MEMS Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 17.5 Billion |

| Market Size (2030) | USD 24.81 Billion |

| Growth Rate (2025 - 2030) | 7.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

MEMS Market Analysis by Mordor Intelligence

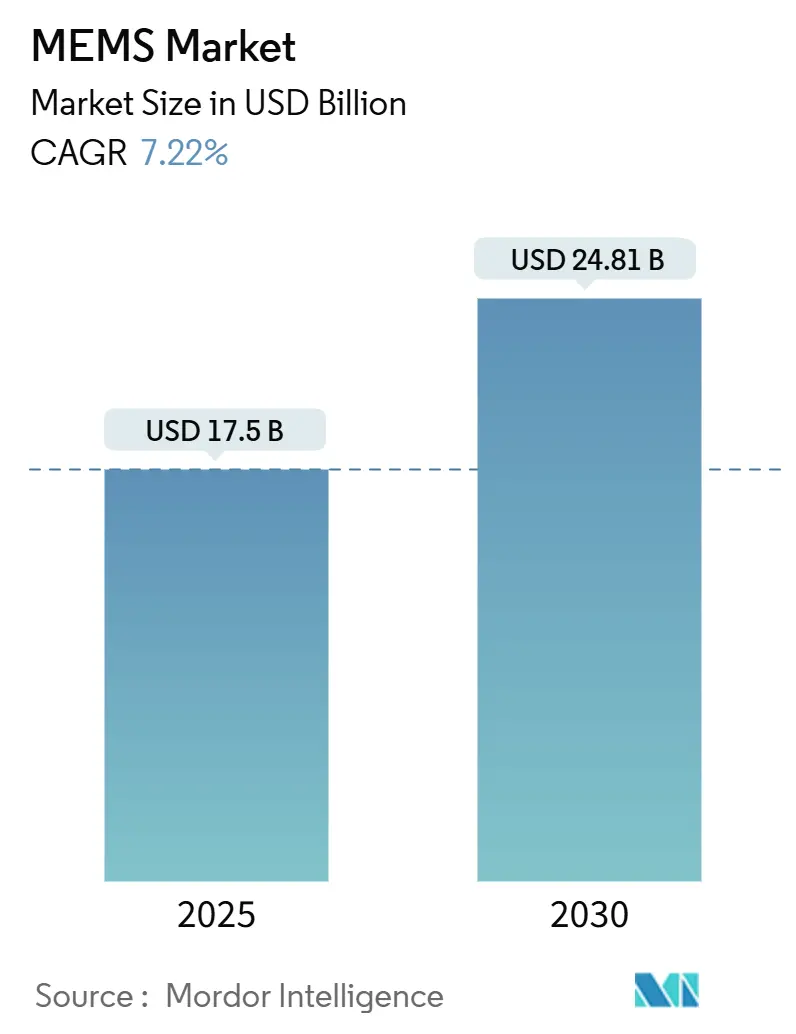

The global MEMS market size stands at USD 17.50 billion in 2025 and is projected to reach USD 24.81 billion by 2030, reflecting a steady 7.22% CAGR. Momentum stems from rising sensor penetration in smartphones, electric vehicles, medical wearables, and industrial IoT nodes that demand durable, low-power, and miniaturized components. Automotive electrification multiplies pressure, temperature, and inertial sensor counts per vehicle, while point-of-care diagnostics pull microfluidic chips from pilot lines into mass production. Advancing 5G infrastructure further amplifies demand for RF MEMS filters that sustain low insertion loss across expanding frequency bands. Supply resilience improves as 300 mm wafer processing enters pilot runs in the United States, yet competition remains fragmented, letting niche specialists capture design wins in emerging use-cases such as edge AI sensor fusion.

- By device class, sensors led with 57% revenue share in 2024, whereas microfluidic chips are forecast to expand at a 9.8% CAGR through 2030.

- By sensor/actuator type, inertial sensors commanded 24.5% of the MEMS market share in 2024, while RF MEMS exhibit the highest projected CAGR at 10.4% through 2030.

- By application, consumer electronics held 38% of the MEMS market size in 2024; healthcare is advancing at an 8.9% CAGR to 2030.

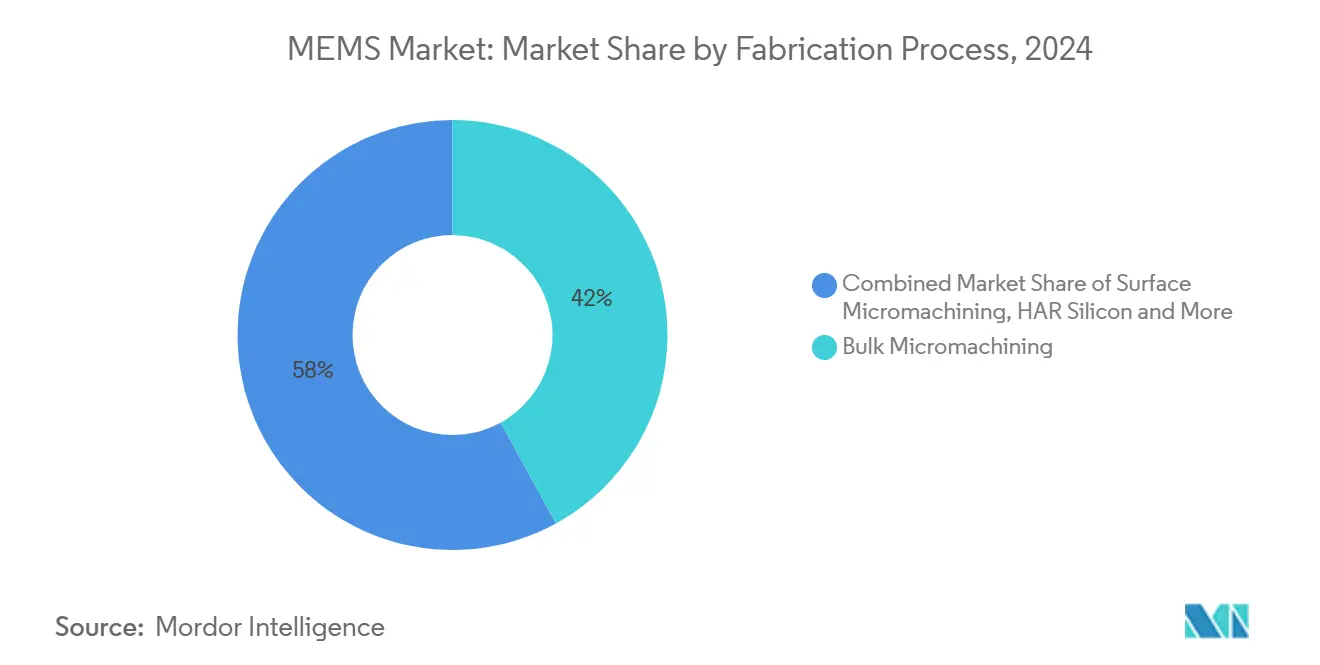

- By fabrication process, bulk micromachining captured 42% revenue share in 2024, whereas 3D-printed MEMS is projected to grow at an 8.22% CAGR between 2025-2030.

- By material, silicon dominated with 66% share in 2024, while piezoelectric materials are poised for 9.4% CAGR growth through 2030.

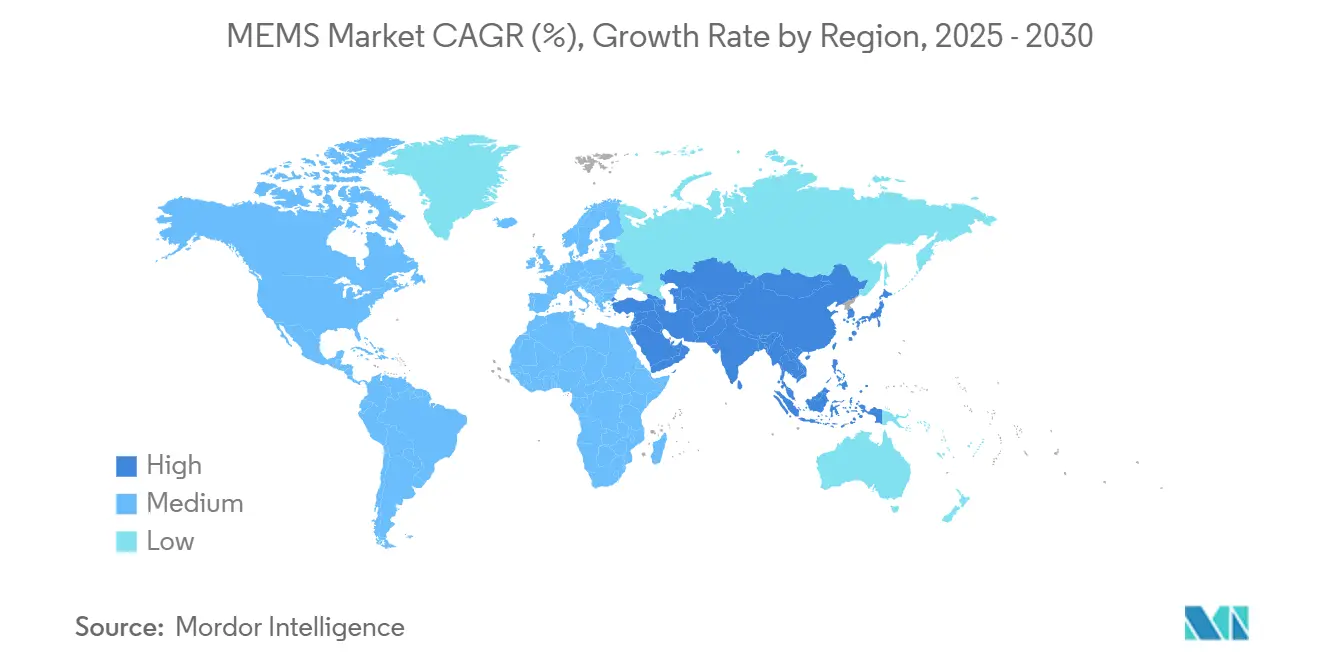

- By geography, Asia accounted for 45% of global revenue in 2024 and is forecast to post the fastest regional CAGR at 10.7% to 2030.

Global MEMS Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of IoT & edge devices | +1.8% | Global, with APAC leading deployment | Medium term (2-4 years) |

| Expanding sensor content in EV & ADAS | +1.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Proliferation of 5G driving RF MEMS filters | +1.2% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Surge in microfluidic MEMS for PoC diagnostics | +0.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising adoption of IoT & edge devices

The climb in connected endpoints obliges factories, buildings, and logistics hubs to embed dozens of sensors per asset, turning low-power accelerometers, gyroscopes, and environmental monitors into standard bill-of-materials components. Semiconductor companies increasingly package MEMS sensors with microcontrollers to deliver localized analytics that cut backhaul bandwidth and cloud latency. Edge AI chips that run decision trees or lightweight neural networks directly on sensor nodes push suppliers to rethink design rules for power budgets below 50 µW, prompting sustained redesign cycles that enlarge the MEMS market.

Expanding sensor content in EV & ADAS

Electric vehicles contain 2-3 × more pressure, inertial, and environmental sensors than internal-combustion cars. Murata’s new domestic line for automotive-grade inertial sensors underlines how Japanese suppliers pivot to mobility revenue as legacy handset volumes plateau newswitch. Optical MEMS mirrors from TDK enable adaptive headlights and solid-state LiDAR, adding differentiated sockets per vehicle. LiDAR vendor RoboSense captured 33.5% global automotive LiDAR revenue in 2024, underscoring the intertwined growth of advanced driver assistance and high-precision sensing.[1]RoboSense, “RoboSense Releases 2024 Annual Results,” Robotics Tomorrow

Proliferation of 5G driving RF MEMS filters

Massive MIMO base stations require hundreds of tunable RF paths. RF MEMS switches and filters deliver low insertion loss and high isolation between 600 MHz and 110 GHz, attributes difficult to replicate with solid-state devices.[2]Eric Westberg et al., “5G Infrastructure RF Solutions,” IEEE Microwave Magazine Integrated front-ends like NXP’s RapidRF accelerate time-to-deploy by embedding MEMS-based filter banks that dynamically align with evolving spectrum allocations.

Surge in microfluidic MEMS for PoC diagnostics

Healthcare systems replace central labs with bedside testing. NIH-backed ACME-POCT programs have shepherded 22 micro-scale diagnostic platforms from prototype to validation, reinforcing confidence in MEMS accuracy for clinical workflows.[3]National Institutes of Health, “Atlanta Center for Microsystems Engineered Point of Care Technologies”FDA clearance of the MY01 continuous compartment-pressure monitor in March 2025 demonstrates regulator trust in capacitive micro-sensors for critical care.[4]U.S. Food and Drug Administration, “MY01 Continuous Compartmental Pressure Monitor” Investment flows such as TDK Ventures’ funding of genome-editing start-up Mekonos highlight how microfluidics cross into therapeutics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex & capital-intensive manufacturing | −1.1% | Global, particularly affecting smaller players | Long term (≥ 4 years) |

| RF MEMS patent thickets raising licensing costs | −0.7% | Global, concentrated in developed markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Complex & capital-intensive manufacturing

Transitioning to 300 mm wafers cuts die cost but demands new lithography, bonding, and metrology tools whose acquisition can exceed USD 500 million per line. SEMI projects 6% growth in 300 mm wafer shipments in Q1 2025, yet smaller MEMS fabs struggle to raise capital for the upgrade.[5]SEMI, “Worldwide Silicon Wafer Shipments Increase 2% Year-on-Year in Q1 2025”U.S. CHIPS Act incentives ease financing for a handful of domestic projects, including Rogue Valley Microdevices’ Florida fab slated for 2025 production. Suppliers without -300 mm capacity face widening cost gaps that compress margins.

RF MEMS patent thickets raising licensing costs

RF MEMS innovations sit behind dense webs of overlapping claims. The USPTO forecasts 1.5% more patent filings in fiscal 2025, evidence that rights holders continue to extend coverage that can block new entrants. China-based firms filed 2,600 RF front-end patents between 2019-2023, giving domestic incumbents bargaining leverage over foreign OEMs. Extended negotiations delay product launches and inflate bill-of-materials costs, pressuring the MEMS market where time-to-design-win is critical.

Segment Analysis

By Device Class: Sensors Drive Volume, Microfluidics Lead Innovation

Sensors generated 57% of 2024 revenue as handset OEMs, automotive Tier-1 suppliers, and industrial automation houses all standardize inertial, pressure, and environmental packages. This dominant slice of the MEMS market underlines how mature manufacturing nodes deliver cost efficiency while maintaining reliability in harsh environments. The segment benefits from smartphones that embed up to six discrete motion and audio sensors, and vehicles that now integrate triple-redundant accelerometers for airbag, stability, and ADAS functions. In contrast, actuators deliver stable but slower growth tied to optical image-stabilization motors and micro-mirror arrays for LiDAR beam steering. Oscillators displace quartz timing in automotive powertrains, foreseeing rising attach rates as electrification accelerates.

Microfluidic chips, at 9.8% CAGR, represent the technology frontier. Lab-on-a-chip cartridges combine capillary flow control, electrochemical sensing, and on-board reagents, cutting diagnostic cycle time from days to minutes. Hospital procurement managers value simplified sample prep and minimal operator training, pushing device makers toward fully disposable units that rely on polymer-based MEMS flow channels. Pharmaceutical firms explore organ-on-chip platforms to model human tissue response, creating additional pull for high-precision microfluidic fabrication. This emerging basket supports sustained differentiation and positions suppliers that master surface chemistry as premium partners, expanding the MEMS market beyond traditional electromechanical spheres.

Note: Segment shares of all individual segments available upon report purchase

By Sensor/Actuator Type: Inertial Sensors Dominate, RF MEMS Accelerate

Inertial sensors secured 24.5% of 2024 revenue, underpinning smartphone orientation detection, automotive rollover protection, and industrial track-and-trace modules. Their proven reliability under vibration and temperature extremes cements the category’s relevance within the MEMS market. Continuous performance improvements, such as bias drift under 1°/h, extend use-cases into precision agriculture and warehouse automation robotics. Meanwhile, RF MEMS components deliver 10.4% CAGR as 5G deployments request agile spectrum tuning unattainable with fixed ceramic filters. Foundries invest in hermetic wafer-level packaging to guard high-Q cavities against moisture ingress, safeguarding yield and elevating average selling prices.

MEMS microphones, pressure sensors, and environmental detectors sustain steady volume growth. STMicroelectronics’ 2024 release of an autonomous industrial IMU that integrates finite-state-machine logic underscores the pivot toward edge intelligence where small code snippets filter events before transmission. Optical MEMS mirrors advance solid-state LiDAR, benefiting from minimal moving mass and mechanical fatigue resistance.

By Application: Consumer Electronics Lead, Healthcare Accelerates

Consumer electronics retained 38% share in 2024 as flagship handsets and wearables continue multi-sensor integration. Unit demand rises but average selling price pressure keeps revenue trajectories moderate, requiring device makers to differentiate through adding edge-AI co-processors that boost bill-of-materials resilience. Automotive end-markets grow sensor count per vehicle for battery management, cabin monitoring, and ADAS redundancy. Industrial IoT implementations migrate from pilot cells to full production lines, leveraging vibration and thermal data to extend equipment service intervals.

Healthcare posts 8.9% CAGR by 2030. FDA clearances for MEMS-based diagnostic tools, such as continuous compartment-pressure monitors, legitimize use in critical-care pathways. Wearable medical patches equipped with piezoelectric micro-pumps and pressure sensors support outpatient chronic-disease management. Telecom infrastructure remains vital as operators densify small-cell networks; RF MEMS filters and switches lower power consumption per site, improving total cost of ownership for network gear.

By Fabrication Process: Bulk Micromachining Leads, 3D Printing Emerges

Bulk micromachining captured 42% of 2024 revenue thanks to its compatibility with existing semiconductor toolsets, enabling rapid amortization of capital. Deep-reactive ion etching advances reinforce aspect-ratio control, granting designers wider latitude to sculpt resonant cavities or through-silicon vias in a single masking step. Wafer throughput advantages keep cost-per-die low, sustaining competitiveness across high-volume sensor families that anchor the MEMS market.

3D-printed MEMS grows quickest at 8.22% CAGR, serving rapid-prototype cycles for aerospace and biomedical instrumentation. Additive processes allow complex hollow structures unattainable in subtractive silicon micromachining and foster hybrid assemblies combining metals and polymers. Rogue Valley Microdevices’ plan to initiate 300 mm additive MEMS lines highlights momentum toward scaling novel geometries for production volumes. Surface micromachining, SOI technologies, and LIGA keep supporting optical and RF devices where multilayer control over thin-film stress or X-ray lithography precision is essential.

Note: Segment shares of all individual segments available upon report purchase

By Material: Silicon Dominates, Piezoelectric Materials Accelerate

Silicon accounted for 56% of 2024 revenue, an anchor enabled by mature supply chains, defect-density learning curves, and continuous process design kits that simplify tape-out cycles. The MEMS market relies on silicon’s thermal match with CMOS, allowing monolithic integration of analog signal conditioning to shrink die footprints. Polymers gain traction in disposable medical diagnostics where biocompatibility and flexibility matter more than thermal conductivity. Metals provide high-conductivity electrodes and structural anchors, while compound semiconductors furnish RF MEMS with superior high-frequency loss characteristics.

Piezoelectric materials exhibit 9.4% CAGR, largely for automotive actuators and energy-harvesting patches in industrial deployments. Aluminum nitride on silicon substrates doubles as both a dielectric layer and an active transducer, allowing vendors like TDK to propose higher-density inverter modules for electric drivetrains. Research programs evaluate lead-free PZT replacements to align with tightening environmental directives, promising new revenue streams as formulations reach automotive qualification.

Geography Analysis

Asia-Pacific retained 45% revenue share in 2024 and is tracking a 10.7% CAGR through 2030. China’s domestic vendors accelerate patent filings in RF front-ends, aiming to localize supply for 5G and satellite communications. Japanese champions TDK and Murata extend capacity for automotive-grade inertial sensors to capture global electrification demand. South Korea leverages advanced memory cleanrooms to diversify into MEMS timing devices, while Singapore and Malaysia expand test-and-assembly clusters that offer lower labor cost structures.

North America benefits from strong aerospace and defense programs as well as medical device innovation pipelines. The CHIPS Program Office awarded multi-billion-dollar grant negotiations to fabs that incorporate MEMS pilot lines, encouraging shorter domestic supply chains. Silicon wafer shipments rose 2.2% year-on-year in Q1 2025, with 300 mm category demand signalling readiness for high-volume production. Florida’s new MEMS foundry will add regional resilience when it enters volume production in 2025.

Europe concentrates on automotive safety, industrial automation, and medical wearables. Regulatory frameworks mandating advanced driver assistance functions accelerate sensor penetration, boosting the region’s contribution to the MEMS market. STMicroelectronics’ autonomous industrial IMU caters to stringent long-lifecycle demands from German and Italian equipment makers. The Middle East and Africa remain nascent, yet smart-city pilots in Gulf states create lighthouse references for distributed air-quality sensing and intelligent lighting.

Competitive Landscape

The MEMS market shows moderate concentration, with diversified revenue across consumer, automotive, and industrial verticals preventing any single supplier from exceeding 15% share. Bosch, Broadcom, and STMicroelectronics leverage captive 200 mm to 300 mm fabs that yield scale benefits and automotive qualification depth. TDK catapulted to the 3rd global rank after integrating InvenSense’s inertial portfolio, validating acquisition-driven portfolio expansion. Chinese challengers cultivate domestic RF MEMS capacity, underwritten by local demand for 5G radios, thereby tightening lead-time commitments offered to regional OEMs.

Consolidation persists. Syntiant’s USD 150 million purchase of Knowles’ consumer MEMS microphone division augments its edge-AI chipset roadmap with proven acoustic front-ends, letting the buyer bundle voice processing into turnkey modules. Bosch Ventures earmarked USD 270 million for start-ups in automation and electrification, signalling corporate venture capital as a supplementary scouting tool for disruptive MEMS concepts. Patent fences in RF MEMS create licensing income for early movers but can stifle smaller actors, encouraging cross-licensing alliances that mitigate royalty outlays.

Strategic capacity investments shape competitive moats. Rogue Valley Microdevices’ 300 mm U.S. fab promises domestic low-volume, high-mix runs attractive to medical-device OEMs requiring ISO-13485 compliance. European foundries focus on specialty piezoelectric lines to serve haptics and actuator niches, doubling down on material science depth. Suppliers differentiate by bundling firmware and algorithms that compress customer development time, thereby raising switching costs and sustaining pricing discipline despite overall unit price erosion in commoditized sensor categories.

MEMS Industry Leaders

-

Broadcom Inc.

-

Robert Bosch GmBH

-

STMicroelectronics NV

-

Texas Instruments Inc.

-

Qorvo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bosch Ventures committed USD 270 million to automation and electrification start-ups, aiming to secure early access to next-generation sensing technologies that complement Bosch’s automotive and industrial portfolios.

- April 2025: TDK, Kirin Holdings, and Murata launched Japan’s first chemical recycling loop for PET resin in non-food electronic packaging, aligning MEMS component supply chains with circular-economy goals.

- March 2025: The FDA cleared MY01 Inc.’s continuous compartment-pressure monitor, embedding capacitive MEMS sensors, signalling regulatory confidence in microscale diagnostics for orthopedic trauma care.

- January 2025: Omnitron Sensors raised USD 13 million to accelerate novel MEMS architectures targeting lower capex per wafer, seeking to democratize access for mid-tier fabless designers.

Global MEMS Market Report Scope

Micro-electromechanical systems (MEMS) technology is defined as the miniaturization of mechanical and electromechanical elements, such as devices and structures, manufactured and fabricated using microfabrication techniques. The types of MEMS devices vary from relatively simple structures with no moving elements to structures with multiple moving elements under the control of integrated microelectronics.

The MEMS Market is segmented by type (RF MEMS, oscillators, microfluidics, environmental MEMS, optical MEMS, MEMS microphones, inertial MEMS, pressure MEMS, thermopiles, microbolometers, inkjet heads, accelerometers, and gyroscopes), by application (automotive, healthcare, industrial, consumer electronics, telecom, aerospace, and defense), and by geography (North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa). The market sizes and forecasts are provided in terms of value in USD for all the segments.

| By Device Class | Sensors | |||

| Actuators | ||||

| Oscillators and Timing | ||||

| Microfluidic Chips | ||||

| Power/Motion Micro-generators | ||||

| By Sensor / Actuator Type | Inertial Sensors | |||

| Pressure Sensors | ||||

| RF MEMS | ||||

| Optical MEMS | ||||

| Environmental Sensors | ||||

| MEMS Microphones | ||||

| Microbolometers and IR Detectors | ||||

| Ink-jet Heads | ||||

| Others | ||||

| By Application | Consumer Electronics | |||

| Automotive | ||||

| Industrial and Robotics | ||||

| Healthcare and Medical Devices | ||||

| Telecom Infrastructure | ||||

| Aerospace and Defense | ||||

| Others | ||||

| By Fabrication Process | Bulk Micromachining | |||

| Surface Micromachining | ||||

| HAR Silicon Etching / DRIE | ||||

| Silicon-on-Insulator (SOI) MEMS | ||||

| LIGA and X-ray Lithography | ||||

| Advanced 3D-Printed MEMS | ||||

| By Material | Silicon | |||

| Polymers | ||||

| Piezoelectric (AlN, PZT) | ||||

| Metals | ||||

| Compound Semiconductors | ||||

| Quartz and Glass | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| France | ||||

| United Kingdom | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| APAC | China | |||

| Japan | ||||

| South Korea | ||||

| India | ||||

| Southeast Asia | ||||

| Australia and New Zealand | ||||

| Rest of APAC | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| UAE | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

| Sensors |

| Actuators |

| Oscillators and Timing |

| Microfluidic Chips |

| Power/Motion Micro-generators |

| Inertial Sensors |

| Pressure Sensors |

| RF MEMS |

| Optical MEMS |

| Environmental Sensors |

| MEMS Microphones |

| Microbolometers and IR Detectors |

| Ink-jet Heads |

| Others |

| Consumer Electronics |

| Automotive |

| Industrial and Robotics |

| Healthcare and Medical Devices |

| Telecom Infrastructure |

| Aerospace and Defense |

| Others |

| Bulk Micromachining |

| Surface Micromachining |

| HAR Silicon Etching / DRIE |

| Silicon-on-Insulator (SOI) MEMS |

| LIGA and X-ray Lithography |

| Advanced 3D-Printed MEMS |

| Silicon |

| Polymers |

| Piezoelectric (AlN, PZT) |

| Metals |

| Compound Semiconductors |

| Quartz and Glass |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| APAC | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Southeast Asia | |||

| Australia and New Zealand | |||

| Rest of APAC | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the global MEMS market and how fast is it growing?

The MEMS market size is USD 17.5 billion in 2025 and is forecast to expand to USD 24.8 billion by 2030 at a 7.22% CAGR.

Which MEMS device class is expanding the fastest?

Microfluidic chips lead growth with a projected 9.8% CAGR through 2030, driven by rising point-of-care diagnostic adoption.

How does 5G deployment affect demand for MEMS components?

5G infrastructure sharply increases requirements for RF MEMS filters and switches that deliver low-loss, high-isolation performance across wider frequency bands.

Which end-use application holds the largest revenue share today?

Consumer electronics account for 38% of total MEMS revenue in 2024 thanks to multi-sensor integration in smartphones, tablets, and wearables.

Why is Asia-Pacific considered the dominant regional market?

Asia-Pacific captures 45% of global revenue because of its extensive semiconductor fabrication base, strong consumer-electronics production, and accelerating EV and 5G rollouts.

What manufacturing trend is reshaping cost structures for MEMS suppliers?

The transition to 300 mm wafer processing—highlighted by new U.S. fabs slated for 2025 production—lowers die cost but raises capital requirements, favoring scale players.