Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.97 Billion |

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 8.29% CAGR |

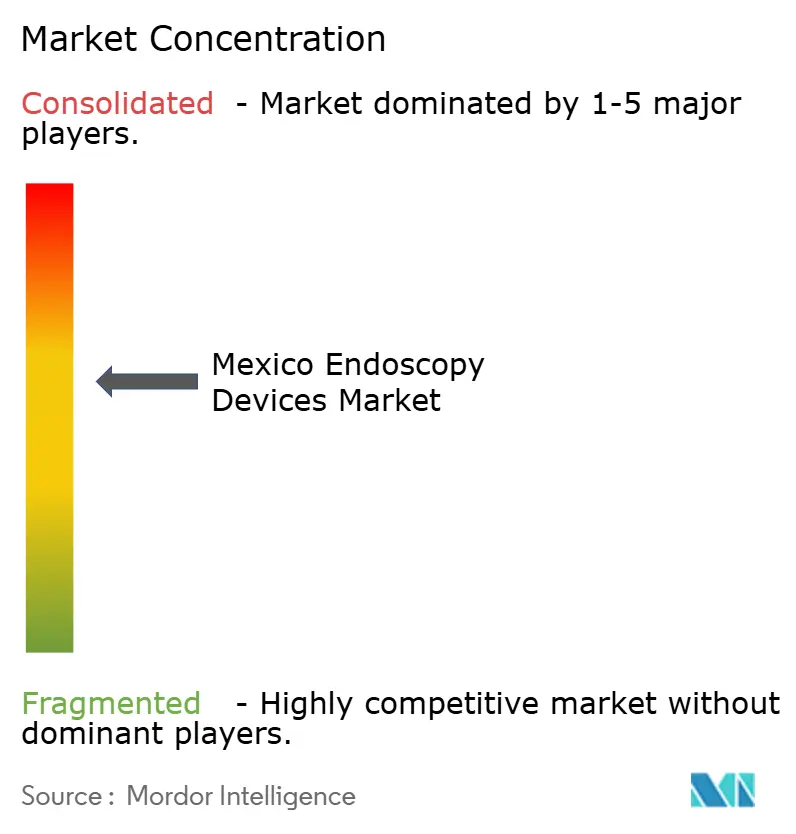

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Endoscopy Devices Market Analysis by Mordor Intelligence

The Mexico Endoscopy Devices Market size is projected to be USD 0.97 billion in 2025, USD 1.04 billion in 2026, and reach USD 1.55 billion by 2031, growing at a CAGR of 8.29% from 2026 to 2031.

Strong private spending, which now accounts for about 55% of national health outlays, is reshaping procedure volumes as patients shift toward fee-for-service hospitals and ambulatory centers. Public purchasers are responding with an MX$4 billion program that will open 31 hospitals and upgrade 256 operating rooms by the end of 2026, adding procurement momentum on the institutional side. Demand is also boosted by fast-imaging upgrades as tertiary networks adopt 4K and artificial-intelligence visualization, while tightening infection-control rules create early pull for single-use platforms. Competitive pressure is intensifying as Medtronic, Olympus, KARL STORZ, Fujifilm, Johnson & Johnson MedTech, and Intuitive Surgical expand bundled offerings that pair visualization, energy devices, and software analytics. Finally, COFEPRIS’ abbreviated approval pathway, released in 2025, is shortening market-entry times for multinational products that already hold IMDRF or MDSAP credentials.

Key Report Takeaways

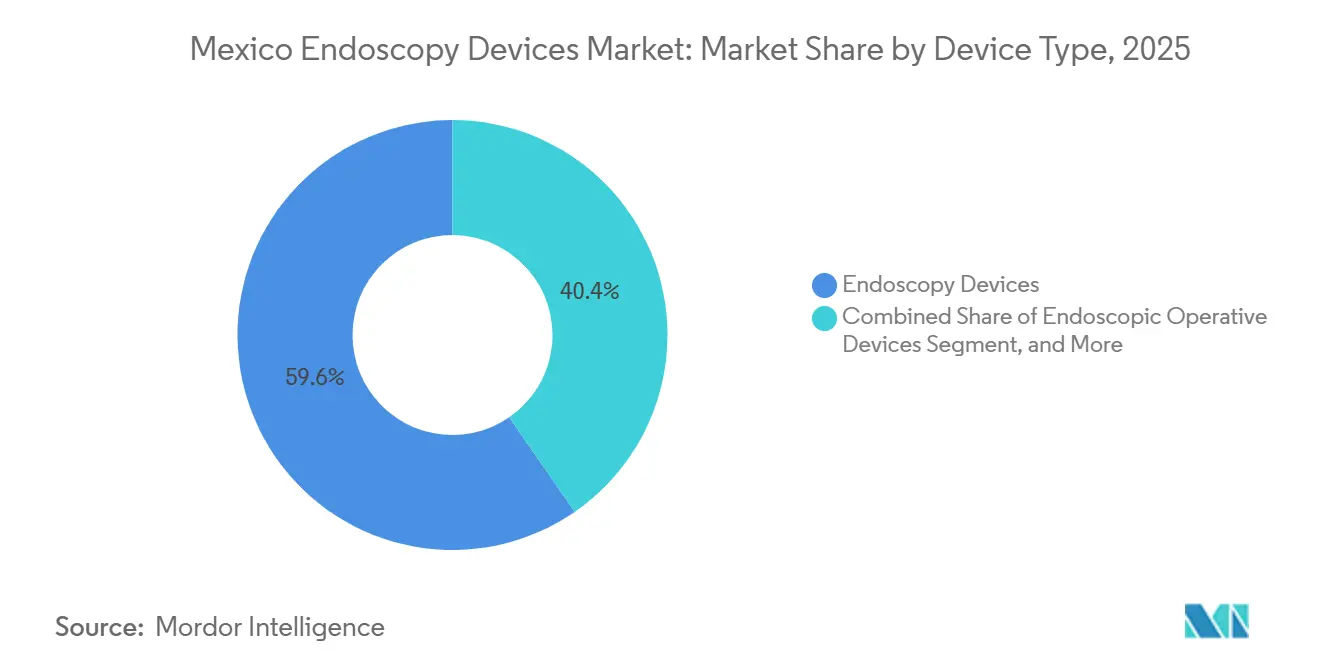

- By device type, endoscopes led with 59.62% of Mexico endoscopy devices market share in 2025, while endoscopic operative devices are forecast to post the highest 8.62% CAGR through 2031.

- By application, gastrointestinal endoscopy accounted for 42.03% of revenue in 2025; gynecology procedures are projected to grow at a 9.69% CAGR through 2031.

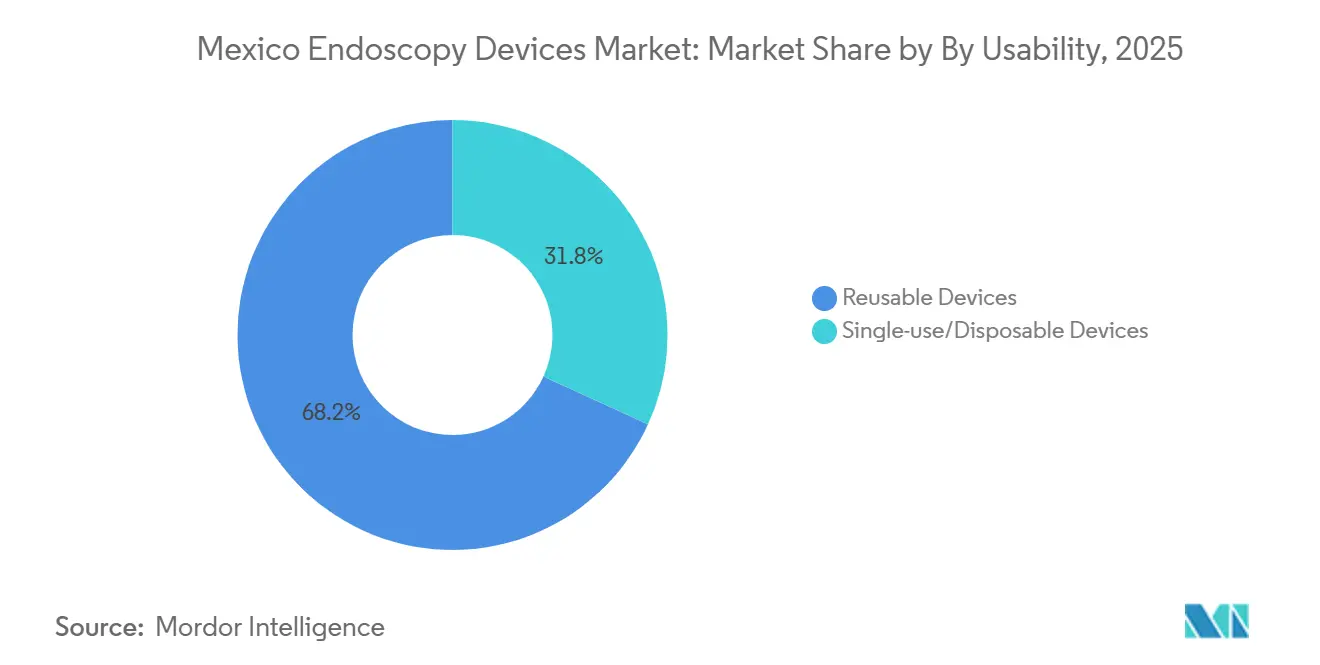

- By usability, reusable equipment dominated at 68.18% in 2025, yet single-use systems are expected to rise at a 9.01% CAGR over the same period.

- By end user, hospitals accounted for 68.18% in 2025, whereas specialty clinics are set to grow fastest at a 11.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Gastrointestinal (GI) Disorders | +1.8% | National, with early gains in Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Expansion of Private Hospitals & ASCs | +2.1% | Urban centers and border regions (Tijuana, Ciudad Juárez, Monterrey) | Short term (≤ 2 years) |

| Government-Backed Early Cancer-Screening Programs | +1.3% | National, pilot programs in select states | Long term (≥ 4 years) |

| Rapid HD/4K & AI-Enabled Imaging Upgrades | +1.6% | Tertiary hospitals in major metros, private hospital networks | Medium term (2-4 years) |

| Medical-Tourism Inflow to Border Cities | +1.2% | Tijuana, Ciudad Juárez, Monterrey, Cancun | Short term (≤ 2 years) |

| Growth In Gastroenterology Fellowship Seats | +0.9% | National, concentrated in teaching hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gastrointestinal Disorders

More than 16,000 new colorectal cancer cases were logged in 2025, and mortality continues to edge upward despite local pilot screening successes. Instituto Mexicano del Seguro Social data show that small bowel bleeding accounted for 65.2% of capsule procedures, with a diagnostic yield of 75.6%, underscoring the need for earlier detection technologies.[1]Secretaría de Salud, “Revisión Rápida de las Tecnologías de Tamizaje para el Cáncer Colorrectal en México,” gob.mxWhile technical performance is comparable to global benchmarks, fragmented procurement across IMSS, ISSSTE, and private payers delays the adoption of standardized solutions. The resulting backlog pushes hospitals to retrofit existing suites with flexible endoscopes capable of advanced imaging, reinforcing baseline demand for core platforms. Device manufacturers that can pair high-diagnostic-yield technologies with capital-light financing are best positioned to convert latent clinical need into installed base growth.

Expansion of Private Hospitals and Ambulatory Centers

Private operators have accelerated construction in major metros, supported by investor confidence in self-pay and insured demand. Large chains such as Star Médica standardized 20 OR1 integrated theaters in 2025, improving workflow and staff utilization while locking in service contracts with KARL STORZ. Smaller specialty clinics focus on high-volume colonoscopy and upper GI cases, capitalizing on shorter scheduling windows than public institutions. This facility mix upgrades visualization hardware cycles every three to four years, compared with five-plus years historically. High throughput also favors the adoption of energy devices and suction-irrigation tools, reinforcing cross-selling opportunities across the Mexican endoscopy devices market.

Government-Backed Early Cancer-Screening Programs

Pilot fecal immunochemical test projects delivered a 77.7% colonoscopy follow-through rate, but remain confined to a handful of states. Expansion to a national mandate would immediately scale procedure volumes and accelerate equipment turnover. Public tenders, however, still prioritize reusable fleets to minimize upfront cost. Vendors that align their proposals with value-based procurement metrics, such as reduced adverse-event rates or faster room turnover, may gain an edge as outcome-linked reimbursement pilots mature.

Rapid HD, 4K, and AI-Enabled Imaging Upgrades

Olympus rolled out its VISERA ELITE III 4K platform in 2025, offering backward compatibility that lowers the upgrade hurdle for hospitals already holding large, rigid, and flexible inventories.[2]Olympus Latin America, “Olympus Showcases Next-Generation EVIS X1 Endoscopy System,” olympusamerica.com Johnson & Johnson MedTech embedded real-time analytics into staplers and visualization towers, signaling a market shift toward connected operating rooms that feed data to quality dashboards. Hospitals view modular imaging as a hedge against rapid innovation cycles, further boosting replacement demand within the Mexico endoscopy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Endoscopy Platforms | -1.4% | National, acute in public hospitals and rural facilities | Medium term (2-4 years) |

| Constrained Reimbursement for Outpatient Scopes | -0.9% | National, IMSS/ISSSTE service areas | Long term (≥ 4 years) |

| Shortage of Skilled Endoscopy Staff Outside Metros | -0.7% | Rural and secondary cities | Long term (≥ 4 years) |

| Import-Tariff Uptick on Selected Flexible Scopes | -0.6% | National, with supply-chain impacts on Mexicali manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Endoscopy Platforms

Robotic systems such as da Vinci and Hugo require investments exceeding USD 1 million, a figure beyond the means of many secondary hospitals. Proposed 25% United States tariffs on Mexican-made instruments risk inflating accessory prices in 2026, which could delay purchasing decisions at both public and private facilities. Public infrastructure funds through 2026 favor bricks-and-mortar projects, leaving limited room for premium imaging in annual budgets. Financing models that bundle equipment, service, and training into multi-year operating leases may partially offset the spending bottleneck.

Constrained Reimbursement for Outpatient Scopes

Bulk-purchase frameworks run by Birmex fix procedure tariffs that barely cover staff and reprocessing costs, restraining hospitals from adopting higher-priced single-use consumables.[3]Organización Panamericana de la Salud, “Manual de Esterilización para Centros de Salud,” pediatria.gob.mx Delays of 12–18 months before new devices appear in the National Compendium further lengthen payback periods. Private insurers offer more flexibility, yet they insure a minority of the population. Until outcome-based payment scales nationally, margins for advanced consumables will stay tight outside large private networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Endoscopes Sustain Core Volume, Operative Devices Outpace

Endoscopes generated 59.62% of Mexico endoscopy devices market revenue in 2025. Growth remains tethered to flexible platforms that cover gastrointestinal, pulmonology, and urology procedures. Robotic-assisted scopes, clustered in 27 tertiary hospitals, raise procedural precision but still command a premium. Visualization extensions that pair high-definition camera heads with existing scopes broaden the addressable budget without requiring full fleet replacement.

Endoscopic operative devices are forecast to expand at an 8.62% CAGR, the fastest growth rate in the market. Hospitals favor integrated bipolar sealers such as Olympus POWERSEAL that streamline instrument exchanges and reduce smoke generation. As procedure volume rises, suction-irrigation systems and wound protectors see parallel demand curves, cementing cross-category sales within the Mexico endoscopy devices market.

By Application: GI Holds Lead, Gynecology Scales Quickly

Gastrointestinal procedures represented 42.03% of the total market in 2025, anchored by colonoscopy volumes tied to rising colorectal cancer incidence. Capsule endoscopy remains niche but shows potential for expansion as reimbursement mechanisms evolve.

Gynecology is projected to grow at a 9.69% CAGR to 2031, supported by robotic hysterectomy programs in Guadalajara, Mexico City, and Monterrey. Medtronic’s Hugo RAS launch is expected to democratize access beyond the three metro clusters, lifting procedure counts and, by extension, the Mexico endoscopy devices market size for women’s health applications.

By Usability: Reusable Dominates, Single-Use Gains Momentum

Reusable equipment accounted for 68.18% of revenue in 2025, consistent with public-sector cost priorities. Nevertheless, single-use devices are set to rise at a 9.01% CAGR as updated disinfection guidelines highlight reprocessing gaps that pose infection risks. Hospital administrators increasingly weigh the full cycle cost of washers, tracking software, and staff time, opening a path for disposables in high-risk procedures within the Mexico endoscopy devices market.

By End-User: Hospitals Anchor Demand, Clinics Accelerate

Hospitals held a 68.18% share during 2025, buoyed by federal spending on new facilities and operating room upgrades. Integrated theater rollouts, exemplified by Star Médica’s deployment, favor turnkey vendor ecosystems.

Specialty clinics are projected to grow at 11.01% CAGR through 2031, reflecting urban migration trends and the appeal of shorter wait times. Their lean structures favor modular towers and single-use scopes, reducing reprocessing overhead and reinforcing downstream sales trajectories for suppliers active in the Mexican endoscopy devices market.

Geography Analysis

Concentration in Mexico City, Guadalajara, and Monterrey remains pronounced, with these metros housing every certified da Vinci proctor and most 4K visualization suites. Public and private tertiary hospitals in this corridor account for the bulk of robotic hysterectomies and complex GI work.

Border states such as Baja California and Chihuahua benefit from nearshoring of device manufacturing, including Intuitive Surgical’s Mexicali plant and Ambu’s gastroscope facility in Ciudad Juárez. Faster factory-to-facility supply lines shorten service intervals and can cushion tariff shocks on finished goods.

Secondary cities still lag due to workforce scarcity and tighter reimbursement. The national plan to open 31 new hospitals can shift the map if equipment budgets follow construction timelines. Vendor-led virtual training from Johnson & Johnson and Olympus aims to narrow skill gaps, a prerequisite for balanced regional growth across the Mexico endoscopy devices market.

Competitive Landscape

Olympus, KARL STORZ, Fujifilm, Medtronic, Intuitive Surgical, and Johnson & Johnson command the high-value tiers through ecosystem offers that combine imaging, energy, and data analytics. KARL STORZ’s OR1 integration across Star Médica underscores the stickiness of bundled deals, while Olympus secures back-end revenue with single-use energy disposables matched to its 4K towers.

Medtronic positions Hugo RAS as a lower-cost robotic alternative, courting ISSSTE and IMSS which seek to scale minimally invasive surgery without overextending capital budgets. Intuitive Surgical faces tariff exposure on Mexicali-produced accessories, although its entrenched installed base provides short-term insulation.

White-space opportunities lie in single-use scopes and capsule systems where adoption is still low. Ambu leverages domestic manufacturing to sidestep potential tariff costs, and Pentax Medical builds share through training partnerships in public institutes. Competitive depth therefore widens, but high service requirements keep the Mexico endoscopy devices market moderately consolidated.

Mexico Endoscopy Devices Industry Leaders

Olympus Corporation

Boston Scientific Corporation

Fujifilm Holdings

Karl Storz SE & Co. KG

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Mexico Bariatric Center opened Hospital AZAR in Tijuana, featuring dedicated endoscopy and fluoroscopy suites tailored to international patients.

- January 2024: Olympus Latin America showcased the EVIS X1 system to 150 healthcare professionals in Mexico City, highlighting TXI, RDI, BAI-MAC, and NBI capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, defines the Mexico endoscopy devices market as the sale value of new rigid, flexible, capsule, single-use, robot-assisted endoscopes, their operative systems (energy, insufflation, fluid management), and integrated visualization units that enter Mexican healthcare facilities for diagnostic or minimally invasive therapeutic procedures. The definition aligns with federal device listings under COFEPRIS and excludes refurbished equipment and disposable accessories sold separate from a complete endoscopic system.

Scope Exclusions: refurbished endoscopes, stand-alone imaging carts not bundled with an endoscope, and open-surgery cameras are outside this study.

Segmentation Overview

- By Device Type

- Endoscopes

- Rigid Endoscopes

- Flexible Endoscopes

- Capsule Endoscopes

- Robotic-assisted Endoscopes

- Endoscopic Operative Devices

- Irrigation / Suction Systems

- Access Devices

- Wound Protectors

- Other Endoscopic Operative Devices

- Visualization Equipment

- Endoscopes

- By Application

- Gastrointestinal Endoscopy

- Laparoscopy

- Pulmonology / Bronchoscopy

- ENT / Otolaryngology

- Urology

- Gynecology

- Cardiology

- Other Applications

- By Usability

- Reusable Devices

- Single-use / Disposable Devices

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed GI surgeons, pulmonologists, sterile processing managers, and leading distributors across Mexico City, Guadalajara, Monterrey, and border medical tourism hubs. The conversations verified annual procedure counts, adoption intent for single-use scopes, typical price erosion, and warranty structures, filling gaps left by desk research and letting us fine tune model drivers.

Desk Research

We compiled foundational inputs from open sources such as Secretaria de Salud hospital discharge files, INEGI foreign trade data on HS codes 9018 and 9011, Mexican Social Security Institute (IMSS) procurement bulletins, and clinical procedure volumes reported in Gaceta Medica. Trade publications and association portals, such as the Mexican Association of Endoscopic Surgery, OECD Health Statistics, and peer-reviewed papers in Revista de Gastroenterologia, helped us benchmark utilization patterns and average selling prices.

To enrich company-level intelligence, we drew on D&B Hoovers for manufacturer revenue splits, Dow Jones Factiva for local tender wins, and GlobalData's installed base snapshots for visualization towers. These sources are illustrative; many other references were reviewed to validate figures and clarify assumptions.

Market-Sizing & Forecasting

A top-down reconstruction starts with national GI, urology, and ENT procedure volumes, which are converted to device demand using prevalence-to-procedure ratios and replacement cycles; bottom-up checks, such as supplier roll-ups and sampled ASP times unit data, validate totals. Key variables include: (1) annual GI endoscopic procedures, (2) installed high-definition tower base, (3) public versus private bed additions, (4) average device price curves, and (5) peso to USD exchange trends. Multivariate regression, supplemented by scenario analysis for technology shifts, projects demand through 2030, while gaps in bottom-up data, such as small clinic purchases, are bridged using distributor share proxies discussed during interviews.

Data Validation & Update Cycle

Outputs pass variance checks against independent trade statistics and prior year hospital spend, after which a senior reviewer signs off. Reports refresh every twelve months, with interim revisions triggered by material events, such as device recalls, reimbursement resets, or peso shocks, so clients always receive a current view.

Why Mordor's Mexico Endoscopy Devices Baseline Is Dependable

Published market values often differ; scope choices, update cadence, and price assumptions typically create the gaps.

Key gap drivers here include whether visualization towers are counted, which procedure groups anchor demand, the year of currency conversion, and how aggressively learning curve price declines are modeled. Mordor's model reports the base case and refreshes annually, whereas some publishers freeze forecasts for longer intervals or rely mainly on global ratios adjusted downward for Latin America.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.96 B (2025) | Mordor Intelligence | - |

| USD 0.82 B (2024) | Regional Consultancy A | Narrower device scope and older currency baseline |

| USD 0.75 B (2024) | Trade Journal B | Uses global macro ratios; limited Mexican procedure data |

In short, our disciplined blend of verified clinical volumes, local pricing insight, and annual recalibration gives decision makers a transparent, balanced baseline they can retrace and stress test with confidence.

Key Questions Answered in the Report

How large is the Mexico endoscopy devices market in 2026?

It is valued at USD 1.04 billion and is on track to reach USD 1.55 billion by 2031.

What is the expected CAGR for Mexico endoscopy devices through 2031?

The market is projected to grow at 8.29% between 2026 and 2031.

Which device category is expanding fastest?

Endoscopic operative devices are forecast to grow the fastest, at an 8.62% CAGR.

Why is single-use adoption increasing in Mexico?

Updated infection-control guidelines and rising reprocessing costs are driving hospitals toward disposable options.

Which region has the highest concentration of advanced platforms?

Mexico City, Guadalajara, and Monterrey host most robotic systems and 4K visualization suites.

Page last updated on: