Coating Pretreatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 6.15 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coating Pretreatment Market Analysis by Mordor Intelligence

The Coating Pretreatment Market size was valued at USD 4.81 billion in 2025 and estimated to grow from USD 5.01 billion in 2026 to reach USD 6.15 billion by 2031, at a CAGR of 4.17% during the forecast period (2026-2031). Heightened environmental regulation, the shift toward lightweight vehicle architectures, and the adoption of smart-factory operations are the primary forces influencing revenue growth. Phosphate systems still dominate large-scale automotive lines because of their proven corrosion protection, yet the rapid switch to silane and zirconium nano-coats is accelerating as regulators restrict chromate chemistries. Smart inline monitoring, particularly in automotive body shops, is driving higher chemical efficiency, while the aerospace sector’s move to composite structures opens a premium niche for advanced adhesion promoters. On the competitive front, diversified suppliers with chrome-free portfolios gain share, whereas traditional phosphate specialists face margin compression from costly energy inputs and CAPEX-intensive line upgrades.

Key Report Takeaways

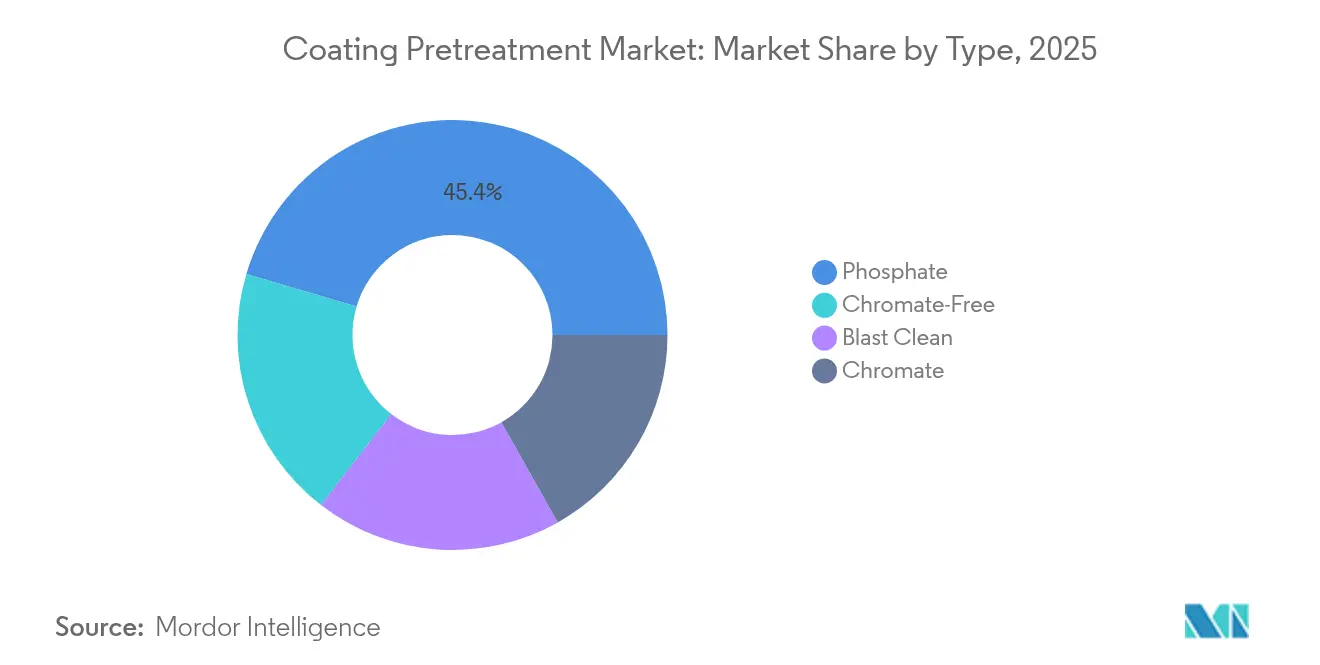

- By type, phosphate systems retained 45.42% of coating pretreatment market share in 2025, while silane technologies are projected to advance at a 5.57% CAGR through 2031.

- By metal substrate, steel accounted for 59.62% of the coating pretreatment market size in 2025, whereas aluminum is forecast to grow at 5.34% CAGR to 2031.

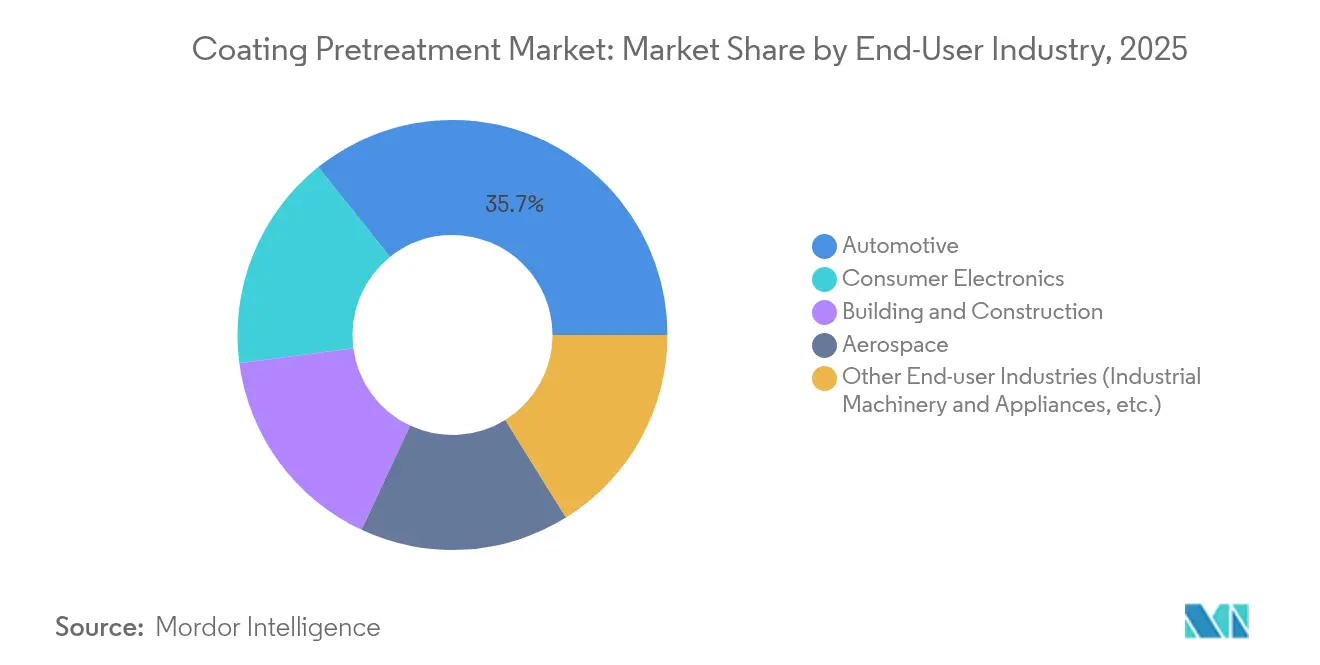

- By end-user industry, automotive and transportation captured 35.74% revenue share in 2025; consumer electronics is anticipated to post the fastest 5.27% CAGR through 2031.

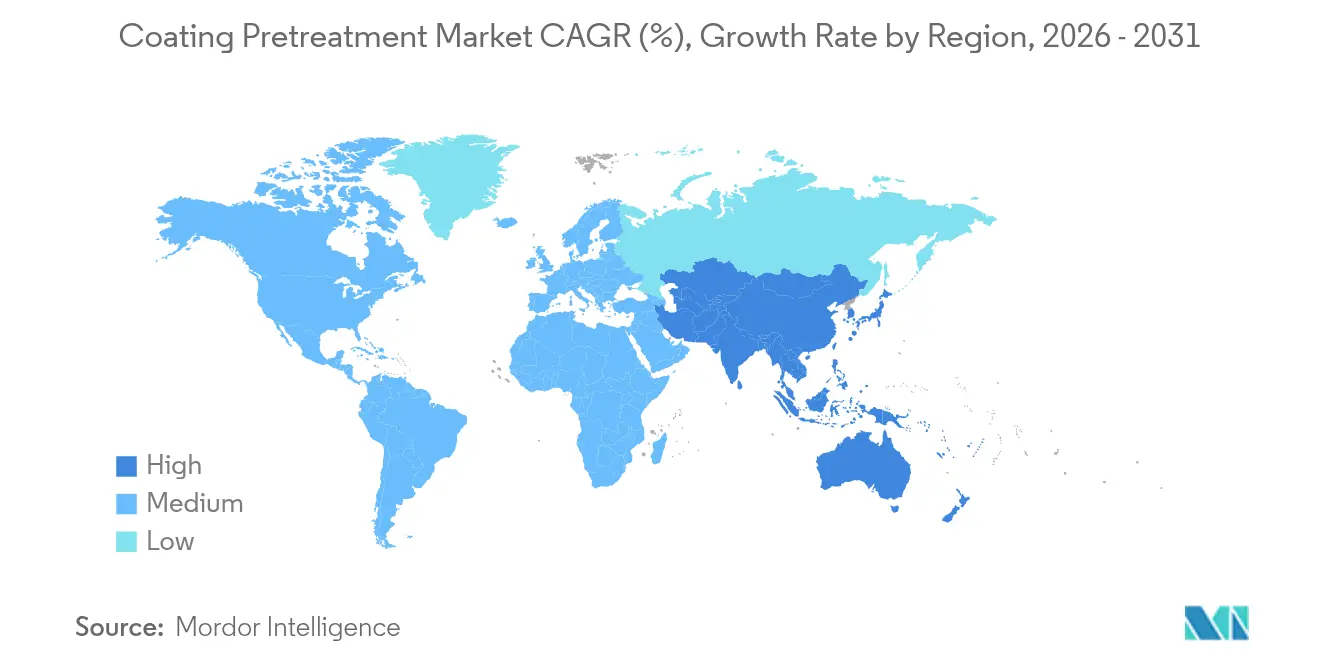

- By geography, Asia-Pacific led with a 44.78% share of the coating pretreatment market size in 2025 and is set to expand at 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coating Pretreatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging OEM demand for phosphate-based multi-metal systems | +1.2% | Global, with concentration in North America & Asia-Pacific | Medium term (2-4 years) |

| Rapid switch to eco-friendly zirconium and silane nano-coats | +1.8% | Europe & North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Smart-factory retrofits boosting inline pretreatment adoption | +0.7% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Aerospace composites requiring novel adhesion promoters | +0.4% | North America & Europe primarily | Long term (≥ 4 years) |

| OEM warranty extensions driving corrosion-resistance specs | +0.6% | Global, strongest in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging OEM Demand for Phosphate-Based Multi-Metal Systems

Global automakers continue to favor advanced zinc phosphate baths that deliver reliable corrosion protection on mixed-metal body-in-white assemblies. PPG’s Versabond formulation enables fast kinetics and consistent crystal formation, allowing line speeds to rise without compromising quality. The rise of battery-electric vehicles intensifies the need for galvanic-corrosion mitigation between steel frames and aluminum battery housings. Toyota’s USD 922 million Kentucky paint-shop upgrade exemplifies OEM commitment to high-throughput, multi-metal capable processes. Asian steelmakers echo this trend: Angang Guangzhou commissioned an additional 400,000 tpa galvanizing line to feed expanded vehicle output.

Rapid Switch to Eco-Friendly Zirconium and Silane Nano-Coats

European REACH updates and the UK’s 2024 chromate ban catalyze adoption of low-sludge zirconium and silane chemistries[1]European Commission, “Authorisation for Use of Substances under REACH,” european-commission.europa.eu . BASF’s Oxsilan and PPG’s ZircoBond deliver equivalent corrosion protection at half the coating weight of conventional phosphates while cutting sludge up to 80%. Silane nano-layers polymerize at room temperature, lowering energy use by around 30% compared with 60–70 °C phosphate baths. As OEMs pursue Scope 3 emission cuts, these low-energy chemistries become integral to plant decarbonization roadmaps.

Smart-Factory Retrofits Boosting Inline Pretreatment Adoption

Industry 4.0 tools—inline pH probes, ML-driven dosing algorithms, and vision-guided robot sprayers—have shrunk chemical usage and scrap rates. PPG’s digital transformation raised a US plant’s monthly revenue by USD 400,000 while trimming recordable injuries 6.5%. ABB’s Paint 4.0 suites push first-pass yields near 100% through early defect detection. Dürr installed 120 EcoBell3 atomizer robots at BYD’s European paint shop, capturing quality data in real time to optimize film build.

Aerospace Composites Requiring Novel Adhesion Promoters

The growing ratio of carbon-fiber structures in aircraft drives demand for chromate-free primers that bond to non-metallic substrates. The University of Oklahoma secured USD 4.8 million to advance non-toxic aerospace primers that meet MIL-SPEC durability standards. PPG’s adhesion-promoter range, designed for composite fuel tank and nacelle components, pairs with low-VOC topcoats to satisfy OEM sustainability targets. Electrochemical oxidation treatments on carbon fiber have lifted interfacial shear strength by 48.8%, demonstrating material-level innovations critical to next-gen aircraft.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening chromate regulations and disposal costs | -1.1% | Global, most severe in Europe & North America | Short term (≤ 2 years) |

| Energy-intensive high-temperature phosphate lines | -0.8% | Global, particularly impacting energy-intensive regions | Medium term (2-4 years) |

| Rising CAPEX for multi-metal flexible lines | -0.5% | Global, affecting smaller players disproportionately | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Chromate Regulations and Disposal Costs

The UK’s September 2024 prohibition on hexavalent chromium pretreatments underscores fast-moving policy action, exposing legacy chrome users to sudden competitive risks. California’s Air Resources Board mandates full phase-out of hex-chrome decorative plating by 2030, offering USD 10 million in grants but leaving many small platers facing steep retrofit bills[2]California Air Resources Board, “Chrome Plating ATCM Amendments,” arb.ca.gov. Hazardous-waste disposal fees continue to climb as permitted treatment capacity tightens, compelling manufacturers to accelerate R&D on trivalent or non-chromium routes.

Energy-Intensive High-Temperature Phosphate Lines

Maintaining phosphate baths at 60–70 °C absorbs sizeable electrical and steam loads. In Europe, carbon taxes inflate operating costs, pushing total pretreatment energy outlays toward 25% of line OPEX. Audi’s Neckarsulm wet-on-wet paint project showed energy savings of 140 kWh per vehicle by re-engineering bake and flash zones. The financial case for room-temperature silane or zirconium pathways strengthens as volatile natural-gas prices erode phosphate economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silane Innovation Challenges Phosphate Dominance

Phosphate baths held 45.42% of the coating pretreatment market in 2025 thanks to entrenched OEM approvals and broad substrate compatibility. They remain the default for high-volume, corrosion-critical applications such as automotive underbodies. However, silane chemistries are expanding at a 5.57% CAGR because of lower sludge generation and ambient-temperature processing that minimizes energy spend. The coating pretreatment market size for silane platforms is on track to double by 2031 as sustainability mandates intensify, while chromate share collapses under legislative pressure. Suppliers differentiate through hybrid zirconium-silane formulations that combine nano-layer uniformity with faster cure windows, helping line operators avoid throughput penalties.

Silane suppliers also benefit from easier waste-water management; discharge limits tighten worldwide, and nano-coats typically exhibit lower metals load. Process simplicity further appeals to electronics finishers that require tight film-build control on intricate geometries. As OEMs harmonize approval specifications across global plants, silane adoption is poised to accelerate in Asia’s greenfield factories, narrowing phosphate’s historical cost advantage.

By Metal Substrate: Aluminum Growth Outpaces Steel Dominance

Steel dominated with 59.62% coating pretreatment market share in 2025 because most mass-produced cars still rely on press-hardened steel for passenger-cell strength. Zinc-phosphate layers on steel achieve paint-adhesion metrics that meet stringent 10-year anti-perforation warranties. Despite that dominance, the aluminum sub-market is growing 5.34% annually, reflecting automotive lightweighting and the broader use of aluminum skins in mobiles and laptops. The coating pretreatment market size attributed to aluminum is projected to close the gap as EV makers favor extruded battery enclosures and hood assemblies.

Process engineers now integrate non-etch silane cleaners that preserve brushed finishes on premium electronics housings, preventing micro-pitting that can appear under anodized colors. Aerospace primes for aluminum-lithium alloys incorporate sol-gel precursors that enable robust bonding to composite fairings. Together, these technical advances underpin aluminum’s rising throughput share across global pretreatment lines.

By End-User Industry: Electronics Surge Challenges Automotive Dominance

Automotive accounted for 35.74% of total revenue in 2025, reflecting the sector’s large unit volumes and tight OEM corrosion standards. Yet the electronics segment is projected to grow 5.27% CAGR through 2031 as high-end smartphones and wearables demand flawless cosmetic coatings. The coating pretreatment market share leadership may gradually diversify as consumer electronics brands specify chrome-free, low-VOC chemistries that also work on magnesium and stainless sub-frames.

Aerospace remains a value-rich but lower-volume customer, buying sophisticated adhesion promoters for composite wings and nacelles. Building and construction applications, such as coil-coated roofing panels with cool-pigment fluoropolymers, sustain steady demand for phosphoric-based cleaners, while heavy machinery and appliance manufacturers adopt hybrid zirconium technologies to balance cost and durability.

Geography Analysis

Asia-Pacific held 44.78% of global revenue in 2025 and is forecast to expand 5.12% annually to 2031, cementing its position as both the largest and fastest-growing regional hub. China’s electric-vehicle surge drives extensive investments in multi-metal pretreatment capacity, illustrated by BYD’s new European plant equipped with over 120 Dürr robots designed in Shenzhen for export installations. Japanese Tier-1 suppliers focus on low-sludge nano-coats to align with corporate carbon-neutral pledges, while Vietnam’s electronics boom spurred PPG to double its local waterborne-coating output.

North America leverages deep aerospace and light-truck production, with smart-factory retrofits leading to faster digital uptake. Europe tightens regulatory screws, forcing line conversions to chrome-free chemistries ahead of other regions. South America and the Middle East & Africa, although smaller, represent upside tied to vehicle assembly shifts and infrastructure expansion requiring corrosion-resistant steel fabrication. The coating pretreatment market size in these emerging regions remains modest today but attracts multinational suppliers keen to localize service capability.

Competitive Landscape

The market demonstrates moderate consolidation: the top five companies together control about 60% of global revenue, yet numerous regional applicators and chemical formulators thrive in specialist niches. PPG, Henkel, Chemetall, Quaker Houghton, and Nippon Paint anchor the leadership tier, wielding broad product catalogs and multi-regional manufacturing. PPG allocated USD 300 million for North American plant automation, capturing 30% productivity gains from digital dashboards. Quaker Houghton’s USD 153 million purchase of Dipsol Chemicals expanded its Asia-Pacific steel-pretreatment footprint to serve automakers in Thailand and Indonesia.

Niche innovators target chrome-free solutions: OxMet Technologies advances zirconium-silane blends for aerospace MRO, while start-ups like Coventya Digital deliver cloud-linked dosing pumps for medium-sized coaters. Incumbents emphasize service contracts and on-site lab support to lock in consumables revenue amid rising raw-material volatility. Overall, suppliers with agile R&D and shared intellectual property agreements gain a strategic edge as OEM qualification cycles shorten under sustainability pressure.

Coating Pretreatment Industry Leaders

Henkel AG & Co. KGaA

PPG Industries, Inc.

Axalta Coating Systems, LLC

BASF

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Henkel Adhesive Technologies published a white paper on cleaner and coater technology, enabling single-step metal pretreatment. This innovation reduces process steps by half, conserving energy and water.

- October 2023: Sherwin-Williams Aerospace Coatings introduced Jet Prep Pretreatment, a chrome-free, water-based sol-gel for aluminum substrates in aerospace. The two-part kit provides corrosion protection and adhesion, compatible with aerospace-grade epoxy primers and topcoat systems.

Global Coating Pretreatment Market Report Scope

The coating pretreatment market report includes:

| Phosphate |

| Chromate |

| Chromate-Free |

| Blast Clean |

| Steel |

| Aluminum |

| Automotive |

| Aerospace |

| Consumer Electronics |

| Building and Construction |

| Other End-user Industries (Industrial Machinery and Appliances, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Phosphate | |

| Chromate | ||

| Chromate-Free | ||

| Blast Clean | ||

| By Metal Substrate | Steel | |

| Aluminum | ||

| By End-User Industry | Automotive | |

| Aerospace | ||

| Consumer Electronics | ||

| Building and Construction | ||

| Other End-user Industries (Industrial Machinery and Appliances, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the coating pretreatment market size in 2026 and how fast is it growing?

The market is valued at USD 5.01 billion in 2026 and is projected to expand to USD 6.15 billion by 2031 at a 4.17% CAGR.

Which region currently holds the largest share of the coating pretreatment market?

Asia-Pacific leads with 44.78% of global revenue in 2025 and is also the fastest-growing region at a 5.12% CAGR through 2031.

Why are silane-based pretreatments gaining rapid adoption?

Silane chemistries operate at ambient temperature, cut sludge by up to 80%, and align with strict environmental rules, driving their 5.57% CAGR.

How do smart-factory retrofits influence pretreatment operations?

Inline sensors and machine-learning dosing tools have boosted first-pass quality near 100% and lifted plant productivity by roughly 30%.

Page last updated on: