Medication Adherence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

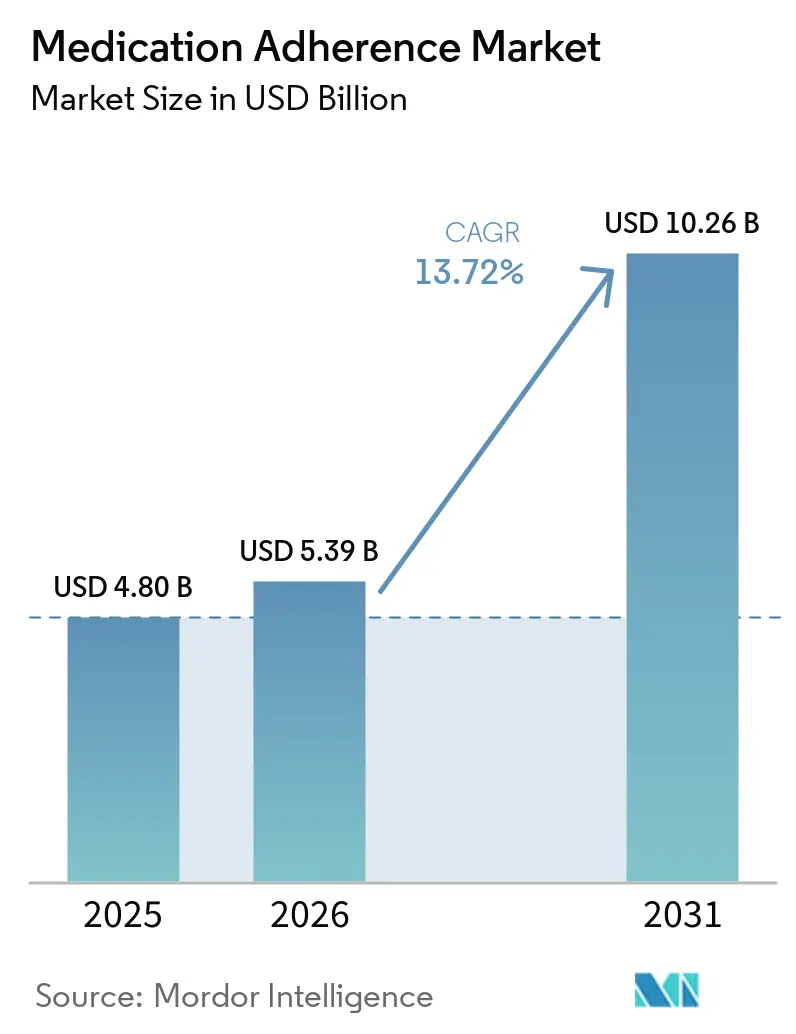

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 10.26 Billion |

| Growth Rate (2026 - 2031) | 13.72% CAGR |

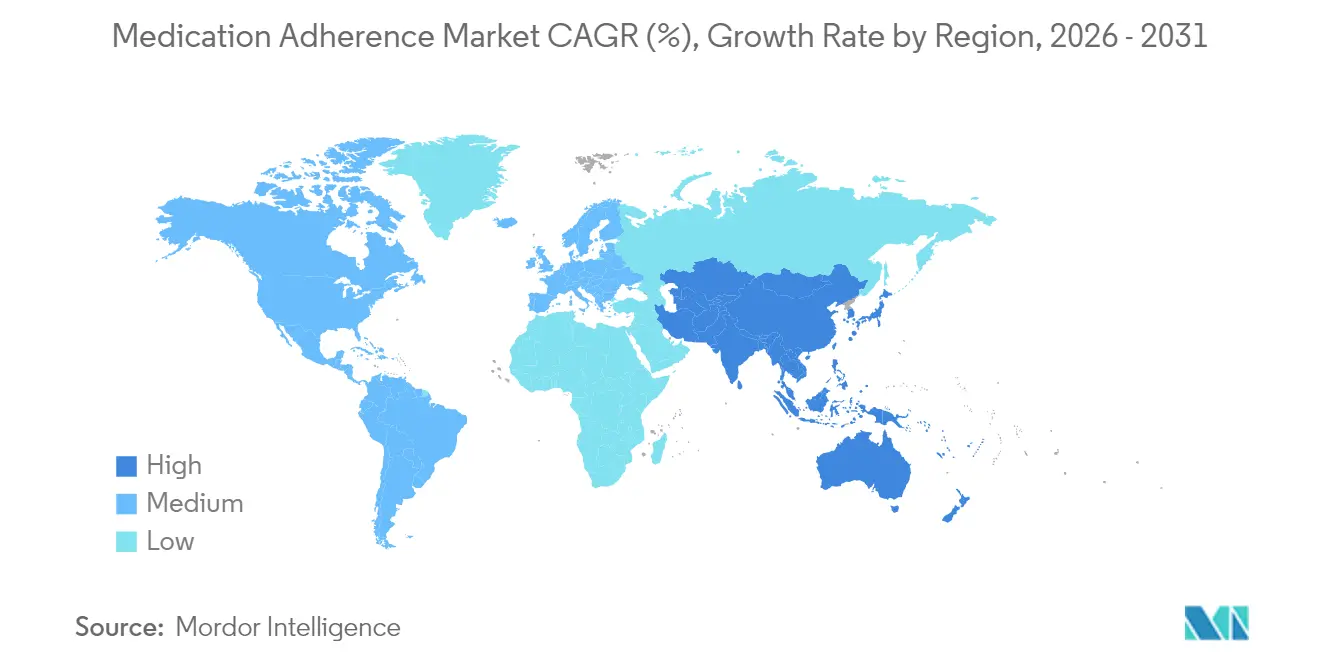

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medication Adherence Market Analysis by Mordor Intelligence

The Medication Adherence Market size is expected to grow from USD 4.80 billion in 2025 to USD 5.39 billion in 2026 and is forecast to reach USD 10.26 billion by 2031 at 13.72% CAGR over 2026-2031.

Rising chronic-disease prevalence, fast-expanding digital therapeutics regulations, and mounting pressure to curb the USD 125 billion annual cost of non-adherence in Europe propel the uptrend.[1]Source: European Cooperation in Science and Technology, “Technological Solutions for Improving Medication Adherence,” cost.eu Software-centric platforms lead adoption because smartphone diffusion and AI analytics enable payers and providers to share risk and tie reimbursement to adherence outcomes. At the same time, hardware solutions such as smart inhalers gain momentum as objective verification tools, reinforcing value-based-care contracts. Hospitals remain the dominant customers, yet home care gains ground on the back of decentralized clinical trials and remote patient monitoring. Geographically, North America holds the largest portion of revenue, while Asia Pacific records the fastest expansion due to widespread mobile-health uptake and large-scale public investment.

Key Report Takeaways

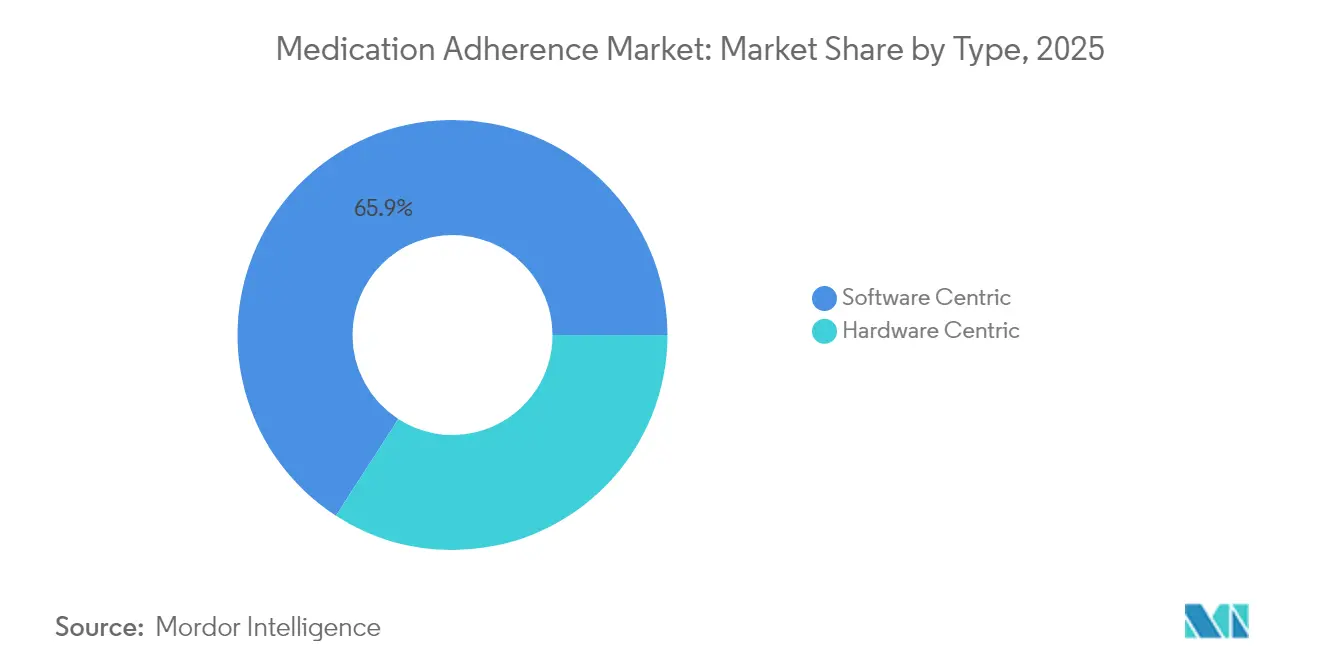

- By type, software centric segment held 65.88% of the medication adherence market share in 2025; hardware solutions are forecast to grow at a 15.39% CAGR through 2031.

- By medication class, cardiovascular segment led with 28.62% revenue share in 2025; oncology medicines are projected to expand at a 15.72% CAGR to 2031.

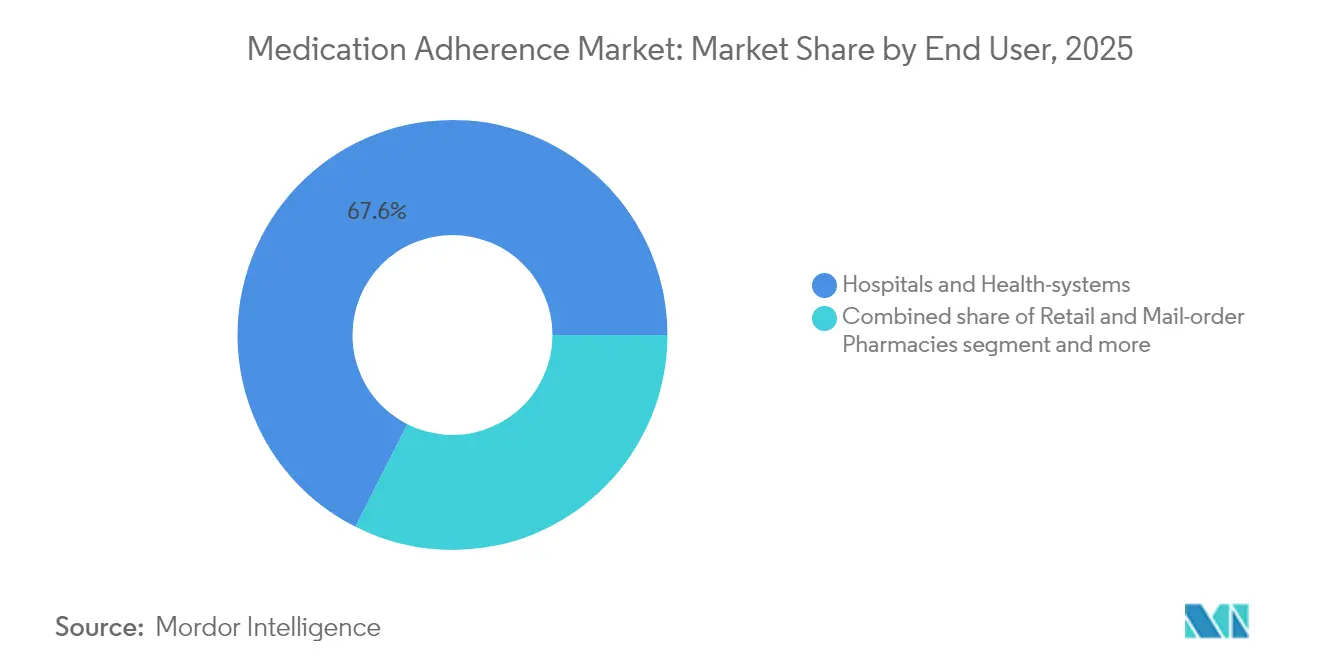

- By end user, hospitals and health systems commanded 67.55% of the medication adherence market size in 2025, while home-care settings are advancing at a 14.54% CAGR through 2031.

- By geography, North America accounted for 38.12% of the medication adherence market in 2025; Asia Pacific is forecast to grow at a 15.02% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Medication Adherence Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-disease burden & ageing demographics | +3.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Value-based-care incentives tying reimbursement to adherence outcomes | +2.8% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Rapid consumer adoption of mHealth and smartphones | +2.1% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| AI-driven predictive adherence analytics enabling risk-sharing contracts | +1.9% | North America & EU, early adoption in urban APAC | Medium term (2-4 years) |

| Demand from decentralised clinical trials for remote adherence verification | +1.4% | Global, with concentration in major pharmaceutical hubs | Short term (≤ 2 years) |

| Employer-sponsored PBM programmes embedding adherence guarantees | +1.1% | North America primarily, limited EU adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic-disease burden & ageing demographics

Global adherence gaps widen as populations age and multimorbidity rises. Half of all patients do not follow prescribed regimens, and the proportion climbs to 60% among older adults coping with multiple conditions. Every percentage-point improvement can save healthcare systems USD 2-7 billion per year. China’s integrated digital platforms illustrate tangible value, delivering 3.4% larger post-prandial glucose reductions among highly compliant diabetes patients compared with standard care. The demographic shift toward outcome-based reimbursement intensifies the focus on adherence measurement and intervention.

Value-based-care incentives linking pay to adherence outcomes

Medicare Advantage star-rating rules in the United States embed adherence metrics directly into reimbursement, pushing providers to adopt monitoring technologies that drive quality scores. Analyses show that patients missing adherence measures incur 11-20% higher costs depending on the number of gaps. Results from Aetna’s programs reveal a 49% jump in members reaching HbA1c targets alongside a 7% decline in hospital admissions after value-based models replaced fee-for-service contracts. The Duke-Margolis Center estimates that harmonizing drug and delivery reforms could unlock USD 50 billion in savings annually while widening access.

Rapid consumer adoption of mHealth and smartphones

Smartphone penetration exceeds 80% in priority markets, making app-based reminders and education readily accessible. Randomized trials in China report that mobile interventions boost gout medication adherence more effectively than routine care over 24 weeks. AI-powered personalization heightens engagement, yet older adults still cite usability and family support as essential factors for sustained use.

AI-driven predictive adherence analytics enabling risk-sharing contracts

Machine-learning models reach 87.25% accuracy in forecasting daily adherence among breast-cancer survivors, allowing pharmaceutical firms to guarantee outcomes in payer agreements. The FDA’s 2025 framework for AI credibility in submissions confirms regulator openness to predictive adherence endpoints. Platforms such as AllazoHealth combine algorithms with behavioral interventions to reduce therapy drop-off.

Restraints Impact Analysis of Medication Adherence Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient-data privacy and cyber-security concerns | -1.8% | Global, with highest impact in EU due to GDPR | Short term (≤ 2 years) |

| High upfront cost of connected hardware for providers and payers | -1.3% | Global, with disproportionate impact in emerging markets | Medium term (2-4 years) |

| Algorithmic bias in AI adherence platforms attracting regulatory scrutiny | -1.1% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Limited reimbursement pathways for digital therapeutics beyond diabetes & mental-health | -0.9% | Global, with varying impact by healthcare system maturity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient-data privacy and cyber-security concerns

GDPR enforcement heightens compliance complexity for vendors operating in Europe, prompting larger investments in encryption, consent management, and audit trails. The FDA’s Digital Health Advisory Committee underscores the security expectations for connected devices, while prominent acquisitions such as 23andMe trigger public debate about genetic data stewardship. Fragmented national rules across the EU add further cost and implementation hurdles.

High upfront cost of connected hardware for providers and payers

Smart inhalers, electronic pillboxes, and wearables carry capital costs that strain budgets, especially in lower-income regions. Meta-analyses highlight 12% average device-failure rates that create replacement and support expenses. For manufacturers, tariff exposure raises input costs, as illustrated in Omnicell’s earnings commentary that flagged USD 40 million of additional charges tied to hardware imports. Device-as-a-service subscriptions and risk-sharing contracts are emerging financing mechanisms, but they require mature contracting capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medication Adherence Market Segment Analysis

By Type:

Hardware Acceleration Drives Connected CareHardware-centric solutions accounted for 34.12% of revenue in 2025 but are growing at a 15.39% CAGR, the fastest across the medication adherence market. Smart inhalers, automated dispensers, and ingestible sensors generate definitive, time-stamped dose records that underpin value-based payment and clinical-trial verification. The Hailie Smartinhaler, FDA-cleared for use with multiple AstraZeneca therapies, has deployed more than 170,000 sensors worldwide and features in over 95 peer-reviewed studies, demonstrating clinical traction.

Market momentum reflects the need for verifiable dosing information that software reminders cannot provide in isolation. Next-generation smart pill dispensers now integrate 28 secure dosing chambers with cellular connectivity, enabling real-time analytics and caregiver alerts. University of Southern California engineers are testing AI-guided swallowable devices that locate pills inside the gastrointestinal tract and report transit patterns. The hardware surge pushes the medication adherence market size for connected devices toward double-digit expansion through 2031 while forcing vendors to refine durability and user-friendliness.

By Medication Class:

Oncology Urgency Accelerates InnovationCardiovascular drugs represented 28.62% revenue in 2025, the largest slice of the medication adherence market. Continuous monitoring is fundamental to hypertension and heart-failure management, and digital interventions have lifted adherence rates above 80% in supported cohorts. In contrast, oncology records the highest growth at 15.72% CAGR. High-cost oral therapies such as relugolix generate economic and clinical consequences when non-adherence leads to progression; real-world studies show more than 90% adherence among Medicare beneficiaries, underscoring the urgency of precision support.

Central nervous system agents illustrate adherence complexity: forgetfulness impairs 42% of enzalutamide users versus 17% of abiraterone users among elderly patients. Diabetes regimens benefit from continuous-glucose monitors paired with smartphone apps such as Gluroo, which demonstrate improved self-care behaviors over traditional logging methods. Respiratory drugs rely heavily on connected inhalers, though device durability remains a constraint. Overall, oncology’s urgency and budget impact anchor sustained investment in specialized adherence interventions.

By End User:

Home Care Transformation Reshapes DeliveryHospitals and health systems captured 67.55% of medication adherence market share in 2025 thanks to centralized purchasing and enterprise workflow integration. Omnicell generated USD 270 million in Q1 2025 revenue on the strength of its XT Amplify automation suite, reflecting sustained institutional demand.

Home-care environments are the fastest-growing channel at 14.54% CAGR through 2031. FDA guidance on decentralized trials encourages sponsors to equip participants with user-friendly digital tools that collect adherence evidence without site visits. Retail and mail-order pharmacies leverage deep customer engagement: CVS Health’s updated mobile app grew its active user base by 22% after adding personalized reminders and AI search features. Innovations such as MIT’s CircTrek wearables that track therapeutic cells in real time will further shift high-acuity therapies into the home setting.

Geography Analysis

North America Medication Adherence Market

North America held 38.12% of revenue in 2025 on the strength of value-based-care incentives, sophisticated PBM programs, and clear digital-health regulations. CMS is rolling out electronic-prescribing interoperability standards by 2027, steering providers toward integrated platforms for adherence tracking. CVS Health’s USD 20 billion modernization plan spans nearly 10,000 retail pharmacies and more than 1,100 clinics, illustrating private-sector commitment to end-to-end digital infrastructure. Canada and Mexico contribute meaningful growth via cross-border tele-pharmacy services that require robust monitoring to validate remote dispensing.

APAC Medication Adherence Market

Asia Pacific is the fastest-growing region, expanding at 15.02% CAGR through 2031. China’s rural Health All-in-One Machines increased patient visits by 37.85% and pharmaceutical sales by 32.84% after full deployment, demonstrating measurable impact. Mobile-health adoption rates surpass 80% in multiple disease-management programs, paving the way for large-scale adherence data collection. Japan’s insurance-claim analytics indicate 76.7% mean medication-possession ratios for bisphosphonate therapy, confirming advanced monitoring capabilities. India adapts culturally tailored apps and bilingual reminders to raise adherence across diverse populations.

EMEA and LATAM Medication Adherence Market

Europe enforces stringent data-privacy and device regulations that raise compliance costs but ultimately build trusted ecosystems. GDPR drives vendors to enhance consent and encryption processes, while the medical-device regulation introduces stricter post-market surveillance expectations. Regional scaling studies reveal that harmonized standards and strategic partnerships are essential for cross-border platform deployment. In the Middle East and Africa, South Africa spearheads telemedicine uptake, and GCC smart-city projects embed medication-management systems. Latin America’s growth centers on Brazil and Argentina, where public programs integrate digital adherence support to address chronic disease burdens in underserved communities.

Competitive Landscape

Competition in the medication adherence market is moderately fragmented, with cloud-based platform providers, connected-device specialists, and diversified health conglomerates pursuing differentiated strategies. Omnicell leads in hospital pharmacy automation through its OmniSphere cloud orchestration and XT Amplify upgrade path, targeting USD 1.9-2 billion annual revenue by 2025. CVS Health exploits its nationwide footprint and extensive data assets to build integrated adherence ecosystems that link retail, mail, and virtual care. Cardinal Health is expanding specialty-drug services through acquisitions valued at USD 3.9 billion, strengthening its presence in gastroenterology and advanced diabetes supplies.

AI-driven personalization forms a critical white space. Predictive-analytics vendors partner with payers and pharmaceutical firms to structure risk-sharing contracts that guarantee outcome targets. Hardware innovators develop ingestible sensors and connected inhalers that capture hard evidence of dose events, enhancing the credibility of value-based payments. Market consolidation accelerates: Akili Interactive was acquired for USD 34 million after reimbursement hurdles slowed independent growth, and Pear Therapeutics filed for bankruptcy, signaling financial pressure on single-product developers. The FDA’s 2025 draft guidance for AI-enabled devices rewards companies with rigorous clinical validation and quality systems, encouraging scale players to absorb niche startups.

Future competition will hinge on interoperability, user experience, and payer alignment. Vendors that combine hardware, software, and analytics within unified data architectures are best positioned to manage end-to-end medication adherence life cycles. Partnerships between device manufacturers and electronic-health-record vendors are expected to deepen, while class-II and class-III device makers explore hybrid subscription models that blend equipment leasing with continuous analytics. As real-world evidence requirements for reimbursement expand, ownership of longitudinal adherence datasets will become an increasingly strategic asset.

Medication Adherence Industry Leaders

AdhereTech

McKesson Corporation

Omnicell, Inc.

Medminder Systems, Inc.

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Medication Adherence Market Companies Covered in this Report

- Omnicell

- Cardinal Health

- Mckesson

- Koninklijke Philips

- Johnson & Johnson

- AdhereTech

- Medminder Systems

- Proteus Digital Health

- CVS Health (Caremark)

- Walgreens Boots Alliance

- AdhereHealth

- Pear Therapeutics

- Validose

- AstraZeneca (Propeller/Respiro)

- Baxter

Recent Industry Developments in Medication Adherence Market

- February 2025: Validose raised USD 2 million to combat clinical-trial non-adherence with AI-powered medication-delivery systems.

- December 2024: Omnicell announced OmniSphere, a cloud-native software workflow engine that integrates robotics and smart devices across care settings.

- August 2024: Omnicell launched Central Med Automation Service to improve adherence through enhanced automation in healthcare facilities.

Medication Adherence Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the medication adherence market as the total annual revenue generated worldwide from purpose-built software platforms, connected sensors, smart packaging, and related services that help patients follow prescribed dosage, timing, and duration instructions. According to Mordor Intelligence, value is tracked at the point where adherence functionality is delivered to payers, providers, or consumers.

Scope exclusion: traditional pharmacy automation hardware that does not monitor or prompt patient behavior is outside this analysis.

Segments Covered in This Report

- By Type

- Hardware Centric

- Software Centric

- By Medication Class

- Cardiovascular

- Central Nervous System

- Diabetes

- Oncology

- Respiratory

- Gastrointestinal

- Musculoskeletal

- Other Medication Classes

- By End User

- Hospitals and Health-systems

- Retail and Mail-order Pharmacies

- Home-care Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Analysts interviewed clinicians, hospital pharmacy managers, payers, and founders of digital health firms across North America, Europe, and Asia-Pacific. Conversations validated adoption thresholds, average selling prices, and likely upgrade cadences, enabling us to plug real-world guardrails into model assumptions.

Desk Research

We began with extensive literature sweeps of tier-1 public sources such as the World Health Organization, the U.S. Centers for Medicare & Medicaid Services, Eurostat, the International Pharmaceutical Federation, and peer-reviewed titles including JAMA and the BMJ. Company 10-Ks, investor decks, patent filings, and regulatory dossiers supplied cost benchmarks and pipeline counts. Where financial disclosures were sparse, Mordor analysts leveraged D&B Hoovers and Dow Jones Factiva to triangulate revenue streams. These examples illustrate, yet do not exhaust, the secondary inputs reviewed.

A parallel desk effort mapped regional prescription volumes, smartphone penetration, and chronic disease incidence to anchor demand pools. Country-level reimbursement guidelines and device approval registers then refined the accessible segment.

Market-Sizing & Forecasting

A top-down construct starts with national prescription counts and chronic disease cohorts, which are then adjusted for typical non-adherence rates and technology penetration. Select bottom-up cross-checks, supplier roll-ups and sampled ASP × unit volumes, calibrate totals. Variables tracked include repeat-prescription share, smartphone coverage, e-pharmacy growth, device replacement cycles, regulatory incentives, and medication error costs. Multivariate regression ties these drivers to historic revenue patterns, while scenario analysis stress-tests upside and downside paths through 2030.

Data Validation & Update Cycle

Outputs undergo variance checks against external benchmarks, peer review by a senior analyst, and reruns if anomalies persist. Models refresh annually, with interim updates when material events, major reimbursement changes and landmark product approvals, occur.

How Mordor Intelligence's Medication Adherence Market Size Compares to Other Published Estimates

Published estimates differ because firms adopt distinct scopes, variable selections, and refresh cadences. Some track only connected devices, others bundle broader medication management software, and currency conversions or ASP deflators vary widely.

Key gap drivers include: (a) Mordor reports revenue from all adherence-focused software, hardware, and service layers, whereas several publishers isolate hardware; (b) our model blends primary price points with real prescription volumes, while others rely mainly on desk data; (c) yearly updates capture fast-moving launches that slower cycles miss.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.88 B (2025) | Mordor Intelligence | - |

| USD 4.10 B (2024) | Global Consultancy A | Software-only scope; services omitted |

| USD 3.90 B (2024) | Market Publisher B | Uniform ASP compression, limited primary validation |

| USD 4.50 B (2025) | Industry Analyst C | Smart-device focus, reminder apps excluded |

These contrasts show that Mordor's balanced, transparently sourced approach produces a dependable baseline that decision-makers can retrace, test, and confidently apply.

Key Questions Answered in the Report

What is the current Global Medication Adherence Market size?

The Global Medication Adherence Market is projected to register a CAGR of 13.86% during the forecast period (2026-2031)

Who are the key players in Global Medication Adherence Market?

AdhereTech, McKesson Corporation, Omnicell, Inc., DrFirst and Medminder Systems, Inc. are the major companies operating in the Global Medication Adherence Market.

Which is the fastest growing region in Global Medication Adherence Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Medication Adherence Market?

In 2025, the North America accounts for the largest market share in Global Medication Adherence Market.

What years does this Global Medication Adherence Market cover?

The report covers the Global Medication Adherence Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Medication Adherence Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: