Measurement While Drilling (MWD) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.07 Billion |

| Market Size (2031) | USD 5.94 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

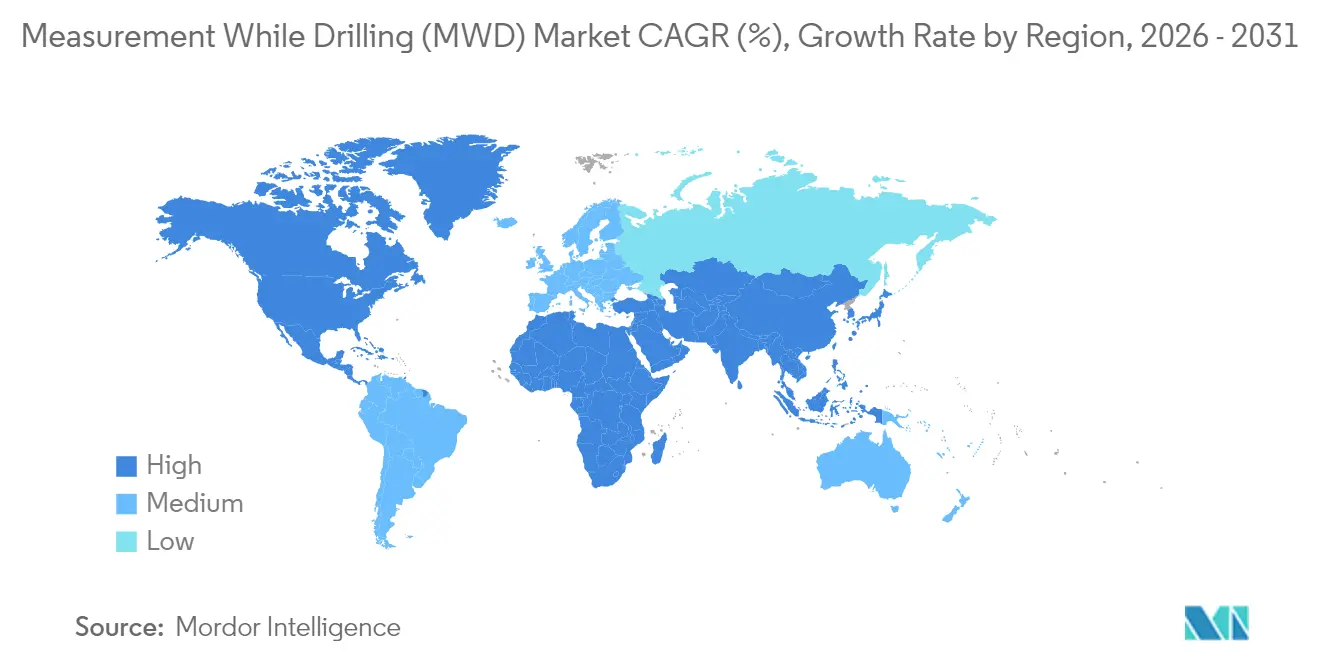

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

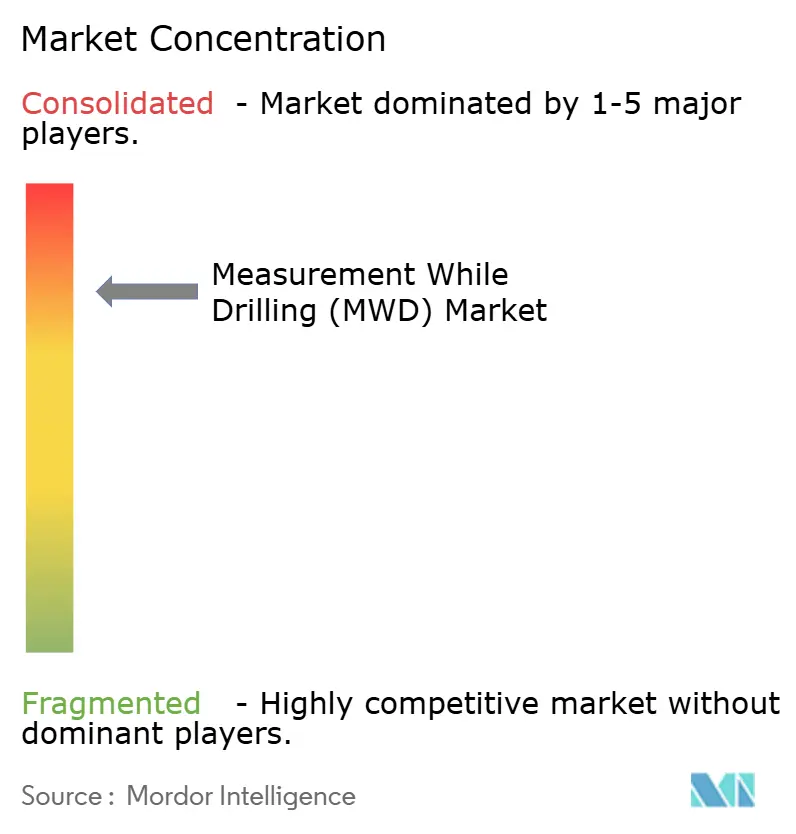

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Measurement While Drilling (MWD) Market Analysis by Mordor Intelligence

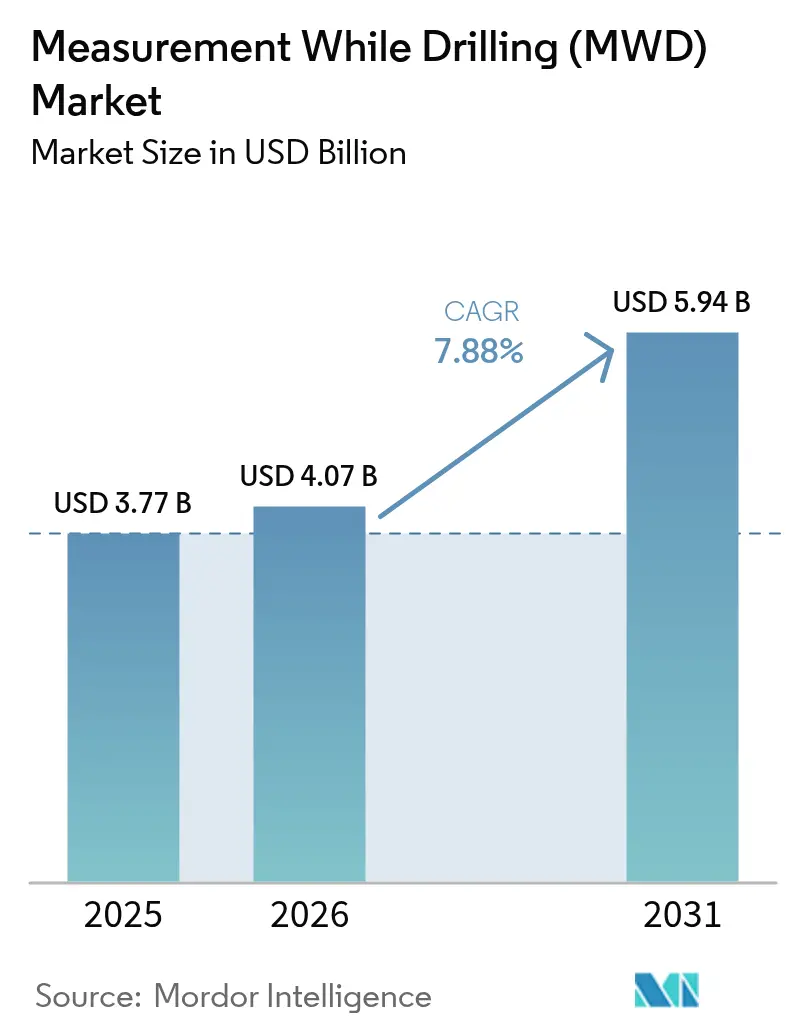

The Measurement While Drilling Market size is expected to grow from USD 3.77 billion in 2025 to USD 4.07 billion in 2026 and is forecast to reach USD 5.94 billion by 2031 at 7.88% CAGR over 2026-2031.

The accelerated adoption of real-time data acquisition, autonomous drilling, and high-bandwidth telemetry underpins this growth as operators strive to reduce non-productive time and enhance wellbore placement in complex formations.[1]SLB, “Autonomous Directional Drilling Systems,” slb.com Unconventional shale development in North America, a rebound in deep- and ultra-deep-water spending, and rising geothermal activity combine to widen the measurement while drilling market opportunity set. Competitive differentiation now pivots on artificial intelligence and closed-loop automation that boost drilling speed and reservoir contact while tempering safety risks. High-temperature reliability limits in HPHT wells and commodity price volatility remain the principal technical and commercial constraints.

Key Report Takeaways

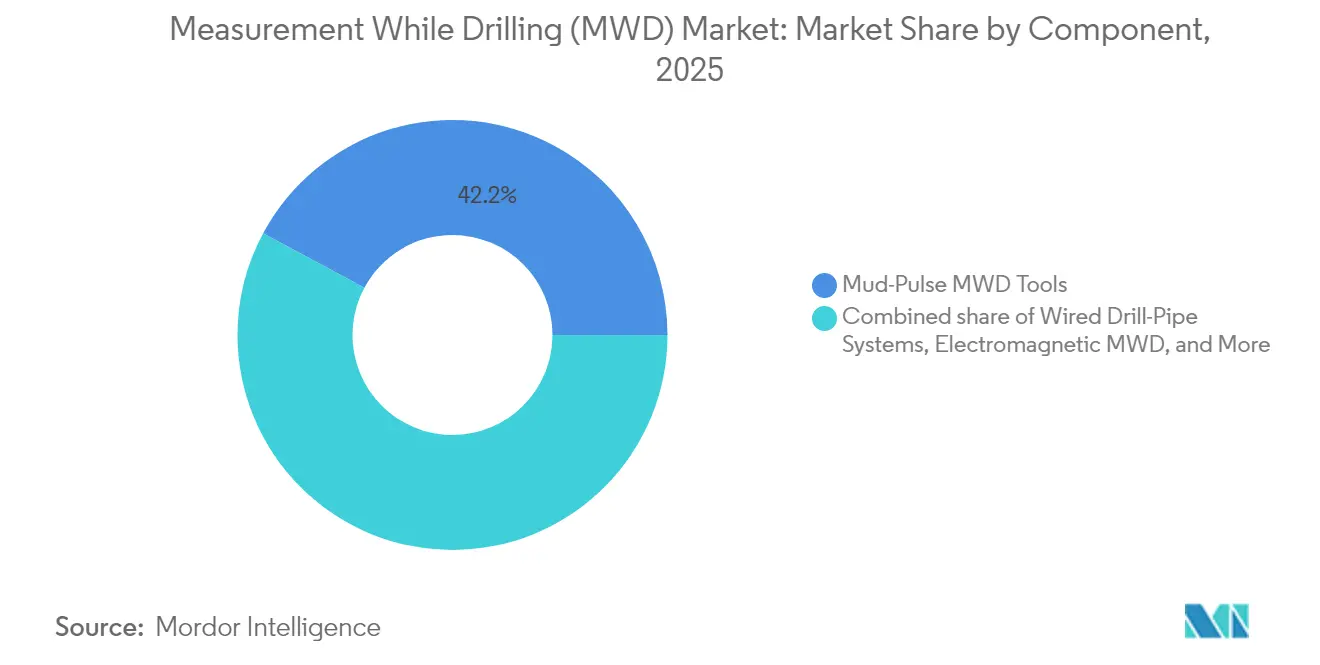

- By component, Mud-Pulse MWD tools led the measurement while drilling market share at 42.15% in 2025, while Wired Drill-Pipe systems are on track for a 9.73% CAGR through 2031.

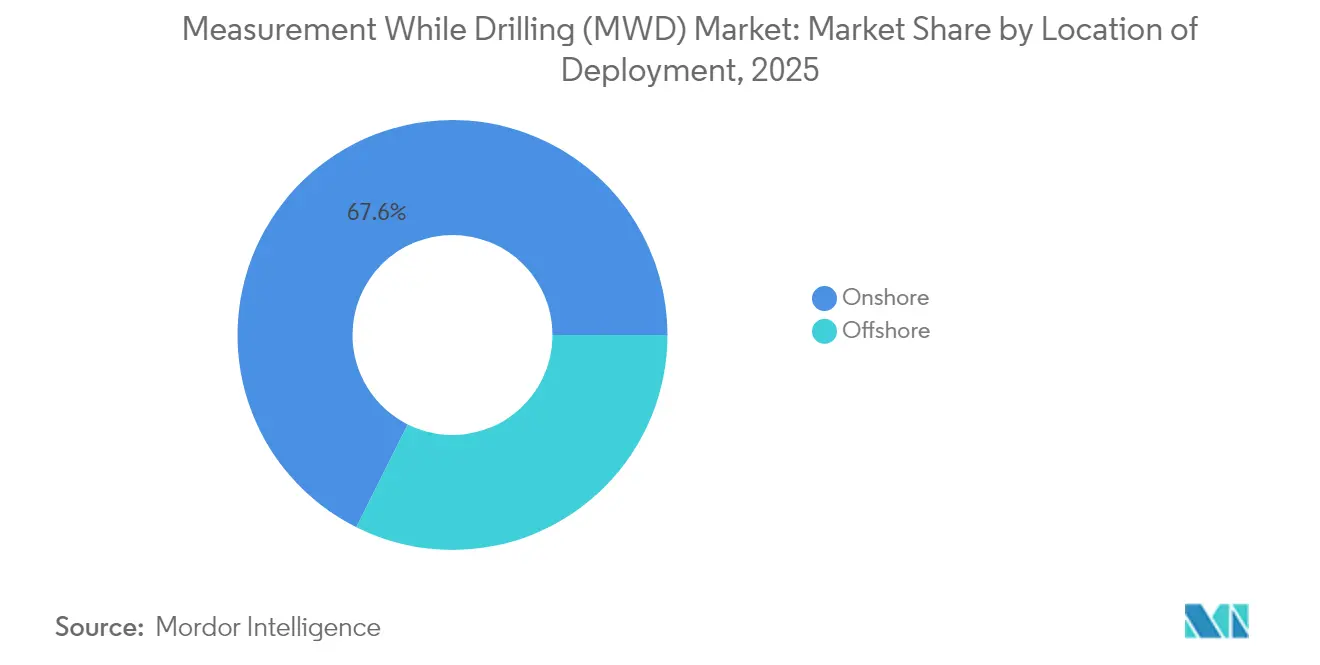

- By location of deployment, onshore operations captured 67.62% of 2025 activity, whereas offshore deployments are projected to advance at a 9.05% CAGR between 2026 and 2031.

- By geography, North America accounted for 38.12% of 2025 revenue, and the Asia-Pacific region is forecast to expand at an 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Measurement While Drilling (MWD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in unconventional shale drilling | +2.1% | North America, Argentina, Australia | Medium term (2-4 years) |

| Rising need to reduce NPT & well-costs | +1.8% | Global | Short term (≤ 2 years) |

| Deep- & ultra-deep-water CAPEX rebound | +1.5% | North Sea, Gulf of Mexico, Brazil, West Africa | Medium term (2-4 years) |

| Wired drill-pipe adoption | +1.2% | Global with early gains in North Sea and Gulf of Mexico | Long term (≥ 4 years) |

| Geothermal drilling for energy transition | +0.8% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Unconventional Shale Drilling

Horizontal shale wells in the Permian Basin continue to increase in length, with annual basin output expected to rise by 300,000 barrels per day, reaching 6.9 million barrels per day by 2026. Complex geosteering requirements in these extended laterals elevate demand for high-precision MWD systems that maintain borehole stability and optimize landing zones. Argentina’s Vaca Muerta program is scaling similar practices, using real-time pressure monitoring and formation mapping to unlock tight reservoirs efficiently. Continuous directional control enabled by advanced measurement while drilling market technology minimizes dogleg severity, lowers casing wear, and sustains reservoir contact across 10,000-foot laterals. Operators also deploy rotary steerable systems integrated with MWD sensors to decrease slide time and increase the average rate of penetration, thereby amplifying the economic benefit of each incremental foot drilled. Strategic focus on maximizing resource recovery at low break-even prices reinforces investment in robust downhole telemetry across unconventional portfolios.

Rising Need to Reduce NPT & Well-Costs via Real-Time Data

Unplanned events account for 15-20% of total drilling time, intensifying operator pressure to curtail non-productive time through continuous downhole feedback. Wired drill-pipe field trials by BP achieved average drilling time savings of 10%, proving that sub-second data improves weight-on-bit management and mitigates stuck-pipe risk.[2]OnePetro, “High-Bandwidth Wired Drill-Pipe Field Trial,” onepetro.org Real-time azimuthal gamma and resistivity measurements further sharpen geosteering accuracy, directly linking better placement to higher initial production rates. Measurement while drilling market technology capable of bidirectional command enables prompt parameter changes without tripping tools, eliminating costly lost circulation incidents. Enhanced reservoir exposure ultimately lifts estimated ultimate recovery, supporting capital-discipline strategies that dominate budget allocations in a volatile pricing world. The result is a compounding return on digital drilling investments even in mature fields.

Deep- & Ultra-Deep-Water CAPEX Rebound

Global offshore upstream spending is projected to exceed USD 300 billion in 2025 after rising 11% from 2024, signaling renewed capital flow into high-value deep-water prospects. Ultra-deepwater wells, located below 1,500 meters of water depth, require high-temperature, high-pressure-rated MWD systems that guide the bit trajectory through salt and sub-salt strata with narrow fracture gradients. The cost of remedial sidetracks increases offshore; therefore, real-time formation evaluation is crucial for selecting a safe casing point. Operators in Brazil and the Gulf of Mexico increasingly specify AI-enabled MWD packages that can predict drilling dysfunctions and autonomously adjust rotary steerable commands. Measurement-while-drilling market solutions supporting extended-reach wells also address the floating rig fleet’s need for shorter time-to-target to maintain project economics. Growth in subsea tiebacks and multi-well templates drives demand for high-bandwidth telemetry that can handle multi-phase flows and dynamic pressure changes without signal dropout.

Wired Drill-Pipe Adoption Enabling High-Bandwidth Telemetry

Data rates exceeding 57,000 bits per second over wired drill pipe contrast sharply with traditional mud-pulse telemetry, which operates at 10-40 bits per second, opening the path for real-time imaging while drilling and autonomous weight-on-bit control. The powerline system co-developed by Parker Wellbore and TDE shows industry commitment to robust and reusable downhole networks. Bidirectional communication allows surface engineers to modify tool programming on the fly, saving rig hours previously spent circulating for firmware updates. Although rig retrofits and handling practices require an upfront investment, early adopters report a measurable increase in penetration rate and a reduction in tortuosity in complex 3-D trajectories. Over the forecast horizon, the measurement while drilling market penetration of wired drill pipe is expected to transition from niche offshore pilots to mixed fleets across high-density shale pads, underpinning the market’s real-time automation narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility impacting E&P budgets | -1.4% | Global | Short term (≤ 2 years) |

| Reliability challenges of MWD in HPHT wells | -0.9% | Middle East, North Sea, Asia-Pacific | Medium term (2-4 years) |

| Data-ownership & cyber-security concerns | -0.6% | Global | Long term (≥ 4 years) |

| Shortage of skilled MWD field engineers | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Impacting E&P Budgets

Historical data show that every USD 1 decline in crude price is associated with an average disengagement of 64 drilling rigs worldwide, underscoring the sector’s sensitivity to price swings. US exploration and production companies trimmed 2024 capital spending to USD 61.7-65.4 billion, echoing a cautious stance toward discretionary drilling budgets. Tight-oil projects require breakeven levels near USD 50 per barrel, so marginal campaigns become uneconomic during downturns, delaying measurement while drilling market deployments. The asymmetric recovery pattern further depresses service pricing power, compelling providers to stretch payment terms and manage spare tool inventory. Financial uncertainty also slows large-scale telemetry upgrades as operators favor incremental enhancements over full wired drill-pipe conversions until price stability returns.

Reliability Challenges of MWD Tools in HPHT Wells

Conventional MWD electronics are generally rated for 175 °C, whereas ultra-HPHT wells in the Middle East and China can routinely exceed 200 °C and 30,000 psi. Failure rates increase markedly with temperature, reducing tool life and inflating non-productive time through unexpected trips. Shunbei deep-carbonate projects reported elevated incidence of downhole tool failures, prompting reliance on positive-displacement motors and limiting continuous telemetry in critical intervals. Next-generation sapphire-based sensor housings and high-temperature batteries are progressing; however, commercial release cycles lag behind near-term drilling schedules. Until proven HPHT-ready systems reach scale, the measurement while drilling market expansion into ultra-deep reservoirs will face technical challenges, particularly in fields that require continuous formation evaluation for safety compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: High-Speed Telemetry Reshapes Demand

Mud-Pulse systems dominated 2025 revenue with a 42.15% of measurement-while-drilling market share, as their reliability and rig-floor familiarity remain valuable in standard pressure and temperature conditions. However, the segment confronts mounting competition from Wired Drill-Pipe systems, projected to grow at a 9.73% CAGR through 2031, as operators equate higher bandwidth with faster decision-making cycles. The measurement while drilling market size tied to Electromagnetic MWD tools continues to rise in air-drilling and low-conductivity fluid operations, providing an alternate option where mud-pulse telemetry attenuates severely. Rotary steerable system modules are increasingly equipped with gyro-while-drilling and downhole vibration sensors, blending measurement and actuation within a single platform that supports autonomous navigation.

Demand for downhole telemetry sensors that capture dynamic pressure, shock, and rotational speed increases as real-time analytics enable immediate drill-string health management. SLB’s NeoLink demonstrates the migration toward integrated hardware and cloud-native software that shortens learning loops from the bit to the rig control system. Future growth in the measurement while drilling market hinges on modular tool designs that allow for rapid reconfiguration for geothermal, carbon capture, or extended-reach wells without inflating the string length. Providers investing in solid-state electronics, advanced vibration damping, and retrievable battery packs are likely to command premium day rates once drilling activity shifts toward more thermally and mechanically demanding plays.

By Location of Deployment: Onshore Scale Meets Offshore Complexity

Onshore drilling captured 67.62% of 2025 tool runs, supported by extensive shale development across North America, China, and the Middle East, where pad economies encourage high spud counts per rig. Land rigs benefit from lower logistics costs and improved well-site accessibility, enabling service providers to cycle tools efficiently and maintain high utilization rates. Nevertheless, offshore deployments are on track for a 9.05% CAGR to 2031, as deepwater campaign approvals accelerate and high-spec rigs demand integrated measurement while drilling market solutions that support managed pressure drilling and dual-gradient systems.

In ultra-deepwater Brazil and the Gulf of Mexico, continuous pressure while drilling modules detect micro-fracture gradients, enabling casing design optimization and safeguarding against kicks. The measurement while drilling market size, linked to offshore projects, benefits from premium pricing because downhole failures carry outsized cost penalties, incentivizing the adoption of high-reliability tools and redundancy protocols. Integration of seismic-while-drilling in challenging salt provinces informs real-time velocity models that guide bit steering, shrinking drilling uncertainty envelopes. Land projects continue to evolve towards factory-style operations where wired drill-pipe and closed-loop rig control drive rapid cycle times, cementing onshore as the volume anchor even as offshore remains the innovation pacesetter.

Geography Analysis

North America retained 38.12% of 2025 revenue in the measurement while drilling market, supported by sustained shale activity in the Permian Basin and deep-water exploration in the Gulf of Mexico. The region’s mature supply chain, abundant rig fleet, and data-driven operating culture drive the rapid adoption of automation, increasing the rate of penetration and minimizing sidetrack drilling. Canada’s oil-sands SAGD wells and emerging geothermal initiatives are driving demand for high-temperature MWD tools that can handle steam-assisted environments. Mexico continues to advance the Trion ultra-deepwater development, awarding multi-year contracts that specify AI-enabled service delivery to reduce well cycle time and enhance safety. The regulatory emphasis on remote real-time monitoring by agencies such as the Bureau of Safety and Environmental Enforcement further underscores the need for reliable, high-bandwidth telemetry in offshore wells.

The Asia-Pacific region is the fastest-growing, with an 8.56% CAGR expected through 2031, as national oil companies ramp up drilling to meet demand and improve energy security. China’s South China Sea projects deploy seismic-while-drilling for real-time formation imaging, enabling precise casing points in HPHT zones. India’s active rig count is projected to rise from 111 in 2024 to 142 by 2028, reflecting higher domestic production goals that translate into robust measurement while drilling market orders. Australia’s offshore gas fields and geothermal pilots similarly require high-temperature sensors and autonomous steering to control wellbore deviation in fractured granites. Southeast Asian operators in Indonesia and Malaysia focus on cost-effective MWD packages that balance real-time formation evaluation with lean rig budgets, highlighting the region’s price-performance sensitivity.

Europe’s market revolves around North Sea brownfield redevelopment and geothermal drilling aligned with decarbonization policy targets. Norway champions drilling automation, pairing Halliburton LOGIX software with Sekal AS algorithms to deliver autonomous directional drilling at scale. The measurement while drilling (MWD) market size in geothermal applications is expanding as Germany and the Netherlands incentivize the development of deep geothermal wells for district heating, necessitating tools that operate in corrosive brines at temperatures of up to 200 °C. The Middle East continues to experience steady growth, spurred by national oil company investments in unconventional reservoirs, such as Saudi Aramco’s Jafurah shale. Africa sees momentum in West Africa’s deep-water discoveries, while South America leverages Brazil’s pre-salt and Argentina’s shale developments to stimulate demand for high-spec MWD services capable of navigating tight pore-pressure margins.

Competitive Landscape

The measurement while drilling market features a balanced structure, where three integrated service majors combine for approximately 51.8% of global revenue. Baker Hughes leads at 23.99%, closely followed by Halliburton at 15.4% and SLB at 12.41%, leveraging global service coverage and proprietary telemetry systems. These companies capitalize on scale to fund R&D in AI-driven autonomous control, high-temperature electronics, and digital twin optimization, which shortens drilling days and elevates the average rate of penetration. Mid-tier firms focus on niche offerings such as gyro-while-drilling for magnetic interference zones or modular battery-free tools aimed at geothermal markets.

Strategic alliances accelerate technology deployment. The Turnwell venture, which involves ADNOC Drilling, SLB, and Patterson-UTI, integrates advanced tools with regional rig capacity, securing multi-year contracts that guarantee fleet utilization. Nabors Industries’ acquisition of Parker Wellbore strengthens its presence in managed pressure drilling and downhole power transmission, complementing the adoption of wired drill pipe. Large operators also partner directly with service firms, exemplified by Chevron and Halliburton’s intelligent hydraulic fracturing initiative, which utilizes ZEUS IQ™ to synchronize surface and subsurface data for real-time optimization.

Innovation pipelines remain active. Patent filings for high-power laser drilling, solid-state downhole batteries, and multi-mode telemetry highlight attempts to transcend mud-pulse bandwidth limits and expand operating envelopes beyond 230 °C. Suppliers delivering integrated hardware, analytics, and cloud connectivity are best positioned to secure premium contracts, particularly in offshore and HPHT projects, where reliability guarantees and data ownership clarity significantly influence tender outcomes. Smaller companies can still capture a share by excelling in specialist segments, such as azimuthal sonic logging or extreme-temperature electronics for geothermal wells, indicating that technological agility offsets some of the scale disadvantages.

Measurement While Drilling (MWD) Industry Leaders

Baker Hughes Co.

Halliburton Company

Schlumberger Limited

National-Oilwell Varco Inc.

Weatherford International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chevron and Halliburton deployed the ZEUS IQ™ intelligent fracturing platform that automates stage execution with subsurface feedback for real-time optimization.

- March 2025: SLB introduced EWC™ electric well-control systems that replace hydraulic units and deliver continuous data feeds for safer operations.

- February 2025: Halliburton and Sekal AS deployed the first autonomous on-bottom drilling solution on the Norwegian Continental Shelf.

- January 2025: SLB and Star Energy Geothermal agreed to accelerate the development of drilling technologies for geothermal assets, with a focus on subsurface characterization.

Global Measurement While Drilling (MWD) Market Report Scope

The measurement while drilling (MWD) market report include:

| Mud-Pulse MWD Tools |

| Electromagnetic MWD Tools |

| Wired Drill-Pipe Systems |

| Gyro-While-Drilling Systems |

| RSS-Integrated MWD Modules |

| Downhole Telemetry Sensors |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Netherlands | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Nigeria | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Mud-Pulse MWD Tools | |

| Electromagnetic MWD Tools | ||

| Wired Drill-Pipe Systems | ||

| Gyro-While-Drilling Systems | ||

| RSS-Integrated MWD Modules | ||

| Downhole Telemetry Sensors | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Netherlands | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Nigeria | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected growth rate for the measurement while drilling market between 2026 and 2031?

The market is forecast to grow at a 7.88% CAGR, rising from USD 4.07 billion in 2026 to USD 5.94 billion in 2031.

Which component segment leads the measurement while drilling market share today?

Mud-Pulse MWD tools lead with 42.15% of 2025 revenue owing to broad rig compatibility and proven reliability.

Why is wired drill-pipe gaining traction in measurement while drilling operations?

Wired drill-pipe enables data rates above 57,000 bps, supporting real-time decision making and autonomous drilling that cuts average well time by about 10%.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to expand at an 8.56% CAGR as China, India, and Australia increase drilling to meet energy demand.

How do oil-price fluctuations influence measurement while drilling tool demand?

Lower prices prompt operators to defer advanced drilling programs, with each USD 1 price decline historically linked to an average drop of 64 active rigs, directly reducing MWD service uptake.

What technical hurdle limits MWD adoption in HPHT environments?

Conventional electronics typically fail above 175 °C, so operators in HPHT wells above 200 °C face higher tool failure rates until new high-temperature systems become commercially available.

Page last updated on: