Medical Suction Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.60 Billion |

| Market Size (2031) | USD 25.52 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

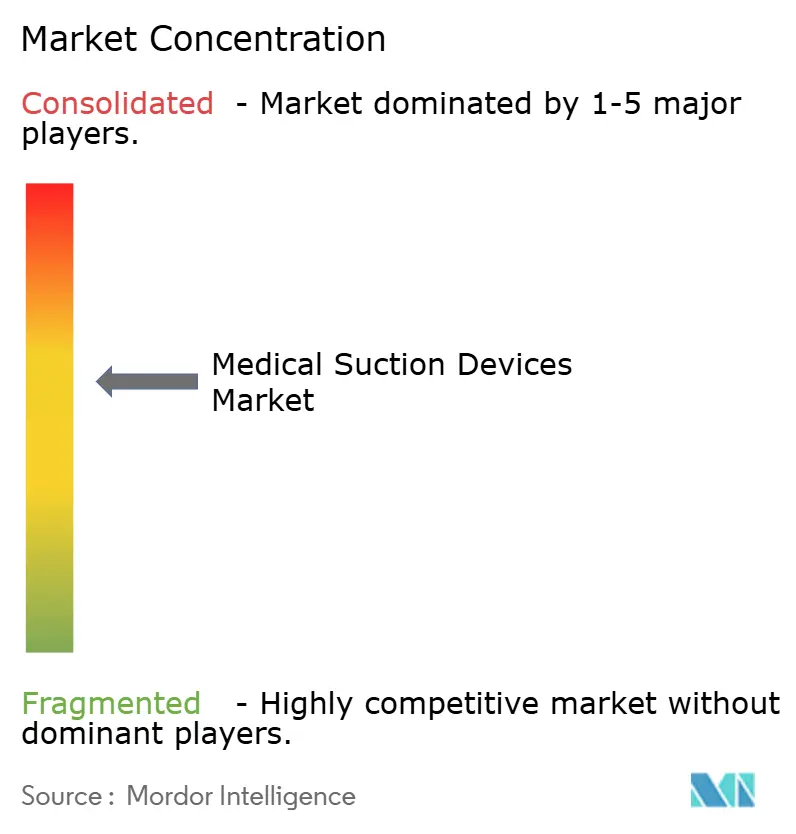

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Suction Devices Market Analysis by Mordor Intelligence

Medical Suction Devices Market size in 2026 is estimated at USD 19.60 billion, growing from 2025 value of USD 18.60 billion with projections showing USD 25.52 billion, growing at 5.42% CAGR over 2026-2031.

Rising surgical throughput, a persistent burden of chronic respiratory disease, and the shift of care to home settings continue to shape capital-equipment priorities across hospitals and alternate-site providers. Portable and dual-powered units increasingly complement fixed wall systems as health systems prepare for grid instability, emergency surge events, and value-based payment incentives that tie reimbursement to shorter lengths of stay. Regulatory scrutiny around ventilator-associated pneumonia and catheter sterility is elevating technical specifications, prompting suppliers to integrate closed-circuit designs, antimicrobial materials, and automated usage logging. Large manufacturers are strengthening supply-chain resilience by regionalizing component sourcing and expanding clean-room capacity, while smaller entrants differentiate on connectivity and ergonomics to reach underserved ambulatory and home-care niches.

Key Report Takeaways

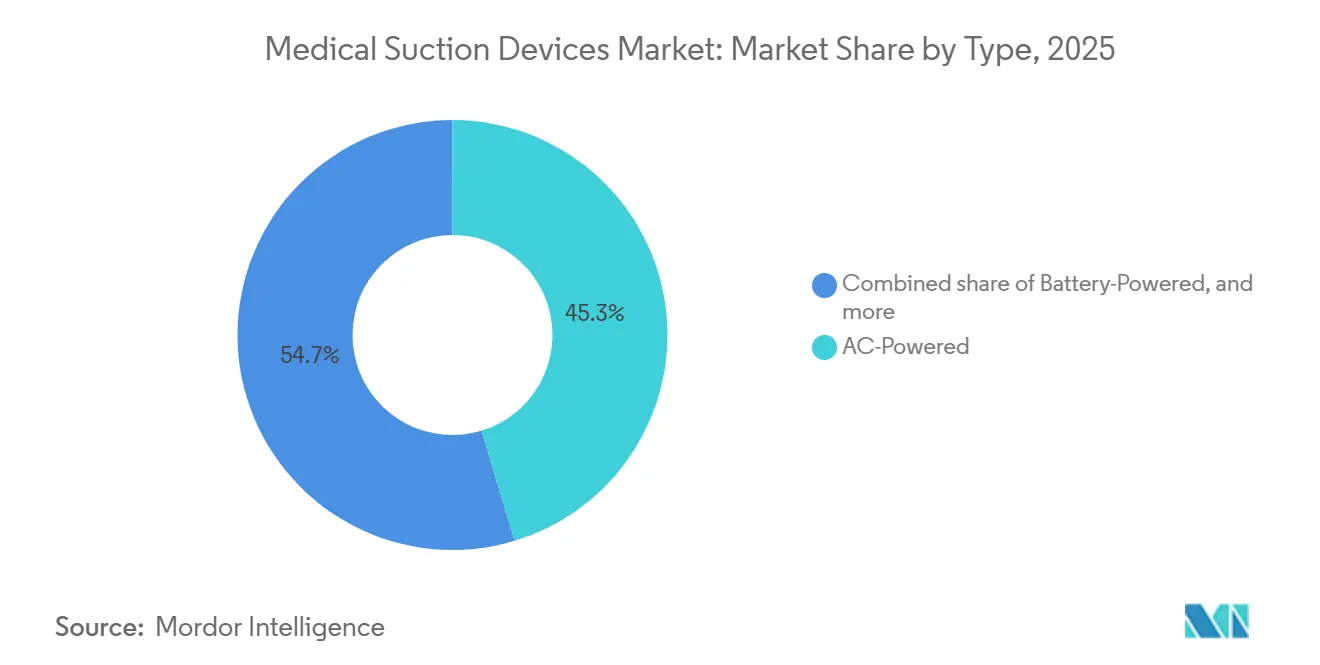

- By type, AC-powered units held 45.32% share in 2025 and are projected to grow at a 7.54% CAGR from 2026 to 2031.

- By portability, wall-mounted systems led with 46.54% share in 2025, while hand-held and portable configurations are set to post an 8.21% CAGR through 2031.

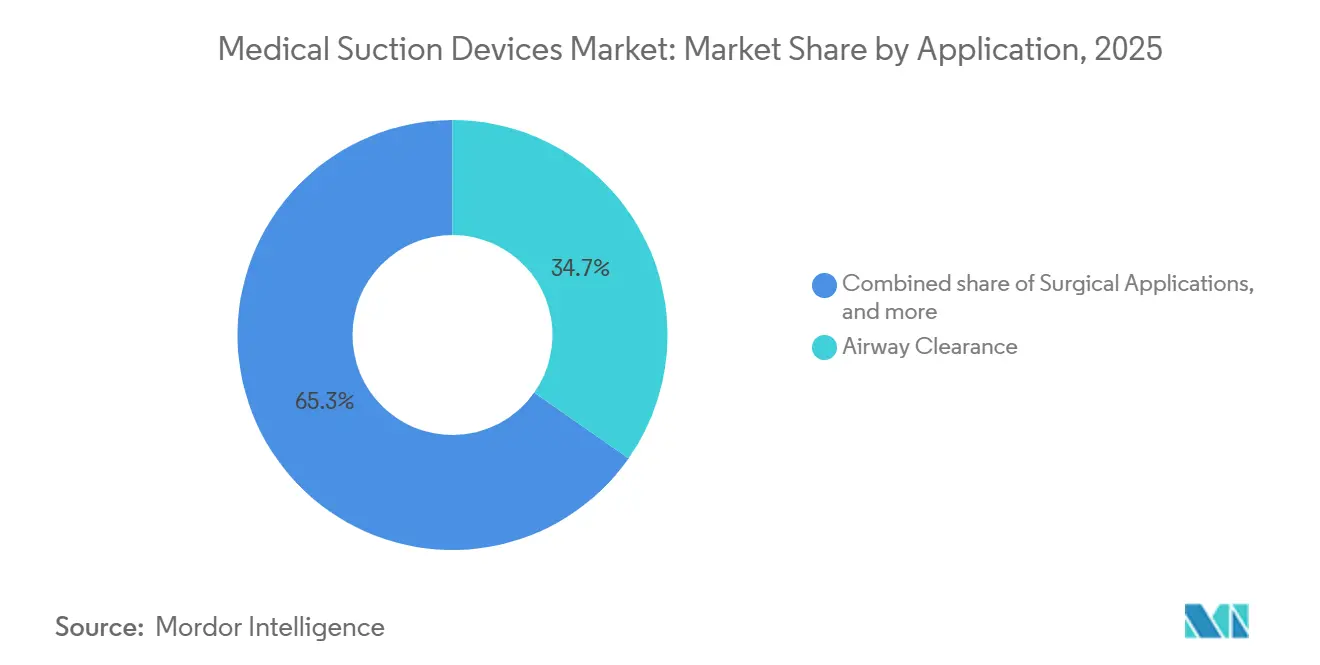

- By application, airway-clearance devices accounted for 34.74% of revenue in 2025 and will advance at a 7.33% CAGR between 2026 and 2031.

- By end user, hospitals captured a 42.55% share in 2025, and home healthcare settings are expected to expand at an 8.65% CAGR through 2031.

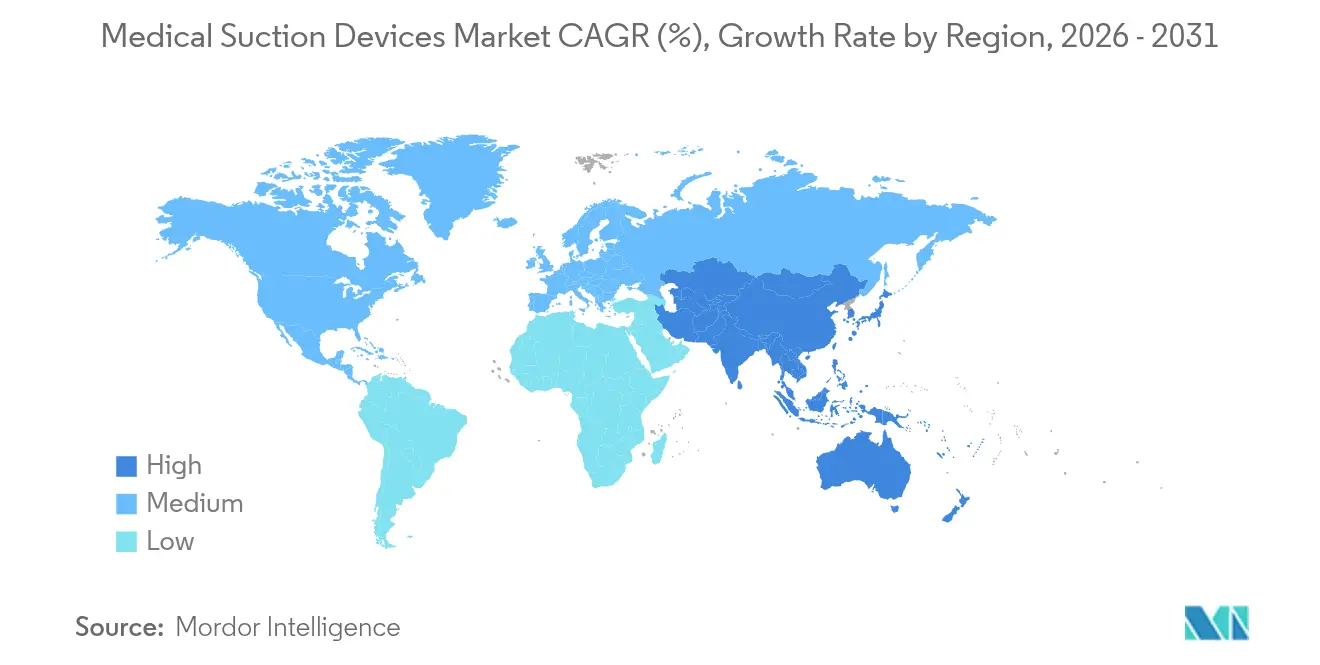

- By geography, North America generated 42.43% of 2025 revenue, and Asia-Pacific is forecast to rise at a 6.97% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Suction Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Surgical Volume Globally | +1.4% | Global, with concentration in North America, Europe, and APAC urban centers | Medium term (2-4 years) |

| Rising Prevalence of Respiratory Diseases | +1.6% | Global, particularly APAC and MEA due to air quality and aging demographics | Long term (≥ 4 years) |

| Expansion of Home Healthcare Services | +1.2% | North America and Europe lead; APAC emerging | Medium term (2-4 years) |

| Stringent Infection Control Regulations | +0.8% | Global, with EU and North America enforcing ISO 10079 and FDA standards | Short term (≤ 2 years) |

| Technological Advancements in Portable Suction Devices | +1.0% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Surgical Volume Globally

Worldwide surgical procedures reached 310 million in 2025, with minimally invasive techniques responsible for 60% of incremental growth. The higher procedural load drives demand for reliable operating-room suction that maintains clear visualization and prevents thermal injury. Ambulatory surgery centers, which now handle 72% of elective cases in the United States, prefer compact, cart-mounted units that can be moved between suites without requiring facility-wide pipeline upgrades. Emerging economies in Southeast Asia and Latin America are adding theater capacity at double-digit rates, yet inconsistent grid performance spurs procurement of dual-powered configurations capable of seamless AC-to-battery switchover. Standardization initiatives tied to value-based purchasing encourage health systems to negotiate fleet-wide contracts, driving volume discounts and accelerated refresh cycles. Collectively, these forces sustain steady replacement demand and position the medical suction devices market for continued uptake in core surgical environments.

Rising Prevalence of Respiratory Diseases

Chronic respiratory diseases affected 569.2 million people in 2023, causing 4.2 million deaths and ranking as the third-leading global killer[1]Source: Institute for Health Metrics and Evaluation, “Global Burden of Disease Study 2024,” healthdata.org. Chronic obstructive pulmonary disease and asthma account for three-quarters of the burden, underscoring the need for airway-clearance suction in critical care and home-monitoring programs. Hospital readmission penalties incentivize care teams to deploy portable units after discharge, cutting 30-day readmissions by 18% in pilot cohorts. Air-quality deterioration across South Asia and sub-Saharan Africa is widening the patient pool among younger demographics, reinforcing long-term volume growth. Closed-suction systems mandated by infection-control guidelines reduce microbial colonization by 40% compared to open techniques. The convergence of epidemiological pressure and protocol evolution sustains long-run demand across both institutional and home-care channels.

Expansion of Home Healthcare Services

Global home healthcare spending exceeded USD 250 billion in 2024, expanding 6%-8% annually as aging populations and payer incentives migrate treatment out of hospitals. Medicare Advantage plans now reimburse portable suction rentals for tracheostomized and neuromuscular patients, eliminating an important barrier to home deployment. Telehealth-ready units transmit usage logs and vacuum alerts to clinicians, enabling early intervention that lowers emergency-department visits by 22% in study groups. Europe and Japan have aligned home-use device standards with hospital-grade specifications, compressing approval timelines and encouraging suppliers to launch dual-market platforms. Growing caregiver familiarity with lightweight, battery-powered models supports sustained momentum for the medical suction devices market in residential settings.

Stringent Infection Control Regulations

ISO 10079 performance testing, FDA 510(k) substantial equivalence reviews, and the European MDR collectively increase documentation requirements and on-site audit frequency. Closed inline catheters account for 85% of intensive-care protocols, reducing ventilator-associated pneumonia by 40%. Single-use consumables eliminate reprocessing risk but generate 1.2 million tons of plastic waste annually, prompting regulators to explore mandates for biodegradable polymers. MDR compliance costs have risen 30% for mid-sized manufacturers, tilting competitive advantage toward companies with robust quality management systems. Harmonized standards enable multinational firms to amortize certification costs across multiple regions, thereby reinforcing their presence in the medical suction devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Suction Equipment | -0.9% | Asia-Pacific, Latin America | Short term (≤ 2 years) |

| Limited Reimbursement For Capital Equipment | -0.8% | North America, Europe | Medium term (2-4 years) |

| Availability Of Alternative Airway Clearance Methods | -0.6% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Environmental Concerns Related To Disposable Components | -0.5% | Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Suction Equipment

Premium portable systems incorporating connectivity and extended battery life list at USD 2,500-USD 4,000, straining budgets of rural clinics and low-income households. Hospital capital budgets fell 8% in 2024 as funds shifted to workforce retention, lengthening replacement cycles from five to seven years. Emerging markets face import tariffs up to 25% on medical electronics, inflating landed costs and deterring adoption[2]World Trade Organization, “Tariff Profiles for Medical Devices 2025,” wto.org. Equipment-as-a-service models spread slowly where credit infrastructure is weak, limiting creative financing options. Low-acuity facilities sometimes revert to manual pumps, cannibalizing potential volume for powered devices in the medical suction devices market.

Limited Reimbursement for Capital Equipment

The U.S. DMEPOS fee schedule caps monthly rentals at USD 150, insufficient to cover a USD 3,000 acquisition within the typical 24-month period. European public health systems classify suction units as non-reimbursable capital, forcing hospitals to finance purchases from constrained operating budgets. Although value-based payment models acknowledge reduced readmissions tied to portable airway clearance, coding updates will not finalize before 2028[3]American Association for Respiratory Care, “Advocacy Update on DMEPOS Reimbursement 2026,” aarc.org. Fragmented payer policies discourage home-care agencies from stocking adequate inventory, limiting patient access, and tempering near-term growth prospects within the medical suction devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: AC-Powered Units Anchor Hospital Infrastructure

AC-powered systems captured 45.32% of the medical suction devices market share in 2025, and the segment is advancing at a 7.54% CAGR through 2031. High vacuum capacity exceeding 600 mmHg and flow rates of 40 L/min satisfy strict operating-room requirements, sustaining entrenched demand among perioperative stakeholders. Performance verification under ISO 10079-1 covers vacuum stability, noise emissions, and electromagnetic compatibility, adding compliance confidence for biomedical teams. Smart sensors now monitor canister fill levels, motor temperature, and vacuum pressure, issuing alerts before clinical disruption. Dual-powered designs, priced 15% higher, win contracts in seismic zones and areas prone to grid failure, reinforcing resilience planning across new hospital projects.

Battery-powered units trail in absolute revenue yet post the fastest growth as lithium-ion platforms narrow runtime gaps and maintenance-free brushless motors enhance reliability. Manual devices persist in austere regions; however, donor programs increasingly prioritize electrified donations equipped with solar charging kits, gradually eroding the manual installed base. As performance parity tightens, the medical suction devices market sees procurement decisions pivot toward interoperability with electronic health records and ease of field servicing.

By Portability: Mobility Redefines Care Delivery

Wall-mounted networks held 46.54% of the medical suction devices market in 2025, benefitting from centralized vacuum plants that feed multiple patient rooms and procedure suites. Installation cost, however, exceeds USD 500,000 for a 200-bed facility, deterring smaller ambulatory centers. Portable hand-held and cart-mounted units are therefore projected to rise at an 8.21% CAGR to 2031, buoyed by home healthcare migration, emergency preparedness mandates, and telehealth integration. Pandemic drills accelerated adoption of battery-backed units that can be deployed in tented wards and transport vehicles within minutes.

Hand-held devices weighing under 1.5 kilograms lower caregiver fatigue and have reduced Medicare readmissions by 18% in pilot programs. Cart-mounted platforms now integrate oxygen concentrators and patient monitors, turning them into mobile respiratory stations for post-anesthesia care. Harmonized FDA, CE, and PMDA approvals shorten global launch cycles, allowing manufacturers to amortize tooling costs across regions and to scale production faster. Consequently, mobility-first architectures reorient purchasing criteria throughout the medical suction devices market.

By Application: Airway Clearance Dominates Clinical Demand

Airway-clearance devices accounted for 34.74% of demand in 2025 and are forecast to grow at a 7.33% CAGR through 2031, reflecting persistent chronic respiratory morbidity and ICU infection-prevention protocols. Closed-circuit catheters, now standard in 85% of ICUs, lower ventilator-associated pneumonia incidence by 40%. Surgical applications follow, driven by laparoscopic and robotic procedures requiring continuous fluid evacuation to maintain visualization and thermal safety. Obstetric suites in emerging economies replace foot-pump devices with electric models offering adjustable vacuum to minimize neonatal scalp trauma.

Diagnostics and research settings remain niche but benefit from miniaturized suction catheters with integrated biopsy channels that support precision-medicine workflows. Smoke-evacuation add-ons address occupational-health concerns and comply with updated OSHA particulate guidelines. As procedure complexity increases, demand for intelligent flow control and contamination tracking augments the value proposition of premium systems, thereby shaping specification roadmaps across the medical suction devices market.

By End User: Home Healthcare Outpaces Institutional Growth

Hospitals represented 42.55% of the medical suction devices market size in 2025, maintaining leadership through steady replacement of theater, ICU, and ward equipment. Yet home healthcare settings are expanding at an 8.65% CAGR to 2031 as payers emphasize early discharge and infection avoidance. Telemonitor-enabled units deliver usage data to clinicians, trimming emergency admissions and supporting bundled-payment objectives.

Dental clinics constitute a stable revenue stream linked to practice expansion cycles and upgrades to quieter, oil-free vacuums that meet stricter noise regulations. Other users—veterinary hospitals, research labs, and industrial hygiene teams—provide diversification and resilience against institutional budget swings. Group purchasing organizations negotiate single-vendor deals that yield 15%-20% price relief and simplify maintenance logistics for hospitals, reinforcing brand stickiness within the medical suction devices market.

Geography Analysis

North America captured 42.43% of revenue in 2025, supported by USD 4.5 trillion in U.S. healthcare expenditure, rigorous infection-control mandates, and extensive home-care reimbursement. Canada pursues province-wide equipment standardization, while Mexico’s private-hospital expansion fuels demand for premium portable systems. FDA 510(k) oversight and Joint Commission accreditation create high compliance thresholds that favor incumbent suppliers, although value-based payment models are unlocking incremental budgets for connected suction fleets. Hospital capital allocations contracted 8% in 2024 but are rebounding as labor stabilization frees funds for deferred equipment projects.

Asia-Pacific is projected to grow at 6.97% through 2031, the fastest regional pace, propelled by China’s USD 860 billion healthcare sector, India’s rapid hospital construction, and Japan’s aging population. China’s Healthy China 2030 program funnels investment into county hospitals that prioritize dual-powered suction for emergency readiness. India’s Ayushman Bharat insurance scheme stimulates procedural volume, driving uptake of obstetric and surgical systems. Japan encourages home-care transitions, boosting demand for compact caregiver-friendly models. Southeast Asian nations add operating rooms at double-digit rates, yet unreliable electricity enhances the appeal of battery-backed configurations.

Europe contributes significant share through Germany, the United Kingdom, and France, where ISO 10079 compliance is obligatory and MDR-related audits intensify vendor selection rigor. The Gulf Cooperation Council allocates USD 100 billion to healthcare infrastructure from 2024-2030, specifying premium suction in new mega-hospitals. Brazil expands surgical capacity under SUS, although tariff policies and fiscal pressure tilt buyers toward lower-cost models. Argentina’s currency instability slows replacement cycles, encouraging refurbished purchases that prolong equipment life yet limit penetration of advanced telemetry-enabled devices in the medical suction devices market.

Competitive Landscape

The top five suppliers—Medela, Stryker, Ambu, Cardinal Health, and Drive DeVilbiss—jointly hold roughly 40%-45% of global revenue, leaving the remainder fragmented among regional specialists. ISO 10079 compliance records, swift FDA 510(k) clearances, and strong group-purchasing contracts underpin their competitive resilience. Baxter’s USD 12.4 billion Hillrom acquisition expanded its respiratory-care footprint, enabling cross-selling of suction systems alongside monitors and ventilators. Patents for brushless motors, battery-management algorithms, and cloud-based fleet analytics intensify differentiation efforts.

Smaller innovators target pediatric transport, veterinary, and industrial niches overlooked by larger firms, leveraging direct-to-consumer e-commerce to bypass durable-medical-equipment distributors and capture more margin. Quality-system demands under the European MDR and stricter FDA post-market surveillance elevate compliance costs, discouraging low-budget entrants and reinforcing the moderate consolidation trajectory of the medical suction devices market. Regionalization of component sourcing and near-shoring of assembly lines mitigate geopolitical supply-chain risk, an emerging procurement criterion among health systems following pandemic disruptions.

Strategic collaborations also proliferate: Cardinal Health and Philips co-develop closed-suction integrated ventilator platforms; Stryker scales Michigan capacity to meet rising outpatient demand; and Medela introduces Bluetooth-enabled units positioned for telehealth expansion. These initiatives collectively signal an industry shift toward connected, data-rich devices that align with value-based reimbursement and predictive maintenance objectives, thereby shaping long-term share dynamics within the medical suction devices market.

Medical Suction Devices Industry Leaders

Precision Medical, Inc.

Medela AG

ZOLL Medical Corporation (Asahi Kasei)

Drive DeVilbiss Healthcare

Laerdal Medical AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Momcozy launched the SniffEase Baby Nasal Aspirator with hospital-grade suction for safe, effective relief. This easy-to-use device not only provides instant congestion relief but also reduces the need for frequent pediatric visits, offering parents peace of mind and a more comfortable experience for their babies.

- January 2025: Dale Medical Products introduced its patent-pending Scrape-n-Suction Tongue Cleaner to enhance oral care for patients. The Scrape-n-Suction Tongue Cleaner is the only product on the market that offers a unique combination of effective scraping and suction to thoroughly clear tongue biofilm, the company says. This design helps remove bacteria and toxins, potentially reducing the risk of ventilator-associated pneumonia (VAP) and other respiratory infections.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the worldwide medical suction devices market as factory-new AC-powered, battery-powered, dual-powered, and manual pumps sold with integral canisters that evacuate fluids during airway clearance, surgery, obstetrics, emergency response, and diagnostics across hospitals, ambulances, dental offices, and home-care settings. Values are captured at the manufacturer invoice level and expressed in constant 2025 US dollars.

Scope Exclusion: We deliberately exclude central pipeline vacuum plants, dedicated dental saliva ejectors, and disposable suction tips.

Segmentation Overview

- By Type

- AC-Powered

- Battery-Powered

- Dual (AC & Battery) Powered

- Manually Operated

- By Portability

- Hand-Held / Portable

- Wall-Mounted

- Trolley / Cart-Mounted

- By Application

- Airway Clearance

- Surgical Applications

- Obstetrics & Gynecology

- Research & Diagnostics

- Other Applications

- By End User

- Hospitals

- Home Healthcare Settings

- Dental Clinics

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held multiple touchpoints with biomedical engineers, EMS fleet heads, procurement officers, and home-health nurses across North America, Europe, India, and Brazil. Their insight on stocking ratios, battery-life pain points, and brand switching let us fine-tune usage assumptions and price-erosion curves.

Desk Research

We started with authoritative, non-paywalled repositories such as WHO Health Expenditure, OECD Health Stats, Eurostat surgery counts, the US FDA 510(k) database, and AdvaMed briefs, which let us size demand pools and installed base. Company 10-Ks, capital-budget tender portals, and leading media reports refined average selling prices and replacement cycles. Paid assets, including D&B Hoovers for supplier splits and Volza shipment logs for cross-border flow checks, helped validate regional shares. The sources noted are illustrative, and many other references guided data collection and fact checks.

We conducted a second pass that merged customs codes, hospital construction trackers, and patent filings to ensure emerging portable designs were captured before numbers fed our worksheets.

Market-Sizing & Forecasting

We lead with a top-down build that converts procedure counts, live-birth volumes, COPD prevalence, and ambulance fleet additions into device demand using clinically validated suction-per-event factors. Select bottom-up roll-ups of supplier revenues and sampled ASP × unit estimates test and adjust the totals. Key drivers modeled forward include global inpatient surgeries, emergency call-outs, hospital-bed growth, EMS portable penetration, and replacement-cycle length. Multivariate regression, supported by scenario analysis and expert consensus, projects each variable through 2030.

Data Validation & Update Cycle

Mordor analysts run outputs through variance triggers versus trade data and public company reports; deviations above five percent send estimates back for senior review. Reports refresh annually, with interim updates when recalls, reimbursement shifts, or major M&A alter market math. A final analyst pass ensures clients receive the freshest view.

Why Mordor's Medical Suction Devices Baseline Commands Reliability

Published estimates often diverge; Mordor builds on procedure-linked variables and dual-track validation, while some peers rely on catalog counts or pre-pandemic multipliers.

Major gaps also arise when manual pumps or Latin America are omitted and when list prices are left unadjusted.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.52 B | Mordor Intelligence | |

| USD 1.25 B | Global Consultancy A | Omits home-care channel; uses unadjusted list prices |

| USD 1.07 B | Industry Association B | Relies on 2019 multipliers; excludes Latin America |

These comparisons show that Mordor's transparent variables, yearly refresh, and multi-step validation deliver the dependable baseline decision-makers require.

Key Questions Answered in the Report

How large is the medical suction devices market in 2026?

The medical suction devices market size is USD 19.60 billion in 2026 and is forecast to reach USD 25.52 billion by 2031.

Which segment grows fastest by portability?

Hand-held and portable units are advancing at an 8.21% CAGR, outpacing wall-mounted systems through 2031.

Why are airway-clearance applications leading demand?

A global chronic respiratory disease prevalence of 569.2 million cases drives sustained need for frequent airway suction in hospitals and at home.

What share do AC-powered units hold?

AC-powered devices captured 45.32% of 2025 revenue and will continue expanding on the strength of operating-room demand.

Which region shows the highest growth rate?

Asia-Pacific is projected to expand at a 6.97% CAGR between 2026 and 2031, led by China and India.

What impedes rapid adoption in low-income regions?

High upfront costs and limited reimbursement hinder acquisition of advanced connected devices in price-sensitive markets.

Page last updated on: