Mexico Diabetes Care Drugs And Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

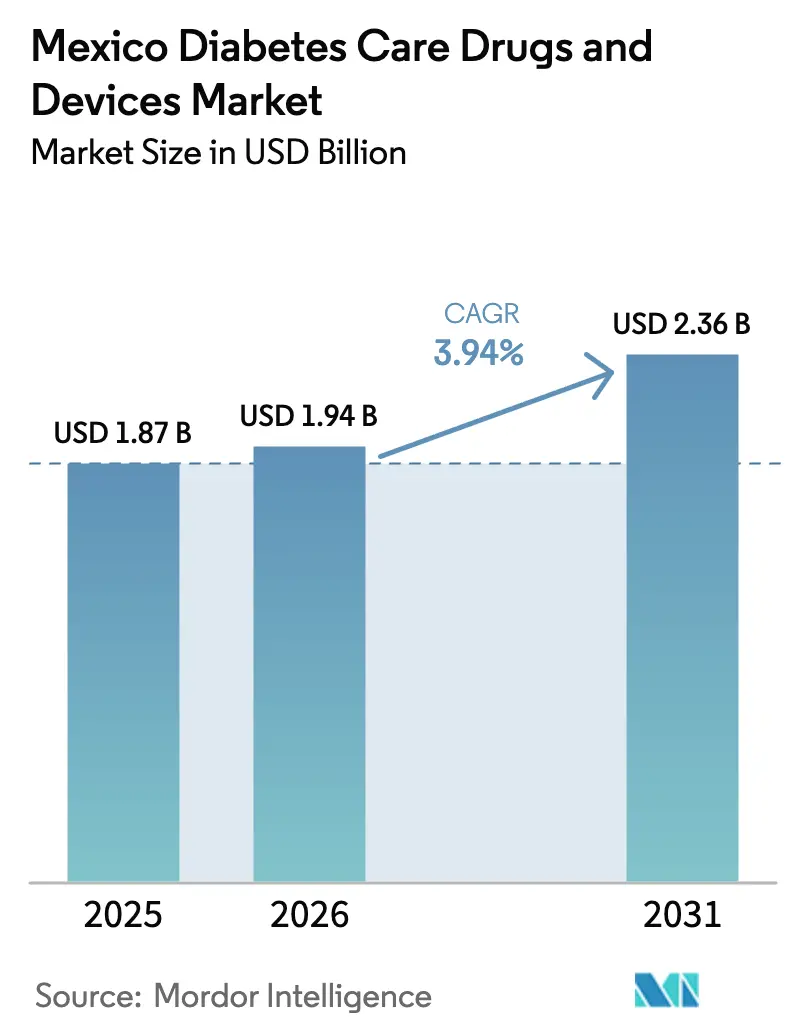

| Base Year Market Size (2025) | USD 1.87 Billion |

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Diabetes Care Drugs And Devices Market Analysis by Mordor Intelligence

The Mexico diabetes care drugs and devices market size was valued at USD 1.87 billion in 2025 and estimated to grow from USD 1.94 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 3.94% during the forecast period (2026-2031). Increasing life expectancy, rapid urbanization, and an obesity prevalence exceeding 75% among adults are expanding the patient pool, while President Claudia Sheinbaum’s bulk-procurement “Pharmacies for Well-being” program is lowering acquisition costs and reshaping competitive bidding. Once-weekly GLP-1 analogs, mobile-first continuous glucose monitoring (CGM) systems, and tele-endocrinology pilots are driving technology adoption across both private and public payers. Simpler patent clarification rules approved in February 2025 are expected to shorten regulatory review cycles for originator and generic products alike, which may widen treatment access once COFEPRIS clears its current backlog. In parallel, counterfeit GLP-1 injectables and uneven reimbursement for high-end insulin pumps continue to hinder uniform quality of care, especially outside major metropolitan areas.

Key Report Takeaways

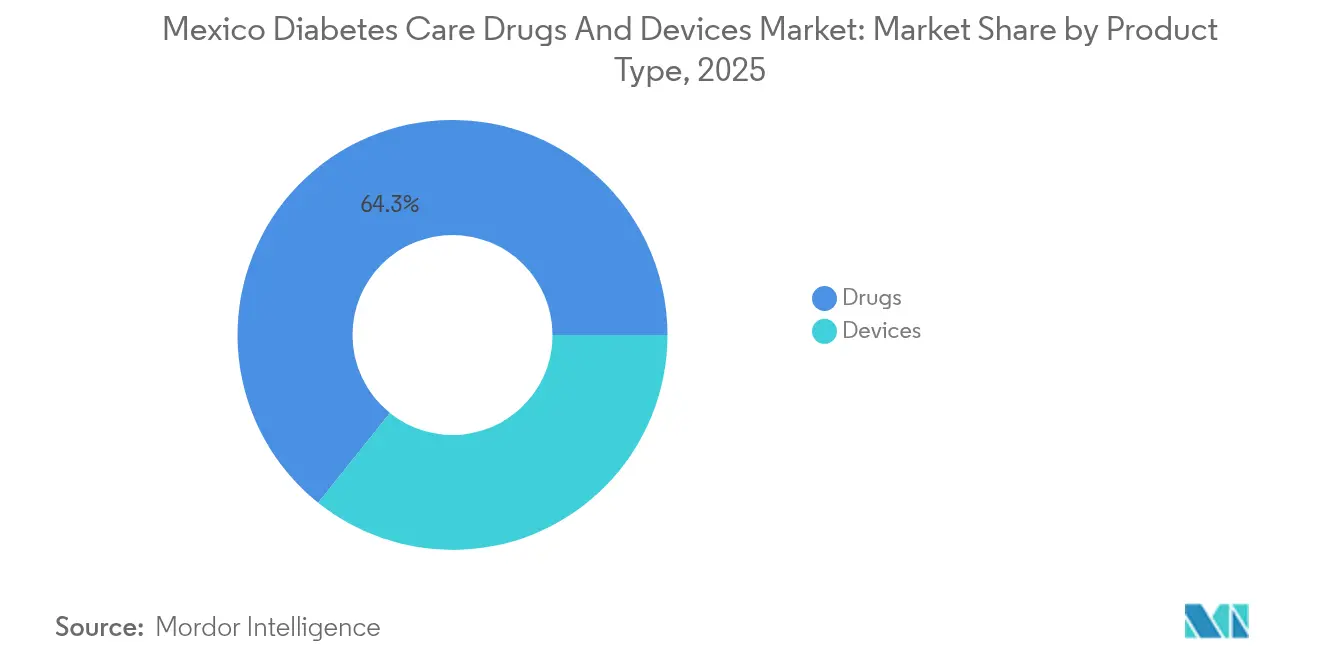

- By product type, drugs dominated with 64.25% of Mexico diabetes care drugs and devices market share in 2025, while devices are projected to register the fastest 4.76% CAGR through 2031.

- By diabetes type, type 2 diabetes accounted for 90.78% of Mexico diabetes care drugs and devices market size in 2025; type 1 diabetes is anticipated to expand at a 4.82% CAGR between 2026-2031.

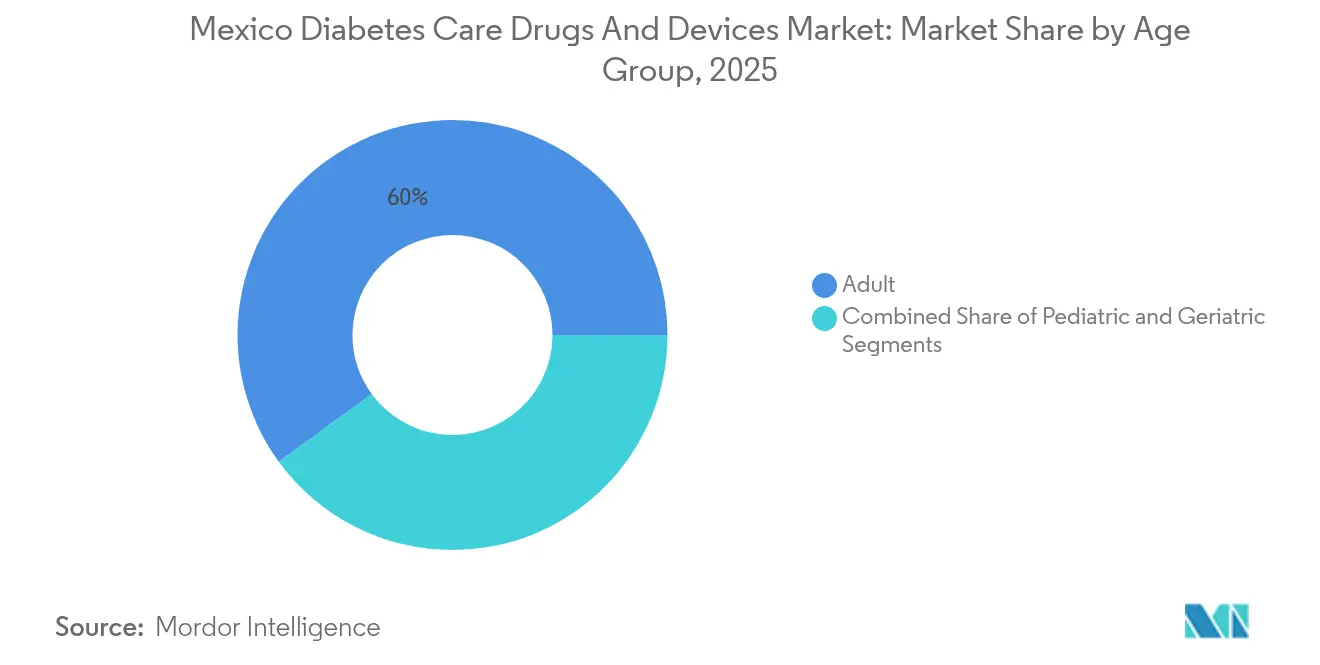

- By age group, adults held 60.03% revenue share of the Mexico diabetes care drugs and devices market in 2025, whereas the geriatric segment is positioned to grow at a 4.67% CAGR over the same period.

- By distribution channel, offline outlets retained 72.65% share of the Mexico diabetes care drugs and devices market size in 2025, but online sales are forecast to rise at a 4.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Diabetes Care Drugs And Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward once-weekly GLP-1 therapies | +1.2% | National, with early adoption in Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Mobile-first CGM adoption through public insurance apps | +0.8% | National, with rural state prioritization | Short term (≤ 2 years) |

| Government "Pharmacies for Well-being" bulk procurement | +0.7% | National coverage across 26 health institutions | Short term (≤ 2 years) |

| Rising prevalence of pre-diabetes in adolescents | +0.6% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Tele-endocrinology expansion in rural states | +0.5% | Rural Mexico, particularly southern states | Medium term (2-4 years) |

| Employer coverage race for anti-obesity injectables | +0.4% | Urban centers, multinational corporation hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Once-Weekly GLP-1 Therapies

Novo Nordisk’s launch of semaglutide 2.4 mg in April 2025 creates a dual-indication opportunity that addresses glycemic control and weight reduction in the same dosing schedule. Evidence from Spanish outpatient settings shows 77.1% of users achieving HbA1c targets below 7%, along with mean weight loss of 9.72 kg, standards now referenced by Mexican specialists. The simplified once-weekly regimen improves adherence compared with daily injections and aligns with employers’ interest in productivity gains, prompting large insurers to pilot formulary coverage in urban centers. COFEPRIS public advisories against unregulated semaglutide sales underscore official intent to secure supply integrity as demand accelerates.

Mobile-First CGM Adoption Through Public Insurance Apps

IMSS’s expansion of smartphone-based follow-up combined with Abbott’s Libre Rio and Lingo over-the-counter CGMs creates a direct-to-patient channel that sidesteps endocrinologist shortages in rural municipalities. The Dulce Wireless Tijuana study recorded HbA1c reductions of 3.0% after 6 months of text-messaging support and real-time glucose alerts. Roll-out across public insurance portals is expected to expand the Mexico diabetes care drugs and devices market by onboarding newly diagnosed patients into continuous monitoring without clinic visits.

Government “Pharmacies for Well-being” Bulk Procurement

The centralized tender covering 4,429 products across 26 institutions delivered MXN 30 billion (USD 1.5 billion) in savings and has locked in supply contracts through 2026. Price transparency pressures manufacturers to rebalance portfolios toward cost-effective formulations while guaranteeing baseline volumes. Free provision of essential diabetes drugs in low-income districts is projected to lift therapy initiation rates and deepen the Mexico diabetes care drugs and devices market.

Rising Prevalence of Pre-Diabetes in Adolescents

A national survey detected an 8.6% pre-diabetes rate among children aged 4-19, foreshadowing a surge in demand for pediatric diabetes management solutions. Community-based prevention programs have proven to boost insulin sensitivity and quality of life for Latino youth at 12-month follow-up, suggesting future market entrants could include child-friendly CGMs and family-centered coaching platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| COFEPRIS backlog delaying novel drug approvals | -0.9% | National regulatory bottleneck | Short term (≤ 2 years) |

| Counterfeit GLP-1 products in informal channels | -0.6% | Border regions and urban informal markets | Medium term (2-4 years) |

| Uneven reimbursement for advanced insulin pumps | -0.4% | Regional disparities across states | Long term (≥ 4 years) |

| Low endocrinologist density outside Mexico City | -0.3% | Rural and semi-urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

COFEPRIS Backlog Delaying Novel Drug Approvals

Average review times for complex biologics extend up to 18 months versus the statutory 30-day target, stalling patient access to next-generation insulins and GLP-1 combinations [1]RAPS, "Latin America Roundup: Mexico’s patent office, COFEPRIS sign agreement on drug patents," raps.org. A February 2025 memorandum between the patent office and COFEPRIS is meant to streamline dossier verification, yet near-term approvals remain vulnerable to resource constraints within the agency.

Counterfeit GLP-1 Products in Informal Channels

Pan-American monitoring detected 596 substandard or falsified medicine incidents during 2017-2018, many involving diabetes therapies. COFEPRIS shutdowns of seven unauthorized online pharmacies in 2024 illustrate the scope of digital risk. Persistent infiltration tends to erode clinician confidence in newer agents and can trigger abrupt product recalls that disrupt legal supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Drive Innovation Despite Drug Dominance

Devices generated a 4.76% CAGR outlook through 2031, even as drugs preserved 64.25% of Mexico diabetes care drugs and devices market share in 2025. Over-the-counter CGMs such as Abbott’s Libre Rio now retail in high-street pharmacies without prescriptions, expanding penetration beyond endocrinology clinics . Tandem Diabetes Care and Abbott signed a June 2025 agreement to co-develop sensors with ketone detection, responding to diabetic ketoacidosis prevention gaps . At the same time, once-weekly GLP-1 drugs continue to anchor revenue for the pharmaceutical segment, protected by semaglutide patents valid until at least 2031. The interplay of simplified monitoring and extended-release injectables is expected to lift adherence, reduce emergency admissions, and broaden total addressable demand in the Mexico diabetes care drugs and devices market.

Government bulk purchasing influences both categories. Essential insulin analogs are bundled with glucometers at negotiated caps, whereas advanced pumps remain outside standard formularies, relying on private out-of-pocket spend. Nevertheless, pilot reimbursement for continuous subcutaneous insulin infusion in IMSS clinics, evaluated at MXN 478,020 per QALY for HbA1c > 9% patients, shows incremental acceptance for high-cost hardware among severe cases. Consequently, the total Mexico diabetes care drugs and devices market size for devices could narrow the gap with drugs over the forecast window.

By Diabetes Type: Type 1 Growth Accelerates Through Technology Adoption

Type 2 conditions comprise 90.78% of Mexico diabetes care drugs and devices market size because of sheer prevalence, yet type 1 is projected to post a 4.82% CAGR through 2031. Telemedicine programs for type 1 patients in rural communities delivered cost savings of USD 72.94 per visit and maintained satisfaction similar to in-person endocrinology follow-up. Automated insulin delivery platforms integrated with FreeStyle Libre sensors minimize hypoglycemic episodes and reduce emergency department use, outcomes that are key for public insurers. Persistent gender gaps, however, show women recording higher diagnosis rates than men due to proactive antenatal screening and primary care attendance.

Type 2 management is transitioning from oral monotherapy to combination regimens that include GLP-1 or SGLT2 agents when HbA1c remains uncontrolled. Community-based education among Mayan populations achieved 60% metabolic control versus 35.4% prior baselines. These culturally tailored models are now being replicated in other indigenous regions, signalling that effective localized care can sustain market expansion for both drugs and devices in the Mexico diabetes care drugs and devices market.

By Age Group: Geriatric Acceleration Reflects Demographic Transition

Adults retained 60.03% of 2025 demand, but the cohort aged ≥ 65 is forecast to surge at 4.67% CAGR, raising new requirements for polypharmacy management and cognitive-friendly devices. Diabetes prevalence among individuals ≥ 50 years is projected to hit 34.0% by 2050. IMSS clinical protocols for frail seniors emphasize individual HbA1c targets to balance hypoglycemia risk with cardiovascular protection, providing guidelines for differentiated product labeling and training. Manufacturers are responding with larger-print CGM readers, simplified app dashboards, and pen injectors with audible dose clicks.

Pediatric pre-diabetes growth to 8.6% adds a second demographic tailwind. Family-centered CGM subscriptions bundle caregiver alerts and nutrition coaching, fostering early brand loyalty. As these cohorts age into chronic disease management, they will enlarge lifetime value potential for the Mexico diabetes care drugs and devices market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline networks still held 72.65% share of the Mexico diabetes care drugs and devices market in 2025 due to established pharmacy penetration and physician-directed dispensing. Yet online platforms are forecast for a 4.7% CAGR through 2031 as COFEPRIS certifies compliant e-pharmacies and links them with public insurance portals. Smartphone penetration above 90% in many rural municipalities means app-based refills can outpace bricks-and-mortar visits, particularly when combined with teleconsultation vouchers. Pilot projects under the MIDO screening program now route newly diagnosed patients to digital onboarding, where algorithmic reminders nudge medication adherence and enable one-click CGM reorders.

Large retail chains are adopting omnichannel models. Customers can initiate orders online and pick up temperature-sensitive GLP-1 injectables at accredited cold-chain counters inside physical stores. This hybrid strategy mitigates last-mile logistics challenges and addresses counterfeit worries by ensuring visible chain-of-custody. As a result, distribution innovation is likely to lift total Mexico diabetes care drugs and devices market share for online channels without cannibalizing essential in-clinic counseling roles.

Geography Analysis

Mexico City, Guadalajara, and Monterrey anchor specialist care hubs, concentrating endocrinologists, private hospitals, and trial sites for advanced therapeutics. Patients in these metros benefit from same-day CGM sensor replacement and bundled weight-loss programs, accelerating uptake in the Mexico diabetes care drugs and devices market. Border cities such as Tijuana add medical-tourism inflows and host crossover studies like Dulce Wireless, which validate mobile care models before national roll-out.

Southern states, many with significant indigenous populations, historically lag in effective coverage, yet IMSS-Bienestar now directs incremental budget lines to 19 states serving 10.8 million uninsured citizens. Culturally adapted peer-education lowered HbA1c by 1.3 percentage points in pilot Mayan communities, demonstrating the role of language-appropriate curricula. Adoption of cloud-based data platforms lets those clinics transmit glucose stats to urban specialists for asynchronous consultation, mitigating physician shortages.

Rural regions face logistics hurdles, from road connectivity to cold-chain integrity, which makes once-weekly injectables and low-maintenance CGMs particularly suitable. Drone-assisted last-mile pilots are under feasibility review to reduce stock-out days for insulin vials. Together, differential regional strategies contribute to balanced volume growth and strengthen the Mexico diabetes care drugs and devices market across diverse geographies.

Competitive Landscape

Market concentration is fragmented, with global multinationals leading but domestic generics firms capturing volume contracts under government tenders. Abbott and Medtronic’s alliance to integrate FreeStyle Libre with automated insulin delivery sets a benchmark for platform ecosystems. Novo Nordisk defends its GLP-1 franchise with patent cover until 2031 while concurrently pursuing price-volume negotiations to lock in formulary positions.

Local players leverage fast-track COFEPRIS listings for metformin, gliclazide, and basal insulin biosimilars, supplying “Pharmacies for Well-being” at scale. Bayer’s Lerma expansion injects MXN 1.1 billion into finished-dose capacity, positioning Mexico as a regional export base. Takeda’s new Innovation Capability Center focuses on digital patient-support services, reflecting the pivot toward data-driven adherence.

Competitive intensity also stems from start-ups delivering AI-powered diet apps and connected glucometers aimed at underserved semi-urban customers. If post-2025 patent reforms accelerate biosimilar GLP-1 entries, branded manufacturers may respond with value-added service bundles rather than price concessions. Overall, technology convergence and procurement centralization will push firms to differentiate on integration, affordability, and population-health partnerships within the Mexico diabetes care drugs and devices market.

Mexico Diabetes Care Drugs And Devices Industry Leaders

-

Medtronics

-

Roche

-

Sanofi

-

NovoNordisk

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mexico’s patent office and COFEPRIS agreed on a joint framework to clarify pharmaceutical patent status and accelerate regulatory approvals.

- January 2025: Mexican Ministry of Health secured essential medicines and medical supplies for the 2025-2026 cycle, achieving 97.6% procurement coverage and MXN 30 billion (USD 1.5 billion) in savings.

- January 2025: Bayer announced a MXN 1.1 billion (USD 55 million) expansion of its Lerma manufacturing plant to serve Latin American and North American markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Mexico diabetes care drugs and devices market as all prescription antidiabetic medicines, including insulin analogs, human insulin, oral agents, and non-insulin injectables, as well as patient-use hardware such as glucometers, test strips, lancets, continuous glucose monitoring (CGM) sensors, insulin pens, pumps, and associated disposables that reach the Mexican end user through retail, hospital, or reimbursement channels.

Scope Exclusions: Veterinary formulations, research-only reagents, and standalone laboratory HbA1c analyzers remain outside our remit.

Segmentation Overview

-

By Product Type

-

Devices

-

Monitoring Devices

- Self-Monitoring Blood Glucose Meters

- Continuous Glucose Monitoring Systems

- Management Devices

-

Monitoring Devices

-

Drugs

- Oral Anti-Diabetic Drugs

- Insulin Drugs

- Non-Insulin Injectables

- Combination Drugs

-

Devices

-

By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

-

By Age Group

- Adult

- Geriatric

- Pediatric

-

By Distribution Channel

- Offline

- Online

Detailed Research Methodology and Data Validation

Primary Research

Our team spoke with endocrinologists in Mexico City and Monterrey, state-level procurement officers, leading pharmacy chains, and two CGM distributors; their insights filled data gaps on therapy adherence, channel mark-ups, and regional uptake of once-weekly GLP-1 drugs, helping us refine key assumptions.

Desk Research

We began with public datasets from the Ministry of Health's SINAVE registry, COFEPRIS device import notices, the National Health and Nutrition Survey, International Diabetes Federation Atlas, and OECD Health Statistics, which together outline prevalence, treatment coverage, reimbursement rules, and trade flows. Company filings, investor presentations, and press releases added shipment trends, while paid access to D&B Hoovers and Dow Jones Factiva helped us benchmark corporate revenue and news triggers. The sources listed illustrate, but do not exhaust, the wider literature we reviewed.

Market-Sizing & Forecasting

We first reconstructed demand using a top-down prevalence-to-treated-cohort build that multiplies the diagnosed adult population by drug-class penetration and average yearly spend; then we mirrored that for devices through user pools and replacement cycles. Selective bottom-up checks, including supplier roll-ups and sampled average selling price multiplied by volume for high-weight segments, validated totals and guided adjustments. Variables such as obesity-adjusted prevalence growth, public formulary expansion, CGM sensor change frequency, insulin analog price erosion, and peso-USD exchange swings feed a multivariate regression that projects values to 2030. Gaps in granular distributor data were bridged using nearest-neighbor proxies from customs records and confirmed during expert follow-ups.

Data Validation & Update Cycle

Outputs pass variance and anomaly screens, after which a senior analyst reviews every figure. Models refresh annually, and we trigger interim updates when regulatory shifts, currency shocks, or product launches materially alter assumptions.

Why Our Mexico Diabetes Drugs And Devices Baseline Commands Reliability

Published numbers often diverge because firms pick different product baskets, patient cohorts, and forecast levers.

Key gap drivers include some studies that fold bariatric procedures and clinical lab equipment into market value; others quote aggressive uptake curves for premium CGM systems; a few use global ASPs without peso conversion. Mordor Intelligence maintains a narrower, therapy-specific scope, refreshes inputs yearly, and calibrates adoption rates against physician survey feedback.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.87 B (2025) | Mordor Intelligence | - |

| USD 3.92 B (2025) | Regional Consultancy A | Bundles bariatric devices and hospital lab analyzers into total |

| USD 1.20 B (2024) | Global Consultancy B | Excludes non-insulin injectables and CGM consumables |

| USD 0.46 B (2023) | Industry Journal C | Reports devices only, omits drug revenues entirely |

Taken together, the comparison shows that when scope and currency choices shift, figures swing widely; our disciplined variable selection and transparent update cadence give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the Mexico diabetes care drugs and devices market size in 2026?

The market is valued at USD 1.94 billion in 2026.

What compound annual growth rate (CAGR) is projected for 2026-2031?

The overall market is forecast to grow at a 3.94% CAGR through 2031.

Which product segment is expected to expand the fastest?

Devices are projected to post the highest 4.76% CAGR, driven by wider continuous glucose-monitoring adoption.

How will the “Pharmacies for Well-being” program affect the market?

By centralizing procurement and saving MXN 30 billion (USD 1.5 billion), the program improves medicine availability and pressures suppliers to offer competitive pricing, boosting overall treatment uptake.

Why are once-weekly GLP-1 therapies gaining traction in Mexico?

They improve adherence, deliver proven HbA1c and weight-loss outcomes, and address the country’s overlapping diabetes-obesity burden.

What key challenge does counterfeit medicine pose?

Substandard and falsified GLP-1 products circulating in informal and online channels threaten patient safety and can disrupt legitimate supply chains.

Page last updated on: