Mecoprop Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

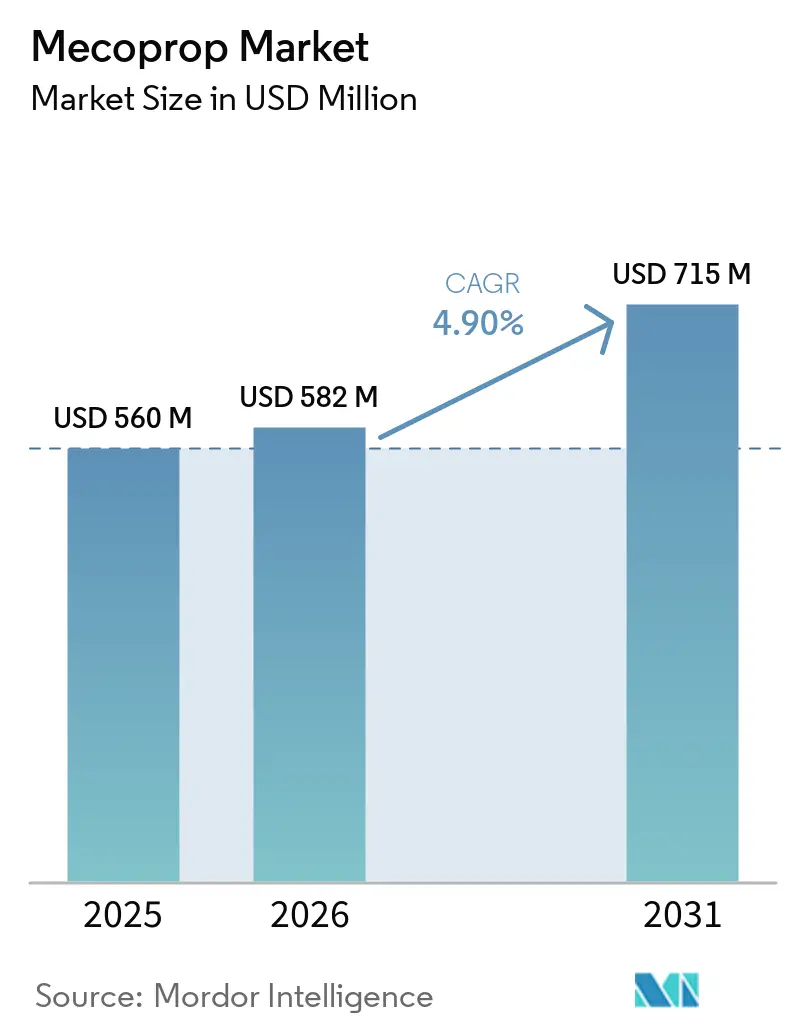

| Market Size (2026) | USD 582 Million |

| Market Size (2031) | USD 715 Million |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mecoprop Market Analysis by Mordor Intelligence

The mecoprop market size was valued at USD 560 million in 2025 and estimated to grow from USD 582 million in 2026 to reach USD 715 million by 2031, at a CAGR of 4.9% during the forecast period (2026-2031). Market momentum is shaped by six primary growth drivers, notably municipal and institutional bans on glyphosate, which are pushing turf managers toward selective phenoxy programs and fast-track approvals of lower-toxicity Mecoprop-P, unlocking consumer and professional demand across North America, Europe, and Australia. Urban expansion in Asia-Pacific, the Middle East, and Africa is swelling professional turf contracts, while the rise of online agrochemical marketplaces is widening distribution in developing nations, each adding roughly +0.8% to the forecast. At the same time, four headwinds temper growth with stringent residue limits in food crops, broadleaf weed resistance, volatile costs for 2,4-dichlorophenol feedstock, and a gradual shift toward organic lawn care in high-income municipalities, together subtracting about 2.0% from potential gains.

Key Report Takeaways

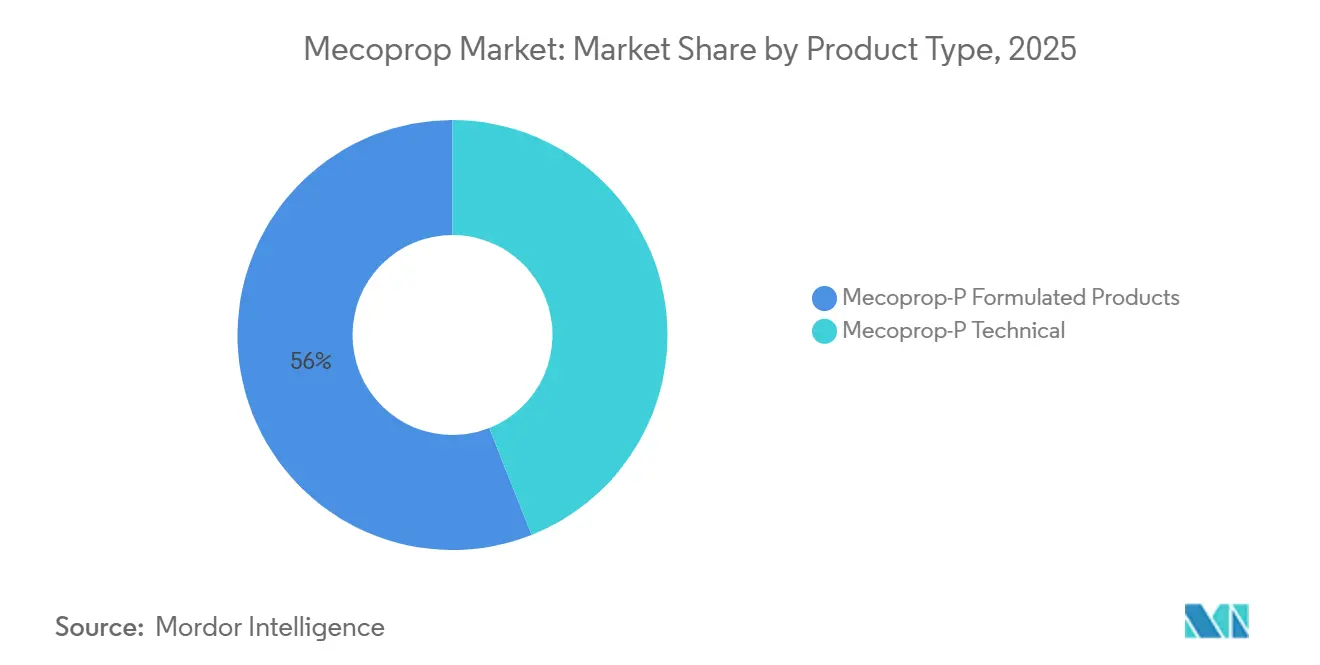

- By product type, Mecoprop-P formulated products held the largest share, accounting for 56% of the mecoprop market share in 2025, while Mecoprop-P technical concentrates are forecast to record the fastest 7.7% CAGR through 2026-2031.

- By formulation, emulsifiable concentrates held the largest share, accounting for 40% of the market in 2025, while ready-to-use aerosols are projected to register the fastest 8.4% CAGR during 2026-2031.

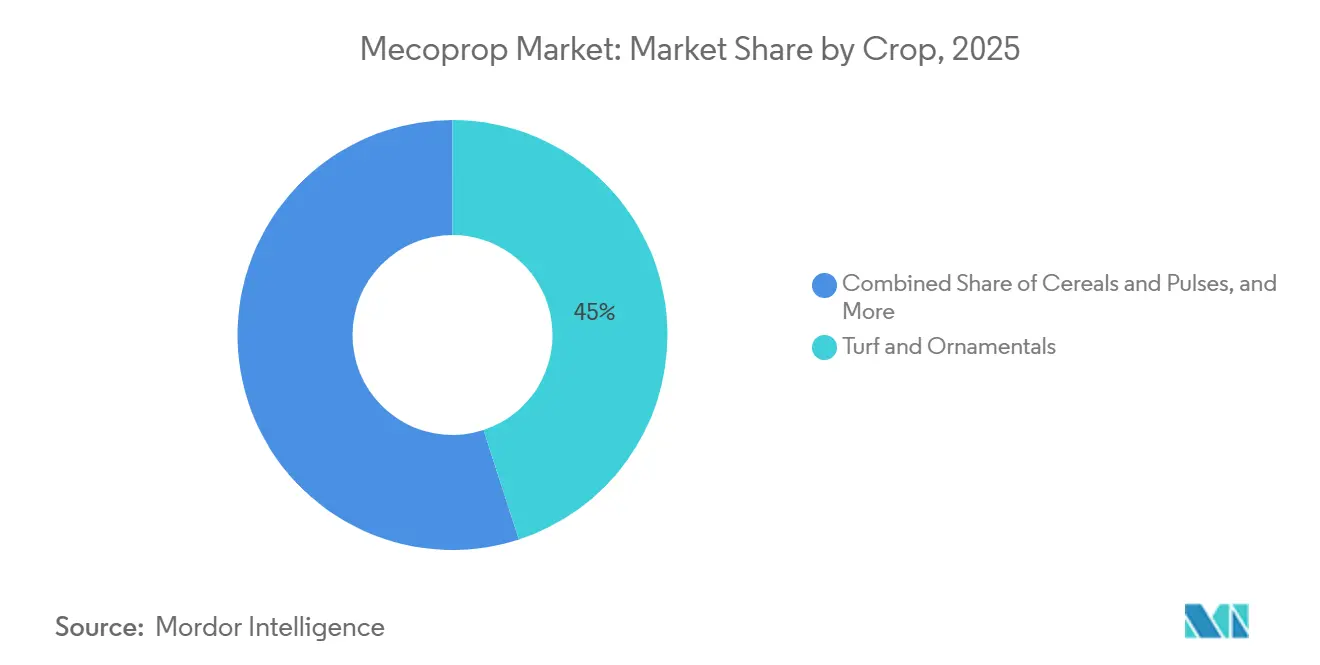

- By application, turf and ornamentals held the largest share, accounting for 45% of the mecoprop market size in 2025, while residential lawns and gardens are anticipated to chart the fastest 7.2% CAGR through 2026-2031.

- By distribution channel, direct sales to distributors captured the largest 51% of market share in 2025, while online agrochemical platforms are anticipated to post the fastest 8.9% CAGR over 2026-2031.

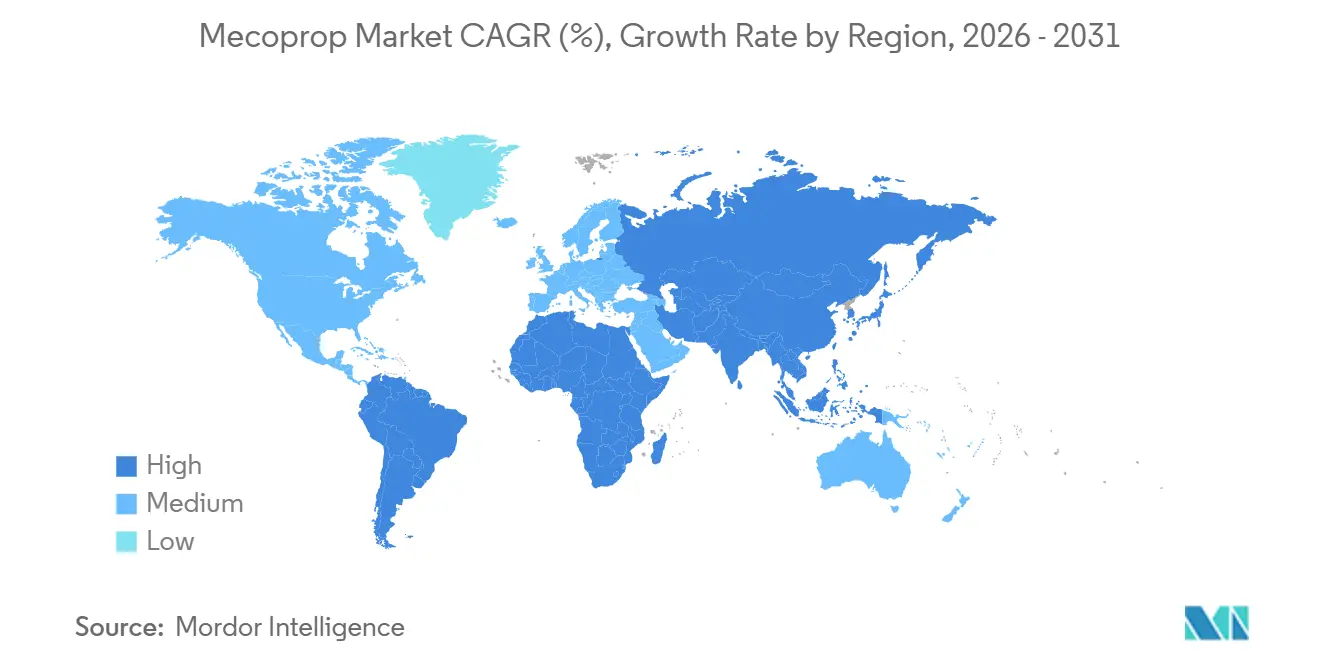

- By geography, North America held the largest share, accounting for 31% of the market in 2025, while Asia-Pacific is set to expand at the fastest 8.6% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mecoprop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding bans on glyphosate pushing turf managers toward selective phenoxy herbicides | +1.2% | North America and Europe, with spillover to urban Asia-Pacific municipalities | Medium term (2-4 years) |

| Regulatory approvals of Mecoprop-P enantiomer with lower toxicity profile | +0.9% | Global, led by North America, Europe, and Australia | Short term (≤ 2 years) |

| Growth of professional turf and lawn care services in urbanizing economies | +0.8% | Asia-Pacific core, the Middle East, and Africa | Long term (≥ 4 years) |

| Integration of herbicide-tolerant seed coatings enabling combined pre and post emergence control | +0.6% | North America, South America, and the Asia-Pacific grain belts | Medium term (2-4 years) |

| Rising adoption of ready-to-use consumer lawn weed control products in DIY retail | +0.7% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Rapid growth of online agrochemical marketplaces boosting distribution reach in developing nations | +0.8% | Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Bans on Glyphosate Pushing Turf Managers Toward Selective Phenoxy Herbicides

Municipal limitations on glyphosate have accelerated substitution toward phenoxy herbicides in golf courses, sports fields, and municipal parks. Turf managers increasingly adopt three-way mixes of 2,4-D, dicamba, and Mecoprop-P to maintain broadleaf control without depending on non-selective burndown programs. Health Canada renewed multiple Mecoprop-P combinations in 2025, keeping professional and residential label uses open[1]Source: Pest Management Regulatory Agency, “Applications Containing Mecoprop-P,” hc-sc.gc.ca. Extension guides in the Pacific Northwest recommend broadcast rates of 0.75 pound acid equivalent per acre, highlighting Mecoprop-P’s safety on fine bentgrass. Ongoing United States policy reviews of glyphosate supply reliability reinforce the shift, ensuring steady demand for phenoxy alternatives through 2031[2]Source: United States Environmental Protection Agency, “Mecoprop-P 98 Technical Registration,” epa.gov . The trend provides a durable tailwind for the mecoprop market across mature and emerging regions.

Regulatory Approvals of Mecoprop-P Enantiomer with Lower Toxicity Profile

Fast-track registrations for single-enantiomer Mecoprop-P reduce mammalian toxicity and environmental persistence relative to racemic mixtures, unlocking new consumer and professional applications. Health Canada cleared several new or renewed dossiers in 2025, signaling confidence in the R-enantiomer’s safety profile. The University of Hertfordshire database still flags racemic Mecoprop-sodium as posing reproductive hazards, underscoring the advantage of purified material. Manufacturers with enantiomer-specific synthesis capacity are gaining regulatory preference, consolidating market share in high-value turf segments. Lower hazard ratings open distribution in jurisdictions that previously restricted phenoxy use, such as several European municipalities. As approvals spread, demand for Mecoprop-P formulations will support stable volume growth and improved pricing power during 2026-2031.

Growth of Professional Turf and Lawn Care Services in Urbanizing Economies

Rapid urban expansion in Asia-Pacific, the Middle East, and Africa is increasing the construction of golf courses, stadiums, and public parks that need professional weed management. Rising disposable incomes and government investment in green infrastructure sustain year-round service contracts that specify selective herbicides with low turf injury. BASF SE and Corteva Agriscience launched the Clearfield Mustard system in India in 2026, demonstrating corporate commitment to trait-herbicide packages for emerging markets. Syngenta Group introduced VIRESTINA technology in Argentina in 2026 and plans wider rollouts across Asia-Pacific, demonstrating parallel innovation focused on selective weed control. These developments strengthen the mecoprop market outlook as contractors standardize Mecoprop-P in integrated programs to meet performance and safety requirements.

Integration of Herbicide-Tolerant Seed Coatings Enabling Combined Pre and Post Emergence Control

Seed companies are embedding multi-mode herbicide tolerance traits into cereals and oilseeds, permitting over-the-top phenoxy applications without crop damage. The 2022 BASF SE and Corteva Agriscience collaboration aims to commercialize soybean stacks tolerant to 2,4-D choline, glufosinate, PPO inhibitors, and glyphosate in the early 2030s, paving a path for Mecoprop-compatible programs. Clearfield systems show the scalability of non-transgenic tolerance in mustard and canola, reinforcing farmer familiarity with post-emergence phenoxy use. Trait stacks allow flexible in-season weed control, reducing reliance on pre-plant burndown and supporting phenoxy demand in cereals and pulses. As more seed coatings reach commercial scale, acreage suitable for Mecoprop-P applications will rise steadily. The trend is particularly important in regions facing herbicide resistance, where alternative modes help preserve yield.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent maximum residue limits for phenoxy acids in food crops | -0.6% | Global, with heightened enforcement in Europe and North America | Medium term (2-4 years) |

| Emerging resistance in broadleaf weeds is reducing field efficacy | -0.5% | North America's grain belt, Europe's cereal regions, and Australia | Long term (≥ 4 years) |

| Price volatility of key feedstock 2,4-Dichlorophenol is impacting production cost | -0.4% | Global, affecting all phenoxy manufacturers | Short term (≤ 2 years) |

| Increasing shift toward organic lawn and landscape management | -0.5% | North America and Europe urban municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Maximum Residue Limits for Phenoxy Acids in Food Crops

Food-safety regulators in Europe and North America enforce lower residue tolerances that restrict phenoxy applications in cereals, oilseeds, and forage. Extension guides list long preharvest intervals for 2,4-D and related mixtures, highlighting compliance challenges. Export-oriented growers face shipment rejection if residues exceed destination limits, prompting avoidance of Mecoprop in edible rotations. The University of Hertfordshire database continues to flag reproductive hazards for certain salts, adding regulatory pressure for tighter oversight. As scrutiny mounts, demand migrates from food crops to turf, ornamentals, and industrial vegetation management, potentially trimming mecoprop market growth.

Emerging Resistance in Broadleaf Weeds is Reducing Field Efficacy

Waterhemp populations in Michigan showed confirmed resistance to 2,4-D in 2025, extending phenoxy resistance beyond prior hotspots. Ontario detected 47 resistant waterhemp samples in 2025, many of which showed multigene resistance, illustrating rapid genetic adaptation[3]Source: Ontario Ministry of Agriculture Food and Rural Affairs, “Resistant Weed Testing Results,” omafra.gov.on.ca . Pacific Northwest guides now list multiple phenoxy-resistant weeds in alfalfa establishment, signaling broader erosion of efficacy. Resistance forces higher use rates, tank mixes, or chemistry rotation, adding cost and complexity for growers. Without new stewardship measures, declining control could threaten future demand for Mecoprop and moderate mecoprop market share in cereal rotations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Formulated Solutions Dominate End-User Purchases

Mecoprop-P formulated products generated the largest 56% share of mecoprop market size in 2025 as contractors and homeowners preferred the ready-to-spray ease of use. Technical concentrates serve toll formulators and experienced distributors and are projected to grow at the fastest 7.7% CAGR during 2026-2031, propelled by rising generic output in China and India. Regulatory pathways, such as United States conditional registrations, allow new technical imports once data call-ins are met. Growing concentrate availability boosts local formulation in price-sensitive regions. Consequently, formulated products will retain the bulk of the mecoprop market, while concentrates expand their reach into emerging economies.

Technical material buyers benefit from flexible blending that tailors solvent choice, adjuvants, and packaging to local agronomic needs. Asian formulators often down-pack into one-liter bottles that align with the purchasing power of smallholders. Larger distributors in South America prefer drum imports that feed automated filling lines for regional brands. As phytotoxicity data accumulate for Mecoprop-P alone and in mixes, demand for concentrates should strengthen. The interplay between premium branded formulations and cost-efficient generics will shape future mecoprop market dynamics.

By Formulation: Aerosols Capture Homeowner Spend

Emulsifiable concentrates maintained the largest 40% mecoprop market share in 2025 because professional applicators value tank-mix flexibility and equipment compatibility. Soluble concentrates followed due to higher active loading and lighter packaging. Ready-to-use aerosols are forecast for the fastest 8.4% CAGR from 2026-2031, supported by DIY merchandising, low-volatility salts, and built-in drift guards. Granular formulations serve niche lawn segments where combined fertilizer and weed control provide season-long benefit. Continued innovation in emulsifiable technology, such as built-in safeners, maintains relevance in broadacre cereals facing resistant weeds.

Consumer convenience dictates aerosol growth as homeowners seek grab-and-go weed solutions without measuring. Retail planograms place aerosols near sprinkler gear and grass seed to capture impulse traffic. Manufacturers reformulate to reduce odor and staining, increasing acceptance among suburban households. Water-based, soluble concentrates appeal to parks departments seeking to reduce solvent emissions. Segment diversity ensures steady demand and balances the overall mecoprop market size against evolving user preferences.

By Crop/Application: Turf and Ornamentals Remain Core Usage

Turf and ornamentals delivered the largest 45% revenue in 2025, driven by golf courses, sports venues, and sod farms that demand selective broadleaf control with minimal turf injury. Residential lawns and gardens are advancing at a 7.2% CAGR through 2026-2031 as urbanization raises homeownership and lawn care spending in Asia-Pacific. Industrial and non-crop sites, such as rights-of-way and energy facilities, provide stable demand where cost and persistence matter more than crop safety. Cereal and pulse acreage uses smaller volumes due to stringent residue limits and competing chemistries. As glyphosate scrutiny persists, integrated programs featuring Mecoprop-P mixes remain attractive for turf managers seeking resistance stewardship.

Homeowners increasingly treat lawns as lifestyle symbols, buying seasonal three-way mixes that include Mecoprop-P. Contractors schedule split applications aligned with spring and summer flushes of clover and plantain. Rights-of-way managers value phenoxy blends for broadleaf knockdown without brownout of perennial grasses that stabilize soil. In food crops, Mecoprop-P serves as a rotational tool in areas where ALS or PPO resistance limits other options. Collectively, these uses anchor the mecoprop market while providing headroom for growth in urban and infrastructure segments.

By Distribution Channel: Digital Platforms Accelerate Direct Access

Direct sales to distributors accounted for 51% of revenue in 2025, reflecting entrenched wholesale structures that serve professional turf managers and farm retailers. Retail garden centers remain important for homeowner traffic in developed markets and account for a significant share of regional sales. Online agrochemical platforms will post the fastest 8.9% CAGR during 2026-2031, propelled by lower transaction costs, transparent pricing, and data-driven marketing. Manufacturers leverage drop-shipping from regional hubs to minimize inventory risk and speed delivery. Hybrid omnichannel models emerge as distributors launch proprietary apps to retain customer relationships.

Digital adoption widens the mecoprop market by making branded products visible to small growers who historically bought unlabelled generics. Loyalty points, instructional videos, and agronomy hotlines embedded in apps improve correct use and repeat purchases. Payment gateways partner with micro-finance providers, easing cash flow for low-income farmers. Brick-and-mortar distributors respond by bundling services such as sprayer calibration and resistance testing. Competition between channels should ultimately improve the availability and stewardship of Mecoprop-P worldwide.

Geography Analysis

North America held the largest 31% share of the mecoprop market in 2025, driven by extensive use on golf courses, sports fields, and residential lawns. Growth is forecast to be at a descent CAGR during 2026-2031, as mature demand is offset by stricter municipal pesticide bylaws and rising organic preferences. United States policy discussions on glyphosate supply encourage diversification into phenoxy mixes, underpinning baseline Mecoprop demand. Canada maintains a streamlined registration process, renewing multiple Mecoprop-P products in 2025 to ensure continued supply. Resistance emergence in waterhemp and kochia underscores the need for integrated management, but phenoxy herbicides remain a critical tool.

Asia-Pacific is the fastest-growing regional market, with a 8.6% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and expanding e-commerce distribution. China dominates technical production and exports, while India and Southeast Asian nations add residential lawn adoption. BASF SE and Corteva Agriscience introduced the Clearfield Mustard production system in India in 2026, showcasing the corporate focus on trait packages that can be transferred to turf and specialty crops. Australia’s golf and sports turf sector continues to invest in selective herbicides to manage resistant broadleaf weeds, sustaining Mecoprop volume. Regional governments fund park construction and greening projects, thereby increasing demand for professional turf services.

Europe accounted for a significant share of 2025 sales and is projected to grow at descent CAGR during 2026-2031, given regulatory tightness and rising organic lawn care. Nufarm Ltd.’s Wyke facility delivered volume gains in 2025 but faced margin pressure from low phenoxy prices. Herbicide resistance surveys in Ireland and the United Kingdom highlight the spread of ALS and ACCase resistance, prompting renewed interest in multi-mode mixes that include phenoxy actives. Germany and France sustain agricultural use in cereals and oilseeds, while the United Kingdom depends on turf and amenity markets. Eastern Europe shows steady demand from broadacre grains, although geopolitical uncertainties influence spending patterns.

Competitive Landscape

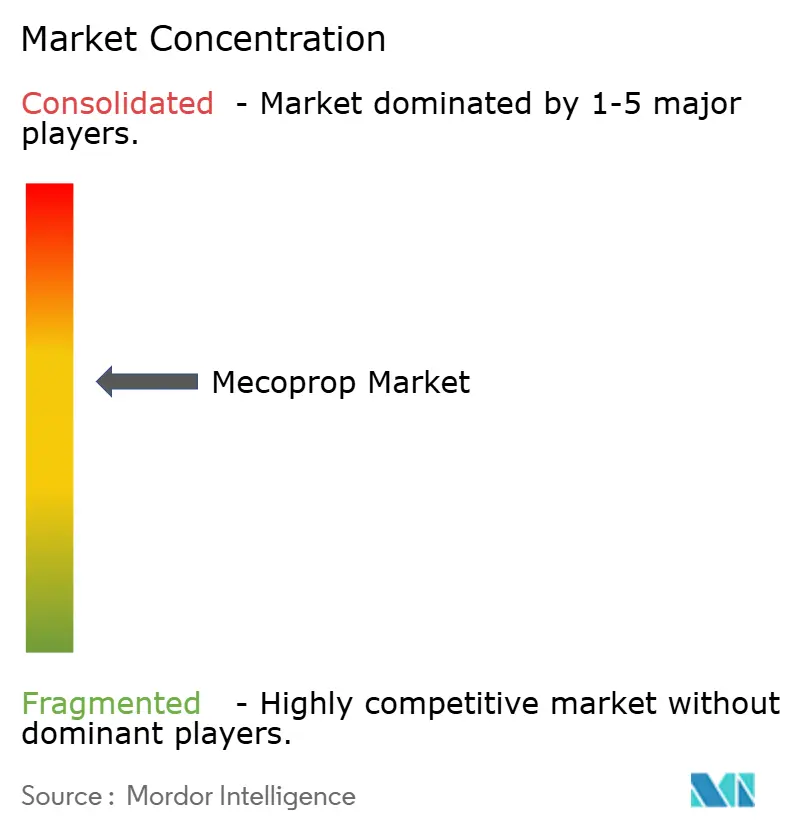

The mecoprop market is moderately concentrated, with the top five suppliers, including BASF SE, Corteva Agriscience, Bayer AG, Nufarm Limited, and Syngenta Group, collectively accounting for a dominant share of the mecoprop market size in 2025. BASF SE strengthened its lead by winning United States approval in 2026 for Engenia herbicide on dicamba-tolerant soybeans and cotton, underscoring its emphasis on trait-enabled weed control. It also introduced Ridivex herbicide for corn in 2026, adding a safener-enhanced premix that broadens the spectrum and lengthens residual activity. Corteva Agriscience deepened its collaboration with BASF SE to co-develop multistack herbicide-tolerant soybeans slated for the early 2030s, signaling sustained investment in complementary phenoxy use patterns.

Bayer AG is advancing icafolin-methyl, filed in four major markets in 2025 with first launches targeted for 2028, which could reshape post-emergence broadleaf programs. Nufarm Limited upgraded its Wyke and Laverton synthesis sites in 2025 to improve reliability, even as temporary idle charges compressed margins. Syngenta Crop Protection AG (Syngenta Group) gained Argentine approval in 2026 for VIRESTINA technology, which targets resistant grass weeds, widening its portfolio beyond traditional phenoxy chemistry. Together, these three companies bolster market stability through diverse pipelines, global manufacturing footprints, and extensive stewardship training.

Growth momentum also comes from agile challengers. Albaugh, LLC, FMC Corporation, and UPL Limited expand private-label and value brands that appeal to cost-focused buyers in South America and Southeast Asia. Chinese producers Jiangsu Jiangnan Agrochemical Co., Ltd., Zhejiang Xinan Chemical Industrial Group Co., Ltd., and Shandong Rainbow Agro Co., Ltd. scale low-cost Mecoprop-P technical, pressuring prices while widening access in emerging markets. Nutrien Ltd., HELM AG, Gowan Company, LLC, and Valent U.S.A. LLC (Sumitomo Chemical Co., Ltd.) leverages digital platforms, distribution alliances, and reformulation know-how to reach turf managers and smallholders directly. Continued capital spending, product innovation, and omnichannel sales strategies are anticipated to extend market breadth through 2031.

Mecoprop Industry Leaders

BASF SE

Corteva Agriscience

Nufarm Limited

Syngenta Group

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Syngenta Group unveiled VIRESTINA technology, the first selective herbicide in 40 years to control resistant grass weeds in soybean and cotton, with initial approval in Argentina and planned registrations in Brazil, Australia, the United States, and Canada. The arrival of a new mode of action drives integrated weed-management programs that layer broadleaf phenoxy partners, thereby sustaining incremental demand for Mecoprop formulations.

- March 2026: BASF SE announced Ridivex herbicide for corn, a post-emergence premix combining diflufenzopyr, dicamba, and pyroxasulfone that offers up to eight weeks of residual control, pending United States EPA registration. Such multi-site blends reinforce growers' reliance on selective broadleaf actives for rotational flexibility, indirectly supporting Mecoprop market growth through complementary tank mixes.

Global Mecoprop Market Report Scope

Mecoprop is a systemic, selective phenoxy herbicide and plant growth regulator commonly used to manage broadleaf weeds in turf, lawns, and cereal crops. It is often applied in combination with herbicides such as 2,4-D or dicamba and disrupts weed cell division.

The Mecoprop Market Report is Segmented by Product Type (Mecoprop-P Technical, and Mecoprop-P Formulated Products), by Formulation (Emulsifiable Concentrate (EC), and More), by Crop/Application (Turf and Ornamentals, and More), by Distribution Channel (Direct Sales to Distributors, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD)

| Mecoprop-P Technical |

| Mecoprop-P Formulated Products |

| Emulsifiable Concentrate (EC) |

| Soluble Concentrate (SL) |

| Granular Formulations |

| Ready-to-Use Aerosols |

| Turf and Ornamentals |

| Cereals and Pulses |

| Residential Lawns and Gardens |

| Direct Sales to Distributors |

| Online Agrochemical Platforms |

| Retail Garden Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Mecoprop-P Technical | |

| Mecoprop-P Formulated Products | ||

| By Formulation | Emulsifiable Concentrate (EC) | |

| Soluble Concentrate (SL) | ||

| Granular Formulations | ||

| Ready-to-Use Aerosols | ||

| By Crop/Application | Turf and Ornamentals | |

| Cereals and Pulses | ||

| Residential Lawns and Gardens | ||

| By Distribution Channel | Direct Sales to Distributors | |

| Online Agrochemical Platforms | ||

| Retail Garden Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the mecoprop market by 2031?

The mecoprop market size is forecast to reach USD 715 million by 2031.

Which region will register the fastest growth through 2031?

Asia-Pacific is anticipated to grow at an 8.6% CAGR during 2026-2031, the fastest among all regions.

Which product type currently holds the largest revenue share?

Mecoprop-P formulated products led with 56% of global revenue in 2025.

What is the growth outlook for online agrochemical platforms?

Online platforms are projected to expand at an 8.9% CAGR during 2026-2031 as digital access improves in developing regions.

Who are the leading suppliers in the mecoprop market?

BASF SE, Corteva Agriscience, Bayer AG, Nufarm Limited, and Syngenta Group together held a dominant share of global revenue in 2025.

Page last updated on: