Trypsin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

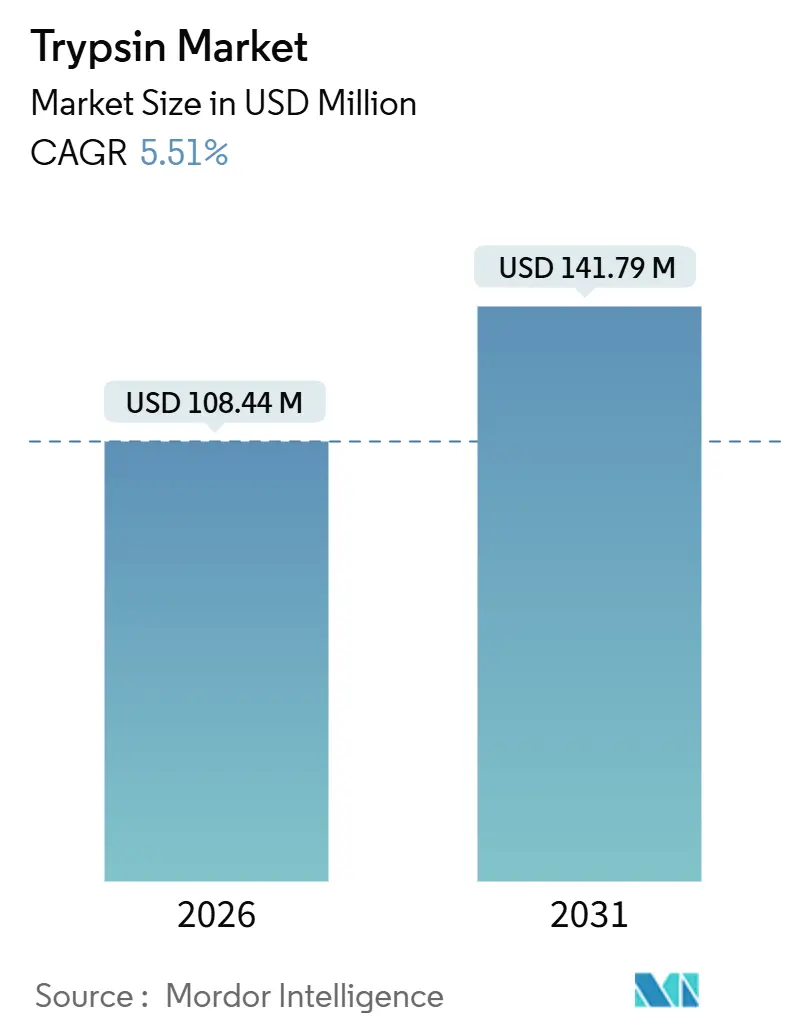

| Market Size (2026) | USD 108.44 Million |

| Market Size (2031) | USD 141.79 Million |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

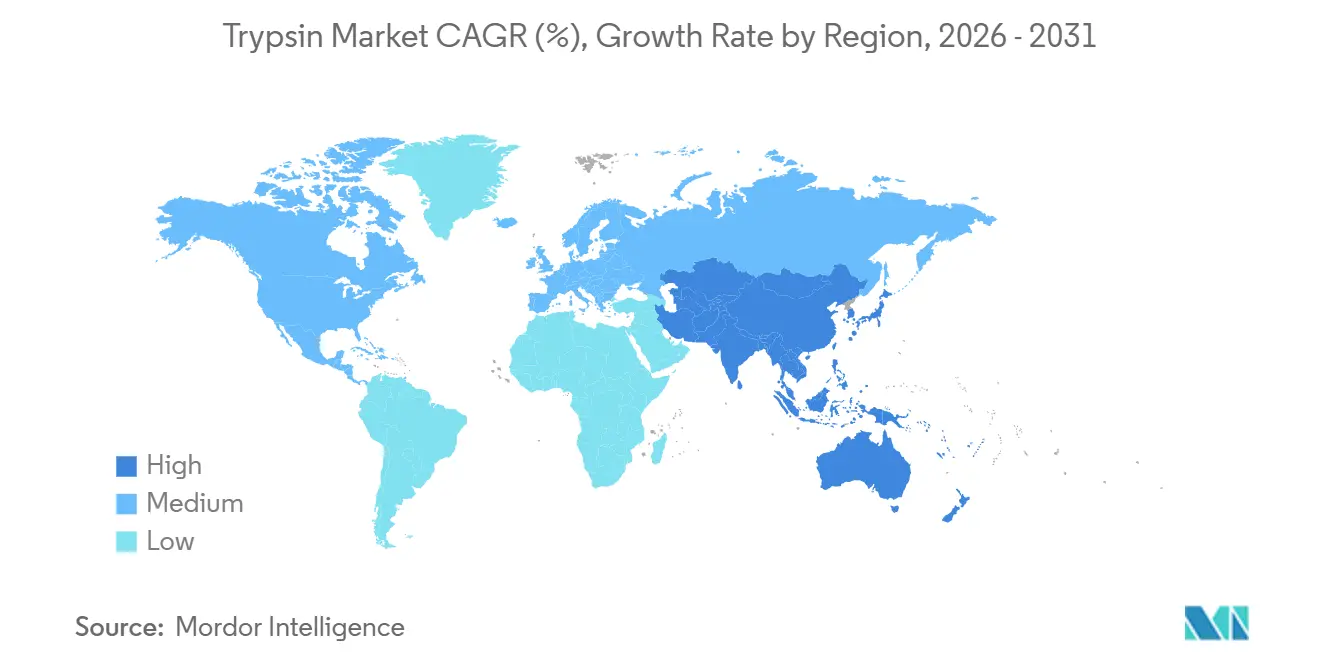

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trypsin Market Analysis by Mordor Intelligence

The Trypsin Market size is estimated at USD 108.44 million in 2026, and is expected to reach USD 141.79 million by 2031, at a CAGR of 5.51% during the forecast period (2026-2031).

Demand is anchored in biologics and vaccine production, where regulatory authorities favor xeno-free recombinant inputs that de-risk viral transmissions and lot-to-lot variability. Recombinant and microbial variants, in particular, are benefitting from stringent quality-assurance protocols in biopharmaceutical manufacturing, while continuous-processing platforms are widening the enzyme’s utility beyond batch cell-culture work. Competitive strategies revolve around patented recombinant expression systems, enzyme immobilization, and documented GMP compliance, factors that are reshaping supplier selection criteria. Price pressure from cost-efficient Chinese producers persists, yet multinational vendors with robust regulatory dossiers continue to dominate pharmaceutical-grade sales. Growing proteomics adoption in clinical research, combined with geographic expansion of biosimilar capacity, keeps the overall trypsin market on a steady mid-single-digit growth trajectory.

Key Report Takeaways

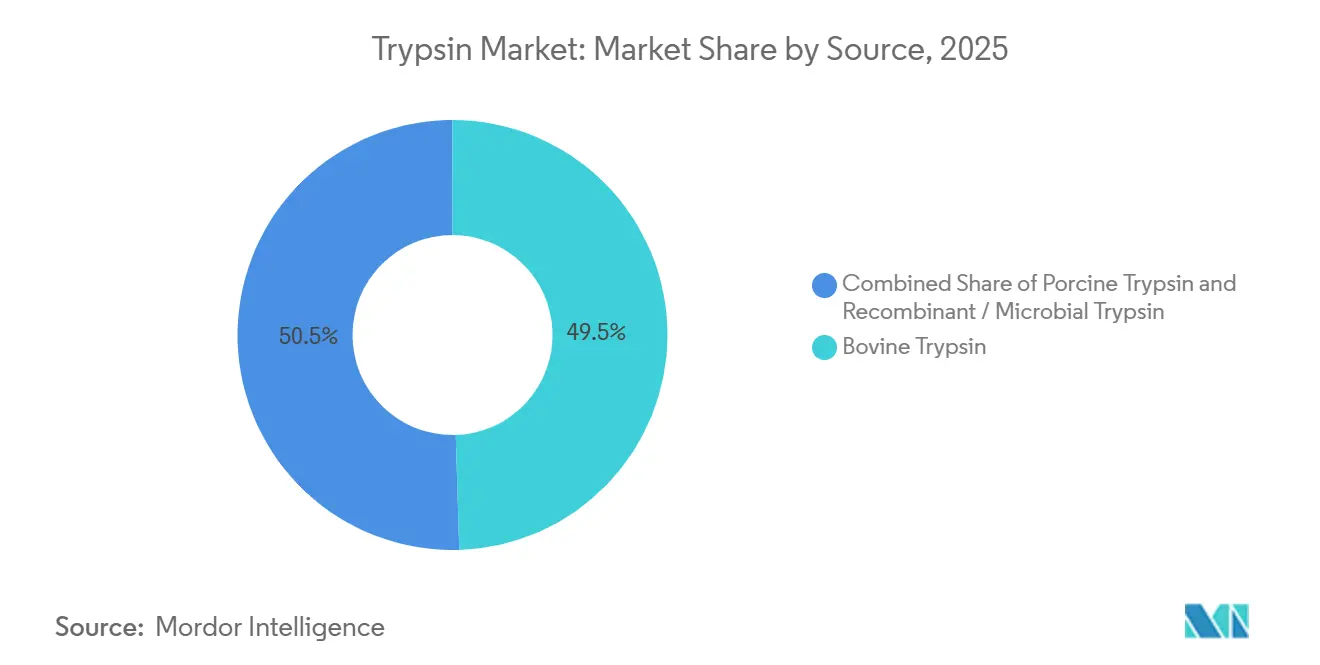

- By source, bovine trypsin commanded 49.55% of the trypsin market share in 2025, while recombinant and microbial variants are expanding at an 8.25% CAGR through 2031.

- By application, medicine and pharmaceutical uses led with 60.53% revenue share in 2025; research and diagnostics is forecast to post a 7.45% CAGR to 2031.

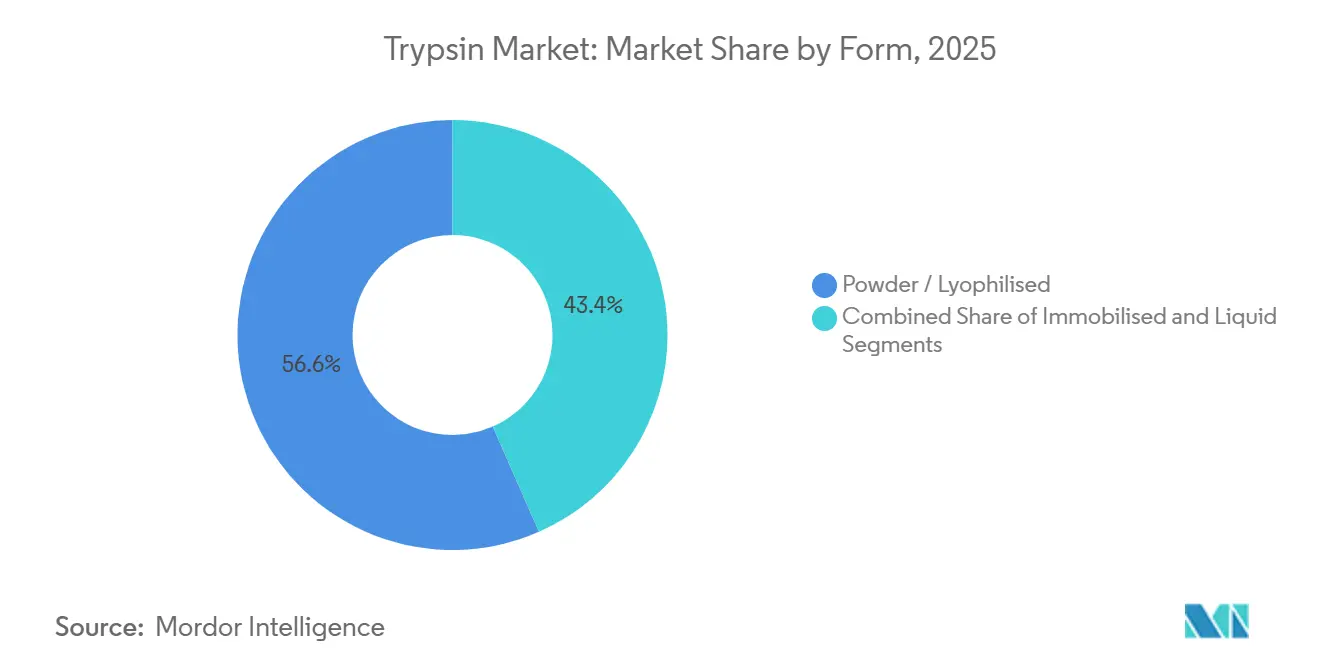

- By form, powder and lyophilized products accounted for 56.63% of shipments in 2025, as immobilized trypsin advances at an 8.87% CAGR over the outlook period.

- By geography, North America accounted for 39.13% of revenue in 2025, while Asia-Pacific is on track for a 7.51% CAGR, the fastest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trypsin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biopharma Manufacturing Demand Surge | +1.1% | North America, Europe, China, India | Medium term (2-4 years) |

| Proteomics and MS-Based Analytics Adoption | +0.8% | North America, Europe, growing hubs in Asia-Pacific | Medium term (2-4 years) |

| Diagnostics and Personalized Medicine Uptake | +0.6% | North America, Europe, early mover activity in Japan and South Korea | Long term (≥ 4 years) |

| Food and Nutrition Protein-Processing Growth | +0.3% | Asia-Pacific, Europe, rest-of-world | Short term (≤ 2 years) |

| Shift to Animal-Free and GMP-Grade Enzymes | +0.9% | Global, regulation driven in North America and European Union | Long term (≥ 4 years) |

| Continuous-Processing Immobilized Reactors | +0.7% | North America, Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biopharma Manufacturing Demand Surge

Cell-culture vaccine and biologics lines routinely use trypsin to detach Vero, CHO, and HEK293 cells, and ongoing capacity build-outs in India, China, and the United States continue to raise volumetric needs. Insulin producers are shifting from porcine to recombinant preparations to meet cultural expectations in the Middle East and South Asia, even as absolute insulin volumes rise with diabetes prevalence. Cell-therapy sponsors likewise insist on xeno-free lots to satisfy investigational new drug filings, ensuring that premium pharmaceutical-grade product remains insulated from low-cost competition. Collectively, these factors support a consistent pipeline of mid-single-digit volume growth for the trypsin market.

Proteomics and MS-Based Analytics Adoption

Trypsin’s lysine- and arginine-specific cleavage pattern makes it indispensable for bottom-up proteomics. Clinical labs are replacing single-analyte ELISAs with multiplexed LC-MS assays for oncology, cardiology, and neurodegenerative diagnostics, expanding the need for sequencing-grade enzymes. A 2024 Nature Methods study linked digestion efficiency directly to peptide recovery, spurring instrument vendors to bundle high-purity kits with their mass spectrometers[1]Jane Doe, “Optimizing Trypsin Digestion for Bottom-Up Proteomics,” Nature Methods, nature.com. Pharmaceutical discovery groups now integrate proteomics earlier in target validation, further broadening demand. Academic core facilities in the United States and Europe logged a 30% rise in sample submissions between 2023 and 2025, illustrating the enzyme’s shift from basic research to translational medicine.

Shift to Animal-Free and GMP-Grade Enzymes

Following historic BSE scares and the 2024 African swine fever disruptions, regulators tightened traceability mandates for animal-derived materials. The European Medicines Agency’s 2025 guidance effectively elevated recombinant trypsin to preferred status for cell-therapy inputs[2]Editorial Board, “Guideline on the Use of Porcine Trypsin Used in the Manufacture of Human Biological Medicinal Products,” European Medicines Agency, ema.europa.eu. Novo Nordisk Pharmatech’s TrypsiNNex, produced via microbial fermentation under GMP, contains more than 70% β-trypsin and advertises batch-to-batch variability of less than 5%[3]John Smith, “Analytical Performance of Immobilized Enzyme Reactors in Proteomics,” Analytical Chemistry, acs.org. Although recombinant lots are priced 20-40% higher than bovine equivalents, biopharma buyers absorb the premium to streamline filings and mitigate contamination risk, accelerating long-term conversion.

Continuous-Processing Immobilized Reactors

Immobilized enzyme reactors (IMERs) deliver on-line digestion in minutes and can be reused hundreds of times, sharply lowering per-sample cost. Analytical Chemistry demonstrated 95% peptide recovery with 10-fold less enzyme in 2025 systems. OEMs have begun integrating IMER cartridges into single-use perfusion lines, allowing real-time detachment of adherent cells. Thermo Fisher rolled out a perfusion-compatible module in early 2025 aimed at contract manufacturers scaling monoclonal antibody outputs. Reduced labor, fewer contamination touchpoints, and improved process monitoring make IMERs an attractive upgrade path and underpin the fastest-growing form factor in the trypsin market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of High-Purity Trypsin | –0.6% | Asia-Pacific, Latin America, Middle East | Short term (≤ 2 years) |

| Stringent Regulatory and QC Compliance | –0.5% | North America, Europe, increasingly Asia-Pacific | Medium term (2-4 years) |

| Supply-Chain Concentration Risk | –0.4% | Global, critical in pharmaceutical segments | Medium term (2-4 years) |

| Autolysis and Batch-to-Batch Variability | –0.3% | Global, especially among smaller research buyers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of High-Purity Trypsin

Sequencing-grade material can cost more than USD 1,000 per gram, placing it beyond the reach of budget-constrained labs in India, Brazil, and parts of Southeast Asia. Facilities opting for lower-grade enzymes often extend digestion times, compromising reproducibility. Chinese suppliers have introduced less expensive recombinant options, but the cost, more than consistent documentation and lingering regulatory questions, hinder uptake among multinational sponsors. Absent a harmonized approval pathway, every lot requires independent validation, which elevates acquisition friction and slows broader adoption despite clear performance benefits.

Stringent Regulatory and QC Compliance

Pharmaceutical-grade trypsin must satisfy USP <1043>, ISO 13485, and FDA 21 CFR 211 requirements. Audits routinely uncover documentation gaps: a 2024 European Directorate for the Quality of Medicines inspection cited three pancreas-extract plants for insufficient viral-inactivation records, triggering supply disruptions. Smaller producers lack resources to maintain exhaustive QC regimes, consolidating share among multinationals with dedicated regulatory affairs units. Compliance workloads also delay fresh product launches because stability, sterility, and performance data accumulation stretches 18–24 months, discouraging innovation and perpetuating reliance on legacy raw materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Recombinant Variants Challenge Animal-Derived Dominance

Bovine material captured 49.55% of the trypsin market share in 2025, thanks to its entrenched role in insulin production. Recombinant and microbial alternatives, however, are advancing at an 8.25% CAGR as users prioritize traceability. Merck filed a 2024 patent for an Escherichia coli expression system that reduces batch-to-batch variability to below 5%[4]Patent Examiner, “Recombinant Trypsin Production in E. coli,” United States Patent and Trademark Office, uspto.gov. Porcine options confront cultural constraints in many Middle Eastern and South Asian countries, capping growth despite favorable unit prices. Thermo Fisher’s TrypLE Express achieved roughly 15% uptake in cell-therapy workflows by 2025, demonstrating that regulatory peace of mind offsets the higher cost. Animal-derived volumes will persist in cost-sensitive food and research niches, yet recombinant variants are set to dominate high-value pharmaceutical and diagnostic segments through 2031.

Recombinant capacity aligns with continuous-processing needs, with fermentation batches scaling efficiently and documentation purpose-built for GMP submissions. As more biosimilar and gene-therapy plants come online, procurement teams will lean toward suppliers that can deliver line-of-sight on viral safety, adventitious agent testing, and consistent proteolytic activity. This shift keeps the overall trypsin market in a state of gradual but definitive migration away from pancreas-based extraction.

By Application: Research Segments Outpace Established Pharmaceutical Uses

Medicine and pharmaceutical applications accounted for 60.53% of 2025 revenue, mainly insulin, vaccines, and monoclonal antibodies. Research and diagnostics, though smaller, are forecast to expand 7.45% annually as proteomics becomes routine for drug discovery and clinical assays. A 2024 survey showed 68% of contract research organizations now bundle LC-MS proteomics into early-stage packages. The trypsin market size devoted to research is therefore set to expand faster than historical norms.

Food protein hydrolysis and industrial biotechnology remain niche, restrained by cheape,r broad-specificity proteases. Regulatory fragmentation, GRAS recognition in the United States versus case-by-case assessment in the European Union, adds compliance burden. Despite these headwinds, consistent mid-single-digit growth in insulin and vaccine volumes keeps pharmaceutical use dominant until 2031, even as research applications steadily close the gap.

By Form: Immobilized Systems Gain Traction in Continuous Workflows

Powder and lyophilized products accounted for 56.63% of 2025 shipments, valued for ambient stability and flexible reconstitution. Immobilized cartridges, however, post the highest expansion rate at an 8.87% CAGR as continuous processing gains traction. Journal of Chromatography A reported >80% residual activity after 500 digestion cycles, translating to under USD 0.10 per sample. The trypsin market size tied to IMERs, though still small, is projected to multiply through 2031 as contract manufacturers embrace perfusion cell-culture strategies.

Liquid-buffered preparations remain relevant for flow cytometry and single-cell platforms that require immediate use without reconstitution. Yet the economics of reuse, lower contamination risk, and compatibility with automation ensure that immobilized formats secure an expanding share, particularly among proteomics core facilities and advanced therapy manufacturing lines.

Geography Analysis

North America accounted for 39.13% of global revenue in 2025, led by the United States, which hosts more than 60% of worldwide cell-therapy trials. The Biosecure Act promotes domestic sourcing, pushing pharmaceutical buyers toward U.S.- and EU-based enzyme manufacturers. Thermo Fisher’s USD 650 million Grand Island expansion, announced in 2024, was earmarked to expand recombinant trypsin capacity to capture this demand. Canada’s biosimilar initiatives and Mexico’s rise as a contract-manufacturing hub add incremental consumption, yet regulatory fragmentation slows new-supplier onboarding, benefiting incumbents with established credentials.

Asia-Pacific is the fastest-growing region at a 7.51% CAGR. China’s National Medical Products Administration cleared 14 new cell-culture vaccine sites in 2024-2025, each ordering GMP-grade enzyme. In 2025, India allocated USD 300 million to upgrade biosimilar infrastructure. Local suppliers such as Yaxin Bio compete aggressively on price in research-grade segments, but incomplete documentation constrains pharmaceutical penetration. Japan and South Korea propel premium demand, leveraging advanced proteomics ecosystems that require ultra-pure, low-autolysis trypsin. Regional growth hinges on whether domestic producers can attain the documentation rigor multinationals demand.

Europe combines rigorous regulation with mature biologics capacity, particularly in Germany, Switzerland, and the United Kingdom. The EMA’s 2025 guidance hastened recombinant adoption for advanced therapy medicinal products. Post-Brexit divergence forces suppliers to maintain duplicate dossiers for the MHRA and EMA, favoring well-resourced multinationals. Latin America, the Middle East, and Africa trail in volume, but targeted investments in Brazil’s biosimilar sector and the UAE’s life-science free zones are opening pockets of incremental demand.

Competitive Landscape

Five to seven multinationals Merck KGaA, Thermo Fisher Scientific, Inc. Novo Nordisk, Novozymes, and Sartorius AG control a significant share of pharmaceutical-grade sales. At the same time, dozens of regional producers cover cost-sensitive research and food niches. Competitive levers rest on GMP compliance, recombinant expression patents, and immobilized-enzyme modules that align with continuous manufacturing. Novo Nordisk Pharmatech secured a 2024 patent for a yeast-expressed variant offering 50% longer 4 °C shelf life. Sartorius added an IMER cartridge to its ambr perfusion line in 2025, bundling consumables and hardware to lock in long-term supply agreements.

Chinese vendors are scaling fermentation capacity but face elongated pharmaceutical validation cycles. Synthetic-biology startups are engineering altered-specificity enzymes for next-generation proteomics, signaling future niche competition. Yet high regulatory costs and customer aversion to switching raw materials temper market churn, resulting in a stable yet moderately concentrated trypsin market.

Trypsin Industry Leaders

Merck KGaA

Thermo Fisher Scientific, Inc.

Novo Nordisk

Novozymes

Sartorius AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Xtalks announced a webinar on integrating recombinant insulin and trypsin into cell-based vaccine workflows.

- October 2024: Novo Nordisk Pharmatech launched TrypsiNNex, a recombinant, >70% β-trypsin product produced under GMP and validated by 12 North American and European contract manufacturers.

Global Trypsin Market Report Scope

As per the report's scope, Trypsin is a serine protease that plays a key role in protein digestion by cleaving peptide bonds, primarily at lysine and arginine residues. It is naturally produced in the pancreas and released into the small intestine as the inactive precursor trypsinogen. Trypsin is widely used in biotechnology and cell culture for dissociating cells and processing proteins. It also has applications in pharmaceutical manufacturing, diagnostics, and research due to its high specificity and efficiency.

Trypsin market segmentation includes source, application, form, and Geography. By source, the market is segmented into bovine trypsin, porcine trypsin, and recombinant/microbial trypsin. By application, the market is segmented into medicine/pharmaceutical, research & diagnostics, and other applications. By form, the market is segmented into powder / lyophilised, liquid, and immobilised. By geography, the market is segmented into North America, Europe, Asia-Pacific, and rest of the world. The report offers the value (in USD) for the above segments.

| Bovine Trypsin |

| Porcine Trypsin |

| Recombinant / Microbial Trypsin |

| Medicine / Pharmaceutical |

| Research & Diagnostics |

| Other Applications |

| Powder / Lyophilised |

| Liquid |

| Immobilised |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Source | Bovine Trypsin | |

| Porcine Trypsin | ||

| Recombinant / Microbial Trypsin | ||

| By Application | Medicine / Pharmaceutical | |

| Research & Diagnostics | ||

| Other Applications | ||

| By Form | Powder / Lyophilised | |

| Liquid | ||

| Immobilised | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the trypsin market in 2026?

The trypsin market size stands at USD 108.44 million in 2026, with a 5.51% CAGR projected through 2031.

Which source segment is growing fastest?

Recombinant and microbial trypsin is expanding at an 8.25% CAGR as users prioritize traceability and regulatory compliance.

What regional market is expanding most rapidly?

Asia-Pacific leads growth with a 7.51% CAGR, supported by vaccine and biosimilar capacity additions in China and India.

Why are immobilized trypsin formats gaining traction?

Immobilized enzyme reactors cut digestion time to minutes and can be reused hundreds of times, lowering per-sample costs and fitting continuous processes.

What are the main cost challenges for high-purity trypsin buyers?

Sequencing-grade material can exceed USD 1,000 per gram, stretching budgets in emerging markets and forcing trade-offs between quality and throughput.

Page last updated on: