Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Singapore Data Center Rack Market is Segmented by Rack Size (Quarter Rack, Half Rack, Full Rack), by Rack Height (42U, 45U, 48U, Other Heights (≥52U and Custom), Rack Type (Cabinet (Closed) Racks, Open-Frame Racks, Wall-Mount Rack), Data Center Type (Colocation Facilities and More), Material (Steel and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

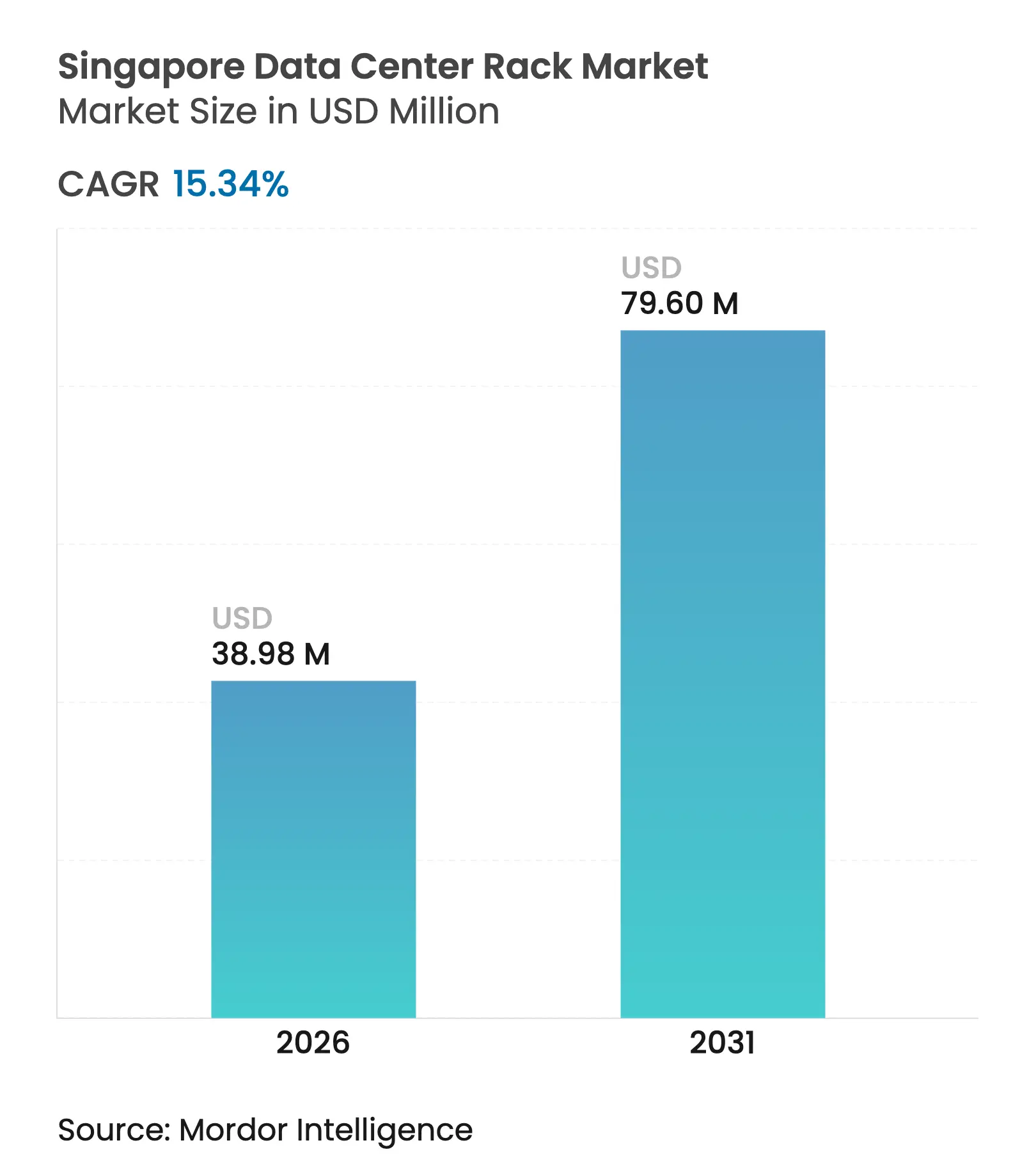

| Market Size (2026) | USD 38.98 Million |

| Market Size (2031) | USD 79.6 Million |

| Growth Rate (2026 - 2031) | 15.34 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Singapore data center rack market size was valued at USD 33.8 million in 2025 and estimated to grow from USD 38.98 million in 2026 to reach USD 79.6 million by 2031, at a CAGR of 15.34% during the forecast period (2026-2031). The growth trajectory reflects the city-state’s Smart Nation 2.0 program, which earmarked SGD 120 million (USD 89 million) for AI infrastructure, together with the post-moratorium allocation of 300 MW of green energy capacity to new facilities. [3]Rich Miller, “Singapore Lifts Moratorium With 300MW Green Quota,” datacenterfrontier.com Accelerated nationwide 5G coverage achieved in mid-2025, combined with ubiquitous fiber backhaul, is stimulating edge-computing deployments that require specialized racks capable of operating in non-traditional environments.[1]Smart Nation and Digital Government Office, “Smart Nation 2.0,” pmo.gov.sgRack demand is also elevated by sovereign-cloud mandates that compel banking and healthcare operators to keep sensitive workloads onshore. Against this backdrop, hyperscale providers are standardizing full-height enclosures to host high-density AI clusters, while sustainability rules are steering purchasing toward liquid-cooling-ready designs. [2]International Trade Administration, “Singapore – Telecommunications Equipment and Services,” commerce.gov

Key suppliers, notably Schneider Electric and Vertiv, are consolidating share by bundling racks with integrated power and cooling subsystems that address Singapore’s tropical climate and strict carbon-reduction policies. Cabinet formats dominate because enclosed frames facilitate airflow containment, physical security and sensor-based monitoring. Meanwhile, aluminum frames are gaining momentum as operators seek lighter weight and higher thermal conductivity for 60-120 kW AI racks. Cyber-physical security obligations, a looming 2026 embodied-carbon rule that will raise steel costs, and a shortage of skilled technicians are the principal restraints tempering expansion .

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (+) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G network roll-out and traffic surge

5G network roll-out and traffic surge

| +3.2% | Singapore; ASEAN spill-over | Medium term (2-4 years) | (+) % Impact on CAGR Forecast:

+3.2%

|

Geographic Relevance

:

Singapore; ASEAN spill-over

|

Impact Timeline

:

Medium term (2-4 years)

|

Country-wide fiber densification

Country-wide fiber densification

| +2.8% | Core island; enterprise edge | Short term (≤ 2 years) | |||

Government Smart Nation and sovereign-cloud mandates

Government Smart Nation and sovereign-cloud mandates

| +4.1% | National | Long term (≥ 4 years) | |||

Shift toward AI-ready high-density racks

Shift toward AI-ready high-density racks

| +3.7% | Global hyperscale; Singapore | Medium term (2-4 years) | |||

Liquid-cooling-ready rack designs

Liquid-cooling-ready rack designs

| +2.9% | SG & MY hubs | Long term (≥ 4 years) | |||

Green-energy-quota procurement

Green-energy-quota procurement

| +2.1% | National | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Government “Smart Nation” and sovereign-cloud mandates

Singapore’s Smart Nation 2.0 policy prioritizes data sovereignty. New rules oblige ministries, banks and hospitals to process regulated workloads locally, creating rack demand in on-premises sovereign clouds that meet AI inference and real-time fraud-detection needs. The Digital Infrastructure Act, due in 2025, will extend these obligations to critical digital services, effectively guaranteeing medium-term growth for enterprise-grade enclosures with tamper-proof access controls. Vendors with Singapore assembly and transparent supply chains receive preferred-bidder status, reinforcing localization advantages.

Shift toward AI-ready high-density racks

GPU clusters now draw 60-120 kW per rack versus the traditional 15 kW envelope. Hyperscale operators are retrofitting floors to accommodate liquid-cooling distribution, high-amperage busways and rack-level telemetry that automatically optimizes thermal load. Schneider Electric’s joint work with NVIDIA produced a turn-key 120 kW rack that integrates power, cooling and AI-led monitoring, a blueprint that accelerates full-rack standardization . Suppliers that can pre-engineer these converged frames benefit from faster deployment cycles and premium pricing.

5G network roll-out and traffic surge

Full island-wide 5G coverage has unlocked autonomous-vehicle pilots and IoT sensor grids. These low-latency applications need proximity compute, shifting rack sales toward compact, weather-resistant frames deployed in telecom exchanges and roadside cabinets. Designs must tolerate Singapore’s 90% humidity and deliver remote management because manpower at edge nodes is scarce. Vendors able to ruggedize data-center-grade enclosures for the street environment are enlarging addressable demand.

Liquid-cooling-ready rack designs tied to sustainability bids

The Infocomm Media Development Authority’s Green Data Centre Roadmap requires applicants for the new 300 MW quota to meet strict PUE and water-usage limits imda. Racks that accept direct-to-chip manifolds, rear-door heat exchangers or immersion tanks are therefore scoring bid points. Microsoft’s plan to use zero-waste water systems in future Singapore builds exemplifies the linkage between compliance and rack selection. Manufacturers that ship racks with pre-installed liquid lines or quick-connect plates shorten integration time and reduce leakage risk.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating ransomware & cyber-physical threats

Escalating ransomware & cyber-physical threats

| -2.1% | Asia-Pacific; SG focus | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-2.1%

|

Geographic Relevance

:

Asia-Pacific; SG focus

|

Impact Timeline

:

Short term (≤ 2 years)

|

Energy and land caps limiting new white-space

Energy and land caps limiting new white-space

| -1.8% | National | Medium term (2-4 years) | |||

2026 embodied-carbon rules raising steel costs

2026 embodied-carbon rules raising steel costs

| -1.4% | National; EU alignment | Medium term (2-4 years) | |||

Skilled labour crunch for customised racks

Skilled labour crunch for customised racks

| -1.2% | APAC; SG acute | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating ransomware and cyber-physical threats

Asia-Pacific suffered 34% of global cyberattacks in 2024; Honeywell logged a 46% jump in OT ransomware incidents that spilled into data-center infrastructure in early 2025. Singapore’s amended Cybersecurity Bill now obliges operators to certify cabinet locks, intrusion sensors and firmware integrity before a rack enters service. Added testing inflates costs by up to 20% and extends delivery by several weeks, dampening near-term installation volumes.

Energy and land caps limiting new white-space

Singapore’s 300 MW ceiling creates a scarcity premium. Operators pursue extreme-density racks to maximise compute per kilowatt, but specialised gear carries longer lead times and higher prices. Rising carbon taxes—SGD 25 per tonne in 2024 climbing to SGD 45 in 2026—also tilt purchasing toward efficient frames nea.gov.sg. The convergence of space and carbon limitations slows absolute unit growth even as per-rack value climbs.

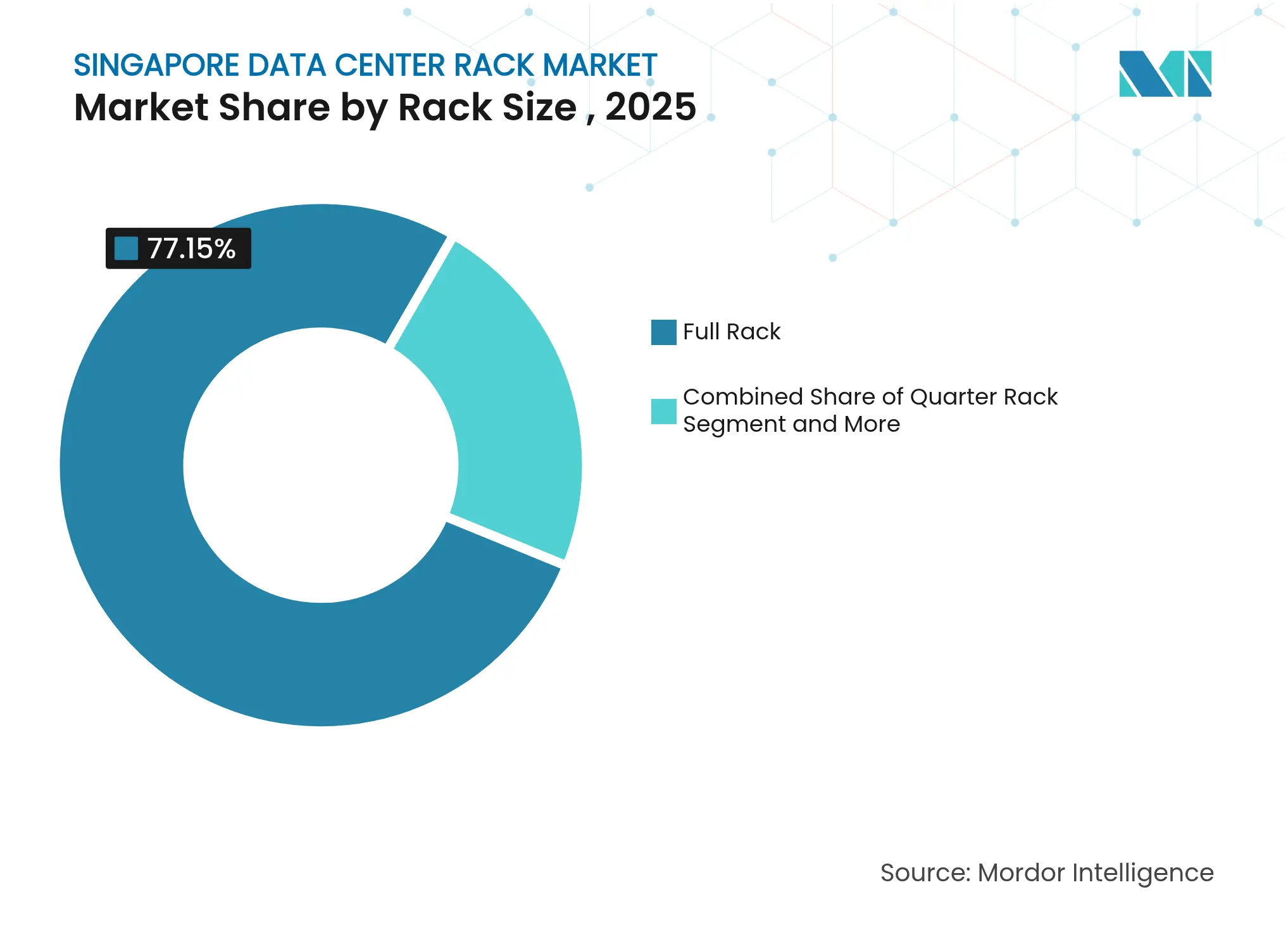

By Rack Size: Full racks drive standardisation

Full racks controlled 77.15% of the Singapore data center rack market share in 2025, and the segment is forecast to grow at 18.12% CAGR. Adoption is propelled by hyperscalers that favour uniform enclosures to streamline cabling, airflow and maintenance. The Singapore data center rack market benefits because consistent sizing lets operators pre-configure liquid-cooling headers and high-amp bus bars off-site, shortening commissioning. Full-height frames also support GPU servers that weigh over 1,200 kg once cool-plates and manifolds are installed. Quarter and half racks remain essential for edge nodes where floor space is scarce, yet these formats attract lower ASPs and do not materially alter market value.

Liquid cooling further entrenches full-height use. Distribution units, pumps and redundant plumbing typically occupy 6-8U in a cold-plate system, space that smaller racks cannot spare. Flex’s 120 kW liquid-ready chassis, already deployed in Singapore AI retrofits, illustrates this design logic As public-cloud zones expand, buyers increasingly request vendor-agnostic rails, busbars and quick-disconnect fittings, forcing suppliers to certify against multiple server brands. That complexity incentivises systems integrators to place bulk orders with a handful of globally recognised rack OEMs, strengthening top-tier vendor leverage in the Singapore data center rack market.

Note: Segment shares of all individual segments available upon report purchase

By Rack Height: 48U emerges as AI standard

Legacy 42U frames held 55.75% revenue in 2025, yet 48U is the fastest riser at 16.72% CAGR as hyperscalers prioritise additional vertical space for power shelves and coolant manifolds. A 48U envelope accommodates dual 60 kW power shelves in the base while still leaving unobstructed airflow for vertical plenums. The Singapore data center rack market size for 48U configurations could exceed USD 19.25 million by 2031, reflecting widespread GPU adoption. Operators appreciate that 48U retains compatibility with aisle-containment systems originally built for 42U, limiting the need for wholesale room refits.

Custom heights such as 52U cater to HPC labs chasing super-dense petaflop nodes, but shipping logistics and seismic certification difficulties prevent mass rollout. Suppliers future-proof their catalogues by offering modular roof extensions and drop-in blanking plates, allowing customers to toggle between 42U and 48U without forklift upgrades. Such flexibility preserves residual value in legacy inventory and reassures CFOs scrutinising capex in the Singapore data center rack market.

By Rack Type: Cabinet security drives adoption

Cabinet designs captured 74.58% revenue in 2025 and will accelerate at an 18.02% CAGR. Enclosed frames deliver granular airflow management, vital when inlet temperatures hover near 32 °C in Singapore’s humid environment. They also provide the physical access control demanded by the Cybersecurity (Amendment) Bill, which mandates tamper-evident doors and real-time audit logging for critical infrastructure. Open-frame racks linger in network closets and test labs where airflow and security are less stringent, while wall-mount formats fill telco edge sites.

Growing AI footprints amplify the security case for cabinets because GPU boards carry sensitive firmware. Financial institutions now specify dual authentication and automatic lock-down triggers connected to building management systems. These tighter specs raise ASPs and lift vendor margins in the Singapore data center rack market. In response, OEMs bundle environmental probes, RFID door sensors and micro-segmented PDUs into turnkey cabinet SKUs, shrinking the aftermarket add-on ecosystem.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

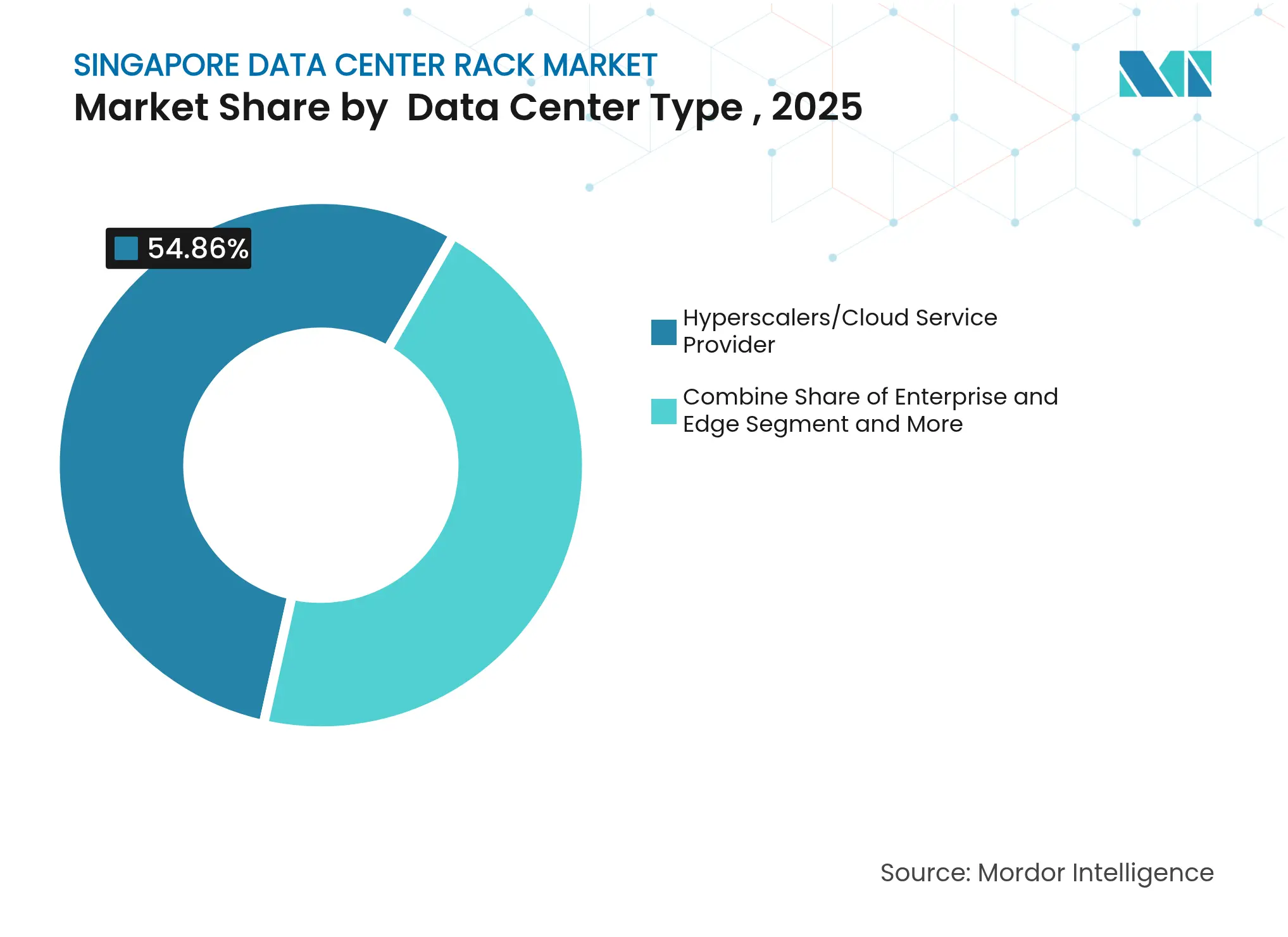

By Data Center Type: Hyperscalers lead infrastructure evolution

Hyperscale and cloud providers accounted for 54.86% revenue in 2025 and post the fastest CAGR at 18.92%. Google’s completed Singapore expansion and Microsoft’s forthcoming Malaysia region anchor multibillion-dollar capex cycles that cascade into bulk rack orders. Colocation operators follow by standardising on the same full-rack layouts to woo hyperscale overflow tenants, a copy-cat dynamic that reinforces design homogeneity across the Singapore data center rack market.

Enterprise and edge facilities remain relevant, particularly for sovereign-cloud and latency-sensitive industrial IoT workloads mandated by Smart Nation 2.0. These buyers often need custom airflow curtains or telecom-grade shock isolation, creating a long-tail of bespoke orders. However, volume clustering around hyperscalers means that contract manufacturers optimise their production lines to 48U, liquid-cool-ready cabinets, locking in economies of scale that smaller segments find hard to match.

Note: Segment shares of all individual segments available upon report purchase

By Material: Aluminum gains traction for high-density AI

Steel held 81.55% share in 2025 due to cost advantage and high load ratings. Nonetheless, aluminum frames are forecast to climb at 16.66% CAGR as operators seek lighter structures that simplify hot-aisle containment retrofits. Aluminum’s superior thermal conductivity assists heat rejection when racks operate at 80 kW and above, shaving a few degrees off coolant inlet temperatures. Such gains help facilities hit the 1.2 PUE threshold required for green-quota allocations, directly affecting the Singapore data center rack market.

Material policy also nudges adoption. Singapore will align with EU embodied-carbon reporting in 2026, exposing steel to higher carbon-adjustment costs. Early movers already balance upfront aluminum premiums against avoided carbon taxes and weight-driven logistics savings. Composite hybrids, mixing steel posts with aluminum side panels, are emerging as compromise solutions, preserving structural inertia while trimming mass. These design experiments underscore the engineering creativity now flowing into the Singapore data center rack market.

Singapore remains the epicentre of rack demand, underpinned by Smart Nation 2.0 funding and the reopened 300 MW data-center quota for operators that commit to renewable power. The Singapore data center rack market size for domestic deployments is projected to double between 2026 and 2031 as hyperscalers integrate AI clusters into their three existing availability zones. Regulatory certainty, rapid permit cycles and world-class submarine-cable density underpin the city-state’s attractiveness. However, land scarcity and rising carbon taxes compel developers to pursue ever-denser rack architectures to maximise compute per square metre.

Johor in southern Malaysia has become a safety valve. More than USD 23 billion of announced investments in 2024, including NTT’s 290 MW campus and AirTrunk’s second facility, ensure contiguous capacity that effectively enlarges the functional Singapore data center rack market. Hyperscalers procure identical racks for Johor and Singapore sites so equipment can be re-balanced depending on power allocation or tax incentives. This cross-border standardisation favours OEMs with distribution hubs in both countries, smoothing lead times and customs clearance.

Within ASEAN, Indonesia and Thailand constitute emerging nodes but trail Singapore’s connectivity. Their slower policy alignment on data-sovereignty and carbon accounting limits near-term rack import volumes. Nonetheless, Singapore’s leadership in design standards radiates outward: regional operators often copy Singapore-validated rack SKUs to reassure investors and regulators. Such diffusion widens the addressable base while cementing Singapore’s influence over specification roadmaps in the broader Singapore data center rack market.

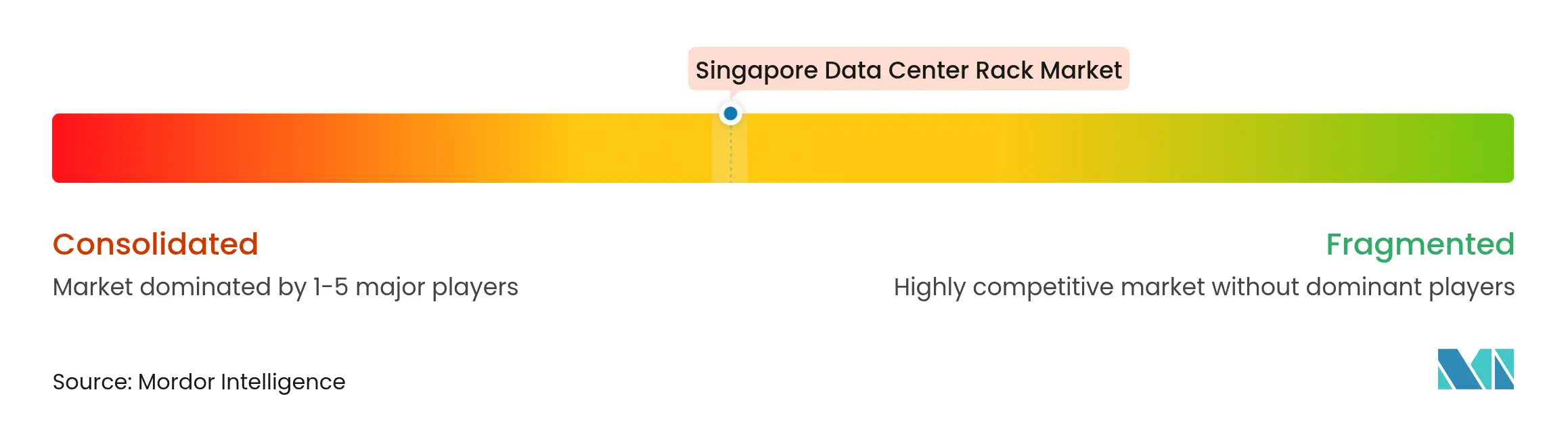

Market Concentration

The Singapore data center rack market contains a solid core of global multinationals—Schneider Electric, Vertiv, Legrand, Eaton and HPE—supplemented by regional specialists that customise frames for humidity control and seismic resilience. Schneider Electric leverages its EcoStruxure management layer to couple racks with real-time energy dashboards, enabling operators to fine-tune load distribution and prove compliance under Singapore’s carbon-tax regime. Vertiv’s acquisition of liquid-cooling firm CoolTerra accelerates its portfolio of 120 kW sealed cabinets, which will be showcased at Supercomputing Asia 2025 in Singapore.

Legrand has made nine acquisitions since 2024, pushing datacenter revenue to 20% of group sales and positioning its Minkels brand as a preferred cabinet for colocation suites that demand modular side-channel airflow. Flex focuses on contract manufacturing, shipping turnkey liquid-ready racks direct from its Penang plant to Singapore, trimming transport time by two days and avoiding red-lane customs inspection. HPE recently rolled out the CX 10040 switch series that clips into standard 42U and 48U rails, giving the hardware vendor a wider touchpoint in cabinet specification discussions.

Price competition is tempered by the technical complexity of AI racks. Buyers evaluate mechanical strength, coolant compatibility, firmware security and embodied-carbon certificates before awarding contracts. These multidimensional criteria elevate switching costs and foster moderate consolidation in the Singapore data center rack market. Yet pockets of opportunity remain for niche entrants that solve edge-site problems, for example IP-65-rated outdoor cabinets or hydrogen-compatible enclosures destined for Keppel’s floating data-center pilot.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Singapore Data Center Rack Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 33.8 million (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 860 million (2024) | Global Consultancy A | Broad scope bundles PDUs and aisle containment kits, applies global ASP curve without local discounts | ||

141,428 racks (2024) | Trade Journal B | Reports unit volume only; no price translation and omits enterprise on-premise retrofits |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.