Metal Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.52 Billion |

| Market Size (2031) | USD 18.61 Billion |

| Growth Rate (2025 - 2030) | 5.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Coatings Market Analysis by Mordor Intelligence

The Metal Coatings Market size is expected to increase from USD 13.96 billion in 2025 to USD 14.52 billion in 2026 and reach USD 18.61 billion by 2031, growing at a CAGR of 5.09% over 2026-2031. As global VOC thresholds tighten and public works spending reaches unprecedented levels, industries are rapidly transitioning from solvent-borne chemistries to alternatives such as water-borne, powder, and UV-cured solutions. Infrastructure rehabilitation in North America, Europe, and Japan is driving up the demand for protective coatings. At the same time, the automotive industry's focus on lightweighting and electrification is increasing the demand for coil coatings on aluminum substrates. Emerging specialty niches include intumescent systems that decelerate thermal propagation in battery packs and ultra-high-temperature linings for hydrogen pipelines. The competitive landscape is becoming more intense - major formulators are expanding powder capacities in the Asia-Pacific region, while local players are leveraging regional distribution channels to maintain their market presence.

Key Report Takeaways

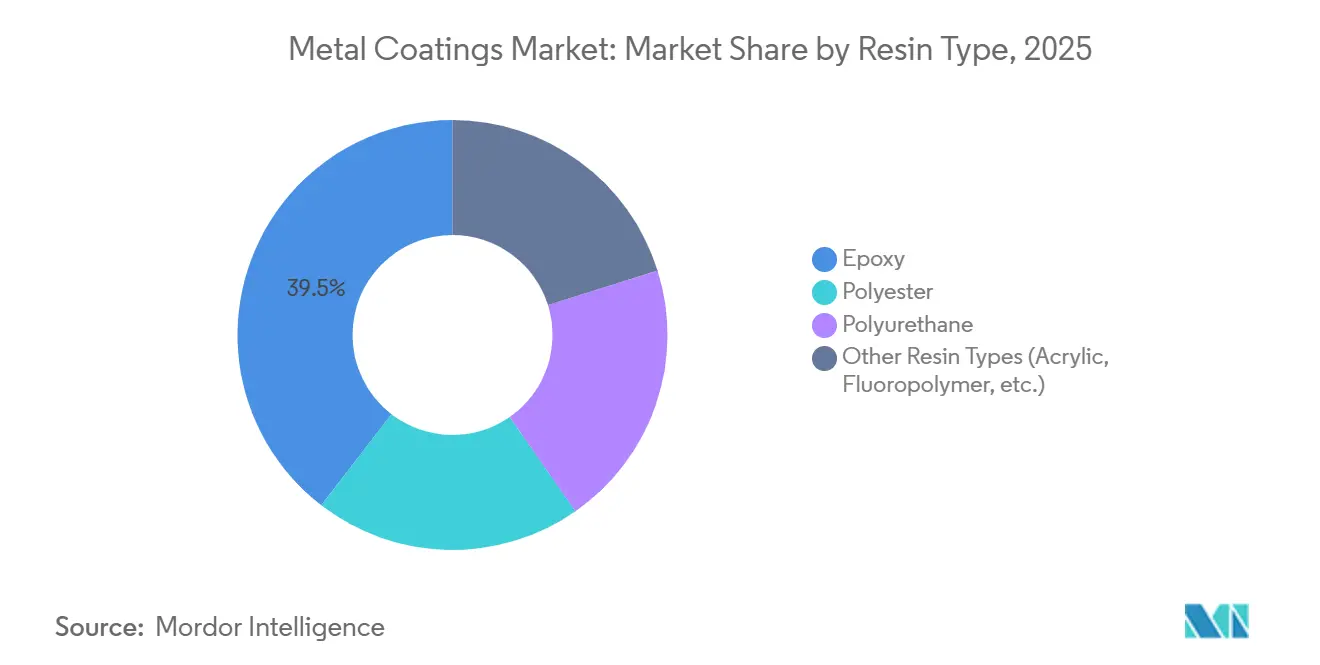

- By resin type, epoxy captured 39.54% of the metal coatings market share in 2025; the Other Resin Types segment is forecast to expand at a 6.89% CAGR through 2031.

- By technology, solvent-borne processes held 47.71% of 2025 revenue, whereas UV-cured platforms are projected to grow at 6.47% over 2026-2031.

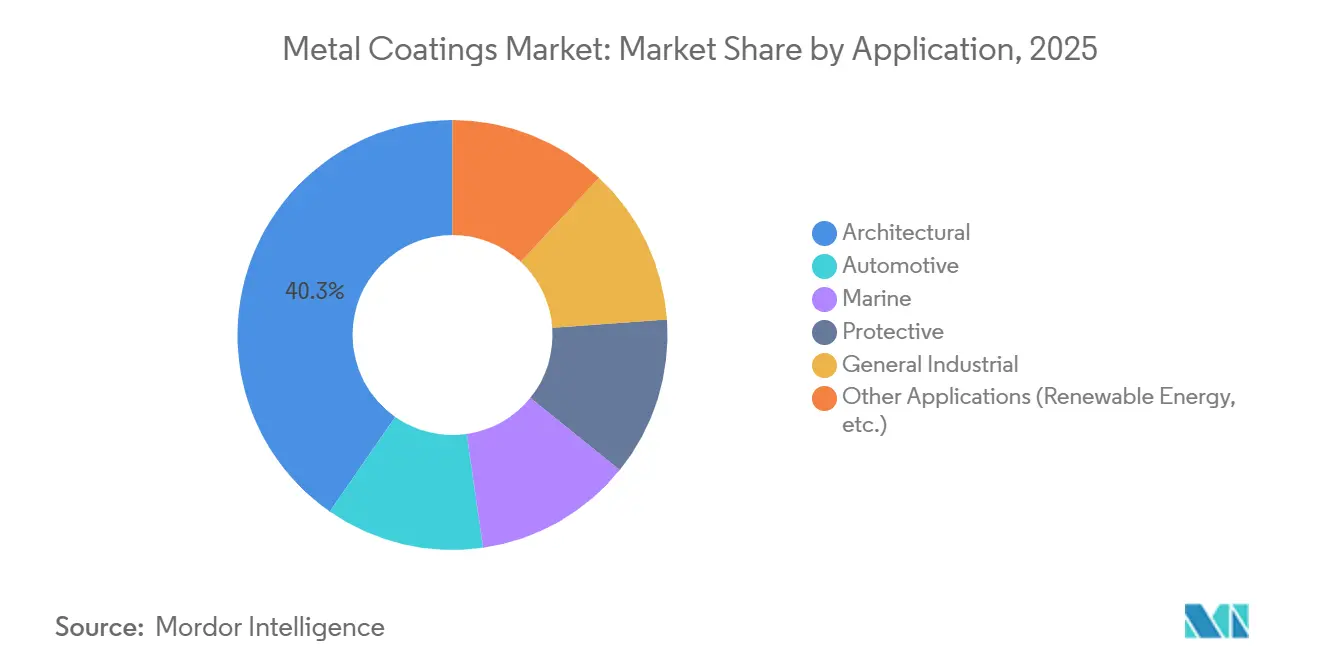

- By application, architectural uses led with 40.32% of 2025 turnover, while protective coatings are advancing at a 6.62% CAGR to 2031.

- By geography, Asia-Pacific accounted for 46.95% of 2025 demand and is expected to expand at 6.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Stringent VOC caps accelerating water-borne chemistries | +1.00% | Global, with North America and EU leading enforcement | Medium term (2-4 years) | |

| Re-roofing and bridge-rehab up-cycle in OECD markets | +0.90% | North America, Europe, Japan | Medium term (2-4 years) | |

| Automotive light-weighting pushing aluminum coil coatings | +0.80% | APAC core (China, South Korea), spill-over to North America | Short term (≤ 2 years) | |

| EV battery-pack safety driving intumescent metal coatings | +0.60% | Global, with early gains in China, Germany, California | Long term (≥ 4 years) | |

| Hydrogen pipelines demanding high-temperature anti-corrosion linings | +0.50% | Europe, Middle-East (Saudi Arabia, UAE), with pilot projects in North America | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Stringent VOC Caps Accelerating Water-Borne Chemistries

Regulators across three continents have set stringent ceilings on volatile organic compounds (VOCs), effectively resetting formulation baselines. In 2024, the United States capped VOCs in architectural coatings. Meanwhile, the European Union is pushing for a reduction by 2030. Germany, ahead of the curve, has already set a limit for metal substrates. In 2025, China mandated VOC audits for appliance and metal-furniture lines in Guangdong and Jiangsu. Singapore, not to be left behind, established a threshold in January 2025. Water-borne options have surged, now accounting for a significant portion of North America's architectural metal output, a notable rise from earlier years. However, achieving C5 corrosion protection remains a challenge without hybrid polyurethane-acrylic chemistries. Suppliers are now combining flash-rust inhibitors with innovative latent catalysts, effectively reducing cure windows under ambient conditions. Formulators offering ISO 12944-compliant water-borne systems for marine or oil-and-gas sectors stand to reap premium margins in the metal coatings arena.

Re-Roofing and Bridge-Rehab Up-Cycle in OECD Markets

Aging transport assets are fueling a consistent demand for coatings. In the United States, many bridges have surpassed their 50-year service life, leading to a significant need for protective coatings by 2030. Europe, recognizing the urgency, has allocated funds for bridge and tunnel refurbishments under its TEN-T program. Meanwhile, Japan’s Longevity Plan is addressing thousands of bridges, employing zinc-rich epoxy primers to extend repainting intervals. As commercial roof lifecycles shorten, driven by the pursuit of cool-roof credits under LEED v5, there is a heightened demand for fluoropolymer and silicone-modified polyester top-coats. However, shortages in zinc dust and titanium dioxide are causing project delays, simultaneously creating a market for low-zinc epoxy alternatives that provide galvanic protection and mitigate supply risks.

Automotive Light-Weighting Pushing Aluminum Coil Coatings

In response to OEM fuel-economy targets, global demand for aluminum body panels has surged, with shipments projected to rise significantly. To maintain substrate temper, coil lines are capping cure temperatures below 230 °C, steering formulators towards polyester or polyurethane systems enhanced with blocked isocyanates. China's goal for EV penetration by 2030 has already spurred heightened demand for coated aluminum. South Korea’s Hyundai-POSCO venture highlights the critical role of vertical integration in securing paint supplies. While fluoropolymer top coats boast impressive exterior durability, their premium price confines their adoption to the high-end EV market. Nevertheless, the relentless demand for lighter, pre-finished panels underscores transportation's central role in the metal coatings landscape.

EV Safety and Hydrogen Pipelines Lifting Specialty Protective Solutions

UN ECE GTR 20 stipulates that battery enclosures must withstand thermal propagation for five minutes. This mandate has driven a surge in demand for intumescent products, known for their significant expansion when exposed to heat. Simultaneously, hydrogen pipeline projects in Europe and the Middle-East are enforcing rigorous standards: linings must endure temperatures of 400 °C and limit permeation to below 0.01 cc/m²/day. Only fluoropolymers or ceramic-filled epoxies can meet these stringent benchmarks. With Saudi Arabia's ambitious NEOM contracts and the U.S. DOE's Hydrogen Shot initiative, the demand for these high-margin chemistries has intensified. Suppliers who skillfully balance cost, performance, and evolving regulations are poised to capture a significant share as decarbonization infrastructures advance, further propelling the metal coatings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Epoxy resin supply volatility linked to BPA regulations | -0.60% | Global, with acute impact in EU and North America | Short term (≤ 2 years) | |

| Compliance cost of solvent-borne lines in ASEAN and LATAM | -0.50% | ASEAN (Vietnam, Thailand, Indonesia), LATAM (Brazil, Argentina, Mexico) | Medium term (2-4 years) | |

| Under-cured powder defects in large offshore components | -0.40% | Global offshore wind markets (North Sea, East China Sea, U.S. Atlantic coast) | Short term (≤ 2 years) | |

| Source: Mordor Intelligence | ||||

Epoxy Resin Supply Volatility Linked to BPA Regulations

In January 2025, the EU's ban on food-contact epoxy coatings forced the market to pivot toward bisphenol F and pricier bio-based substitutes[1]European Commission, “Regulation 2024/3190 on Bisphenol A,” ec.europa.eu . France’s ANSES expedited phase-outs, while the U.S. FDA encouraged beverage canners to move away from traditional epoxies via voluntary guidance. In 2025, spot resin prices spiked, squeezing converter margins and postponing project tenders, as specifiers sought to requalify alternatives. BPA-free systems, with their lower crosslink density, require thicker films, leading to increased consumption per square meter. This pressure is felt across the metal coatings market, disproportionately impacting small and midsize can-coating firms in Europe.

Compliance Cost of Solvent-Borne Lines in ASEAN and LATAM

Emerging economies are tightening their regulatory frameworks. In July 2024, Vietnam set a VOC cap, and Thailand followed suit with similar thresholds in 2025[2]Ministry of Natural Resources and Environment Vietnam, “VOC Standard for Industrial Paint,” monre.gov.vn . These regulations compel operators to invest in thermal oxidizers, with high costs per line. Brazil's stricter ozone-precursor regulations effectively mandate a reduction in solvent emissions within three years. Meanwhile, Argentina's new regulatory framework delegates standards to individual provinces, resulting in a fragmented compliance landscape. Smaller converters, unable to shoulder these costs, are either exiting the market or forming alliances, leading to a swift consolidation. While these retrofit expenses reduce the forecasted growth for the 2026-2031 period, they simultaneously create opportunities for water-borne and powder specialists to cater to the burgeoning demand in the metal coatings sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Transition Beyond Epoxy Anchors Future Expansion

In 2025, epoxy resins captured 39.54% of the market revenue, largely due to their superior adhesion and chemical resistance, particularly in ISO 12944 C4 and C5 services. Meanwhile, other resin types - including acrylics, fluoropolymers, and silicone hybrids - are set to outpace the broader metal coatings market, with a projected CAGR of 6.89% during the forecast period of 2026-2031. While epoxies traditionally dominated heavy-duty protection, allowing for thicker films with fewer coats, buyers have increasingly gravitated toward polyester and polyurethane blends. This shift, influenced by BPA restrictions and rising costs, was especially evident in applications prioritizing weatherability over immersion service.

Bio-based cardanol epoxies and bisphenol F variants provided some relief, but users faced a trade-off: a decrease in crosslink density necessitated a thicker build to match the performance of conventional barriers. Conversely, while fluoropolymers came at a premium, they were favored for coastal and high-rise façade projects, where long-term gloss retention was paramount. Additionally, silicone-modified polyesters gained traction in coil lines, particularly in scenarios where temperatures had to be controlled to avoid aluminum temper loss. These developments further broadened the metal coatings market for specialty resins. Suppliers adeptly navigating environmental regulations while ensuring efficient film builds are set to shape resin-mix dynamics through 2031.

By Technology: UV Platforms Shrink Energy Footprint

In 2025, solvent-borne routes accounted for 47.71% of the output, bolstered by established assets and flexible application windows. Yet, UV-cured systems are on the rise, boasting a CAGR of 6.47% during the forecast period of 2026-2031. This surge is largely attributed to a notable decline in LED unit costs, which promise significant energy savings over traditional mercury lamps. Powder coatings, celebrated for their zero VOC emissions and high transfer efficiency, encountered hurdles in adoption. A primary challenge was the limitation of convection-oven size, restricting their use for parts beyond certain diameters - a crucial factor for offshore wind towers.

Hybrid UV-powder solutions emerged as a solution, offering both immediate surface curing and deep heat penetration without oversized ovens. As EPA and EU regulations tightened, water-borne volumes saw an uptick. However, challenges like flash-rust risk and prolonged drying times hindered their adoption in the marine and oil-and-gas sectors, where solvent-borne epoxies held a competitive advantage. By modernizing legacy lines with catalytic IR or dual-cure stations, converters adeptly balanced compliance with throughput demands, reinforcing their foothold in the metal coatings market.

By Application: Infrastructure and Energy Projects Steer Demand Mix

In 2025, architectural applications dominated, accounting for 40.32% of the revenue. This dominance was largely due to the expansive square footage of roofing and façades. Protective systems, meanwhile, are projected to grow by 6.62% during the forecast period of 2026-2031, spurred on by energy-transition megaprojects. The automotive industry, buoyed by a surging demand for aluminum coil-coating - closely tied to electrification - saw a boost. In the marine realm, coatings grappled with the dual mandates of adhering to IMO sulfur-cap regulations and achieving low-friction standards.

General industrial sectors, spanning from machinery to metal furniture, increasingly adopted powder coatings to curtail solvent recovery costs. Furthermore, renewable-energy initiatives in desert and coastal locales underscored the need for coatings with enduring durability, spotlighting the significance of fluoropolymer and polyurethane chemistries. These varied end uses not only expanded the metal coatings market but also provided suppliers with a cushion against downturns in any singular segment.

Geography Analysis

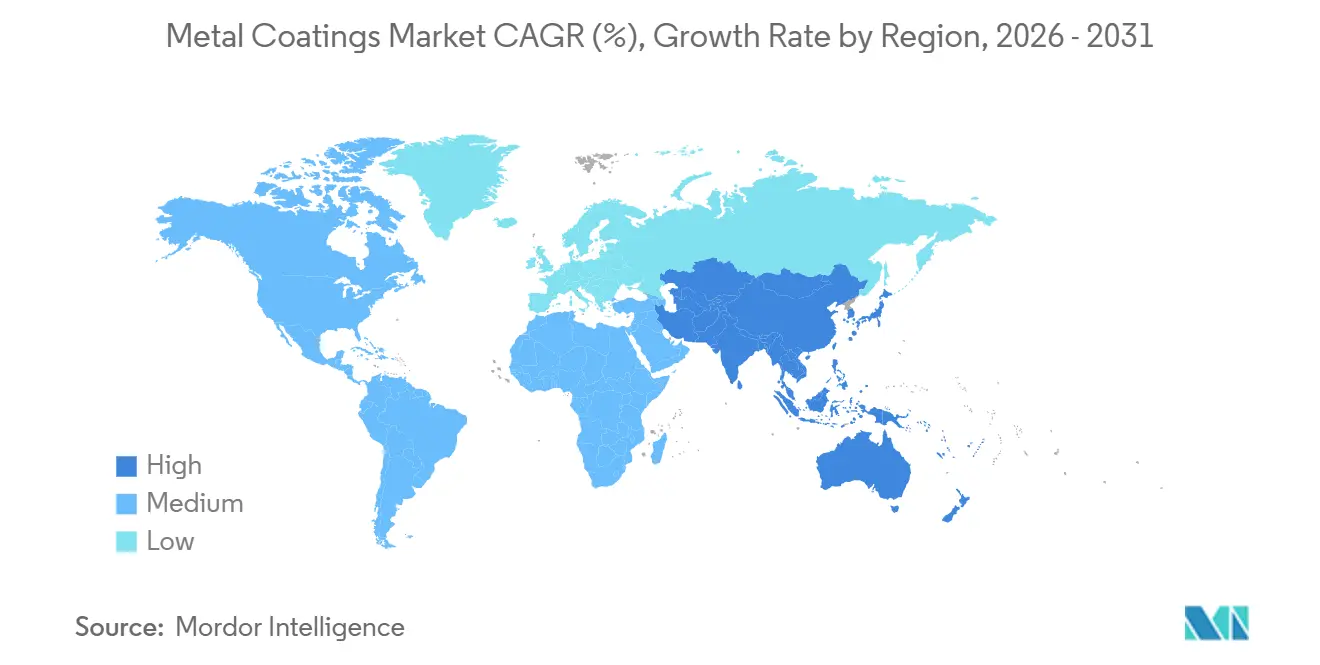

Asia-Pacific, accounting for 46.95% of global sales in 2025, is projected to grow at a CAGR of 6.41% through the forecast period of 2026-2031. This growth is bolstered by China's strong manufacturing base, India's ambitious infrastructure projects, and ASEAN's strict VOC regulations. China's push for a significant share in the EV market by 2030 is driving the uptake of coil-coated aluminum. Simultaneously, audits in Guangdong and Jiangsu are accelerating the shift to water-borne solutions. In India, budgets for steel structures are increasingly being allocated to protective paints, ensuring consistent tenders that benefit both domestic and international suppliers. Vietnam's newly imposed cap is prompting line retrofits, guiding regional production towards compliant coatings.

North America, which holds a substantial share of 2025's turnover, is reaping benefits from the Bipartisan Infrastructure Law, especially given that many of its bridges are over 50 years old. Europe not only contributes significantly to the revenue but also leads in regulatory innovations, from banning BPA to defining hydrogen-pipeline standards under its Hydrogen Backbone vision. These established regions emphasize high-value protective specifications, reinforcing the demand for solvent-borne epoxies, even as powder and water-based platforms gain momentum.

While South America and the Middle-East currently hold a smaller combined market share, they are poised for rapid percentage growth. Brazil's strict ozone regulations and Saudi Arabia's NEOM contracts are broadening protective niches. Yet, challenges arise with Argentina's fragmented provincial VOC regulations and inconsistent enforcement in certain ASEAN countries, complicating supply-chain planning. Nonetheless, these challenges also unveil acquisition and greenfield opportunities for global formulators seeking a stronger presence in the metal coatings market.

Competitive Landscape

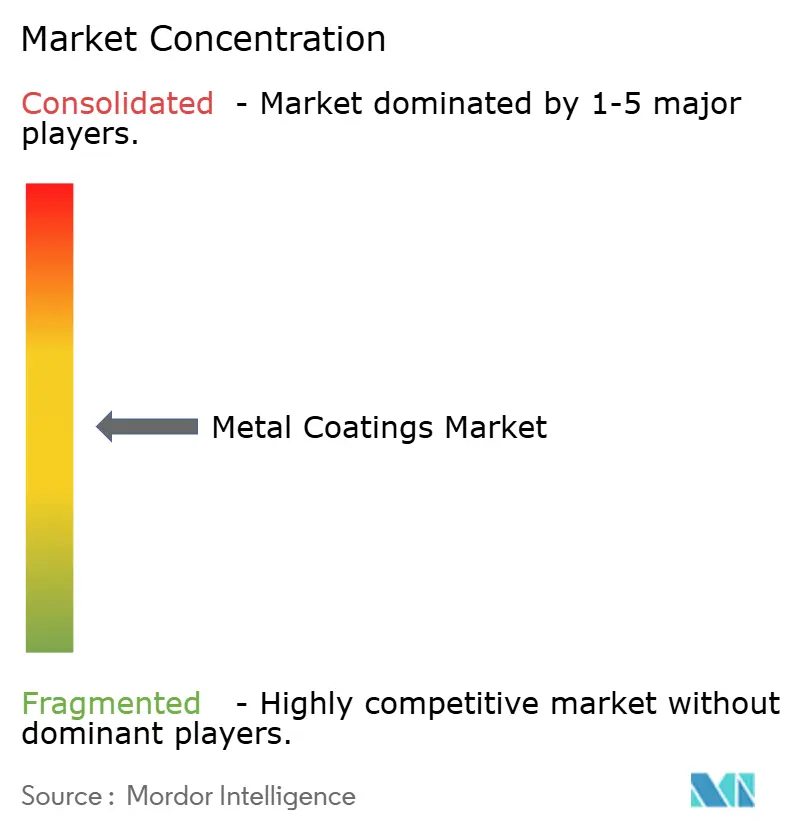

The metal coatings market is moderately fragmented. Leading players captured a notable share of 2025's sales, hinting at opportunities for midsize contenders. Industry frontrunners are adopting three main strategies: boosting powder capacity in the Asia-Pacific, innovating with UV-cure or bio-based epoxies, and selectively pursuing vertical integration. Sherwin-Williams' acquisition of a powder company expanded its footprint with multiple European factories. Similarly, AkzoNobel's investment in the Changzhou site enhanced its automated capacity.

Nippon Paint's takeover of Turkish assets strategically aligns it with Middle-Eastern builders. Concurrently, PPG's investment in a Brazilian protective firm cements its position in the oil-and-gas domain. Intellectual-property filings, like PPG's UV-powder hybrid designed for offshore wind towers, highlight the industry's focus on technical differentiation over pricing. Disruptors such as Teknos are gaining traction with swift color-matching services and 48-hour technical support - features that challenge larger multinationals to replicate on a large scale.

Quality standards like ISO 12944, ISO 2808, and LEED v5 set high entry barriers, requiring extensive multi-year field data. Pricing dynamics reveal pressure in appliance segments, with Chinese powder suppliers underpricing their European counterparts. However, this strategy carries the risk of under-curing in larger sections, potentially hindering expansion. In conclusion, suppliers who adeptly navigate regulations, build localized service capabilities, and innovate in specialty niches are set to outpace the broader metal coatings market.

Metal Coatings Industry Leaders

Axalta Coating Systems, LLC

The Sherwin-Williams Company

Akzo Nobel N.V.

PPG Industries, Inc.

Nippon Paint Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Jindal India, a part of the BC Jindal Group, commissioned a new advanced metal coating line at its Ranihati manufacturing facility in Howrah. This new line was projected to increase the production of value-added coated steel products by approximately 60%, reaching around 0.3 million metric tons.

- July 2025: Dunn-Edwards Corporation launched ULTRASHIELD, a heavy-duty industrial maintenance coatings series. ULTRASHIELD Aluminum Epoxy is a low-VOC, high-performance, aluminum-filled micaceous iron oxide (MIO) epoxy designed to deliver superior corrosion protection for marginally prepared steel and intended for application on metal surfaces.

Global Metal Coatings Market Report Scope

Metal coatings are chemicals used for metallic surfaces for functional properties such as anti-corrosion, anti-slip surface, anti-bacterial, etc.

The metal coatings market is segmented by resin type, technology, application, and geography. By resin type, the market is segmented into epoxy, polyester, polyurethane, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder, ultraviolet (UV)-cured, and light emitting diode (LED) curing. By application, the market is segmented into architectural, automotive, marine, protective, general industrial, and other applications. The report also covers the market size and forecasts for metal coatings in 28 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types (Acrylic, Fluoropolymer, etc.) |

| Water-borne |

| Solvent-borne |

| Powder |

| Ultraviolet (UV)-Cured |

| Light Emitting Diode (LED) Curing |

| Architectural |

| Automotive |

| Marine |

| Protective |

| General Industrial |

| Other Applications (Renewable Energy, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Thailand | |

| Malaysia | |

| Phillipines | |

| Vietnam | |

| Singapore | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Qatar | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Resin Type | Epoxy | |

| Polyester | ||

| Polyurethane | ||

| Other Resin Types (Acrylic, Fluoropolymer, etc.) | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder | ||

| Ultraviolet (UV)-Cured | ||

| Light Emitting Diode (LED) Curing | ||

| By Application | Architectural | |

| Automotive | ||

| Marine | ||

| Protective | ||

| General Industrial | ||

| Other Applications (Renewable Energy, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Malaysia | ||

| Phillipines | ||

| Vietnam | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Egypt | ||

| Qatar | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global spending on metal coatings be by 2031?

The metal coatings market size stands at USD 14.52 billion in 2026, and it is projected to reach USD 18.61 billion by 2031 at a 5.09% CAGR.

Which resin group is growing fastest?

Other Resin Types that include acrylics, fluoropolymers, and silicone hybrids are set to grow 6.89% yearly, outpacing epoxy.

Why are UV-cured products gaining popularity?

LED equipment prices have fallen below USD 80,000 per line, and cut process energy use by 70%, accelerating the adoption of UV platforms.

What region accounts for the largest demand?

Asia-Pacific held 46.95% of 2025 consumption and remains the principal growth engine through 2031.

How are BPA regulations affecting epoxy supply?

EU and North American BPA restrictions have lifted epoxy prices by 28% during 2025 and forced costly reformulations that squeeze converter margins.

Which application will expand fastest during 2026-2031?

Protective coatings linked to renewable energy and hydrogen infrastructure projects are forecast to grow at a 6.62% CAGR.

Page last updated on: