Malaysia Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

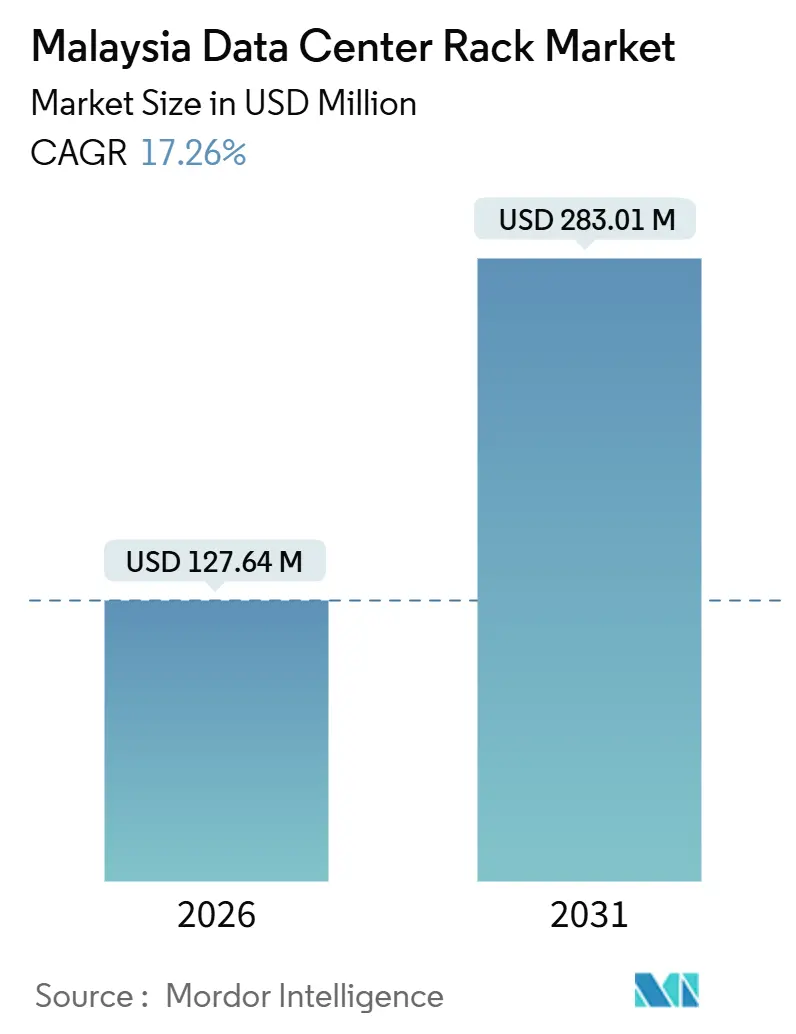

| Market Size (2026) | USD 127.64 Million |

| Market Size (2031) | USD 283.01 Million |

| Growth Rate (2026 - 2031) | 17.26% CAGR |

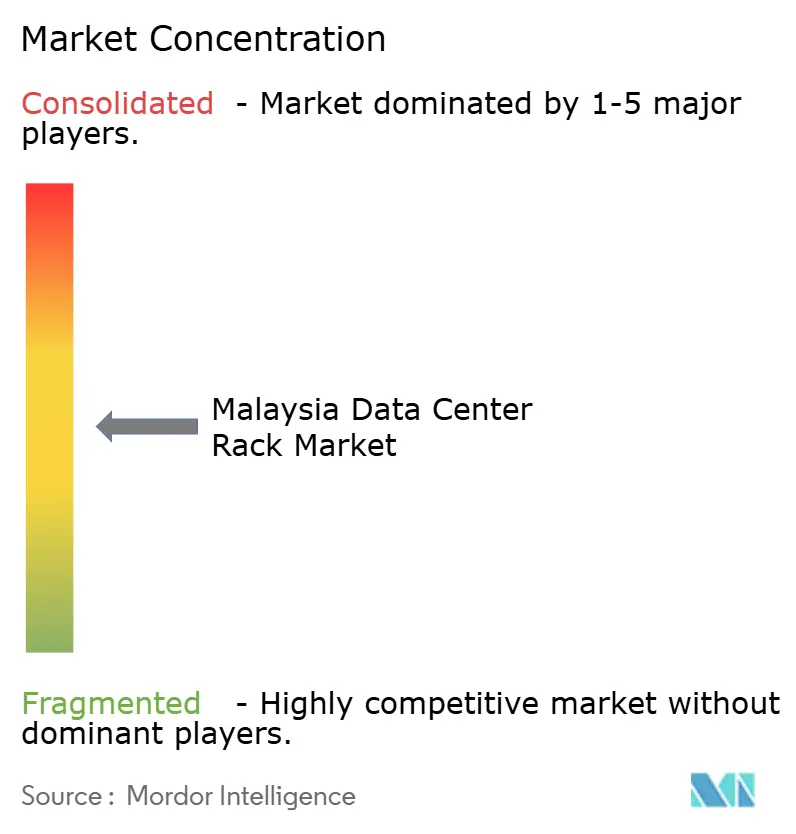

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Data Center Rack Market Analysis by Mordor Intelligence

The Malaysia data center rack market size stands at USD 127.64 million in 2026 and is projected to reach USD 283.01 million by 2031, growing at a 17.26% CAGR. The acceleration of the Malaysia data center rack market is closely tied to USD 16 billion in hyperscale cloud pledges, the diffusion of artificial intelligence (AI) workloads that demand 30 kilowatt-plus rack densities, and government data-localization mandates that force in-country deployments. New capacity requests emphasize enclosed cabinets that integrate liquid cooling, hot-aisle containment, and smart power distribution, allowing operators to triple compute density within the same footprint. Simultaneously, edge data centers positioned at 5G tower sites are stimulating demand for half-rack and wall-mount formats that tolerate temperature swings of more than 20 degrees Celsius. Competitive differentiation is shifting from basic sheet-metal fabrication toward rack-level telemetry, predictive maintenance analytics, and integrated leak-detection, enabling suppliers to limit unplanned downtime and lower total cost of ownership.

Key Report Takeaways

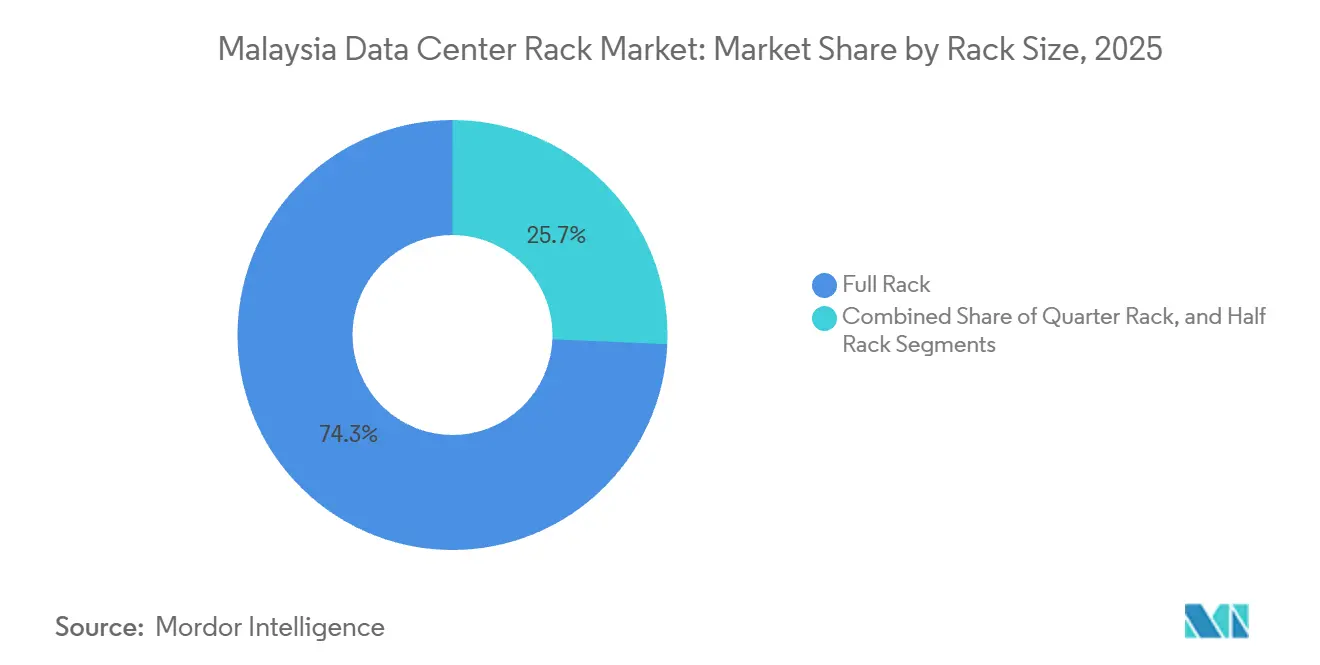

- By rack size, full racks captured 74.32% revenue share in 2025, while half racks are forecast to expand at an 18.53% CAGR through 2031.

- By rack type, enclosed cabinets accounted for 79.33% of 2025 revenue and are advancing at an 18.47% CAGR through 2031.

- By tier type, Tier 3 facilities led with 56.21% demand share in 2025, but Tier 4 infrastructure is pacing the field with an 18.12% CAGR as financial services and government agencies pursue fault-tolerant designs.

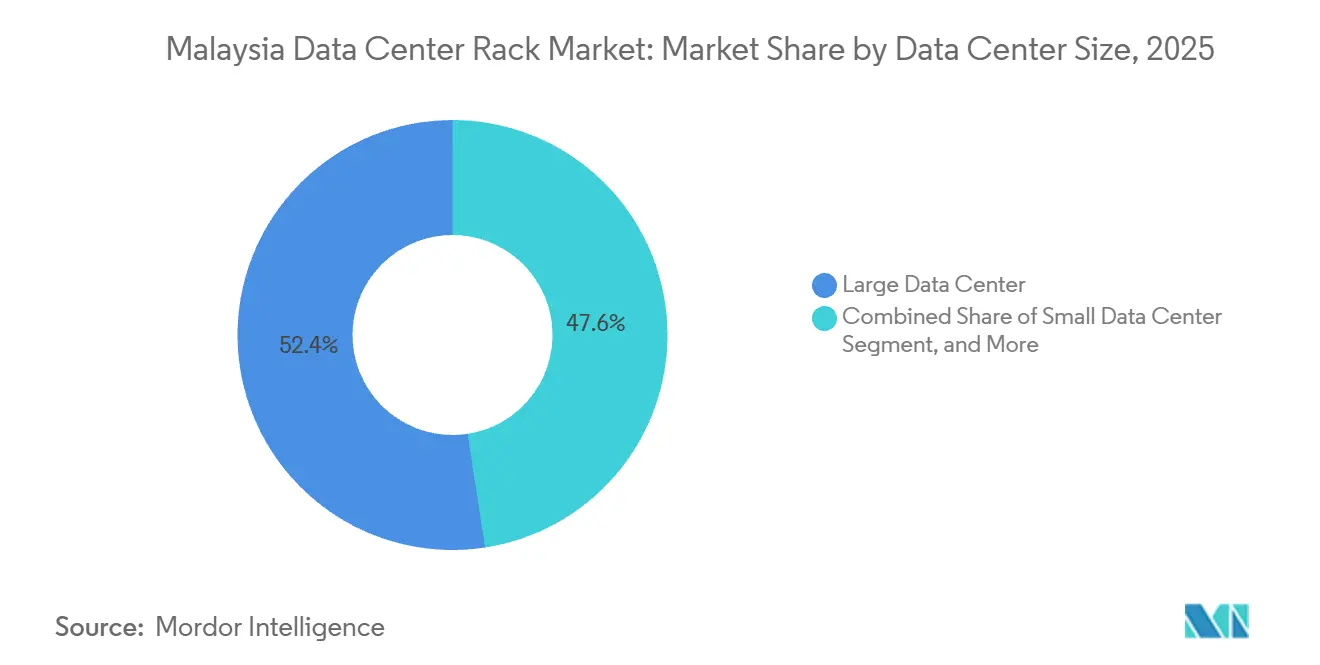

- By data center size, large facilities accounted for 52.42% of 2025 revenue, yet hyperscale sites above 100 megawatts are expanding at an 18.71% CAGR through 2031.

- By data center type, colocation maintained a 51.53% share in 2025, although hyperscalers and cloud service providers are growing fastest at an 18.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia represents one dimension of a structure that spans multiple countries, continents and economic zones. Our global data center rack market report covers details on that full structure.

Malaysia Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cloud and Hyperscale Investments | +5.2% | National, concentrated in Klang Valley and Johor | Medium term (2-4 years) |

| Surge in AI Workloads Requiring High-Density Racks | +4.1% | National, with early adoption in Cyberjaya and Iskandar | Medium term (2-4 years) |

| Government Data-Localization Policies and MSC 3.0 Incentives | +3.3% | National, strongest in MSC Malaysia designated zones | Long term (≥ 4 years) |

| Rising Dominance of the 5G Network | +2.8% | National, with urban-rural gradient | Short term (≤ 2 years) |

| Fiber Connectivity Network Expansion | +1.4% | National, prioritizing underserved regions | Medium term (2-4 years) |

| Expansion of Edge Data Centers Along Rural Telco Towers | +1.2% | Rural and semi-urban areas, Sabah and Sarawak | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud and Hyperscale Investments

Malaysia hosts more than USD 16 billion in announced cloud and AI allocations from Amazon Web Services, Google Cloud, Microsoft, and Oracle.[1]Amazon Web Services, “AWS Announces Plans for New AWS Region in Malaysia,” aws.amazon.com Each hyperscaler specifies repeatable rack bills of materials, integrating 400-gigabit spine switches, liquid-cooling manifolds, and advanced cable management that enable 30-kilowatt-plus densities while reducing installation labor by 20%. Pre-negotiated volume commitments shorten procurement cycles for rack vendors, but they also compress hardware margins because hyperscalers benchmark every sub-assembly against open-source alternatives. The scale of these commitments elevates the Malaysia data center rack market to first-tier status within Southeast Asia, encouraging local subsidiaries of global banks to migrate latency-sensitive workloads from Singapore to Cyberjaya. Regional supply chains respond by qualifying new sheet-metal fabricators in Johor and Penang, thereby lowering freight costs and creating a diversified vendor base. As new cloud regions enter service, hyperscalers are pivoting toward renewable-sourced power purchase agreements, indirectly boosting demand for rack controllers that report real-time energy consumption and carbon intensity.

Surge in AI Workloads Requiring High-Density Racks

Artificial intelligence training clusters shift rack power budgets from 10 kilowatts to 150 kilowatts, forcing operators to adopt direct-to-chip or rear-door heat-exchanger cooling. STT GDC implemented 150 kilowatt racks in Cyberjaya and achieved a partial power usage effectiveness of 1.15. [2]Source: STT Global Data Centres, “Malaysia Data Centers,” sttelemediagdc.com Hewlett Packard Enterprise offers fanless liquid cooling that lowers carbon emissions by 90% relative to air-cooled configurations. Supermicro’s DLC-2 coolant distribution unit accommodates 250 kilowatts per rack, delivering 40% energy savings. These breakthroughs compel rack manufacturers to redesign enclosures with leak-detection channels, redundant quick-disconnect couplings, and manifold mounting rails, adding 30% to 50% to the bill of materials but enabling operators to triple compute density per square meter. Because AI workloads require deterministic thermal response, suppliers embed fiber-optic temperature sensors that provide sub-millisecond feedback, ensuring graphics processing units remain within safe junction thresholds during rapid load swings.

Government Data-Localization Policies and MSC 3.0 Incentives

Malaysia’s data-localization rules mandate in-country storage of sensitive financial, healthcare, and public-sector data, while the MSC 3.0 framework offers 10-year tax holidays and import-duty waivers on data-center equipment. [3]Source: Malaysia Digital Economy Corporation, “Malaysia Digital Catalytic Programs,” mdec.my These incentives cut the total cost of ownership by as much as 20% compared with jurisdictions lacking similar concessions, and they tilt procurement toward enclosed cabinets that simplify compliance audits by segregating tenant hardware at the rack level. Operators such as AIMS and STT GDC expanded their campuses to 50 megawatts and 130 megawatts, respectively, explicitly citing MSC 3.0 as a determinant for capacity allocation. Equinix’s KL1 data center in Cyberjaya, designed for 900 cabinets, aligns with financial services compliance needs by integrating biometric rack-level access controls. Although localization is clear for banking data, ambiguity persists for AI model training traffic, prompting hybrid architectures that mirror datasets across Malaysia and Singapore. This dual-site strategy inflates rack demand because every replicated workload requires a redundant enclosure.

Rising Dominance of the 5G Network

Digital Nasional Berhad achieved 80% population coverage for 5G by end-2024, and U Mobile switched on Malaysia’s second 5G network in January 2025. Ultra-low-latency applications, including autonomous vehicles and smart manufacturing, hinge on edge micro-data centers positioned at tower sites. EdgePoint Infrastructure, working with CelcomDigi, deploys half-rack enclosures fortified against humidity and temperature spikes exceeding 20 degrees Celsius. Although revenue per rack at edge sites is 40% lower than in centralized colocation hubs, the nationwide 5G build-out compels operators to standardize on ruggedized, pre-integrated enclosures that cut field installation time from two days to four hours. Rack suppliers now bundle remote-management firmware, environmental sensors, and anti-vibration mounts, enabling one technician to commission an edge site rather than the three previously required.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delays in Power-Grid Upgrades Causing Deployment Bottlenecks | -2.1% | Klang Valley, Cyberjaya, Shah Alam | Short term (≤ 2 years) |

| Low Availability of Skilled Data-Center Personnel | -1.7% | National, acute in Tier 2 cities | Medium term (2-4 years) |

| Increasing Cybersecurity Threats and Ransomware | -0.9% | National, concentrated in colocation and enterprise segments | Medium term (2-4 years) |

| Escalating Land Prices in the Klang Valley Corridor | -0.8% | Klang Valley, Cyberjaya, Shah Alam, Selangor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Delays in Power-Grid Upgrades Causing Deployment Bottlenecks

Tenaga Nasional Berhad forecasts data-center electricity demand of 5,000 megawatts by 2035, yet substation upgrades in Cyberjaya and Shah Alam lag behind capacity reservations. Operators report 18- to 24-month lead times for new grid connections above 10 megawatts, forcing phased builds and inflating financing costs. Some facilities now rely on diesel or battery systems that raise operating expenses by 15%. The shortfall is most acute for AI-oriented racks pulling 150 kilowatts, which require dedicated feeders that legacy switchgear cannot accommodate. Johor benefits from prioritized substation construction tied to the Iskandar economic zone, motivating hyperscalers to shift builds southward and, in turn, concentrate future rack shipments in that region.

Low Availability of Skilled Data-Center Personnel

Malaysia faces a gap of 60,000 engineers and 26,430 cybersecurity practitioners, limiting the pace at which operators can deploy advanced racks integrating liquid cooling, 400 gigabit networks, and predictive maintenance software. Huawei’s training center certified 2,000 specialists in 2024, yet courses skew toward application development rather than infrastructure. Attrition rates top 20% as hyperscale cloud providers offer salaries 40% above colocation norms, leaving mid-tier operators understaffed. As a workaround, rack vendors bundle turnkey installation and 24/7 monitoring into lease agreements, effectively outsourcing expertise and allowing facilities teams to focus on customer-facing service-level agreements instead of component-level maintenance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Edge-Optimized Half Racks Accelerate Adoption

Full racks remain the backbone of hyperscale campuses, accounting for 74.32% of 2025 shipments, but the Malaysia data center rack market sees half-rack units growing at an 18.53% CAGR through 2031 as operators extend compute to mobile-edge locations. Within the Malaysia data center rack market size for rack size segmentation, half racks will command an expanding share as tower-based micro-data centers support 5G backhaul and real-time analytics. EdgePoint Infrastructure’s deployments with CelcomDigi validate modular half-rack economics because ruggedized cabinets withstand temperature oscillations while keeping power budgets under 5 kilowatts.

Second-generation half racks integrate uninterruptible power supplies, 1.5 kilowatt lithium-ion battery packs, and energy-harvesting sensors, reducing site visits and shrinking total cost of ownership by 25%. Quarter racks remain below 10% share but are finding use in retail outlets and factory floors where on-premises inference accelerates camera-based quality-inspection workflows. Supermicro’s GB200 NVL72 packs 72 graphics processing units in one full rack, prompting operators to redesign floor plans to accommodate heat-exchanger corridors rather than expand gross square footage. Vendors compete by offering accessories such as sliding rail kits, cable-chain escorts, and adjustable depth frames, enabling half racks to accept diverse server chassis without field re-machining.

By Rack Type: Enclosed Cabinets Anchor Thermal Efficiency

Enclosed cabinets generated 79.33% of rack-type revenue in 2025 within the Malaysia data center rack market and are forecast to sustain an 18.47% CAGR. They dominate because hyperscale tenants demand hot-aisle containment, door-perforation patterns exceeding 80% open area, and adaptive airflow baffles that curtail parasitic cooling losses by as much as 25%. The Malaysia data center rack market share for enclosed cabinets will edge higher as operators retrofit liquid cooling manifolds that require sealed frames to avoid condensation.

Open-frame racks, favored by universities and engineering labs for accessibility, held about 15% share but cannot accommodate direct-liquid-cooling loops. Wall-mount formats, though under 6% share, grow at 16.8% because small and medium retailers deploy point-of-sale servers in tamper-proof enclosures. Schneider Electric’s NetShelter uses tool-less cable-management arms and rear-door heat exchangers that dissipate 80% of rack exhaust before entering the hot aisle. Vertiv and Rittal now embed vibration sensors and thermal imaging modules that flag impending fan failures, decreasing unplanned downtime by 30%. These intelligence layers transform the Malaysia data center rack market from a commodity steel segment into a platform for data-driven operations.

By Tier Type: Tier 4 Proliferates Across Financial Workloads

Tier 3 facilities provided 56.21% of rack placements in 2025, delivering 99.982% uptime, yet Tier 4 sites expand at an 18.12% CAGR as regulatory expectations tighten. As a result, the Malaysia data center rack market size for Tier 4 sites will move from single digits toward a more material share by 2031. Irix’s Kuching 1 achieved the country’s first Tier IV Constructed Facility certification, demonstrating that Tier 4 economics are tenable in lower-cost regions outside Kuala Lumpur.

Bank Negara Malaysia risk guidelines reference Tier standards, pushing banks to migrate core workloads into 2N + 1 redundant environments. Rack suppliers respond with Tier 4-ready enclosures that incorporate dual power rails, redundant network trunks, and seismic bracing compliant with IEC 60068-2-6. Although capital cost per rack rises 30%, operators command premium rentals, preserving payback periods below four years. Tier 1 and Tier 2 footprints continue shrinking as legacy rooms undergo refurbishment or decommissioning.

By Data Center Size: Hyperscale Wave Redefines Procurement

Large facilities between 10 and 50 megawatts represented 52.42% of revenue in 2025, but hyperscale campuses exceeding 100 megawatts are expanding at an 18.71% CAGR. The Malaysia data center rack market size for hyperscale builds will therefore outpace other size classes. Amazon Web Services, Google Cloud, Microsoft, and Oracle each mandate Open Compute Project-compatible frames, compressing vendor shortlists to suppliers certified under the OCP program.

These hyperscale orders prioritize 400 gigabit network backplanes and factory-installed bus-bar power distribution, shrinking installation time by 40%. Medium sites between 5 and 10 megawatts, often serving regional enterprises, grow at 16.9% CAGR as government agencies pursue dedicated footprints outside public cloud. Small data centers under 5 megawatts, usually embedded in manufacturing zones, remain niche but essential for latency-sensitive control loops. Rack suppliers triage production slots, favoring hyperscale orders that improve utilization, thereby lengthening lead times for smaller buyers.

By Data Center Type: Colocation Holds Share While Hyperscalers Surge

Colocation operators captured 51.53% of rack revenue in 2025, delivering multi-tenant environments with economies of scale, yet hyperscaler and cloud service provider segments post an 18.82% CAGR, reflecting direct investment in single-tenant builds. Consequently, the Malaysia data center rack market continues its shift toward provider-owned campuses optimized for AI training. Colocation firms such as AIMS and STT GDC counter by bundling cross-connect ecosystems, regulatory compliance audits, and remote-hands services that hyperscalers often self-perform.

Enterprise and edge deployments, accounting for roughly 30% share, grow in tandem with 5G and fiber expansion as manufacturers embed micro-data centers on factory floors. Rack vendors now maintain dual product lines, custom OCP variants for hyperscalers and ruggedized, pre-integrated models for edge sites. This bifurcation intensifies competition, rewarding suppliers that master configuration flexibility and rapid fulfillment.

Geography Analysis

Klang Valley, encompassing Cyberjaya, Shah Alam, and Selangor, clusters more than 60% of national rack installations, anchored by AIMS’s 50 megawatt campus, Equinix’s 900-cabinet KL1 site, and NTT’s Cyberjaya 5 facility with 80 kilowatt rack cooling envelopes. Land prices in Cyberjaya and Shah Alam have escalated 15%-20% per year since 2024, prompting developers to consider Johor, Penang, and Melaka for expansion. Telekom Malaysia and Singtel Nxera’s 20-megawatt Johor build illustrates the state’s emergence as a hyperscale alternative, leveraging prioritized substation access and proximity to Singapore to achieve sub-10-millisecond fiber latency.

Penang and Melaka attract edge facilities linked to electronics and medical device manufacturing clusters, yet fiber density remains patchy, prompting operators such as TIME dotCom and TNB Allo to extend backbone routes. Sabah and Sarawak are frontier markets, where 5G tower upgrades are driving demand for half-rack enclosures capable of rugged outdoor operation. However, shipment lead times to East Malaysia run four to six weeks, compelling rack vendors to hold higher safety stock, which inflates working capital requirements by roughly 12 days of inventory.

Johor’s adjacency to Singapore offsets the island’s land scarcity and carbon caps, making it a magnet for hyperscale overflow. Iskandar’s economic zone incentives reduce development fees, which, combined with power discounts, lower operating costs by an estimated 18% compared to the Klang Valley. As projects converge on Johor’s shores, the Malaysia data center rack market enjoys a geographic rebalancing that diversifies risk and broadens supplier ecosystems. Nonetheless, developers must navigate planning approvals that can stretch nine months and resolve cross-border cabling permits with Singaporean authorities.

Mordor Intelligence tracks the data center rack market across other major regions such as Africa, Middle East, and South America, with additional country-level coverage spanning New Zealand, Australia, South Africa, Saudi Arabia, Brazil, and Belgium, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Global suppliers, including Schneider Electric, Eaton, Vertiv, and Rittal, control a majority of high-density shipments, yet the Malaysia data center rack market remains moderately fragmented because local fabricators such as GV Industries and Great Rack Sdn Bhd provide faster customization for Tier 2 and Tier 3 facilities. Schneider Electric and Eaton leverage entrenched relationships with AIMS, Equinix, and NTT to place NetShelter and server-rack lines, bundling environmental sensors and cloud dashboards that cut mean-time-to-repair by 25%. Hyperscalers increasingly specify Open Compute Project designs to standardize power buses and mechanical tolerances, eroding proprietary differentiation.

Liquid cooling defines the new competitive frontier. STT GDC’s adoption of direct-to-chip cooling at 150 kilowatts per rack sets a performance benchmark, while Hewlett Packard Enterprise’s fanless architecture lowers operational carbon by 90%. Supermicro’s DLC-2 unit supports 250 kilowatts and achieves 40% power savings, aligning with AI cluster requirements. Vendors that integrate leak-detection tubing, quick-release couplers, and rear-door heat exchangers into turnkey racks capture hyperscale contracts, whereas purely air-cooled frames find relegation to legacy rooms.

Edge deployments open white-space opportunities for ruggedized, pre-integrated enclosures shipping in ISO-type containers. These units collapse site commissioning from days to hours and embed 48-volt DC power paths that reduce conversion losses. Local fabricators differentiate by offering corrosion-resistant coatings and rapid paint-line turns, but they struggle to finance the computational fluid dynamics modeling needed for 150 kilowatt AI loads. Consequently, the Malaysia data center rack market displays a tug-of-war between global engineering prowess and regional agility, with buyers selecting suppliers on a project-by-project basis rather than signing multi-year exclusives.

Malaysia Data Center Rack Industry Leaders

Eaton Corporation

Schneider Electric SE

Vertiv Group Corp.

Black Box Corporation

Dell Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Amazon Web Services obtained regulatory clearance for its first Malaysia cloud region, unlocking new hyperscale rack demand aligned to 2026 commissioning schedules.

- February 2025: Irix’s Kuching 1 facility earned Malaysia’s inaugural Tier IV Constructed Facility certificate, elevating Sarawak’s profile for mission-critical hosting.

- January 2025: U Mobile activated the country’s second 5G network, extending ultra-low-latency coverage to rural zones and stimulating tower-based half-rack orders.

- November 2024: STT GDC completed nationwide deployment of direct-to-chip liquid cooling, delivering 150 kilowatt racks with energy savings up to 30%.

Malaysia Data Center Rack Market Report Scope

A data center rack is a physical enclosure made up of usually steel housing electronic framework. It is designed to house servers, networking and communication devices, cables, and other data center computing peripherals.

The Malaysia Data Center Rack Market Report is Segmented by Rack Size (Quarter Rack >11U, Half Rack 12-22U, and Full Rack ≥42U), Rack Type (Enclosed Cabinet, Open-Frame, and More), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge), and Country. Market Forecasts are Provided in Terms of Value (USD).

| Quarter Rack |

| Half Rack |

| Full Rack |

| Enclosed Cabinet |

| Open-Frame |

| Wall-Mount and Micro-Edge Enclosure |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| By Rack Size | Quarter Rack |

| Half Rack | |

| Full Rack | |

| By Rack Type | Enclosed Cabinet |

| Open-Frame | |

| Wall-Mount and Micro-Edge Enclosure | |

| By Tier Type | Tier 1 and 2 |

| Tier 3 | |

| Tier 4 | |

| By Data Center Size | Small Data Center |

| Medium Data Center | |

| Large Data Center | |

| Hyperscale Data Center | |

| By Data Center Type | Colocation Data Center |

| Hyperscalers Data Center/CSPs | |

| Enterprise and Edge Data Center |

Key Questions Answered in the Report

What is the projected value of the Malaysia data center rack market in 2031?

The market is forecast to reach USD 283.01 million by 2031.

Which rack size category is expected to grow fastest through 2031?

Half racks spanning 12U to 22U are projected to post an 18.53% CAGR.

Why are enclosed cabinets preferred over open-frame racks in Malaysia?

Enclosed cabinets deliver superior thermal containment, support liquid cooling, and align with hyperscale specification requirements.

How are power-grid delays affecting rack deployments?

Slow substation upgrades extend connection lead times up to 24 months, forcing phased builds and temporary reliance on onsite generation.

Page last updated on: