Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

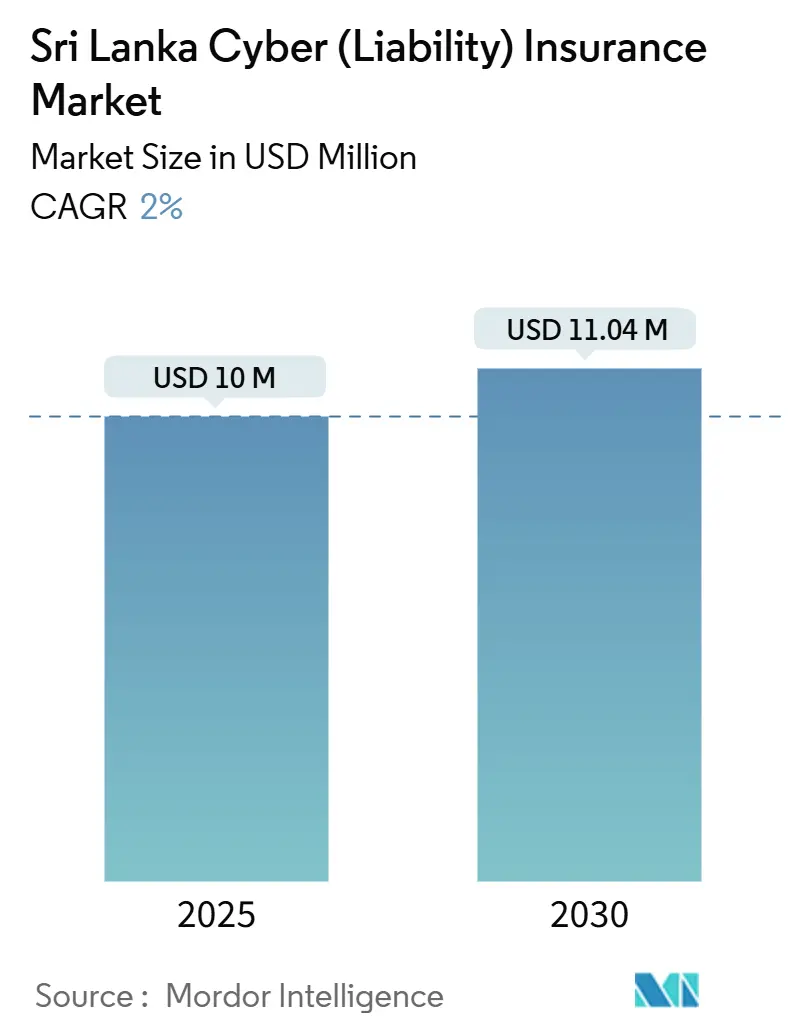

| Market Size (2025) | USD 10 Million |

| Market Size (2030) | USD 11.04 Million |

| Growth Rate (2025 - 2030) | 2.00% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Cyber (Liability) Insurance Market Analysis by Mordor Intelligence

The Sri Lanka cyber (liability) insurance market size is valued at USD 10 million in 2025 and is projected to reach USD 11.04 million by 2030, advancing at a 2% CAGR. The modest topline masks deeper momentum: the Personal Data Protection Act (PDPA) became enforceable on 18 March 2025, triggering mandatory fines and driving liability-transfer conversations across boardrooms. Banking Act Direction No. 16 of 2021 has already required technology-risk frameworks, so financial institutions are extending first-party and third-party cyber cover to satisfy auditors and cross-border data rules [1]Central Bank of Sri Lanka, “Banking Act Direction No. 16 of 2021 on Technology Risk Management,” cbsl.gov.lk. Rapid real-time payments adoption, hyperscale cloud build-outs, and a surge in ransomware incidents are widening attack surfaces, while restrictive reinsurer sub-limits, scant actuarial data, and foreign-exchange volatility temper capacity. As a result, the Sri Lanka cyber (liability) insurance market continues to evolve through bundled micro-products for SMEs, AI-driven underwriting, and government procurement mandates that embed insurance in Digital Public Infrastructure (DPI) tenders.

Key Report Takeaways

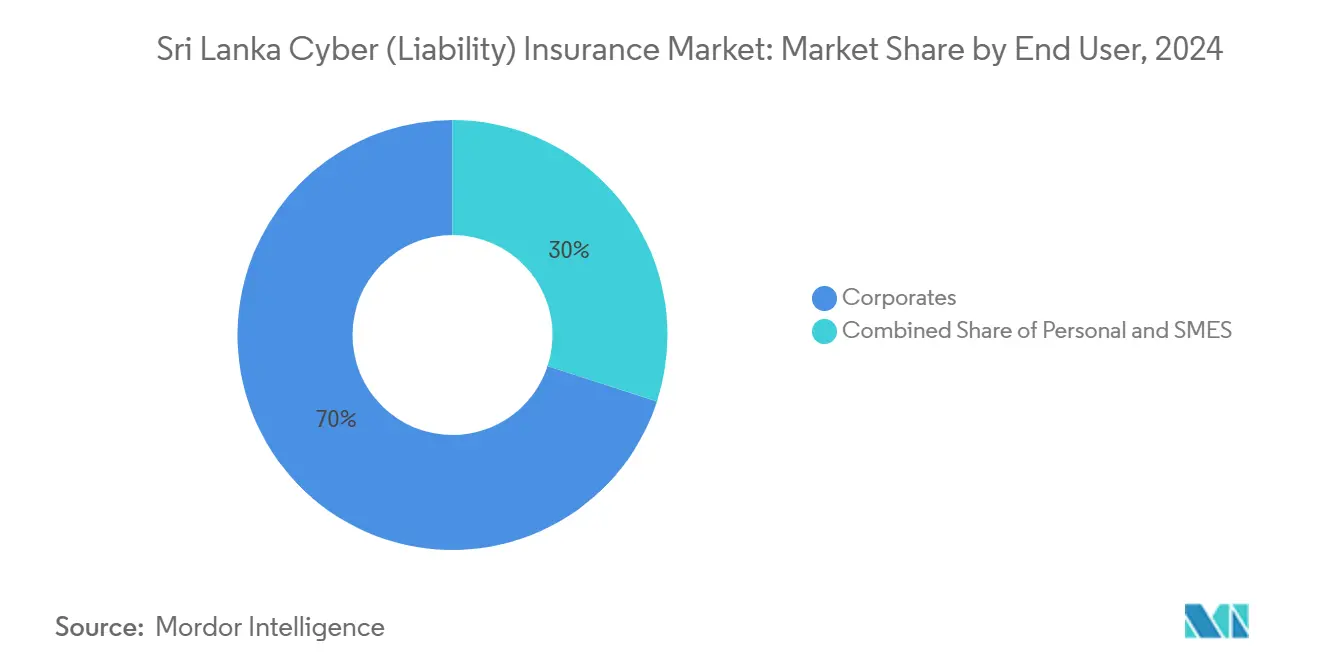

- By end user, corporates captured 70% of the Sri Lanka cyber (liability) insurance market share in 2024, whereas SMEs are forecast to expand at an 8.1% CAGR through 2030.

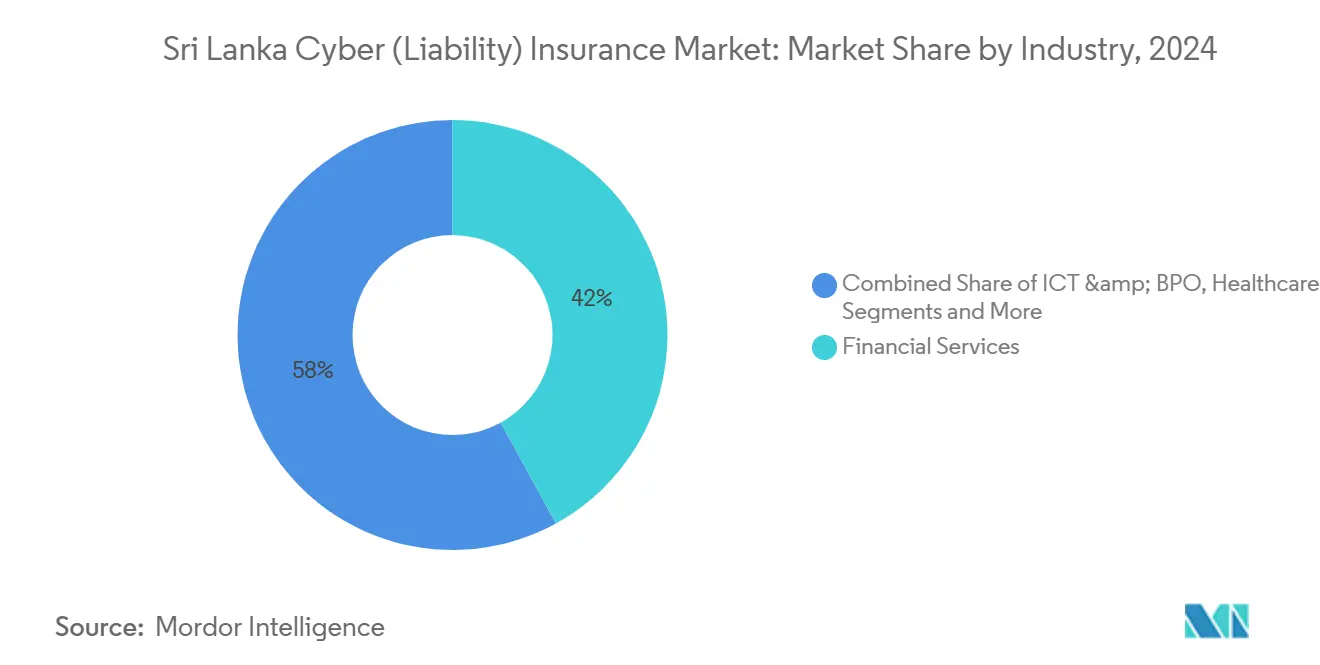

- By industry, financial services controlled 42% revenue share of the Sri Lanka cyber (liability) insurance market in 2024, while ICT and BPO activities are advancing at an 8.9% CAGR to 2030.

- By geography, the Western Province generated roughly 80% of gross written cyber-insurance premiums in 2024, far outstriking all other Sri Lankan provinces that collectively contributed the remaining 20%.

Sri Lanka Cyber (Liability) Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitalization of banking & fintech | +1.2% | Colombo financial district and nationwide payment rails | Short term (≤ 2 years) |

| Enforcement of the Personal Data Protection Act | +0.9% | National, early compliance in Western Province | Medium term (2-4 years) |

| Surge in cloud & hyperscale data centers | +0.5% | Colombo and Gampaha districts | Medium term (2-4 years) |

| Growing ransomware frequency in financial SMEs | +0.7% | Urban commercial hubs nationwide | Short term (≤ 2 years) |

| Public-sector tenders mandating cyber cover | +0.4% | National government procurement | Long term (≥ 4 years) |

| AI-driven low-cost SME underwriting | +0.3% | Pilot deployments in Colombo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitalization of Banking and Fintech Sector Drives First-Party Cyber Demand

Sri Lanka’s payment infrastructure surpassed national GDP in processed value during 2024, with LankaPay clearing 56.9 million real-time transactions worth LKR 4.6 trillion in Q4 2024 alone [2]LankaPay, “Quarterly Payment Statistics Q4 2024,” lankapay.lk. LankaQR widened uptake to 31 mobile-banking apps and 22 banks, intensifying exposure to ransomware-driven business-interruption claims that insurers currently price at 15%-20% of sums insured. JustPay averages 2.5 million wallet transactions monthly, so that a single credential leak would activate first-party forensic and third-party card-reissuance clauses. FinCSIRT, created in 2024, now requires incident reporting across the sector, which normalizes cyber cover as part of regulatory compliance. Carriers are bundling breach-response services and 24/7 hotlines to reposition policies as active risk-management tools rather than passive indemnity promises.

Enforcement of the Personal Data Protection Act Compels Liability Transfer

Core PDPA provisions impose fines of up to LKR 10 million per violation and mandate 72-hour breach disclosure windows. Multinationals juggling both PDPA and GDPR exposures demand broader territorial limits and regulatory-defense sub-limits from their Sri Lanka cyber (liability) insurance market programs. Allianz Lanka recorded a 40% jump in quote requests after March 2025, especially for coverage that reimburses notification costs, credit-monitoring, and reputation management. Local carriers lacking breach-response panels now partner with international managing general agents, ceding 20%-30% of premium in exchange for expertise. Clearer enforcement guidance from the Data Protection Authority reduces ambiguity, turning data-breach risk into a quantifiable liability that underwriters can price.

Cloud and Hyperscale Data-Center Projects Expand Insurable Asset Base

Government procurement for Lanka Government Cloud 2.5 integrates sovereign servers with AWS, Microsoft Azure, and five other hyperscalers, multiplying dependent-business-interruption exposures. Dialog Axiata’s Tier III data center, valued at USD 50 million, carries cyber endorsements covering physical sabotage of cooling and power systems. A regional AWS outage in 2024 halted several fintech apps for six hours, spotlighting aggregation risk; reinsurers now cap per-provider exposure at USD 5 million, forcing primary carriers to layer treaties and pushing up rates. As cloud residency rules bifurcate sensitive and nonsensitive workloads, underwriters refine wording to address jurisdictional ambiguities.

Ransomware Frequency Targeting Financial SMEs Accelerates First-Time Buyer Conversion

SLCERT logged more than 1,200 cyber incidents in 2024, 60% of which involved ransomware or phishing. Double-extortion demands range from USD 15,000 to USD 50,000, eclipsing annual IT budgets of many SMEs. The June 2024 Dialog Axiata breach underscored reputational fallout, spurring telecommunications and BPO operators to raise limits. Micro-cyber products priced between LKR 5,000 and LKR 10,000 are converting previously uninsurable SMEs into policyholders through cooperative channels. Insurers complement coverage with risk-engineering advisories, reducing claim frequency and enhancing underwriting profitability.

Restraints Impact Analysis

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low cyber-risk awareness & affordability in SMEs | -0.8% | Rural and semi-urban districts nationwide | Medium term (2-4 years) |

| Scarce actuarial loss data inflates premiums | -0.6% | All market segments | Long term (≥ 4 years) |

| Forex volatility limiting reinsurer appetite | -0.5% | Macroeconomic constraints across Sri Lanka | Short term (≤ 2 years) |

| Systemic DPI concentration exclusions | -0.3% | Government and large-enterprise segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Cyber-Risk Awareness and Affordability Among SMEs Throttle Penetration

MSMEs account for 75% of all enterprises, yet fewer than 25% maintain IT budgets, and surveys show 75% of owners rank cyber peril below fire or theft [3]MITRE SARDI, “Cybersecurity Landscape of Sri Lankan MSMEs 2024,” mitre.org. Stand-alone premiums of LKR 15,000-25,000 equate to 5%-10% of discretionary spend, while English-only policy wordings alienate Sinhala- and Tamil-speaking proprietors. Rural distribution gaps persist despite Central Bank inclusion drives, limiting the Sri Lanka cyber (liability) insurance market’s geographic reach and keeping penetration below 1% of addressable SMEs. Insurers trial vernacular mobile apps, but uptake hinges on bundling coverage with payment terminals and government digital-village kiosks.

Scarce Actuarial Loss Data Inflates Premiums and Deters Uptake

Only 5% of the 1,200 reported 2024 cyber incidents converted into claims, depriving underwriters of frequency-severity curves. Carriers therefore apply 30%-50% loadings derived from U.S. and U.K. loss models, making premiums uncompetitive versus markets like India, where mandated reporting under IRDAI supports refined pricing. Reinsurers also demand high ceding commissions, squeezing primary-carrier margins and discouraging product innovation. Without an anonymized loss consortium, data scarcity will persist, delaying maturation of the Sri Lanka cyber (liability) insurance industry.

Segment Analysis

By End User: Corporates Anchor Premium, SMEs Drive Volume Growth

Corporates dominated the Sri Lanka cyber (liability) insurance market with 70% premium share in 2024, supported by cross-border data flows and parent-company insurance mandates. Financial-sector corporates often layer USD 5 million-USD 25 million local policies beneath global towers to satisfy territorial rules. Large Colombo-listed banks reference Banking Act Direction No. 16 to justify purchasing high-limit first-party cover for payment-switch outages [4]Central Bank of Sri Lanka, “Financial System Stability Review 2025,” cbsl.gov.lk. Conversely, SMEs post the fastest 8.1% CAGR to 2030 as cooperative insurers bundle micro-cyber riders into property policies, lowering acquisition friction. AI-enabled underwriting cuts cycle time and premium levels, expanding the Sri Lanka cyber (liability) insurance market to merchants previously regarded as sub-scale. Despite progress, fewer than 2% of personal digital users buy individual cyber cover, hindered by low credit-card penetration and limited digital literacy.

Corporate growth remains sensitive to reinsurer appetite and foreign-exchange swings, which can inflate excess-layer pricing by 30%-50%. SMEs rely on vernacular distribution and government digitalization grants to underwrite security upgrades. Fintech-platform partnerships convert insurance from a pull to a push product, embedding micro-limits at checkout or loan origination. Personal-lines potential hinges on reframing coverage around family protection for online fraud and cyberbullying. As insurers calibrate segment-level loss data, granular rating may emerge, aligning premiums with actual risk and fostering healthier expansion of the Sri Lanka cyber (liability) insurance market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Industry: Financial Services Dominate, ICT and BPO Accelerate

Financial services commanded 42% of Sri Lanka cyber (liability) insurance market share in 2024, reflecting real-time payment velocity and strict incident-reporting mandates. Banks buy high deductibles paired with forensic-cost sub-limits, while payment-service providers focus on social-engineering and fraudulent-transfer endorsements. ICT and BPO firms are projected to expand at an 8.9% CAGR through 2030, as Colombo positions itself as a South Asian tech hub. Data-center operators such as Dialog Axiata carry USD 50 million limits including property-damage riders, signaling a shift toward blended cyber-physical policies.

Government agencies, with an 18% premium share, are adding coverage as DPI initiatives mandate minimum limits. Healthcare, professional services, and e-commerce collectively hold the remaining 40% but show uneven maturity; telemedicine platforms raise healthcare demand, while thin margins restrain retail spending. Nano-policies using parametric ransomware triggers cater to social-commerce micro-merchants, illustrating product innovation possibilities. Cross-industry systemic-event exclusions remain a headwind, yet broader sectoral participation is vital for balanced development of the Sri Lanka cyber (liability) insurance industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Colombo and the wider Western Province generated about 80% of the Sri Lanka cyber (liability) insurance market’s premium volume in 2024, reflecting the region’s concentration of banks, telecom headquarters, and government ministries. The proximity of regulators and the Data Protection Authority streamlines compliance conversations, while Tier III data centers and payment-switch assets anchor high-value insured infrastructure. Any ransomware event against LankaPay’s Colombo systems would reverberate nationally, validating demand for large-limit policies.

Outside the Western Province, Central, Southern, and Northern provinces combine for less than 15% of premiums, as informal micro-enterprises operate below the regulatory radar. Digital Villages, slated for launch in 2026, could unlock rural demand if insurers synchronize agent training, vernacular wordings, and mobile-enabled proposal systems. The Eastern Province’s Trincomalee port corridor presents emerging exposure as logistics operators digitize manifests and customs processes, yet underwriters currently apply a uniform rating that may misprice provincial risk.

Geographic penetration depends on closing the data gap; without regional claims benchmarks, carriers load national averages into pricing, discouraging low-risk rural enterprises from purchasing cover. Cooperative networks and affinity distribution through agricultural payment platforms could alleviate outreach costs. Over time, granular geospatial loss mapping can refine tariffs and support healthier provincial expansion of the Sri Lanka cyber (liability) insurance market.

Competitive Landscape

The top five domestic carriers—Fairfirst Insurance, Allianz Lanka, Sri Lanka Insurance Corporation, AXA XL, and Milliman Insurance—held an estimated 81% share of Sri Lanka cyber (liability) insurance market premium in 2024. Fairfirst leads at 28%, leveraging an extensive corporate portfolio and early-mover standalone cyber products. Allianz Lanka deploys its Cyber Protect suite, integrating global breach-response hubs that resonate with multinational buyers. Sri Lanka Insurance Corporation leverages preferential access to government tenders but lags in actuarial sophistication.

International capacity providers—Chubb, AIG, Tokio Marine HCC, and Zurich—participate via broker placements, supplying excess layers and specialist modules for cyber-extortion and social-engineering fraud. Brokers Marsh McLennan and Willis Towers Watson employ tools such as Cyber Catalyst to quantify exposure and negotiate Lloyd 's-backed capacity, although forex volatility adds 30%-50% cost overhead. Competitive differentiation now revolves around AI-enabled underwriting, parametric triggers, and embedded-insurance partnerships with fintechs.

White-space opportunities include SME-bundled covers distributed through digital wallets, parametric ransomware payouts requiring minimal documentation, and cooperative-channel micro-limits priced between LKR 5,000 and LKR 10,000. Softlogic’s instant-quote engine offers a 40% discount to low-risk applicants, pressuring incumbents to digitize workflows or risk ceding share. As more carriers join loss-data pools and refine pricing, competition will likely shift from capacity provision to value-added services that lower claim frequency and protect customer operations, sustaining balanced growth of the Sri Lanka cyber (liability) insurance market.

Sri Lanka Cyber (Liability) Insurance Industry Leaders

Fairfirst Insurance

Milliman Insurance

Allianz Lanka

AXA XL

IIRM Lanka

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: The PDPA’s core sections took effect, imposing fines up to LKR 10 million and causing a 40% spike in corporate policy inquiries.

- January 2025: GovPay soft-launched with 16 public agencies and mandated USD 1 million cyber-liability limits for all payment-service providers.

- October 2024: Government awarded contracts for Lanka Government Cloud 2.5, expanding dependent-business-interruption exposures across hyperscale providers.

- September 2024: Ceylinco General Insurance reported 28% premium growth to LKR 14.9 billion, naming cyber as a 2026 product focus.

Sri Lanka Cyber (Liability) Insurance Market Report Scope

By End User

| Personal |

| SMEs |

| Corporates |

By Industry

| Financial Services |

| Government Bodies / Agencies |

| Healthcare |

| Professional Services |

| ICT & BPO |

| Retail & E-commerce |

| Hospitality & Tourism |

| Other Industries |

By Geography

| Colombo & Western Province |

| Southern Coast |

| Central & Hill Country |

| Rest of the Sri Lanka |

| By End User | Personal |

| SMEs | |

| Corporates | |

| By Industry | Financial Services |

| Government Bodies / Agencies | |

| Healthcare | |

| Professional Services | |

| ICT & BPO | |

| Retail & E-commerce | |

| Hospitality & Tourism | |

| Other Industries | |

| By Geography | Colombo & Western Province |

| Southern Coast | |

| Central & Hill Country | |

| Rest of the Sri Lanka |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Sri Lanka cyber (liability) insurance market?

The market stands at USD 10 million in 2025 and is forecast to reach USD 11.04 million by 2030.

Which end-user group buys the most cyber cover in Sri Lanka?

Corporates account for 70% of written premium, reflecting audit demands and cross-border data obligations.

Which segment is expanding fastest through 2030?

SME policies are projected to grow at an 8.1% CAGR as government digitalization and micro-insurance bundles lower barriers.

How large is the financial services share of cyber premiums?

Financial institutions captured 42% of premiums in 2024 due to high transaction volumes and mandatory incident reporting.

What regulatory change most influences future demand?

Enforcement of the Personal Data Protection Act, starting March 2025, introduces fines up to LKR 10 million, motivating companies to transfer liability through insurance.

Which insurers lead the market today?

Fairfirst Insurance, Allianz Lanka, Sri Lanka Insurance Corporation, AXA XL, and Milliman Insurance jointly control about 81% of premium volume.