policy favors renewables and gas flexibility. Coal capacity is edging lower, and emerging technologies—exemplified by Wärtsilä’s launch of a 100% hydrogen-ready engine plant—offer long-term decarbonization options.

By End User: Industrial Sector Drives Commercial Growth

Utilities retained 68% of the Mexico power market share in 2024, underscoring Comisión Federal de Electricidad’s (CFE) role as the principal off-taker and generator within a framework that reserves 54% of national capacity for the state. The segment’s dominance rests on long-term power-purchase agreements with independent producers, wholesale spot transactions, and emerging cross-border sales that optimize regional dispatch. In parallel, the combined commercial and industrial customer base is expanding at a 7.5% CAGR through 2030, buoyed by nearshoring capital inflows and hyperscale data center pipelines that demand round-the-clock, high-quality power. Automotive assembly plants, electronics fabs, and chemical complexes are increasingly buying or building dedicated plants to hedge reliability risk. Grupo Bachoco’s 190-system distributed-generation rollout across 19 states illustrates this self-supply shift in Mexico.

Commercial services, from shopping malls to hospitality chains, deploy rooftop solar and energy-efficiency retrofits to mitigate rising tariffs, increasing distributed-generation capacity to 2,015 MW, and expanding the Mexico power market size for behind-the-meter assets. Telecommunications upgrades that enable 5G and nationwide fiber backhaul lift electricity intensity, while steel mills and aluminum smelters exploit Mexico’s gas-linked pricing advantage for export-oriented output. Residential demand advances steadily through CFE’s 48.8 million-meter footprint, equal to 99.6% population coverage, and benefits from net-metering incentives that shorten rooftop PV paybacks. Public users include government offices, street lighting, and flagship electrification works such as the Mayan Train, a MXN 6.59 billion project projected to create 2,100 direct jobs and amplify regional load. The evolving policy mix, therefore, channels private capital into joint ventures and long-term contracts that align commercial opportunity with the utility’s strategic oversight, reinforcing CFE’s central position while accelerating low-carbon growth across end-user classes.

Geography Analysis

Northern border states, Sonora, Chihuahua, Tamaulipas, and Baja California, capture the lion’s share of renewable and industrial build-outs due to superior solar irradiation, steady winds, and direct ties to Arizona, Texas, and California. These states account for 58% of incremental capacity additions in 2024 and will likely maintain a 6.3% CAGR through 2030. Sonora hosts Iberdrola’s 137 MW Hermosillo PV park, generating 175 GWh annually, while Baja California leverages Sempra’s high-voltage corridor for export arbitrage.[3]IBERDROLA Corporativa, “Hermosillo PV Plant Commissioning,” iberdrola.com

Central Mexico, anchored by Mexico City, Guadalajara, and Monterrey, remains the prime demand center, absorbing nearly 40% of the national load. The trio houses 500 MW of planned hyperscale data centers that must secure firm, low-carbon power, intensifying pressure on aging sub-transmission backbones. Puebla and Hidalgo anticipate converting the 1.5 GW Tula plant from fuel oil to a combined cycle once the delayed natural-gas pipeline is delivered, which will reduce particulate emissions and free 4.5 million barrels per year of fuel oil for export.

The southern and peninsular regions lag in industrialization but have registered ambitious public-sector electrification projects. The Yucatán Peninsula benefits from twin CFE combined-cycle units in Mérida and Valladolid, safeguarding 2.9 million users against seasonal blackouts. Oaxaca maintains leadership in wind energy with 2,360 MW across 21 farms; however, limited transmission to the Bajío restricts utilization during nocturnal surpluses. A June 2025 blackout that darkened 11 states underscored vulnerability to extreme weather, prompting accelerated investments in looped 400 kV circuits and microgrid pilots.

Competitive Landscape

The Mexico power market demonstrates high concentration: CFE holds more than half of the installed generation, Iberdrola, Enel, Acciona, and Sempra Infrastructure collectively add 18%, and the next 15 producers share the remainder. Multinationals recalibrate strategies to comply with the 54%-46% split, with Iberdrola divesting USD 6.2 billion of gas assets while retaining 6 GW of renewables, and Enel pivoting toward merchant solar backed by long-term US dollar PPAs. Wärtsilä introduces a 100% hydrogen-ready 50 MW engine plant concept, positioning itself for future deep decarbonization mandates in Mexico's heavy industry to maintain its market share in the power sector.[4]Wärtsilä Corporation, “Hydrogen-Ready Engine Power Plant Launch,” wartsila.com

Domestic developers embrace distributed generation niches; Enlight's fintech joint venture finances rooftop PV plus battery bundles that circumvent centralized permitting. Equipment makers compete on grid-code compliance: Diram's 41 STATCOM deployments help heavy industry maintain power-factor standards, while Siemens Energy pilots 420 kV vacuum-interruptor breakers suited to tropical humidity conditions.

Cross-border synergies intensify competitive dynamics as US gas producers co-invest in Mexican combined-cycle plants to ensure an outlet for Permian Basin molecules. Newcomers capitalize on nearshoring tailwinds to propose dispatchable cogeneration facilities integrated into industrial parks, offering power tariff discounts below CFE's medium-voltage rate. Meanwhile, CFE's USD 7.5 billion transmission budget invites EPC consortia to bid on turnkey 400 kV corridors, with Chinese, Spanish, and Canadian firms vying for market entry certifications.

Mexico Power Industry Leaders

Comisión Federal de Electricidad (CFE)

Iberdrola México

Enel Green Power México

Saavi Energía (Actis)

Acciona Energía México

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: President Sheinbaum signed legislation creating the National Energy Commission and eliminating independent regulators; CFE unveiled USD 2.5 billion for five reliability-focused plants.

- February 2025: The Plan for Strengthening and Expansion of the National Electric System 2025-2030 outlines 51 projects worth USD 22.3 billion to add 22.7 GW, including seven wind and nine PV plants.

- November 2024: CFE presented its National Strategy for the Electric Sector 2024-2030, allocating USD 12.3 billion to generation and USD 7.5 billion to transmission.

- February 2024: Iberdrola finalized a USD 6.2 billion asset sale to Mexico Infrastructure Partners, transferring 8.5 GW of gas capacity and 460 employees.

Mexico Power Market Report Scope

Power is generated through various primary sources such as coal, hydro, solar, thermal, etc. In utilities, it is a step before its delivery to end users. Transmission and distribution take place after the process. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) per the end user's requirements. The Mexican power market report includes:

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal, and Others) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Below 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal, and Others) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Below 1 kV) |

Key Questions Answered in the Report

What is the current size of the Mexico power market?

The Mexico power market size reached 123.15 GW in 2025 and is projected to hit 146.81 GW by 2030 at a 3.58% CAGR.

Which segment holds the largest Mexico power market share?

Thermal generation led with 70.3% of the Mexico power market share in 2024, driven by abundant imported natural gas.

How fast are renewables growing within the Mexico power market?

Renewable capacity is expected to expand at a 10.3% CAGR through 2030, raising its contribution to 40.66% of total generation.

What role does nearshoring play in electricity demand?

Manufacturing relocations could lift industrial electricity consumption by 30% by 2030, adding 10.1 GW of required baseload supply.

How significant is cross-border electricity trade potential?

Surplus solar and wind generation could enable up to 4 TWh of annual exports to ERCOT and WECC grids once transmission upgrades clear.

Who regulates the Mexico power industry after the 2025 reform?

The National Energy Commission, created in March 2025, now oversees permitting and market operations following the dissolution of earlier autonomous regulators.

Page last updated on: