Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

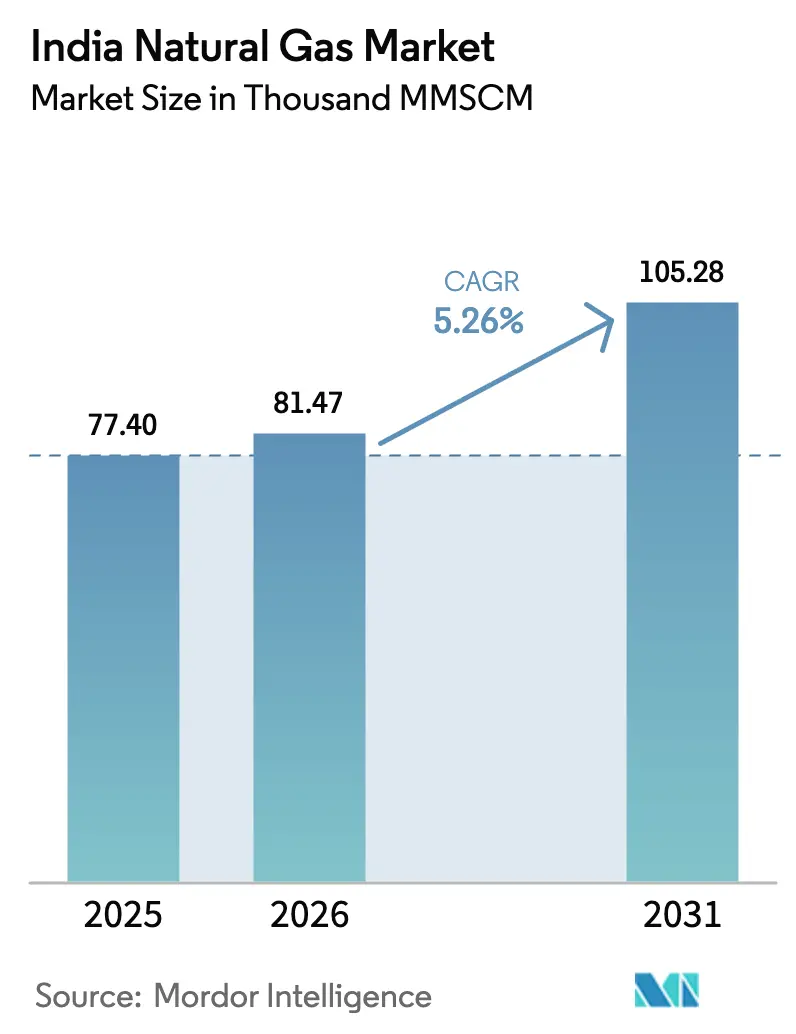

| Base Year Market Size (2025) | 77.40 Thousand MMSCM |

| Market Volume (2026) | 81.47 Thousand MMSCM |

| Market Volume (2031) | 105.28 Thousand MMSCM |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Natural Gas Market Analysis by Mordor Intelligence

The India Natural Gas Market size was valued at 77.40 Thousand MMSCM in 2025 and estimated to grow from 81.47 Thousand MMSCM in 2026 to reach 105.28 Thousand MMSCM by 2031, at a CAGR of 5.26% during the forecast period (2026-2031).

Government plans to raise the fuel’s share in the primary energy mix from 6.7% to 15% by 2030 underpin this outlook, supported by USD 67 billion in trunk pipelines, LNG import terminals, and city-gas projects over the next six years [1]Indian Brand Equity Foundation, “Oil & Gas Industry Report,” ibef.org. Unified tariff adoption at INR 80.97/MMBTU, accelerated city-gas roll-outs across 307 geographical areas, and widening bio-CNG blending mandates add institutional momentum. LNG import capacity nearly doubling by 2026, an east-coast pipeline build-out, and industrial decarbonization incentives for steel, refining, and petrochemicals further broaden demand. Heightened exposure to global LNG prices, declining output from legacy domestic fields, and right-of-way delays on forest corridors moderate near-term growth, prompting industry players to diversify feedstock, restructure LNG contracts toward hub-based indices, and invest in storage as defensive strategies.

Key Report Takeaways

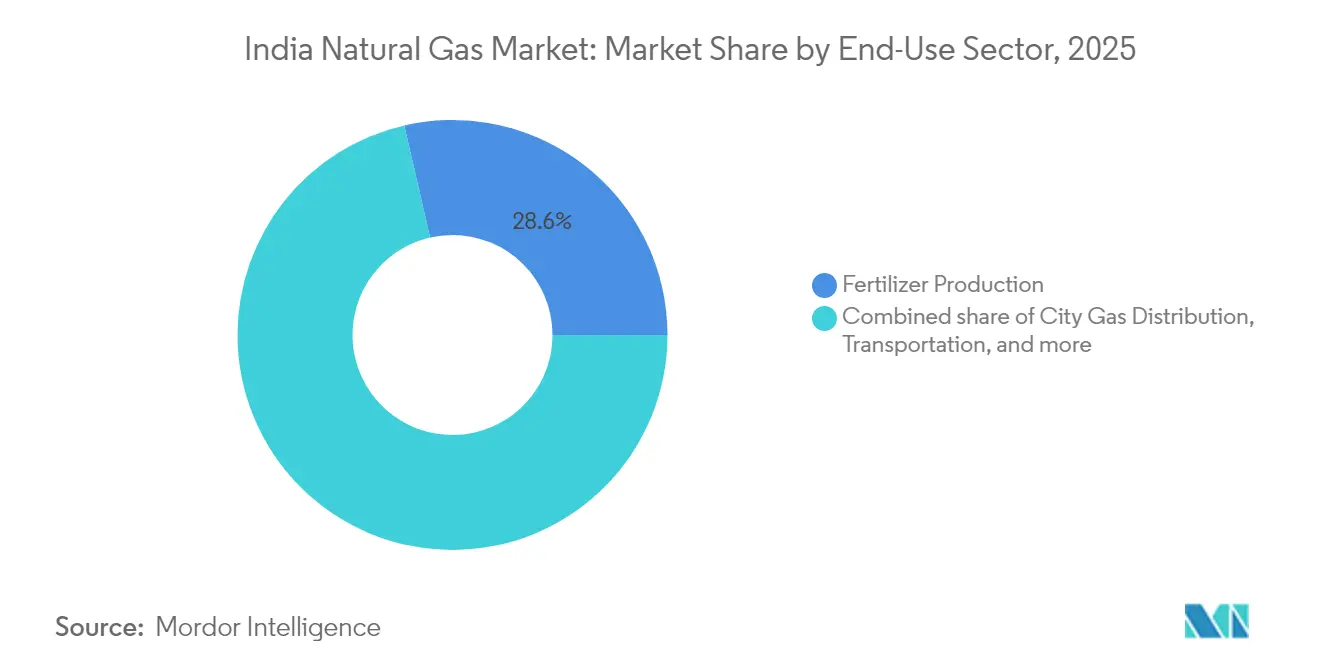

- By end-use sector, fertilizer production retained 28.60% of the India natural gas market share in 2025, while transportation is forecast to grow at a 6.78% CAGR through 2031.

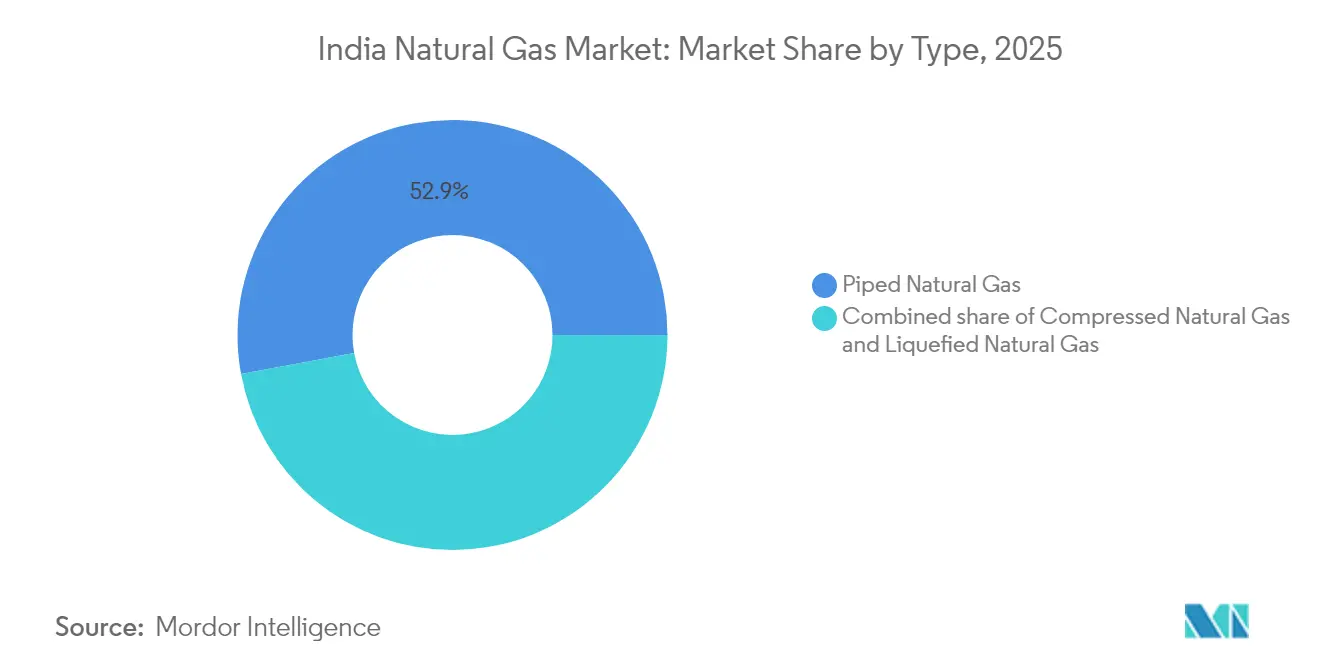

- By type, compressed natural gas (CNG) accounted for 47.10% of the India natural gas market size in 2025 and is expected to expand at a 5.83% CAGR to 2031.

- By source, LNG imports captured 48.00% of the India natural gas market share in 2025 and will post a 5.86% CAGR over the forecast period.

- By geography, Gujarat and Maharashtra jointly contributed 35.70% of the India natural gas market size in 2025, while eastern states are set to register the highest 7.95% CAGR to 2031.

- By company concentration, GAIL, Petronet LNG, Gujarat Gas, Indraprastha Gas and Adani Total Gas together operated major share of pipeline and CGD assets in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Natural Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding City Gas Distribution Network in Tier-2 & Tier-3 Cities | +1.2% | Gujarat, Maharashtra, Uttar Pradesh and other emerging urban centers | Medium term (2-4 years) |

| Fertilizer Sector’s Shift to Gas-Based Feedstock under Nutrient-Based Subsidy Reforms | +0.8% | Major fertilizer hubs nationwide | Short term (≤ 2 years) |

| LNG Contract Restructuring Linking Prices to Emerging Domestic Gas Hub | +0.6% | Coastal LNG terminals and national trade hubs | Long term (≥ 4 years) |

| Industrial Decarbonization Mandates for Steel & Refining Clusters | +0.7% | Odisha, Jharkhand, Gujarat industrial belts | Medium term (2-4 years) |

| Interstate Pipeline Connectivity via “One Nation, One Gas Grid” Policy | +0.9% | Eastern and northeastern states | Long term (≥ 4 years) |

| Emergence of Bio-CNG Blending Targets for CGD Operators | +0.4% | Rural agricultural states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding City Gas Distribution Network in Tier-2 & Tier-3 Cities

Roll-outs across 307 areas aim for 12.6 crore PNG connections and 18,336 CNG stations by 2034, pushing the India natural gas market deep into smaller cities [2]Government of India, “City Gas Distribution Authorisations,” india.gov.in. Gujarat Gas has earmarked INR 1,200 crore to hook 3.3 lakh new homes and 200 CNG outlets in FY25—an approach replicated by other distributors venturing beyond saturated metros. Urbanization trends, cleaner-fuel priorities, and standardized tariffs improve project viability, though low consumption density demands innovative last-mile models and long-term policy backing.

Fertilizer Sector’s Shift to Gas-Based Feedstock under Nutrient-Based Subsidy Reforms

The sector drew 31% of national demand in 2024 and remains insulated from LNG price swings through direct government support. Reforms channel APM and new-well gas to fertilizer plants, incentivizing a move away from naphtha and reinforcing supply security. Stable offtake from this price-inelastic segment cushions the India natural gas market against industrial fuel-switching cycles while anchoring infrastructure utilization.

LNG Contract Restructuring Linking Prices to Emerging Domestic Gas Hub

The Indian Gas Exchange has introduced delivery-based trading at Dahej, Hazira, and Odoru, enabling the discovery of transparent hub-linked prices. GAIL’s multi-supplier long-term deals and Petronet LNG’s 20-year extension with QatarEnergy illustrate diversified portfolios designed to decouple from volatile oil-indexed formulas. As liquidity builds, buyers gain leverage for flexible volumes and slope renegotiations that support downstream affordability.

Interstate Pipeline Connectivity via “One Nation, One Gas Grid” Policy

Operational length rose from 15,340 km in 2014 to 24,945 km by September 2024, with 10,805 km under construction to complete a nationwide grid that equalizes delivered prices irrespective of distance [4]Ministry of Petroleum and Natural Gas, “Monthly Gas Production & Pipeline Status,” mopng.gov.in. Enhanced connectivity unlocks latent demand in the underserved east and northeast, feeds new city-gas concessions, and ensures balanced capacity utilization between LNG terminals and domestic production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Spot LNG Prices Driving Industrial Fuel Switching | -0.9% | National, with coastal industrial centers most affected | Short term (≤ 2 years) |

| Delays in Pipeline Right-of-Way Clearances across Forest Corridors | -0.6% | Eastern and northeastern states, tribal areas | Medium term (2-4 years) |

| Pricing Formula Caps Limiting Upstream Investment Economics | -0.5% | National, with primary impact on domestic production regions | Long term (≥ 4 years) |

| Competition from Rapidly Falling Levelized Cost of Solar-plus-Storage | -0.4% | National, with maximum impact in high solar irradiance states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Spot LNG Prices Driving Industrial Fuel Switching

Spot LNG fluctuated from USD 2/MMBTU in early 2020 to USD 30/MMBTU in late 2021, prompting price-sensitive users to revert to fuel oil or coal whenever landed costs breach viability thresholds. Reliance on spot cargoes for roughly 25% of supply exposes the India natural gas market to exogenous shocks, especially in non-subsidized industries and peaking power plants that lack hedging mechanisms.

Delays in Pipeline Right-of-Way Clearances across Forest Corridors

Complex environmental approvals extend major projects such as the Jagdishpur-Haldia-Bokaro-Dhamra line by 12-18 months. Cost overruns dampen investor appetite and defer gas penetration into eastern heartlands where coal dominance continues, thereby capping near-term throughput on new LNG capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: CNG acceleration outpaces PNG adoption

CNG delivered 47.10% of the India natural gas market size in 2025 and is forecast for a 5.83% CAGR, versus PNG’s dominant 52.90% share but slower trajectory. Rapid station build-outs—8,067 outlets operational by March 2025—and supportive transport policies make CNG an accessible decarbonization lever for commercial fleets. Bajaj Auto’s launch of CNG motorcycles and forthcoming CNG scooter platforms broadens the addressable two-wheeler universe. PNG expansion remains challenged by connection cost, subsidized LPG competition, and lower rural densities, leaving 93 geographical areas without a single household hookup, which compels CGD firms to craft pay-as-you-go and community pipeline solutions.

By Source: Import dependency intensifies despite domestic push

LNG secured 48.00% of the India natural gas market share in 2025, making it the single largest contributor to growth at a 5.86% CAGR through 2031. Planned import capacity rises from 2.1 Tcf to nearly 4 Tcf by 2026, highlighted by the east-coast Dhamra terminal that reduces shipping legs to eastern consumers. Domestic offshore gains struggle to offset decline rates in legacy basins, yet HELP acreage awards and ONGC-IOCL’s Hatta field offer localized boosts. Supplier diversification broadens; Qatar supplied 61% of cargoes in 2024, but the US share climbed to 13.5%, with room to rise toward 18% under recently signed SPAs.

By End-Use Sector: Transportation emerges as growth engine

Fertilizer retained 28.60% of the India natural gas market size in 2025 through protected allocations, but transportation will outpace all other segments at 6.78% CAGR on the back of CNG autos and LNG trucking. City-gas (household and commercial) contributed 19.10%, and industrial process heat in steel, glass, and ceramics is emerging as a high-value, lower-elasticity demand pocket.

Geography Analysis

Gujarat and Maharashtra accounted for 35.70% of India's natural gas market size in 2025, benefiting from proximity to Dahej and Hazira LNG terminals, mature CGD franchises, and dense industrial clusters. Gujarat's network already serves 1.93 million homes via Gujarat Gas, underscoring how early adoption drives sustained offtake . East Coast build-outs are now balancing Western dominance. Andhra Pradesh is positioning itself as a dual LNG-and-bio-CNG hub, with Reliance Industries announcing 500 compressed bio-gas plants valued at INR 65,000 crore, yielding 4 million tons annually.

Eastern states—West Bengal, Odisha, Jharkhand, and Bihar—represent latent reservoirs of demand hindered by pipeline deficits. Completing the Jagdishpur-Haldia-Bokaro-Dhamra corridor and unified tariffs will level delivered gas prices, making natural gas competitive against coal in these coal-rich states and enabling fertilizer, steel, and CGD uptake. Bihar targets 5.3 million household PNG connections by 2030, contingent on faster clearances and last-mile build-outs.

Southern states such as Tamil Nadu and Karnataka are seeing LNG access improve via Ennore and Kochi terminals. Industrial automotive, textiles, and electronics parks are preparing to connect to trunk networks, particularly as grid reliability and decarbonization compliance gain weight in investment decisions. Northeastern terrain complicates linear pipelines, but smaller-diameter, high-pressure lines and virtual LNG trucking bridge gaps until full right-of-way approvals materialize.

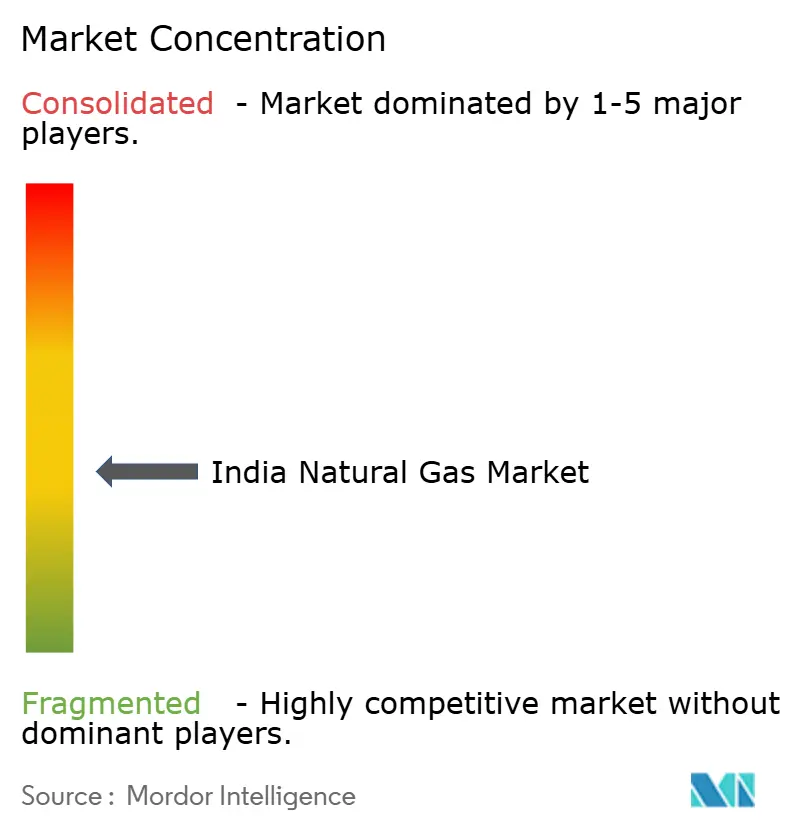

Competitive Landscape

The India natural gas market is moderately fragmented. GAIL controls a major share of pipeline kilometers, underlining a quasi-natural monopoly in transmission. Petronet LNG leads regasification with Dahej and Kochi, yet new terminals at Dhamra and Chhara lower entry barriers for competitors. City-gas distribution is more contested. Gujarat Gas, Indraprastha Gas, and Mahanagar Gas dominate legacy concessions, while Adani Total Gas leverages deep pockets and cross-business synergies to extend into greenfield areas. Recent APM allocation cuts in 2024 squeezed supply by up to 21%, forcing CGD companies to blend higher-cost LNG, tweak consumer tariffs, and accelerate bio-CNG procurement.

Strategic moves lean toward vertical integration and transition fuels. Adani Total Gas secured USD 375 million for network growth; ONGC acquired PTC Energy’s 288 MW wind portfolio, signaling intent to couple gas with renewable generation and carbon-capture pilots. Digitalization, from smart metering to predictive maintenance, is emerging as a competitive differentiator, with large distributors deploying IoT sensors to cut unaccounted-for-gas losses and optimize CNG dispenser uptime.

Regulatory developments also influence rivalry. The Petroleum and Natural Gas Regulatory Board is studying third-party open access to CNG stations, potentially breaking the exclusivity enjoyed by incumbents and allowing fuel retailers to source gas independently. This could foster price competition at the pump and accelerate market deepening if accompanied by transparent network tariffs and supply-balancing mechanisms.

India Natural Gas Industry Leaders

GAIL (India) Limited

Oil & Natural Gas Corporation (ONGC)

Petronet LNG Limited

Indian Oil Corporation Limited

Adani Total Gas Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GAIL announced plans to pick minority stakes in US LNG plants to lock in long-term volumes against India’s forecast 500 MMscm/d demand by 2030.

- April 2025: New allocation rules allow CGD firms to receive domestic gas quotas two quarters ahead, improving supply planning

- March 2025: ONGC Green closed its USD 106 million purchase of PTC Energy, adding 288 MW of wind assets toward a 10 GW renewables goal

- February 2025: Petronet LNG executed a 20-year extension with QatarEnergy for 7.5 MMTPA supply until 2048

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every cubic meter of natural gas that is produced inside India or imported as LNG and finally delivered through pipelines, CGD networks, or cascades for power, fertilizer, transport, residential, and industrial uses, irrespective of contractual tenure or calorific value.

Exclusions: bottled LPG, synthetic gas from coal or biomass, gas traded only for petrochemical feedstock inside refinery gates, and trans-shipment volumes that never enter inland demand centers.

Segmentation Overview

- By Type

- Compressed Natural Gas (CNG)

- Piped Natural Gas (PNG)

- Liquefied Natural Gas (LNG)

- By Source

- Domestic Production - Onshore

- Domestic Production - Offshore

- LNG Imports

- By End-Use Sector

- Fertilizer Production

- City Gas Distribution

- Transportation

- Petrochemical Feedstock

- Others [Industrial Manufacturing, Agriculture (Tea Plantation), IC for Pipeline System, LPG Shrinkage, Sponge Iron/Steel]

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed city-gas distributors, fertilizer plant energy managers, LNG terminal planners, and pipeline EPC contractors across western, northern, and southern clusters to verify utilization rates, spot price pass-throughs, and forward capex schedules. These discussions filled data gaps on unreported captive demand and confirmed the plausibility of model assumptions.

Desk Research

We began with government energy dashboards such as PPAC monthly gas reports, PNGRB tariff filings, and Petroleum Ministry CGD progress notes, which anchor demand and supply balances. Trade flows were cross-checked with customs import data and shipping manifests gathered via Volza and Dow Jones Factiva feeds, while domestic production trends drew on ONGC and Oil India filings and DGH field status notes. Sector splits were refined with fertilizer ministry usage releases, CEA power-plant dispatch sheets, and periodic IEA gas market updates. The listed sources illustrate, but do not exhaust, the wider set we mined for context and numeric validation.

Market-Sizing & Forecasting

A top-down supply-demand balance was first built using production and LNG import series, which are then allocated by sector through historical penetration ratios. Select bottom-up rolls-ups, sampled CGD volumes multiplied by the average offtake per connection and LNG terminal throughput audits, serve as reasonableness checks before final alignment. Key drivers in the model include planned pipeline kilometers commissioned, city-gas household connection growth, domestic output from KG-DWN-98/2, LNG spot-contract differential, and Henry Hub linked price formulas. Multivariate regression with GDP growth, steel output, and vehicle fleet additions frames the forecast, while scenario analysis tweaks import dependency and price elasticity to bracket risk. Gaps in granular bottom-up data are bridged through coefficient adjustments vetted in expert calls.

Data Validation & Update Cycle

Outputs pass a three-layer analyst review that flags anomalies against IEA demand outlooks and CGD metering snapshots. Models refresh annually, and interim updates trigger when LNG landed cost shifts or new trunk pipelines go live.

Why Mordor's India Natural Gas Baseline Commands Reliability

Published estimates differ; definitions, unit choices, and refresh cadences rarely match.

We acknowledge this spread upfront and then show where variances arise.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 77.4 thousand MMSCM (2025) | Mordor Intelligence | - |

| 61.28 billion SCM (2024) | Global Consultancy A | Excludes LNG spot cargoes landed post-April 2024 |

| USD 131 billion (2024) | Regional Consultancy B | Converts volume at fixed FY22 price, omits unified tariff impact |

| USD 16 billion (2024) | Trade Journal C | Tracks only industrial and power demand, ignores CGD and transport |

The comparison shows that once consistent scope, pricing, and latest infrastructure roll-outs are applied, Mordor's balanced figure emerges as the most reproducible starting point for planners who must defend budgets to boards and regulators alike.

Key Questions Answered in the Report

What is the current size of the India natural gas market?

The India natural gas market size was 81,471.24 MMSCM in 2026 and is projected to reach 105,282.06 MMSCM by 2031.

Which end-use sector consumes the most natural gas in India?

Fertilizer manufacturing leads with 28.60% of consumption, owing to government-backed gas allocations that ensure continuous supply.

Why are LNG imports increasing despite domestic production efforts?

Domestic output from mature fields is declining, while new LNG terminals and diversified supply contracts offer quicker, scalable volumes to meet rising demand.

How is unified tariff policy impacting regional gas prices?

A single INR 80.97/MMBTU tariff equalizes transportation costs nationwide, making gas more affordable in previously underserved eastern and northeastern states.

What role does natural gas play in India’s decarbonization strategy?

Natural gas serves as a transition fuel that cuts CO₂ emissions in steel, refining and transport, while its infrastructure also enables future hydrogen adoption.

Which segment is expected to grow fastest to 2031?

The transportation segment, driven by CNG and LNG vehicle adoption, is forecast to expand at a 6.78% CAGR through 2031.

Page last updated on: