Managed File Transfer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

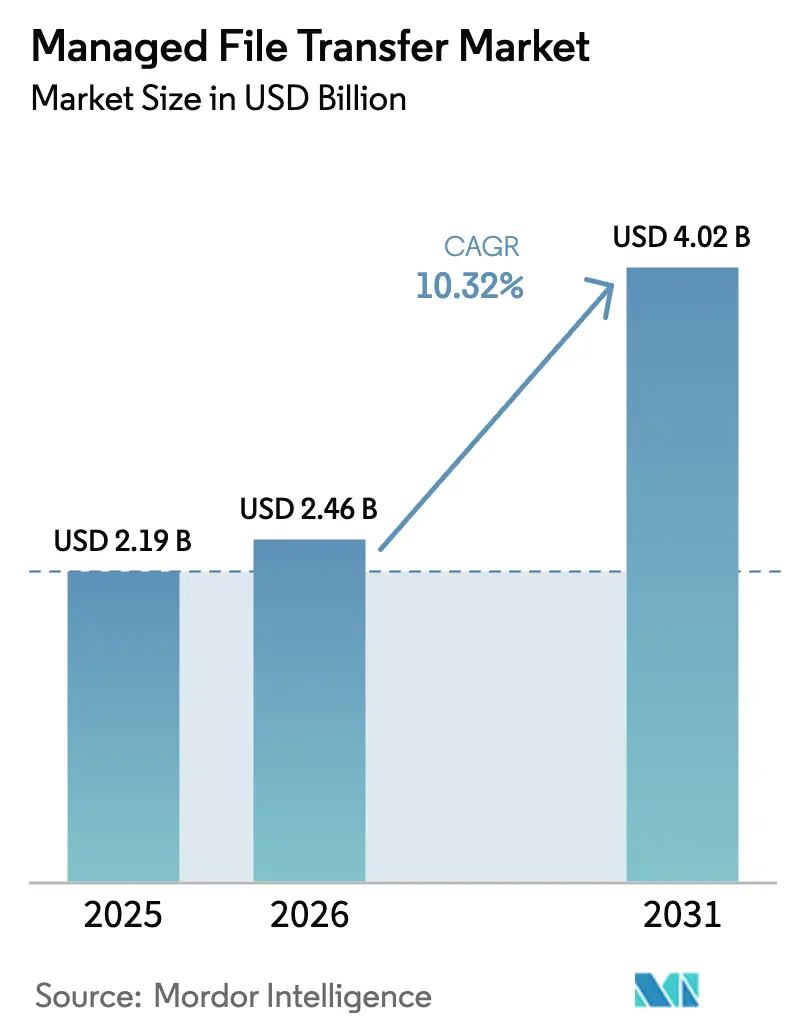

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed File Transfer Market Analysis by Mordor Intelligence

The managed file transfer market size is expected to grow from USD 2.19 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 4.02 billion by 2031 at 10.32% CAGR over 2026-2031. Heightened adoption of zero-trust security frameworks, tighter data protection enforcement, and the need for multi-cloud integration are compelling enterprises to replace legacy protocols with policy-rich platforms that verify every transaction. Penalties such as the EUR 290 million (USD 310 million) fine on Uber and the EUR 530 million (USD 567 million) fine on TikTok confirm that regulators treat governance lapses as systemic failures. Simultaneously, the U.S. Federal Trade Commission’s broadened Health Breach Notification Rule pushes digital-health providers toward auditable solutions. Vendors are responding with cloud-native subscription offerings that bundle compliance templates and AI-driven anomaly detection, tightening competition and compressing margins. Asia-Pacific adoption is accelerating as Digital India and Japan’s transformation programs fuel demand for secure data movement across hybrid architectures.

Key Report Takeaways

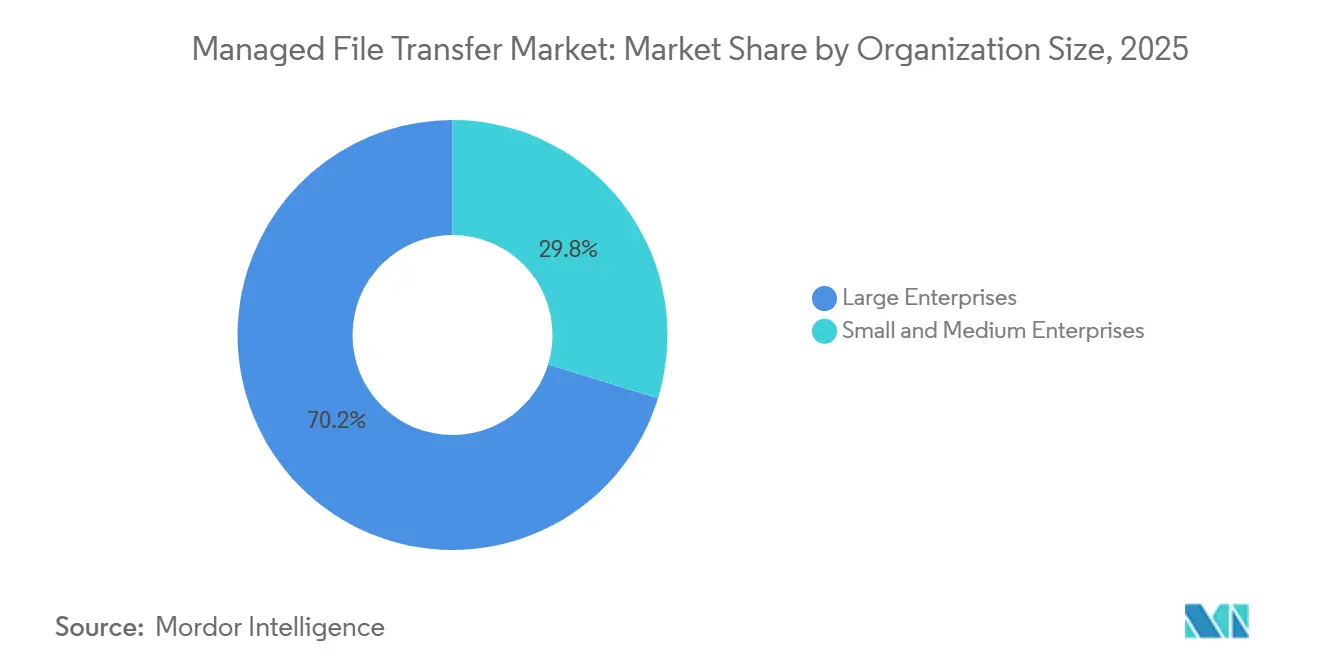

- By organization size, large enterprises held 70.24% of the managed file transfer market share in 2025, while small and medium enterprises are forecast to expand at a 10.07% CAGR through 2031.

- By deployment mode, the on-premise segment accounted for 64.69% of the managed file transfer market size in 2025, whereas cloud-based solutions are projected to progress at a 10.13% CAGR through 2031.

- By transfer type, system-centric workflows captured a 79.37% share of the managed file transfer market size in 2025, and people-centric transfers are advancing at a 10.21% CAGR through 2031.

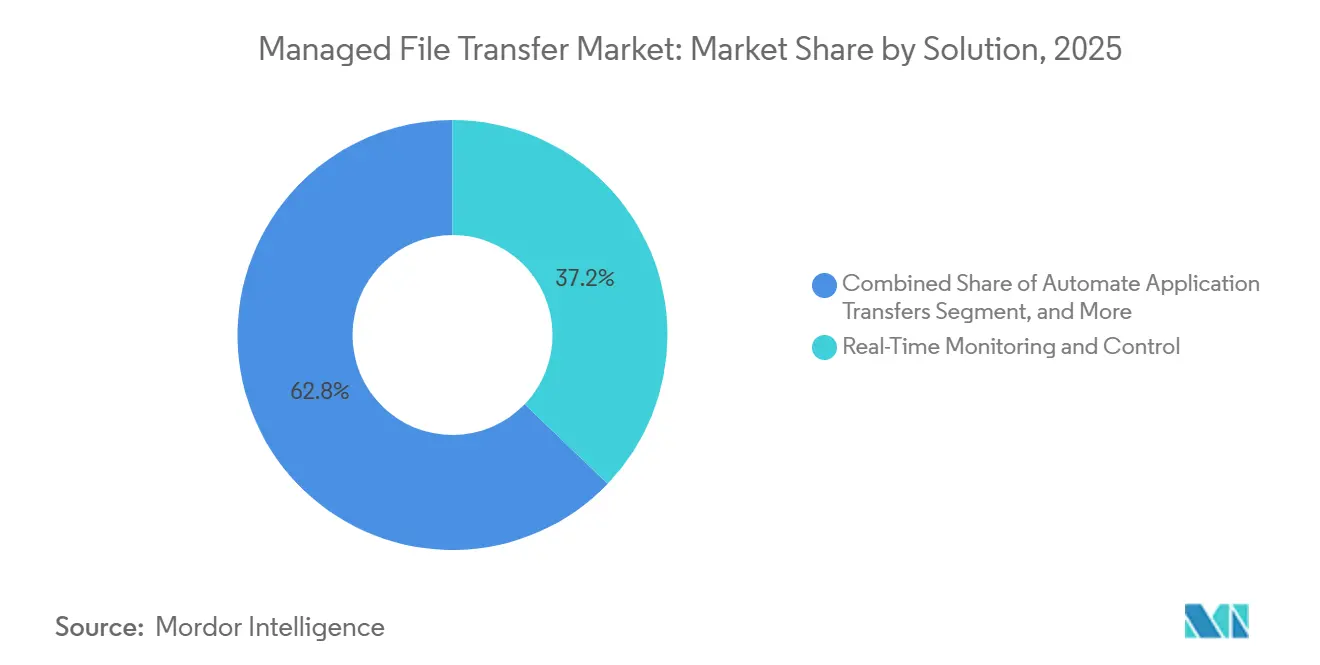

- By solution, real-time monitoring and control is expected to lead with a 37.16% revenue share in 2025, and partner onboarding is projected to register the highest 11.34% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance held a 36.29% share in 2025, while healthcare is projected to post an 11.59% CAGR to 2031.

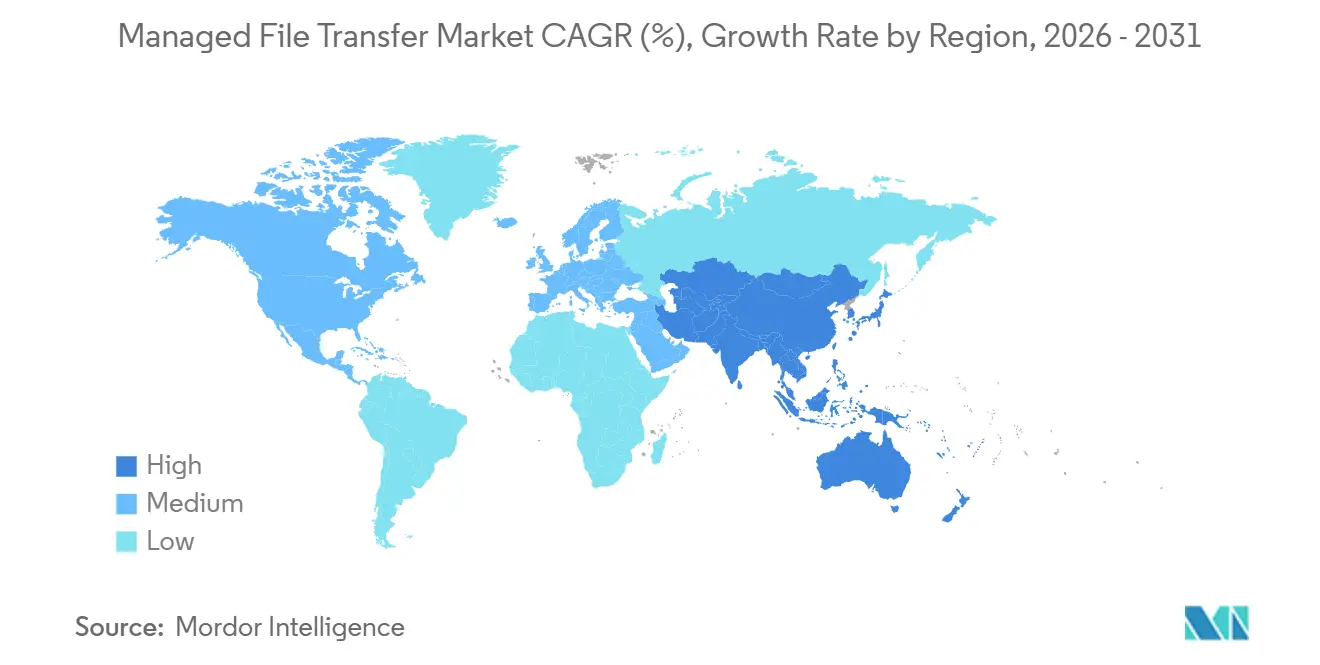

- By geography, North America retained a 37.82% share in 2025, and Asia-Pacific is anticipated to record the fastest CAGR of 11.46% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Managed File Transfer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to Zero-Trust Architectures | +2.1% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Escalating Financial Penalties for Non-Compliance | +1.8% | Europe and North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Multi-Cloud and Hybrid Integration Demand Surge | +1.6% | Global, concentrated in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| AI-Powered Threat Detection in File Transfers | +1.4% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Real-Time Supply-Chain Data Synchronization Needs | +1.3% | Global, with manufacturing hubs in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing Adoption of MFTPaaS by Mid-Market Firms | +1.2% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Zero-Trust Architectures

CISA’s 2024 advisory on living-off-the-land techniques highlighted how attackers exploit trusted file-transfer utilities to circumvent perimeter defenses.[1]U.S. Cybersecurity and Infrastructure Security Agency, “Understanding and Mitigating Living Off the Land Techniques,” cisa.gov As a result, organizations are dismantling implicit-trust zones and demanding platforms that enforce continuous identity validation, device-posture checks, and content inspection for every file. Managed file transfer market vendors embed policy engines tied to identity providers and DLP tools, delivering adaptive access controls without the latency of middleware. Cyber-insurance carriers now require zero-trust attestations, further accelerating platform refresh cycles. Enterprises that adopted zero-trust MFT reduced mean-time-to-detect from days to minutes, limiting breach impact and lowering premiums.

Escalating Financial Penalties for Non-Compliance

The record GDPR fines imposed on Uber and TikTok demonstrate that weak governance around cross-border transfers can trigger top-tier penalties. The FTC’s updated Health Breach Notification Rule extended disclosure mandates to non-HIPAA entities, making audit trails and encryption-at-rest mandatory for health apps.[2]U.S. Federal Trade Commission, “Health Breach Notification Rule,” ftc.gov Enterprises respond by adopting platforms pre-loaded with GDPR, HIPAA, SOC 2, and ISO 27001 templates, cutting certification timelines. Real-time logs and automated incident response reduce breach-notification costs and protect brand equity, which lifts demand across regulated industries and bolsters the managed file transfer market.

Multi-Cloud and Hybrid Integration Demand Surge

AWS booked USD 7.5 billion Asia-Pacific revenue in Q3 2024, underscoring rapid cloud uptake that fragments data across on-premises, public-cloud, and SaaS silos.[3]Amazon Web Services, “Q3 2024 Earnings,” ir.aboutamazon.com Point-to-point scripts cannot scale, introducing operational risk. MFT platforms with pre-built connectors for S3, Azure Blob, Google Cloud Storage, Salesforce, and Workday cut integration effort by up to 70%. API-first designs and webhook triggers enable real-time synchronization, eliminating batch latency. This agility supports just-in-time inventory, instant payments, and cross-border collaboration, reinforcing the growth trajectory of the managed file transfer market.

AI-Powered Threat Detection in File Transfers

IBM’s X-Force Index recorded a 71% jump in exploits targeting file-transfer tools in 2025. Zscaler reported a 45% rise in malware hidden inside encrypted transfers. Vendors now integrate machine-learning models that profile user behavior, file metadata, and traffic patterns to flag anomalies before exfiltration occurs. OPSWAT’s content-disarm technology removes active code from files mid-flow, reducing zero-day exposure. Early adopters cut dwell time and demonstrate due diligence during audits, sustaining premium pricing for AI-rich offerings and advancing the managed file transfer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills Gap in Secure Automation Workflows | -1.1% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Legacy System Lock-In and Integration Complexity | -0.9% | North America and Europe, with pockets in Asia-Pacific | Long term (≥ 4 years) |

| Rising Cross-Border Data-Localization Barriers | -0.7% | China, Russia, and emerging in Middle East | Short term (≤ 2 years) |

| Budget Constraints for SMEs Amid Macroeconomic Volatility | -0.6% | Global, concentrated in SME-heavy regions like Europe and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skills Gap in Secure Automation Workflows

The 2024 ISC2 study highlighted a 4.8 million-person cybersecurity shortfall, with 92% of firms lacking automation skills. Complex scripting, API orchestration, and policy tuning slow MFT rollouts. SMEs often accept default settings, weakening controls, or pay for costly consultants that prolong payback periods. Vendors simplify interfaces and launch managed-services tiers, but recurring fees erode the cost benefits, tempering the near-term growth of the managed file transfer market.

Legacy System Lock-In and Integration Complexity

Mainframe and AS/400 environments still anchor banking and government workloads. Proprietary protocols clash with modern API-driven MFT, necessitating adapters that introduce latency and additional failure points. Hybrid coexistence creates fragmented governance, complicates audits, and inflates the total cost of ownership. Until legacy retirement accelerates, integration hurdles will restrain portions of the managed file transfer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Mid-Market Subscription Uptake Widens Access

Small and medium enterprises are forecast to grow at a 10.07% CAGR, outstripping the overall managed file transfer market. Deloitte found 68% of SMEs face budget pressure, yet cybersecurity spend climbed 15% in 2025. Subscription MFTPaaS eliminates servers and six-figure licenses, letting lean IT teams deploy within days. The October 2025 launch of Automate MFT targets this cohort with a promised 50% TCO cut. Large enterprises retain a 70.24% share due to entrenched on-premises estates, but hybrid strategies signal a gradual pivot toward SaaS connectors. As mid-market adoption increases, the managed file transfer market expands into greenfield accounts that were previously priced out of enterprise-grade security.

Fortune 500 companies are harnessing MFTPaaS for seamless cloud-to-cloud transitions, all the while upholding on-premises gateways for their mainframe connections. This strategic combination ensures uniform policy application and a worldwide presence, all while adhering to data-residency regulations. This adaptability underscores the managed file transfer market's robustness, even amidst economic fluctuations.

By Deployment Mode: Cloud Momentum Undercuts On-Premises Lead

On-premises installations accounted for 64.69% of 2025 revenue, while cloud deployments are expected to register a 10.13% CAGR through 2031. Elastic scaling addresses holiday retail surges and healthcare open enrollment peaks, trimming 30–40% of capacity overhead. OMB Memorandum M-24-15 now mandates FedRAMP authorization, signaling institutional acceptance of secure cloud services.

Kiteworks’ FedRAMP High certification in 2024 proved that MFTPaaS can satisfy stringent controls. Regions with strict localization laws, notably China and Russia, still favor on-premises hubs; yet, hybrid architectures with regional gateways and cloud orchestration mitigate compliance friction. This transition ecosystem widens the managed file transfer market size while rebalancing revenue streams toward recurring subscriptions.

By Transfer Type: Automation Dominates, Collaboration Climbs

System-centric transfers accounted for 79.37% of the 2025 value, as automated workflows underpin supply-chain and reconciliation tasks. CMS handles 3 million transfers each month, spanning 1,200 endpoints. This extensive network highlights the platform's scalability and efficiency in managing high-volume operations. The surge in demand for remote collaboration is evident, with people-centric workflows growing at a 10.21% CAGR, driven by the increasing need for seamless and flexible communication solutions.

Consumer apps without audit trails are being replaced by secure portals that offer drag-and-drop simplicity. While extreme transfers are still a niche, IBM Aspera boasts a 100× speed advantage, and Signiant offers flat-rate pricing, both targeting the 8K video pipeline. In post-production, the adoption of ASC MHL checksums is becoming standard to ensure file integrity. Collectively, these trends are broadening revenue streams in the managed file transfer market.

By Solution: Visibility First, Onboarding Accelerates

Real-time monitoring secured a 37.16% share because visibility is essential for zero-trust and audit compliance. IBM reported a 71% surge in the exploitation of file-transfer vulnerabilities, which has driven organizations to prioritize investments in advanced dashboards. These dashboards are specifically designed to detect unusual IP addresses and monitor spikes in activity during off-hours, enabling enhanced security measures and quicker responses to potential threats.

Partner onboarding is projected to grow at an 11.34% CAGR as retailers and manufacturers rapidly integrate seasonal suppliers. Self-service portals reduce setup time from weeks to days, freeing up IT staff and accelerating revenue. Vendors strengthen their portfolios by incorporating automation tools for database replication and IoT ingestion. These tools not only enhance operational efficiency but also enable vendors to effectively cross-sell their solutions within the managed file transfer market, thereby driving growth and expanding their customer base.

By End-User Industry: Healthcare Leapfrogs

BFSI controlled 36.29% of the expenditure in 2025, yet healthcare is expected to rise at an 11.59% CAGR to 2031. InterSystems' Health Connect has rolled out enhanced support for FHIR R5, streamlining data exchanges between diverse electronic records. This update aims to improve interoperability by enabling seamless communication and integration of healthcare data across various systems, ensuring more efficient and accurate data sharing.

Health apps now face the FTC's expanded breach-notification rule, signaling a pivot away from traditional consumer file-sharing. Retailers are pushing for immediate stock synchronization, while government entities are on the lookout for platforms that meet FedRAMP standards. Meanwhile, telecom companies are prioritizing low-latency transfers to optimize their 5G setups. These diverse demands are fueling the ongoing growth of the managed file transfer market.

Geography Analysis

In 2025, North America captured 37.82% of the revenue, driven by strict regulatory measures, increasing adoption of cyber-insurance, and heightened awareness of cybersecurity threats. Responding to CISA's emphasis on "living-off-the-land" attacks, federal agencies took significant steps to modernize their FTP estates, ensuring enhanced security and compliance. This trend is mirrored by Canada's banking regulator, which has implemented robust cybersecurity frameworks, and manufacturers in Mexico's nearshoring sector, who are adopting advanced measures to safeguard their operations. These developments collectively reinforce the region's momentum in addressing cybersecurity challenges.

Asia-Pacific is forecast to post the fastest 11.46% CAGR. Cloud investments driven by Digital India and Japan’s reform agenda demand secure hybrid transfers. However, China’s PIPL and Russia’s localization laws enforce domestic storage, nudging vendors toward in-country data centers. Europe balances expansion with high compliance pressure. Uber and TikTok fines illustrate uncompromising enforcement that fuels demand for audit-ready platforms. The EU-U.S. Data Privacy Framework offers partial relief yet faces legal scrutiny.

Saudi Arabia's 2024 Personal Data Protection Law aligns closely with the GDPR, and Brazil intensifies its LGPD enforcement with heightened fines. As the Middle East, Africa, and South America emerge as new frontiers, infrastructure gaps in these regions are increasingly leaning towards cloud solutions. This trend is paving the way for vendors with regional Points of Presence (PoPs) to tap into the previously uncharted segments of the managed file transfer market.

Regulatory Landscape

Managed file transfer (MFT) deployments are increasingly shaped by cybersecurity control frameworks and enforceable reporting obligations across major regions. In the United States, NIST SP 800-53 Revision 5 control families used by federal information systems (including information-exchange and information-flow enforcement controls) are pushing agencies and contractors toward policy-driven transfer gateways with auditable logging, strong authentication, and controlled data paths. For defense supply chains, CMMC Level 2 requirements tied to NIST SP 800-171 controls, along with the use of FIPS 140-3 validated cryptographic modules, raise expectations for encryption and key handling in platforms that move Controlled Unclassified Information (CUI).

In Europe, NIS2 introduces supply-chain risk management and fast incident reporting expectations (early warning within 24 hours and notification within 72 hours), which lifts the value of centralized monitoring, immutable audit trails, and incident-ready workflows around third-party exchanges. Financial institutions also operate under the EU Digital Operational Resilience Act (DORA), effective 17 January 2025, tightening third-party ICT risk governance for outsourced processes that often rely on external file exchanges. In payments, PCI DSS 4.0 reached full enforcement on 31 March 2025, reinforcing stronger requirements for logging, encryption, and authentication for environments that handle cardholder data, which accelerates the replacement of unmanaged scripts and legacy FTP implementations.

Value Chain Analysis

The MFT value chain begins with foundational technology providers, including encryption and identity components, secure protocol stacks, and cloud infrastructure, which support secure transport and key management. Platform vendors build on these blocks by providing policy engines, connectors, portals, and audit layers, and hyperscaler services often shape platform capabilities and deployment choices, particularly where organizations rely on pre-built connectors to integrate storage and SaaS endpoints across hybrid and multi-cloud environments.

Downstream, system integrators and managed security or service providers implement MFT in regulated environments by mapping configurations to frameworks such as NIST controls, PCI DSS 4.0, and DORA. They also handle migration from legacy mainframe and AS/400 estates, where adapters and coexistence patterns are common. Channel partners and software ecosystems further influence adoption through integrations that reduce operational friction for high-volume and media-heavy use cases. End users across BFSI, healthcare, government, retail, and manufacturing supply chains drive needs around partner onboarding, real-time monitoring, certificate lifecycle management, and incident-response-ready logging, while recurring bottlenecks persist around legacy integration complexity, certificate expiry management, and maintaining consistent governance during cloud migration under regional data-localization constraints.

Competitive Landscape

The managed file transfer market shows moderate concentration. IBM, Axway, OpenText, and Progress Software leverage deep enterprise ties and broad portfolios. IBM folded MFT into Cloud Pak for Integration, raising switching costs. Progress acquired ShareFile for USD 875 million in 2024, followed by the introduction of Automate MFT in 2025, which undercut on-premises pricing by half. Breaches involving MOVEit, GoAnywhere, and Cleo prompted customers to reassess their vendors, opening the door for cloud-native challengers that tout continuous vulnerability scans and zero-trust defaults.

Extreme transfers for media, FedRAMP High-certified government deployments, and emerging markets demanding local storage continue to see white space. These areas present significant opportunities for vendors to address unmet needs and expand their offerings. Kiteworks achieved FedRAMP High certification, enabling it to cater to stringent government requirements, while Hyland integrated AWS document AI with file transfers to streamline content extraction and enhance operational efficiency.

Vendors are now more frequently unveiling REST APIs and webhook triggers, harmonizing with event-driven architectures vital for real-time supply chain and payment processes. These advancements are critical for enabling seamless data exchange and improving workflow automation. This competitive drive fuels ongoing innovation in the managed file transfer market, pushing vendors to continuously enhance their solutions to meet evolving customer demands.

Managed File Transfer Industry Leaders

IBM Corporation

Axway Software SA

OpenText Corporation

Progress Software Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven modernization is creating whitespace for MFT platforms that can demonstrate control alignment and cryptographic maturity across multiple frameworks in a single operational model. A concrete anchor is NIST SP 800-172 Rev. 3 (final, May 2026), which strengthens enhanced security requirements for protecting CUI in nonfederal systems and reinforces demand for MFT components that can show rigorous access control, auditing, identification and authentication, and communications protection behaviors. Defense supply-chain readiness around CMMC 2.0 Level 2 assessments becoming mandatory in November 2026 also increases procurement focus on MFT solutions that operationalize NIST SP 800-171-aligned controls and support FIPS 140-3 validated cryptographic modules for regulated file exchanges.

Another opportunity is the convergence of secure file transfer with orchestration and broader integration stacks. Enterprises increasingly want MFT to operate as a governed data-movement layer across hybrid and multi-cloud footprints rather than only as a standalone gateway. Current vendor actions in cloud and ecosystem integration support this direction through partnerships and product updates that add connectors, web portals, and automation hooks to reduce double-hop workflows and expand governed exchanges with suppliers and partners. Buyers in regulated industries also increasingly treat continuous monitoring and evidence-ready logging as purchase requirements, which supports demand for MFT offerings that bundle policy templates, real-time anomaly detection, and reporting workflows that fit incident notification obligations and audit response.

Recent Industry Developments

- June 2026: Coviant Software released Diplomat MFT 9.5 with a new web transfer portal aimed at secure, browser-based file exchange. The update reinforces the push toward modern user-facing transfer experiences while keeping governance controls such as authentication and auditability centralized.

- March 2026: Axway delivered Q1 2026 updates across its Managed File Transfer portfolio, including releases for SecureTransport 5.5, Workbench 1.0, and Transfer CFT 3.10. The refresh supports customers standardizing and upgrading long-lived enterprise estates, a common requirement when tightening logging, policy enforcement, and integration across hybrid environments.

- June 2024: Progress Software released MOVEit Transfer v14 with expanded cloud-native deployment options. The release broadened deployment flexibility for organizations modernizing legacy file transfer, supporting migration programs that shift governance and secure exchange capabilities into cloud operating models.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the managed file transfer market covers software and related services used to move files securely between people, applications, and systems, with centralized controls, audit trails, and automation for business workflows.

Scope exclusions: This sizing excludes general email attachments and basic consumer file sharing tools that do not offer managed controls, policy enforcement, and enterprise-grade logging.

Segmentation Overview

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Transfer Type

- System-Centric File Transfer

- People-Centric File Transfer

- Extreme File Transfer

- By Solution

- Real-Time Monitoring and Control

- Fast Partner Onboarding and Collaboration

- Automate Application Transfers

- Other Solutions

- By End-User Industry

- BFSI

- IT and Telecommunications

- Healthcare

- Retail

- Media and Entertainment

- Government and Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the technology scope and the demand signals that usually move this market. We relied on public cybersecurity and digital economy references such as NIST guidance on secure file transfer practices, ISO and IEC security standards, and regulatory texts that influence audit and retention needs in data exchange.

For market inputs, we reviewed public filings and investor decks from solution providers and system integrators, plus product documentation to understand how pricing is structured across cloud and on-premise deployments. We also checked statistics and publications from sources such as the US FTC and other privacy regulators, OECD digital trade notes, and peer-reviewed security journals to capture drivers like compliance, encryption, and automation. Paid database subscriptions were used selectively to standardize company financials and to screen patent activity tied to secure transfer and workflow automation. These desk sources are illustrative, and other public references were used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary interviews and surveys helped confirm what buyers actually pay for managed transfers, how deployments are split between cloud and on-premise, and how adoption differs by regulated industries. We spoke with a mix of solution owners, security and integration leaders, and operations managers across APAC, EMEA, and the Americas. Their input was then used to tighten assumptions on renewal behavior, typical contract terms, and feature-driven price steps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 41% |

| Mid tier: 57% | Functional/Unit leaders: 25% | EMEA: 36% |

| Smaller Players: 15% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build where enterprise secure data exchange spend was reconstructed through deployment mix signals and adoption rates for managed transfer use cases, and then filtered by industries with higher audit and compliance intensity. To keep the totals realistic, we then cross-checked with selective bottom-up approximations using sampled supplier revenues, partner channel checks, and simple ASP times volume math for common user and connection bundles.

Key inputs used in the model included the share of cloud-based deployments versus on-premise, typical subscription and maintenance price ranges, the split of system-centric versus people-centric transfer needs, renewal and expansion patterns in regulated industries, and the observed pace of automation use cases, including application-to-application transfers and onboarding. Where bottom-up references had gaps, missing coverage was handled by applying conservative uplift factors based on the presence of indirect channels and by comparing against adjacent secure integration software signals.

For forecasting, scenario analysis was used so that different adoption speeds for zero-trust enforcement, compliance-driven logging, and multi-cloud integration could be reflected in the curve. Assumptions were aligned to what interviewees saw in pipeline conversion and budget timing, and then smoothed to avoid step changes that were not supported by the inputs.

Data Validation & Update Cycle

Outputs were checked against independent signals such as vendor revenue disclosures, observed cloud migration pace, and the rate of compliance and audit requirements referenced in public guidance, which helps confirm the direction and order of magnitude. If a region or end-use vertical showed an unusual jump, the driver assumptions were revisited, and follow-up questions were sent to a small set of respondents to confirm what changed.

Before sign-off, the model goes through a multi-step review where calculations, currency conversions, and year mapping are rechecked, and any outliers are explained in plain terms. The report is refreshed annually, and interim updates are made when material events occur that can shift demand, pricing, or deployment preferences. Right before delivery, a final review pass is done so clients receive the most current view available.

Mordor Intelligence's Managed File Transfer Market Size Versus Other Published Estimates

Published market sizes for managed file transfer often diverge because different studies draw the line around what counts as managed transfer, and they also vary in how they treat services, cloud subscriptions, and multi-year contract value. Timing matters too, since some estimates lock currency rates and assumptions earlier, while others rework inputs closer to the publication date.

The main gap drivers here are usually whether professional services and support are included, how cloud pricing is annualized for multi-tenant plans, and whether adjacent tools like secure content collaboration are mixed into the same bucket. Another common difference comes from the demand pool used for scaling, since some approaches lean heavily on vendor-reported totals, while others start from regulated file exchange needs and validate them through buyer-side checks, which is the approach used here and refreshed through January 2026 by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.46 B (2026) | |

| Global Consultancy A | USD 2.40 B (2025) | Uses a 2025 base year and a longer forecast window, and the published scope does not clearly separate managed transfer platforms from adjacent secure file sharing features, which can shift the starting value. |

| Regional Consultancy B | USD 2.45 B (2025) | Reports a 2025 snapshot and appears to lean on component splits without showing how subscription pricing is annualized across cloud and on-premise, which can create differences when converting contracts into annual revenue. |

Overall, the spread across the three figures is explained more by scope choices and year alignment than by a disagreement on market direction. By tying the total to deployment mix, transfer types, and buyer-side pricing checks, the estimate remains traceable to clear inputs and can be repeated when new adoption or pricing signals show up.

Key Questions Answered in the Report

What is the current value of the managed file transfer market?

The managed file transfer market size stands at USD 2.46 billion in 2026 and is forecast to rise to USD 4.02 billion by 2031.

Which segment is growing quickest by deployment mode?

Cloud-based platforms are expected to grow at a 10.13% CAGR through 2031 as enterprises favor elastic scaling and subscription pricing.

Why is healthcare adoption accelerating?

Interoperability mandates and the FTC’s expanded breach-notification rule push healthcare providers and health-app developers toward audit-ready, encrypted transfer solutions.

What regions will see the fastest growth?

Asia-Pacific is projected to experience the highest 11.46% CAGR, propelled by digital-transformation programs in India, Japan, and Southeast Asia.

How are zero-trust mandates influencing vendor offerings?

Vendors now embed continuous identity verification, device-posture checks, and AI-based anomaly detection, aligning with NIST 800-207 principles to meet insurance and regulatory requirements.

How concentrated is the vendor landscape?

With the top five players controlling roughly 60% of revenue, the market earns a concentration score of 6, denoting moderate consolidation with ample room for challengers.

Page last updated on: