Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

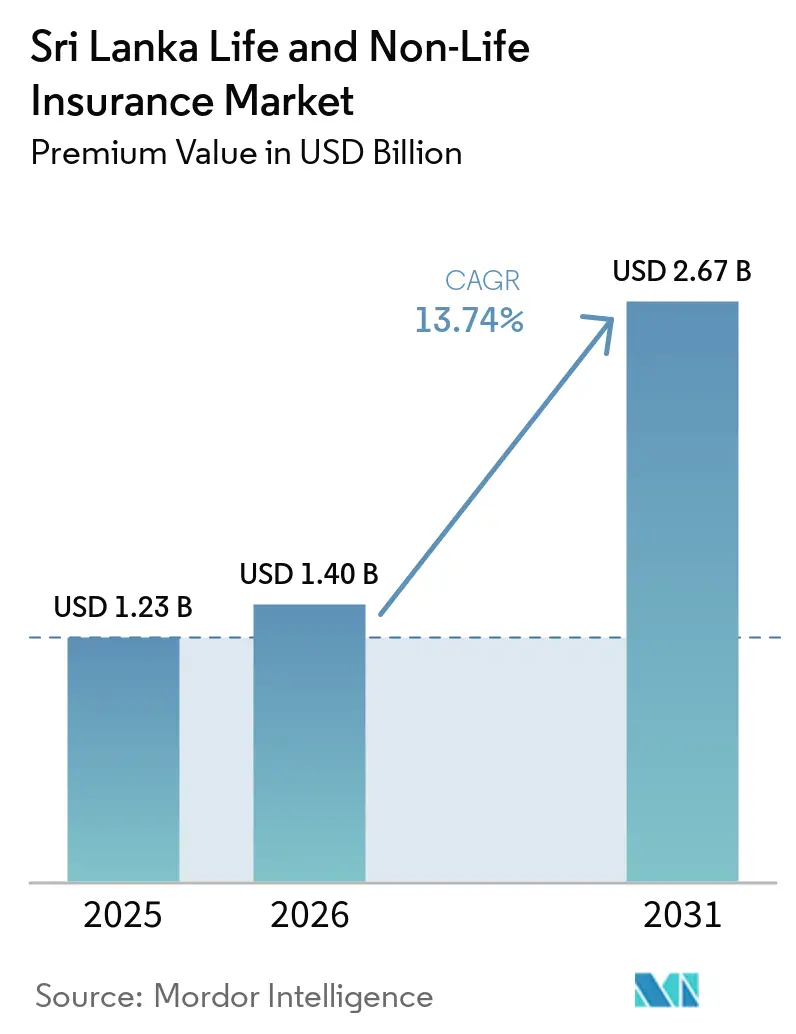

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 2.67 Billion |

| Growth Rate (2026 - 2031) | 13.74% CAGR |

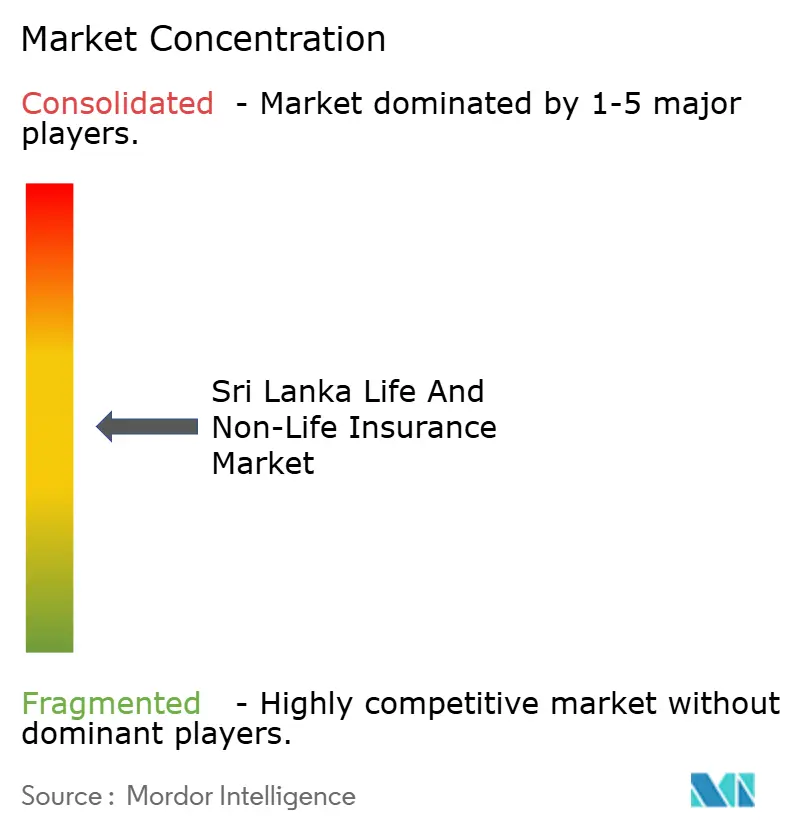

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Sri Lanka Life And Non-Life Insurance Market size in terms of premium value was valued at USD 1.23 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 2.67 billion by 2031, at a CAGR of 13.74% during the forecast period (2026-2031).

Strengthened solvency positions and revised risk-based capital rules support pricing discipline, product innovation, and measured geographic expansion across both life and general lines, which stabilizes operating conditions for the Sri Lanka Life and Non-Life Insurance market in 2026. The regulator’s digital agenda, including standardized medical coding and e-policy verification for motor, reduces frictional costs and helps shift distribution to balanced hybrid and direct models that can scale efficiently. IFRS 17 alignment improves liability measurement and comparability, which strengthens investor confidence and can narrow the cost of capital for well-governed carriers in the Sri Lankan Life and Non-Life Insurance market. The channel mix continues to evolve as bancassurance, mobile-enabled embedded covers, and online aggregators complement agency forces, which broadens access and underpins persistency for the Sri Lanka Life and Non-Life Insurance market.

Key Report Takeaways

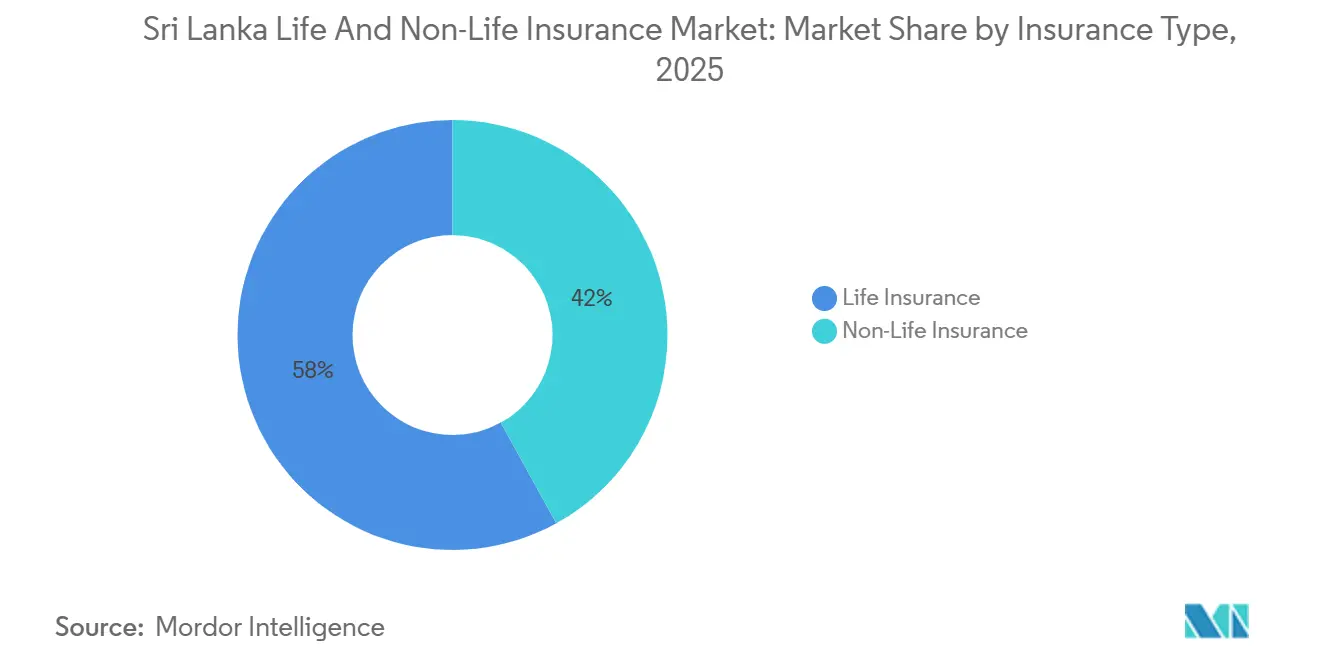

- By insurance type, life insurance led with 58.02% revenue of the Sri Lanka Life and Non-Life Insurance market share in 2025, non-life is positioned to record faster growth to 2031, while life is advancing at an 11.21% CAGR through 2031.

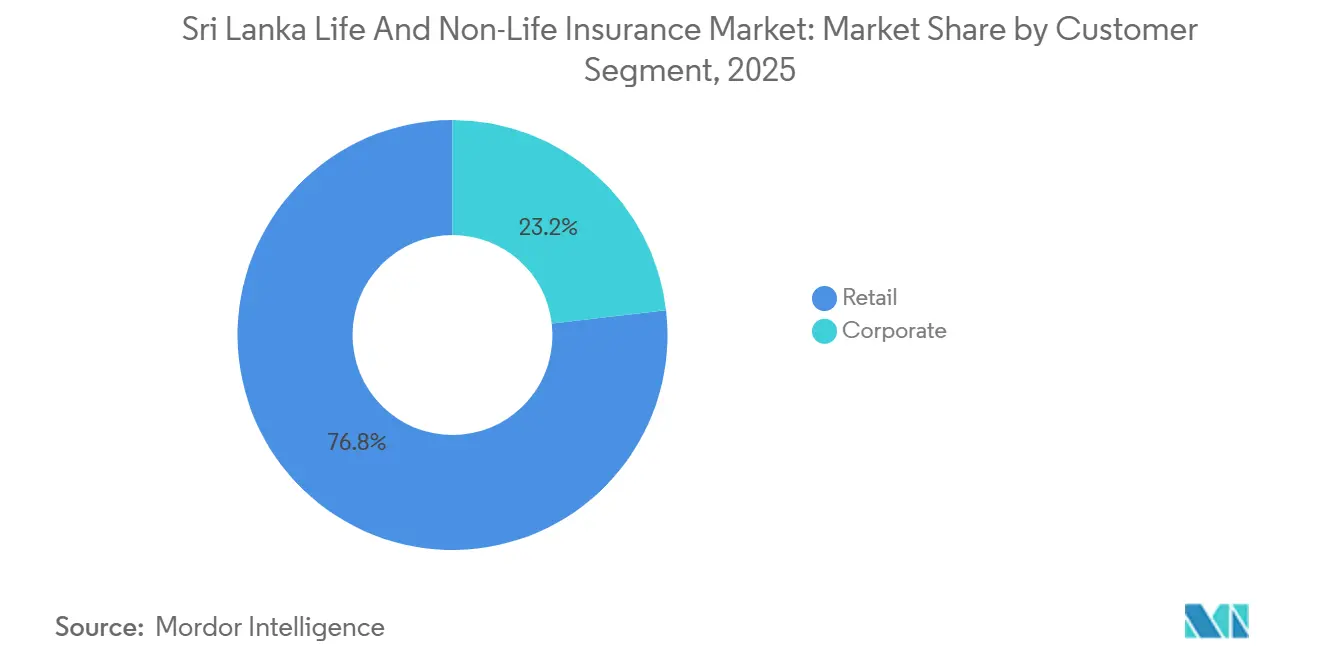

- By customer segment, retail accounted for 76.84% of premiums of the Sri Lanka Life and Non-Life Insurance market share in 2025, and corporate lines recorded the fastest projected growth at a 9.83% CAGR through 2031.

- By distribution channel, agents held a 36.74% of the Sri Lanka Life and Non-Life Insurance market share in 2025, digital and direct channels posted the highest projected growth at a 13.96% CAGR through 2031.

- By geography, Western Province captured 43.67% of premiums of the Sri Lanka Life and Non-Life Insurance market share in 2025, Northern Province is projected to deliver the fastest regional growth at an 11.56% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sri Lanka Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Motor import normalization expands motor GWP and cross-sells into add-ons | +2.8% | National, with early gains in Western Province | Short term (≤ 2 years) |

| Rapid uptake of digital and embedded micro-insurance via MNO/FLO channels | +1.9% | National, with rural spill-over | Medium term (2-4 years) |

| Strengthening bancassurance partnerships expands protection reach | +2.3% | National, concentrated in Western and Southern Provinces | Medium term (2-4 years) |

| Improved solvency (RBC) headroom enables product innovation and/ growth | +1.6% | National, regulatory uplift for all licensed insurers | Medium term (2-4 years) |

| An optional third-party motor compensation scheme boosts compliance and retention | +1.2% | National, stronger in Northern and Eastern Provinces | Short term (≤ 2 years) |

| IFRS 17 and revised RBC alignment enhance pricing transparency and investor confidence | +1.1% | National, listed insurers gain valuation benefits | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Motor Import Normalization Expands Motor GWP and Cross-Sell into Add-Ons

The staged reopening of vehicle imports through 2024 and early 2025 unlocked pent-up demand that had constrained motor premium growth and limited the breadth of comprehensive coverage in prior years, which improves near-term motor GWP and supports cross-sell into natural perils and roadside assistance in the Sri Lanka Life and Non-Life Insurance market [1]ETAuto, “Sri Lanka to lift ban on vehicle imports by Feb 2025,” AUTO.ECONOMICTIMES.INDIATIMES.COM, auto.economictimes.indiatimes.com. Listed and private carriers that had paused or narrowed comprehensive offerings during the import ban have restored full-feature policies and riders as parts supply and dealer networks normalize, which lifts average ticket sizes and stabilizes renewal rates for retail and fleet portfolios. Digital motor e-cards and a centralized verification database launched in January 2026 reduce fraud risk and simplify enforcement, which encourages compliance for mandatory third-party covers across the Sri Lanka Life and Non-Life Insurance market. The optional third-party compensation scheme and road-safety fund allocations complement this infrastructure and build public trust around claim settlement, which supports renewals and upgrades from liability-only to comprehensive policies. Portfolio breadth, better pricing signals, and streamlined verification collectively lower acquisition costs and improve persistency, which strengthens the revenue recovery path for general insurers in the Sri Lankan Life and Non-Life Insurance market.

Strengthening Bancassurance Partnerships Expand Protection Reach

Exclusive, long-duration bancassurance partnerships and leadership summits show deepening bank-insurer alignment around digital-first customer journeys, analytics-led cross-sell, and lifestyle engagement programs that move beyond transactional referrals in the Sri Lanka Life and Non-Life Insurance market. Referral programs tied to retail mortgages, auto loans, and SME working-capital lines integrate credit-life and protection at the point of banking need, which lifts attachment rates and lowers distribution costs per policy. Commission structures that favor life first-year premiums, renewal discipline, and welcome-call safeguards align economics with conduct standards, which helps protect customer outcomes as bancassurance grows. Joint wellness events and youth-focused engagement expand brand affinity and frame protection as part of everyday goals, which supports persistency and higher rider penetration across the Sri Lanka Life and Non-Life Insurance market. Strong solvency at leading life carriers provides comfort to partner banks on claim-paying ability through cycles, which supports broader product shelf space and sustained investment in joint digital workflows.

Optional Third-Party Motor Compensation Scheme Boosts Compliance and Retention

The optional compensation pathway provides ex gratia payments for third-party motor accident victims without court proceedings, which speeds relief and raises trust in claim outcomes across the Sri Lanka Life and Non-Life Insurance market [2]Insurance Regulatory Commission of Sri Lanka, “The Blueprint for Financial Resilience: IRCSL’s Mission to Transform Sri Lanka’s Insurance Industry,” IRCSL.GOV.LK, ircsl.gov.lk. The maximum compensation for death or permanent disability increased to Rs. 1 million in September 2025, which reflects higher medical and funeral costs and improves adequacy for victims. Clear eligibility rules and a six-month application window encourage timely reporting and protect the scheme’s focus on vulnerable third parties, which complements mandatory third-party motor coverage. Regulator hotlines and Insurance Ombudsman offer escalation channels that reduce friction and raise settlement confidence, which supports renewal rates for comprehensive motor policies. These elements reinforce compliance and encourage upgrades from liability-only to broader covers, which strengthen unit economics in the Sri Lanka Life and Non-Life Insurance market.

IFRS 17 and Revised RBC Alignment Enhance Pricing Transparency and Investor Confidence

IFRS 17 introduces a consistent recognition and measurement framework for insurance contracts, which improves comparability of embedded value, new business strain, and profit emergence across carriers in the Sri Lankan Life and Non-Life Insurance market. The transition required investments in actuarial systems and data integration, as evidenced by implementation programs across leading carriers, which have improved control environments and auditability. Harmonization between solvency and accounting measurement reduces dual-stack complexity and clarifies the bridge between statutory and regulatory numbers, which streamlines stakeholder communication. Anchored long-term inflation and discount-rate settings stabilize product pricing and guarantee calibration, which supports risk-appropriate returns and portfolio resilience. Greater transparency invites more informed capital allocation and broadens engagement from institutional investors, which benefits well-governed participants in the Sri Lankan Life and Non-Life Insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened premium payment enforcement elevates lapse/cancellation risk | -1.4% | National, acute in motor | Short term (≤ 2 years) |

| Claims-cost inflation in motor and medical pressures on underwriting margins | -1.8% | National, concentrated in Western Province | Medium term (2-4 years) |

| Low consumer trust/awareness slows conversion despite low penetration | -2.1% | National, more pronounced in rural provinces | Long term (≥ 4 years) |

| Compulsory cessions/SRCCT remittances compress non-life profitability | -1.3% | National, higher impact on catastrophe-exposed portfolios | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightened Premium Payment Enforcement Elevates Lapse/Cancellation Risk

Premium payment rules for general insurance were tightened through Circular No. 03 of 2025, including a staged reduction of motor credit periods to 30 days from January 2026 and movement toward upfront settlement by January 2028, which raises near-term lapse and cancellation risk among price-sensitive customers in the Sri Lanka Life and Non-Life Insurance market [3]Insurance Regulatory Commission of Sri Lanka, “Circular No. 03 of 2025: Requirement of Premium Payment for General Insurance,” IRCSL.GOV.LK, ircsl.gov.lk. Insurers may defer liability or postpone claims until premiums are fully paid, and non-payment by due dates can trigger cancellations, which shift payment discipline directly onto policyholders. The policy seeks to curb deferred-premium practices that strained cash flow during the 2022 shock, while aligning with regional norms that favor pay-as-you-go or installment-linked payments through banks and digital wallets. Carriers are investing in reminders, app-based renewals, and early-payment incentives to protect persistency, which becomes critical to maintaining revenue stability as rules phase in. The approach also strengthens revenue recognition under IFRS 17 and supports AML and CFT controls through clearer payment trails, which improves financial integrity across the Sri Lanka Life and Non-Life Insurance market.

Compulsory Cessions/SRCCT Remittances Compress Non-Life Profitability

General insurers must reinsure 30% of total reinsurance liabilities with the National Insurance Trust Fund Board, while motor contributes 2% of third-party premiums to the road-safety fund, which reduces net written premiums before expenses and claims reserves in the Sri Lanka Life and Non-Life Insurance market. Capital tied up in special reserves and dividend-distribution restrictions further tighten liquidity during IFRS 17 and RBC transitions, which require careful balance-sheet planning by carriers. Lack of retrocession cover at the state reinsurer during parts of 2023 to 2026 elevated peak-zone aggregation risk and pushed primary insurers to seek facultative reinsurance from global markets at higher cost. Regulatory engagement and new retrocession programs can mitigate concentration risk, but pass-through of higher reinsurance rates to policyholders may temper demand in price-sensitive segments. The net effect is a modest structural drag on non-life profitability until reinsurance capacity and capital release conditions normalize in the Sri Lankan Life and Non-Life Insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life Dominates GWP, Yet Non-Life Accelerates Post-Import Resumption

Life insurance captured 58.02% of the Sri Lanka Life and Non-Life Insurance market share in 2025 as households prioritized protection and retirement-linked goals across endowment, whole-life, and unit-linked lines, with life projected to grow at an 11.21% CAGR to 2031. The resumption of vehicle imports and stronger climate risk awareness provide a cyclical lift to general lines, which narrows the growth gap and broadens exposure to motor, health, and property in the Sri Lanka Life and Non-Life Insurance market. Revised RBC rules and IFRS 17 alignment create a consistent measurement base that rewards underwriting discipline and transparent pricing across both life and general portfolios. Digital claims, usage-based propositions for fleets, and parametric concepts in weather-linked risks broaden the product set that carriers can deliver without raising frictional costs. Combined with adequate capital buffers, this supports a balanced expansion path that preserves earnings quality in the Sri Lanka Life and Non-Life Insurance market.

General insurers benefit from digital motor e-cards and centralized verification that reduce fraud and sharpen compliance, which in turn lifts renewals and upgrades from liability-only to comprehensive in the Sri Lankan Life and Non-Life Insurance market. Health lines are supported by employer-sponsored group medical and rising private care utilization, while property finds traction in mortgage-linked and SME packages as lenders enforce collateral protection. As climate volatility persists, carriers can refine risk transfer through quota-share treaties and facultative placements, while exploring parametric triggers that reduce adjustment delays and operating costs. Against this backdrop, life remains the anchor of stable compounding, and general acts as a cyclical accelerator that helps the Sri Lanka Life and Non-Life Insurance market sustain a high-teens growth phase from 2026 to 2031.

By Customer Segment: Retail Prevails While Corporate Lines Capitalize on Infrastructure Boom

Retail accounted for 76.84% of premiums in 2025, reflecting the historic dominance of individual life, motor, and health covers distributed through large agency forces and rising direct digital channels in the Sri Lankan Life and Non-Life Insurance market. Corporate lines are projected to grow at a 9.83% CAGR through 2031 as infrastructure, manufacturing, and services adopt group life, group medical, engineering, and liability covers at scale. Bancassurance integration into corporate banking workflows increases keyman, credit-life, and benefits-linked cross-sell, which raises policy density per client in the Sri Lanka Life and Non-Life Insurance market. Employers seeking retention gains are expanding medical benefits and term protection, which support multi-year renewals and claims-managed networks for better cost control. Retail growth still anchors volumes through motor renewals and entry-level protection, with digital onboarding improving persistency fundamentals for the Sri Lanka Life and Non-Life Insurance market.

SME-focused propositions and standardized product packs are widening corporate penetration beyond large enterprises, while broker intermediation remains crucial for complex multi-location and marine risks in the Sri Lankan Life and Non-Life Insurance market. As credit cycles normalize and investment projects proceed, contractors’ all-risk, machinery breakdown, and project liability lines diversify revenue and reduce reliance on retail-heavy mixes. Digital servicing for endorsements, certificates, and claims improves cycle times for corporate clients and lowers back-office costs for carriers. The resulting blend of volume-heavy retail and margin-accretive corporate business supports a healthier earnings mix for the Sri Lanka Life and Non-Life Insurance market. These dynamics point to steady broadening of coverage across households and enterprises as execution improves in 2026 and beyond.

By Distribution Channel: Agents Hold Share Yet Digital/Direct Channels Surge

Agents held 36.74% of the Sri Lanka Life and Non-Life Insurance market size in 2025, sustained by personal relationships, field education, and commission structures that support face-to-face sales in lower-digital literacy segments. Digital and direct channels are the fastest-growing route with a 13.96% CAGR, aided by e-KYC, instant quotes, and e-policies that reduce acquisition costs and compress issuance times for the Sri Lanka Life and Non-Life Insurance market. Bancassurance remains a strong origination source for savings-linked and mortgage-attached covers, while brokers serve complex commercial placements and reinsurance interactions. Tablet-enabled agents and straight-through processing shorten cycle times and lift close rates, which supports persistency for both life and non-life policies. Over the forecast horizon, digital share gains will complement rather than replace agency and broker models in the Sri Lanka Life and Non-Life Insurance market.

The regulator’s standards for MNO and FLO partnerships require transparent disclosures, claims clarity, and data-protection compliance, which protects policyholder outcomes as embedded models scale. Digital motor e-cards and real-time verification reduce fraudulent covers and streamline roadside checks, which increases compliance and renewals for motor. As online aggregators bring transparent price comparisons and instant purchase flows, incumbents sharpen underwriting models and claim automation to compete on value rather than headline price. Hybrid engagement, where advisors guide complex choices and digital handles routine servicing, is becoming the operating norm. This transition keeps customer choice broad while improving economics for the Sri Lanka Life and Non-Life Insurance market.

Geography Analysis

Western Province remains the center of gravity for the Sri Lanka Life and Non-Life Insurance market, with 43.67% of premiums in 2025 due to the clustering of banking, corporate headquarters, and registered vehicles that drive higher-value life and comprehensive motor purchases. Colombo’s financial services workforce and HNWI presence raise penetration of unit-linked and critical-illness riders, while fleet and ride-hailing operators pursue telematics and usage-based policies that increase cross-sell into cargo and liability lines. The concentration of listed insurers also accelerates digital claims and servicing adoption, which boosts persistence and raises average premium per policy. Bancassurance maturity is deeper in this province due to branch density and data infrastructure, which improves lead quality and conversion. These conditions reinforce a premium mix that supports the Sri Lanka Life and Non-Life Insurance market’s revenue base in 2026.

Central and Southern Provinces deliver a meaningful combined contribution as tourism corridors, agrarian belts, and logistics hubs deploy property, liability, and marine covers in tandem with life and health protections for formal employees. Bank-led referrals tied to mortgages and SME finance expand credit-life attachment and group medical take-up, which increases persistency and reduces acquisition costs per policy. Plantation-linked communities are gradually adopting weather-indexed agri-covers, while hotels and logistics operators rely on public liability and marine cargo to protect business continuity. Awareness campaigns and vernacular disclosures improve product understanding and claims literacy, which strengthens the case for protection in these provinces. As digital servicing expands, policy issuance and endorsements are completed faster, which improves customer satisfaction and renewal readiness.

Northern and Eastern Provinces are on a steeper growth curve as reconstruction and small business formation create demand for mortgage, property, and SMEs’ shop-keeper packages, along with basic life and accident covers. Northern Province is projected to post an 11.56% CAGR over 2026 to 2031, which suggests catch-up potential from a low base as awareness efforts and digital onboarding reduce frictions for first-time policyholders in the Sri Lanka Life and Non-Life Insurance market. Coastal Eastern communities are testing parametric protection concepts that can pay in 48 to 72 hours after a verified trigger, which improves perceived value compared with traditional adjustment cycles. Inland agrarian provinces contend with affordability limits that micro-covers and digitized claims can partially address. With consistent education and digital rails, regional coverage can converge toward urban norms over the forecast horizon.

Competitive Landscape

Sri Lanka’s insurance sector shows balanced competition between entrenched leaders and dynamic challengers, with strong solvency discipline and an active focus on digital experience. Ceylinco Life maintained leading profitability and robust capital, including significant participation in listed sustainable debt that aligns with national development priorities and duration needs. Softlogic Life reported strong GWP growth in 2025 and continued to scale share on the back of customer-centric technology and rapid claims processing. LOLC General Insurance advanced its position with growth in motor and selective portfolio moves, reflecting execution in a recovering general market. These moves illustrate how scale, solvency, and digital operating models shape competitive outcomes in the Sri Lankan life and non-life insurance market.

Strategic themes center on inorganic growth, balance-sheet strength, and process automation. One leading player completed the acquisition of a peer’s life book in 2025 after regulatory approval, consolidating distribution and accelerating product cross-sell. Another secured a multi-year Tier 2 facility from development finance institutions in 2026 to deepen inclusive coverage and strengthen digital and service capabilities. Insurers are also prioritizing AI-driven claims platforms that validate medical codes, execute duplicate-check algorithms, and complete bank transfers quickly, which lowers costs and frees underwriting resources for complex cases. These actions boost competitiveness and support greater inclusion while maintaining focus on positive unit economics across the Sri Lankan life and non-life insurance market.

The regulatory environment reinforces market discipline and transparency. Revised solvency rules clarify risk charges and capital instruments, improving comparability and aligning supervisory focus with global practices. IFRS 17 adoption deepens investor confidence through better disclosure and consistent performance measurement across insurers, which supports fair valuation on the equity market. Process improvements and conduct standards across distribution, disclosures, and claims help reduce mis-selling risk and stabilize persistency. Altogether, policy clarity, capital strength, and digital delivery support a competitive yet orderly Sri Lankan life and non-life insurance market.

Sri Lanka Life and Non-Life Insurance Industry Leaders

Ceylinco Life Insurance PLC

Allianz Insurance Lanka Ltd

Softlogic Life Insurance PLC

Sri Lanka Insurance Corporation Life Limited

AIA Insurance Lanka PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SLIC General, in collaboration with the Sri Lanka Tourism Development Authority (SLTDA), launched "Adventure Plus," a personal accident cover targeting high-risk tourism activities, such as hiking, diving, and water sports, to support the growth of Sri Lanka's adventure tourism sector.

- February 2026: Fairfirst Insurance partnered with SLT-Mobitel to introduce Sri Lanka's first motor insurance product, enabling premium payments via mobile billing. This service enhances accessibility, particularly in rural areas, allowing users to manage insurance conveniently through Mobitel connections and the Click2Go platform.

- January 2026: Softlogic Life raised a USD 15 million, 5-year Tier 2 loan from Norfund and OP Finnfund Global Impact Fund I to reinforce its capital base. The funding supports expansion of national reach, digital platforms, and policyholder services, with a focus on microinsurance and AI-enabled underwriting. This capital infusion reflects confidence in the sector’s recovery trajectory and the company’s execution road map.

- January 2026: The Insurance Association of Sri Lanka launched a digital motor insurance e-card, enabling instant electronic proof of coverage and real-time verification by law enforcement. The initiative modernizes motor insurance servicing and reduces fraud through a centralized database and device-enabled checks. This aligns with the IRCSL’s broader digitalization agenda for the sector.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Sri Lankan life & non-life insurance market as the aggregate gross written premiums (GWP) generated by licensed insurers for life policies (whole, term, unit-linked, annuity, pension) and general covers (motor, health, property, travel, agriculture, marine, liability) issued within the country and denominated in Sri Lankan rupees, later converted to USD at annual average rates.

Scope exclusion: reinsurance placed offshore and purely investment-linked funds without a risk cover are not counted.

Segmentation Overview

- By Insurance Type

- Life Insurance

- Non-Life Insurance

- Motor Insurance

- Health Insurance

- Property Insurance

- Liability Insurance

- Other Insurance

- By Customer Segment

- Retail

- Corporate

- By Distribution Channel

- Brokers

- Agents

- Banks

- Direct Sales

- Other Channels

- By Geography

- Western Province

- Central Province

- Southern Province

- Northern Province

- Eastern Province

- North Western Province

- North Central Province

- Uva Province

- Sabaragamuwa Province

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with underwriting managers, bancassurance heads, agent network leaders, and consumer advocates across Western, Central, and emerging Eastern provinces provided firsthand views on premium elasticity, claims ratios, and channel cost structures. These interviews validated desk findings, highlighted hidden lapses in retention rates, and guided the final adjustments that make our estimates realistic yet defensible.

Desk Research

We worked through public macro sources such as the Insurance Regulatory Commission of Sri Lanka, Central Bank annual reports, the Treasury's economic statistics, and trade data from Sri Lanka Customs, which clarify premium flows and vehicle registrations that anchor motor risk pools. Wider context came from regional bodies such as the Asian Development Bank and the World Bank, which track disposable income and health spending trends. Company 10-Ks and investor presentations helped us capture pricing shifts, while reputable press and Statista series supplied timely signals on digital channel uptake. Our analysts also referenced paid intelligence from D&B Hoovers for insurer financials and Dow Jones Factiva for deal news that shaped competitive landscape insights.

The secondary-source list above is illustrative; many additional publicly available and subscription datasets were examined to cross-check figures and fill data gaps.

Market-Sizing & Forecasting

We began with a top-down reconstruction of historical gross written premiums, layering IRCSL filings onto Central Bank exchange rates, then allocating totals by line using reported mix ratios, which are then stress-tested against sampled average premium multiplied by policy volumes from insurer disclosures. Selective bottom-up checks, such as motor policy counts from the Department of Motor Traffic and group-life cover penetration among formal employees, helped us refine outliers. Key drivers in the model include household disposable income, new vehicle registrations, private health expenditure, policy lapse rates, exchange-rate movements, and real lending rates that influence single-premium products. Multivariate regression projected each driver through the forecast period, producing our baseline value and a growth rate. Where primary data were missing, we imputed values using three-year moving averages and conservative variance bands before rerunning validations.

Data Validation & Update Cycle

Every draft model passes anomaly scans, peer review, and senior sign-off. Outputs are reconciled with fresh IRCSL releases and economic updates each quarter; full report refresh follows annually, with interim revisions triggered by regulatory or macro shocks.

Why Mordor's Sri Lanka Life & Non-Life Insurance Baseline Earns Trust

Published estimates often differ because firms pick dissimilar scopes, exchange rates, and refresh cadences.

By centering on regulator-verified GWPs, consistent currency conversion, and annual re-benchmarking, Mordor Intelligence delivers a dependable starting point for planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.20 B (2025) | Mordor Intelligence | - |

| USD 0.87 B (2025) | Regional Consultancy A | Excludes health premiums and micro-insurance, uses narrow agent channel data |

| USD 1.10 B (2024) | Industry Journal B | Relies on preliminary GWP, no currency normalization, omits life single-premium products |

| USD 1.87 B (2023) | Global Consultancy C | Includes investment-linked funds and embedded credit-life; older base year inflates total |

These comparisons show that scope breadth, currency handling, and update timing drive the observed spread. By applying clear definitions, multi-source validation, and yearly recalibration, our baseline offers balanced, transparent figures that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the outlook for the Sri Lanka Life and Non-Life Insurance market through 2031??

The Sri Lanka Life and Non-Life Insurance market is USD 1.40 billion in 2026 and projected to reach USD 2.67 billion by 2031 at a 13.74% CAGR, supported by solvency strength, digitalization, and channel diversification.

Which product side leads in the Sri Lanka Life and Non-Life Insurance market?

Life insurance leads with 58.02% of 2025 premiums and is growing at an 11.21% CAGR to 2031, while general lines are accelerating as motor imports resume and climate awareness lifts property and SME covers.

How are channels shifting in the Sri Lankan Life and Non-Life Insurance market?

Agents remain the largest by share at 36.74% in 2025, while digital and direct channels post a 13.96% CAGR as e-KYC and e-policies reduce acquisition and servicing costs.

Which regions are growing fastest within the Sri Lanka Life and Non-Life Insurance market?

Western Province is the largest at 43.67% of 2025 premiums, while Northern Province is projected to be the fastest at 11.56% CAGR from 2026 to 2031 as reconstruction and microenterprise activity increase adoption.

What regulatory changes are most important for the Sri Lankan Life and Non-Life Insurance market?

IFRS 17 alignment and revised Risk-Based Capital rules improve pricing transparency, comparability, and capital calibration, which strengthens investor confidence and supports disciplined growth.

Which companies made notable strategic moves from 2025 to 2026 in Sri Lanka?

Softlogic Life completed the acquisition of Allianz Life Insurance Lanka's life book in 2025 and raised a USD 15 million Tier 2 facility in 2026 to fund distribution, digital platforms, and inclusive products.

Page last updated on: