United States Plastic Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

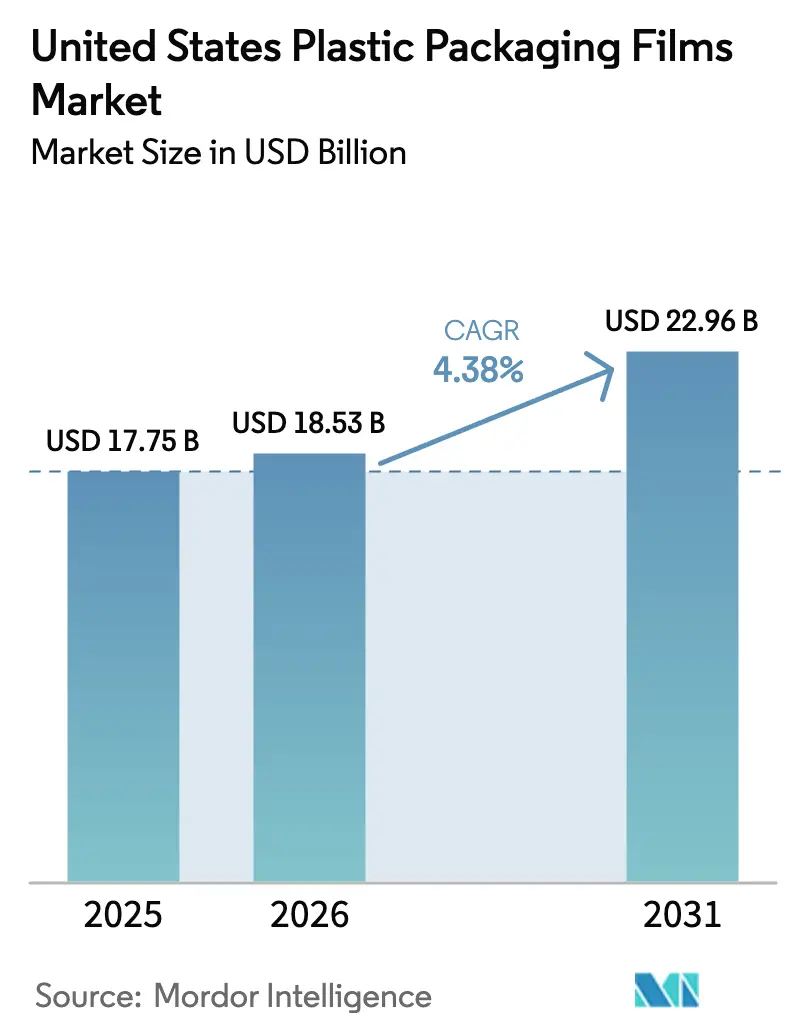

| Base Year Market Size (2025) | USD 17.75 Billion |

| Market Size (2026) | USD 18.53 Billion |

| Market Size (2031) | USD 22.96 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Plastic Packaging Films Market Analysis by Mordor Intelligence

The United States plastic packaging films market size was valued at USD 17.75 billion in 2025 and estimated to grow from USD 18.53 billion in 2026 to reach USD 22.96 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031). Growth is steady rather than explosive because national sustainability mandates now shape material choices and cost structures, even as e-commerce expansion, on-the-go consumption trends, and barrier-film engineering breakthroughs sustain demand. Consolidation among converters, exemplified by the Amcor–Berry Global merger, increases resin-purchasing leverage, while chemical-recycling investments by ExxonMobil and Eastman support a gradual transition toward circular feedstocks. New digital-printing platforms shorten run lengths and enable SKU proliferation, driving converters to adopt faster changeover equipment and thinner gauges to preserve margins. Finally, extended-producer-responsibility (EPR) programs in California, Oregon, and Washington impose fees that accelerate mono-material design adoption but compress profits for converters unable to pass costs through to brand owners.

Key Report Takeaways

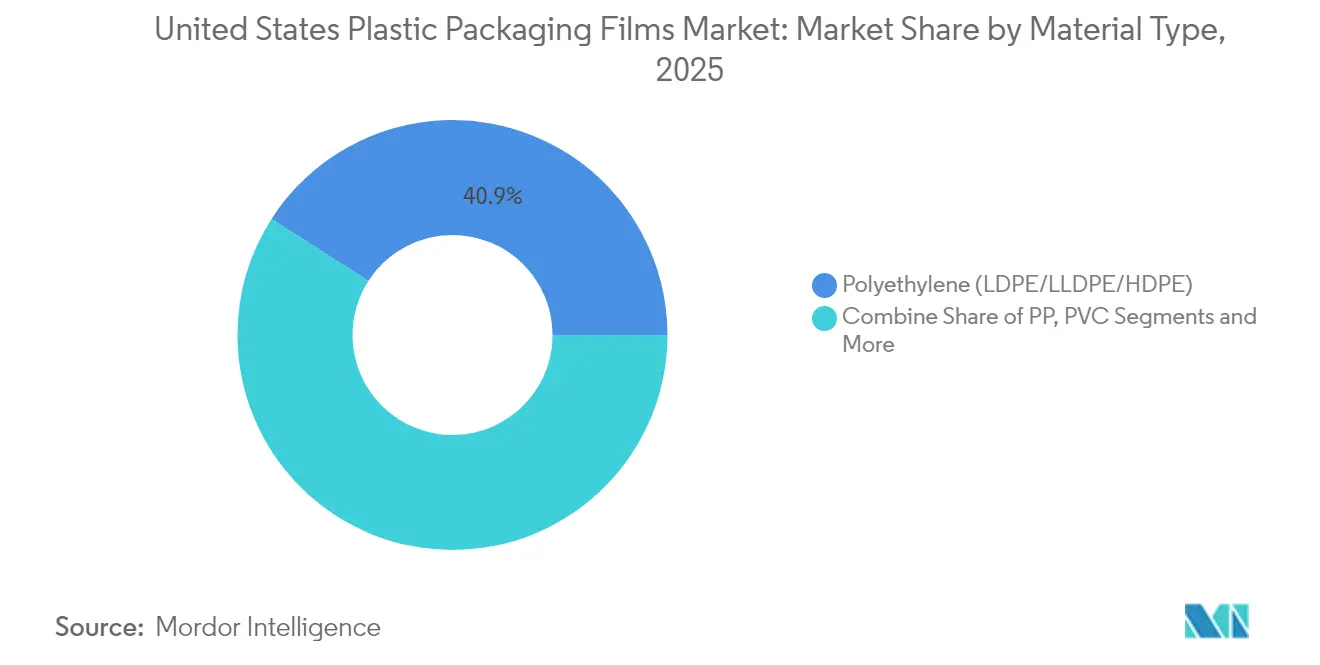

- By material type, polyethylene held 40.92% of United States plastic packaging films market share in 2025, while bio-based and biodegradable films are forecast to expand at a 7.72% CAGR to 2031.

- By functional format, barrier and high-barrier films commanded 26.21% revenue share in 2025, whereas retort and ovenable films are projected to grow fastest at a 8.86% CAGR through 2031.

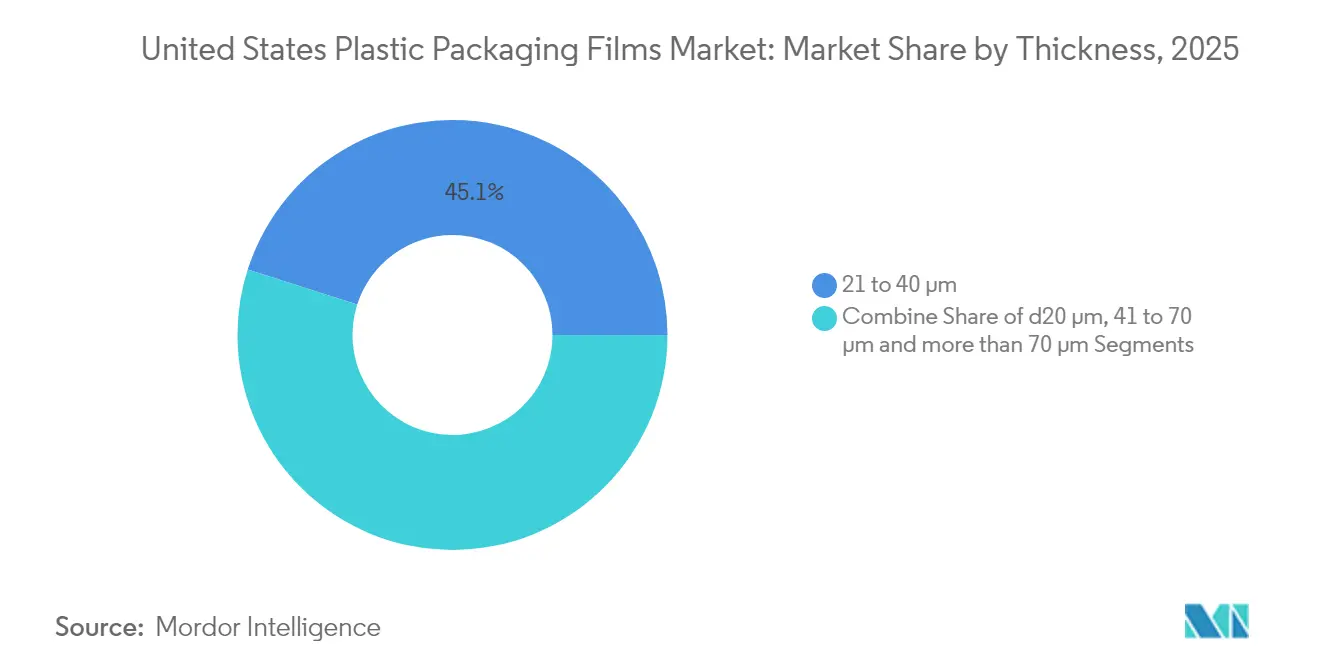

- By thickness, the 21–40 µm range accounted for 45.08% of the United States plastic packaging films market size in 2025; ultra-thin films ≤20 µm are forecast to post a 6.14% CAGR between 2026 and 2031.

- By end-user, food applications represented 65.12% of revenue in 2025, while healthcare and pharmaceutical uses are advancing at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Plastic Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient and on-the-go packaging | +1.2% | National, with early gains in urban centers | Medium term (2-4 years) |

| Rapid growth of e-commerce and omnichannel fulfillment | +1.5% | National, concentrated in logistics hubs | Short term (≤ 2 years) |

| Advances in thin-gauge, high-barrier film technology | +0.8% | National, led by R&D centers in Northeast and West Coast | Long term (≥ 4 years) |

| Brand-owner sustainability targets favoring mono-material films | +1.1% | National, with premium adoption in California and Northeast | Medium term (2-4 years) |

| Scale-up of chemical recycling infrastructure for PE and PP films | +0.7% | Regional, focused in Texas, Louisiana chemical corridors | Long term (≥ 4 years) |

| SKU-proliferation enabled by digital printing on flexible films | +0.9% | National, early adoption in consumer goods centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient and on-the-go packaging

Single-person households rose 13.1% between 2020 and 2024, elevating demand for portion-controlled, resealable pouches that travel well.[1]United States Census Bureau, “Household Income, Poverty and Health Insurance Coverage in the United States: 2023,” census.gov Protein-snack and baby-food producers use stand-up pouches to charge premium prices while slimming down shelf footprints. Sealed Air’s Prismiq 5540 digital printer supports limited-edition visuals and QR-code engagement without lengthy makeready times, helping brands tailor packs to regional tastes. FDA approval of new high-barrier coatings in 2024 widens flexible-film use in pharmaceutical unit-dose formats, a space that historically favored rigid plastics. Convenience remains the overriding consumer value proposition even as recycled content targets tighten, ensuring continued uptake of easy-open and resealable structures.

Rapid growth of e-commerce and omnichannel fulfillment

US e-commerce sales hit USD 1.14 trillion in 2024, with online grocery penetration climbing to 15.3% of food retail.[2]United States Department of Commerce, “Quarterly Retail E-Commerce Sales,” census.gov Films now must resist temperature swings, scuffing, and multiple touches from fulfillment centers to doorsteps. Nova Chemicals’ Indiana recycling hub converts 100 million lb per year of post-consumer LDPE into e-commerce-ready resin that meets Amazon’s 30% recycled-content mandate for 2025. FedEx meanwhile reports a 23% gain in temperature-sensitive pharmaceutical parcels, raising demand for cold-chain barrier films that stay intact during last-mile delays.

Advances in thin-gauge, high-barrier film technology

USPTO filings for nano-enhanced barrier films jumped 47% during 2024, spotlighting graphene-oxide and clay-nanocomposite layers that cut oxygen ingress to near-foil levels. ExxonMobil’s Alpine HA5 resin platform yields recycle-ready pouches containing more than 95% PE yet posts oxygen-transmission rates below 0.1 cc/m²/day. Jindal Films’ J-311AA transparent barrier delivers 0.5 g/m²/day moisture ingress at 38 °C and 90% relative humidity, eliminating foil while preserving shelf appeal. NIST issued new test protocols in 2024 that standardize nano-barrier evaluation, speeding commercialization.[3]National Institute of Standards and Technology, “NIST releases new guidance on nanotechnology-enhanced packaging materials,” nist.gov

Brand-owner sustainability targets favoring mono-material films

SEC climate-disclosure rules effective 2024 oblige public companies to tally Scope 3 packaging emissions, pushing brand owners toward recycle-ready PE or PP constructions. Amcor already reaches 94% recycle-ready status across its flexible portfolio, while The Coca-Cola Company requires 50% recycled content in PET bottles and 25% in flexible films by 2025. Unilever mandates elimination of non-recyclable laminates within the same timeframe, a change that is cascading through converter specification sheets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental pushback on single-use plastics | -1.8% | National, intensified in coastal states | Short term (≤ 2 years) |

| Resin-price volatility linked to crude-oil dynamics | -1.2% | National, acute in Gulf Coast production regions | Short term (≤ 2 years) |

| State-level Extended Producer Responsibility (EPR) fees | -0.9% | Regional, California, Oregon, Washington leading | Medium term (2-4 years) |

| Paper-based flex-pack alternatives gaining shelf acceptance | -0.6% | National, concentrated in premium consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental pushback on single-use plastics

California’s SB 54 imposes a 25% single-use-plastic reduction by 2032 plus a USD 500 million annual fee, prompting immediate specification shifts toward lighter gauges and recycle-ready formats. Oregon and Washington launched similar EPR programs in 2024, each tying fee levels to real-world recyclability performance. Coastal retailers already prefer paper-based or compostable packs for premium ranges, causing some converters to lose shelf facings where they cannot supply functional biofilms on short notice. These policy headwinds temper the overall United States plastic packaging films market trajectory even as innovation accelerates.

Resin-price volatility linked to crude-oil dynamics

Crude prices swung 45% in 2024, swiftly transmitting cost shocks to polyethylene and polypropylene based on ethane and naphtha feedstock ratios. Natural HDPE bale prices leapt 60% year over year, squeezing margins for converters tied to fixed-price supply contracts. Hurricane Francine idled several Gulf Coast crackers for weeks, highlighting infrastructure vulnerability and prompting some brand owners to hedge supply risk through dual-resin specs. Higher Federal Reserve rates also slowed investment in new cracker projects, prolonging domestic capacity constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Dominance Meets Bio-Based Innovation

Polyethylene retained 40.92% of United States plastic packaging films market share in 2025 thanks to low-cost ethane feedstock and wide recycling access. LDPE and LLDPE grades suit frozen-food pillow packs and bread bags, while HDPE variants meet higher stiffness and moisture-barrier needs. Dow’s ELITE AT resins, released in 2024, permit 15% gauge reduction without puncture loss, enabling converters to hit retailer carbon goals without changing equipment.

Bio-based and biodegradable formats, albeit small, are expanding at an 7.72% CAGR as EPR fee modulation rewards compostability. NatureWorks will bring 150,000 t of Ingeo PLA online in 2025, offering a Midwest source that lowers freight and carbon costs for Northeastern converters. Polypropylene remains critical for snack-food BOPP overwraps where gloss and oxygen resistance outperform PE, while PET films serve retort pouches that withstand 121 °C sterilization. Collectively these secondary resins keep the United States plastic packaging films market diversified, safeguarding supply chains when any one feedstock sees price spikes.

By Functional Format: Barrier Films Lead While Retort Applications Surge

Barrier and high-barrier constructions captured 26.21% of United States plastic packaging films market size in 2025 as food processors pursue shelf-life assurance for broader omnichannel reach. EVOH-based multilayers remain the reference choice, yet 2024 saw rapid substitution toward recycle-ready PE structures that embed thin oxide layers. Metallization holds share in dry-goods segments, while transparent barriers support premium coffee where consumers expect product visibility.

Retort and ovenable films are on track for a 8.86% CAGR, the fastest among functional formats, fueled by meal-kit services and food-service automation that demand films tolerating 121 °C sterilization and 200 °F re-therm cycles. Form-fill-seal machines benefit from improved heat-seal windows, cutting cycle times and labor. Stretch films serve logistics wrap, yet shrink films face substitution risk from crate-based distribution models developed to reduce store-level waste. These shifts collectively anchor a medium-term upswing for the United States plastic packaging films market even as regulatory pressure intensifies.

By Thickness: Mid-Range Dominance Challenged by Ultra-Thin Innovation

The 21–40 µm range represented 45.08% of United States plastic packaging films market size in 2025 because it balances mechanical strength and barrier performance for mainstream SKUs. Sealed Air’s Cryovac Opti lineup uses orientation control to cut thickness by 30% while holding oxygen ingress constant, proving converters can meet EPR weight targets without equipment overhaul.

Ultra-thin gauges ≤20 µm will grow at a 6.14% CAGR through 2031, spurred by lightweighting incentives from brand owners facing Scope 3 accounting. Berry Global’s 18 µm PE platform maintains 15 N/15 mm tensile strength through bimodal molecular design, an approach now being trialed for medical-device overwraps. Films >70 µm persist in heavy-duty protein packs and industrial liners where puncture resistance trumps weight reduction; nonetheless, supply-chain CO₂ audits could eventually erode this niche if barrier technology catches up.

By End-User Industry: Food Dominance with Healthcare Acceleration

Food applications controlled 65.12% of United States plastic packaging films market in 2025, a share unlikely to slip soon given USD 856 billion in packaged food sales that year. Fresh-produce shippers specify breathable films that moderate respiration, whereas frozen-meal brands adopt recyclable retort pouches that run through continuous sterilizers. Conagra worked with Amcor in 2024 to finalize an all-PE retort structure that survives −20 °C storage and 200 °F consumer reheating, demonstrating functional parity with legacy nylon-based laminates.

Healthcare and pharmaceutical demand advances 7.05% annually as aging populations and specialty-drug pipelines expand barrier needs. Updated FDA guidance in 2024 elevated moisture-barrier standards for oral solids, increasing multilayer-film orders from blister-pack converters. Johnson & Johnson now requests mono-material PE for non-sterile devices, spurring resin suppliers to seek antimicrobial additives compatible with recycled content. Together, these verticals underpin resilient demand despite policy headwinds on single-use plastics.

Geography Analysis

The Northeast corridor accounts for the highest value density within the United States plastic packaging films market, leveraging premium consumer spend, dense pharmaceutical clusters, and early sustainability uptake. Healthcare packaging alone brought 35% of regional revenue in 2025, anchored by device makers in Massachusetts and New Jersey that demand validated barrier films. Localized EPR debate encourages faster adoption of mono-material packs, giving converters an innovation laboratory that later shapes national specifications.

The Southeast is the fastest-growing region, lifted by expanding protein-processing and favorable labor costs. Tyson Foods’ USD 300 million Tennessee complex added in-line pouch forming in 2024, pulling high-barrier PE orders from regional converters and ratcheting competition on delivery speed. Nearby resin capacity and improving recycling infrastructure reduce freight emissions, a factor now scored in retailer vendor portals.

The Midwest in the United States plastic packaging films market is growing significantly, thanks to food-processing density and manufacturing heritage. General Mills’ Ohio investment in 2024 shifted cereal liners to thin-gauge BOPP, lowering annual resin usage by 1,900 t. The Gulf Coast and Texas serve as resin and chemical-recycling hubs; ExxonMobil’s Baytown expansion will feed 1 billion lb of circular resin into film lines by 2027. California shapes specifications nationwide by wielding SB 54’s regulatory reach; converters must certify 65% recycling rates by 2032 or face penalties, pushing even Midwestern plants to design around West-Coast EPR scoring metrics.

Competitive Landscape

Industry consolidation accelerated in 2025 when Amcor closed its USD 8.4 billion share-for-share acquisition of Berry Global, creating a combined entity controlling nearly 15% of North American flexible-film capacity. The merger pools 400 sites and over 2 million t of resin purchasing, enhancing negotiating clout with petrochemical suppliers while aiming for USD 650 million annual synergies. Sealed Air positions for differentiation through its Prismiq digital-printing and automation suite, which delivered double-digit growth in 2024 service revenues as customers seek order-size agility.

Mid-tier players pursue niche specialization. Charter Next Generation acquired three regional converters in 2024, boosting medical-device barrier capacity and widening its East-Coast footprint. Toppan’s USD 1.8 billion purchase of Sonoco’s flexibles business opens Asian oxygen-barrier technology to US snack brands craving clear-film solutions. Simultaneously, resin suppliers form alliances with converters to guarantee outlets for emerging recycled grades; Amcor’s deal with Nova Chemicals secures mechanically recycled PE volumes that index to virgin-resin pricing for cost predictability.

Competitive intensity also shows in patent filings, which rose 23% for barrier-film technologies in 2024 as converters race for oxygen- and moisture-control breakthroughs.[4]United States Patent and Trademark Office, “Patents Search,” uspto.gov Start-ups backed by venture funds focus on bio-based films, but scale barriers persist given current resin supply chain dominance by petrochemical majors. Overall, the United States plastic packaging films market remains moderately concentrated, yet rapid innovation allows smaller specialists to carve profitable niches.

United States Plastic Packaging Films Industry Leaders

Profol Americas, Inc.

TEKRA, LLC. (A Mativ Brand)

Cosmo Films Inc.

Flex Films (USA) Inc. (UFlex Limited)

Taghleef Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: LyondellBasell approves USD 500 million chemical-recycling plant in Texas to process 150,000 t/year of PE and PP film waste.

- October 2024: Sealed Air debuts Cryovac Darfresh mono-PET rollstock, cutting 5,000 kg of plastic annually while extending shelf life.

- September 2024: Jindal Films launches J-311AA transparent high-barrier film for premium food packs.

- July 2024: Toray Plastics America invests USD 45 million to expand Rhode Island PET film production for retort applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States plastic packaging films market as all mono- and multilayer polymer films supplied in rollstock or converted form for primary or secondary packaging of goods across food, healthcare, personal care, industrial, and e-commerce channels.

Scope exclusion: disposable rigid plastics, stretch/shrink pallet wrap, and agricultural silage films sit outside this assessment.

Segmentation Overview

- By Material Type

- Polyethylene (LDPE, LLDPE, HDPE)

- Polypropylene (BOPP, CPP)

- Polyethylene Terephthalate (BOPET)

- Polyvinyl Chloride (PVC)

- Bio-based and Biodegradable Films

- Other Material Types

- By Functional Format

- Stretch Films

- Shrink Films

- Barrier and High-barrier Films

- Retort and Ovenable Films

- Lidding and Sealant Films

- Form-fill-seal (FFS) Films

- By Thickness

- ≤20 µm

- 21–40 µm

- 41–70 µm

- More than 70 µm

- By End-user Industry

- Food

- Candy and Confectionery

- Frozen Foods

- Fresh Produce

- Dairy Products

- Dry Foods and Cereals

- Meat, Poultry and Seafood

- Pet Food

- Other Food Products

- Beverage

- Healthcare and Pharmaceutical

- Personal Care and Home Care

- Industrial Packaging

- Agriculture and Horticulture

- Other End-user Industry

- Food

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed US film extruders, machinery vendors, packaging engineers at national food brands, and procurement leads at large online retailers. Conversations validated layer structures, average selling prices, recycled-content uptake, and regional lead times, which were critical in testing model sensitivities and gap-filling desk data.

Desk Research

We began by mapping supply using publicly available customs codes, the US Census Annual Survey of Manufactures, and resin capacity releases from the American Chemistry Council. Trade association briefs from the Flexible Packaging Association, FDA packaging compliance notices, and patent filings retrieved via Questel added process and regulatory context. Company 10-Ks, investor decks, and news feeds on Dow Jones Factiva allowed us to benchmark converter revenues and investments. Government datasets on food retail sales and USPS parcel volumes further anchored end-use demand. The sources cited above are illustrative; many other publications informed supporting checks.

Market-Sizing & Forecasting

A top-down reconstruction built on domestic film extrusion output and net trade flows produced the initial 2024 demand pool. This was corroborated with selective bottom-up roll-ups of sampled converter sales and channel checks to refine average price spreads. Key variables include polyethylene and polypropylene resin indices, monthly packaged food shipment values, online parcel counts, landfill fee trajectories, and state recycled-content mandates; each informs volume elasticity or price pass-through. Forecasts employ multivariate regression blended with scenario analysis to reflect resin price cycles and sustainability legislation. Where small converter data gaps emerged, we used median capacity utilization benchmarks gathered during interviews before scaling totals.

Data Validation & Update Cycle

Model outputs face variance scans against historical consumption ratios, peer estimates, and sentinel indicators such as resin off-take reports. Findings pass a two-step analyst review, after which we refresh figures annually and issue interim updates if material events, such as plant closures, resin shocks, or major M&A, alter baselines.

Why Mordor's United States Plastic Packaging Films Baseline Stands Up to Scrutiny

Published estimates vary because firms choose different material baskets, end-use mixes, and refresh cadences.

Key gap drivers include inclusion of pallet wraps and shrink films by some publishers, broader 'flexible packaging' scopes that fold in pouches and labels, and heavy reliance on converter revenue surveys without volume back-checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.75 B (2025) | Mordor Intelligence | - |

| USD 32.7 B (2024) | Regional Consultancy A | Counts stretch, shrink, and PVC industrial wrap; limited primary validation |

| USD 63.46 B (2023) | Global Consultancy B | Measures total flexible packaging (bags, pouches, labels) via revenue extrapolation; lacks tonnage cross-triangulation |

The comparison shows how Mordor's tighter scope, dual research pathway, and variable-level corroboration yield a balanced, transparent baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the United States plastic packaging films market?

The market stands at USD 18.53 billion in 2026 and is forecast to reach USD 22.96 billion by 2031.

Which material holds the largest market share?

Polyethylene led with 40.92% of United States plastic packaging films market share in 2025, driven by cost-effective ethane feedstock and established recycling streams.

Which segment is growing fastest?

Retort and ovenable films are expanding at a 8.86% CAGR because convenience-meal brands need packaging that withstands high-temperature processing through 2031.

How are state EPR laws affecting converters?

Programs in California, Oregon, and Washington impose fees tied to recyclability, prompting rapid adoption of mono-material and ultra-thin designs to control costs.

What role does chemical recycling play in future supply?

Investments from ExxonMobil, Eastman, and LyondellBasell will add more than 1.2 million t of circular resin capacity by 2027, offering brand owners additional recycled-content options without sacrificing performance.

How concentrated is competition in this market?

After the Amcor–Berry Global merger, the top two firms control roughly one-quarter of capacity, giving the market a moderate concentration level that still leaves room for innovative mid-tier and niche players.

Page last updated on: