Manufacturing Execution Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

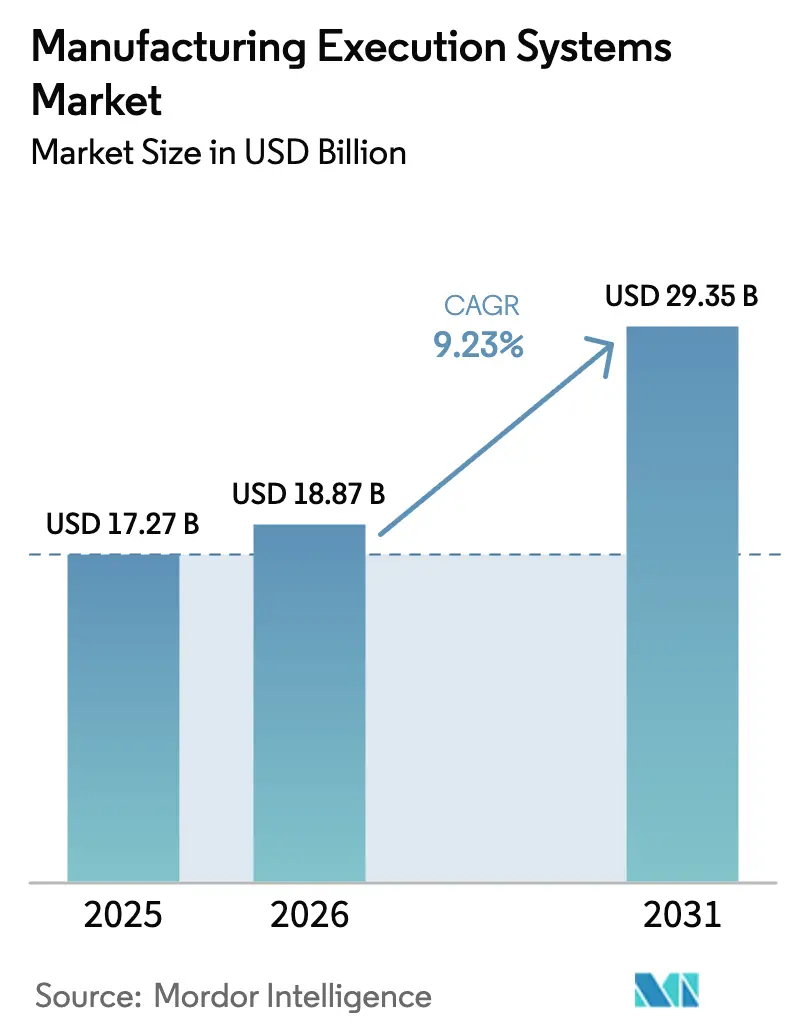

| Market Size (2026) | USD 18.87 Billion |

| Market Size (2031) | USD 29.35 Billion |

| Growth Rate (2026 - 2031) | 9.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manufacturing Execution Systems Market Analysis by Mordor Intelligence

The Manufacturing Execution Systems Market size is expected to grow from USD 17.27 billion in 2025 to USD 18.87 billion in 2026 and is forecast to reach USD 29.35 billion by 2031 at 9.23% CAGR over 2026-2031. This trajectory is anchored by sovereign industrial policies such as the United States’ USD 52.7 billion CHIPS and Science Act and India’s USD 30 billion Production Linked Incentive schemes, both of which convert policy intent into capital-equipment orders that require real-time production orchestration. Enterprises are also racing to satisfy traceability mandates tied to pharmaceutical serialization, electric-vehicle battery passports, and food-safety protocols, further stimulating the manufacturing execution systems (MES) market. Low-code platforms and subscription pricing models are lowering adoption barriers for smaller factories, while cybersecurity certifications like IEC 62443 are shaping vendor short-lists. On the technology front, edge-native architectures that synchronize with cloud analytics are emerging as the default choice for plants seeking latency control without forfeiting remote visibility.

Key Report Takeaways

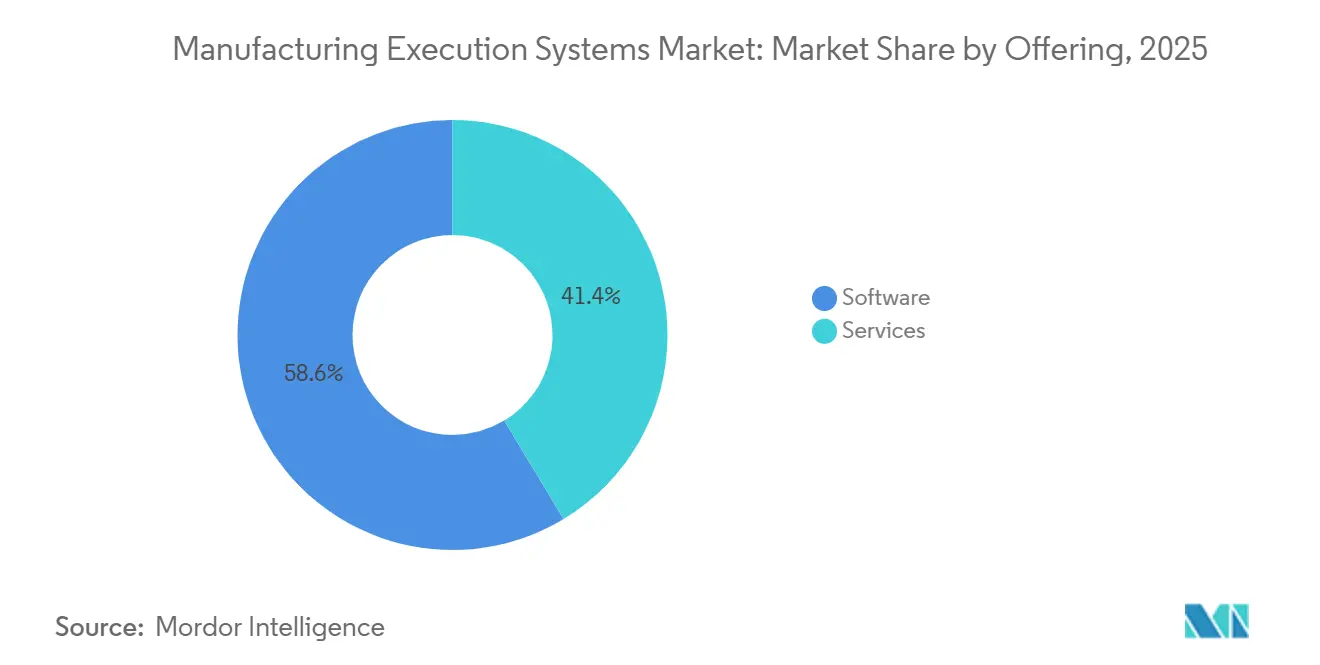

- By offering axis, software captured 58.64% of 2025 revenue, whereas services are projected to expand at an 11.78% CAGR through 2031.

- By deployment modes, on-premise installations commanded 62.46% of 2025 spending, while cloud solutions are advancing at a 10.12% CAGR.

- By end-user industries, automotive led with 27.68% revenue share in 2025, but pharmaceutical and life sciences are forecast to grow at a 10.78% CAGR.

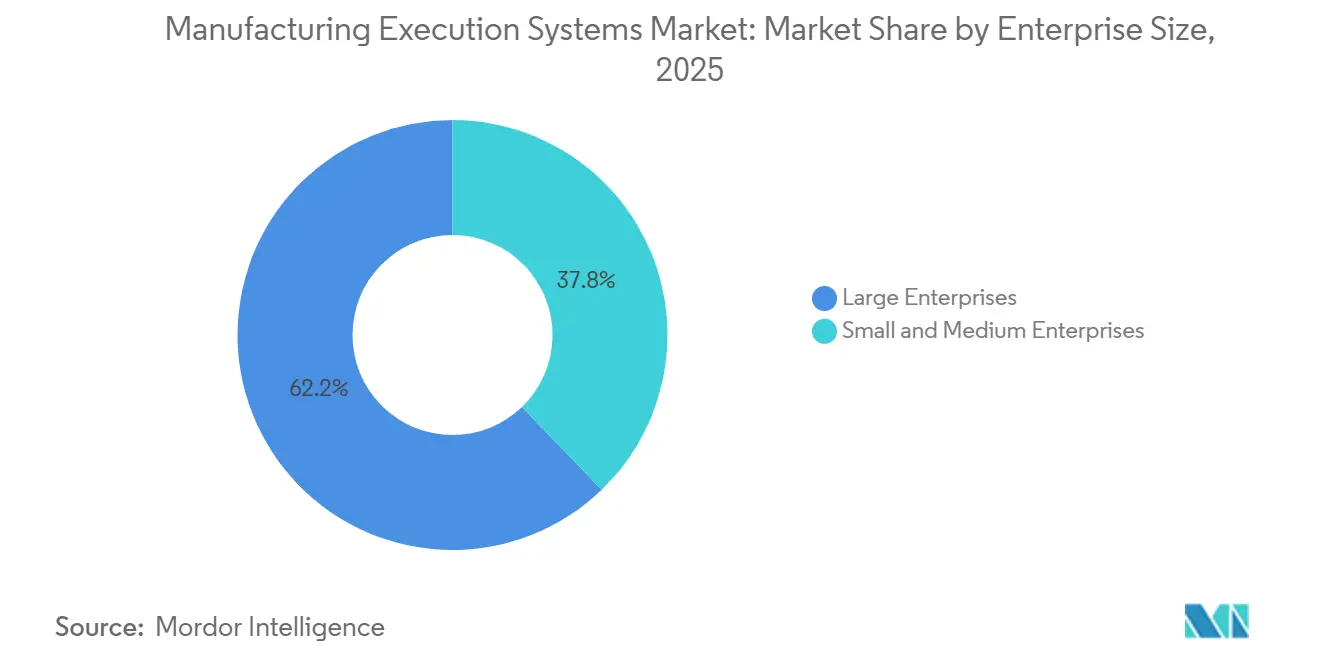

- By enterprise size, large companies held 62.22% of 2025 revenue, yet small and medium enterprises are pacing at a 12.46% CAGR.

- By process type, discrete manufacturing accounted for 50.76% of 2025 spending, whereas hybrid environments are expanding at a 10.49% CAGR.

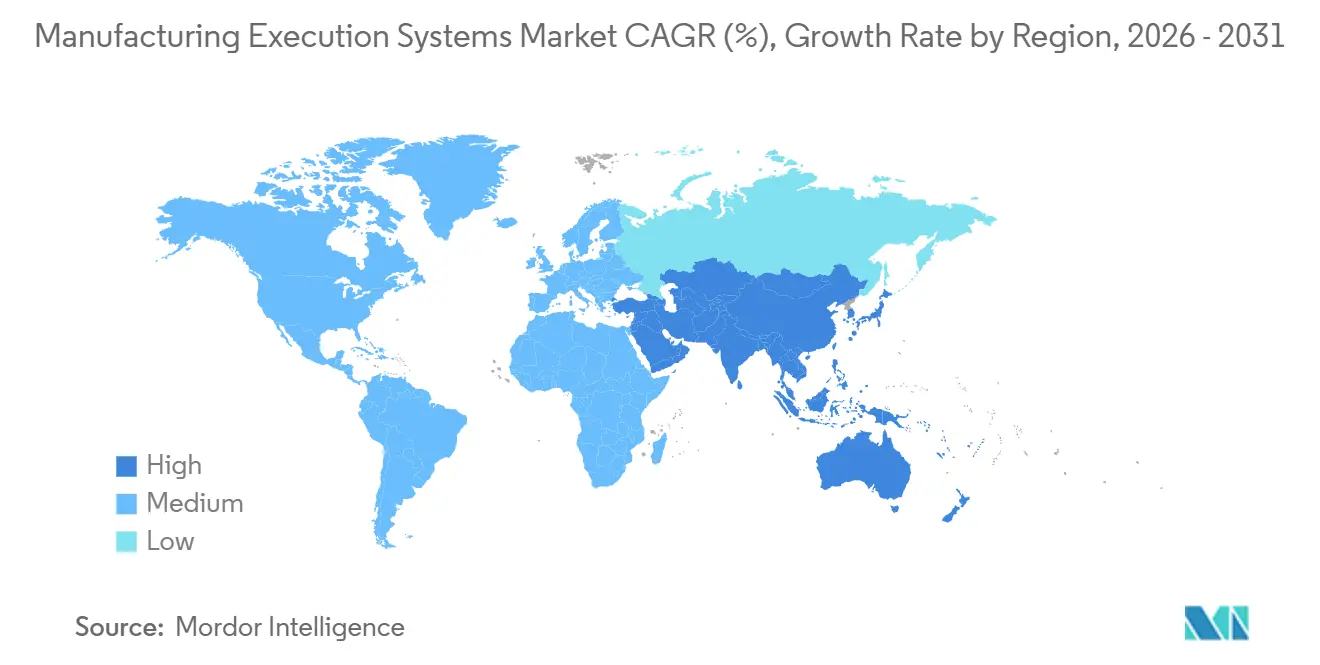

- By geography, North America controlled 36.74% of 2025 value, but Asia Pacific is on track for an 11.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Manufacturing Execution Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 and Smart-Factory Roll-outs | +2.1% | Germany, United States, China, Japan | Medium term (2-4 years) |

| Need for Real-Time Production Visibility | +1.8% | North America and Europe automotive and semiconductor clusters | Short term (≤ 2 years) |

| Compliance-Driven Digital Traceability | +1.6% | North America and Europe pharma, Europe automotive battery, Global F&B | Medium term (2-4 years) |

| SaaS Pricing Lowers CapEx Barriers | +1.3% | Asia Pacific and South America SMEs | Short term (≤ 2 years) |

| Rise of Low-Code Composable MES | +1.0% | North America and Europe SME hubs | Medium term (2-4 years) |

| OEE-as-a-Service Linked to IIoT Analytics | +0.9% | Global discrete manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 And Smart-Factory Roll-outs

National manufacturing agendas continue to de-risk digital-twin investments. In the United States, the Department of Energy’s Smart Manufacturing Innovation Institute funded live production trials in 2025 that cut energy intensity by double-digit percentages.[1]U.S. Department of Energy, “Smart Manufacturing Innovation Institute Awards,” energy.gov Germany’s Manufacturing-X framework requires interoperable asset-administration shells, ensuring that each connected machine can publish status without revealing proprietary know-how. Ireland earmarked grants for pharmaceutical clusters in Cork and Limerick, prompting contract manufacturers to swap spreadsheets for modular execution platforms. The United Kingdom tied innovation vouchers to verifiable scrap-rate reductions, prompting mid-tier suppliers to adopt platform-agnostic data models. Collectively, these initiatives convert abstract policy into direct demand for the manufacturing execution systems (MES) market.

Need For Real-Time Production Visibility

Supply-chain disruptions in 2024 exposed the cost of delayed shop-floor data. Automotive OEMs now require hourly electronic data interchange from tier-1 suppliers, an expectation that paper logs cannot meet. Semiconductor fabs deploy edge gateways that stream metrology readings to advanced process-control algorithms, shrinking excursion detection windows from hours to seconds. By 2025, sensor costs fell below USD 5 per node, enabling high-mix job shops to justify continuous monitoring. Energy-management layers now link machine utilization with time-of-use tariffs, carving 15%-20% off peak charges in regions with interval metering. As a result, live dashboards are becoming table stakes rather than differentiators in the manufacturing execution systems market.

Compliance-Driven Digital Traceability

Regulators are codifying electronic audit trails. The U.S. Food and Drug Administration’s 21 CFR Part 11 demands tamper-evident logs and versioned recipes. The Drug Supply Chain Security Act phases culminated in 2024, compelling unique identifiers down to the unit level. Europe’s Battery Regulation introduced mandatory digital product passports in 2024, forcing electric-vehicle cell makers to reveal chemistry, carbon footprint, and recycled content. Beginning January 2026, the Food Safety Modernization Act obliges food processors to furnish lot genealogy within 24 hours of recall notice. Such statutes directly expand the addressable manufacturing execution systems market size, because manual or legacy tools cannot satisfy serialized, time-stamped data requirements.

SaaS Pricing Lowers CapEx Barriers

Monthly subscription tiers from vendors such as Plex and AVEVA start below USD 100 per user, eliminating the USD 500,000–USD 2 million up-front licenses typical of on-premise suites. Tier-2 suppliers in Mexico and Southeast Asia now deploy core work-order and quality modules in 8-12 weeks, riding multi-tenant architectures maintained by the vendor. Automatic version upgrades deliver machine-learning anomaly detection without renegotiating contracts, tightening capability gaps between small shops and multinational peers. As a result, the manufacturing execution systems market is broadening beyond traditional capital-rich buyers.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-Front Integration Cost With Legacy OT and ERP | -1.4% | North America and Europe brownfield plants | Short term (≤ 2 years) |

| Cyber-Security Risks In Cloud-Connected Plants | -1.1% | Pharmaceutical and defense sectors worldwide | Medium term (2-4 years) |

| OT and IT Skill-Gap Stalling Roll-outs | -0.8% | North America and Europe | Long term (≥ 4 years) |

| IP-Exposure Fears Among Contract Manufacturers | -0.6% | Asia Pacific CMO hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-Front Integration Cost With Legacy OT And ERP

Brownfield facilities often rely on proprietary fieldbus networks such as Modbus or Profibus that predate modern APIs. Bridging these islands requires protocol gateways and custom scripts, inflating project budgets by 40%-60% according to a 2025 MESA survey.[2]Manufacturing Enterprise Solutions Association, “2025 Integration Cost Survey,” mesa.org Pharmaceutical sites add validation overhead, where every change triggers installation, operational, and performance qualifications that consume months and hundreds of thousands of dollars. Such integration burdens can exhaust the first year of ROI models, delaying board approval for incremental modules and tempering growth in the manufacturing execution systems (MES) market.

Cyber-Security Risks In Cloud-Connected Plants

In 2025, the U.S. Cybersecurity and Infrastructure Security Agency issued 14 advisories covering Siemens, Schneider Electric, Rockwell, and ABB vulnerabilities that enabled remote code execution.[3]U.S. Cybersecurity and Infrastructure Security Agency, “ICS Advisories 2025,” cisa.gov Cloud misconfigurations compound the problem, potentially leaking production schedules or proprietary formulations. Fewer than 30% of installed systems meet IEC 62443’s zone-and-conduit segmentation rules. Defense and aerospace primes, bound by ITAR and CMMC, frequently default to air-gapped networks, sacrificing cloud analytics for risk containment. This trust deficit restrains full-scale adoption despite functional advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Capture Momentum In A Complex Landscape

Services revenue is set to outpace software through 2031 as manufacturers outsource integration, validation, and analytics. In 2025, software generated 58.64% of topline demand, yet the growing complexity of multi-plant roll-outs is unlocking double-digit expansion for managed services. Validation-as-a-service bundles shorten pharmaceutical qualification phases from nine months to twelve weeks, illustrating why professional support is eclipsing license fees in the manufacturing execution systems (MES) market size. Remote monitoring packages embedding predictive maintenance and changeover optimization are especially popular among automotive tiers that lack in-house data scientists.

Managed services also act as a talent bridge. Scarcity of ISA-95 architects and cloud-native DevOps engineers prompts factories to contract outcome-based agreements. Vendors assume responsibility for uptime, patching, and upgrades, effectively converting capital purchases into opex lines. This realignment aligns corporate cash-flow preferences with continuous improvement cycles, bolstering the manufacturing execution systems market.

By Deployment Mode: Cloud Gains Despite Validation Inertia

On-premise systems held a 62.46% manufacturing execution systems market share in 2025 due to stringent pharma and semiconductor validation rules. Cloud platforms, however, are growing 10.12% annually as SMEs and contract manufacturers favor rapid configuration over server ownership. Edge-native hybrids satisfy latency and data-sovereignty concerns by performing time-critical loops locally while syncing aggregated metrics to cloud dashboards. The CHIPS and Science Act now ties funding to digital-twin yield dashboards accessible to distributed teams, catalyzing cloud adoption in new U.S. fabs.

Cybersecurity remains the chief hurdle. IEC 62443 certification for cloud services trails on-premise norms, and pharma CMOs negotiate data-residency clauses to lock server locations. Even so, Europe’s Digital Product Passport and similar regulations require secure APIs that cloud infrastructure delivers more cost-effectively than on-premise portals. As regulatory glue hardens, the deployment mix within the manufacturing execution systems market is tilting toward hybrid-cloud.

By End-User Industry: Pharma Compliance Drives Fastest Upside

Automotive contributed 27.68% of 2025 revenue, propelled by battery-cell traceability and multi-tier synchrony. Yet pharmaceutical and life-sciences customers exhibit the fastest expansion at 10.78% through 2031, buoyed by serialization laws and continuous-manufacturing adoption. Cell-and-gene therapy plants demand batch genealogy with patient-level precision, a capability only execution systems can deliver at scale. Electronics makers invest heavily to correlate nanoscale process parameters with defect densities, further enlarging the manufacturing execution systems market size.

Food and beverage processors are late but fast movers because the Food Safety Modernization Act now compels lot-level tracking within 24 hours of recall. Continuous process industries like oil and gas deploy historian-centric modules for energy intensity reduction rather than discrete work-order control. Aerospace and defense emphasize configuration management to maintain part pedigree, underscoring vertical nuances in adoption patterns.

By Enterprise Size: SMEs Close The Digital Divide

Large corporations garnered 62.22% of 2025 demand, but SMEs are growing at a 12.46% clip, outpacing their bigger peers by 3.23 percentage points. Subscription models under USD 100 per user per month transform prohibitively large capital projects into manageable opex lines, swelling the addressable manufacturing execution systems market. Low-code environments empower production supervisors to craft dashboards and alerts without writing code, removing systems-integrator bottlenecks.

Policy catalysts amplify this trend. India’s Production Linked Incentive schemes link subsidy eligibility to digitization milestones, pushing tier-2 electronics suppliers in Ahmedabad and Coimbatore to adopt cloud MES rapidly. Mexico’s nearshoring wave is generating a greenfield SME base in the Bajío, each seeking IATF 16949 compliance within tight timelines incompatible with legacy implementations. Together, these forces democratize access across enterprise sizes.

By Process Type: Hybrid Architectures Proliferate

Discrete operations held 50.76% of spending in 2025, with automotive assembly and SMT lines dominating. Hybrid processes are recording a 10.49% CAGR as modular bioreactors and continuous small-molecule reactors reshape pharmaceutical production. The U.S. FDA’s 2024 guidance elevated continuous manufacturing from pilot to mainstream, prompting retrofits that raise software spend per line. Hybrid food plants mixing extrusion and batch packaging add further momentum to the manufacturing execution systems (MES) market.

Modular process units need execution layers that can switch between campaign and continuous modes without losing genealogy or cleaning validation records. Vendors now offer microservice toolkits to handle these context switches in real time. This functional agility differentiates suppliers and drives new license and service revenue, particularly in life sciences and specialty chemicals.

Geography Analysis

North America’s leadership stems from USD 52.7 billion in semiconductor incentives and a robust pharmaceutical base. Intel’s Ohio and Arizona fabs and TSMC’s Phoenix site embed digital-twin yield dashboards, anchoring execution budgets. Pharmaceutical hubs in New Jersey and Puerto Rico retrofit batch suites with continuous reactors to satisfy FDA serialization and process-verification rules. Canada’s Ontario auto corridor now integrates battery-pack traceability as EV volumes scale, while Mexico’s Bajío SMEs deploy cloud suites to meet IATF 16949 audits rapidly.

Asia Pacific’s 11.94% forecast CAGR reflects policy and supply-chain shifts. China’s Ministry of Industry and Information Technology backs industrial-internet pilots that graduate into full-scale deployments. India’s subsidies hinge on proof of digitization, driving adoption among electronics and pharma SMEs. Southeast Asia absorbs electronics and automotive lines relocating from single-source geographies, and each OEM mandates execution-system compliance as supplier entry criteria. Japan focuses on predictive maintenance to counteract labor shortages, while Australia and New Zealand embed traceability to protect food-export brands.

Europe advances under the weight of regulation. Germany retrofits battery-cell lines to meet digital passport rules. United Kingdom pharma centers fund continuous-manufacturing pilots to offset Brexit-related cost pressures. France’s defense plants favor on-premise, air-gapped deployments for ITAR compliance. Italy’s PDO food processors use execution layers to authenticate provenance, and Spain’s tier-1 automotive suppliers adopt cloud platforms to synchronize cross-border plants. Russia’s refinery optimizations rely on historian integrations, even as sanctions curb Western licenses.

Competitive Landscape

The ten largest vendors hold roughly 55% of global revenue, placing overall concentration in the mid-range. Siemens, Rockwell Automation, Schneider Electric, ABB, and Honeywell exploit their controller footprints to bundle edge-native execution software, simplifying integration for brownfield customers. Enterprise software majors SAP, Oracle, and Dassault Systèmes pitch execution as the operational spine inside broader supply-chain suites, a message that resonates with CIOs tasked with harmonizing ERP and MES layers.

Specialists maintain pricing power by embedding regulatory templates. Emerson’s Syncade dominates pharmaceutical batch records, while Applied Materials automates semiconductor fabs with sub-micron placement constraints. Low-code insurgents Critical Manufacturing and iBASEt court aerospace and semiconductor niches with microservice portfolios, reducing implementation cycles from 18 months to under 12 weeks. Edge-AI modules offering predictive maintenance and dynamic scheduling constitute the next battleground, evidenced by the U.S. Patent Office’s 200-plus 2025 filings on digital-twin synchronization. Cybersecurity posture is now co-equal with functional depth, and IEC 62443 certification appears on nearly every request for proposal.

Manufacturing Execution Systems Industry Leaders

Siemens AG

Rockwell Automation Inc.

SAP SE

ABB Ltd.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Siemens introduced an Opcenter generative-AI scheduler that converts natural-language requests into optimized sequences, cutting planner workload by 30%.

- September 2025: Rockwell Automation launched FactoryTalk Hub, consolidating PLC telemetry, historian data, and ERP transactions into a unified cloud lake for multi-site analytics.

- August 2025: : Honeywell and Microsoft embedded Forge analytics inside Azure IoT Edge, enabling latency-sensitive predictive models for refining and chemicals plants.

- July 2025: SAP and Siemens integrated Digital Manufacturing Cloud with Xcelerator for automated quality-loop closures in continuous pharmaceutical runs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global manufacturing execution systems (MES) market as the total yearly software and allied service revenues earned from standalone platforms that bridge enterprise resource planning and shop-floor automation, recording, guiding, and optimizing every production step across discrete, process, and hybrid plants worldwide. According to Mordor Intelligence, this market is expected to generate USD 17.19 billion in 2025.

We exclude embedded production-management modules bundled solely inside programmable logic controllers or CNC tools without a separate MES license.

Segmentation Overview

- By Offering

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud

- Edge-Based

- By End-User Industry

- Food and Beverage

- Oil and Gas

- Pharmaceutical and Life Sciences

- Automotive

- Electronics and Semiconductor

- Chemicals

- Metals and Mining

- Pulp and Paper

- Aerospace and Defense

- Other End-User Industries

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Process Type

- Discrete Manufacturing

- Process Manufacturing

- Hybrid

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with MES architects, plant digitalization heads, regional integrators, and trade-body experts across North America, Europe, and Asia Pacific help us verify average selling prices, deployment-mix changes, and short-term upgrade pipelines that secondary sources alone cannot surface.

Desk Research

We begin with open sources such as the US Bureau of Labor Statistics, Eurostat PRODCOM, UN Comtrade (HS 847950), and the International Society of Automation for adoption ratios. Company 10-Ks, investor decks, and trade journals clarify pricing, while paid dashboards, including D&B Hoovers, Dow Jones Factiva, and Questel, supply company financials and patent cues. These materials anchor historical baselines; many additional references were used beyond those named.

Market-Sizing & Forecasting

We launch with a top-down reconstruction that scales national manufacturing value-add by MES penetration rates gathered from our interviews, followed by sampled ASP times active-license roll-ups to cross-check totals. Core variables include new smart-factory capex, average license price, cloud share of fresh installs, automotive output index, and discrete-plant digital maturity scores. A multivariate regression projects each driver through 2030, and scenario analysis captures high and low investment paths when data gaps appear.

Data Validation & Update Cycle

Outputs undergo variance checks against quarterly vendor bookings, capital-goods orders, and customs statistics. A second analyst reviews anomalies before sign-off. Reports refresh annually, with interim updates after material events, and a last review happens just before delivery so clients receive the latest outlook.

Credibility Anchored in the Manufacturing Execution System Reality

Published MES estimates often diverge because each firm chooses different scope elements, pricing assumptions, and refresh cadences.

Key Gap Drivers

1. Several publishers drop service revenues, pushing figures below our view.

2. Others roll forward older exchange rates or static ASPs, inflating totals.

3. Some assume rapid cloud displacement, which our field checks show is still emerging in heavy industries.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.19 B (2025) | Mordor Intelligence | - |

| USD 16.18 B (2024) | Global Consultancy A | Excludes integration and support services |

| USD 15.95 B (2025) | Global Consultancy B | Counts only on-premise deployments; uses fixed 2022 FX rates |

| USD 16.57 B (2025) | Industry Publisher C | Applies aggressive cloud uptake curve not yet visible in plant surveys |

By aligning scope tightly to active MES licenses, validating prices directly with buyers, and refreshing numbers each year, Mordor Intelligence provides a balanced, transparent baseline that decision-makers can repeat and trust.

Key Questions Answered in the Report

What CAGR is projected for the manufacturing execution systems (MES) market from 2026 to 2031?

The market is forecast to grow at 9.23% annually, increasing from USD 18.87 billion in 2026 to USD 29.35 billion in 2031.

Which deployment mode is expanding fastest?

Cloud-based solutions are advancing at a 10.12% CAGR as subscription pricing and rapid configuration attract SMEs and greenfield sites.

Why are life-science firms accelerating MES investment?

Regulatory pressures for electronic batch records and continuous manufacturing workflows push life-science plants toward advanced MES platforms to secure compliance and real-time release.

Why are pharmaceutical manufacturers investing heavily in execution systems?

MES platforms support compliance by enabling electronic batch records, audit trails, controlled recipes, and real-time genealogy to meet serialization requirements, continuous-manufacturing expectations, and Annex 1 contamination-control workflows.

How do low-code platforms affect adoption among small factories?

Low-code tools let supervisors create workflows without writing code, slashing implementation cycles and reducing reliance on external integrators.

What is the main cybersecurity standard influencing procurement?

IEC 62443, which specifies zone segmentation and role-based access controls, is now a de facto requirement in most industrial RFPs.

Which region offers the highest growth opportunity?

Asia Pacific is projected to lead with an 11.94% CAGR, driven by policy incentives in China and India and supply-chain diversification into Southeast Asia.

Page last updated on: