Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

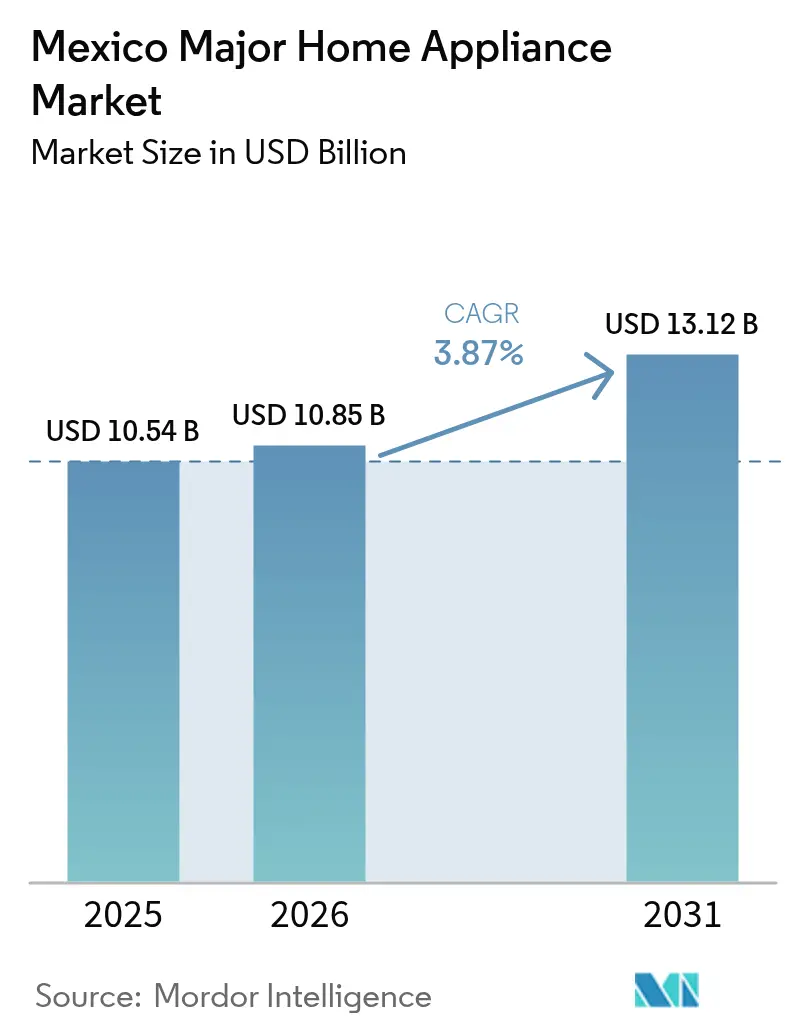

| Base Year Market Size (2025) | USD 10.54 Billion |

| Market Size (2026) | USD 10.85 Billion |

| Market Size (2031) | USD 13.12 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Major Home Appliance Market Analysis by Mordor Intelligence

The Mexico major home appliances market size reached USD 10.54 billion in 2025 and is expected to reach USD 10.85 billion in 2026, and is projected to reach USD 13.12 billion by 2031, reflecting a 3.87% CAGR. This measured expansion signals a maturing industrial ecosystem reshaped by converging forces such as regulatory mandates, nearshoring momentum, and climate-driven replacement cycles. In contrast to the rapid growth seen in emerging markets, Mexico's path is defined by its established manufacturing infrastructure. This infrastructure produces appliance units annually, primarily for export. However, domestic consumption faces challenges, notably peso volatility and inconsistent water infrastructure. The sector embodies a unique duality where manufacturers export to the United States while also catering to a domestic market. Here, households grapple with water pressure dipping below 20 psi, a limitation for water-intensive appliances. These manufacturers navigate this dual landscape by meeting North American demands with localized plants that ensure swift lead times. Simultaneously, they tailor domestic offerings, prioritizing efficiency, reliability, and service while being mindful of inflationary pressures on households.

Key Report Takeaways

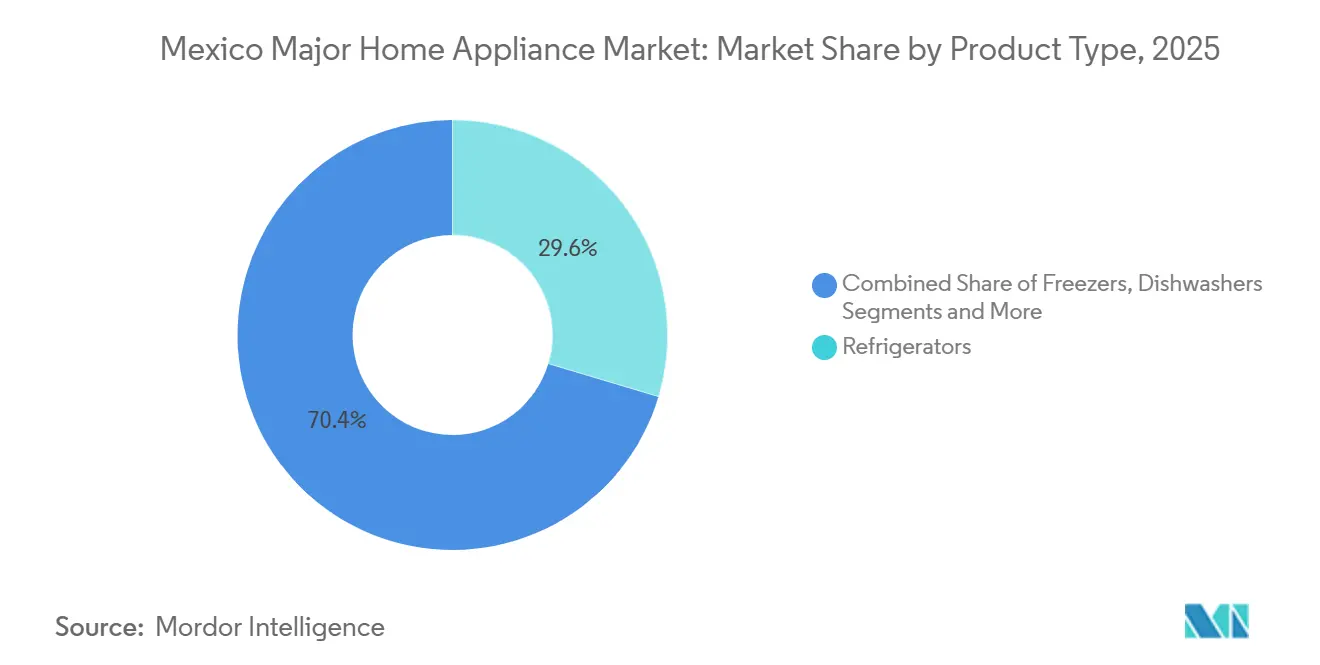

- By product type, refrigerators led with 29.62% of the Mexico major home appliances market share in 2025, whereas dishwashers are forecast to register the highest CAGR of 3.28% through 2031.

- By distribution channel, multi-brand and exclusive brand stores captured 34.30% of the Mexico major home appliances market size in 2025, while online platforms are anticipated to grow at a 6.05% CAGR during the forecast period to 2031.

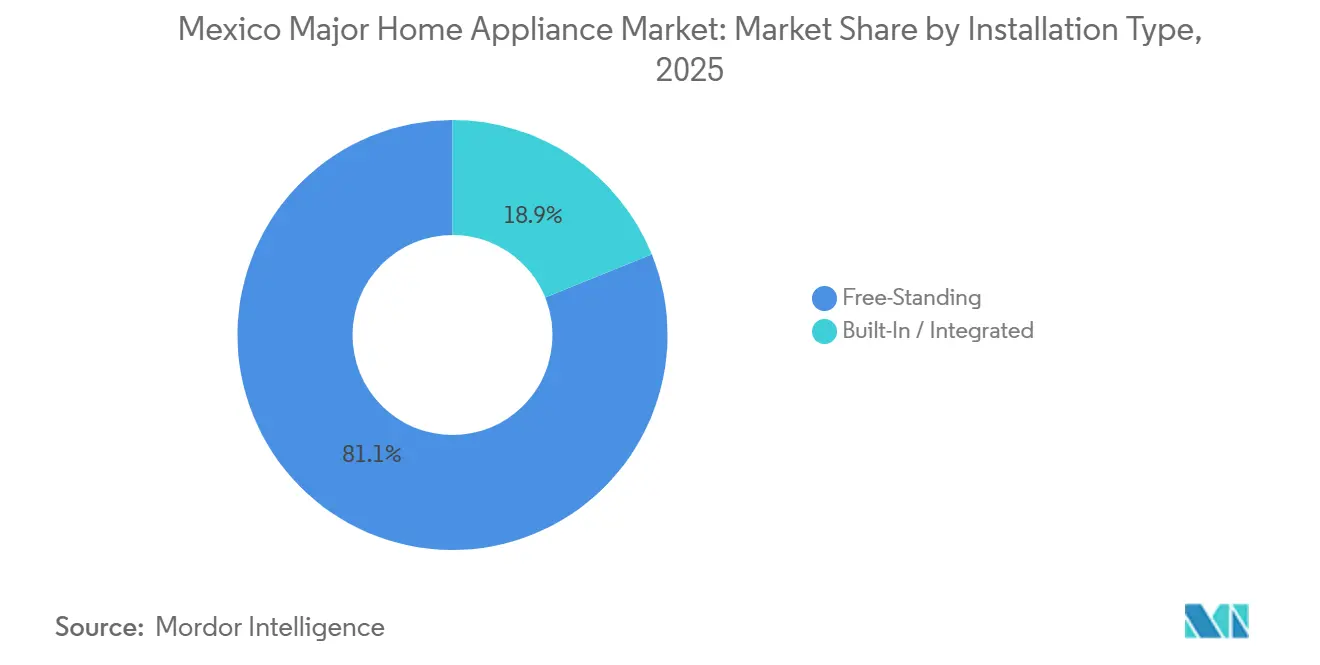

- By installation type, free-standing units held 81.12% of the Mexico major home appliances market share in 2025, while built-in appliances are projected to expand at a 4.45% CAGR through 2031.

- By technology, conventional appliances accounted for 90.12% of the Mexico major home appliances market size in 2025, whereas smart and connected appliances are expected to grow at a 4.52% CAGR through 2031.

- By geography, Northern Mexico accounted for 44.40% of the Mexico major home appliances market size in 2025, while Southern Mexico is projected to expand at a 4.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Major Home Appliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NOM-015 energy-efficiency standards accelerating refrigerator/freezer replacements | +0.5% | National, with early gains in Monterrey, Guadalajara, and Mexico City | Short term (≤ 2 years) |

| Premiumisation and smart-feature upgrades in core categories | +0.4% | National, strongest in Northern and Central urban corridors | Medium term (2-4 years) |

| Omnichannel retail with installments (MSI) is improving the affordability of big-ticket MDAs | +0.6% | National, penetrating Tier-II cities and semi-urban zones | Short term (≤ 2 years) |

| Nearshoring-led capacity and product availability gains | +0.8% | Northern Mexico, with supply-chain spillover to Central Mexico | Medium term (2-4 years) |

| Heatwaves are driving faster-than-expected AC adoption | +0.7% | Northern and Central Mexico, episodic in the Southern coastal zones | Short term (≤ 2 years) |

| Rising household incomes and household formation support durable demand | +0.5% | National, concentrated in manufacturing-belt municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NOM-015 Energy-efficiency Standards Accelerating Refrigerator/Freezer Replacements

Mexico’s refrigerator standard under the NOM-015-ENER framework makes efficiency and energy-label transparency central to replacement decisions, reinforcing a steady upgrade cycle for compressor-based platforms. The yellow energy label with annual kWh disclosure gives shoppers a common benchmark across sizes and formats, and retailers have integrated this data into search filters and in-store signage to reduce decision friction. As compliance thresholds hardened, OEMs refreshed lineups around higher-efficiency architectures and premium configurations that capture larger baskets during replacement. The result is a widening spread between older stock and current-generation models that position quiet operation, stable cooling, and energy savings as everyday benefits rather than niche features. This dynamic supports sustained refrigerator demand even as overall growth remains measured, with the category’s leadership amplified by consistent labeling and audit rules under the NOM framework[1]Instituto Nacional de Electricidad y Energías Limpias, “Guía de Cumplimiento de la NOM-015-ENER,” INEEL, ineel.mx.

Omnichannel Retail with Installments (MSI) Improving Affordability of Big-ticket MDAs

Zero-interest installments and buy-now-pay-later options have become common triggers for big-ticket purchases, lifting conversion during national events and smoothing monthly outlays for households that plan spending in fixed tranches. Retailers and marketplaces have embedded these plans into omnichannel checkouts, where shoppers routinely filter by installment length and monthly cap before choosing capacity or brand. The mechanism pulls mid-tier buyers toward higher-spec SKUs that would be deferred in a full-cash scenario, thereby supporting premium shifts in refrigerators, laundry, and inverter ACs during promotional windows. Installment depth and partner terms vary by banner and region, but the structural effect is consistent, as flexible payment frameworks broaden eligibility beyond traditional bank credit. Periods of tighter unsecured lending can limit availability and suppress promotional surges, which introduces quarter-to-quarter variability in replacement-heavy categories. These retail-finance dynamics are a prominent tailwind for the Mexico major home appliances market, where digital research and checkout have redefined assortment visibility and deal discovery[2]Asociación Mexicana de Venta Online, “Estudio de Venta Online en México 2024,” AMVO, amvo.org.mx.

Nearshoring-led Capacity and Product Availability Gains (Local Manufacturing)

A new wave of plant openings and capacity additions has scaled output for North America, with refrigeration and kitchen platforms gaining localized production and shorter replenishment cycles. Notable projects include a new BSH refrigeration factory in Salinas Victoria that serves Bosch and Thermador brands in premium formats, while upstream investments by global players strengthen regional platform alignment and logistics resilience. Automation upgrades and process certifications at incumbent plants have been used to stabilize cost positions and throughput while improving uptime, helping offset compliance and tooling costs associated with refrigerant transitions. Supplier development remains a multi-year task, particularly for precision components that have stringent qualification gates, yet co-location of assembly and engineering improves the cadence of model rollouts for North American ranges. The onshoring of complex SKUs also reinforces after-sales ecosystems that rely on local parts availability and trained technicians. These shifts support dependable product availability and more predictable lifecycles in the Mexico major home appliances market, as North American lead times compress and export flows diversify across customer programs.

Heatwaves Driving Faster-than-expected AC Adoption

Prolonged heat across Northern and Central states has pulled forward air conditioner purchases and tightened replenishment windows, with inverter minisplits gaining share as buyers weigh performance, noise, and operating costs. Product roadmaps emphasize higher seasonal efficiency ratios, low-GWP refrigerants, and reliability features that address voltage fluctuations and restarts following outages. OEMs are evolving their portfolios toward R32 and other next-generation blends in line with global phase-down commitments, which increase initial engineering and service requirements but position compliant platforms for multi-year runs. Local assembly of mainstream cooling models shortens delivery times during peak months and creates room for channel-specific configurations. These shifts anchor a durable cooling pathway in the Mexico major home appliances market, while compliance rules on refrigerants embed higher-quality thresholds into design and service processes[3]United Nations Industrial Development Organization, “Mexico – Pilot project on energy efficiency in the context of HFC phase-down – project document,” UNIDO, unido.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront costs for energy-efficient HVAC/appliances | -0.6% | National, with acute pressure on the D/E socioeconomic segments | Medium term (2-4 years) |

| Low dishwasher penetration and usage habits are limiting the category scale | -0.3% | National, marginal relief in luxury housing developments | Long term (≥ 4 years) |

| Urban water scarcity concerns constrain water-intensive appliances | -0.4% | Mexico City, Monterrey, Tijuana, and spreading to secondary cities | Medium term (2-4 years) |

| Refrigerant transition raising redesign/compliance costs | -0.5% | National manufacturing base, indirect consumer price transmission | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs for Energy-efficient HVAC/Appliances

Upfront price gaps between entry and higher-efficiency appliances complicate upgrade decisions for value-focused households, even as energy labels elevate awareness of long-term savings. Mandatory efficiency measures, such as inverter compressors and improved insulation, increase engineering and materials costs, which can only be partially passed through to retail. When financing depth narrows or promotions fade, the spread between baseline and compliant platforms slows replacement in the lowest income bands. This sensitivity can open space for non-compliant imports that promise headline savings but lack certification, warranty coverage, and service access. Enforcement of conformity assessment and labeling standards is tightening across categories, raising the risk for sellers who bypass official channels. These factors collectively slow migration toward the most efficient tiers and shape assortment design in the Mexico major home appliances market, where reliability and certification are increasingly important in buyer decisions.

Urban Water Scarcity Concerns Constraining Water-intensive Appliances

Low and variable water pressure in dense urban districts limits the addressable base for dishwashers and, to a lesser extent, front-load washers, which require stable supply conditions to perform as designed. Developers are advancing built-in formats in new projects, but retrofit friction and plumbing requirements remain non-trivial for existing housing stock. Brands with premium positioning have integrated pressure-boost options and compact formats to match smaller kitchens and mitigate installation hurdles. Even with these adaptations, the category expands from a small base and remains uneven across metros that differ in service continuity and infrastructure age. The same constraints reduce the appeal of water-intensive cycles for buyers who prioritize predictability and low maintenance. These structural conditions temper adoption in Mexico's major home appliances market despite rising interest in time-saving kitchen platforms among dual-income households.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigerators Anchor Replacement Demand, Dishwashers Ride Premiumization Wave

Refrigerators captured 29.62% of the Mexico major home appliances market share in 2025, supported by labeling-led comparisons and standard-driven improvements that concentrate demand in compliant, higher-efficiency models. The regulatory signal keeps replacement steady and strengthens the case for premium-capacity units that promise consistent cooling, low noise, and lower lifecycle energy use. As these platforms rotate into local assembly lines, product availability improves in French-door and bottom-mount formats that target urban buyers upgrading from legacy configurations. New manufacturing footprints in Northern Mexico add resilience to premium refrigeration, shortening delivery cycles to North American retailers and stabilizing domestic inventories during promotions. These moves improve alignment with consumer expectations in top metros where shoppers weigh storage flexibility and efficiency together. The result is a category that sits at the center of household replacement plans for the Mexico major home appliances market as retail finance removes some upfront friction in higher-capacity tiers[4]BSH Hausgeräte GmbH, “Milestone for North America Growth Strategy: BSH Opens First Refrigeration Factory in Mexico,” BSH Group Press, bsh-group.com.

The fastest-growing product line is dishwashers, which is projected to expand at a 3.28% CAGR to 2031 as developers standardize built-in kitchens and households adopt compact formats that fit smaller spaces. Infrastructure limits remain a core barrier, so brands lean into pressure-boosting designs, easy-fit form factors, and quiet cycles that fit apartment living. Adoption is strongest in affluent districts where installation is planned during construction, and where purchase timing aligns with broader kitchen upgrades. Awareness campaigns that emphasize hygienic benefits and convenience can influence replacement windows for adjacent categories as families optimize appliances around cooking and cleaning routines. As e-commerce expands fulfillment coverage and MSI-based promotions normalize, more households are exposed to entry-premium dishwashers that anchor bundle deals in new builds. These factors expand the addressable base for the Mexico major home appliances market while keeping growth measured due to service and plumbing constraints.

By Distribution Channel: Multi-Brand Stores Leverage Assortment Depth, Online Platforms Scale via BNPL

Multi-brand and exclusive brand stores accounted for 34.30% of 2025 sales, supported by nationwide footprints, on-site credit approvals, and hands-on evaluation, which remain influential for kitchen and laundry purchases. Store staff demonstrate key functions and surface installation requirements before checkout, which increases confidence for water- and power-sensitive categories. Flagship showrooms provide curated premium assortments and ecosystem demonstrations that frame the value of connected control and energy tracking for busy households. Retailers coordinate with manufacturers during major promotional windows, aligning inventory and display strategies around bestseller formats with rapid turnaround. As a result, brick-and-mortar remains a preferred path to purchase for first-time buyers and for large appliances that require delivery and installation. The structure keeps multi-brand retail central to conversion in Mexico's major home appliances market, even as digital research dominates the upper funnel.

Online platforms are the fastest-growing channel, with a 6.05% CAGR through 2031, reflecting deeper assortment visibility, easy filtering by capacity and features, and embedded installment options at checkout. Retailers integrate click-and-collect and scheduled delivery in high-density metros, where customers value time certainty and tracking updates. Digital carts often mix small and large appliances, which rewards banners that coordinate bundling, slotting, and extended-warranty options. Associations report steady rises in research and online purchases for large appliances, with mobile-first behavior shaping discovery and price matching across retailers. These improvements allow digital channels to match or exceed conversion on premium SKUs, especially when free installation and haul-away are promoted during sales events. The combined online and store experience is now the default path in the Mexico major home appliances market, with MSI and BNPL services serving as a bridging tool for larger baskets.

By Installation Type: Free-Standing Units Dominate via Flexibility, Built-In Gains in New Construction

Free-standing appliances accounted for 81.12% of 2025 sales due to flexible placement, easier moves during relocations, and lower replacement complexity. Households in detached homes and low-rise buildings value plug-and-play convenience and quick availability at retail during urgent replacements. Entry price points stay most accessible with free-standing formats, making them the default in many municipalities far from metro centers. Retailers emphasize core features, energy labels, and service coverage to ensure return assurance for free-standing offers. Even at higher price tiers, free-standing refrigerators and ranges remain a staple in replacement cycles that align with household moves or renovations. These patterns keep free-standing units at the center of daily purchase decisions in Mexico's major home appliances market, as upgrades reflect gradual shifts in efficiency and capacity.

Built-in and integrated appliances are projected to outpace overall growth with a 4.45% CAGR through 2031 as developers bundle equipped kitchens and premium buyers target seamless aesthetics and quiet operation. Refrigeration, dishwashers, and hobs in integrated formats benefit from coordinated cabinetry and professional installation that front-loads fit-and-finish choices during construction. Premium manufacturers with local production can shorten custom lead times and align features with local standards, strengthening the case for built-in packages. Over the lifecycle, service networks and certified installers play a larger role, and warranties reinforce value propositions through longer coverage terms. Replacement cycles can be longer for integrated formats, yet higher realized prices per unit sustain revenue even as volumes remain modest outside top metros. This segment adds an important premium pathway for the Mexico major home appliances market, where urban households fund kitchen personalization through mortgages and planned renovations.

By Technology: Conventional Appliances Retain Mass-Market Grip, Smart Models Surge in Connected Households

Conventional appliances accounted for 90.12% of 2025 sales, reflecting durable demand for platforms that deliver core functions at accessible price points and do not depend on stable broadband. Households in semi-urban and rural areas continue to prioritize upfront affordability and straightforward service pathways over ecosystem features. Retailers position conventional SKUs as reliable workhorses with clear labels, simple maintenance, and nationwide warranty coverage. As efficiency standards elevate base performance, conventional models gain incremental savings and quieter operation without major changes to usage behavior. This combination sustains broad appeal for laundry, refrigeration, and cooking categories where upfront price remains decisive. The structure keeps conventional technology central to the Mexico major home appliances market while connected platforms expand within higher-income segments.

Smart and connected appliances are projected to grow at a 4.52% CAGR through 2031, with adoption strongest in top metros where buyers value app-based control, energy monitoring, and voice integration. Brands highlight convenience features such as remote diagnostics, guided cycles, and schedule optimization aligned with daily routines. Smart ACs and inverter platforms illustrate the pairing of connectivity with energy management, which supports comfort use cases during extended heat. Localized product lines in Mexico include connected cooling and laundry models that integrate with mainstream voice assistants and mobile apps. As more appliances coordinate through standard protocols, interoperability improves and reduces friction for cross-brand households. These upgrades expand the premium segment of Mexico's major home appliances market and encourage step-ups during replacement when financing aligns with promotional events.

Geography Analysis

Northern Mexico led the market with 44.40% of 2025 revenue, as manufacturing payrolls, cross-border logistics, and long cooling seasons support larger household baskets and steady AC adoption. Export-oriented plants consolidate premium refrigeration and cooling models near the Texas border, offering short replenishment paths to North America while maintaining domestic allocations. Localized production of premium formats by global OEMs reinforces inventory depth during national promotions and supports shorter lead times for made-to-order variants. Retailers in this region emphasize high-efficiency ACs, premium refrigeration, and integrated kitchen packages that benefit from installment promotions. As new plants reach scale, component localization and service capacity deepen coverage in satellite cities. These structural features support sustained leadership for Northern states in the Mexico major home appliances market, with a stable base for both export and domestic channels.

Central Mexico combines the country’s largest urban demand center with established industrial corridors that shape household purchase patterns and service expectations. Replacement drives a significant share of category revenue in Mexico City and surrounding municipalities, where energy labels and measured noise levels factor into apartment and townhome selection. E-commerce and omnichannel models are most mature here, and shoppers routinely compare labels, features, and installment options online before choosing store pickup or scheduled delivery. Developers in major metros standardize on built-in packages in higher-end projects, which helps integrated dishwashers and refrigeration reach buyers who plan to install during construction. Retailers partner with OEMs on seasonal events to balance stock across formats and sizes that fit compact kitchens. This region serves as a bellwether for premium adoption in Mexico's major home appliances market, with online demand often leading category shifts that later expand to Tier-II cities.

Southern Mexico is projected to record the fastest growth through 2031, driven by rising household formation in fast-growing tourist corridors and infrastructure projects that extend distribution coverage. Refrigeration and laundry categories expand from a lower installed base, and promotions during national events introduce entry-premium tiers to new buyers. Retailers downshift assortment depth to compact formats and bundle extended service to build trust as after-sales expectations evolve. Cooling demand grows with longer heat seasons along the coasts, which accelerates the migration to inverter ACs in select urban clusters. As coverage widens, retailers apply hub-and-spoke delivery to shorten installation windows and reduce missed appointments. These improvements expand addressable demand in the Mexico major home appliances market while keeping growth more sensitive to credit conditions and logistics capacity in newly served zones.

Competitive Landscape

The Mexico major home appliances market shows moderate concentration, with leading brands sustained by local manufacturing, broad retail footprints, and multi-category portfolios that align with labeling and refrigerant rules. Incumbents with in-country plants coordinate platform upgrades and service training ahead of seasonal peaks, stabilizing prices and inventory for priority SKUs. Whirlpool’s manufacturing sites in Northern Mexico have advanced shop-floor efficiency programs and external certifications that signal production discipline and cost control. BSH’s new refrigeration factory establishes a local premium anchor, shortening timelines for French-door and bottom-mount formats while integrating sustainable operations to meet corporate goals. These moves signal long-term commitments to the region and support domestic availability during campaign periods. The structure supports measured expansion in the Mexico major home appliances market while manufacturers manage compliance and component localization agendas.

Global brands are strengthening smart ecosystems to differentiate user experiences in cooling and laundry, with connected controls, diagnostics, and energy insights that address urban household needs. Product localization for Mexico integrates voltage tolerance and installation flexibility that fit apartment retrofits and new builds. As interoperability improves, premium buyers can mix across categories and brands, which increases the value of reliable service networks and software support. New cooling investments for North America, including facilities dedicated to advanced air handlers, reflect rising thermal management needs in data-intensive sectors that influence residential design and training pipelines. These strategies support the adjacent HVAC channel and shape expectations for inverter performance and low-GWP refrigerants in home AC portfolios. Together, these shifts strengthen the Mexico major home appliances market by aligning platform roadmaps with regional standards and user preferences.

Challenger brands compete on feature-value balance and rapid online response times, often pairing affordable inverter ACs and accessible refrigeration with nationwide service partners. They leverage marketplace visibility during national events and offer extended warranty bundles to build trust in categories with high replacement sensitivity. Retailers now treat connected features as add-ons that can sway decisions when priced near mass thresholds during installment campaigns. In premium tiers, European kitchen brands lean on built-in aesthetics and quiet operation, supported by local manufacturing that reduces delivery variability. Across tiers, conformity assessment and labeling standards remain baseline requirements, raising the bar for entry and narrowing informal channels. This alignment favors brands with established compliance processes and field service coverage, reinforcing a balanced but competitive Mexico major home appliances market where product and service execution determine share shifts.

Mexico Major Home Appliance Industry Leaders

Mabe

Whirlpool

LG Electronics

Samsung Electronics

Hisense

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Daikin Applied's Alliance Air subsidiary completed construction of its USD 121 million energy-efficient HVAC manufacturing facility in Tijuana, spanning 460,000 square feet and employing 1,150 workers to produce custom air handlers and computer-room cooling solutions for North American data centers.

- March 2025: Mabe, Mexico's leading home appliance manufacturer, announced a USD 668 million investment spanning 2025-2027 to refurbish and expand its 15 factories nationwide, focusing on IoT integration, R32 refrigerant transitions, and advanced inverter washing machines; this commitment brings Mabe's total Mexican investment since 2023 to USD 1.1 billion.

- February 2025: Whirlpool Corporation's Horizon and Plastics manufacturing plants in Ciudad Apodaca, Nuevo León, achieved Silver-level World Class Manufacturing (WCM) certification from external auditors, validating 60% expansion of systematic improvement pillars and 7% cost savings over 12 months through waste elimination, inventory optimization, and employee-driven continuous-improvement initiatives.

- January 2025: Samsung Electronics and LG Electronics initiated evaluations of partial production relocations from Mexico to US facilities in response to proposed 25% tariff threats, with Samsung considering shifting dryer output from Querétaro to Newberry, South Carolina, and LG weighing refrigerator/TV transfers to Clarksville, Tennessee, signaling nearshoring's vulnerability to trade-policy volatility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the Mexico major home appliance market as the revenue generated from the sale of new, factory-built "white goods" that perform core household tasks, including refrigerators, standalone freezers, washing machines, dishwashers, cooking ovens (inclusive of microwave and combi units), and room air-conditioners, delivered to residential and small commercial users within Mexico in a given year.

Scope Exclusions: Small countertop devices, spare parts, HVAC chillers, and used or refurbished units are outside the study.

Segmentation Overview

- By Product Type

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Cooktops & Ranges

- Microwave Ovens

- Air Conditioners

- Others (Electric Hobs)

- By Distribution Channel

- Multi-Brand and Exclusive Brand Stores (EBOs)

- Hypermarkets & Supermarkets

- Online / E-commerce Platforms

- Direct-to-Consumer (D2C) & Subscription Models

- By Installation Type

- Free-Standing

- Built-In / Integrated

- By Technology

- Conventional Appliances

- Smart / Connected Appliances

- By Geography

- Northern Mexico

- Central Mexico

- Southern Mexico

Detailed Research Methodology and Data Validation

Primary Research

We interview appliance makers, component suppliers, national retailers, and logistics specialists across Northern, Central, and Southern Mexico. These discussions confirm penetration rates, warranty return ratios, and typical replacement cycles, helping us refine the desk-derived assumptions and triangulate the final model.

Desk Research

Our analysts start with publicly available macro and trade sources such as INEGI household expenditure surveys, Banco de México retail sales indices, UN Comtrade import-export codes 8418 and 8450, CANIETI production releases, and energy-efficiency regulations NOM-015 and NOM-003. Company filings, investor decks, and reputable press are mined to track average selling prices and brand channel strategies. Paid repositories like D&B Hoovers and Dow Jones Factiva assist us in checking manufacturer revenue splits and shipment narratives. The secondary sources cited above are illustrative; many additional references were consulted for validation and clarification.

Market-Sizing & Forecasting

A top-down construct begins with official production, import, and export data to recreate national supply, which is then filtered through estimated domestic sell-through and average selling prices. Select bottom-up checkpoints, including sampled retailer volumes and manufacturer revenue parses, anchor the totals. Key variables include household formation growth, urban electricity tariff trends, replacement cycle length, e-commerce share in durable goods, peso-dollar movements, and enforcement of energy-efficiency norms. Multivariate regression, informed by these drivers and consensus signals from expert calls, projects demand through 2030. Where bottom-up data are spotty, gaps are filled using benchmark price-volume pairs from similar states and years.

Data Validation & Update Cycle

Outputs pass anomaly checks, variance analyses, and multi-analyst peer reviews before sign-off. Reports refresh every twelve months, with mid-cycle revisions triggered by events such as tariff shifts or major plant closures. A final pre-delivery pass ensures clients receive the latest calibrated view.

Why Mordor's Mexico Major Home Appliance Baseline Commands Reliability

Published estimates often differ; definitions, base years, and modeling shortcuts vary, which confuses decision-makers.

Key gap drivers include scope mismatch (some studies fold small devices or exclude built-in air-conditioners), reliance on single-year customs totals without replacement-cycle corrections, older base-year anchoring, and infrequent updates that miss peso volatility. Mordor's disciplined mix of current-year field insight, clearly stated product boundaries, and annual refresh cadence mitigates those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.54 B (2025) | Mordor Intelligence | |

| USD 10.32 B (2024) | Regional Consultancy A | Narrower product mix; air-conditioners excluded |

| USD 11.24 B (2023) | Global Consultancy B | Older base year and customs-only top-down build |

These contrasts show that Mordor Intelligence delivers a balanced, transparent baseline rooted in up-to-date variables and repeatable steps, giving stakeholders a dependable foundation for strategy and investment decisions.

Key Questions Answered in the Report

What is the current size and growth outlook for the Mexico major home appliances market?

The Mexico major home appliances market size was USD 10.54 billion in 2025, is expected at USD 10.85 billion in 2026, and is projected to reach USD 13.12 billion by 2031 at a 3.87% CAGR.

Which product category leads sales in Mexico’s large appliances?

Refrigerators led with a 29.62% revenue share in 2025, supported by energy-efficiency labeling and steady replacement cycles.

Which sales channel is growing fastest for large appliances in Mexico?

Online platforms are the fastest-growing channel, with a 6.05% CAGR, driven by installment payments and stronger omnichannel fulfillment.

Which region contributes the most to Mexico’s major home appliances?

Northern Mexico contributed 44.40% of 2025 revenue due to manufacturing employment, logistics access, and longer cooling seasons.

How is the technology mix evolving across large appliances in Mexico?

Conventional platforms still dominate, accounting for 90.12% of 2025 sales, while smart and connected appliances are growing at a 4.52% CAGR as urban households adopt app-based control and diagnostics.

What are two important drivers shaping demand in Mexico’s large appliances?

Energy-efficiency and labeling standards that accelerate replacement cycles, and installment-based retail finance that lowers upfront barriers for premium features.

Page last updated on: