Logging While Drilling (LWD) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

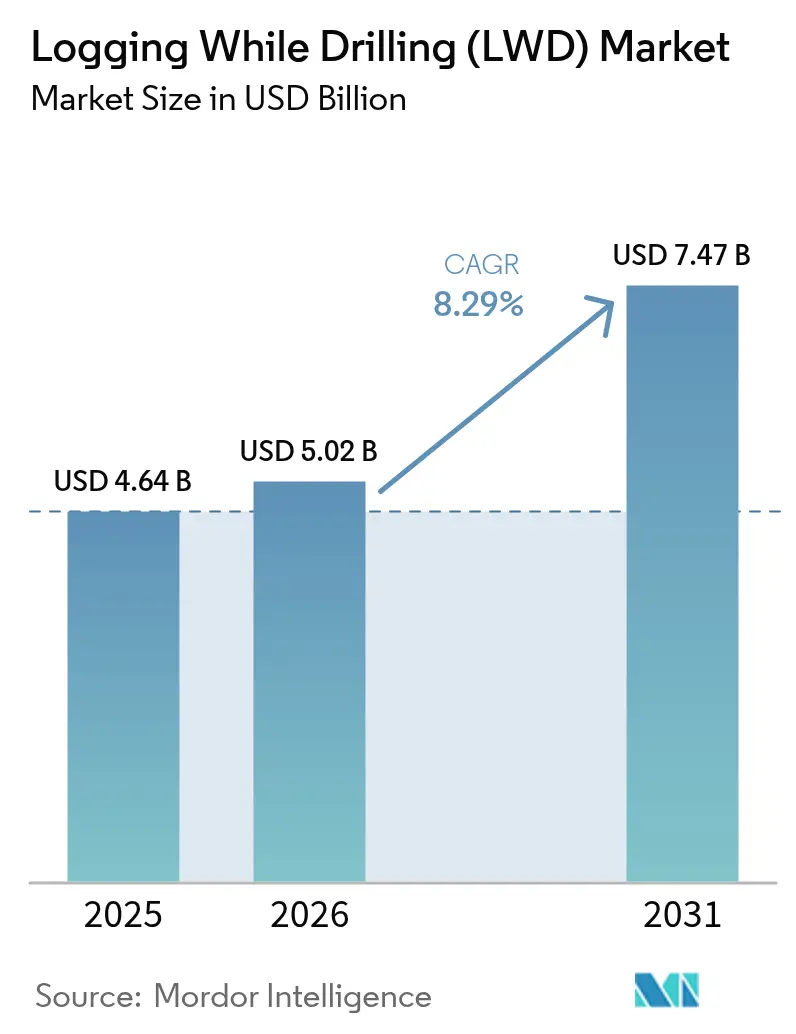

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 7.47 Billion |

| Growth Rate (2026 - 2031) | 8.29% CAGR |

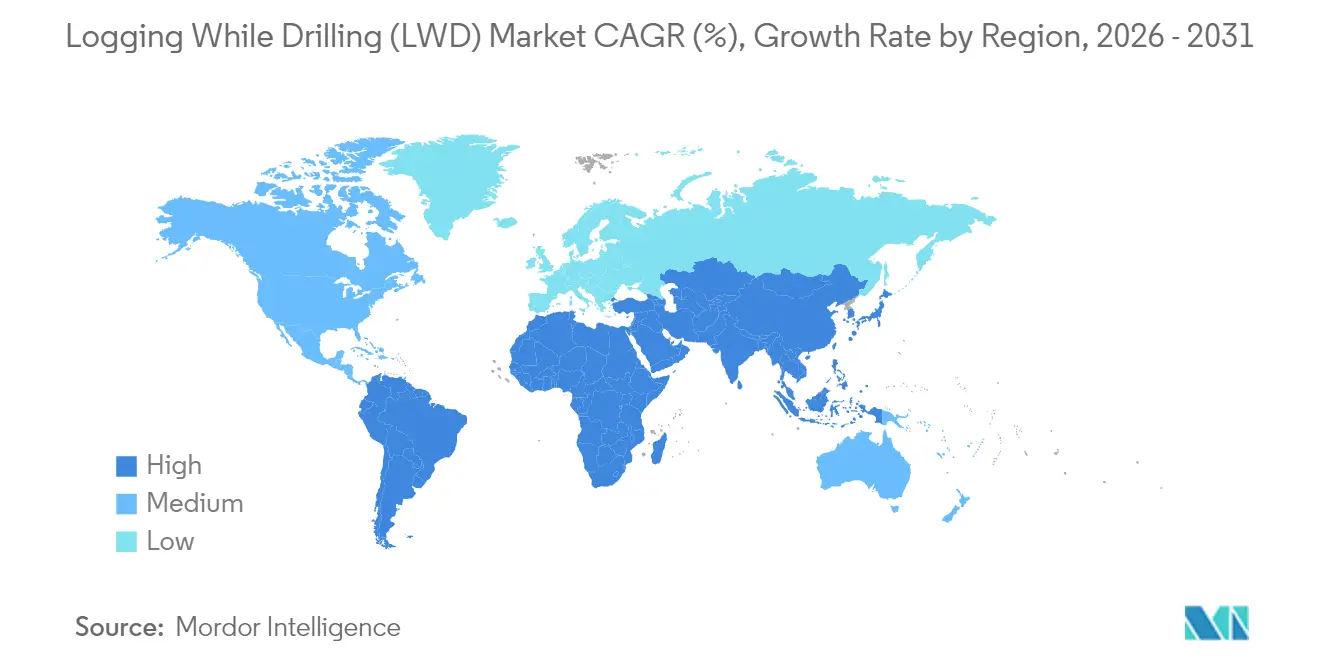

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Logging While Drilling (LWD) Market Analysis by Mordor Intelligence

Logging While Drilling market size in 2026 is estimated at USD 5.02 billion, growing from 2025 value of USD 4.64 billion with 2031 projections showing USD 7.47 billion, growing at 8.29% CAGR over 2026-2031.

Strong growth stems from operators’ preference for real-time formation evaluation and autonomous drilling systems that shorten well construction cycles, reduce non-productive time, and improve wellbore placement accuracy. Horizontal and directional drilling activity continues to expand, particularly in unconventional resource plays and ultra-deepwater prospects, where precise reservoir navigation is essential. Digital-oilfield automation budgets are rising in parallel, accelerating the deployment of AI-enhanced geosteering tools that link downhole sensors with surface control software. Diversification into geothermal and nascent natural-hydrogen drilling is opening new high-temperature service niches, providing a hedge against oil-price volatility. Competitive intensity is elevated as top service providers race to roll out electric well control platforms, at-bit imaging, and remote operations centers capable of supervising multiple rigs simultaneously.

Key Report Takeaways

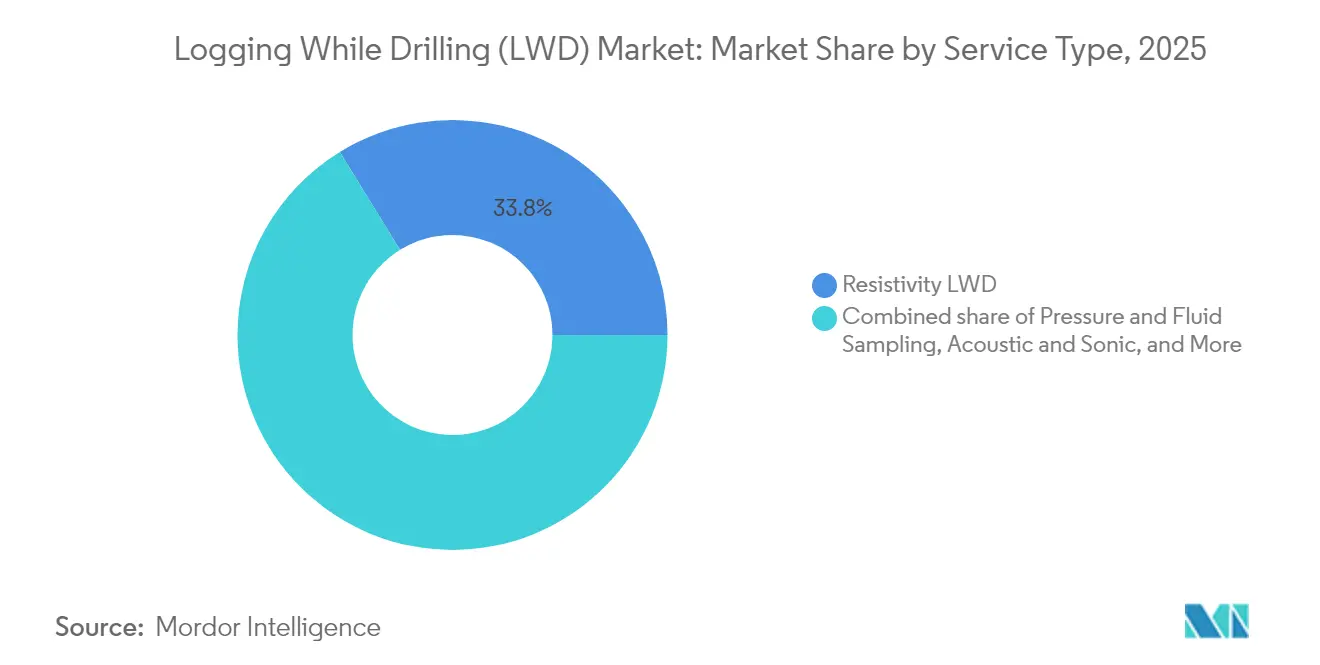

- By service type, resistivity LWD led with a 33.78% share of the logging while drilling market in 2025, while pressure and fluid sampling is projected to grow at a 10.95% CAGR.

- By application, formation evaluation accounted for a 42.35% share of the logging while drilling market size in 2025, and the geosteering and reservoir navigation segment is expanding at a 9.85% CAGR.

- By well type, conventional vertical wells accounted for 35.92% of the logging while drilling market size in 2025, while horizontal wells recorded the highest projected CAGR of 9.57% through 2031.

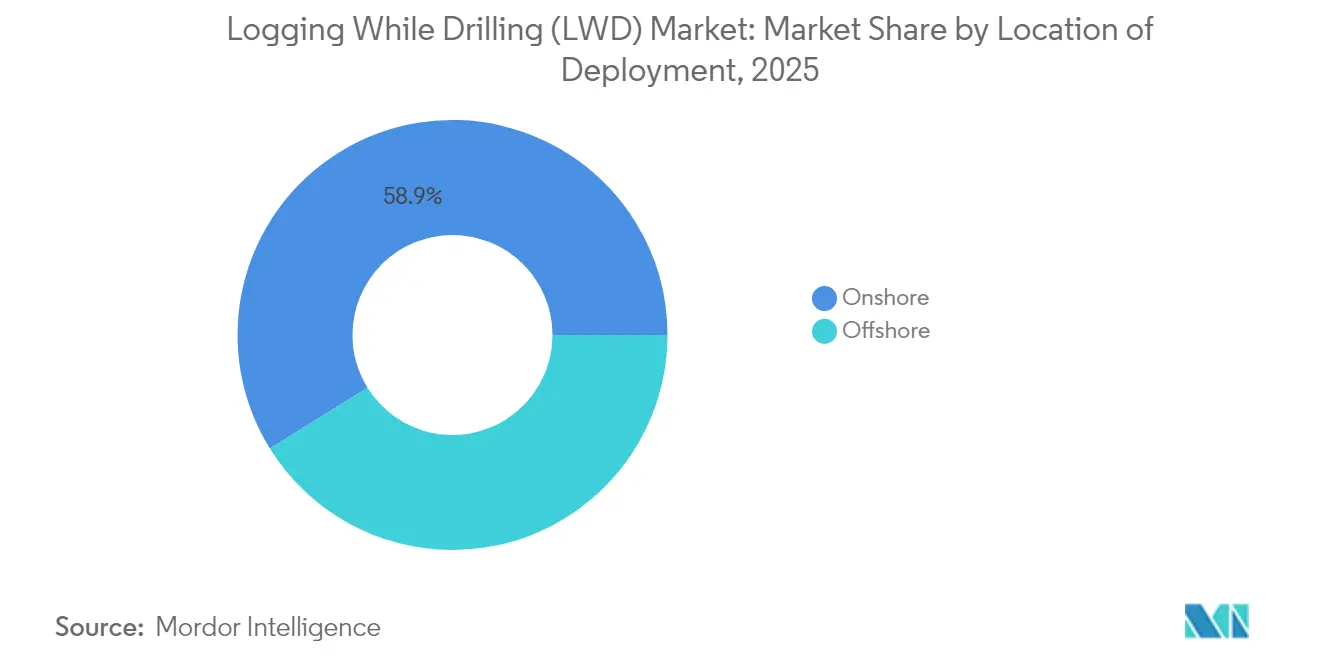

- By location of deployment, onshore operations accounted for 58.85% of the logging while drilling market size in 2025; offshore deployment is forecast to grow at a 9.28% CAGR to 2031.

- By geography, North America commanded 31.42% of the logging while drilling market share in 2025, whereas the Middle East and Africa are the fastest-growing regions, with a 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Logging While Drilling (LWD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising shale & deep-water drilling activity | 2.10% | North America, Brazil, Norway, UK | Medium term (2-4 years) |

| Adoption of real-time formation evaluation | 1.80% | Global, with early gains in North America, Middle East | Short term (≤ 2 years) |

| Surge in horizontal & directional wells | 1.50% | North America, Middle East, China | Medium term (2-4 years) |

| Digital-oilfield automation budgets | 1.20% | Global, spill-over to emerging markets | Long term (≥ 4 years) |

| Geothermal & natural-hydrogen well demand | 0.90% | Europe, North America, select Asia-Pacific | Long term (≥ 4 years) |

| Ultra-deep resistivity tools for SAGD heavy-oil | 0.60% | Canada, Venezuela, select Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Shale & Deep-Water Drilling Activity

Deepwater rig utilization averaged 92% in 2024 as operators pursued higher-return fields in Brazil’s pre-salt and the Gulf of Mexico, boosting demand for real-time downhole data that wireline tools cannot deliver in unstable boreholes.[1]Staff Report, “Deepwater Rig Utilization Hits 92%,” Rigzone, rigzone.com SLB’s USD 800 million contract covering more than 100 Petrobras wells underlines the scale of upcoming ultra-deepwater campaigns that depend on autonomous geosteering to navigate complex reservoirs. The Permian Basin adds further volume: longer laterals and multizone completions require continuous formation evaluation to maintain contact with the pay zone.

Adoption of Real-Time Formation Evaluation

Halliburton’s LOGIX automation platform showed up to 30% gains in rate of penetration after integrating downhole resistivity and gamma-ray telemetry with surface algorithms that adjust weight-on-bit and rotary speed.[2]Technical Team, “LOGIX Automation Delivers 30% ROP Uplift,” World Oil, worldoil.com SLB’s Neuro system steered a well in Ecuador through 25 automated trajectory corrections without manual oversight, illustrating how AI closes the loop between subsurface data and bit direction. Eliminating separate wireline runs trims 10-15% off total well construction time in complex deviated wells, making real-time formation evaluation a universal requirement in high-cost environments.

Surge in Horizontal & Directional Wells

Horizontal wells are the fastest-growing well type, expanding at a 9.8% CAGR as operators exploit thin pay zones in shale and carbonates. China’s ultra-deep initiative, targeting wells with depths of 8,000 meters in the Tarim and Junggar basins, pushes LWD tools to operate under bottom-hole temperatures of 240 °C. High-frequency electromagnetic tools now place the bit within ±3 cm of formation boundaries, boosting recovery from narrow targets.

Digital-Oilfield Automation Budgets

Capital earmarked for robotics, edge computing, and electric well control systems continues to rise, particularly among super-majors that prioritize safety and operating cost efficiency. SLB’s EWC platform replaces hydraulics with electric actuators, enabling finer control and real-time diagnostics that cut non-productive time. Closed-loop drilling, where LWD measurements automatically adjust the trajectory and mud weight, is transitioning from pilot to standard practice in high-volume shale pads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility curbing E&P CAPEX | -1.40% | Global, with acute impact in North America shale | Short term (≤ 2 years) |

| Tightening ESG & environmental mandates | -0.80% | Europe, North America, select Asia-Pacific | Medium term (2-4 years) |

| RF-telemetry bandwidth congestion | -0.50% | Global, particularly deepwater operations | Medium term (2-4 years) |

| Rare-earth sensor supply bottlenecks | -0.30% | Global, with supply concentration in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Curbing E&P CAPEX

US independents trimmed their drilling budgets during 2024-2025, despite Brent prices hovering near USD 80 per barrel, preferring debt reduction and dividends over growth spending.[3]Anjli Raval, “US Shale Drillers Reconsider Capex Plans,” Financial Times, ft.com Global E&P investment is forecast to hold around USD 60-65 billion in 2025, suppressing early-stage exploration where LWD demand is highest. Although deepwater megaprojects are proceeding, smaller shale operators are focusing on generating free cash flow and making slow additions to their rig fleet.

Tightening ESG & Environmental Mandates

The US methane fee, starting in 2025, imposes a fee of up to USD 1,500 per metric ton emitted, forcing operators to reassess the economics of marginal wells.[4]Environmental Protection Agency, “Methane Emissions Reduction Program,” EPA, epa.gov European regulators require comprehensive environmental impact assessments for new offshore developments, extending permitting timelines. Compliance costs drive some operators to defer projects, though the same rules spur demand for high-precision LWD tools that reduce invisible losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Resistivity LWD Maintains Dominance Amid Sampling Technology Surge

Resistivity services generated 33.78% of the logging while drilling market size in 2025, confirming their status as the baseline measurement required on nearly every well. Their ability to flag hydrocarbon-bearing zones in real-time ensures continued adoption in both land and offshore programs. The segment benefits from machine-learning algorithms that now convert resistivity curves into lithology predictions while drilling, further embedding the measurement into automated workflows. Pressure and fluid sampling, although a smaller slice today, is projected to lead growth at 10.95% CAGR as operators seek dynamic formation pressure data and fluid typing without halting drilling. SLB’s SpectraSphere tool and Baker Hughes’ AziTrak family exemplify this trend by enabling downhole PVT sampling that formerly required separate wireline runs. Across mature basins, gamma-ray, density-neutron, and acoustic packages remain staples for porosity and lithology assessment, while borehole imaging is enjoying renewed interest in fractured carbonates, where visualization guides completion design.

The competitive landscape within the services sector is characterized by continuous sensor miniaturization and increased data bandwidth for telemetry. Resistivity tools now transmit multi-depth measurements at 30-bps mud-pulse rates, allowing simultaneous transmission of gamma and pressure data streams. In sampling, downhole spectroscopic analysis enables the identification of moving fluids from surface labs to real-time rig displays, thereby improving decision accuracy. These technology upgrades position both traditional and emerging services to capture incremental spending as digital oilfield budgets rise.

By Application: Formation Evaluation Leadership Challenged by Geosteering Innovation

Formation evaluation controlled 42.35% of the logging while drilling market share in 2025 because every spud requires reservoir and fluid characterization. Tools that deliver porosity, resistivity, density, and sonic logs while drilling cut days from well construction, saving USD 400,000-600,000 per deepwater well. Geosteering, however, is expanding at a 9.85% CAGR as horizontal laterals stretch past 10,000 ft and pay zones narrow to less than 10 ft. Autonomous systems like Neuro use downhole resistivity images to pivot the bit within seconds, maximizing production rates from thin targets. Wellbore stability monitoring is also gaining traction in HPHT wells, where real-time caliper and sonic shear measurements provide early warnings of breakout risks. Finally, real-time drilling optimization blends LWD data with surface analytics to maximize penetration rate while safeguarding hole quality, underpinning the push toward self-driven rigs.

In practical terms, geosteering’s rise reflects the economic premium on precise placement. A single misalignment can reduce the net present value of a North Sea well by EUR 2 million, incentivizing the adoption of AI-supported trajectories. The relative weight of formation evaluation may erode over time, but it remains indispensable, as pressure and saturation models feed reservoir simulation tools that dictate field development strategies.

By Well Type: Conventional Vertical Wells Face Horizontal Drilling Disruption

Vertical wells still comprised 35.92% of the logging while drilling market size in 2025, driven by mature onshore fields and geothermal projects where simpler trajectories are sufficient. However, horizontal wells show the strongest momentum, with a 9.57% CAGR, because longer laterals unlock higher EUR per pad and reduce surface footprint. Extended-reach wells drilled from fixed platforms in the North Sea and Caspian Sea now span 12 km, requiring multi-depth resistivity and pressure-while-drilling to keep the bit within a 2-m window. HPHT wells remain a niche in terms of count but are highly lucrative: service day rates can double due to 300 °C requirements, composite mandrels, and real-time shock mitigation. In each category, the logging while drilling market benefits as complexity drives the need for richer sensor suites.

Horizontal proliferation also reshapes service delivery models. Factory-style pad drilling in the Permian Basin utilizes standardized bottom-hole assemblies, employing a single resistivity platform across dozens of wells, which significantly reduces mobilization time. Conversely, ultra-deep exploration, such as China’s 8,000 m targets, relies on bespoke HPHT tools. These divergent trends illustrate why vendors must maintain a broad catalog ranging from low-cost land solutions to titanium-hulled deepwater kits.

By Location of Deployment: Offshore Growth Outpaces Onshore Despite Market Share Gap

Onshore operations owned 58.85% of the logging while drilling market share in 2025, as global rig counts remain skewed toward land, especially in shale regions. Yet, offshore projects are forecast to expand by 9.28% CAGR through 2031, buoyed by developments in Brazil’s Santos Basin, Mexico’s Trion field, and West African deepwater areas. The offshore growth advantage reflects large well budgets where each hour of rig time exceeds USD 500,000, justifying premium LWD packages that shorten drilling days. Floating rigs in 2,000 m water depths now require downhole systems rated to 25,000 psi and 200 °C, pushing engineering boundaries and driving up service pricing. Onshore remains critical for volume, especially in factory-style shale pads, where telemetry speed and ruggedness are more important than high-end petrophysics.

Ultimately, offshore gains offset onshore volume swings caused by oil-price cycles. As IOC portfolios shift toward deepwater assets with breakevens in the high USD 30s per barrel, demand for AI-driven LWD precision increases. Onshore still offers steady revenue among national oil companies, particularly in the Middle East, where multi-well clusters benefit from standardized assemblies.

Geography Analysis

North America retained 31.42% of the logging while drilling market share in 2025, driven by shale drilling in the Permian Basin, Bakken, and DJ Basin, as well as deepwater activdeepwatere the Gulf of Mexico. Operators here deploy advanced geosteering with edge computing to extract incremental barrels from stacked pays and to drill 3-mile laterals on a single curve. Canadian oil-sands SAGD operations also rely on ultra-deep resistivity to manage steam conformance, while Mexico’s first field development under new PSC terms, Trion, introduces ultra-deepwater demand. The regional CAGR is forecasted at 7.92% to 2031, supported by ample Tier-1 shale inventory and stable service infrastructure.

The Middle East and Africa are expected to exhibit the fastest expansion at a 10.02% CAGR through 2031. Saudi Aramco’s 2025-2030 drilling plan, backed by Vision 2030 targets, drives sustained rig demand, with ADNOC’s USD 750-950 million rig-fleet upgrade similarly stimulating LWD uptake. Offshore West Africa sees pre-sanction momentum in Nigeria’s Bonga Southwest and Senegal’s Yakaar-Teranga, encouraging orders for HPHT-capable sensors. Local content regulations in the UAE, Qatar, and Nigeria compel service providers to invest in regional manufacturing, deepening market penetration.

Asia-Pacific region stands out for its technical ambition rather than volume. China’s state majors are pursuing 8,000-m targets in Tarim and Junggar, mandating electronics that can survive bottom-hole temperatures of 240 °C. India’s OALP-round acreage spurs exploration in deepwater Krishna-Godavari blocks, while Australia expands LNG feedstock drilling in Browse and Bonaparte basins. Regional rig demand accounts for 36% of global fleet requirements, giving the Asia-Pacific region a growing influence on tool-specification roadmaps.

Europe sustains moderate growth from North Sea tie-back campaigns and burgeoning geothermal pilots in Germany, the Netherlands, and Iceland. Operators there seek ultra-high-temperature tools and carbon-accounting features to comply with EU taxonomy rules. Latin America exhibits a two-speed dynamics: Brazil’s pre-salt ultra-deepwater complex remains a magnet for premium services, in contrast to Argentina’s Vaca Muerta shale, where land rig counts fluctuate in line with macroeconomic trends. Across geographies, the logging while drilling market benefits from varied drivers, but converges on a common theme: sensor-rich, digitally integrated bottom-hole assemblies.

Competitive Landscape

The logging while drilling market is moderately concentrated. SLB, Baker Hughes, and Halliburton together control 35-40% of global revenue, leveraging decades of R&D investment and worldwide logistics networks. SLB’s 12.4% share is underpinned by its SpectraSphere fluid mapping, Ora wireline testing, and recent USD 800 million Petrobras contract covering 100 offshore wells. Baker Hughes captures roughly 10.0% through neural-network-driven drilling systems that predict torque and drag in real-time, while Halliburton holds 8.1-15.4% via its LOGIX platform, which improved the rate of penetration by 30% in field trials. Mid-tier challengers, such as Weatherford, NOV, and China Oilfield Services (COSL), pursue market share through lower-cost offerings and regional partnerships.

Technology differentiation is moving beyond individual tools to integrated ecosystems that encompass telemetry, cloud analytics, and remote control. SLB’s Neuro suite enables one engineer to control multiple wells from a Houston center, while Baker Hughes embeds predictive maintenance modules that flag MWD motor wear before it fails. Geothermal and natural-hydrogen pilots open up white space where NOV’s Phoenix bits and insulating drill-pipe coatings excel at temperatures exceeding 300 °C at the bottom hole. Regional players benefit from local content policies: COSL and Sinopec Service capture Chinese projects leveraging domestic manufacturing, while Scientific Drilling gains traction in niche re-entry and multilateral wells through gyro-based MWD systems.

M&A potential remains moderate. Integrated energy companies are now weighing the divestiture of non-core services, creating acquisition opportunities for private-equity-backed specialists. Still, the high capital barrier of tool design and certification limits new entrants. For incumbents, a competitive advantage hinges on AI integration, battery-less telemetry, and closed-loop drilling, which reduces the need for staffed personnel offshore, thereby enhancing both cost and ESG performance metrics.

Logging While Drilling (LWD) Industry Leaders

Schlumberger Limited

Halliburton Company

Weatherford International Plc.

Baker Hughes Company

National Oilwell Varco

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SLB secured a multi-year contract from Woodside Energy to deliver AI-enabled drilling services for the Trion ultra-deepwater development offshore Mexico.

- April 2025: SLB released electric well control technology, replacing hydraulics for instant actuation and continuous power monitoring.

- December 2024: SLB introduced Neuro autonomous geosteering that executed 25-bit trajectory changes without human input in Ecuador.

- August 2024: SLB OneSubsea received a contract for two pre-salt FPSO projects in Brazil’s Santos Basin, including trees and a control system.

Global Logging While Drilling (LWD) Market Report Scope

The logging while drilling (LWD) market report include:

| Resistivity LWD |

| Gamma-Ray and Spectral |

| Density-Neutron |

| Acoustic and Sonic |

| Pressure and Fluid Sampling |

| Borehole Imaging |

| Formation Evaluation |

| Geosteering and Reservoir Navigation |

| Wellbore Stability Monitoring |

| Real-time Drilling Optimization |

| Conventional Vertical |

| HPHT |

| Horizontal |

| Extended-Reach |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Norway | |

| Russia | |

| Ukraine | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Nigeria | |

| Algeria | |

| Rest of Middle East and Africa |

| By Service Type | Resistivity LWD | |

| Gamma-Ray and Spectral | ||

| Density-Neutron | ||

| Acoustic and Sonic | ||

| Pressure and Fluid Sampling | ||

| Borehole Imaging | ||

| By Application | Formation Evaluation | |

| Geosteering and Reservoir Navigation | ||

| Wellbore Stability Monitoring | ||

| Real-time Drilling Optimization | ||

| By Well Type | Conventional Vertical | |

| HPHT | ||

| Horizontal | ||

| Extended-Reach | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Norway | ||

| Russia | ||

| Ukraine | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Nigeria | ||

| Algeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the logging while drilling market?

The logging while drilling market size stands at USD 5.02 billion in 2026 and is forecast to reach USD 7.47 billion by 2031.

Which region holds the largest share of the logging while drilling market?

North America leads with 31.42% market share because of prolific shale and Gulf of Mexico deepwater drilling activity.

Which service segment is growing the fastest?

Pressure and fluid sampling services are expanding at 10.95% CAGR thanks to operators’ need for real-time reservoir fluid data.

What are the main factors restraining market growth?

Oil-price volatility that curbs exploration spending and tighter ESG regulations that increase compliance costs together reduce expected CAGR by 2.2 percentage points.

Which companies dominate the logging while drilling market?

SLB, Baker Hughes, and Halliburton together capture roughly 35-40% of global revenue, primarily through AI-enabled drilling platforms and worldwide service networks.

How fast is geosteering demand growing?

Geosteering and reservoir navigation applications of LWD are rising at a 9.85% CAGR through 2031 on the back of longer horizontal wells.

Page last updated on: