Meal Replacement Shakes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

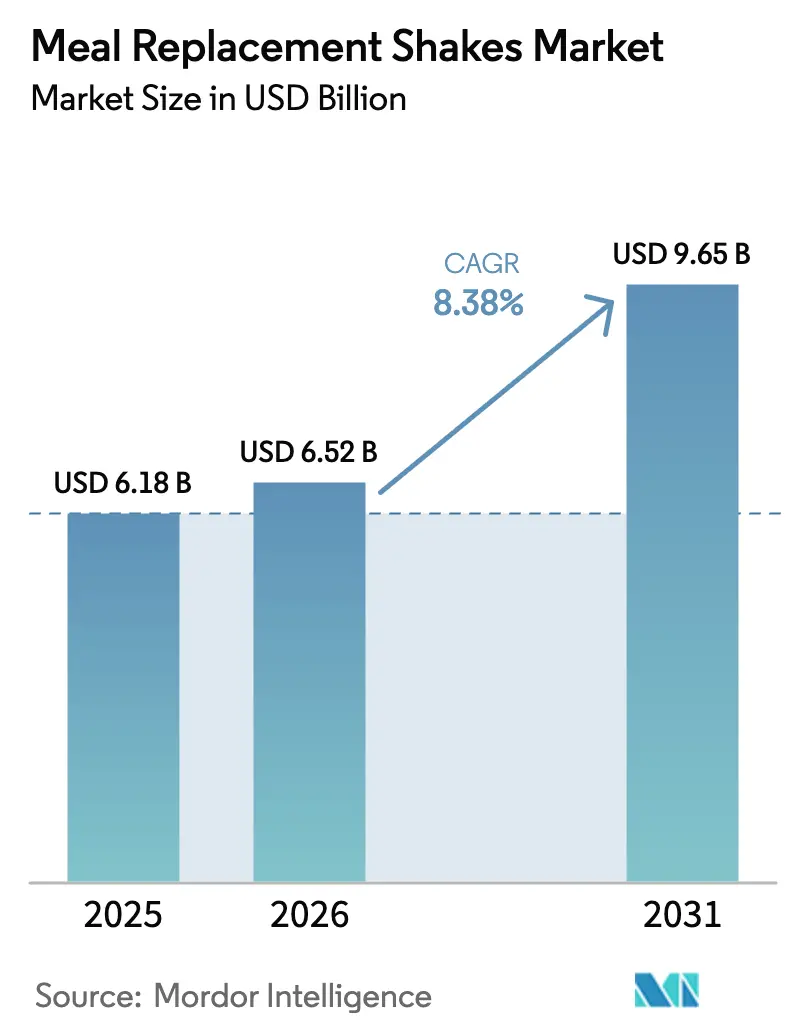

| Market Size (2026) | USD 6.52 Billion |

| Market Size (2031) | USD 9.65 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

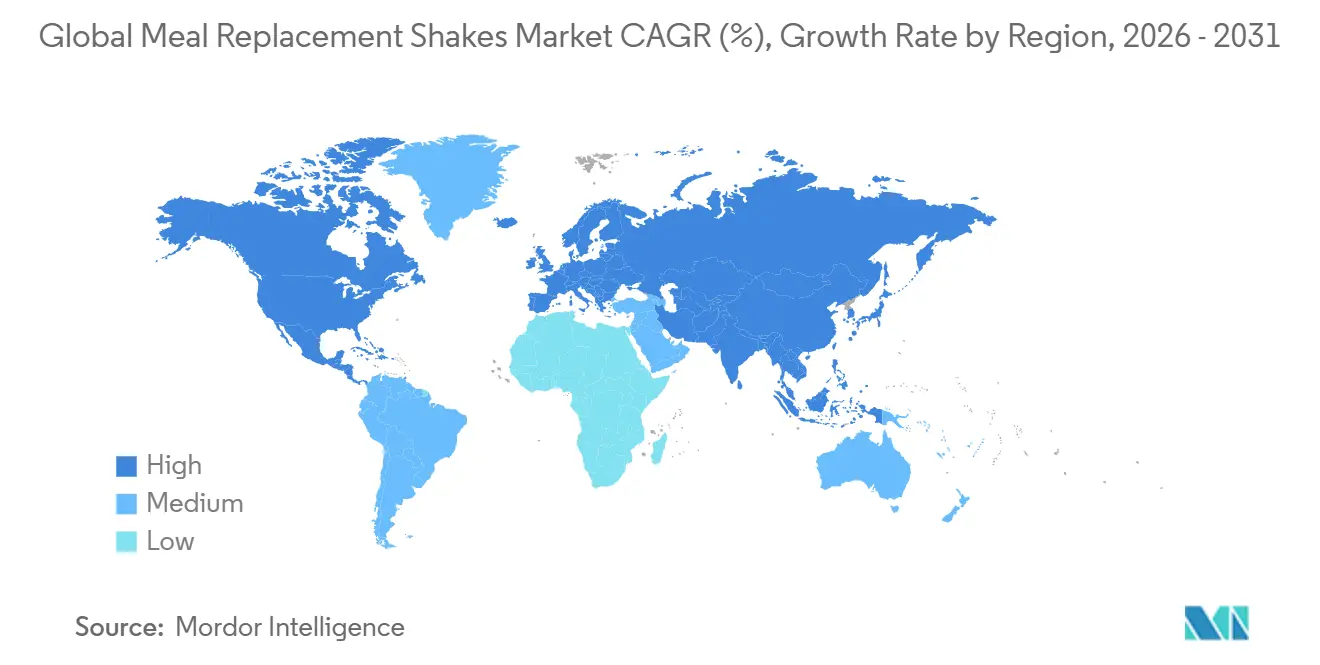

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meal Replacement Shakes Market Analysis by Mordor Intelligence

The meal replacement shakes market size is valued at USD 6.52 billion in 2026, growing from the 2025 value of USD 6.18 billion, and is forecast to climb to USD 9.65 billion by 2031, advancing at a 8.38% CAGR. Greater medical endorsement, stricter nutrient‐claim rules, and rapid formulation upgrades are moving the category beyond mere convenience toward clinically aligned nutrition solutions. Ready-to-drink (RTD) formats continue to dominate shelves, yet concentrates and syrups are expanding fastest as hospitals, schools, and nursing homes pivot to lower freight and packaging footprints. Pediatric malnutrition programs and geriatric sarcopenia management are widening the consumer base, while plant-based proteins and zero-sugar formulas unlock new premium niches. Distribution economics are also shifting; supermarkets still drive volume, but subscription-based direct-to-consumer (D2C) models are raising lifetime value through automated replenishment cycles.

Key Report Takeaways

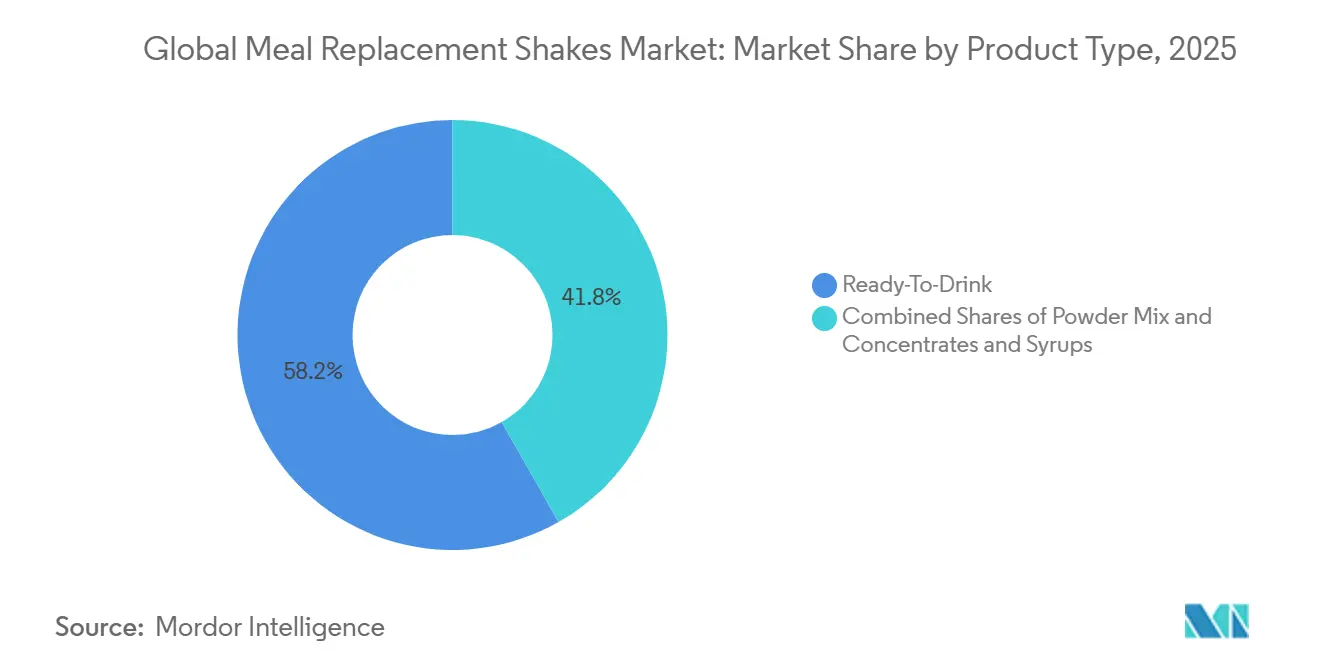

- By product type, ready-to-drink formats held 58.21% of the meal replacement shakes market share in 2025, while concentrates and syrups are forecast to register an 11.20% CAGR through 2031.

- By age group, adults accounted for 45.68% share of the meal replacement shakes market in 2025; the children segment is projected to grow at a 9.81% CAGR to 2031.

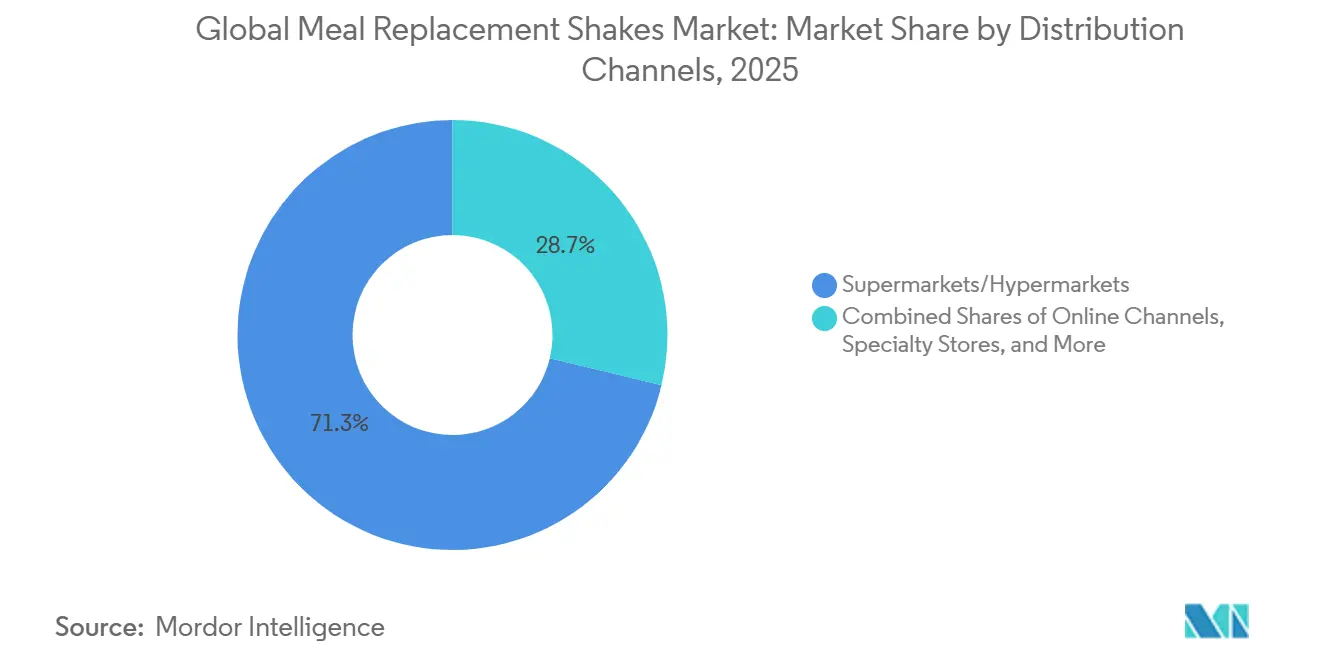

- By distribution channel, supermarkets and hypermarkets commanded 71.25% share of the meal replacement shakes market in 2025, whereas online retail and D2C are advancing at a 10.58% CAGR through 2031.

- By geography, North America contributed 48.25% of the revenue share to the meal replacement shakes market in 2025, and the Asia-Pacific region is forecast to expand at an 11.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meal Replacement Shakes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busy urban lifestyles drive need for quick, portable meal options | +1.8% | Global, with concentration in North America, Western Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rising Health Consciousness Boosts Preference for Nutrient-Dense Shakes | +1.5% | Global, particularly North America, Europe, and affluent Asia-Pacific markets | Medium term (2-4 years) |

| Product Innovation in Plant-Based, Low-Sugar, and Functional Variants | +2.1% | North America and Europe lead; Asia-Pacific adoption accelerating | Medium term (2-4 years) |

| Fitness Trends and Gym Culture | +1.3% | North America, Europe, and urban Asia-Pacific (China, India, South Korea) | Short term (≤ 2 years) |

| E-Commerce Expansion and Subscription Models | +1.4% | Global, with highest penetration in North America and Western Europe | Medium term (2-4 years) |

| Medical Endorsements for Weight Loss and Malnutrition Management | +1.7% | North America and Europe for weight management; Asia-Pacific, South America, and MEA for malnutrition | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Busy Urban Lifestyles Drive Need for Quick, Portable Meal Options

Urban professionals, constrained by time, are now reducing their meal durations to less than 10 minutes. This shift in behavior was emphasized in the USDA's 2024 Eating & Health Module, which found that 42% of employed adults skip at least one traditional sit-down meal during weekdays[1]Source: U.S. Food and Drug Administration, “FDA Issues Updated Definition of ‘Healthy’ Claim,” fda.gov. Consequently, liquid meal formats that require no preparation, utensils, or significant cleanup are gaining popularity. Ready-to-drink shakes have emerged as the preferred option for commuters, shift workers, and remote employees who often merge work and meals. This trend is especially evident in megacities such as Tokyo, Mumbai, and São Paulo, where average commute times exceed 60 minutes. In these cities, dense retail networks support impulse purchases at subway kiosks and convenience stores. Brands that secure strategic placements in high-traffic transit areas attract regular customers who value speed over taste. This dynamic explains the 30% to 40% price premium that single-serve RTD formats hold compared to per-serving costs of powder mixes.

Rising Health Consciousness Boosts Preference for Nutrient-Dense Shakes

In South Africa, a 2024 national health and nutrition survey found that 78% of consumers aim to lead healthier lifestyles, with 45% actively tracking their calorie consumption. This changing perspective has led consumers to view meal replacements as functional foods that provide essential micronutrients often missing from ultra-processed convenience meals, rather than just diet aids. Brands are adapting to this trend by highlighting ingredients such as bioavailable minerals like chelated magnesium and ferrous bisglycinate, prebiotic fibers like inulin and resistant starch, and omega-3 fatty acids such as algal DHA, distinguishing themselves from conventional protein powders. Abbott's Ensure, which achieved over USD 3 billion in global sales in 2024, reformulated its core product line to include 27 vitamins and minerals. This strategy targets consumers who see meal replacements as a way to address dietary gaps rather than as emergency food options. The medicalization of nutrition has elevated the category from being discretionary to essential, ensuring steady demand even during economic downturns.

Product Innovation in Plant-Based, Low-Sugar, and Functional Variants

From 2010 to 2023, Google Trends data highlighted a remarkable 3,355% increase in the adoption of plant-based proteins. This growth is primarily driven by the rising popularity of flexitarian diets, increased focus on allergen avoidance, and growing sustainability concerns, particularly among millennial and Gen Z consumers. Pea protein isolates have become strong competitors, equaling whey in digestibility and amino acid profiles. Additionally, faba bean and mung bean concentrates, with their neutral flavor profiles, are simplifying the formulation process. Addressing consumer concerns over the 15 to 20 grams of added sugars in traditional formulations, Beachbody launched Shakeology 0g Added Sugar in June 2024. This product, sweetened with monk fruit and stevia, delivers 130 to 140 kilocalories per serving. Ingredients previously limited to niche wellness brands, such as adaptogens (e.g., ashwagandha and rhodiola), nootropics (e.g., lion's mane and citicoline), and probiotics (e.g., Lactobacillus rhamnosus GG), are now entering mainstream products. This shift is blurring the distinction between meal replacements and dietary supplements. Consequently, regulatory agencies are under pressure to establish clearer labeling standards. For instance, the FDA's December 2024 update on the "healthy" claim explicitly excludes products with added sugars exceeding 2.5 grams per serving.

Medical Endorsements for Weight Loss and Malnutrition Management

Physicians are increasingly supporting meal replacements for weight management and diabetes remission, driven by growing clinical evidence. The Look AHEAD trial, which monitored participants over 8 years, revealed that intensive lifestyle interventions incorporating meal replacements resulted in sustained weight loss and reduced cardiovascular risks. Similarly, the DIRECT and DIADEM-I trials, which employed total diet replacement protocols, reported type 2 diabetes remission rates of 46% and 61%, respectively. These notable findings prompted the Brazilian Association for the Study of Obesity and Metabolic Syndrome (ABESO) to recommend meal replacements as a Class IIa, Level A intervention for structured low-calorie diets in their 2024 guidelines. In addressing malnutrition, the World Health Organization endorses ready-to-use therapeutic foods for severe acute malnutrition, a category closely associated with high-protein shakes, particularly in pediatric and geriatric care[2]Source: World Health Organization, “Guideline: Ready-to-Use Therapeutic Foods,” who.int. To meet the rising demand for PediaSure and Ensure, products frequently prescribed by physicians for growth challenges and age-related muscle loss, Abbott established new manufacturing facilities in Jhagadia, India; Tipp City, Ohio; and Jiaxing, China in 2025.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Scrutiny on Nutrition Claims and Sugar Content | -0.9% | Global, with strictest enforcement in North America and Europe | Short term (≤ 2 years) |

| Intense Competition From Bars, Soups, and Ready-to-Drink Alternatives | -0.7% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Lack of Satiety Compared to Solid Meals | -0.5% | Global | Medium term (2-4 years) |

| High Costs Compared to Whole Foods | -0.6% | Global, with greatest impact in price-sensitive emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny on Nutrition Claims and Sugar Content

In December 2024, the FDA finalized new criteria for the "healthy" claim, introducing limits on saturated fat, sodium, and added sugars. These updated standards disqualify many existing product formulations, requiring brands to either reformulate or discontinue front-of-package health messaging. Products with more than 2.5 grams of added sugars per serving are prohibited from carrying "healthy" claims, effectively excluding chocolate and vanilla flavors sweetened with cane sugar or high-fructose corn syrup. Additionally, in 2024, the Food and Drug Administration proposed front-of-package nutrition labeling rules. These rules would require clear disclosure of saturated fat, sodium, and added sugar content. While this enhances transparency, it also exposes formulation weaknesses that competitors could exploit through comparative advertising. In the European Union, Regulation 609/2013 imposes strict requirements for meal replacements targeting weight control. These products must provide 200 to 400 kilocalories, at least 25% of the daily recommended intake for vitamins and minerals, and a minimum of 25 grams of protein. These standards create a compliance barrier that smaller brands often struggle to overcome. In Brazil, ANVISA's RDC 243/2018 regulation classifies dietary supplements as "Suplemento Alimentar." This regulation restricts ingredient lists to those outlined in IN 28/2018 and IN 29/2018. Additionally, the registration process, which takes 12 to 18 months, presents a significant challenge for new entrants to the market.

Intense Competition from Bars, Soups, and Ready-to-Drink Alternatives

From 2013 to 2024, protein bars experienced a fourfold rise in high-protein claims, according to Mintel. These bars now compete directly with shakes, catering to health-conscious consumers seeking convenience. Bars offer better portability, as they do not require refrigeration and eliminate the risk of spillage. Their solid form also enhances satiety by promoting stronger gastric distension and slower gastric emptying compared to liquids. Introduced in fall 2024, the David Bar delivers 28 grams of protein, 150 kilocalories, and zero sugar. This product represents the next generation of bar formulations, matching or surpassing the macronutrient profiles of shakes without the need for shaker bottles or blenders. Brands like Huel and Soylent are redefining categories with ready-to-eat meal kits, soups, and refrigerated bowls. These products incorporate whole-food ingredients and offer textural variety, addressing limitations associated with liquid shakes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentrates Capture Cost-Focused Demand

Concentrates and syrups are projected to grow at an impressive 11.20% CAGR, surpassing the overall growth rate of the meal replacement shakes market. This format is particularly favored by hospitals and schools due to its cost-efficiency; one liter can yield up to 15 servings, significantly reducing freight and packaging expenses by nearly 70% compared to ready-to-drink (RTD) options. On the other hand, RTD products, known for their convenience, are expected to maintain a dominant position, capturing a notable 58.21% revenue share in 2025. Powder mixes occupy a middle ground between concentrates and RTD products, but their multi-step preparation process can deter consumers seeking quick and mobile solutions. Advances in microencapsulation technology are enhancing the shelf life of powders, while flavor-focused product launches, such as those by Huel, are proving that powders can offer a variety comparable to RTD options.

The concentrates segment is also gaining traction due to its alignment with environmental mandates, as it uses less plastic compared to other formats. However, certain challenges persist, including high viscosity, which limits protein loading, and the risk of flavor dilution errors, which can negatively impact consumer acceptance. To address these challenges, RTD products are evolving by introducing plant-based and zero-sugar variants. These innovations aim to narrow the gap between cost and performance while ensuring a competitive shelf presence in the market.

By Age Group: Pediatric Shakes Outpace the Core Adult Base

Propelled by the increasing medicalization of growth supplementation, the children segment is projected to expand at a robust 9.81% CAGR through 2031. The growing success of PediaSure in India highlights the rising trend of physicians prescribing nutritional products to address feeding difficulties in children. This shift reflects a broader acceptance of medical-grade nutritional solutions for pediatric care. In contrast, the adult cohort, which is expected to account for a 45.68% market share in 2025, is showing signs of market saturation. However, companies like Herbalife continue to maintain their foothold in this segment by utilizing a multi-level marketing model that emphasizes personalized coaching to engage consumers effectively.

Meanwhile, the senior demographic exhibits the highest per-capita consumption of nutritional products, driven by increasing protein requirements of 1.0-1.2 g/kg body weight, as recommended by geriatric dietary guidelines. Healthcare reimbursement policies and insurance coverage are increasingly influencing market dynamics, shifting the focus toward pediatric and senior nutritional formulas. These specialized formulas not only command premium price points but also demonstrate lower promotional elasticity compared to mainstream adult stock-keeping units (SKUs). This trend underscores the growing demand for targeted nutritional solutions that cater to specific age groups and health needs.

By Distribution Channel: Online Retail Captures Subscription Economics

Online retail and D2C are expected to grow at a robust 10.58% CAGR, fueled by advancements in automated replenishment systems and the advantage of lower channel fees. Brands such as Soylent and Huel are leveraging subscription models by offering discounts ranging from 12% to 25%, which has successfully increased purchase frequency from two to four orders annually. Additionally, the integration of social commerce features on platforms like TikTok and Instagram is transforming influencer engagement into seamless and expedited checkout experiences, particularly appealing to Gen Z consumers who prioritize convenience and digital interaction.

Supermarkets and hypermarkets continue to dominate with a substantial 71.25% market share, primarily due to their ability to attract high foot traffic. However, the imposition of slotting fees and markdown guarantees is exerting pressure on brand margins, making profitability a challenge. Convenience and drug stores remain essential for fulfilling top-up purchase needs, as demonstrated by Premier Protein’s widespread availability in CVS and 7-Eleven outlets. Meanwhile, specialty nutrition stores are carving out a niche by offering expert advice, which significantly enhances conversion rates for clinically targeted products such as Ensure and Boost, catering to consumers seeking tailored nutritional solutions.

Geography Analysis

North America generated 48.25% of the meal replacement shakes market revenue in 2025, supported by insurance reimbursement for medical nutrition and diversified retail coverage. High obesity prevalence and physician acceptance of meal replacements sustain consumer interest. The FDA’s 2024 nutrient-claim tightening will impose reformulation expense through 2027, particularly for sugar-heavy flavors. Consolidation persists as illustrated by Hormel’s 2024 Muscle Milk acquisition, which strengthens its high-protein beverage portfolio.

Asia-Pacific is the fastest-growing region with an 11.28% CAGR to 2031. Urbanization, higher disposable income, and streamlined import regulations allow multinationals to localize formulas across India, China, and Southeast Asia. Abbott expanded manufacturing in Jhagadia and Jiaxing during 2025 to meet pediatric and geriatric demand. China’s population aged over 60 is on track to hit 400 million by 2035, underpinning sustained volume growth for high-protein shakes.

Europe enforces EU Regulation 609/2013, creating high compliance costs that favor established players[3]Source: EUR-Lex, “Regulation (EU) No 609/2013,” eur-lex.europa.eu. Germany leads per-capita consumption owing to strong pharmacy channels, whereas France’s Nutri-Score grading penalizes high-sugar SKUs. South America faces currency volatility, with Brazil’s real depreciation raising whey input costs and testing price elasticity. ANVISA’s restrictive ingredient lists further slow new entry. The Middle East and Africa present long-run potential as governments tackle obesity and malnutrition, evidenced by South Africa’s 6.3% annual growth in weight-management products.

Competitive Landscape

The meal replacement shakes market, with a moderate concentration, highlights the dominance of a few key multinationals: Abbott, Nestlé, Glanbia, Herbalife, and Danone. Abbott’s Ensure achieved a significant milestone in 2024, surpassing USD 3 billion in revenue. This success was driven by its strong clinical validation and strategic positioning within reimbursement frameworks. Similarly, Herbalife demonstrated its ability to adapt to emerging trends with the February 2024 launch of its GLP-1 Nutrition Companion, showcasing how established players are aligning with drug-adjacent innovations to maintain relevance and capture new opportunities.

Digitally native challengers are leveraging advanced data integration to disrupt the market. Brands such as AG1 and Huel have integrated their offerings with fitness-tracking applications, enabling them to deliver personalized subscription bundles. This approach not only enhances customer lifetime value but also eliminates the need for slotting fees, providing a competitive edge. Additionally, smaller brands are capitalizing on attributes like plant-based formulations and zero-sugar options to carve out distinct niches, effectively bypassing the portfolios of larger incumbents. Mergers and acquisitions remain a critical growth strategy in this market. For example, Nestlé’s phased acquisition of Orgain strengthens its plant-based product portfolio, while Glanbia’s introduction of a SlimFast plant-based variant aligns with the growing flexitarian consumer trend, further diversifying its offerings.

Regulatory compliance continues to shape the competitive landscape, creating both challenges and opportunities. Companies that proactively invest in sugar reduction initiatives and adopt clean labeling practices are better positioned to defend their product claims and maintain shelf visibility. This is particularly crucial as global nutrient-profile labeling regulations become increasingly stringent, compelling market players to adapt and innovate to meet evolving standards.

Meal Replacement Shakes Industry Leaders

Abbott Laboratories

Nestlé S.A.

Glanbia PLC

Amway Corp.

Herbalife Nutrition

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Synutra International launched Xianfeng meal replacement drinks, leveraging its milk protein expertise amid the government's three-year weight control plan. The formulation includes milk protein concentrates for satiety, MCTs, 10 vitamins, four minerals, and maltodextrin fiber, designed as complete meal substitutes rather than low-carb powders.

- June 2025: Sur Nutrition launched its certified-organic, plant-based Organic Meal Replacement Shake, targeting athletes and wellness enthusiasts. Developed by an in-house certified research chef, the chocolate-flavored shake features North American PURIS pea protein for muscle recovery.

- September 2024: Arla Foods debuted Protein Food to Go, a line of milk-based meal replacement drinks in Denmark. Available in chocolate caramel and vanilla hazelnut flavors, each serving provides 30g of protein, 12g of fiber, vitamins, and minerals for complete nutrition on the go.

- August 2024: Drink Wholesome launched vegan meal replacement powders from Gilford, NH, expanding from egg white variants to serve consumers with chronic digestive issues using a blend of almonds, oats, coconut, black walnuts, and monk fruit.

Global Meal Replacement Shakes Market Report Scope

A meal replacement product is a beverage, bar, soup, etc. with a set amount of calories and nutrients that is meant to replace a solid meal. The global meal replacement shakes market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into ready-to-drink products and powdered products. By distribution channel, the market studied is segmented into convenience stores, hypermarkets/supermarkets, specialty stores, online retail stores, and other distribution channels. The study also covers the global level analysis of the major regions, such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Powder Mix |

| Ready-to-Drink (RTD) |

| Concentrates and Syrups |

| Children (≤12 yrs) |

| Adults (18-64 yrs) |

| Seniors (65+) |

| Supermarkets and Hypermarkets |

| Convenience and Drug Stores |

| Online Retail and D2C |

| Specialty Nutrition Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Powder Mix | |

| Ready-to-Drink (RTD) | ||

| Concentrates and Syrups | ||

| By Age Group | Children (≤12 yrs) | |

| Adults (18-64 yrs) | ||

| Seniors (65+) | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience and Drug Stores | ||

| Online Retail and D2C | ||

| Specialty Nutrition Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the meal replacement shakes market?

The meal replacement shakes market size is USD 6.52 billion in 2026.

How fast is the category expected to grow through 2031?

Revenue is projected to advance at an 8.38% CAGR, reaching USD 9.65 billion by 2031.

Which product format leads sales today?

Ready-to-drink shakes hold the largest share at 58.21% of 2025 revenue.

Which region is expanding the fastest?

Asia-Pacific is forecast to post an 11.28% CAGR through 2031 due to urbanization and rising disposable income.

Page last updated on: