Market Overview

| Study Period | 2020 - 2030 |

|---|---|

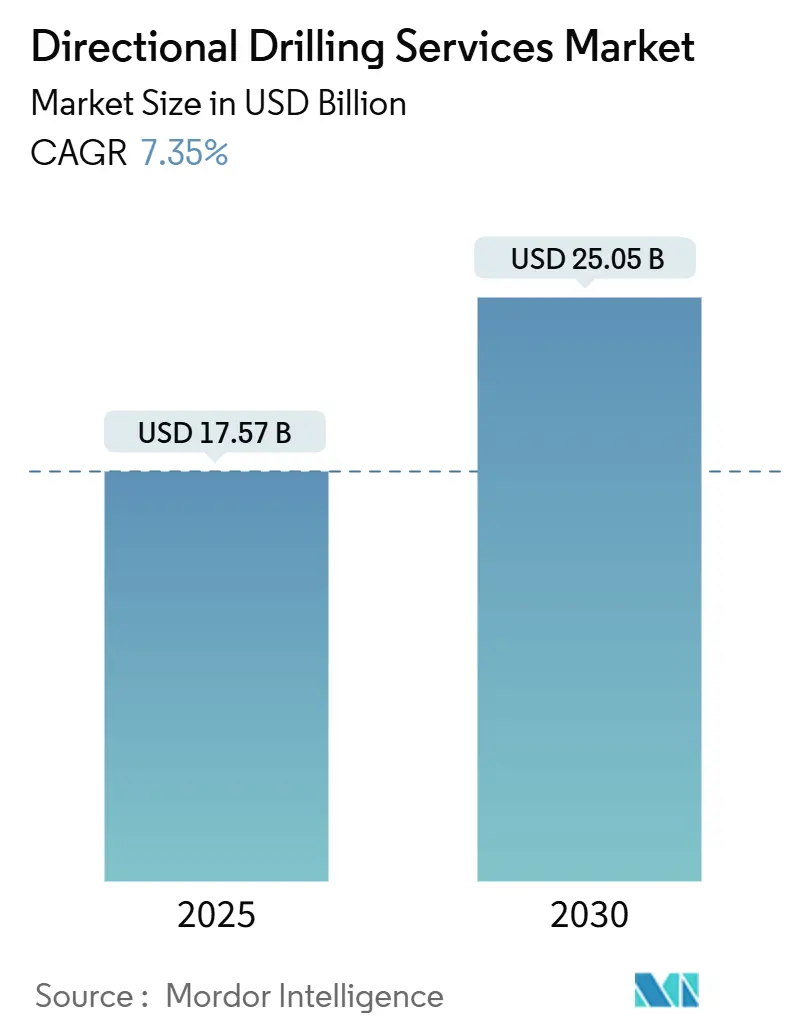

| Market Size (2025) | USD 17.57 Billion |

| Market Size (2030) | USD 25.05 Billion |

| Growth Rate (2025 - 2030) | 7.35% CAGR |

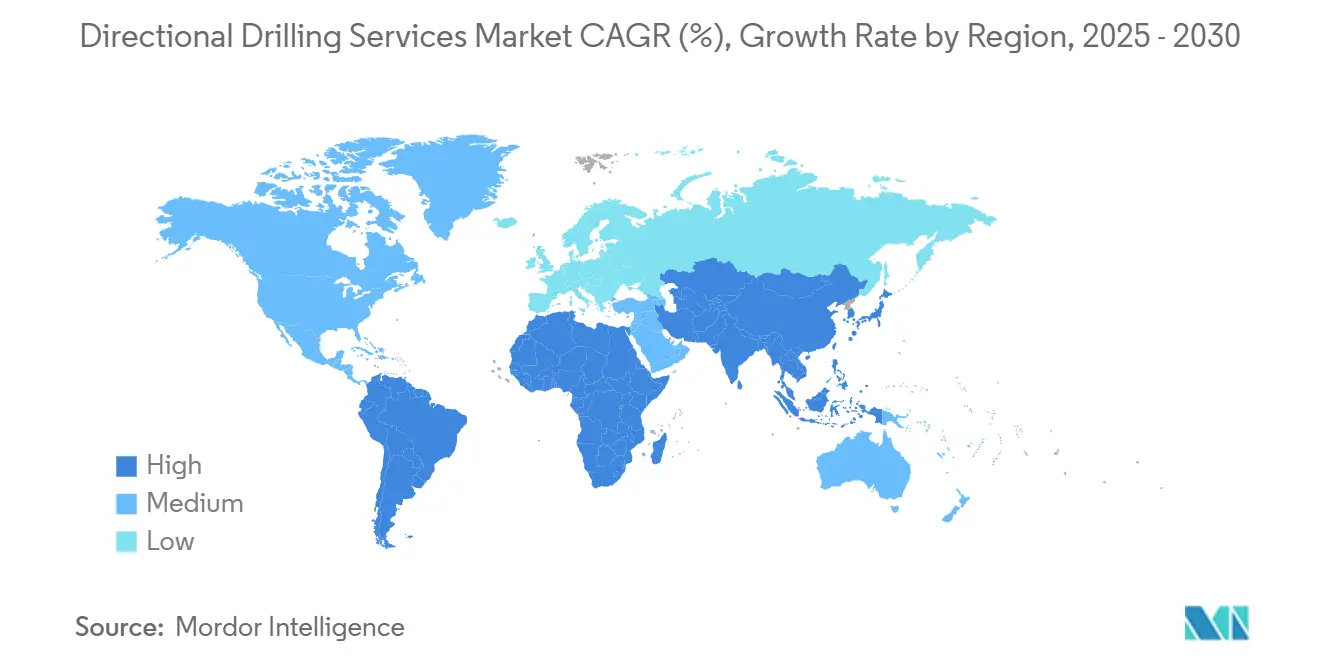

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Directional Drilling Services Market Analysis by Mordor Intelligence

The Directional Drilling Services Market size is estimated at USD 17.57 billion in 2025, and is expected to reach USD 25.05 billion by 2030, at a CAGR of 7.35% during the forecast period (2025-2030).

This expansion rests on operators’ shift toward precision drilling technologies that extend reservoir contact while shrinking the surface footprint. Lateral-length optimization in shale plays, deeper offshore discoveries, and an uptick in geothermal and carbon capture wells collectively sustain spending despite commodity price swings. Rotary steerable systems (RSS) hold technological primacy because they pair continuous proportional steering with real-time downhole data, enabling faster well construction and better wellbore quality. Artificial-intelligence platforms now automate trajectory adjustments in real-time, reducing human-in-loop interventions and lowering error rates. Regional spending is rebalancing: North America still accounts for 36.8% of global footage drilled, yet the Middle East and Africa post the quickest growth as national oil companies deploy long-reach wells to monetize low-carbon barrels. Supply-chain vulnerabilities linger, tungsten export controls and semiconductor shortages lengthen MWD/LWD lead times, but consolidation among service providers is easing cost pressure and broadening tool availability.

Key Report Takeaways

- By service, measurement-while-drilling accounted for 32.2% of 2024 revenue, while rotary-steerable services were projected to have the highest CAGR of 9.3% from 2024 to 2030.

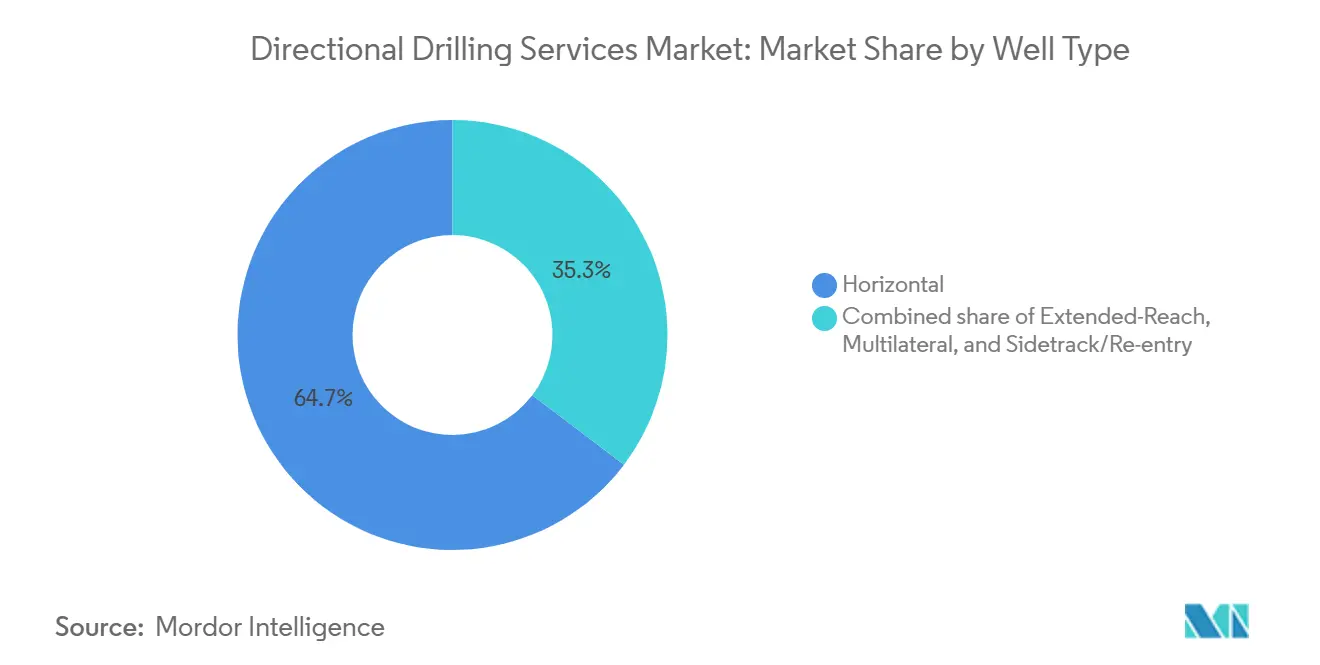

- By well type, horizontal wells accounted for 64.7% of the directional drilling services market size in 2024, whereas extended-reach wells are forecast to advance at 8.9% CAGR through 2030.

- By application, oil and gas production retained a 70.9% share in 2024; geothermal and CCUS wells are poised to grow at an 11.5% CAGR through 2030.

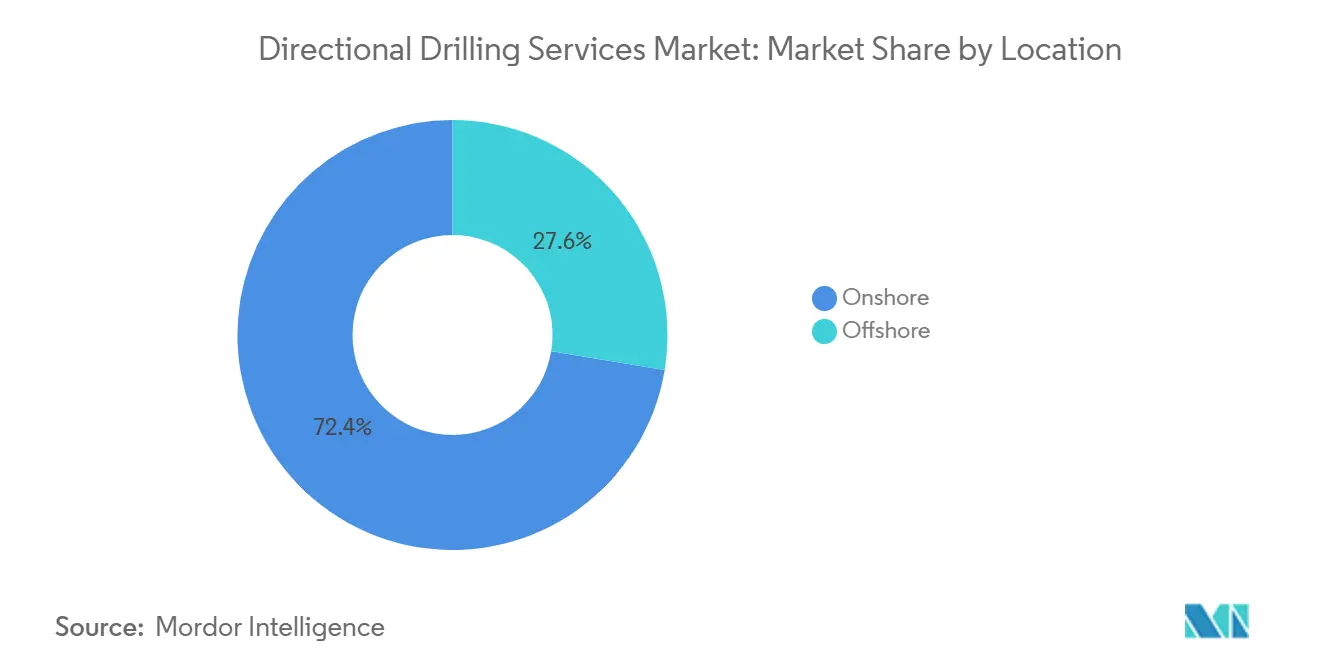

- By location, onshore operations captured a 72.4% share in 2024, while offshore activity shows a 7.8% CAGR to 2030.

- By geography, North America led with a 36.8% share in 2024, while the Middle East & Africa region is the fastest-growing, with an 8.4% CAGR through 2030.

Global Directional Drilling Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising shale & tight-oil development in North America | +1.80% | North America, with spillover to Argentina | Medium term (2-4 years) |

| Offshore ultra-deepwater expansion in South America & MEA | +1.50% | South America, MEA, with selective Asia-Pacific projects | Long term (≥ 4 years) |

| Productivity gains from next-gen rotary-steerable systems | +1.20% | Global, with early adoption in North America & Middle East | Short term (≤ 2 years) |

| Autonomous well-path optimisation & AI-driven slide-avoidance | +0.90% | Global, concentrated in high-tech drilling regions | Medium term (2-4 years) |

| Geothermal & CCUS well demand for complex trajectories | +0.80% | North America, Europe, with emerging Asia-Pacific interest | Long term (≥ 4 years) |

| North-African gas appraisal requiring extended-reach drilling | +0.60% | North Africa, with potential Mediterranean expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Shale & Tight-Oil Development in North America

Robust unconventional drilling maintains high pad efficiency as operators extend laterals beyond 5 miles in the Marcellus and Permian plays, sustaining tool demand even when rig counts plateau.[1]Jordan Blum, “Shale Producers Extend Lateral Lengths to Record Levels,” hartenergy.com Integrated AI platforms cut drilling time 30% by automating weight-on-bit and rotary speed, preserving capital discipline while holding production flat. Vaca Muerta replicates this model abroad, leveraging RSS and high-rate telemetry to unlock tight reservoirs at competitive breakevens. Nonetheless, 25% steel tariffs inflate OCTG costs, straining junior producers and nudging them toward service-company turnkey packages.

Offshore Ultra-Deepwater Expansion in South America & MEA

Deepwater capex now targets frontier arenas such as Namibia’s Orange Basin, where early discoveries accelerate FPSO orders and raise demand for ultra-deep directional kits rated beyond 35,000 psi. Brazil’s multi-year drilling envelope encompasses more than 100 wells and secures premium RSS day rates, shielding service margins from supply-chain cost fluctuations. Drillship utilisation hit 97% in 2025, tightening the spot market and incentivising rig upgrades with managed-pressure drilling packages. West Africa’s fiscal resets and rising LNG appetite further cement long-reach wells as the default platform for pre-salt reservoirs.

Productivity Gains from Next-Gen Rotary-Steerable Systems

Continuous proportional steering cuts slide–rotate cycles, preserving drill-bit life and improving hole quality. Baker Hughes’ Lucida RSS logs record a 35% faster rate of penetration compared with conventional motor assemblies, translating to one less run per well across mature Permian pads. Halliburton’s iCruise, bundled with LOGIX automation, yields 30% faster footage drilling and uniform borehole curvature, simplifying casing runs. ADNOC’s USD 270 million stake in Gordon Technologies underlines how telemetry and RSS co-development now underpins national E&P cost targets. Chinese land drills exceed 7,000 m horizontal displacements, evidencing swift technology diffusion and raising the competitive bar worldwide.

Autonomous Well-Path Optimisation & AI-Driven Slide-Avoidance

Closed-loop control merges surface rig automation with downhole steering to lock tilt corrections within inches of plan, shortening learning curves and freeing personnel for complex wells. Corva’s predictive suite delivers 20-45% rate-of-penetration gains and USD 100,000 savings per well by preventing stick-slip before it arises. SLB–Shell multi-region contracts incorporate AI geosteering as a standard deliverable, signaling operator confidence in algorithmic well delivery for high-cost, deepwater assets. Field rollouts confirm that trusted data pipelines and cybersecurity protocols are mandatory for broad adoption, especially in jurisdictions mandating in-country data residency.[2]SLB, “Neuro Autonomous Solution Delivers Production Gains,” slb.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility hurting E&P capex planning | -1.40% | Global, with heightened sensitivity in North America shale | Short term (≤ 2 years) |

| High capital cost of RSS & downhole electronics | -0.80% | Global, particularly affecting smaller operators | Medium term (2-4 years) |

| Semiconductor shortages delaying MWD/LWD tool deliveries | -0.60% | Global, with supply chain concentration in Asia-Pacific | Short term (≤ 2 years) |

| ESG-driven capital flight from hydrocarbon projects | -0.50% | Europe, North America, with selective impact in other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Hurting E&P Capex Planning

Public shale operators now recycle barely 40% of operating cash flow into new drilling, preferring shareholder returns and debt reduction, which dampens rig demand even at USD 70 oil.[3]American Oil & Gas Reporter, “Upstream Reinvestment Rates Hit Lows,” aogr.comNational oil companies echo this discipline: Saudi Aramco has suspended over 20 jackups, trimming MEA growth projections from 4% to 1%. Offshore FIDs slipped 29% year on year in 2024, deferring some floater starts to 2026 as contractors await FPSO hulls and regulatory sign-offs. Operators mitigate exposure by drilling longer laterals with fewer rigs, but this raises tool turnover and squeezes lead times for high-spec RSS kits.

High Capital Cost of RSS & Downhole Electronics

RSS packages cost 3-4 times more than positive-displacement motor assemblies, burdening independents that lack multibasin economies of scale. Steel tariffs, which add 25% to equipment costs, have pushed OCTG prices up 15%, widening the affordability gap. Service companies respond by retrofitting existing drillships with MPD gear rather than ordering newbuilds, a strategy that increases utilisation to 87% for upgraded assets compared to 77% for standard rigs. Rising wages add 3-8% to engineering overheads, while chip shortages delay high-frequency telemetry modules, slowing MWD/LWD turnaround to eight weeks in some basins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: MWD Dominance Faces RSS Services Challenge

Measurement-while-drilling held 32.2% of 2024 revenue, reflecting its universal application across every hole section and basin. Despite this, rotary-steerable services are on course for the quickest 9.3% CAGR through 2030, setting the pace for total directional drilling services market growth. RSS services blend directional control with high-bandwidth data; Quantum Energy’s Mesh175 merges electromagnetic and mud-pulse telemetry at 32 bps, guaranteeing connectivity even in depleted zones.

Logging-while-drilling expands as operators request real-time resistivity and sonic imaging to land laterals precisely in thin pay. SLB’s Ora intelligent wireline platform and SpectraSphere fluid mapping-while-drilling service enable reservoir characterization without round trips, resulting in a 15–20% reduction in emissions per well. Motor services remain price-competitive for vertical sections; however, downhole vibration and stick-slip mitigation technology is increasingly derived from RSS learnings, elevating performance expectations across the board.

By Well Type: Extended-Reach Growth Outpaces Horizontal Dominance

Horizontal wells commanded a 64.7% share of the directional drilling services market size in 2024, the natural outcome of multi-well pad economics in shale basins. Conversely, extended-reach wells post the swiftest 8.9% CAGR as offshore and remote onshore projects pursue reservoirs 5–7 miles from surface facilities. ExxonMobil’s 22,211-ft lateral in the Permian demonstrates that frontier laterals are no longer the domain of niche operators.

Extended-reach success hinges on catenary trajectory design, which reduces friction by 23.8% compared to classical arcs, and relies on high-torque RSS mandrels, as well as real-time friction factors from wired drillpipe. SLB helped Equinor drill a 34,145-ft Gulf of Mexico well in 18.8 days by combining SonicVISION cement evaluation with closed-loop performance software. Chinese land operators push 3,700-m horizontals using tailored high-lubricity fluids and slim RSS, evidence that extended-reach drilling is primed to diffuse globally.

By Application: Geothermal and CCUS Transform Energy Landscape

Oil and gas production still occupies 70.9% of 2024 activity; however, geothermal and carbon-capture wells show an 11.5% CAGR, broadening the client base for directional drilling services market suppliers. Fervo Energy cut geothermal well times by 70% and costs to USD 4.8 million by adopting shale-style pad drilling, proving cross-sector scalability.

The US Department of Energy targets 90 GW of geothermal capacity by 2050, up from 3.7 GW, implying the need for thousands of deep, hot-rock wells that require high-temperature RSS and ultra-high-speed telemetry. Horizontal directional drilling also drives telecom ducting: Vermeer’s D24 boasts a 100-hp engine and automated pipe handling for urban fibre builds. Ditch Witch’s JT120 delivers 120,000 lb thrust for utility-scale crossings, reflecting how trenchless-tech demand buffers rig shops when oil prices wobble.

By Location: Offshore Growth Accelerates Despite Onshore Dominance

Onshore campaigns accounted for 72.4% of 2024 revenue, with Permian rigs still capturing nearly 60% of US land activity. The offshore slice of the directional drilling services market nonetheless registers a 7.8% CAGR to 2030 as ultra-deepwater fields finalize FIDs. Drillship utilisation reached 97% in 2025, setting a floor under day rates and spurring rig owners to invest in MPD and high-voltage subsea wiring to win Brazil and Mexico scopes.

ADNOC Drilling is spending USD 750-950 million to add 15 rigs, chasing low-emission Gulf barrels, while the US Gulf maintains a steady 1.80 million bpd production level with a consistent rig count. Africa’s inventory surpasses 1,100 planned wells for 2024, with 19 floaters on contract and potential upside to 25 units if Angola and Namibia sanction new deepwater hubs.

Geography Analysis

North America maintained a 36.8% share in 2024, underpinned by its shale footprint; however, the Middle East & Africa achieved the highest 8.4% CAGR to 2030 as national champions unwind capacity caps imposed during the pandemic. ADNOC Drilling recorded a 32% revenue growth in Q1 2025 and booked USD 733 million for the extended-reach Zakum wells, securing tool supply chains through localised MWD joint ventures.

Africa anticipates USD 43 billion capex in 2025, half focused on West African deepwater developments where pre-salt geometry demands sophisticated RSS and high-frequency imaging. Algeria's partnership with Chevron illustrates North Africa's ambition to capture Mediterranean gas export premiums, while Namibia's string of discoveries elevates the country from a frontier to a hub status. Europe faces regulatory headwinds; TotalEnergies weighs a New York listing to escape ESG valuation discounts, signalling capital flight that could redirect service fleets toward US or MEA jobs. Asia–Pacific growth is more selective, driven by India's push for import substitution and Southeast Asian gas backfill for LNG trains.

Competitive Landscape

Moderate consolidation shapes the directional drilling services market as scale becomes a prerequisite for AI-ready tool development. Helmerich & Payne’s USD 1.97 billion takeover of KCA Deutag boosts its Middle East rig tally from 12 to 88 and centralises circulating inventory, trimming per-well tool logistics by 12%. Nabors’ acquisition of Parker Wellbore adds 17 rigs and targets USD 40 million annual synergies, enlarging its turnkey footprint for geothermal and CCUS clients.

Technology differentiators now command bidding premiums: SLB’s Neuro autonomous geosteering secured multibasin Shell contracts and underpinned a USD 800 million Brazilian deepwater package spanning nine ultra-deep rigs. Baker Hughes unveiled all-electric subsea systems that cut hydraulic leaks and simplify umbilical architecture, pairing with its Lucida RSS to offer full well-construction stacks. Start-ups such as Quantum Energy Technologies disrupt incumbents with dual-modem telemetry and rapid-cycle firmware updates, attracting independents seeking agile deployment.

White-space lies in geothermal spudding: Fervo’s unlocks prove that oilfield know-how converts to hot-rock economics, while NOV repurposes drillstring vibration dampeners for 200 °C environments. Patent filings surge, Halliburton’s rotating housing for offsettable drive shafts exemplifies fresh IP that tightens operational envelopes in 12¼-inhole sizes. Meanwhile, China’s curbs on tungsten and indium hinder bit manufacture, spotlighting raw-material risk in a market otherwise trending toward digital resilience.

Directional Drilling Services Industry Leaders

Schlumberger Ltd

Weatherford International PLC

Halliburton Company

Baker Hughes Company

China Oilfield Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chevron brought the Ballymore subsea tieback online in the Gulf of Mexico, targeting 300,000 boe/d by 2026.

- April 2025: SLB has launched new electric well control (EWC) technologies and secured a front-end engineering and design (FEED) contract for an all-electric blowout preventer (BOP) control system in the North Sea. The EWC technology was launched in March 2025.

- March 2025: Nabors Industries completed the acquisition of Parker Wellbore, adding 17 rigs to its fleet and boosting expected annual adjusted EBITDA by USD 150 million. The acquisition also includes Parker's wellbore construction solutions, including Quail Tools, a rental provider of downhole tubulars.

- February 2025: Halliburton and Sekal delivered the first autonomous on-bottom drilling system for Equinor’s North Sea program.

- January 2025: Halliburton has been awarded Brazil's largest integrated drilling contract by Petrobras, focusing on both pre-salt and post-salt wells. This three-year contract, beginning in 2025, encompasses drilling services for development and exploration wells across several offshore fields.

Global Directional Drilling Services Market Report Scope

Directional drilling employs specialized techniques to create non-vertical wells and bores, facilitating access to underground resources and the controlled installation of utilities. Industries such as oil and gas utilize this method to tap into reservoirs from a surface point. Additionally, in utility work, directional drilling enables the installation of pipelines, cables, and conduits beneath obstacles, minimizing the need for extensive surface excavation.

The directional drilling services market is segmented by service, well type, application, location of deployment, and geography. By service, the market is segmented into measurement-while-drilling and survey, rotary steerable services, and more. By well type, the market is segmented into horizontal, extended-reach, multilateral, and sidetrack/re-entry. By application, the market is segmented into oil and gas production, geothermal and CCUS wells, utility installation, and more. By location of deployment, the market is segmented into onshore and offshore. The report also covers the market sizes and forecasts for the global directional drilling services market across major countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Service

| Measurement-While-Drilling (MWD) and Survey |

| Logging-While-Drilling (LWD) |

| Rotary Steerable Services (RSS) |

| Downhole Motors |

By Well Type

| Horizontal |

| Extended-Reach |

| Multilateral |

| Sidetrack/Re-entry |

By Application

| Oil and Gas Production |

| Utility Installation (HDD) |

| Telecommunications Ducting |

| Geothermal and CCUS Wells |

By Location of Deployment

| Onshore |

| Offshore |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service | Measurement-While-Drilling (MWD) and Survey | |

| Logging-While-Drilling (LWD) | ||

| Rotary Steerable Services (RSS) | ||

| Downhole Motors | ||

| By Well Type | Horizontal | |

| Extended-Reach | ||

| Multilateral | ||

| Sidetrack/Re-entry | ||

| By Application | Oil and Gas Production | |

| Utility Installation (HDD) | ||

| Telecommunications Ducting | ||

| Geothermal and CCUS Wells | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected size of the directional drilling services market by 2030?

The market is projected to reach USD 25.05 billion by 2030.

Which technology currently leads the directional drilling services market?

Rotary steerable systems lead with 58.5% share in 2024 and demonstrate a 7.8% forecast CAGR.

Why is the Middle East & Africa the fastest-growing regional market?

Aggressive national-oil-company drilling programs and low-cost, low-carbon barrel ambitions drive an 8.4% CAGR in the region.

How are artificial intelligence tools impacting drilling operations?

AI platforms reduce human intervention, boost rate of penetration by up to 45%, and shorten drilling days, enhancing overall project economics.

What role do geothermal and CCUS applications play in market growth?

These emerging applications post an 11.5% CAGR, diversifying revenue streams beyond oil and gas and reinforcing long-term service demand.

Are supply-chain issues still affecting tool availability?

Yes, tungsten export limits and semiconductor shortages extend lead times for drill bits and MWD/LWD electronics, though consolidation helps offset some delays.

Page last updated on: