China Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

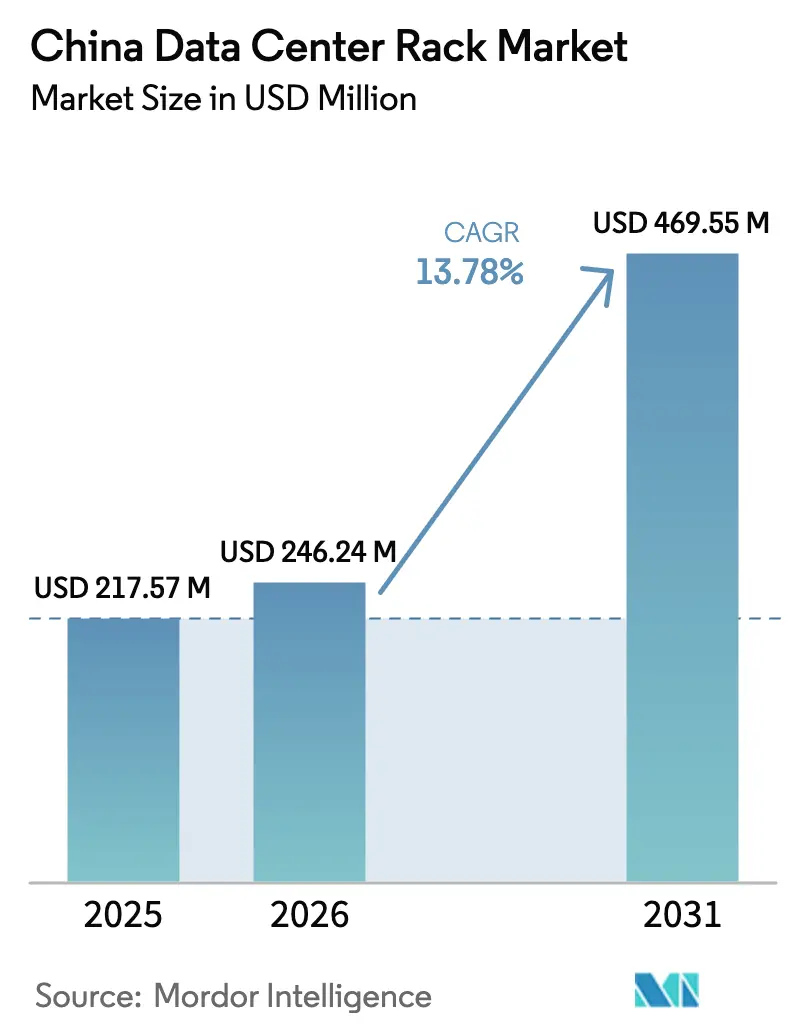

| Base Year Market Size (2025) | USD 217.57 Million |

| Market Size (2026) | USD 246.24 Million |

| Market Size (2031) | USD 469.55 Million |

| Growth Rate (2026 - 2031) | 13.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Data Center Rack Market Analysis by Mordor Intelligence

The China data center rack market size is expected to grow from USD 217.57 million in 2025 to USD 246.24 million in 2026 and is forecast to reach USD 469.55 million by 2031 at a 13.78% CAGR over 2026-2031. Demand is accelerating as the Eastern Data, Western Computing policy moves hyperscale workloads toward inland hubs that offer inexpensive renewable energy and free-cooling climates. Liquid-cooling cabinets, once niche, now command mainstream adoption because rack power densities have climbed past 30 kilowatts in artificial-intelligence clusters. State-owned carriers are standardizing on full-height cabinets with busway distribution and factory-installed containment, thereby reducing installation time and improving consistency across regions. Mid-sized enterprises and 5G operators, meanwhile, favor compact half-height formats for edge nodes where floor space is constrained. Against this backdrop, vendors able to ship pre-commissioned rows with integrated power, telemetry, and coolant loops capture growing preference from both hyperscalers and colocation providers.

Key Report Takeaways

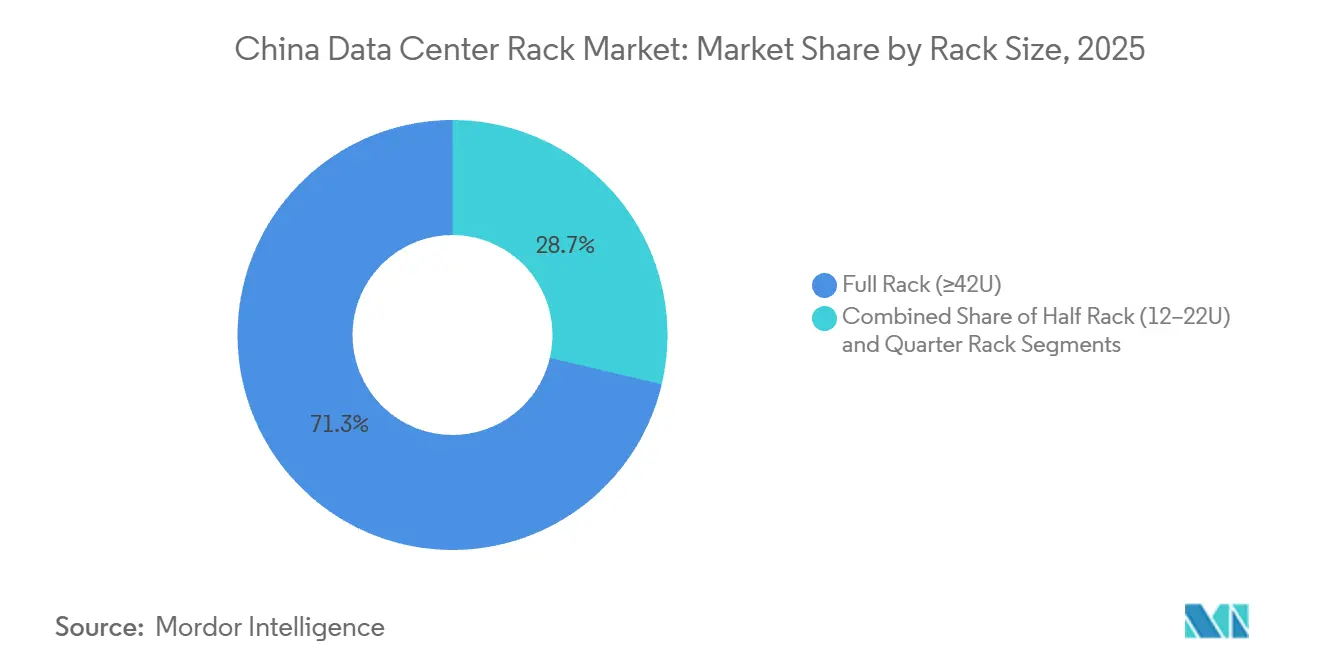

- By rack size, full racks held 71.32% of share in 2025, while half racks are forecast to grow at a 14.54% CAGR through 2031.

- By rack type, enclosed cabinets commanded 75.33% share in 2025, and this segment is projected to advance at a 14.76% CAGR over 2026-2031.

- By tier, Tier 3 facilities captured 53.21% of share in 2025, whereas Tier 4 sites will expand at a 14.68% CAGR during the forecast horizon.

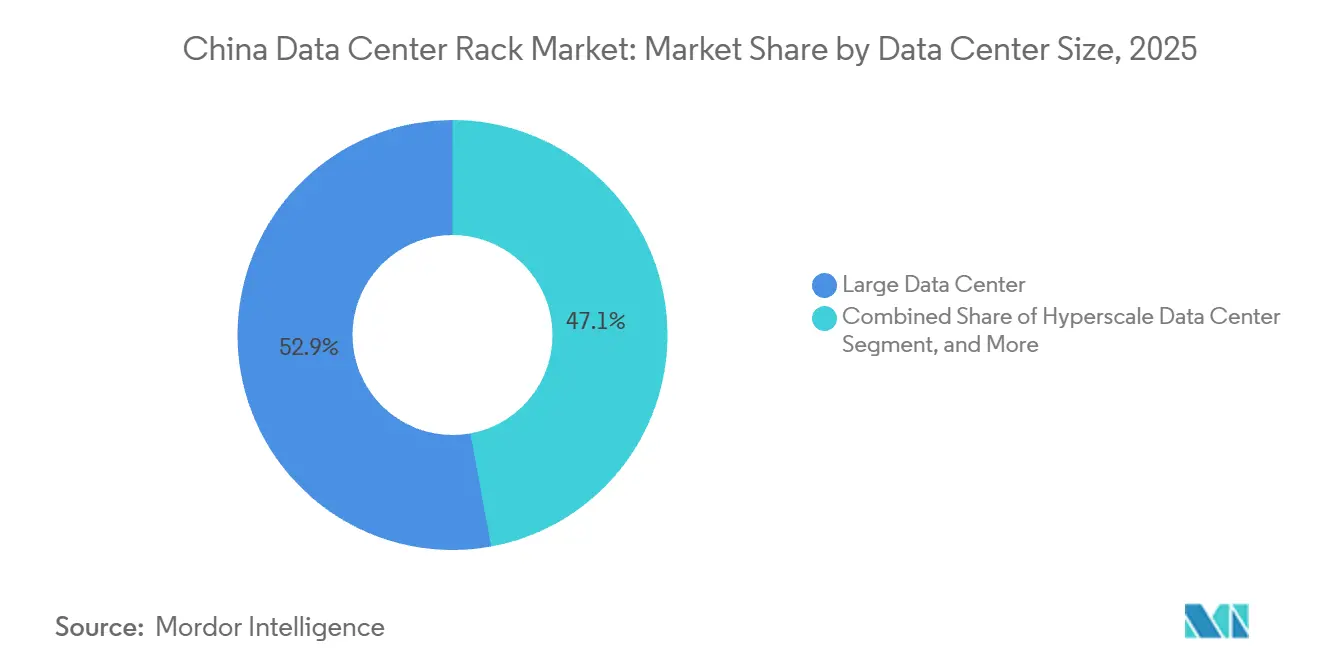

- By data-center size, large facilities accounted for 52.88% of share in 2025, while hyperscale complexes are poised to register a 14.24% CAGR.

- By data-center type, colocation operators held 51.68% share in 2025, but hyperscalers and cloud-service providers are set to post the fastest 14.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Anticipated developments are shaped at a system level, with China signals feeding into a larger global picture. The outlook on global data center rack market consolidates these expectations.

China Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Cloud and AI Workloads Driving High-Density Rack Demand | +3.5% | National, Beijing-Tianjin-Hebei, Yangtze River Delta, Greater Bay Area | Short term (≤ 2 years) |

| Increasing Deployment of Hyperscale and Colocation Facilities | +3.0% | National, accelerated in western hubs | Medium term (2-4 years) |

| Government Eastern Data, Western Computing Initiative Accelerating Build-Outs | +2.8% | Eight western hubs | Long term (≥ 4 years) |

| Carbon-Neutral Mandates Fostering Liquid-Cooling-Ready Rack Adoption | +2.2% | National, earliest in Shanghai, Guangdong, Beijing | Medium term (2-4 years) |

| 5G Edge Build-Outs Requiring Compact Micro-Racks in Base Stations | +1.5% | National Tier 1 and Tier 2 cities, rural west | Short term (≤ 2 years) |

| Rising BFSI Digital-Core Upgrades Requiring Secure On-Prem Racks | +1.2% | Key financial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Cloud and AI Workloads Driving High-Density Rack Demand

Artificial-intelligence clusters now exceed 30 kilowatts per rack, forcing operators to retrofit old cabinets with liquid manifolds designed for only 8-12 kilowatts. Huawei’s CloudMatrix 384 testbed showed that power delivery must scale to 50 kilowatts to host eight H100-class accelerators per server. Domestic AI revenues surpassed USD 41 billion in 2025 and could top USD 96 billion by 2028. Sensitive sectors such as finance and healthcare account for only 5% of server demand but insist on on-prem cabinets with tamper detection, nudging racks toward active cooling and security functions. Dell’Oro Group reported that direct liquid-cooling revenue more than doubled in Q1 2026, mirroring a 40% surge in busway power rails needed for 600-kilowatt rows.[1]IT-HSDA Staff, “The Server Battleground: The Hardware Competition Behind The Middle East's AI Race,” IT-HSDA, it-hsda.com Together, these forces propel the China data center rack market toward higher wattages, richer telemetry, and factory-integrated coolant loops.

Increasing Deployment of Hyperscale and Colocation Facilities

GDS Holdings committed 88,000 square meters of new white space in Q3 2024, while BroadNet operated 72,000 cabinets by mid-2025 with another 230,000 in pipeline.[2]IT-HYLLSI News Desk, “Middle East Server Industry Booms, With Chinese Enterprises Deeply Involved In Promoting International Trade Cooperation,” IT-HYLLSI, it-hyllsi.com Colocation leaders standardize on Scorpio frames that arrive with busbars, PDUs, and containment, cutting on-site labor by 60%. Gansu State Grid’s cloud node invested USD 137 million for 3,000 racks, underscoring the capital intensity of turnkey rows. Hyperscalers now bypass distributors, locking multi-year rack contracts directly with manufacturers, a practice that disadvantages small vendors lacking co-engineering capacity. VNET Group’s Q3 2024 revenue climbed 14.3% year-over-year on persistent colocation demand, spotlighting the scale dividends accruing to players that can deliver thousands of identical cabinets each quarter.

Government Eastern Data, Western Computing Initiative Accelerating Build-Outs

The 2021 policy mapped eight national hubs and funneled more than USD 6.1 billion into interior provinces rich in wind, solar, and hydro resources.[3]Xinhua News Agency, “China Issues Guideline To Boost Data-Related Disciplines,” Gov.cn, gov.cn Sichuan alone targeted 500,000 racks by 2025, and Shanghai ruled that half of future smart-computing cabinets must use liquid cooling. Xinjiang’s JiangSuan program will deliver 20,000 petaflops across thousands of high-density racks, each backed by renewable energy-linked energy storage. Updated Green Data Center standards now require ≥3,000 racks, PUE ≤ 1.30, and renewable share thresholds, concentrating demand among large carriers able to scale. Provincial bids increasingly cite Dawei Technology’s Zhangbei center, commissioned in October 2025, as the benchmark for cold-plate specs.

Carbon-Neutral Mandates Fostering Liquid-Cooling-Ready Rack Adoption

National guidelines target an average PUE below 1.5 by 2025, dropping to 1.2 in inland hubs, essentially mandating liquid cooling. China Telecom’s Huailai immersion pilot trimmed annual energy use by more than 1.1 million kilowatt-hours and ran at PUE 1.15, confirming 30-50% efficiency gains. Gree Electric is rolling out phase-change coolant loops that hit PUE 1.15 even at 50 °C ambient, satisfying Greater Bay Area mandates. Six ministries now require energy-storage systems for any new data center to buffer intermittency, compelling racks to integrate leak detection and quick-disconnects for in-service server swaps. H3C’s 200-kilowatt cabinets house 8,192 cores and demonstrate how elevated bill-of-materials costs are offset by lifecycle savings, a calculus that resonates with operators chasing carbon caps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Blade and Converged Systems Reducing Traditional Rack Counts | -2.1% | National, especially BFSI | Medium term (2-4 years) |

| Land and Power Quota Caps in Tier-1 Cities Tightening Data-Center Approvals | -1.8% | Beijing, Shanghai, Shenzhen, Guangzhou | Short term (≤ 2 years) |

| U.S. Export-Control Limits on High-End Chips Slowing Ultra-Dense Rack Roll-Outs | -1.5% | National, hyperscale AI clusters | Short term (≤ 2 years) |

| Skilled-Labor Shortages for Advanced Rack Integration and Maintenance | -0.9% | National, acute in Tier 1 and western hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Blade and Converged Systems Reducing Traditional Rack Counts

Hyper-converged appliances pack compute, storage, and networking into a single chassis, trimming rack footprints for BFSI and branch sites. Although unit shipments decline, average selling prices rise because converged cabinets need heavier frames, dual busbars, and reinforced casters. Enterprises retrofitting three-tier networks often upsize from 42U to 48U formats, partially cushioning unit erosion. Vendors therefore face a nuanced threat; fewer cabinets but richer content per cabinet. Competitive positioning hinges on supplying reinforced enclosures that can handle 1,500-kilogram static loads without sacrificing airflow.

Land and Power Quota Caps in Tier-1 Cities Tightening Data-Center Approvals

Beijing, Shanghai, and Shenzhen have halted new mega-campuses inside core districts, forcing operators to upgrade older sites or migrate workloads west. Shanghai’s 1.3 PUE ceiling effectively blocks air-cooled rows, accelerating liquid adoption. Guangdong uses power caps to push taller racks that squeeze more compute into existing rooms, incentivizing modular systems arriving ready to energize in days. Firms unable to secure urban permits sub-lease space from carriers with legacy allotments, favoring vendors that already supply those carrier footprints. The combined outcome is a demand shift toward modular, factory-tested solutions that minimize construction delays and satisfy rapidly changing municipal rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Half Racks Capture Edge Build-Outs

Half racks will outpace the broader China data center rack market with a 14.54% CAGR because micro edge sites and 5G radio nodes need compact, rugged formats. The China data center rack market size for half racks is expanding as operators install cabinets rated IP65 to handle dust and moisture near street-level base stations. Edge deployments seldom exceed 3-4 kilowatts, yet still demand biometric locks and remote telemetry to deter vandalism. In contrast, full racks secured 71.32% of share in 2025 thanks to hyperscale contracts that standardize on 42U and 48U Scorpio frames. These larger enclosures streamline airflow and cable routes, lowering assembly hours and boosting consistency across multiple campuses.

Full-height formats will remain the backbone inside hyperscale halls because operators buy them in container-load volumes, compressing margins but creating predictable factory throughput. Quarter racks and wall-mount micro enclosures persist in retail chains and branch offices where aesthetics trump density. Inspur’s desert-rated “Desert Ship” family highlights the march toward wide-temperature, dust-filtered cabinets that are now repatriating to western China wind belts. Rapid-deploy designs that arrive pre-cabled slash installation times by up to 40%, a productivity edge valued by colocation providers racing to bring new halls online.

By Rack Type: Enclosed Cabinets Dominate Security-Sensitive Workloads

Enclosed cabinets held 75.33% share in 2025, reflecting strict BFSI rules for tamper detection, EMI shielding, and seismic anchoring. The segment will grow faster than the overall China data center rack market, advancing 14.76% CAGR as cyber-risk regulations tighten. Open-frame racks remain favored by hyperscalers where access is already restricted and airflow efficiency is paramount. Even so, hyperscale operators increasingly add mesh-door inserts and blind-spot cameras, narrowing the cost gap.

Wall-mount and micro-edge styles gain traction in IoT gateways, retail checkout hubs, and smart-factory cells. The China data center rack market share for enclosed cabinets therefore remains dominant because enterprises continue to prioritize physical compliance features over initial cost savings. Schneider Electric and Vertiv compete head-to-head with modular accessories vertical PDUs, brush strip ingress panels, and environmental probes that integrate seamlessly into their respective EcoStruxure and Vertiv Life platforms, giving operators unified dashboards for power and thermal data.

By Tier Type: Tier 4 Rises for Mission-Critical AI

Tier 3 accounted for 53.21% of share in 2025, but Tier 4 sites will log a 14.68% CAGR as sovereign AI training clusters, fintech clearinghouses, and high-frequency traders pursue 2N+1 redundancy. The China data center rack market for Tier 4 deployments is expanding as government owners require concurrent maintainability, which requires dual PDUs and manifold-redundant coolant feeds. Retrofitting a Tier 3 hall to Tier 4 often means swapping legacy racks that lack dual-feed provisions.

While Tier 1 and Tier 2 rooms still serve edge caches and disaster-recovery vaults, their growth lags as customers redirect core data to more robust nodes. Huawei’s Atlas 900 deployment abroad demonstrated the density achievable when racks are purpose-built for AI ASICs and liquid loops, a template now mirrored in domestic finance hubs. Vendors able to ship racks with integrated static-transfer switches and self-purging coolant manifolds win bids where downtime must approach zero.

By Data-Center Size: Hyperscale Purchases Drive Volume

Large facilities owned by colocation specialists captured 52.88% of the share in 2025, but it is hyperscale complexes that will post the strongest 14.24% CAGR, underpinning the long-run expansion of the China data center rack market. Hyperscale buyers insist on Scorpio-standard rows with 400-600 amp busbars, dual PDUs, and aisle-containment doors that nest seamlessly into ceiling plenums. Such turnkey rows compress on-site labor by roughly 60%, an advantage when projects add thousands of cabinets per quarter.

Medium centers bridge regional cloud providers and managed-service firms seeking 500-2,000 cabinets yet unable to command hyperscale pricing. Small centers, usually below 500 cabinets, now cluster near 5G macro towers or retail campuses to deliver millisecond latency. Vendors straddling both hyperscale and boutique needs must balance volume economics with customization flexibility a dual competency that only a handful of suppliers currently master.

By Data-Center Type: Cloud Providers Accelerate Direct Procurement

Colocation halls owned by GDS, 21Vianet, and VNET supplied 51.68% of the share in 2025, but hyperscalers and cloud-service providers will advance at a brisk 14.85% CAGR, outpacing every other customer class. These internet giants negotiate multi-year framework deals, stipulating racks shipped with busway rails, containment doors, and sensor arrays so that commissioning is a plug-and-play exercise. The channel bypass slashes distributor margins and shifts value capture upstream to manufacturers able to co-engineer power and thermal modules with the cloud buyer’s reference design.

Enterprises and edge users remain profitable niches because each rack commands a 20-30% premium for biometric locks, EMI gasketing, and seismic bracing. ZTE’s reorganization to court internet-firm orders reveals how server makers realign around this procurement model, promising 24-hour engineering responses and 48-hour supply-chain commits. The China data center rack industry thus bifurcates into high-volume, thin-margin hyperscale rows and smaller, high-margin specialty enclosures.

Geography Analysis

The coastal triad of Beijing-Tianjin-Hebei, Yangtze River Delta, and Guangdong–Hong Kong–Macao Greater Bay Area hosts most racks today because it sits near cloud regions, stock exchanges, and export manufacturing. Yet incremental growth is shifting west as the Eastern Data, Western Computing mandate channels data into Inner Mongolia, Guizhou, Gansu, Ningxia, Shaanxi, Sichuan, Chongqing, and Xinjiang. Inland hubs tout wind-cooled climates that push annual PUE below 1.25, saving operators millions in energy bills. Sichuan aimed for 500,000 racks by 2025, leveraging hydro reservoirs to supply cheap renewable electrons.

Beijing, Shanghai, and Shenzhen have imposed rack moratoriums in urban cores and hard PUE limits near 1.3, forcing retrofits with taller 48U and 52U frames to pack more compute into static footprints. Shanghai additionally requires that half of smart-computing racks adopt liquid cooling by 2025, accelerating the phase-out of legacy air cabinets. Guangdong’s border with Hong Kong enables cross-border interconnects, making Shenzhen and Guangzhou prime for multinational cloud on-ramp sites that demand bilingual compliance reporting.

Relocating capacity west raises logistical hurdles. Trucks crossing 2,000 kilometers of mountainous highways face longer lead times, and operators insist on local spares depots for four-hour break-fix SLAs. Eaton’s Industry 4.0 overhaul of its Changzhou plant lifted output efficiency 26% while halving greenhouse emissions, enabling quicker shipments inland. Vertiv’s Malaysia factory, due online in Q1 2026, will feed both coastal and western China with liquid-ready enclosures, trimming ocean freight days. Vendors without comparable regional capacity risk exclusion from state tenders that stipulate domestic content and rapid service response.

Analysis of the data center rack market by Mordor Intelligence spans multiple other regional evaluations across Middle East, South America, and Europe, supported by country-level insights for Taiwan, India, Saudi Arabia, Chile, Netherlands, and Norway, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Schneider Electric and Vertiv were virtually tied in global physical infrastructure share as of Q1 2026, a rivalry that spills over into the China data center rack market. They leverage integrated portfolios spanning racks, PDUs, busways, and DCIM software, giving customers a single-vendor pathway from inlet to chip. Domestic OEMs Huawei, Inspur, and H3C capitalize on sovereignty mandates to win state projects, bundling wide-temperature cabinets, dust filters, and immersion kits that commission 40% faster than multinational peers.

Strategic investments focus on vertical integration and regional manufacturing. Eaton broke ground on a Dubai plant slated to employ 700 and produce advanced switchgear and thermal assemblies for data centers opening in 2026. Vertiv paid about USD 1 billion for PurgeRite, adding nationwide fluid-flushing crews that tackle liquid-cooler start-ups, a chronic bottleneck as rack power climbs. nVent is building a 117,000 square-foot Minnesota site dedicated to liquid-loop hardware, evidence that thermal is now central to capital planning.

Niche innovators like Gree Electric and Envicool undercut global brands by 30-40% yet meet new PUE and renewable-integration codes, gaining traction with state carriers. The white-space frontier involves 800-volt HVDC containerized pods housing 200-kilowatt racks, a design that sidesteps legacy AC switchgear upgrades. Vendors lacking R&D heft retreat to ruggedized edge, seismic banking, or explosion-proof oil-and-gas enclosures where certification barriers shelter margins. Ultimately, the decisive advantage lies in shipping rows that arrive pre-commissioned, instrumented, and ready to energize, slashing on-site labor by up to 60% and speeding time-to-revenue for fast-growing colocation providers.

China Data Center Rack Industry Leaders

Eaton Corporation

Black Box Corporation

Rittal GmbH & Co. KG

Schneider Electric SE

Vertiv Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Vertiv’s Malaysia manufacturing facility is expected to reach full capacity in Q1 2026, producing power and liquid-cooling systems for high-density AI loads across Asia-Pacific, including China.

- January 2026: nVent’s 117,000-square-foot Minnesota plant is slated to open in early 2026, adding 175 jobs focused on liquid-cooling components for data centers.

- October 2025: Eaton began building a 36,000-square-meter advanced manufacturing and engineering center in Dubai that will employ more than 700 staff and supply power-management hardware for global data centers.

- October 2025: Dawei Technology commissioned a 60-megawatt cold-plate computing center in Zhangbei that now serves as a provincial procurement benchmark.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the China data center rack market as the yearly spending on new racks, open-frame, wall-mount, and cabinet enclosures installed inside colocation, hyperscale, enterprise, and edge facilities across mainland China. Racks built for telecom outside the controlled data-hall environment and refurbished or gray-market units are out of scope.

Segmentation Overview

- By Rack Size

- Quarter Rack (More than 11U)

- Half Rack (12-22U)

- Full Rack (More than Equal to 42U)

- By Rack Type

- Enclosed Cabinet

- Open-Frame

- Wall-Mount and Micro-Edge Enclosure

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Size

- Small Data Center

- Medium Data Center

- Large Data Center

- Hyperscale Data Center

- By Data Center Type

- Colocation Data Center

- Hyperscalers Data Center/CSPs

- Enterprise and Edge Data Center

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with facility planners at leading colocation operators, procurement heads of cloud service providers in Beijing and Shenzhen, and local rack integrators in Suzhou. These discussions verified refresh cycles, liquid-cool ready dimensions, and current average selling prices, which anchored our model's moving inputs.

Desk Research

We start with trade statistics from China's General Administration of Customs, public tenders posted on Tenders Info, and shipment splits from Volza to size inbound rack volumes. Industry associations such as the China Data Center Committee, policy notes from the Ministry of Industry and Information Technology, and energy-use disclosures tied to the 'East-Data-West-Compute' hubs add macro signals. Company filings, IPO drafts, and Tier-1 news archives on Dow Jones Factiva supplement pricing and capacity announcements. This list is illustrative; many more sources inform baseline assumptions.

Market-Sizing & Forecasting

A top-down build starts with installed IT load (MW) published by regulators, which is converted to rack counts using verified power-per-rack densities. Spend is then derived by multiplying sampled ASPs, and results are cross-checked through partial bottom-up roll-ups from five key suppliers. Variables tracked quarter by quarter include GPU rack penetration, average rack height migration (42U to 48U), regional PUE mandates, and steel price trends that sway frame costs. Forecasts rely on multivariate regression where hyperscale capex, cloud revenue, and AI training workloads explain over 80 % of variance; scenario analysis adjusts for policy or supply shocks. Gaps in bottom-up data are bridged with conservative proxy ratios confirmed in interviews.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance checks against customs volumes, and anomaly flags if quarter-on-quarter change exceeds 7 %. Models refresh annually, and we revisit them mid-cycle whenever policy, currency, or material cost shifts cross preset thresholds.

Credibility Anchor: Why Our China Data Center Rack Baseline Commands Reliability

Published estimates often differ because firms adopt unique scopes, refresh speeds, or pricing mixes. By tying rack demand to hard federal IT-load releases and validating prices through live purchase orders, Mordor presents a balanced midpoint buyers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 217.6 million (2025) | Mordor Intelligence | - |

| USD 374.2 million (2023) | Global Consultancy A | Includes Hong Kong & Taiwan racks and uses list prices without discount factors |

| USD 4.62 billion (2024) | Industry Journal B | Aggregates rack PDUs, containment, and retrofit spend, inflating base value |

In short, other publishers widen or narrow definitions and vary currency conversions, whereas our disciplined scope, dual-track validation, and timely refresh give decision-makers a dependable starting point.

Key Questions Answered in the Report

What is the current China data center rack market size and how fast is it forecast to grow?

The market is valued at USD 246.24 million in 2026 and is projected to reach USD 469.55 million by 2031, reflecting a 13.78% CAGR over 2026-2031.

How fast is rack demand growing inside western Chinese data-center hubs?

Inland clusters are expanding faster than coastal regions as national policy channels workloads west, supporting the overall 13.78% CAGR.

Which rack form factor is preferred for 5G edge sites?

Half-height cabinets rated IP65 dominate 5G base-station deployments because they fit tight spaces and shield electronics from dust and rain.

Why are enclosed cabinets gaining share among financial institutions?

BFSI mandates require biometric locks, EMI shielding, and seismic bracing, making enclosed cabinets the default choice for branch and core banking halls.

What impact do national carbon-neutral goals have on rack design?

PUE limits below 1.3 effectively enforce liquid-cooling readiness, so new racks integrate manifold pipes, leak sensors, and quick-disconnect couplings.

How are hyperscalers changing procurement practices?

Alibaba Cloud, Tencent, and ByteDance now sign multi-year contracts directly with manufacturers, purchasing turnkey rack rows that arrive pre-wired and containment-ready.

Page last updated on: