Mexico Data Center Physical Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

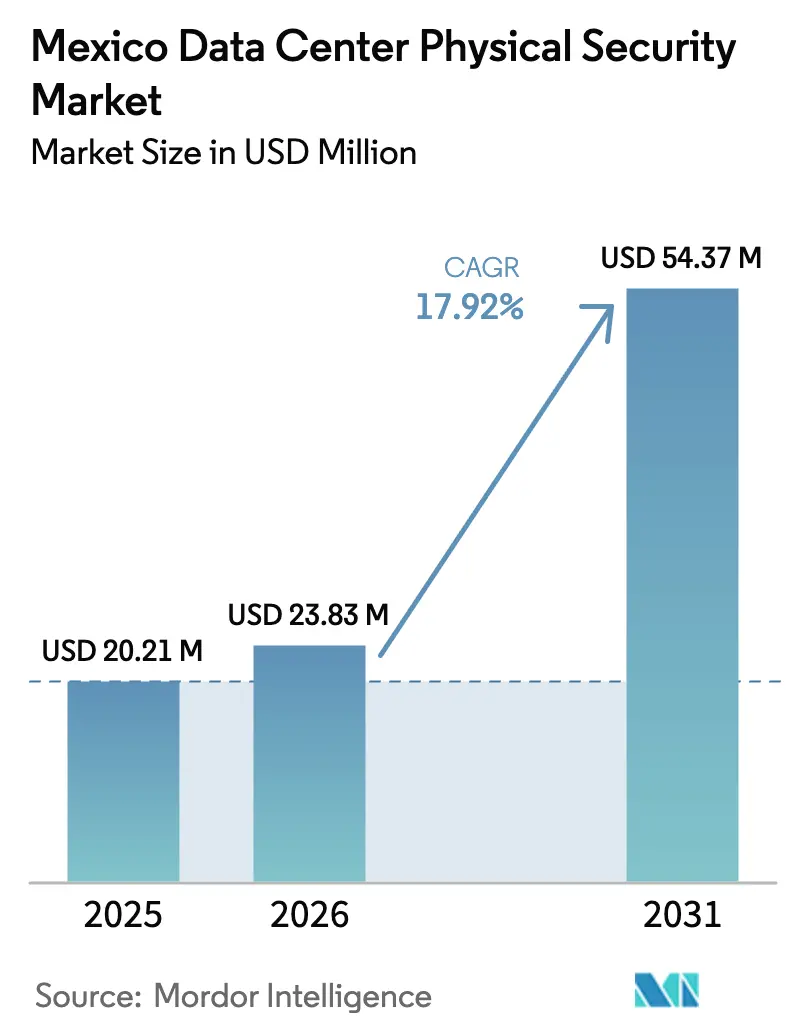

| Base Year Market Size (2025) | USD 20.21 Million |

| Market Size (2026) | USD 23.83 Million |

| Market Size (2031) | USD 54.37 Million |

| Growth Rate (2026 - 2031) | 17.92% CAGR |

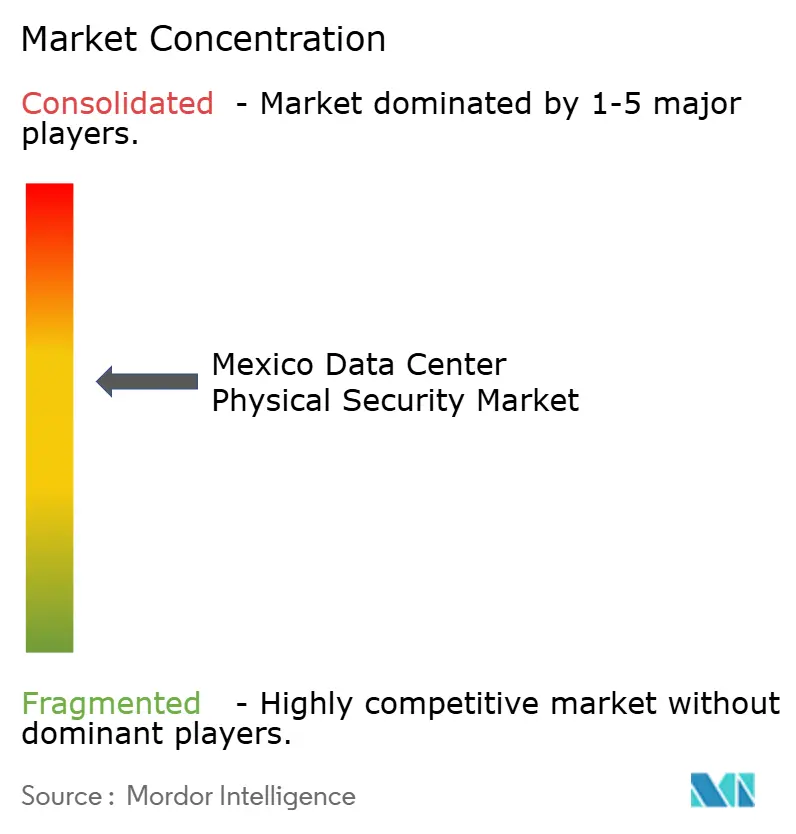

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Data Center Physical Security Market Analysis by Mordor Intelligence

The Mexico data center physical security market size was valued at USD 20.21 million in 2025 and estimated to grow from USD 23.83 million in 2026 to reach USD 54.37 million by 2031, at a CAGR of 17.92% during the forecast period (2026-2031). This pace reflects the country’s rapid elevation from regional provider to continental hub as near-shoring injects unprecedented capital into digital infrastructure. Hyperscale announcements from AWS, Microsoft, and Google Cloud are redefining security standards, while Tier III and Tier IV builds dominate new capacity decisions. Compliance pressures stemming from Mexico’s rewritten data-protection regime are pushing operators toward integrated, audit-ready platforms. Simultaneously, falling lithium-ion UPS prices and AI-enabled video analytics are freeing budgets for advanced defenses, creating a virtuous cycle of upgrade spending. Power-availability risks around Querétaro are beginning to redirect investment toward San Miguel de Allende and San Luis Potosí, forcing vendors to support multi-site security rollouts that span urban and semi-rural footprints.

Key Report Takeaways

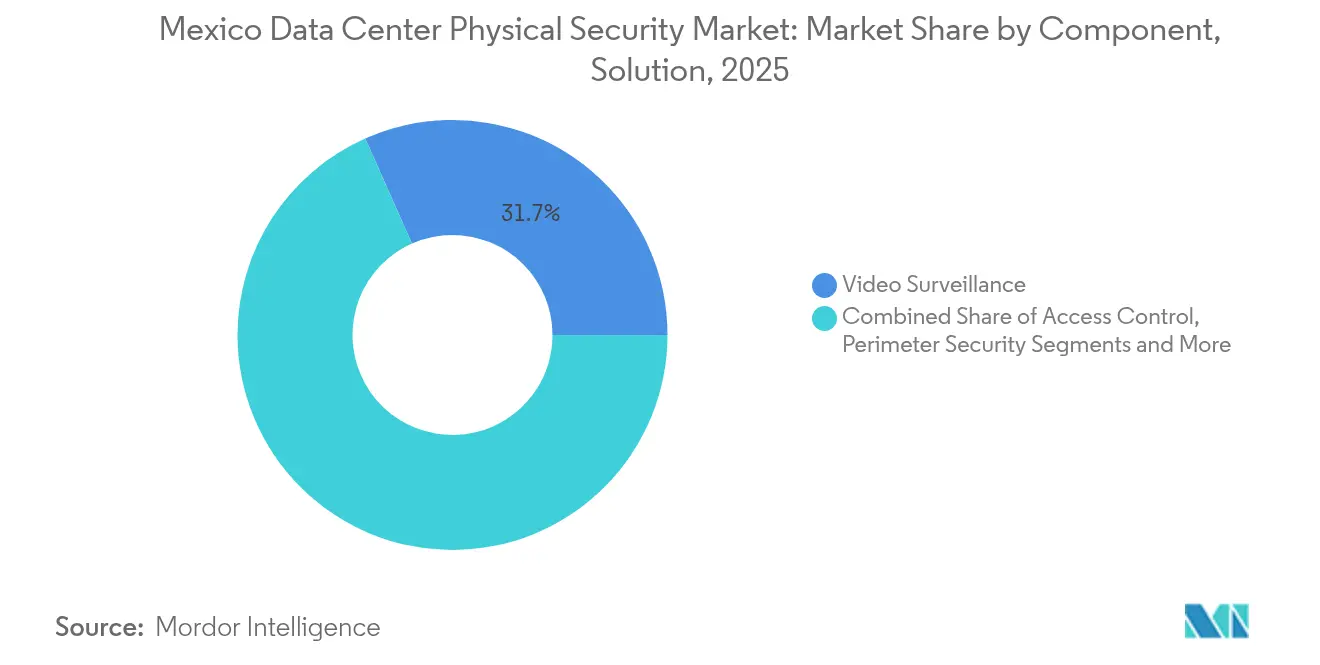

- By solution type, video surveillance led with 31.65% of Mexico data center physical security market share in 2025, while access control systems are expanding at 19.05% CAGR through 2031.

- By data-center tier, Tier III facilities commanded 56.65% of the Mexico data center physical security market size in 2025; Tier IV sites are set to grow at a 19.78% CAGR to 2031.

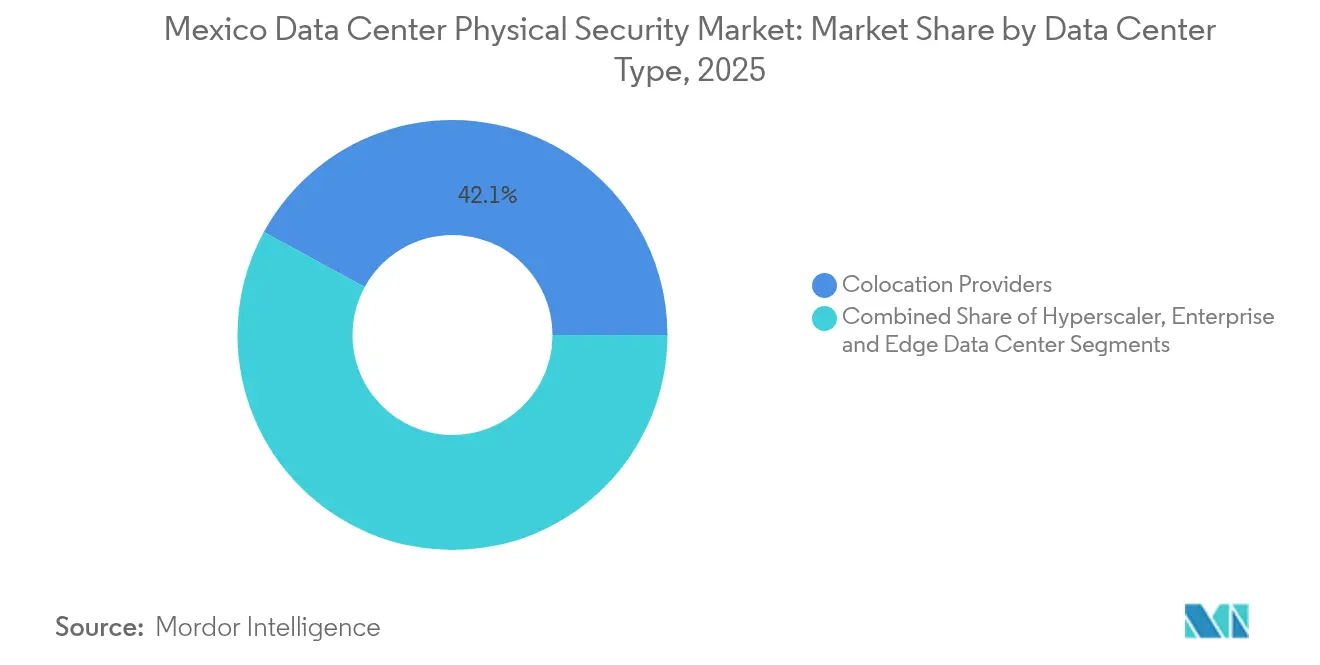

- By data-center type, colocation providers accounted for 42.05% of the Mexico data center physical security market size in 2025, yet hyperscaler deployments are advancing fastest at 19.45% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico represents one dimension of a structure that spans multiple countries, continents and economic zones. Our global data center physical security market report covers details on that full structure.

Mexico Data Center Physical Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-computing boom fuels hyperscale builds | +4.2% | National, concentrated in Querétaro-CDMX corridor | Medium term (2-4 years) |

| Tightening compliance with Mexico's Personal Data Protection Law | +3.1% | National, with enhanced focus on financial services hubs | Short term (≤ 2 years) |

| Surge in near-shoring boosts colocation and edge sites | +3.8% | Northern border states and central manufacturing zones | Medium term (2-4 years) |

| Falling Li-ion UPS prices free budget for security upgrades | +2.1% | National, with greater impact on Tier III+ facilities | Short term (≤ 2 years) |

| AI-driven video analytics slash OPEX for large campuses | +2.4% | Major metropolitan areas with large-scale deployments | Long term (≥ 4 years) |

| Rapid deployment of 5G networks spawns edge micro-data centers | +2.6% | Urban centers and industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Video Surveillance Holds the Largest Market Share

Hyperscale projects are redefining the Mexico data center physical security market. AWS’s USD 5 billion commitment triggered competitive responses, accelerating a wave of 100-MW-plus campuses that rely on biometrics, multi-factor portals and AI surveillance to protect high-density racks. Microsoft’s Colón facility highlights this architectural shift; water-cooled halls require extra monitoring of pipes and pumps, merging environmental and intrusion sensors within the same dashboard. Vendors that present unified, zero-trust-ready platforms are now appearing on every hyperscaler bid list, positioning themselves to capture multi-site rollouts across the 2025-2030 horizon.

Tightening compliance with Mexico's Personal Data Protection Law

March 2025 reforms dissolved INAI and placed oversight under the Ministry of Anti-Corruption and Good Governance, raising the compliance bar for physical access, evidence retention, and audit trails. Banco de México’s Regulation 4/2016 already obliges payment facilities to log every ingress event, keep video for 90 days, and run quarterly drills. [1]Banco de México, “Reglamento 4/2016 Physical Security Controls,” Banco de México, banxico.org.mx Financial operators pivoted quickly: Nubank unified on-premise doors and cloud logs into one policy engine, trimming audit prep time by 30%. Such examples reinforce demand for modular platforms that can map evolving ministerial decrees onto existing hardware through firmware updates instead of forklift swaps

Surge in near-shoring boosts colocation and edge sites

Automotive, electronics, and fintech firms relocating functions from Asia now insist on low-latency compute within Mexico’s industrial belts. American Tower’s edge partnership with IBM shows how unmanned 250 kW pods can anchor real-time factory analytics while maintaining centralized lock-state telemetry. [2]American Tower Corporation, “American Tower and IBM extend edge partnership,” American Tower, americantower.com.These micro-sites amplify surface area, turning vandal-resistant housings, vibration sensors, and remote video diagnostics into high-volume procurement lines. Security integrators able to preconfigure kits for rooftop, warehouse, and cell-tower environments sit at an advantage as near-shoring momentum persists.

AI-driven video analytics slash OPEX for large campuses

False-alarm reductions of up to 90% unlock staffing savings; Johnson Controls’ pilot in Nuevo León re-deployed six guards to higher-value tasks after algorithmic analytics filtered wildlife and weather triggers. [3]Johnson Controls, “Physical security in hyperscale facilities,” Johnson Controls, johnsoncontrols.comRobots integrated with these analytics patrol service roads, extending coverage and capturing 360° feeds that feed the same AI engine, an approach increasingly written into RFPs for sites over 20 MW.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for multi-layered security infrastructure | -2.8% | National, with greater impact on smaller operators | Short term (≤ 2 years) |

| Shortage of certified security-cleared technicians | -1.9% | National, particularly acute in northern industrial zones | Medium term (2-4 years) |

| Peso volatility inflates imported hardware costs | -1.4% | National, with regional variations based on import dependencies | Short term (≤ 2 years) |

| Rising land and real-estate prices in Central Mexico corridor | -1.1% | Querétaro-CDMX corridor and major metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for multi-layered security infrastructure

Comprehensive defenses can top 15% of build cost as operators incorporate dual-factor airlocks, seismic sensors, and ISO-rated vault partitions. For a 5 MW edge build, that equates to USD 2 million in upfront spend, a hurdle that forces smaller firms toward leasing or managed-service contracts whose premiums erode operating margins. Banco de México rules further inflate the cost by demanding quarterly third-party audits, each priced at USD 25,000–40,000.

Shortage of certified security-cleared technicians

Industry associations estimate 15,000 additional roles by 2026 against a pipeline of 4,000 graduates, placing upward wage pressure of 8-10% annually. Specialists able to calibrate AI analytics or integrate biometric databases routinely command 30% premiums, delaying go-live dates and inflating TCO. Remote commissioning and robot-assisted maintenance partially offset the gap, but still need initial human configuration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Video surveillance retains scale while access control accelerates

Video surveillance captured 31.65% of the 2025 spend within the Mexico data center physical security market. This dominance stems from mature ecosystems of IP cameras, VMS software, and analytics that slot into existing command centers. That share translates into a Mexico data center physical security market size of USD 6.4 million in 2025, rising at an 10.84% CAGR. Access control’s 19.05% CAGR, however, signals a pivot toward proactive mitigation. Banco de México clauses and hyperscaler zero-trust models push biometric readers, mobile credentials, and encryption-backed door controllers onto every new rack row. Operators employ unified dashboards that marry video with door events so anomalies trigger real-time cross-checks.

Growth of access control is highest in BFSI complexes, where risk assessments show up to 60% of breaches originate from credential misuse. SALTO’s mobile-credential suite cuts issuance times by 40%, demonstrating real-world ROI for converged badge-plus-phone scenarios. Video vendors now embed ONVIF-based door status overlays, illustrating how convergence defines the next wave of procurement decisions in the Mexico data center physical security market.

By Data-Center Tier: Tier III anchors spend while Tier IV races ahead

Tier III sites held 56.65% of 2025 outlays. Their resilience profile meets most enterprise SLAs without the double-fault redundancy that inflates Tier IV builds. Tier IV campuses, though smaller in absolute numbers, are sprinting at 19.78% CAGR on the back of hyperscale multi-building precincts. ODATA’s 400 MW Querétaro campus embodies this leap, specifying duplicate perimeter rings and dual command centers that can swap roles during maintenance.

Tier IV rollouts intertwine security with uptime: guardhouses possess failover generators and redundant fiber to prevent a security blackout from triggering SLA penalties. Such design thinking migrates downstream as regulators weigh codifying minimum dual-path video links for Tier III upgrades, foreshadowing further spend inside the Mexico data center physical security market.

By Data-Center Type: Colocation still leading while hyperscalers surge

Colocation players controlled 42.05% of 2025 revenue, equal to a Mexico data center physical security market share. Their multitenant model requires granular segmentation of cages, mantraps, and cameras to satisfy each customer's audit. Hyperscaler builds, however, are growing 19.45% CAGR as global clouds plant availability-zone triangles across the country. Security specs for these sites call for five-factor identity checks, AI perimeter drones and cryptographically signed visitor passes—technologies cascading down into enterprise RFPs and propelling overall sophistication of the Mexico data center physical security industry.

Enterprise facilities and emerging 5G edge nodes round out demand, adopting “lite” versions of cloud blueprints. Vendors winning hyperscale contracts often re-package the same firmware stacks for SMEs, expanding TAM without additional engineering.

Geography Analysis

Central Mexico’s CDMX-Querétaro corridor accounted for major share of 2025 spending, anchored by dense fiber, skilled labor and tax incentives. Yet grid constraints have stretched lead times for new power feeds beyond 24 months, nudging projects north to San Luis Potosí and east toward Guanajuato. Northern border states such as Nuevo León and Baja California are expanding at 21.4% CAGR through 2031, fueled by automotive and electronics near-shoring that demands sub-10 ms latency to U.S. ERP backbones. Security architectures here emphasize modular, pre-cabled solutions that can be installed during plant re-tooling shutdowns measured in days, not months. Southern and coastal geographies including Jalisco and Yucatán trail in absolute volumes but post 15-17% CAGR. Their attraction lies in disaster-resilient topography and submarine-cable landings that position them as redundancy nodes for multinational DR strategies. Government digitization programs further spur localized micro-data-centers that must integrate hurricane-rated enclosures with facial-recognition kiosks for citizen-service counters. Geographic diversification therefore obliges integrators to master climatic variation—from high-altitude dust-proof housings in Toluca to corrosion-resistant casings in Mérida—driving a wide parts catalogue inside the Mexico data center physical security market.

Mordor Intelligence tracks the global data center physical security market across other major regions such as Africa, South America, and Europe, with additional country-level coverage spanning United States, Brazil, Nigeria, Sweden, Netherlands, and Saudi Arabia, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competition is moderate, with no single vendor owning more than 15% share. Johnson Controls, Honeywell, Bosch, Axis, Cisco, Schneider Electric, Siemens, Genetec, Milestone and ASSA ABLOY comprise the core slate, each coupling hardware breadth with open APIs. Recent bid trends favor platform vendors able to merge physical events with SIEM feeds, a capability Johnson Controls illustrates through its OpenBlue suite that binds video, biometrics and environment telemetry into one data lake. Genetec and Milestone differentiate via software-only stacks that integrate third-party cameras, appealing to cost-sensitive colocation operators.

Innovation pockets focus on AI analytics and post-quantum credentialing. Dormakaba’s stake in Safetrust brings crypto-agile readers to market in 2025, a move echoing hyperscaler concerns about quantum-era replay attacks. Regionally, KIO Networks and ODATA collaborate with local integrators to tailor global gear for Mexican electrical codes and seismic ratings. Managed-service propositions also grow: security-as-a-service models spread CAPEX over five-year terms, bundling hardware swaps and firmware patches. Customers weigh these offers against data-sovereignty anxieties, suggesting hybrid models—hardware owned on-prem, analytics licenced from the cloud—will dominate mid-term procurement across the Mexico data center physical security industry

Mexico Data Center Physical Security Industry Leaders

Johnson Controls

Honeywell International Inc.

Bosch Building Technologies

Axis Communications AB

Securitas Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ODATA inaugurated Latin America’s largest data-center campus in Querétaro with USD 3 billion investment and 400 MW IT capacity, integrating Delta Cube cooling and tiered physical security

- March 2025: Mexico dissolved INAI and transferred data-protection oversight to the Ministry of Anti-Corruption and Good Governance, tightening audit obligations for operators.

- February 2025: Dormakaba invested in Safetrust to advance post-quantum identity readers ahead of ISC West 2025

- February 2025: AWS confirmed USD 5 billion for a new Mexican cloud region, accelerating hyperscale security demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Mexico data-center physical security market as all capital and service spending on hardware, software, and managed tasks deployed to deter, detect, or delay unauthorized physical access at colocation, enterprise, edge, and hyperscale facilities within Mexican territory. Covered items include perimeter fencing, video-surveillance cameras, intrusion alarms, biometric or card readers, mantraps, patrol-automation software, and fire or environmental devices that directly shield IT halls and supporting infrastructure; only new installations, upgrades, and linked service contracts are counted.

Scope exclusion: pure cyber or network controls and generic building-management systems lie outside this boundary.

Segmentation Overview

- By Component

- By Solution Type

- Video Surveillance

- Access Control

- Perimeter Security (Mantraps, Fences, Bollards)

- Intrusion Detection and Monitoring

- Environmental and Fire Safety Systems

- By Service Type

- Consulting

- Integration and Deployment

- Maintenance and Managed Services

- By Solution Type

- By Data-center Tier

- Tier I and II

- Tier III

- Tier IV

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and short surveys with facility managers, regional integrators, component distributors, and underwriting specialists across central and northern states let us validate camera-to-rack ratios, Tier IV mantrap premiums, and the adoption speed of AI analytics.

Desk Research

We began with open datasets from Mexico's Secretariat of Infrastructure, Communications and Transport and INEGI, then mined quarterly customs filings that map HS codes for CCTV and access-control gear. Next, we layered insights from National Telecommunications Industry Chamber journals, listed colocation operators' annual reports, and trade articles on ALAS Seguridad to trace installed-base shifts and pricing norms.

Paid resources such as D&B Hoovers, Dow Jones Factiva, and Volza added supplier revenue trails and shipment counts. These examples illustrate, not exhaust, the secondary sources consulted.

Market-Sizing & Forecasting

A top-down model converts announced power-capacity and floor-space additions into a demand pool, multiplies it by average security spend per square meter by tier, and cross-checks results through a selective bottom-up roll-up of supplier billings and sampled ASP × volume data. Key variables like hyperscale megawatt additions, INAI compliance deadlines, lithium-ion UPS cost curves, and on-prem workload shifts feed a multivariate regression for 2025-2030 projections. Interview-based ratios bridge any gaps in bottom-up inputs.

Data Validation & Update Cycle

Before sign-off, Mordor analysts run variance checks against import volumes, insurer loss-history data, and integrator backlogs, followed by a three-layer peer review. Models refresh annually, with interim updates triggered by major campus announcements or regulatory moves, ensuring clients receive the latest view.

Why Mordor's Mexico Data Center Physical Security Baseline Commands Reliability

Published estimates often diverge because scopes, price decks, and refresh rhythms vary.

Our disciplined inclusion of only proven physical-layer controls and yearly recalibration gives planners a dependable baseline. Key gap drivers elsewhere include mixed-in logical defenses, blanket Tier IV assumptions, and single-source price averages lacking duty adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.21 million (2025) | Mordor Intelligence | - |

| USD 18.24 million (2024) | Regional Consultancy A | Omits integration and maintenance contracts; relies on one customs snapshot |

| USD 30.0 million (2024) | Global Consultancy B | Bundles cyber controls and retrofits beyond formal data centers |

These contrasts show that Mordor's scoped variables, dual-path modeling, and timely updates yield a transparent, traceable figure clients can audit with confidence.

Key Questions Answered in the Report

What is the current size of the Mexico data center physical security market?

The market is valued at USD 23.83 million in 2026 and is projected to reach USD 54.37 million by 2031.

Which solution type holds the largest share?

Video surveillance leads with 31.65% of 2025 revenue, yet access control shows the fastest CAGR at 19.05%.

Why are Tier IV facilities growing so quickly?

Hyperscale cloud deployments and financial-services compliance demand the highest uptime, propelling Tier IV sites at 19.78% CAGR.

How do new data-protection laws affect security spending?

The March 2025 legal overhaul intensified audit requirements, driving immediate investment in unified logging, biometrics and video retention.

Page last updated on: