Hair Transplant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

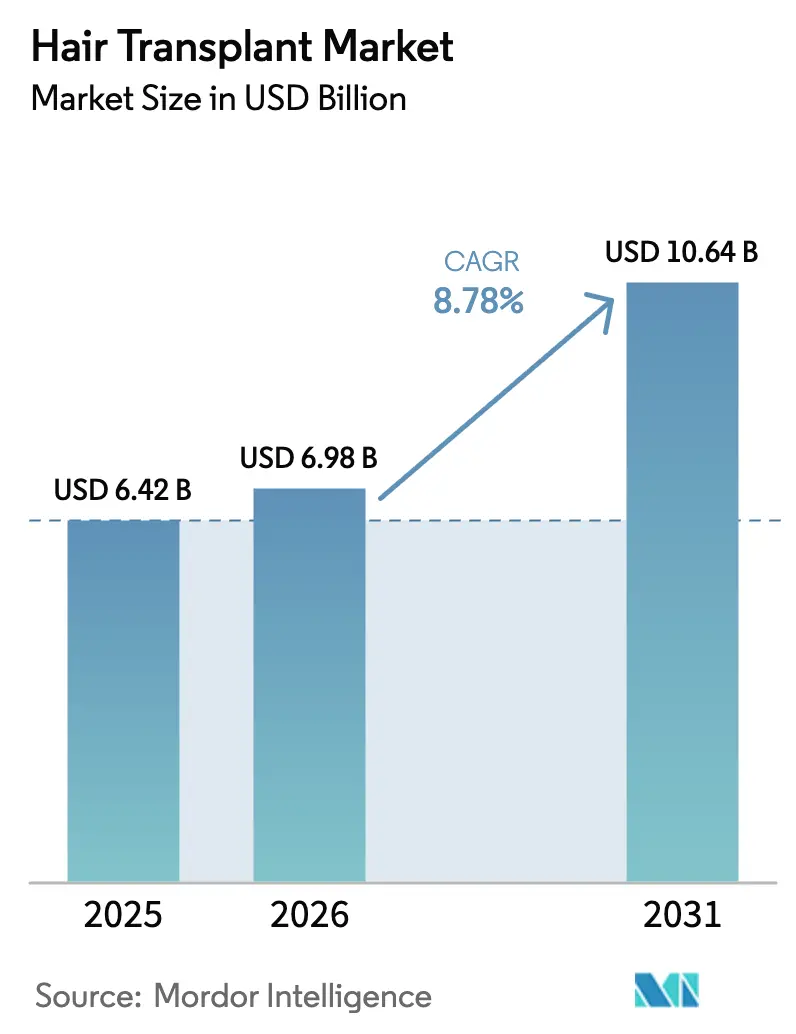

| Market Size (2026) | USD 6.98 Billion |

| Market Size (2031) | USD 10.64 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

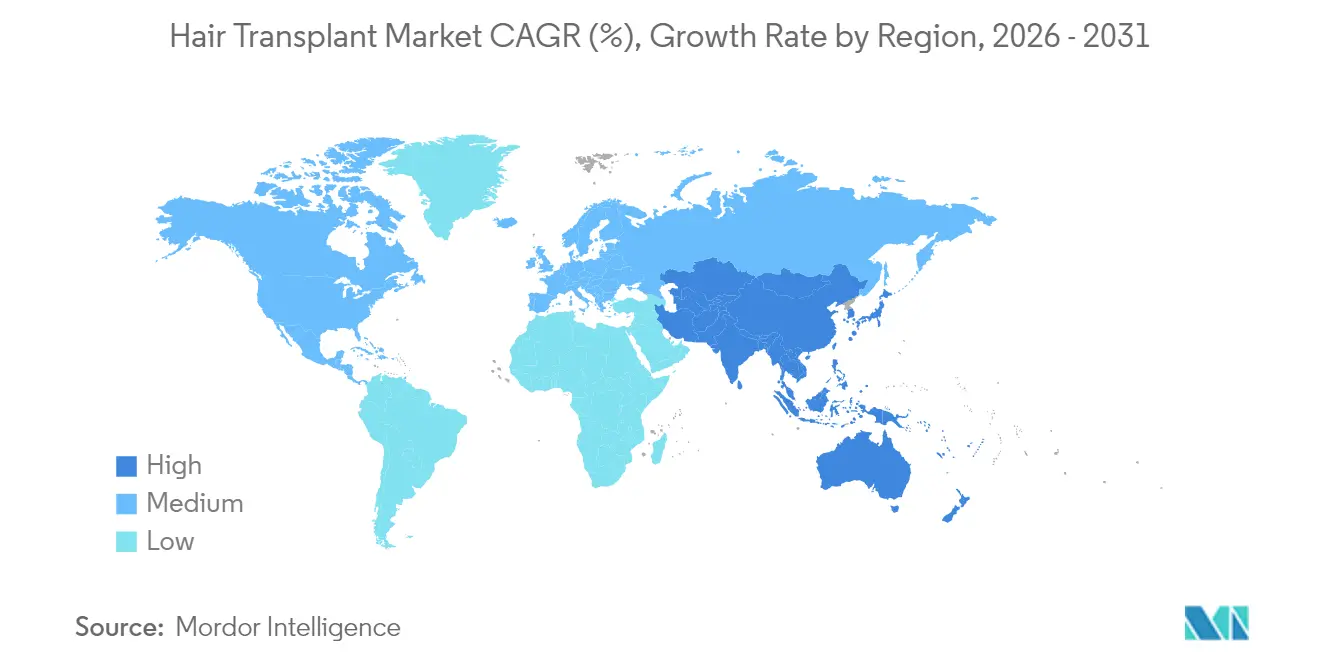

| Fastest Growing Market | Asia |

| Largest Market | North America |

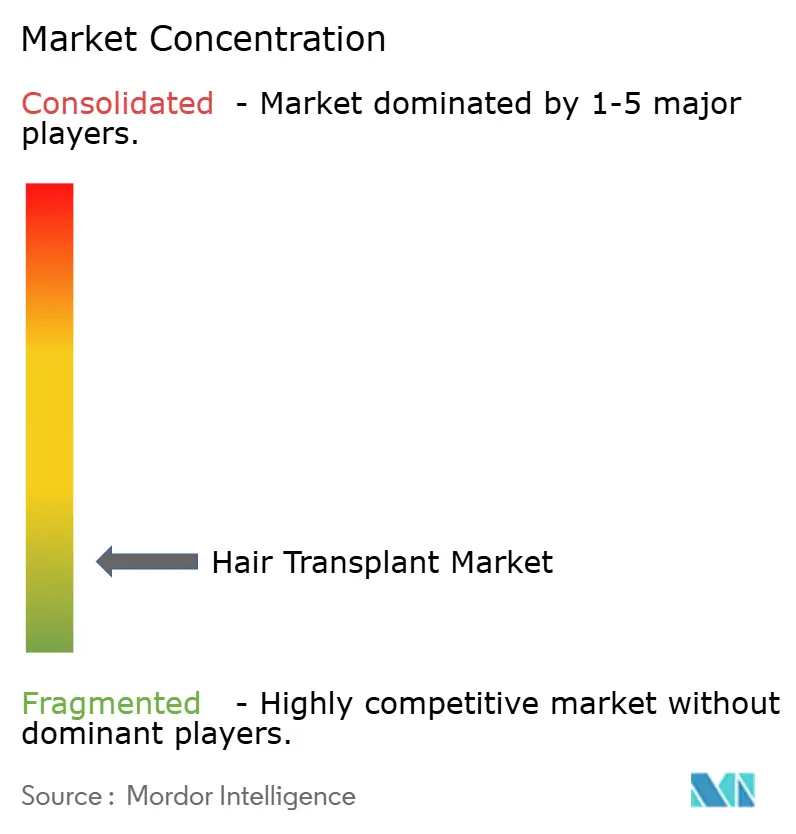

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hair Transplant Market Analysis by Mordor Intelligence

The hair transplant market size was valued at USD 6.42 billion in 2025 and estimated to grow from USD 6.98 billion in 2026 to reach USD 10.64 billion by 2031, at a CAGR of 8.78% during the forecast period (2026-2031). Rising adoption of robotic systems such as ARTAS iXi and FUEsion X 5.0, widening medical-tourism routes, and stronger societal acceptance of appearance-enhancement procedures underpin this expansion. Demographic pressures—including an earlier onset of androgenetic alopecia among adults in their 20s—are enlarging the addressable patient base, while regulatory approvals such as the FDA clearance of deuruxolitinib widen therapeutic options. Clinics are pairing surgery with regenerative adjuncts (PRP, stem cells) to improve graft survival and open ancillary revenue streams. Competitive intensity has grown, yet brand-led firms leverage technology‐enabled precision and influencer marketing to sustain price premia and mitigate discounting pressures.

Key Report Takeaways

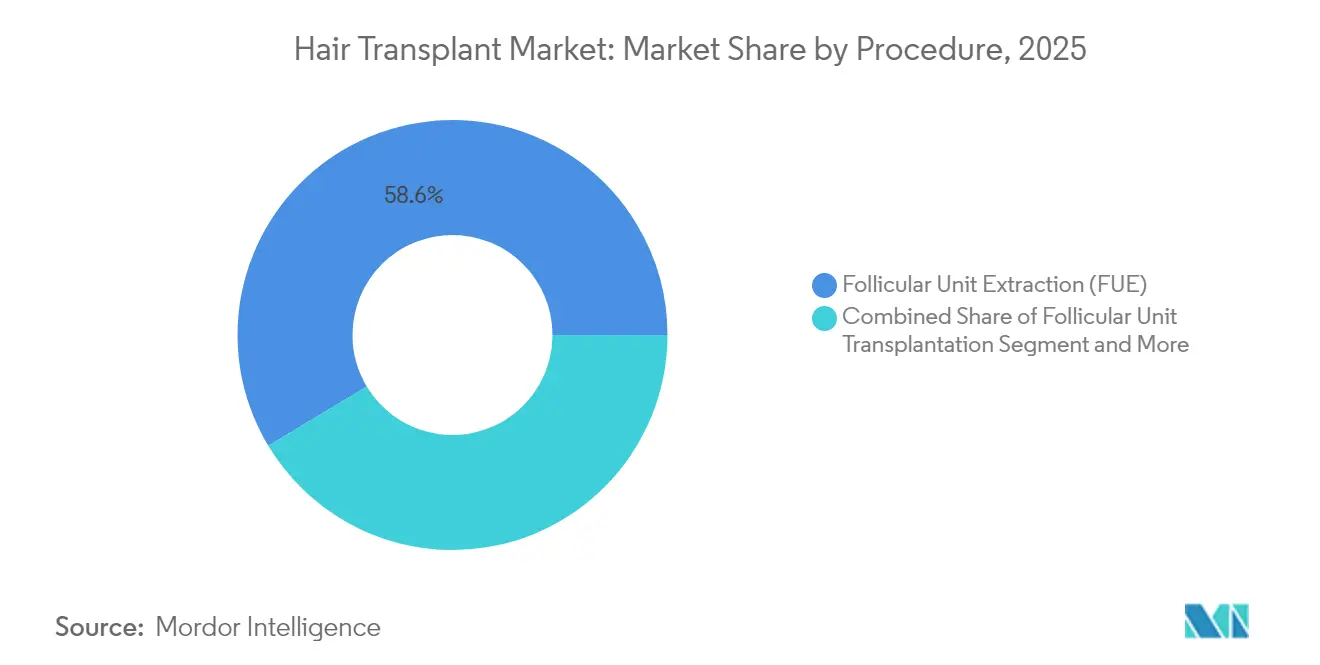

- By procedure, Follicular Unit Extraction led with 58.62% of hair transplant market share in 2025, whereas the combined FUT + FUE approach is forecast to post the fastest 14.88% CAGR to 2031.

- By gender, males accounted for 78.74% of revenue in 2025, while the female cohort is projected to expand at a 10.74% CAGR through 2031.

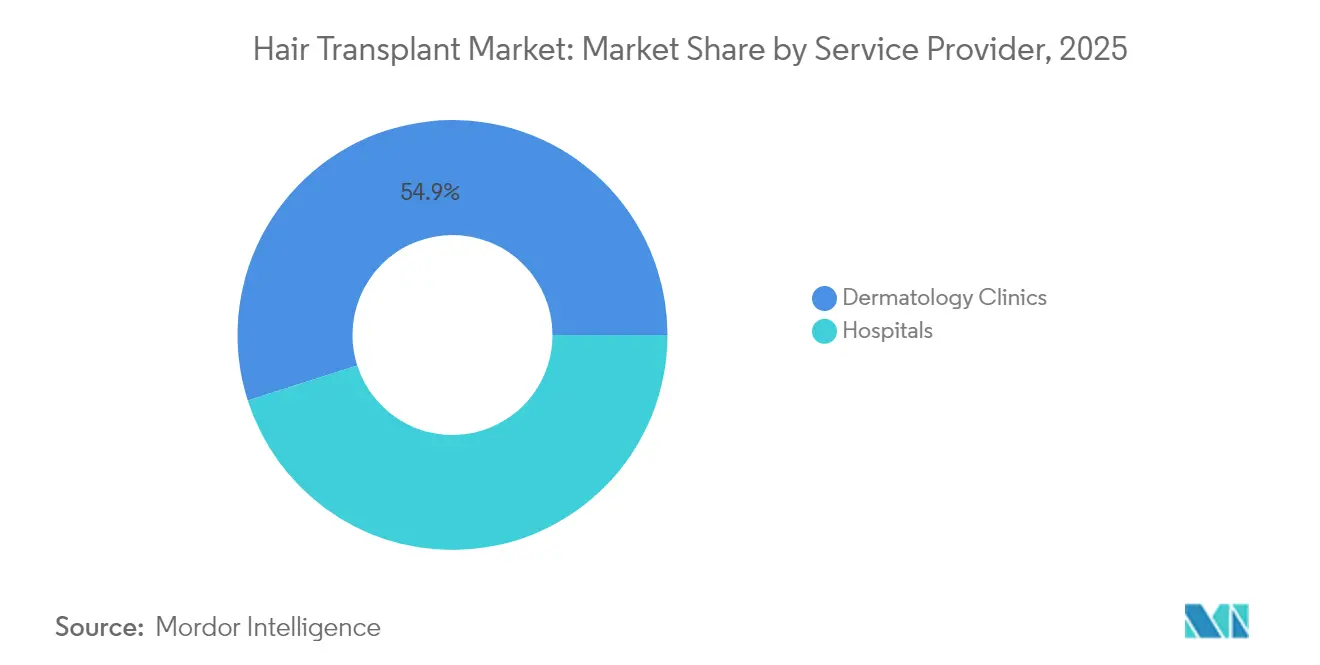

- By service provider, dermatology clinics held 54.93% of revenue in 2025 and are growing at 11.34% annually.

- By geography, North America contributed 33.29% of revenue in 2025; Asia-Pacific is expected to grow the quickest at 12.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hair Transplant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Popularity of transplants to enhance self-esteem | +2.1% | North America, Europe, gradually global | Medium term (2-4 years) |

| Rising prevalence of dermatological disorders | +1.8% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Higher disposable income & medical tourism | +2.3% | Asia-Pacific core, MEA and Latin America spillover | Medium term (2-4 years) |

| Emergence of regenerative PRP & stem-cell adjuncts | +1.5% | North America, EU leading; Asia-Pacific adopting | Long term (≥ 4 years) |

| Social-media-driven male grooming boom | +1.2% | Urban centers worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Hair Transplants to Enhance Looks & Self-Esteem

Social platforms have normalized cosmetic procedures, prompting adults in their late 20s to view transplantation as preventive rather than corrective care. Clinical studies report 98% satisfaction with FUE, underscoring the psychosocial uplift patients gain. Younger cohorts, especially professionals in entertainment and sales, are scheduling surgeries earlier to preserve personal branding. This attitudinal shift broadens revenue beyond traditional middle-aged males to women and Gen Z consumers. Clinics partner with influencers and athletes to showcase authentic results, which reduces stigma and lowers the average age of first-time patients. Preventive demand also sustains follow-up visits for topical therapies, stimulating recurring spend.

Increasing Prevalence of Dermatological Disorders Causing Hair Loss

China counts 250 million residents with androgenetic alopecia—an illustration of mounting medical burden. Lifestyle stressors and hormonal shifts bring onset forward, multiplying candidate numbers. Autoimmune segments benefit from the 2024 FDA nod to deuruxolitinib, expanding treatment pathways. Female pattern loss is increasingly classified as a standalone disorder requiring tailored graft placement and hormone balance strategies. Systematic reviews show platelet-rich fibrin injections improving density in women[1]Hassan Haidar, “Injectable Platelet-Rich Fibrin for Treatment of Female Pattern Hair Loss,” Journal of Cosmetic Dermatology, tandfonline.com. Early detection platforms integrate dermoscopy and AI diagnosis, enabling clinics to counsel patients before extensive follicle miniaturization occurs.

Rising Disposable Income & Medical Tourism in Emerging Economies

Cross-border surgery remains price-sensitive; US procedures average USD 12,767, while accredited Turkish centers charge USD 2,056 for 2,000 grafts. Governments in Turkey and India promote streamlined visas and hospital accreditations, encouraging inbound flows. Yet the cost gap abridges as European hospitals market USD 2,000 packages, forcing Istanbul clinics to refresh pricing and value propositions. Asia-Pacific domestic demand jumps as middle-class incomes rise; India’s clinics operate at global standards and capture repatriated traffic. International trademark protection and multilingual aftercare lines help providers reassure long-haul travellers.

Emergence of Regenerative PRP & Stem-Cell Adjuncts Boosting Outcomes

Meta-analyses confirm PRP efficacy for alopecia areata and cicatricial alopecias[3]“Platelet-Rich Plasma in Alopecia Areata and Primary Cicatricial Alopecias: A Systematic Review,” National Institutes of Health, ncbi.nlm.nih.gov. Stem-cell suspensions from adipose tissue demonstrate improved density in 12 randomized trials. Japan’s regulatory framework enabled Shiseido’s cultured dermal-sheath therapy in 2024, proving commercial viability. Clinics now bundle PRP with FUE to raise graft take-rates by more than 10% on average, extending revenue beyond the surgical ticket. Continuous innovation in biologics is positioning clinics for upselling packages that combine extraction, topical JAK inhibitors, and autologous cell infusions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost constraints & high post-surgery care | -1.9% | Emerging markets lacking insurance | Medium term (2-4 years) |

| Surgical risks & side-effects | -1.3% | Regions with variable regulatory oversight | Short term (≤ 2 years) |

| Regulatory scrutiny on unlicensed clinics | -0.8% | Turkey, Eastern Europe, new tourism destinations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Constraints and High Post-Surgery Care Needs

Price hurdles exclude many middle-income patients, especially where insurance refuses cosmetic reimbursement. Ancillary expenditures on analgesics and medicated shampoos can add 30% to total costs within 12 months. Economic slowdowns directly dent clinic bookings, evidenced by Venus Concept’s 15% revenue dip in Q3 2024 while equipment debt was halved to preserve liquidity. UK health services report investing extra resources to manage complications from discounted overseas surgeries, highlighting hidden long-term costs.

Surgical Risks and Side-Effects Impacting Patient Willingness

Folliculitis and donor-site scarring remain concerns; multicenter studies pinpoint technique and hygiene as primary predictors. The International Society of Hair Restoration Surgery warns that every surgical step must be physician-directed to avoid misdiagnoses. Social media amplifies negative stories of botched travel surgeries, injecting caution into decision cycles. Regulatory agencies now issue public advisories against unlicensed clinics, tightening oversight and adding compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure: Technological Convergence Reshapes Extraction Methods

Follicular Unit Extraction generated 58.62% of 2025 revenue as patients prioritized minimal scarring and faster recovery within the hair transplant market. Clinics adopting ARTAS iXi recorded harvest rates of 500–700 grafts per hour with 44-micron precision, underscoring equipment contributions to productivity. Yet elite surgeons continue to favor manual punch sets for curly or light-colored hair, demonstrating the coexistence of high-tech and artisanal craft within the same surgical day.

Combination FUT + FUE is projected to grow at 14.88% CAGR, reflecting demand for hybrid protocols that maximize graft counts while disguising donor scars. Under this model, surgeons strip‐harvest central occipital zones (yield) and punch peripheral regions (concealment), delivering natural density for patients requiring 3,500+ grafts. The hair transplant market size for combination techniques is forecast to grow to USD 3.52 billion by 2031, expanding the equipment aftermarket for microscopes and dual-modality punch systems.

Second-generation robots like FUEsion X 5.0 introduce augmented-reality overlays that map follicle angle in real time, reducing transection below 4%. Early adopters charge 15-20% price premiums that many urban millennials accept. Direct Hair Implantation, no-shave FUE, and needle-free anaesthesia platforms address micro-niches of patients seeking discreet recovery.

By Gender: Female Uptake Redraws Demand Profile

Male patients remained the revenue backbone with 78.74% share in 2025, yet the female cohort’s 10.74% CAGR signals a decisive demographic shift in the hair transplant market. Greater awareness of diffuse thinning in women has normalised surgical solutions previously considered last-resort. Dedicated guidelines from the International Society of Hair Restoration Surgery help physicians customise recipient-site density and control hairline direction, restoring a natural central part.

Female patients typically require fewer grafts (1,000–1,500) but demand meticulous angulation and preservation of existing vellus hair, prolonging surgical hours and elevating average selling price per graft. PRF injections yield visible density gains and can postpone surgical needs by 6–12 months, creating bundled therapy pathways. The hair transplant market size for female procedures is projected at USD 2.26 billion in 2031, supported by rising cases of traction alopecia among women of African descent. Clinics in Turkey quote USD 2,200–3,500 packages inclusive of aftercare, maintaining tourism inflow even as European rivals cut prices.

By Service Provider: Dermatology Clinics Strengthen Specialist Position

Dermatology clinics captured 54.93% revenue in 2025 and are forecast to grow 11.34% annually, consolidating dominance in the hair transplant market. Board-certified dermatologists leverage existing trichology consults to funnel patients into surgical theatres, lowering acquisition cost per surgery. As regenerative biologics gain traction, dermatology practices lead adoption owing to expertise in skin microenvironment.

Hospitals, while well equipped for complicated comorbidities, lag in volume efficiency and service personalization. However, academic centers use clinical trials in stem-cell and exosome therapy to remain innovation hubs. Chain clinics expand through franchising to standardize protocols and quality, winning repeat visits from medical-tourism clients wary of single-site operators. The hair transplant market share of multisite franchises is expected to hit 23.60% by 2031, aligning with consumer preference for recognizable brands.

Geography Analysis

North America retained the largest regional stake at 33.29% in 2025, buoyed by high disposable income and early adoption of robotics. Domestic surgery volumes remain strong, yet cost-sensitive consumers still travel to accredited Turkish facilities, evidencing price elasticity. Regulatory clearance for deuruxolitinib and impending cell-therapy trials expand therapeutic breadth, likely sustaining regional procedure counts.

Europe presents a two-speed profile: established providers in Germany and Spain observe steady local demand, while low-cost Eastern European and Turkish centers lure price-driven patients from the United Kingdom and Scandinavia. European hospitals offering USD 2,000 packages shrink the arbitrage that previously fueled outbound tourism, driving Istanbul clinics toward value-added services such as concierge recovery suites.

Asia-Pacific posts the fastest 12.41% CAGR through 2031. China’s sub-0.2% procedure penetration against 250 million hair-loss sufferers depicts vast headroom. Japan’s aging yet image-conscious population fuels demand for minimally invasive robotics, and South Korea’s K-beauty culture promotes preventive follicular care. Local government incentives—for example, India’s medical-visa reforms—further institutionalize cross-border care within the region.

Competitive Landscape

The hair transplant market is structurally fragmented, with more than 5,000 licensed and unlicensed clinics concentrated in Istanbul, intensifying price competition. Global device firms adopt acquisitive strategies; Venus Concept’s takeover of Restoration Robotics merged ARTAS robotics with NeoGraft pneumatic systems, allowing single-supplier packages that streamline clinic capital planning. US giants such as Bosley partner with Lumenis to co-develop FoLix laser therapy, reinforcing vertical integration that locks patients into multi-tier service lines.

Technology remains the primary differentiator. AI-guided imaging identifies donor-area density, enabling dynamic graft allocation and improving aesthetic symmetry. Clinics pilot augmented-reality overlays that project postoperative hairlines to aid shared decision-making. Emerging entrants like Stemson Therapeutics pursue cell-based follicle manufacturing, a potential disruption that could reduce reliance on donor harvesting.

Regulatory crackdowns on unlicensed operators in Turkey and Mexico are likely to elevate compliance costs and shift share toward accredited chains. In developed markets, subscription-based teledermatology platforms from Hims & Hers convert pharmaceutical customers into surgical leads, broadening funnel integration. Overall, the competitive narrative centers on pairing surgical precision with supportive biologics and digital engagement to uplift lifetime customer value.

Hair Transplant Industry Leaders

Bosley Hair Restoration & Transplant

Aderans (Hair Club)

Venus Concept

NeoGraft

DHI Medical Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Asli Tarcan Clinic introduced a robotic DHI protocol designed for Afro-textured hair, expanding service inclusivity.

- February 2025: Istanbul providers cut list pricing after European hospitals launched USD 2,000 transplant bundles, intensifying regional price convergence.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hair transplant market as revenues generated from surgical procedures that relocate autologous hair follicles, most commonly Follicular Unit Extraction and Follicular Unit Transplantation, performed in licensed medical settings across all recipient areas of the body. Value is captured at the point a clinic bills the patient for the surgery and any immediate peri-operative services.

Scope exclusion: Non-surgical hair loss products, prescription drugs, low-level laser devices sold for home use, and cosmetic camouflage solutions are excluded so that the model tracks only surgical transplant activity.

Segmentation Overview

- By Procedure

- Follicular Unit Transplantation (FUT)

- Follicular Unit Extraction (FUE)

- Manual FUE

- Robotic FUE

- Combination of FUT & FUE

- Other Procedures

- By Gender

- Female

- Male

- By Service Provider

- Hospitals

- Dermatology Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with transplant surgeons, device engineers, and administrators in North America, Turkey, India, and Brazil. Their insights helped us verify regional graft counts, realistic utilization rates, and price dispersion, closing gaps left by secondary data and ensuring our assumptions reflect day-to-day operating realities.

Desk Research

We began by mapping the universe of transplant activity through publicly available procedure surveys from the International Society of Hair Restoration Surgery, national hospital discharge datasets, and customs trade codes that track import volumes of micro-punches, implanters, and robotic systems. Government health statistics portals, patent filings indexed on Questel, and peer-reviewed articles in Dermatologic Surgery added clinical incidence rates and success benchmarks. Company financials from D&B Hoovers and news flows collected via Dow Jones Factiva supplied pricing ranges and expansion plans that anchor average selling price (ASP) assumptions. This list is illustrative, not exhaustive; many other materials shaped the evidence base.

Market-Sizing & Forecasting

A top-down, bottom-up hybrid guides the model. We first reconstruct global demand from annual procedure counts and regional ASP bands, which are then corroborated with sampled clinic revenue roll-ups and channel checks to fine-tune totals. Key variables like alopecia prevalence, average grafts per patient, inbound medical-tourism flows, disposable income per capita, and device adoption rates drive both the baseline and the growth trajectory. Multivariate regression links these indicators to observed market values, while scenario analysis stress-tests high and low uptake cases. Where bottom-up estimates are sparse, we impute volumes using clinic capacity benchmarks confirmed during interviews.

Data Validation & Update Cycle

Analysts run variance and anomaly screens, compare outputs with third-party health expenditure series, and escalate deviations for peer review before sign-off. Reports refresh annually, and any material regulatory or reimbursement change triggers an interim update. A final pass just before delivery ensures clients receive the latest view.

Why Mordor's Hair Transplant Baseline Commands Reliability

Published transplant figures often diverge because each publisher scopes the market differently, applies unique price ladders, or refreshes data on its own timetable.

Key gap drivers include the inclusion of regenerative add-ons by some firms, aggressive ASP escalation baked into others' models, and limited primary validation that overlooks cross-border procedure flows; factors our disciplined scope, variable selection, and yearly refresh explicitly tackle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.42 B (2025) | Mordor Intelligence | |

| USD 7.44 B (2024) | Global Consultancy A | Includes PRP and stem-cell revenue, minimal field interviews |

| USD 22.06 B (2024) | Industry Analytics B | Bundles non-surgical products, single-point ASP inflation, infrequent updates |

In short, our numbers rest on clearly defined surgical boundaries, multi-source evidence, and recurring validation, giving decision-makers a balanced and reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the hair transplant market?

The market is valued at USD 6.98 billion in 2026 and is forecast to reach USD 10.64 billion by 2031 at an 8.78% CAGR.

Which procedure type leads global demand?

Follicular Unit Extraction holds 58.62% of 2025 revenue, making it the most widely chosen method.

Why is Asia-Pacific the fastest-growing region?

Large untreated populations, rising disposable incomes, and pro-tourism policies are driving a 12.41% CAGR in the region.

How are regenerative therapies influencing outcomes?

Adjuncts such as PRP and stem-cell suspensions raise graft survival and density, creating new revenue layers for clinics.

What key risk should prospective patients consider?

Common complications include folliculitis and donor-site scarring, highlighting the importance of licensed, experienced surgeons.

Page last updated on: