Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Low Temperature Coatings Market Report is Segmented by Resin (Polyester, Epoxy, and More), Technology (Powder, Liquid – Solvent-Borne, Liquid – Water-Borne, UV/EB-cured), Substrate (Metals, Plastics and Composites, Wood, Other Substrates), End-User Industry (Architectural, Industrial, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

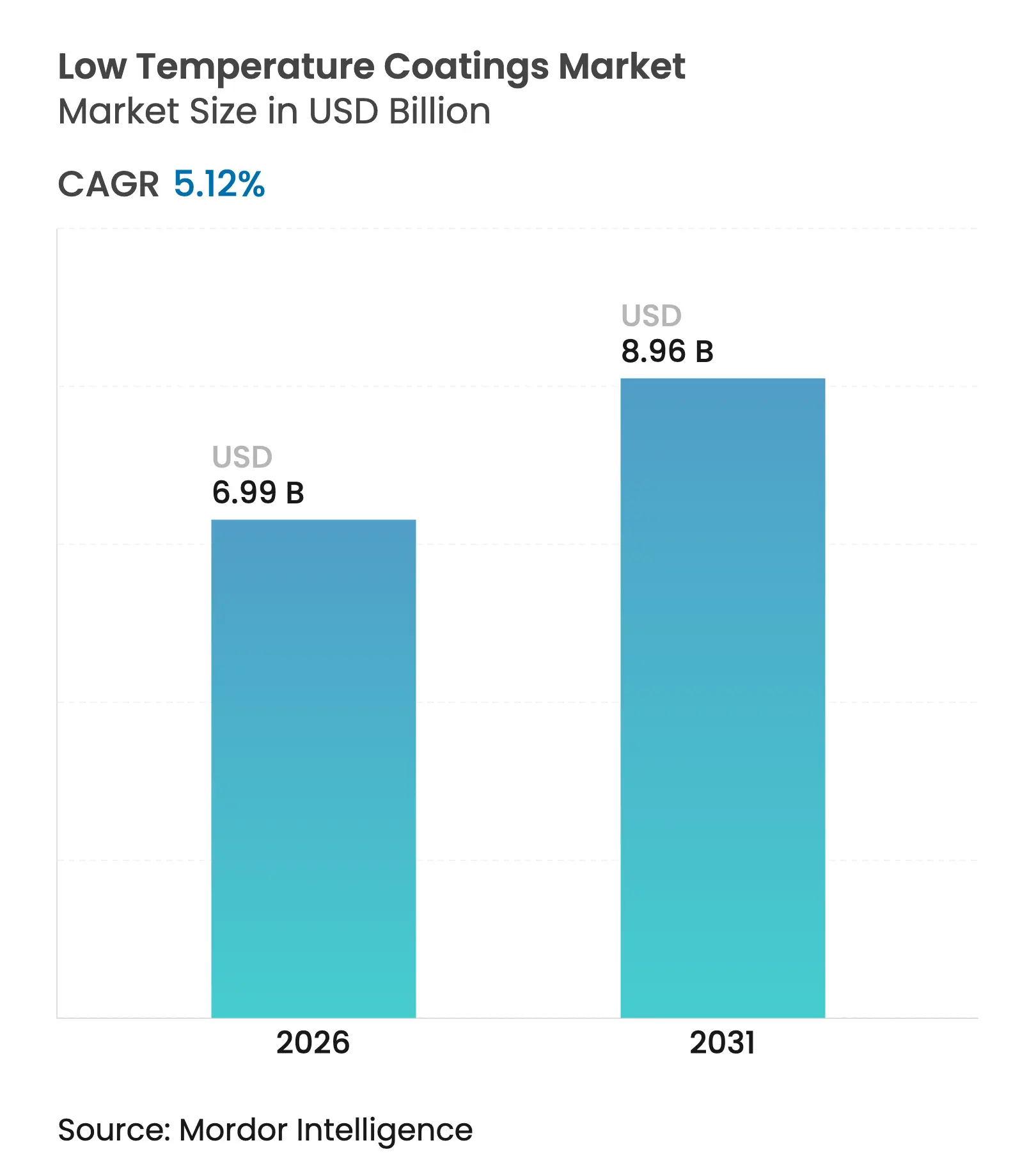

| Market Size (2026) | USD 6.99 Billion |

| Market Size (2031) | USD 8.96 Billion |

| Growth Rate (2026 - 2031) | 5.12 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Low Temperature Coatings market size is expected to grow from USD 6.65 billion in 2025 to USD 6.99 billion in 2026 and is forecast to reach USD 8.96 billion by 2031 at 5.12% CAGR over 2026-2031. The steady advance reflects regulatory pressure to trim process-heat emissions, rising energy prices that reward cooler cure profiles, and technological progress that now allows full performance at temperatures close to 120 °C. Energy savings of up to 25% have become common when plants shift from 375 °F bake cycles to formulations that cure at 285 °F, improving throughput and lowering carbon footprints. Demand is also boosted by the growing use of plastics, composites, and 3-D-printed parts that deform under conventional oven conditions, as well as the surge in electric vehicle (EV) production that requires thermally stable but gently cured battery enclosures. Competitive intensity is moderate: leading suppliers leverage resin chemistry, laser-assisted curing, and strategic acquisitions to defend share while niche players target ultra-low-bake segments such as offshore wind maintenance and additive manufacturing. Raw-material cost swings, notably titanium dioxide, and the technical difficulty of depositing ultra-thin films below 25 µm remain the principal headwinds.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Energy savings from reduced cure temperatures

Energy savings from reduced cure temperatures

| +1.2% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, with strongest impact in North America & EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing adoption for heat-sensitive substrates in

electronic vehicles and electronics

Growing adoption for heat-sensitive substrates in

electronic vehicles and electronics

| +1.8% | APAC core, spill-over to North America | Long term (≥ 4 years) | |||

Process-heat carbon pricing accelerating adoption

Process-heat carbon pricing accelerating adoption

| +0.9% | EU & California, expanding to other regions | Short term (≤ 2 years) | |||

3-D printed parts requiring ultra-low-bake coatings

3-D printed parts requiring ultra-low-bake coatings

| +0.7% | North America & EU, emerging in APAC | Long term (≥ 4 years) | |||

Offshore wind tower maintenance shift to low-temp cures

Offshore wind tower maintenance shift to low-temp cures

| +0.5% | Europe & North America coastal regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Energy Savings from Reduced Cure Temperatures

Plants that retrofit to low-temperature powder systems save up to 25% in gas or electricity consumption, a figure confirmed by production lines that dropped cure peaks from 400 °F to 325 °F while maintaining corrosion resistance. Shorter oven residence also pushes line speeds higher, improving asset utilization. Regions with high energy tariffs such as California and Germany adopt these formulations first, yet the payoff is now similar elsewhere because carbon charges are widening. Payback is often achieved within one year thanks to slimmer utility bills and fewer filter-maintenance cycles. The move lowers scope 1 emissions, positioning users for future carbon-border fee regimes[1]California Air Resources Board, “Industrial Cap-and-Trade Program Overview,” arb.ca.gov .

Growing Adoption for Heat-Sensitive Substrates in Electric Vehicles and Electronics

EV battery housings and electronic modules cannot tolerate the thermal shock typical of legacy bakes. Coatings that polymerize at 130 °C protect dielectrics, preserve adhesive layers, and meet insulation resistance targets without disturbing battery cell chemistries. Thermal interface materials are bonded at 35 °C, so paint shops now integrate integrated low-bake zones downstream of cell assembly. Semiconductor packaging lines mirror the trend by asking for sub-150 °C cycles that avoid warpage in fine-pitch boards. Asia-Pacific leads because of its EV supply-chain density, but North American gigafactories are rapidly specifying identical cure windows.

Process-Heat Carbon Pricing Accelerating Adoption

California’s cap-and-trade and the EU Emissions Trading System raise the cost of every therm generated above baseline, converting a technical choice into a financial imperative. Facilities with large gas-fired curing ovens now calculate direct savings from 0.9% CAGR uplift linked to carbon surcharges. Canada’s Clean Electricity Regulations and the United States methane-fee rule reinforce the effect by encouraging equipment upgrades that shave kilowatt-hours per coated part. Firms that shift to ultra-low-bake technologies therefore not only reduce bills but also bank surplus allowances.

3-D-Printed Parts Requiring Ultra-Low-Bake Coatings

Additive manufacturing often employs nylon 6, polycarbonate, and carbon-fiber-reinforced polymers whose heat-deflection temperatures hover near 140 °C. Newly engineered powders melt and flow at 110 °C, then crosslink under laser flashes or catalytic infrared in minutes, eliminating dimensional drift[2]Allnex, “UV/EB Low-Temperature Curable Powder Coatings,” allnex.com. Early adopters in aerospace and motorsport use laser-cured powders that free factory floor space once occupied by convection tunnels. Department of Energy grants signal readiness for broader industrial roll-out by 2025, expanding addressable tonnage for the low temperature coatings market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited ability to achieve ultra-thin films

Limited ability to achieve ultra-thin films

| -0.8% | Global, particularly in precision applications | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global, particularly in precision applications

|

Impact Timeline

:

Medium term (2-4 years)

|

Competition from ambient-cure UV/EB systems

Competition from ambient-cure UV/EB systems

| -0.6% | North America & EU, expanding to APAC | Short term (≤ 2 years) | |||

Thermal-shock defects on composite substrates

Thermal-shock defects on composite substrates

| -0.4% | APAC manufacturing hubs, aerospace sectors | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Ability to Achieve Ultra-Thin Films

Below 25 µm, many powder chemistries suffer orange-peel and pore formation because lower oven temperatures restrict flow and leveling. Automotive clearcoat programs therefore hesitate to convert entire fleets, instead reserving low-bake lines for mid-coat layers where film build can remain thicker. Catalyst packages that accelerate crosslink density at 135 °C help but add formulation cost. Research into hybrid polyesters and nanofilled resins continues, yet large-scale breakthroughs remain two to four years away.

Competition from Ambient-Cure UV/EB Systems

UV-cured powders liquefy at 120 °C and snap-cure in seconds once exposed to ultraviolet or electron beams, eliminating the need for prolonged bake cycles. Recent advances extend penetration depth to 2.5 cm, sufficient for many wood and thick-gauge metal parts. Equipment prices are falling, making conversion cost competitive. However, UV lines struggle with deep cavities and pigmented shades, leaving space for thermo-reactive low-bake systems. The two technologies will coexist but share battles will trim 0.6 percentage points off forecast CAGR in some regions.

By Resin: Polyurethane Innovation Drives Market Evolution

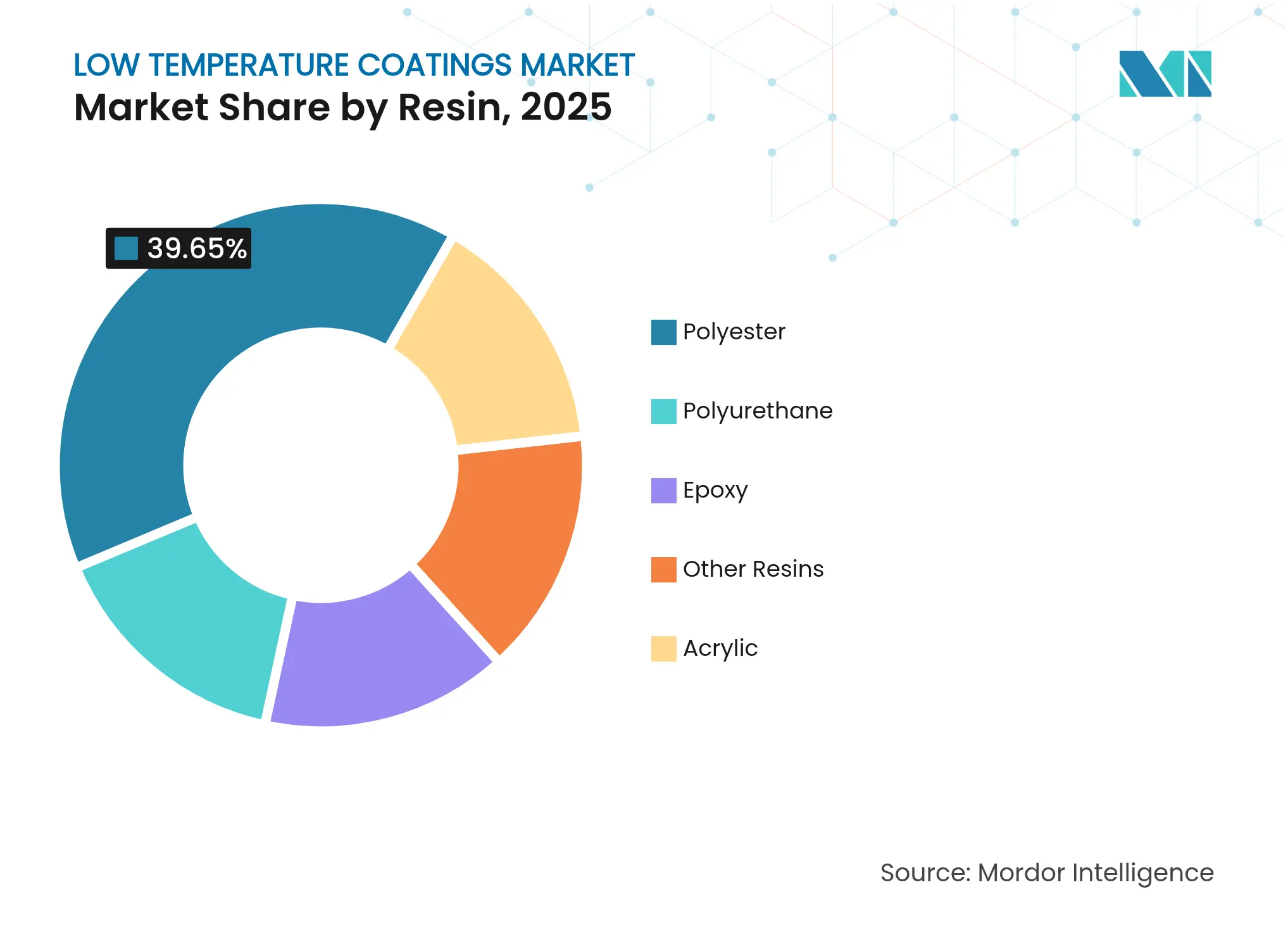

Polyester systems accounted for 39.65% of 2025 revenue, supported by a long record of architectural durability and competitive pricing. Polyesters also bond well to galvanized steel, a high-volume substrate in construction, which cements their baseline position. The low temperature coatings market nevertheless favors polyurethane for applications demanding both flexibility and chemical resistance. Two-component and blocked isocyanate chemistries cure at 120 °C, opening plastic and composite categories that polyesters cannot reach.

Polyurethane volumes are projected to expand at a 6.92% CAGR, the fastest among resins, as EV makers specify flexible dielectric layers for battery covers. Mexico’s 5-7% annual growth in polyurethane consumption underscores global momentum. Water-borne 2K-PUR hybrids meet VOC caps yet still deliver the adhesion required for consumer electronics bezels. These factors together reinforce polyurethane’s rise within the low temperature coatings market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: UV/EB Systems Challenge Powder Dominance

Powder technology held 71.55% of 2025 revenue owing to scale economics and process familiarity. Formulators have driven cure thresholds from 180 °C a decade ago to 140 °C today, slashing energy intake per square meter by roughly one-third. The largest powder suppliers now offer laser-cured systems that reach full properties in three minutes at room temperature, an innovation poised to lift line productivity further.

UV/EB curing is the sprinter, forecast at a 7.12% CAGR to 2031. It merges solvent-free operation with cure temperatures as low as 110 °C, which appeals to MDF furniture lines and vinyl flooring plants. Adoption accelerates whenever operators need instant handling to feed just-in-time assembly zones. These capabilities broaden technological choice and stimulate healthy rivalry inside the low temperature coatings market size segment, where UV/EB solutions already command double-digit shares in industrial wood.

By Substrate: Plastics and Composites Surge Ahead

Metal remained the primary substrate base with 57.25% share in 2025, anchored by infrastructure steel, white goods, and automotive body-in-white. Corrosion standards such as ASTM B117 still lean on metallic corps for benchmark testing, ensuring a durable market core. Even so, plastics and composites are set to record an 7.6% CAGR to 2031 as transportation platforms chase mass reduction targets.

UV-powder blends that fuse at 110 °C have proven effective on polycarbonate headlamp bezels and carbon-fiber body panels. Pretreatments like atmospheric plasma roughen low-energy surfaces, boosting adhesion strength by more than 30% over standard sand-blast routines. The shift enlarges the low temperature coatings market size for non-metallic parts and introduces new value propositions such as EMI shielding and thermal dissipation layers.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End-User Industry: EV Battery Enclosures Drive Innovation

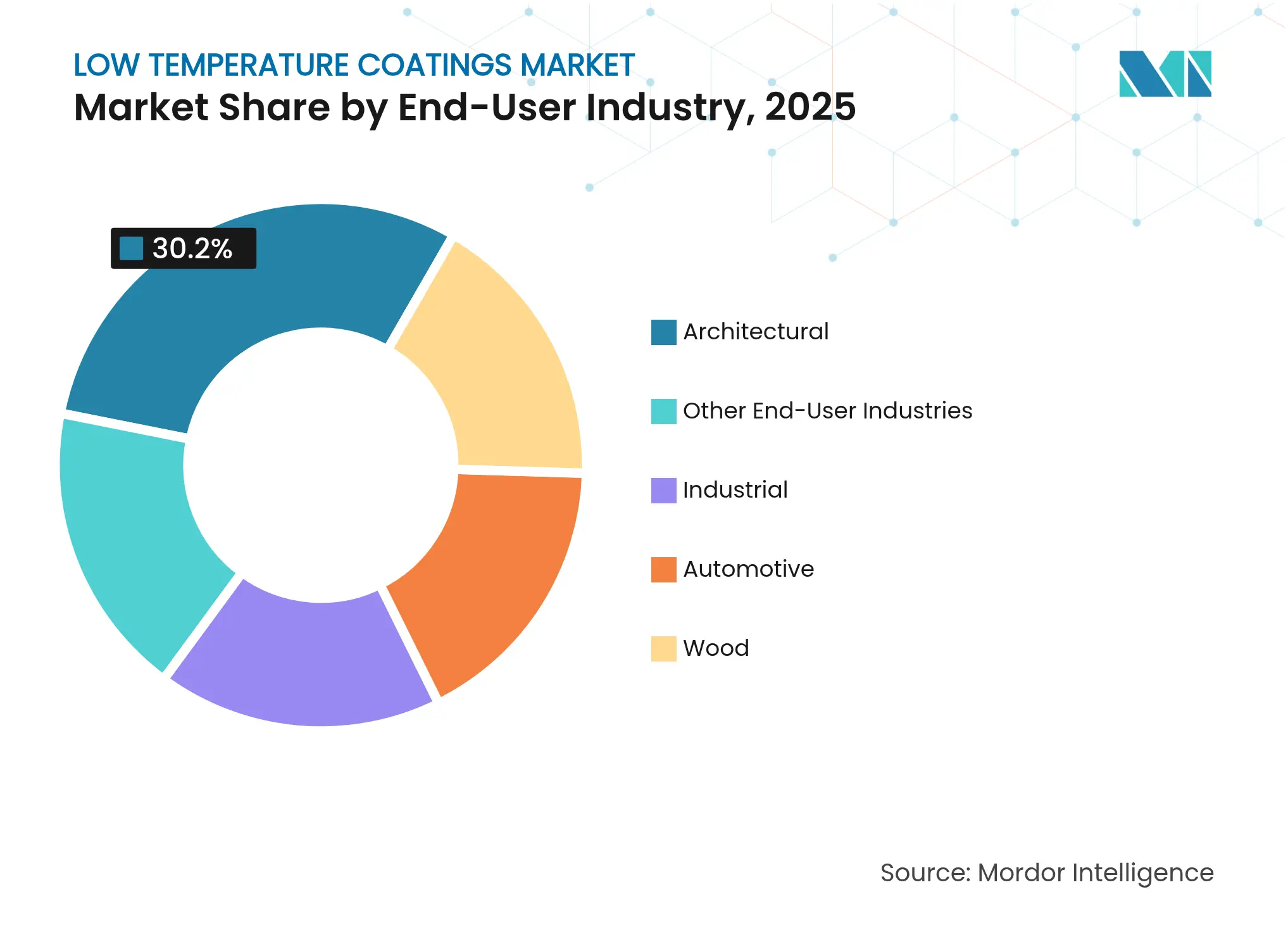

The architectural sector delivered 30.20% of 2025 sales as builders specify cool-roof pigments and low-bake primers to meet green-building codes. Solar-reflective topcoats can drop surface temperatures by 40 °F, reducing HVAC loads and satisfying LEED credits. These features keep architecture an anchor of the low temperature coatings industry.

EV battery enclosures, however, represent the quickest growth vector at 7.48% CAGR. Automakers demand dielectric integrity between -20 °C and 45 °C ambient, a range that low-bake polyurethanes meet without embrittlement. OEM sourcing teams also favour single-step powder routes to remove solvent flash-off rooms, aligning with factory footprints of new gigafactories. The momentum cements transportation electrification as a central driver inside the low temperature coatings market.

Note: Segment shares of all individual segments available upon report purchase

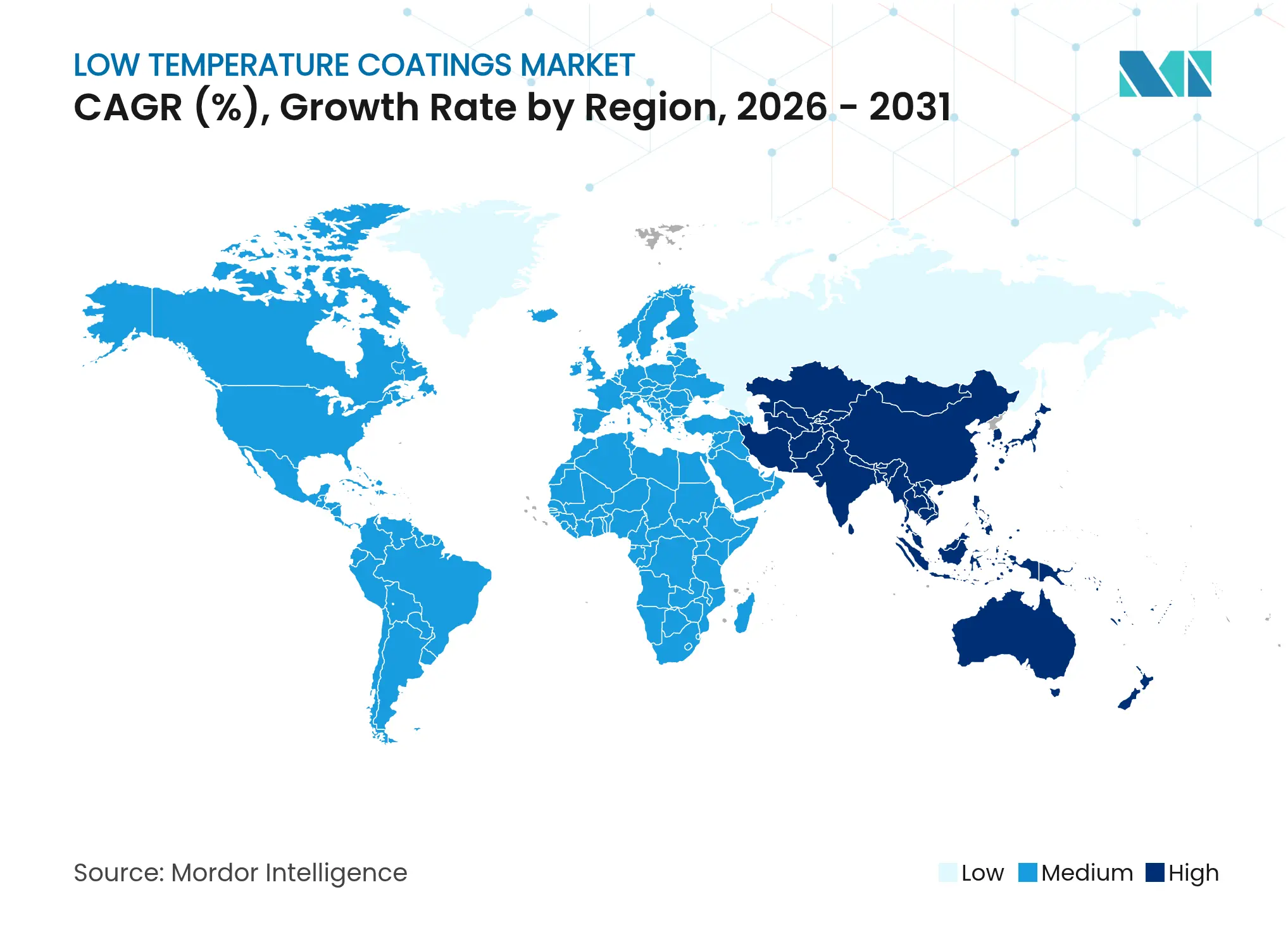

Asia-Pacific dominated the landscape with 45.70% of 2025 revenue and is projected to compound at 6.98% CAGR, the fastest regional clip. China’s vast powder coating clusters benefit from high-volume appliance and EV production, while India’s automotive buildouts and Indonesia’s appliance exports supply additional pull. Rising energy tariffs and intensifying VOC rules in major cities further encourage the adoption of cooler-cure chemistries.

North America ranks second in value; its growth rests on both policy and technology leadership. The U.S. Department of Energy’s funding for laser-cured powder research shortens commercialization timelines, and California’s process-heat regulations translate lab breakthroughs into real purchasing commitments. Mexico adds momentum by expanding coil-coat lines with USD 3.6 million in new capacity, strengthening cross-border supply chains.

Europe matches North America for innovation yet differs by wielding aggressive carbon pricing. The EU Industrial Carbon Management strategy sets explicit storage targets, nudging industrial coaters toward energy-lean options. Meanwhile, manufacturers across the Middle East, Africa, and South America gradually migrate to low-bake systems as multinational customers enforce uniform specifications, enlarging the overall low temperature coatings market footprint.

Market Concentration

Market structure is moderately consolidated with the top tier dominated by Sherwin-Williams, PPG Industries, AkzoNobel, and BASF. Sherwin-Williams expanded its Ohio R&D hub and posted USD 23.1 billion in 2023 net sales, signaling robust cash flow for formulation upgrades. PPG introduced the ENVIRO-PRIME EPIC 200R electrocoat that cures 20 °C lower than its predecessor, unlocking energy savings at automotive plants. AkzoNobel invested USD 3.6 million to lift Mexican coil-coating output by 35%, reinforcing its regional coverage.

Mergers and divestments continue to reshape the field. Nippon Paint’s USD 2.3 billion acquisition of AOC enlarges its Asian presence, while BASF’s move to explore divestiture of its USD 6.8 billion coatings arm may trigger further consolidation. Technology collaborations deepen: Axalta and Dürr Systems jointly commercialize overspray-free digital painting, and PPG partners with Shaw Industries on next-gen resinous flooring. Competitors outside the traditional circle, such as laser-curing specialists and graphene-dispersion start-ups, capture niche share in wind, 3-D-print, and battery markets. The result is an ecosystem where incumbents protect scale yet newcomers inject rapid innovation, collectively advancing the low temperature coatings market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The global low temperature coatings market report includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.