Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 315.72 Million |

| Market Size (2026) | USD 367.44 Million |

| Market Size (2031) | USD 783.9 Million |

| Growth Rate (2026 - 2031) | 16.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Vertical Farming Market Analysis by Mordor Intelligence

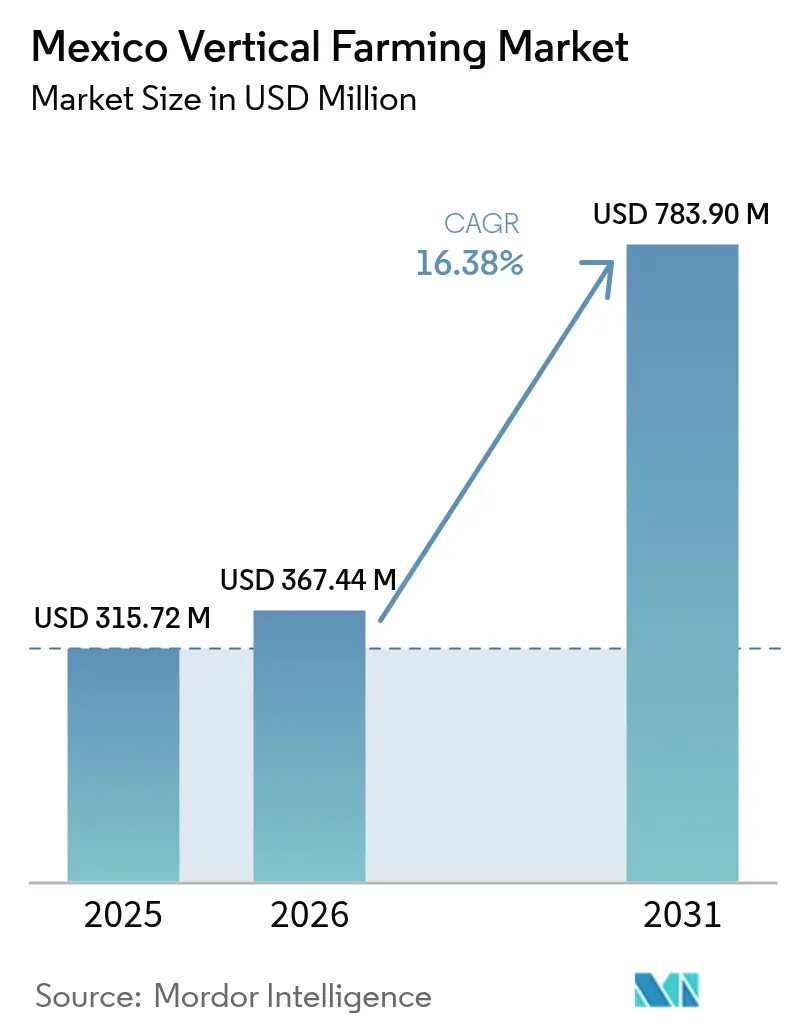

The Mexico vertical farming market size is expected to grow from USD 315.72 million in 2025 to USD 367.44 million in 2026 and is forecast to reach USD 783.9 million by 2031 at 16.38% CAGR over 2026-2031. The market is expanding due to the need for advanced agricultural solutions to address food security, urbanization, and environmental sustainability challenges. According to World Bank data, Mexico's urbanization rate increased from 80.4% in 2019 to 81.5% in 2023, contributing to a steady reduction in arable land. Water scarcity, government food sovereignty policies, and increasing agricultural technology adoption drive the Mexico vertical farming market growth, while improved LED efficiency and mobile containerized farms create new urban opportunities. Government support through the Ministry of Agriculture and Rural Development (SADER), technology incentives, and the National Water Commission (CONAGUA) Mexico Hydric Plan encourage farmers to adopt water-efficient systems. Public-private partnerships facilitate investment in controlled-environment projects that deliver consistent year-round produce yields. Despite challenges such as imported automation equipment delays, workforce skill gaps, and high initial investments, the transition to data-driven cultivation continues. The market's growth fundamentals, supportive regulations, and advancing technology indicate sustained double-digit growth rates through 2030.

Key Report Takeaways

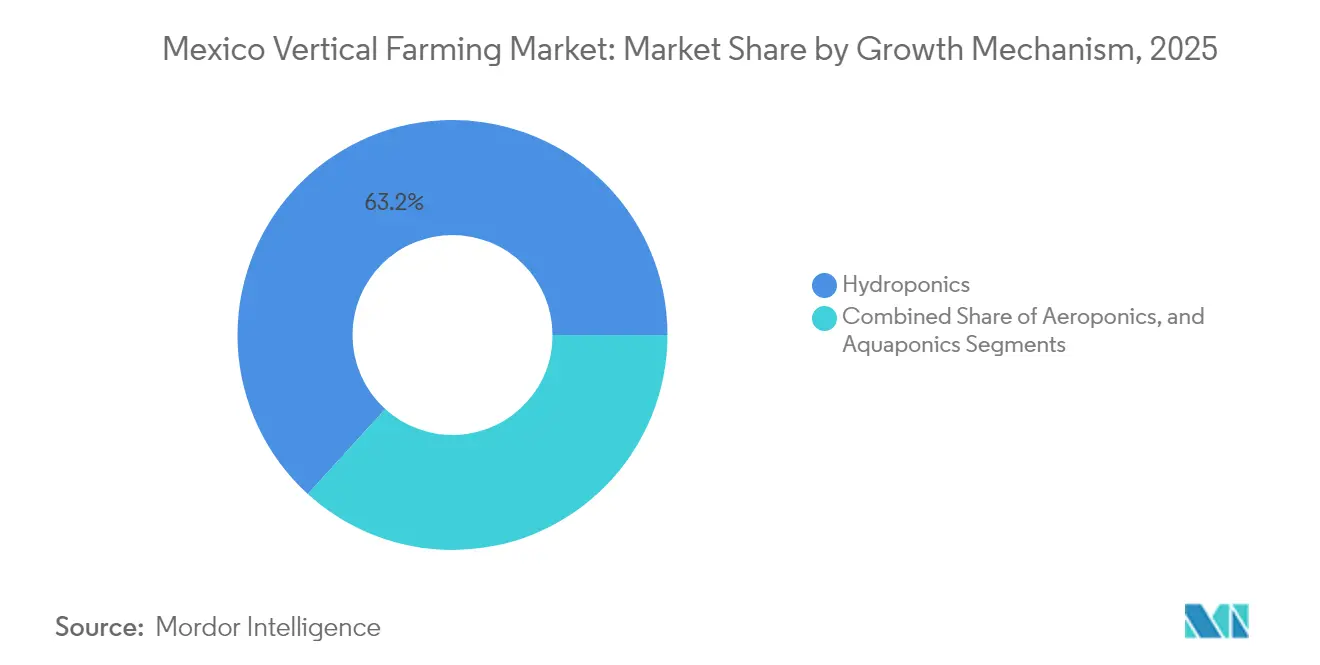

- By growth mechanism, hydroponics led with 63.25% of the Mexico vertical farming market share in 2025, whereas aeroponics is projected to grow fastest at 17.12% CAGR through 2031.

- By structure, building-based vertical farms captured 55.62% of the Mexico vertical farming market size in 2025, while shipping-container-based vertical farms are set to record a 16.55% CAGR over the same period.

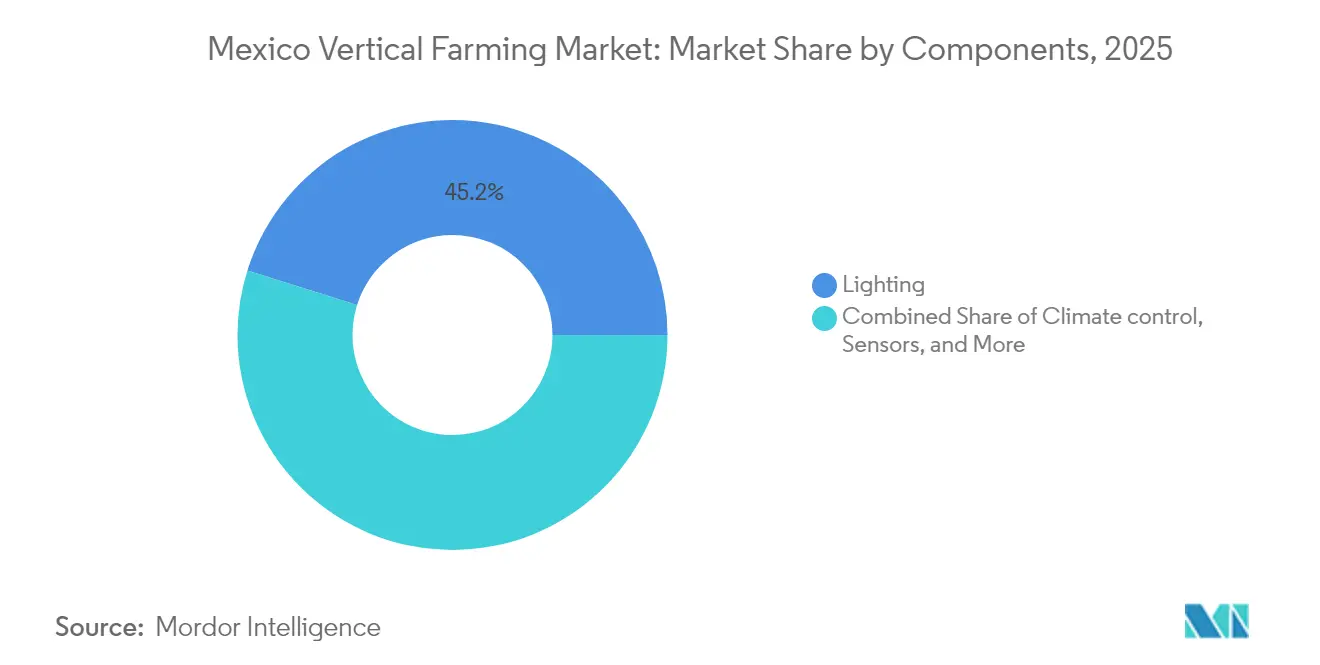

- By components, lighting components held 45.15% of 2025 sales, but sensors are forecast to expand at a 17.36% CAGR to 2031.

- By crop types, lettuce and leafy vegetables commanded 29.88% of 2025 output, while microgreens are poised for 16.62% CAGR growth toward 2031.

- Verde Compacto S.A.P.I. de C.V., Karma Verde Fresh S.A.P.I. de C.V., Comercializadora Hydro Environment S.A. de C.V., Village Farms International, and Freight Farms Inc. (Growcer) held a minority share of the market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Vertical Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising water scarcity and shrinking arable land | +2.4% | Nationwide, acute in Sonora, Chihuahua, and Nuevo León | Long term (≥ 4 years) |

| Increased focus on food security | +2.5% | National, priority in Mexico City metro | Medium term (2-4 years) |

| Government subsidies for ag-tech innovation | +2.0% | National, early adoption in Jalisco, Querétaro, and Estado de México | Medium term (2-4 years) |

| Growing adoption of LED lighting optimized for tropical latitudes | +1.8% | National, faster in southern states | Short term (≤ 2 years) |

| Re-purposing vacant retail facilities into indoor farms | +1.4% | Mexico City, Guadalajara, Monterrey, and Puebla | Short term (≤ 2 years) |

| Agrivoltaics integration with rooftop solar mandates | +1.2% | High-irradiation zones countrywide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Water Scarcity and Shrinking Arable Land

Mexico's National Water Commission (CONAGUA) 2024-2030 National Hydric Plan redistributes water from agricultural to urban use, highlighting irrigation inefficiencies and compelling farmers to adopt closed-loop vertical farming systems that reduce water consumption by up to 90%[1]Source: Food and Agriculture Organization of the United Nations, “Perfiles de Países de la FAO: México,” fao.org. Northern Mexican states report groundwater extraction rates 40-60% above annual replenishment levels, providing container farms that can relocate near stable aquifers with operational advantages. The implementation of digital water concession management discourages traditional flood irrigation methods and increases private investment in hydroponic and aeroponic systems that reduce water extraction costs. With increasing drought periods, water-efficient farming methods have become an economic requirement rather than an environmental choice, making vertical farming more viable than conventional field agriculture.

Increased Focus on Food Security

Mexico's food sovereignty decree of December 2024 addresses the 23% fresh produce import gap through vertical farming initiatives. The government's USD 4,188 million "Cosechando Soberanía" program, launched in April 2025, directs infrastructure funding to protected cultivation methods within urban areas. This approach aims to protect supply chains from external disruptions while enabling year-round production. Urban farming operations reduce transportation distances, minimize product spoilage, and provide transparent production tracking. The government's financial support through grants and concessional loans drives growth in Mexico's vertical farming market.

Government Subsidies for Ag-Tech Innovation

The Mexican Secretariat of Agriculture and Rural Development (SADER) allocated increased funding for protected agriculture in its 2025 budget. The organization's technical assistance program, supported by the Food and Agriculture Organization, provides USD 260,000 for sustainable agri-food system pilots. In Jalisco, the state government promotes youth employment through co-funded vertical farming apprenticeships that combine agricultural science with data analytics. The subsidies reduce capital expenditure by 10-15% for early adopters, reduce payback periods to less than five years, and incentivize small and medium-sized growers to implement hydroponic or aeroponic systems rather than traditional greenhouses. The recurring grant cycles accelerate market adoption and improve technological capabilities among operators.

Agrivoltaics Integration with Rooftop Solar Mandates

Mexico's 2024 building codes mandate solar installations on new commercial roofs across multiple states, enabling agrivoltaic greenhouses and rooftop vertical farms to generate additional revenue through surplus energy sales[2]Source: Secretaría de Energía, “Norma Técnica Para Instalaciones Fotovoltaicas en Edificios,” Secretaría de Energía, sener.gob.mx. Developers combine power purchase agreements with produce supply contracts to create dual income streams, improving project financing potential. This model helps offset high electricity costs and provides farms with energy security in remote locations. Agrivoltaic systems enhance the competitiveness of vertical farming operations compared to traditional greenhouse facilities without integrated power generation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment | -2.4% | Nationwide, especially in smaller urban centers | Medium term (2-4 years) |

| Limited skilled labor pool | -1.8% | National, acute in secondary cities | Long term (≥ 4 years) |

| Uncertain access to long-term water rights | -1.2% | Groundwater-stressed northern and central states | Long term (≥ 4 years) |

| Customs delays on imported automation equipment | -0.9% | Countrywide, affecting technology-dependent projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment

The cost of turn-key vertical farms ranges from USD 2-4 million per hectare equivalent, significantly higher than the USD 50,000 median investment capacity of small Mexican growers. Import duties of 15-25% on essential components such as LED fixtures, sensors, and climate controllers increase overall costs. Mexican lenders require land as collateral, making it difficult to secure financing for technology assets. The agricultural lending sector's focus on land-backed collateral creates a financing gap for vertical farming ventures. While container farms, priced between USD 150,000-300,000 per unit, offer a lower entry point, they remain beyond the financial reach of many rural producers. As a result, vertical farming adoption remains concentrated among well-funded corporations and startups in major metropolitan areas.

Limited Skilled Labor Pool

The vertical farming sector requires specialized technicians with skills in nutrient solution calibration, IoT device maintenance, and sensor data analysis - competencies not typically included in traditional agricultural education programs[3]Source: Instituto Nacional de Estadística y Geografía, “Encuesta Nacional de Ocupación y Empleo 2025,” INEGI, inegi.org.mx. While Jalisco's training programs produce hundreds of qualified workers annually, significant skill gaps remain across Mexico. This shortage compels vertical farm operators to hire international talent or external consultants. The water management sector's aging workforce, with an average age of 55-60 years, exemplifies the broader agricultural labor challenges impacting vertical farming implementation. Mexican vertical farming operations often depend on international technical expertise for system installation and maintenance, which increases operational expenses and reduces their ability to operate independently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Growth Mechanism: Hydroponics Dominates Despite Aeroponics Acceleration

Hydroponics accounted for 63.25% of the Mexico vertical farming market share in 2025. This dominance stems from the alignment of nutrient film technique and deep-water culture with local agricultural expertise and existing greenhouse operations. The technology offers faster return on investment compared to alternative methods due to reduced maintenance requirements and straightforward operational training. Hydroponics also aligns with Mexico's export-focused production of lettuce, herbs, and peppers, delivering consistent yields at efficient cost levels.

Aeroponics is projected to grow at a CAGR of 17.12%, driven by its superior water conservation capabilities and accelerated crop cycles, particularly in regions facing water scarcity. Initial implementations demonstrate 10-15% increased yields per square meter and 20% reduction in fertilizer usage, particularly benefiting premium leafy green production. Container farming operations prefer aeroponics as its compact misting systems maximize vertical space utilization, increasing overall production capacity. These factors indicate that aeroponics will significantly expand its share in the Mexico vertical farming market over the next five years.

By Structure: Building-Based Vertical Farms Lead While Shipping-Container-Based Vertical Farms Gain Momentum

Building-based vertical Farms account for 55.62% of the Mexico vertical farming size in 2025, leveraging vacant retail and industrial properties in urban centers following the pandemic. These facilities support extensive racking systems, comprehensive climate control infrastructure, and integrated solar power generation, enabling operators to achieve economies of scale required to compete with imported produce. Their strategic location near population centers reduces transportation costs and product loss, reinforcing their market dominance.

Shipping-container-based vertical farms are projected to grow at a 16.55% CAGR, primarily serving secondary cities and rural areas with limited access to fresh produce. Their modular design enables rapid deployment within weeks, making them particularly suitable for franchise expansion. The lower initial capital requirements attract impact investors focused on addressing food accessibility issues. The Mexico vertical farming market of container systems is projected to increase throughout the forecast period, driven by modularization and targeted micro-market strategies.

By Components: Lighting Leads While Sensors Drive Innovation

Lighting sub-systems represented 45.15% of the Mexico vertical farming market share in 2025. LED arrays constitute approximately one-third of total construction costs and require regular upgrades. Mexican vertical farms are implementing spectrum-optimized fixtures that reduce power consumption to comply with state energy efficiency regulations. The lighting segment maintains its dominant market position due to the gradual nature of lighting system upgrades.

The sensor platforms segment is projected to grow at a 17.36% CAGR, driven by decreasing IoT hardware costs and cloud analytics subscription services that improve operational decisions. These systems enable remote nutrient management and early disease detection, reducing labor requirements and waste while addressing the shortage of skilled workers. The increasing adoption of sensor technologies supports the development of autonomous farming operations, creating a cycle of increased digital technology integration in the Mexico vertical farming market.

By Crop Types: Lettuce and Leafy Vegetables Dominate While Microgreens Surge

Lettuce and leafy vegetables accounted for 29.88% of the Mexico vertical farming market share in 2025, driven by strong domestic consumption and established export routes to the United States and Canada. The short growth cycles, consistent plant structure, and stable pricing make leafy greens a low-risk option for new market entrants. Existing supply contracts with food-service chains provide guaranteed sales volumes, facilitating bank financing.

The microgreens segment is projected to grow at a 16.62% CAGR, supported by demand from high-end restaurants and health-conscious consumers. The minimal space requirements of microgreens suit container farming operations, allowing restaurants and retailers to maintain production facilities near their kitchens. Despite higher energy costs per unit, the superior profit margins per kilogram attract both new ventures and established companies to this market segment. As a result, Mexico's vertical farming market for microgreens continues to expand, even with its specialized market position.

Geography Analysis

Vertical farming capacity concentrates in six states that contain a substantial portion of protected-agriculture infrastructure. Estado de México holds a significant share of operational units due to its proximity to Mexico City's consumer market. Sinaloa and Baja California utilize their export corridors and greenhouse experience to support large-scale facilities, primarily focusing on hydroponic tomatoes and peppers. Chihuahua and Sonora focus on closed-loop systems to maintain production amid increasing groundwater scarcity. These regional hubs demonstrate how market growth aligns with established agricultural export routes and water availability in the Mexico vertical farming market.

Jalisco has developed into an innovation center through its annual Green Tech Americas forum, ag-tech accelerators, and government support for youth employment in advanced horticulture. The state's strategic location at major transportation intersections facilitates efficient produce distribution to domestic markets and Pacific ports. Querétaro leverages its skilled manufacturing workforce to expand sensor-equipped container farming operations, offering a moderate cost base with central highland logistics advantages. These central states have established a technology-focused region that competes with northern exporters in both project numbers and venture capital investment.

Southern expansion is progressing as Smart City Tehuantepec plans to establish 22 automated farms by 2028, while coastal Oaxaca explores aquaponics systems that combine fish recirculation with leafy green production. The region's lower land costs and growing tourism sector encourage specialty crop experiments in herbs and edible flowers, while abundant renewable energy resources support combined solar-agricultural facilities. Despite infrastructure limitations, municipal incentives and NGO partnerships help reduce pilot project risks, indicating that geographic diversification will characterize the next phase of growth in the Mexico vertical farming market.

Competitive Landscape

Verde Compacto S.A.P.I. de C.V., Karma Verde Fresh S.A.P.I. de C.V., Comercializadora Hydro Environment S.A. de C.V., Village Farms International, and Freight Farms Inc. (Growcer) collectively held a minority share of the Mexico vertical farming market in 2024, indicating moderate market concentration. Verde Compacto markets Huvster smart containers that increase productivity through aeroponic misting and AI scheduling. Karma Verde Fresh operates urban hydroponic towers in grocery stores and mall basements. Village Farms International utilizes North American Free Trade Agreement duty-free access to distribute Mexican-grown tomatoes and cucumbers to North American supermarkets, generating USD 336.2 million in consolidated revenue in 2024.

The market features three distinct business models. Domestic companies focus on modular systems and reduced logistics costs to serve regional markets. Export-focused multinationals invest in large-scale greenhouse facilities in border states to benefit from favorable labor and sunlight conditions. Technology providers supply sensors, nutrient systems, and LED lighting to both groups, generating recurring revenue through software subscriptions. The market is seeing increased collaboration through joint ventures, where container manufacturers partner with equipment suppliers to provide complete farming solutions to hotels and universities.

Market leaders distinguish themselves through regulatory compliance and supply chain management. Companies with environmental clearances from the Secretariat of Environment and Natural Resources and sufficient inventory reserves navigate customs processes more efficiently than their smaller competitors. Certifications, including Global G.A.P. and the United States Department of Agriculture's Organic equivalence, enable access to premium retail markets. As automation costs increase, investors prefer operators demonstrating above-average production efficiency per square meter. Market consolidation activity is projected to increase, with three domestic companies planning capital raises for regional expansion over the 2026-2027 period.

Mexico Vertical Farming Industry Leaders

Verde Compacto S.A.P.I. de C.V.

Karma Verde Fresh S.A.P.I. de C.V.

Village Farms International

Comercializadora Hydro Environment S.A. de C.V.

Freight Farms Inc. (Growcer)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Verde Compacto, in collaboration with Club Deportivo Guadalajara (Chivas) and Revive It Sustainability Office, has installed HUVSTER, a vertical hydroponic farm within Mexico's Estadio Akron stadium. This installation demonstrates a replicable model for incorporating vertical farming into sports venues, which can be implemented in other stadiums, urban spaces, and institutional food systems.

- March 2025: Rising Farms expanded its operations by acquiring a production facility in San Luis Potosí. This acquisition increased the company's installed capacity by 52% and added 350 employees, bringing its total workforce to 900.

- November 2024: Globalmex International Inc., operating under the Magic Sun brand, has introduced hydroponic greenhouse-grown Roma tomatoes in central Mexico. The integration of hydroponic systems and high-elevation locations in central Mexico provides natural protection from weather variations, ensuring consistent crop production.

Mexico Vertical Farming Market Report Scope

Vertical farming is an agricultural method through which crops are grown in vertically stacked layers. It is done in a controlled environment using techniques such as aquaponics, hydroponics, and aeroponics that do not make use of soil. The Mexico vertical farming market is segmented by growth mechanism (aeroponics, hydroponics, and aquaponics), structure (building-based vertical farms and shipping container-based vertical farms), component( lighting devices, climate control, sensors, and other components), and crop type (tomato, berries, lettuce & leafy vegetables, pepper, cucumber, microgreens, and other crop types). The report offers market estimation and forecasts in value (USD) for the above-mentioned segments.

By Growth Mechanism

| Aeroponics |

| Hydroponics |

| Aquaponics |

By Structure

| Building-Based Vertical Farms |

| Shipping-Container-Based Vertical Farms |

By Components

| Lighting |

| Climate Control |

| Sensors |

| Other Components (Nutrients, etc.) |

By Crop Types

| Tomato |

| Berries |

| Lettuce and Leafy Vegetables |

| Pepper |

| Cucumber |

| Microgreens |

| Other Crop Types (Herbs, Edible Flowers, etc.) |

| By Growth Mechanism | Aeroponics |

| Hydroponics | |

| Aquaponics | |

| By Structure | Building-Based Vertical Farms |

| Shipping-Container-Based Vertical Farms | |

| By Components | Lighting |

| Climate Control | |

| Sensors | |

| Other Components (Nutrients, etc.) | |

| By Crop Types | Tomato |

| Berries | |

| Lettuce and Leafy Vegetables | |

| Pepper | |

| Cucumber | |

| Microgreens | |

| Other Crop Types (Herbs, Edible Flowers, etc.) |

Key Questions Answered in the Report

What is the current valuation of the Mexico vertical farming market?

The sector is valued at USD 367.44 million in 2026 and is projected to reach USD 783.9 million by 2031.

How fast is the market expanding?

It is growing at a 16.38% CAGR, propelled by water-efficiency mandates, food-security policies, and LED-driven energy savings.

Which technology holds the largest share today?

Hydroponic systems account for 63.25% of 2025 revenue owing to their relative simplicity and established operator familiarity.

What segment is forecast to grow the quickest?

Aeroponics will register the highest 17.12% CAGR because of superior water use efficiency and rapid crop cycles.

Which regions inside Mexico are seeing the most installations?

Estado de México, Sinaloa, Jalisco, Chihuahua, Sonora, and Baja California host nearly two thirds of total vertical farming capacity.

Page last updated on: