Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

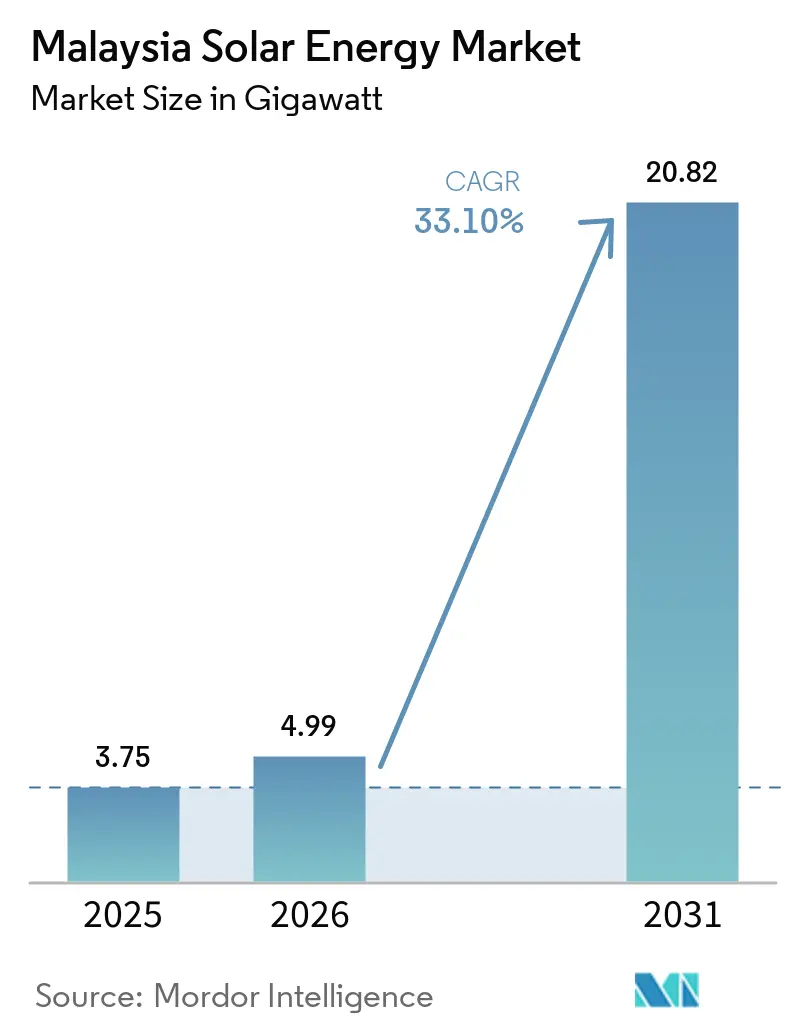

| Base Year Market Size (2025) | 3.75 gigawatt |

| Market Volume (2026) | 4.99 gigawatt |

| Market Volume (2031) | 20.82 gigawatt |

| Growth Rate (2026 - 2031) | 33.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Solar Energy Market Analysis by Mordor Intelligence

The Malaysia Solar Energy Market size is expected to grow from 3.75 gigawatt in 2025 to 4.99 gigawatt in 2026 and is forecast to reach 20.82 gigawatt by 2031 at 33.1% CAGR over 2026-2031.

The growth trajectory places the Malaysia solar energy market among the fastest-expanding clean-power segments in Southeast Asia. Escalating government auction volumes, robust corporate renewable procurement, and persistent cost declines in photovoltaic (PV) equipment anchor this momentum. Utility-scale projects receive predictable offtake through the Large Scale Solar (LSS) mechanism, while Virtual Net Energy Metering (NEM) 3.0 accelerates distributed generation. Intensifying data center expansion in Johor and Selangor further boosts demand for solar-plus-storage solutions that enhance grid flexibility. Competitive intensity remains moderate because local developers collaborate with global suppliers to secure bankable technology and financing on a large scale.

Key Report Takeaways

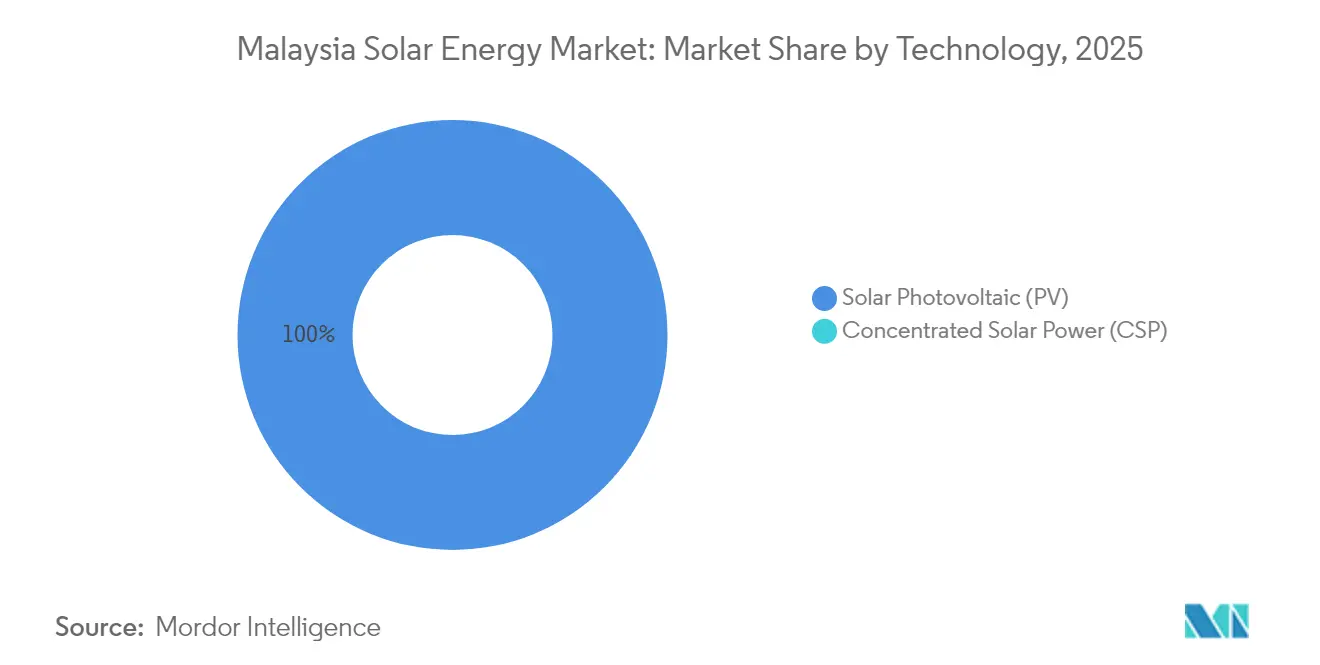

- By technology, solar PV held 100.00% of the Malaysia solar energy market share in 2025 and continues at a 33.1% CAGR through 2031.

- By grid type, on-grid assets accounted for 91.42% of the Malaysian solar energy market size in 2025, while off-grid systems are projected to advance at a 38.1% CAGR to 2031.

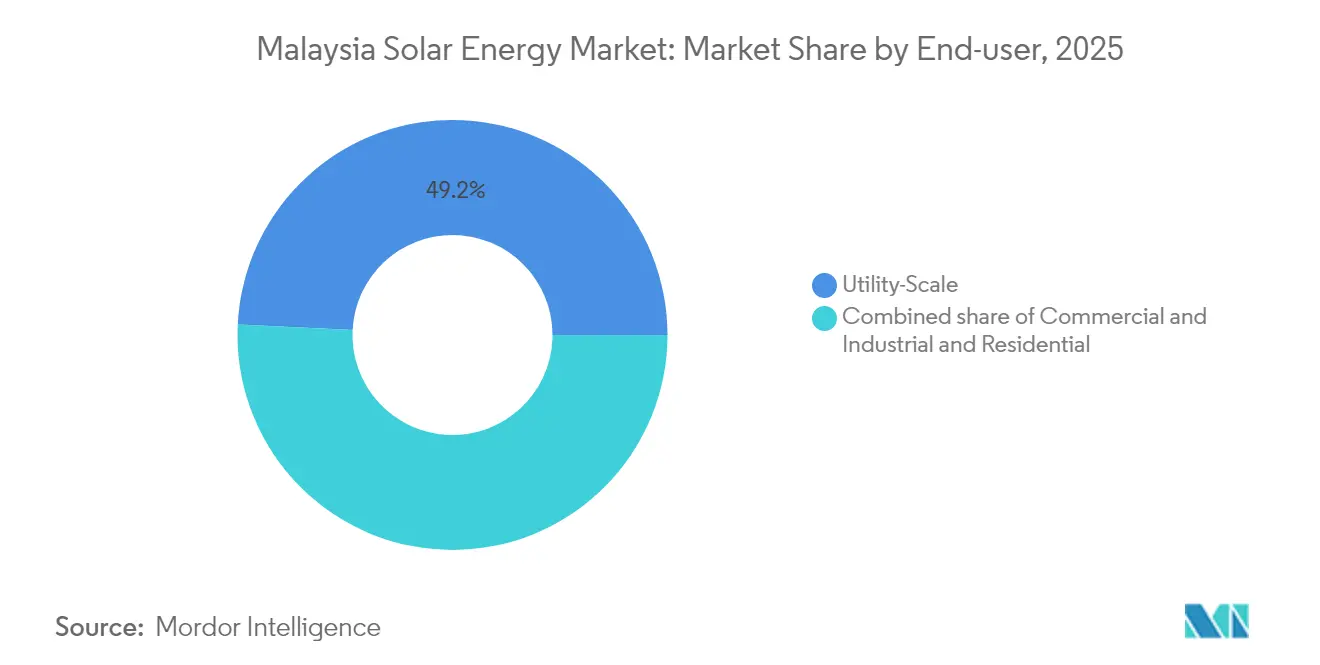

- By end-user, utility-scale projects captured a 49.22% share of the Malaysian solar energy market size in 2025; residential installations are expected to expand at a 36.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government LSS auction expansions | +8.50% | National, Peninsular Malaysia | Medium term (2 - 4 years) |

| Declining PV module costs | +6.20% | Global supply chains | Short term (≤ 2 years) |

| Rising corporate-PPA / RE100 demand | +7.80% | Johor and Selangor | Medium term (2 - 4 years) |

| Data-center power demand spike | +5.90% | Johor and Selangor | Short term (≤ 2 years) |

| Virtual NEM policy roll-out | +4.10% | National | Medium term (2 - 4 years) |

| Reservoir-based floating solar push | +2.40% | Sarawak and Sabah | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government LSS Auction Expansions Drive Market Acceleration

Malaysia continues to enlarge the LSS program, providing transparent capacity pipelines and price discovery that underpin project bankability. LSS5 was awarded 2 GW in 2024 at an average tariff of RM0.1699 per kWh.(1)The Star, “LSS PETRA 5 + Solar Tender to Offer 2 GW Capacity,” thestar.com.my LSS PETRA 5 + aims for another 2 GW in 2025, maintaining competitive pressure on cost while standardizing storage requirements. Predictable scheduling enables developers to secure supply contracts early, mitigate logistics risk, and meet stringent grid-code milestones. The policy lowers regulatory uncertainty and signals long-term commitment that attracts both domestic and foreign direct investment into the Malaysia solar energy market.

Declining PV Module Costs Accelerate Project Economics

A global supply glut led to a nearly 20% decline in module prices in 2024, enabling sub-RM 0.20 per kWh levelized costs at Malaysian utility sites. Cheaper panels shorten payback periods for rooftop adopters,thereby broadening the customer base of the solar energy market in Malaysia. However, U.S. anti-dumping duties on Malaysian exports disrupt manufacturing utilization, creating procurement timing risk that developers must hedge through diversified sourcing strategies. Lower hardware outlays nevertheless outweigh the volatility, reinforcing the competitiveness of new projects.

Rising Corporate PPA and RE100 Demand Transforms Procurement Patterns

Multinational corporations in the electronics and cloud services sectors pursue RE100 commitments, which require the purchase of long-term renewable energy certificates. Microsoft and Google anchor more than 500 MW of prospective solar procurement in Johor and Selangor.(2)The Edge Markets, “Microsoft, Google Investments Boost Johor Data Center Hub Renewable Energy Demand,” theedgemarkets.com The Corporate Renewable Energy Supply Scheme (CRESS) allows direct transactions with developers, creating premium pricing for long-tenor PPAs. Stable, creditworthy counterparties strengthen debt-service coverage ratios, enhancing the investability of the Malaysia solar energy market.

Data Center Power Demand Spike Creates Industrial Anchor Load

Hyperscale facilities necessitate 24/7 high-quality power, catalyzing hybrid solar and storage configurations that mitigate intermittency. Microsoft’s USD 2.2 billion cloud investment translates into renewable energy requirements exceeding 300 MW in Johor. Concentrated demand justifies grid-reinforcement projects and unlocks economies of scale for adjacent solar parks. Strong baseload contracts reduce merchant risk and tilt project finance terms in favor of Malaysia renewable energy developers within the solar energy in malaysia market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in Peninsular grid | -4.70% | Peninsular Malaysia | Short term (≤ 2 years) |

| High financing cost for rooftop SME projects | -3.20% | National SME sector | Medium term (2 - 4 years) |

| Land-use conflicts with agriculture | -2.10% | Rural plantation zones | Long term (≥ 4 years) |

| Import-supply volatility for PV modules | -2.80% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Congestion in Peninsular Grid Constrains Integration Capacity

Transmission capacity has not kept pace with the rapid expansion of solar energy. Tenaga Nasional Berhad has earmarked RM 10.3 billion until 2030 for grid modernization, yet the roll-out lags behind near-term connection requests. Peak PV output coincides with mid-day industrial lulls, aggravating reverse-flow constraints that prompt curtailment. Developers increasingly add storage or clusters near load centers to mitigate bottlenecks, but systemic relief hinges on timely transmission upgrades that sustain the growth of the solar energy in malaysia market.

High Financing Cost for Rooftop SME Projects Limits Market Penetration

Banks frequently demand personal guarantees and collateral, which pushes loan rates for SME solar projects above 6%. Lengthy permitting processes increase soft costs, eroding the economic case for smaller rooftops, even when tariffs support self-consumption. The absence of direct subsidies for SMEs contrasts with residential rebates, narrowing the addressable deployment in the solar energy market in malaysia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Maintains Complete Market Dominance

Solar PV held 100.00% of Malaysia's solar energy market share in 2025, underscoring its entrenched position as the only commercially deployed technology. Robust irradiation of 4.5-5.5 kWh/ m² /m²/day permits capacity factors that keep levelized costs below grid parity. The Malaysia solar energy market size for PV is projected to climb at a 33.1% CAGR through 2031, reflecting proven performance, abundant local assembly, and streamlined permitting. No concentrated solar power (CSP) ventures entered planning because direct normal irradiance falls short of economic thresholds, and higher capital intensity dampens appetite.

Local module assembly by JinkoSolar and LONGi reduces shipping lead times and hedges currency fluctuation, improving cost certainty for developers. Bankability gains further traction from the Sejingkat 60 MW / 80 MWh battery project, which validates hybrid PV-storage for frequency regulation. Energy Commission grid codes mandate IEC compliance and advanced inverter functionality, elevating quality while ensuring PV assets integrate safely into the Malaysia solar energy market.

By Grid Type: Off-Grid Acceleration Despite On-Grid Dominance

On-grid arrays captured 91.42% of Malaysia's solar energy market share in 2025, as LSS auctions and corporate PPAs channel investments into utility-scale nodes. Grid-connected projects hedge merchant risk through fixed tariffs or long-term indexation, facilitating project finance structures that attract multilaterals and local banks. Off-grid installations nonetheless register a 38.1% CAGR through 2031 as storage prices fall and remote loads seek diesel displacement. Sabah's 100 MW / 400 MWh storage complex exemplifies standalone resilience and underscores the scalability of off-grid hybrid systems.

Telecom towers, mining camps, and island communities are increasingly selecting modular solar-plus-battery packages that deliver round-the-clock power without requiring fuel logistics. Simplified licensing for systems below 1 MW accelerates deployment, and digital monitoring platforms lower operations costs. Together, these factors broaden participation and diversify revenue across the Malaysia solar energy market.

By End-User: Residential Growth Outpaces Utility-Scale Leadership

Utility-scale plants accounted for 49.22% of Malaysia's solar energy market share in 2025, driven by 2 GW of LSS5 awards that underpin multi-year construction backlogs. Bankable PPAs, land aggregation expertise, and EPC economies of scale continue to make utility projects the largest revenue pool. Residential rooftops, however, are projected to record a 36.7% CAGR to 2031, supported by the SolaRIS rebate and the Virtual NEM bump in export tariffs.

Urban homeowners adopt 3-7 kW arrays to counter rising retail electricity tariffs, while digital financing portals streamline the application and loan approval process. Commercial and Industrial rooftops lag because SMEs often pay higher interest rates and frequently lease property, which complicates collateralization. Even so, sustained policy support positions residential uptake as a vital pillar of the Malaysia solar energy market.

Geography Analysis

Peninsular Malaysia accounts for the bulk of existing capacity owing to mature transmission links and concentrated industrial demand. Northern states obtain superior irradiation but face transfer constraints that require grid upgrades before additional gigawatts can interconnect. Johor emerges as a marquee growth hub near Singapore, leveraging hyperscale data-center clusters that lock in multi-decade solar PPAs. Microsoft’s and Google’s combined commitments surpass 500 MW, catalyzing ancillary investments in substations and battery storage. These anchor loads establish economies of scale that ripple throughout the Malaysia solar energy market.

Selangor commands another expansion front because its manufacturing base seeks renewable electricity to satisfy export supply-chain audits. Despite limited land, developers repurpose industrial rooftops and quarry sites to sidestep land-use friction. Grid congestion persists in select districts, yet Tenaga Nasional’s modernization plan aims to relieve chokepoints by 2027. Success will recalibrate project siting decisions and influence risk premiums embedded in the Malaysia solar energy market.

The East Malaysian states of Sabah and Sarawak chart a differentiated pathway, anchored in off-grid and floating concepts. Sarawak Energy’s 50 MW reservoir array at Batang Ai demonstrates water-borne feasibility, complementing hydropower dispatch and mitigating evaporation losses. Sabah’s hybrid solar-storage programs show how large batteries provide reserve margin on weak grids while displacing imported diesel. Cross-border electricity trading via the Enegem platform lays the groundwork for an ASEAN green-power corridor, extending the commercial reach of the Malaysia solar energy market.

Competitive Landscape

No single developer controls a commanding share, yielding a moderate concentration profile that fosters innovation. Local EPCs, such as Solarvest Holdings, Cypark Resources, and Samaiden Group, leverage in-country permitting expertise to secure LSS quotas, while global suppliers like JinkoSolar, First Solar, and Canadian Solar provide high-efficiency modules and warranty backing. Partnerships multiply: Solarvest teams with Huawei to co-package inverters and storage, whereas Plus Xnergy couples with Leader Energy to pilot sodium-sulfur batteries.(5)The Edge Markets, “Solarvest-Huawei Partnership Advances Solar Storage Integration,” theedgemarkets.com These alliances raise technical ceilings and diffuse risk across the Malaysia solar energy market.

Cost competitiveness remains the primary award metric under LSS tenders; yet, developers increasingly differentiate themselves through storage expertise, floating installations, and green financing credentials. The first 98 MW floating project by Cypark validates alternate siting and signals new service revenue for O&M players. JinkoSolar’s 2 GW Malaysian production expansion underscores localization trends that cut lead times while hedging currency swings. Financing structures are diversifying, with Islamic green sukuk and blended-finance vehicles lowering the weighted average cost of capital in the Malaysian solar energy market.

International entrants eye merchant export to Singapore as the Energy Exchange Malaysia matures, providing fresh offtake paths. Domestic incumbents respond by scaling land banks and pre-qualifying multi-technology pipelines. On balance, moderate fragmentation incentivizes service quality, technology upgrades, and aggressive tariff bidding, which benefit end-users and accelerate the Malaysian solar energy market.

Malaysia Solar Energy Industry Leaders

JA SOLAR Technology Co.,Ltd.

Solarvest Holdings Berhad

TNB Engineering Corporation Sdn. Bhd.

Canadian Solar Inc.

Plus Xnergy Holding Sdn. Bhd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Tenaga Nasional Berhad has announced a RM 10.3 billion (USD 2.3 billion) grid modernization program spanning 2030 to support the integration of renewable energy and address transmission constraints in Peninsular Malaysia.

- September 2024: Malaysia launched the LSS PETRA 5+ auction program, targeting a 2 GW solar capacity allocation for 2025 deployment, following the successful completion of LSS5, which awarded 2 GW of capacity.

- August 2024: Sarawak Energy commissioned Malaysia's first large-scale 60 MW/80 MWh battery energy storage system (BESS) in Sejingkat, demonstrating the benefits of grid stability and enabling higher penetration of renewable energy.

- July 2024: Sabah Electricity commissioned a 100 MW/400 MWh BESS project in partnership with Sungrow, representing the largest utility-scale energy storage installation in East Malaysia.

- June 2024: Malaysia Energy Exchange (Enegem) launched a cross-border electricity trading platform, enabling the exchange of renewable energy certificates between Malaysia, Singapore, and other ASEAN markets.

Malaysia Solar Energy Market Report Scope

Solar energy refers to the energy obtained from the sun that is converted into thermal or electrical energy by using technologies such as solar photovoltaic panels and concentrating solar-thermal power (CSP). Solar heating and cooling are well-established technologies in renewable energy ecosystems. Solar energy is an environmentally friendly and sustainable technology.

The Malaysian solar energy market is segmented by end-user. By end-user, the market is segmented into residential, commercial & industrial (C&I), and utility. For each segment, market sizing and forecasts have been done based on installed capacity (MW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

What is the forecast size of Malaysia’s solar sector by 2031?

Installed capacity is projected to reach 20.82 GW by 2031, expanding from 4.99 GW in 2026.

How fast is solar growing in Malaysia?

The market is expected to log a 33.1% CAGR between 2026 and 2031.

Which policy mechanism drives most new large-scale projects?

The Large Scale Solar auction program provides predictable offtake and price discovery for utility-scale developers.

Why is residential solar adoption accelerating?

Virtual NEM 3.0 export credits combined with the SolaRIS rebate shorten payback periods to fewer than five years.

How do data centers influence solar demand in Malaysia?

Hyperscale facilities in Johor and Selangor require hundreds of megawatts of renewable power, anchoring long-term PPAs that boost solar deployment.

What role does energy storage play in Malaysia’s solar build-out?

Battery projects such as the 60 MW / 80 MWh BESS at Sejingkat enhance grid stability and allow higher penetration of variable photovoltaics.

Page last updated on: