Lipid Regulators Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

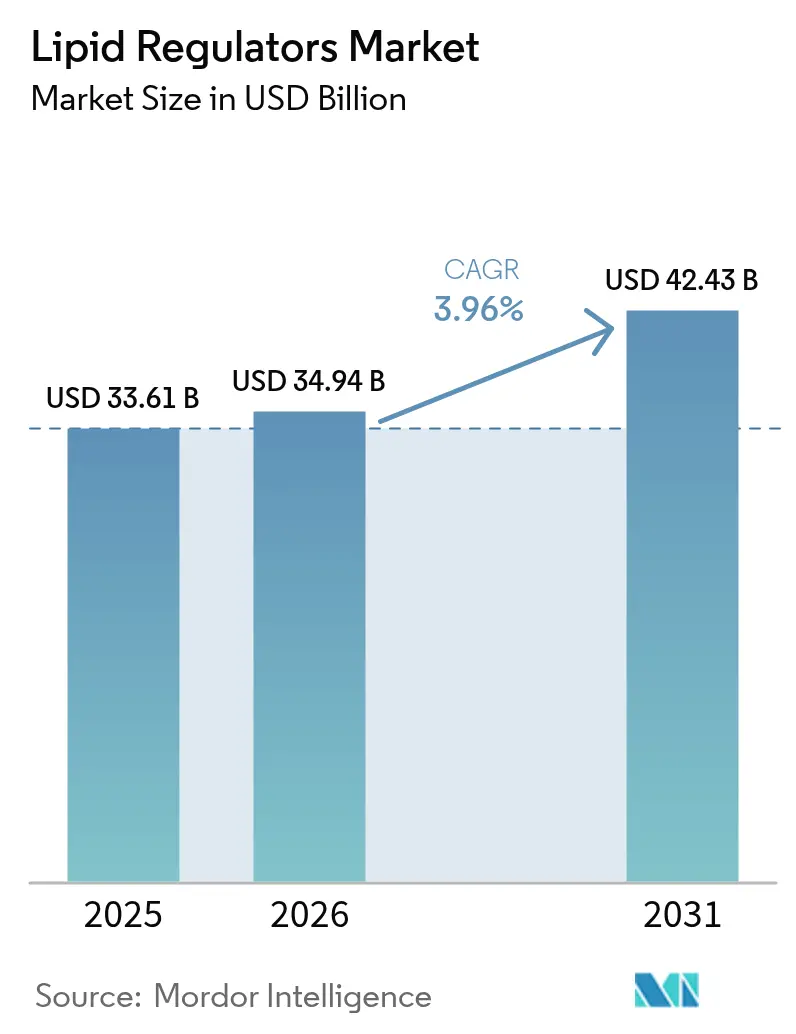

| Market Size (2026) | USD 34.94 Billion |

| Market Size (2031) | USD 42.43 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

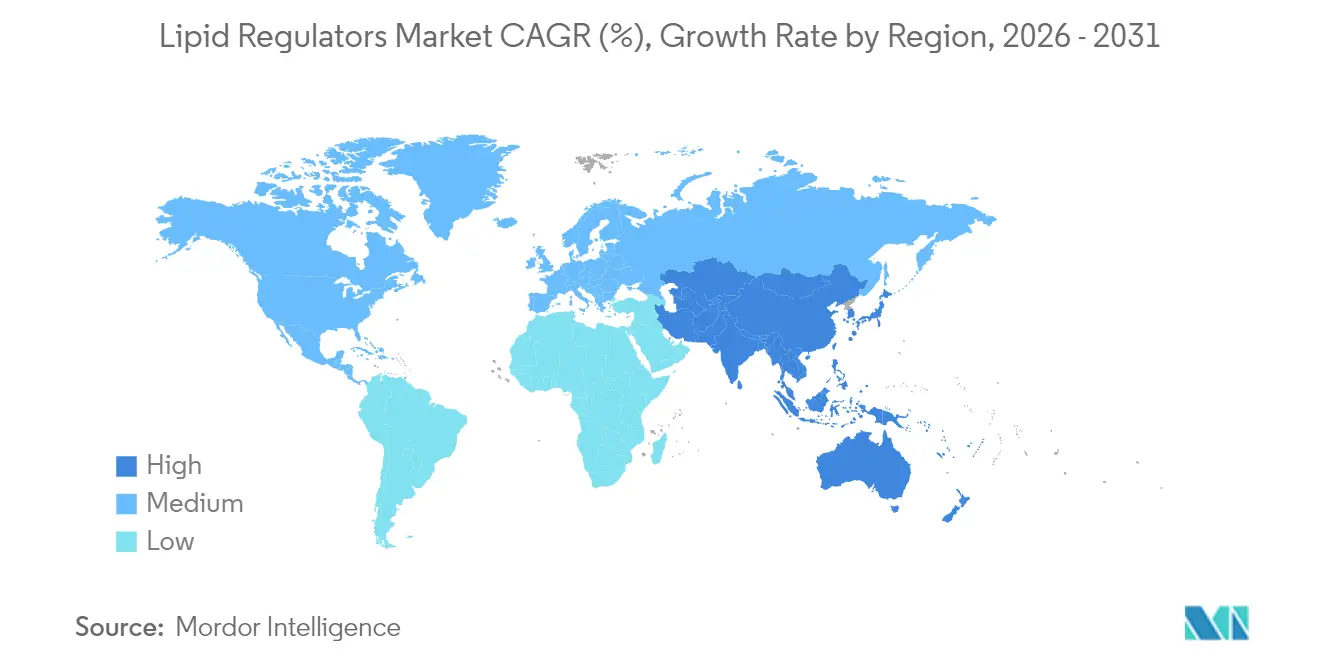

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lipid Regulators Market Analysis by Mordor Intelligence

The lipid regulators market size was valued at USD 33.61 billion in 2025 and estimated to grow from USD 34.94 billion in 2026 to reach USD 42.43 billion by 2031, at a CAGR of 3.96% during the forecast period (2026-2031). This controlled expansion follows the post-statin patent-cliff stabilization and reflects the shift toward precision therapeutics such as RNA-interference and oral PCSK9 inhibitors. Demand is underpinned by the escalating global cardiovascular disease burden, where high LDL-cholesterol contributed to 3.81 million deaths in 2021. Growing acceptance of combination therapies, expanding screening initiatives in emerging economies, and payer willingness to reimburse high-risk patients for advanced agents further reinforce momentum. Simultaneously, digital adherence platforms and remote monitoring programs enhance persistence, improving real-world outcomes and supporting steady revenue growth for manufacturers.

Key Report Takeaways

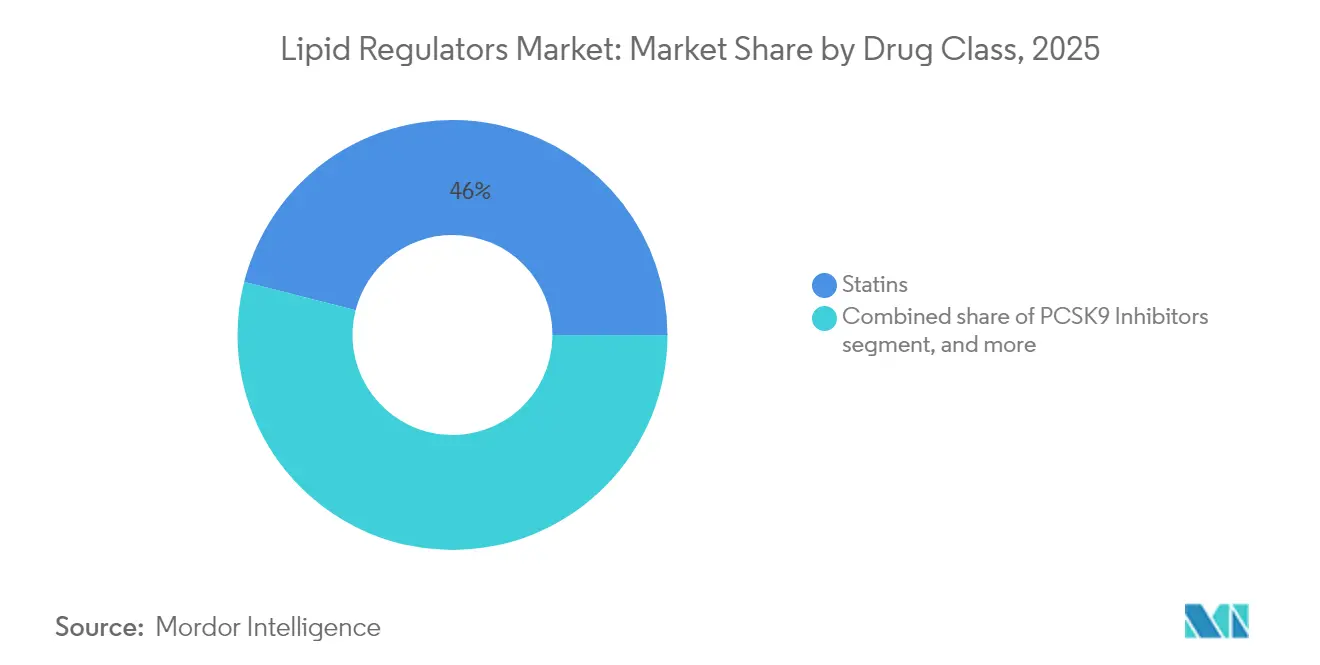

- By drug class, statins retained 46.02% of the lipid regulators market share in 2025, whereas PCSK9 inhibitors posted the fastest 6.35% CAGR to 2031.

- By patient type, primary hypercholesterolemia accounted for 38.12% of the lipid regulators market size in 2025, while hypertriglyceridemia registered the sharpest 6.28% CAGR.

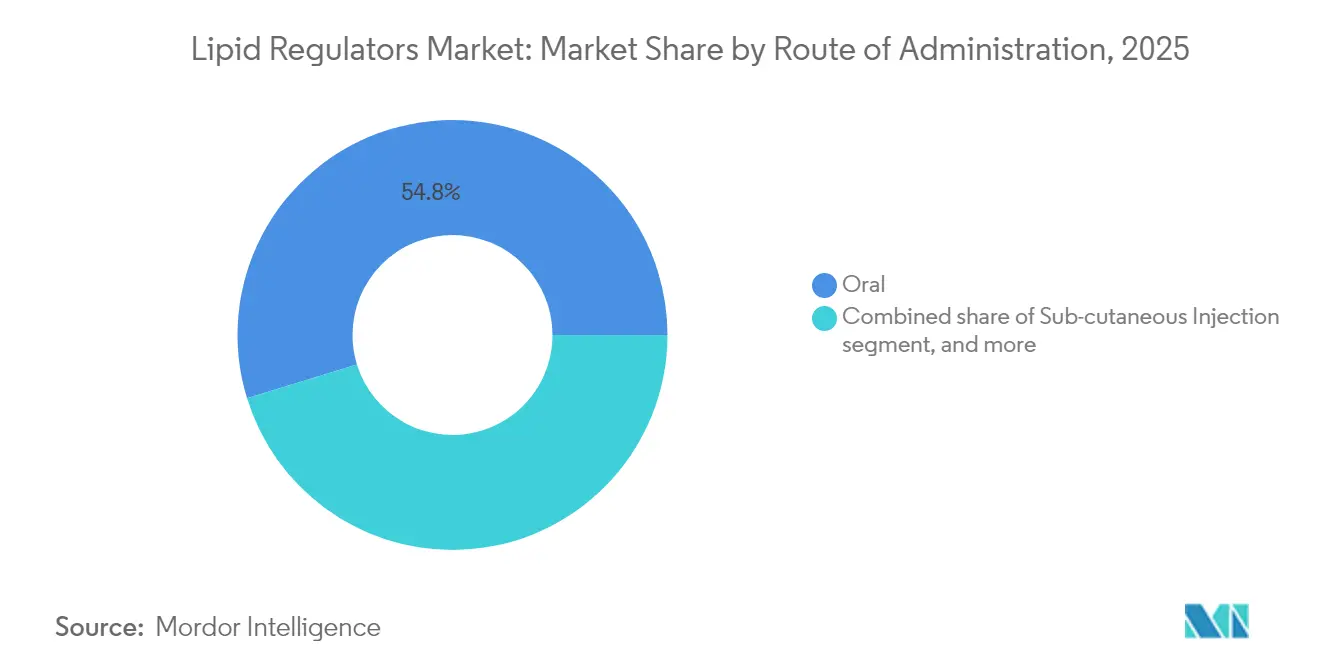

- By route of administration, oral dosage forms captured 54.76% share of the lipid regulators market size in 2025; in-vivo gene therapy is projected to accelerate at a 7.1% CAGR through 2031.

- By distribution channel, hospital pharmacies held 57.21% revenue share in 2025 as online pharmacies expanded fastest at a 7.4% CAGR.

- By geography, North America held 42.75% revenue share in 2025, whereas, Asia-Pacific is projected to grow at a CAGR of 5.21% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lipid Regulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cardiovascular disease burden | +1.2% | North America & Europe lead | Long term (≥ 4 years) |

| Rising adoption of combination lipid-lowering therapies | +0.8% | North America & EU, extending to APAC | Medium term (2–4 years) |

| Innovation in long-acting RNAi and oral PCSK9 inhibitors | +1.1% | Global, led by North America | Medium term (2–4 years) |

| Increasing reimbursement coverage for high-risk populations | +0.7% | Core markets in North America & EU | Short term (≤ 2 years) |

| Expansion of preventive screening programs | +0.5% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Growing integration of digital adherence tools | +0.4% | Global, early uptake in North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Cardiovascular Disease Burden

Cardiovascular disease affects 127.9 million Americans in 2025, with atherosclerotic events driving USD 422.3 billion in annual economic costs[1]American Heart Association, “Heart Disease and Stroke Statistics 2025 Update,” heart.org. High LDL-cholesterol remains the most modifiable risk factor, producing an addressable global population of more than 1.5 billion adults. Aging demographics in high-income nations and rapid urbanization in Asia combine to push incidence upward. Consequently, healthcare systems intensify focus on preventive lipid control, ensuring the lipid regulators market gains durable volume growth. Multisector partnerships that subsidize screening in community clinics further expand the treated pool and support long-term prescription demand.

Rising Adoption of Combination Lipid-Lowering Therapies

Clinical trials such as TANDEM demonstrated that obicetrapib plus ezetimibe trimmed LDL-cholesterol by 48.6% over placebo. Fixed-dose combinations reduce pill burden and raise adherence, encouraging physicians to initiate dual therapy earlier, especially for familial hypercholesterolemia. Guideline revisions in 2024 introduced LDL-cholesterol targets below 55 mg/dL for very-high-risk patients, accelerating uptake. In response, companies launched products like Nexlizet, winning expanded FDA approval for risk reduction. This shift from stepwise escalation to precision combinations magnifies revenue per treated patient and consolidates brand loyalty in the lipid regulators market.

Innovation in Long-Acting RNAi and Oral PCSK9 Inhibitors

Inclisiran achieves roughly 50% LDL-cholesterol reductions with two injections per year[2]U.S. Food and Drug Administration, “Inclisiran Prescribing Information,” fda.gov. Emerging siRNA agents such as zerlasiran cut lipoprotein(a) by more than 80% in mid-stage trials[3]American College of Cardiology, “Zerlasiran First-in-Human Results,” acc.org. Meanwhile, AstraZeneca’s oral PCSK9 inhibitor AZD0780 delivered a 50.7% LDL-cholesterol fall in Phase IIb results. These modalities overcome injection fatigue and broaden specialist as well as primary-care prescribing. As safety data accumulate, long-acting RNAi and convenient oral agents are expected to migrate from niche high-risk cohorts to mainstream dyslipidemia management, augmenting the lipid regulators market.

Increasing Reimbursement Coverage for High-Risk Populations

Medicare’s 2024 decision to reimburse Wegovy for cardiovascular risk reduction opened the door for broader payer acceptance of preventive lipid therapy. The CLEAR Outcomes trial confirmed bempedoic acid’s 13% drop in major events, prompting an FDA label expansion that enlarges the U.S. eligible population to about 70 million adults. Health technology bodies in Europe also endorsed inclisiran based on cost-effectiveness. Improved coverage compresses patient out-of-pocket costs, stimulates prescribing, and offsets the high list prices of advanced therapies, directly lifting the lipid regulators market size.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying generic competition in statin segment | −0.9% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| High treatment costs of novel biologics | −0.6% | Global, particularly affecting LMIC access | Long term (≥ 4 years) |

| Limited access in low- and middle-income countries | −0.7% | LMICs across MEA, South America & parts of APAC | Long term (≥ 4 years) |

| Manufacturing complexity of nucleic acid therapies | −0.5% | Global, with heightened impact on decentralized production regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Intensifying Generic Competition in Statin Segment

Expired patents hand sizeable share to low-cost producers, compressing prices and eroding branded revenue. Many national formularies enforce step-therapy protocols mandating generic statin trials before approving advanced drugs. In emerging markets, aggressive tendering further narrows margins. Manufacturers counter by bundling statins with ezetimibe or bempedoic acid, yet competitive intensity still moderates overall lipid regulators market growth during the forecast window.

High Treatment Costs of Novel Biologics

Annual therapy with PCSK9 monoclonal antibodies remains near USD 14,000, dwarfing sub-USD 100 generic statin regimens. RNA-based products require specialized manufacturing and cold-chain logistics, limiting cost-reduction levers. Although payer coverage improves in high-income regions, affordability in low- and middle-income countries lags, leaving sizeable populations undertreated and restraining universal lipid regulators market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Therapeutic Innovation Commands Premium Uptake

Statins contributed nearly half of 2025 revenue, yet their growth plateaus under generic commoditization. Fixed-dose combinations such as bempedoic acid plus ezetimibe differentiate through additive efficacy and convenience, cushioning erosion. PCSK9 inhibitors are projected to outpace others with a 6.35% CAGR, driven by mounting cardiovascular outcome evidence and the arrival of self-administered and oral formats. Cholesterol absorption inhibitors maintain relevance as backbone add-on agents. Meanwhile, ATP-citrate-lyase inhibitors gain traction among statin-intolerant populations after the 2024 FDA label expansion. Pipeline entrants targeting lipoprotein(a) could reshape the lipid regulators market size for high-risk genetic subsets once late-stage trials conclude.

Continued R&D investment focuses on oral small molecules and longer-acting injectables that address adherence bottlenecks. Developers emphasize robust endpoint trials, given payer insistence on outcome validation to justify premium costs. As competitor portfolios diversify, cross-class combination strategies proliferate, further boosting average selling prices without compromising tolerability.

By Patient Type: Risk Stratification Drives Therapeutic Allocation

Primary hypercholesterolemia remained the anchor cohort, yet hypertriglyceridemia recorded the steepest 6.28% CAGR as clinicians recognize triglycerides’ role in residual cardiovascular risk. Familial hypercholesterolemia populations, especially heterozygous variants, gravitate toward RNAi and PCSK9 agents when statins underperform. Secondary prevention after ASCVD events solidifies consistent biologic demand due to stringent guideline targets. Diabetes and obesity prevention segments expand following GLP-1 cardiovascular data, opening cross-selling avenues for lipid-lowering brands.

Precision medicine tools, including polygenic risk scoring, segment patients more finely, informing therapy escalation earlier in the disease continuum. As payers reimburse pharmacogenetic testing, manufacturers tailor educational outreach to physicians, reinforcing guideline-aligned prescribing and elevating lipid regulators market share within high-risk clusters.

By Route of Administration: Convenience Shapes Preference Hierarchy

Traditional oral tablets dominated with 54.76% share, reflecting patient familiarity and broad primary-care integration. Injectable biologics sustain strong uptake in cardiology and endocrinology clinics because of potent LDL-cholesterol reductions, but frequent administration limits adherence in some cohorts. Long-acting RNAi regimens that require twice-yearly dosing partially resolve this friction, while emerging oral PCSK9 molecules promise to recast the competitive landscape by uniting potency with convenience.

Gene-editing therapeutics, delivered intravenously or via lipid nanoparticles, advance through early trials targeting lifelong LDL-lowering in a single treatment. If safety hurdles clear, such one-time modalities could cannibalize chronic dosing models, expanding the total lipid regulators market size by offering curative appeal to payers.

By Distribution Channel: Digital Platforms Strengthen Patient Reach

Hospital pharmacies continued to secure most sales, particularly for cold-chain-dependent biologics. Retail chains broaden over-the-counter statin service offerings, incorporating pharmacist-led lipid panels and algorithmic prescribing. Online pharmacies surged at a 7.4% CAGR, propelled by direct-to-consumer teleconsultations and automatic refills. Specialty clinics emerged as coordination hubs for familial hypercholesterolemia and complex dyslipidemia, integrating genetic counseling with therapy initiation.

COVID-era shifts toward home delivery normalized mail-order dispersion of chronic medications. Coupled with real-time adherence analytics, e-commerce platforms enhance persistence and hold potential to shift a greater portion of lipid regulators market share away from traditional bricks-and-mortar channels.

Geography Analysis

North America accounted for 42.75% of 2025 revenue, benefitting from broad insurance coverage, mature clinical trial ecosystems, and rapid adoption of digital adherence tools. Strong payer emphasis on outcome-based reimbursement accelerates biologic uptake as long-term cost-offset models gain credibility. Prior authorization complexity still moderates immediate growth, yet streamlined electronic benefit verification systems reduce delays and support stable demand.

Europe follows a value-driven trajectory underpinned by unified EMA approvals and rigorous health technology assessments that reward demonstrable cardiovascular event reduction. Strong generic penetration lowers baseline treatment costs, enabling reinvestment in premium agents for high-risk cohorts. Ongoing post-Brexit regulatory realignment produces temporary launch stagger, but cross-border reference pricing maintains relative affordability and cushions patients from list-price volatility.

Asia-Pacific registers the swiftest 5.21% CAGR, stimulated by rising urban cardiovascular risk, policy-backed screening programs, and expanding middle-class insurance coverage. Local generic statin production ensures baseline access, but affordability gaps for newer agents persist. Evolving regulatory harmonization expedites novel product review, while multinational alliances with domestic firms facilitate market entry. China’s Healthy China 2030 agenda and India’s Ayushman Bharat scheme are expected to enlarge public funding envelopes for preventive cardiometabolic care, widening the addressable base for premium lipid-lowering therapies.

South America, the Middle East, and Africa witness gradual improvement through donor-supported essential-medicine initiatives. Nevertheless, biologic uptake remains limited by constrained budgets and distribution logistics. Progressive tiered-pricing models and regional manufacturing partnerships are likely prerequisites to meaningful penetration in these territories.

Competitive Landscape

The lipid regulators market hosts a moderate concentration profile. Novartis leverages inclisiran’s twice-yearly dosing to protect its leading position, while Amgen rides evolocumab’s robust outcome data and expanding pediatric indication. AstraZeneca differentiates through the oral PCSK9 candidate AZD0780, aiming to capture injection-averse patients. Combined, these three companies controlled just under 35% of 2024 global revenue.

Strategic collaborations accelerate pipeline diversification. Novartis invested USD 60 million in Ionis to co-develop second-generation lipoprotein(a) siRNA therapies, complementing its RNA portfolio. AstraZeneca’s USD 100 million deal with CSPC Pharmaceutical for a novel Lp(a) disruptor reinforces its dyslipidemia franchise. Meanwhile, Eli Lilly’s acquisition of Verve Therapeutics positions the firm at the forefront of in-vivo base-editing for once-and-done LDL-lowering.

Challenger biotech firms, including NewAmsterdam Pharma and Esperion Therapeutics, exploit oral small-molecule platforms to undercut injectable competition on convenience. Incremental entrants cultivate niche indications such as homozygous familial hypercholesterolemia, using accelerated regulatory pathways to reach market quickly. As portfolios widen, cross-class combination regimens become a central competitive lever, raising the total addressable revenue per treated patient.

Lipid Regulators Industry Leaders

AstraZeneca

AbbVie Inc

Teva Pharmaceuticals

Pfizer, Inc.

AbbVie, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eli Lilly acquired Verve Therapeutics to advance one-time PCSK9 gene-editing treatments targeting familial hypercholesterolemia.

- May 2025: HLS Therapeutics partnered with Esperion to commercialize NEXLETOL and NEXLIZET in Canada through a USD 1 million upfront agreement.

- April 2025: Novartis announced positive V-MONO Phase III inclisiran monotherapy data, broadening the eligible patient base.

- March 2025: AstraZeneca’s oral PCSK9 inhibitor AZD0780 achieved a 50.7% LDL-cholesterol reduction in PURSUIT Phase IIb.

- March 2024: FDA expanded bempedoic acid labels to include cardiovascular risk reduction in primary prevention.

- October 2024: AstraZeneca licensed CSPC’s small-molecule Lp(a) disruptor YS2302018 for USD 100 million upfront.

Global Lipid Regulators Market Report Scope

As per the scope of the report, lipid regulators or lipid-regulating drugs are used to treat dyslipidemia, cardiovascular problems, osteoporosis, and post-menopause complications. This is why these lipid regulators come under the class of most prescribed medications. The lipid regulators market is segmented by Type (Statins (Branded statins, Statin combinations, and Generic statins), and Non-statins (Fibric-acid derivatives, Bile-acid sequestrants, Nicotinic acid derivatives, and Other new products)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Statins | Branded Statins |

| Generic Statins | |

| Fixed-Dose Combinations | |

| PCSK9 Inhibitors | mAbs (Alirocumab, Evolocumab) |

| siRNA (Inclisiran) | |

| Oral Small-Molecule PCSK9i | |

| Cholesterol Absorption Inhibitors (Ezetimibe) | |

| Bempedoic-acid / ACLY Inhibitors | |

| Fibric-acid Derivatives | |

| Bile-acid Sequestrants | |

| Omega-3 Fatty Acid Derivatives | |

| Nicotinic-acid Derivatives | |

| Lipoprotein(a) Targeted Agents |

| Primary Hypercholesterolemia | Heterozygous FH |

| Homozygous FH | |

| Mixed Dyslipidemia | |

| Hypertriglyceridemia (≥500 mg/dL) | |

| ASCVD Secondary Prevention | |

| Diabetes / Obesity Preventive Care |

| Oral |

| Sub-cutaneous Injection |

| Intravenous |

| In-vivo Gene Therapy |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Statins | Branded Statins |

| Generic Statins | ||

| Fixed-Dose Combinations | ||

| PCSK9 Inhibitors | mAbs (Alirocumab, Evolocumab) | |

| siRNA (Inclisiran) | ||

| Oral Small-Molecule PCSK9i | ||

| Cholesterol Absorption Inhibitors (Ezetimibe) | ||

| Bempedoic-acid / ACLY Inhibitors | ||

| Fibric-acid Derivatives | ||

| Bile-acid Sequestrants | ||

| Omega-3 Fatty Acid Derivatives | ||

| Nicotinic-acid Derivatives | ||

| Lipoprotein(a) Targeted Agents | ||

| By Patient Type | Primary Hypercholesterolemia | Heterozygous FH |

| Homozygous FH | ||

| Mixed Dyslipidemia | ||

| Hypertriglyceridemia (≥500 mg/dL) | ||

| ASCVD Secondary Prevention | ||

| Diabetes / Obesity Preventive Care | ||

| By Route of Administration | Oral | |

| Sub-cutaneous Injection | ||

| Intravenous | ||

| In-vivo Gene Therapy | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Specialty Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast growth rate for the lipid regulators market between 2026 and 2031?

The lipid regulators market is expected to expand at a 3.96% CAGR, rising from USD 34.94 billion in 2026 to USD 42.43 billion by 2031.

Which drug class is growing fastest?

PCSK9 inhibitors represent the fastest-growing class with a projected 6.35% CAGR through 2031, reflecting stronger clinical evidence and emerging oral formulations.

Why are combination lipid-lowering therapies gaining traction?

Trials like TANDEM show larger LDL-cholesterol reductions and better adherence, prompting updated guidelines that favor early combination use in high-risk patients.

What role do digital tools play in lipid management?

Mobile adherence apps and remote monitoring programs have cut LDL-cholesterol by an average 24 mg/dL, supporting persistence and improving real-world outcomes.

Which region is expected to record the highest growth rate?

Asia-Pacific is projected to post a 5.21% CAGR as screening programs expand and insurance coverage widens, especially in China and India.

How concentrated is the competitive landscape?

The top five companies account for roughly 50% of global revenue, pointing to moderate concentration with opportunities for innovative biotech entrants.

Page last updated on: