Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

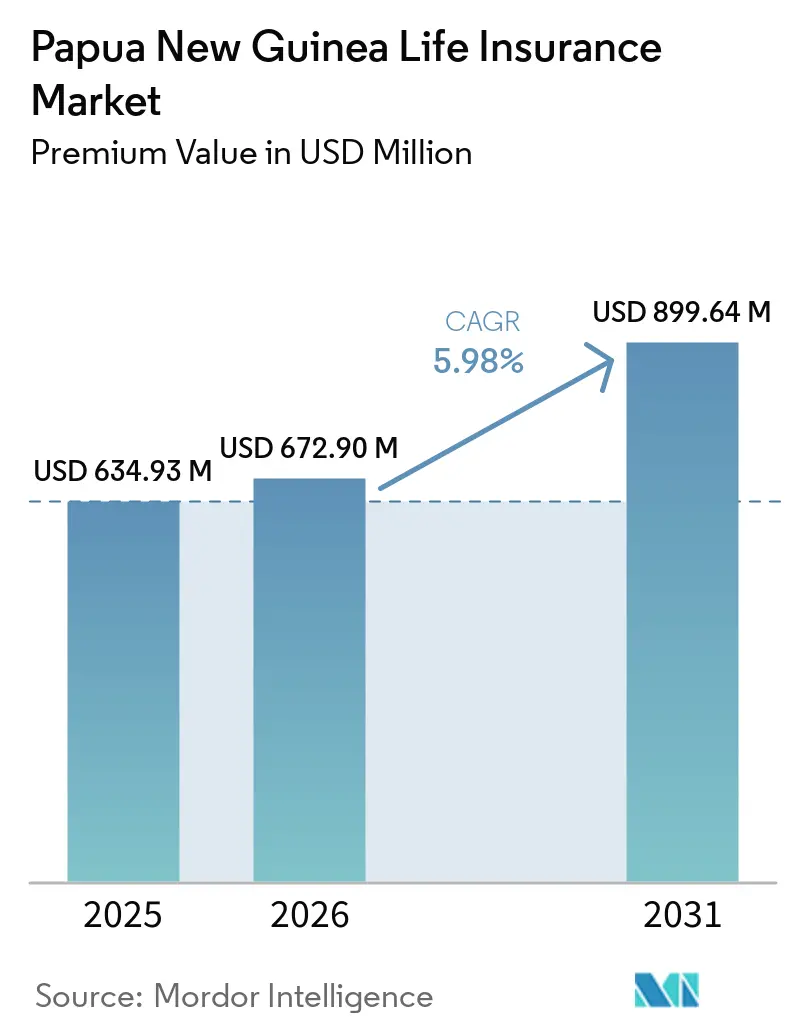

| Base Year Market Size (2025) | USD 634.93 Million |

| Market Size (2026) | USD 672.90 Million |

| Market Size (2031) | USD 899.64 Million |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Papua New Guinea Life Insurance Market Analysis by Mordor Intelligence

The Papua New Guinea Life Insurance Market size in terms of premium value is expected to grow from USD 634.93 million in 2025 to USD 672.90 million in 2026 and is forecast to reach USD 899.64 million by 2031 at 5.98% CAGR over 2026-2031.

The trajectory reflects mandatory superannuation-linked group plans, rising mobile micro-insurance, and climate-resilient product innovation that widens reach into the country’s largely informal economy. Unit-linked policies have benefited from recovering commodity revenues, while annuities ride demographic shifts toward retirement income planning. Insurers leverage bancassurance and mobile agents to offset geographic dispersion costs, and stronger prudential oversight under the Bank of Papua New Guinea encourages capital inflows, including reinsurance capacity. Still, low financial literacy, cyber risk, and foreign-exchange constraints temper growth prospects as carriers balance product affordability with solvency requirements.

Key Report Takeaways

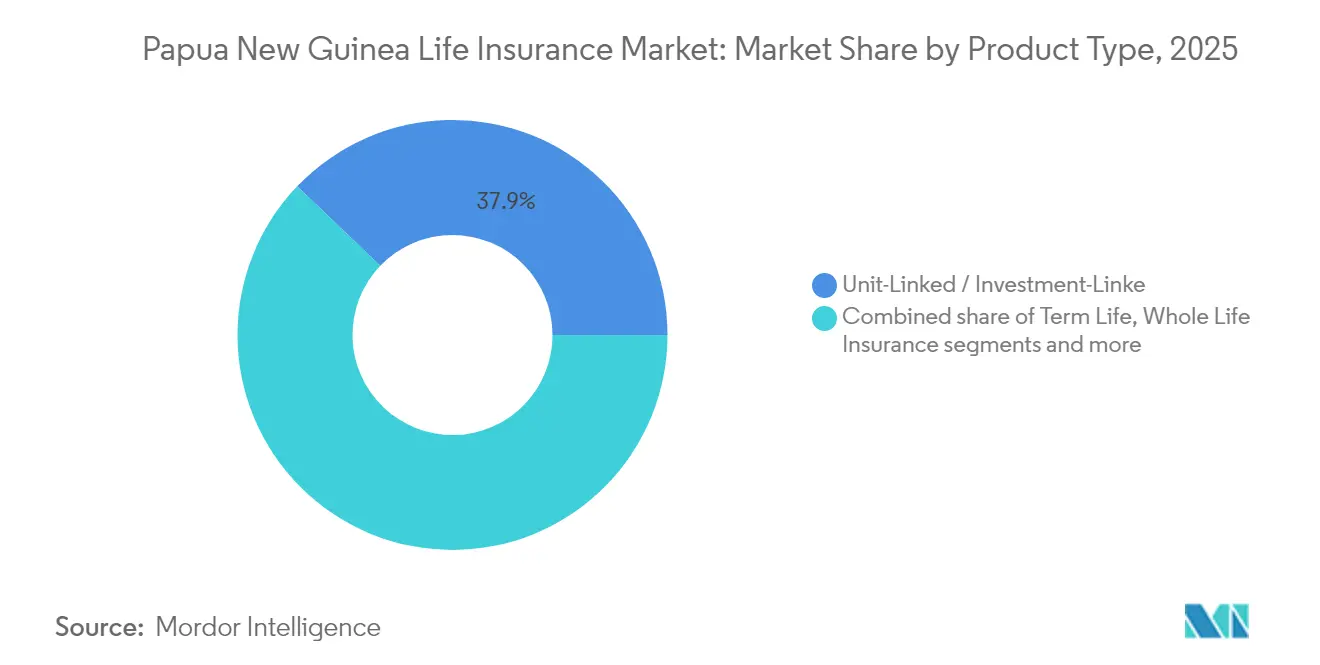

- By product type, unit-linked offerings led with 37.85% of Papua New Guinea life insurance market share in 2025, while annuity products are projected to record the fastest 6.87% CAGR through 2031.

- By distribution channel, agents accounted for 44.15% of Papua New Guinea's life insurance market size in 2025, whereas online marketplaces posted the highest 7.72% CAGR forecast to 2031.

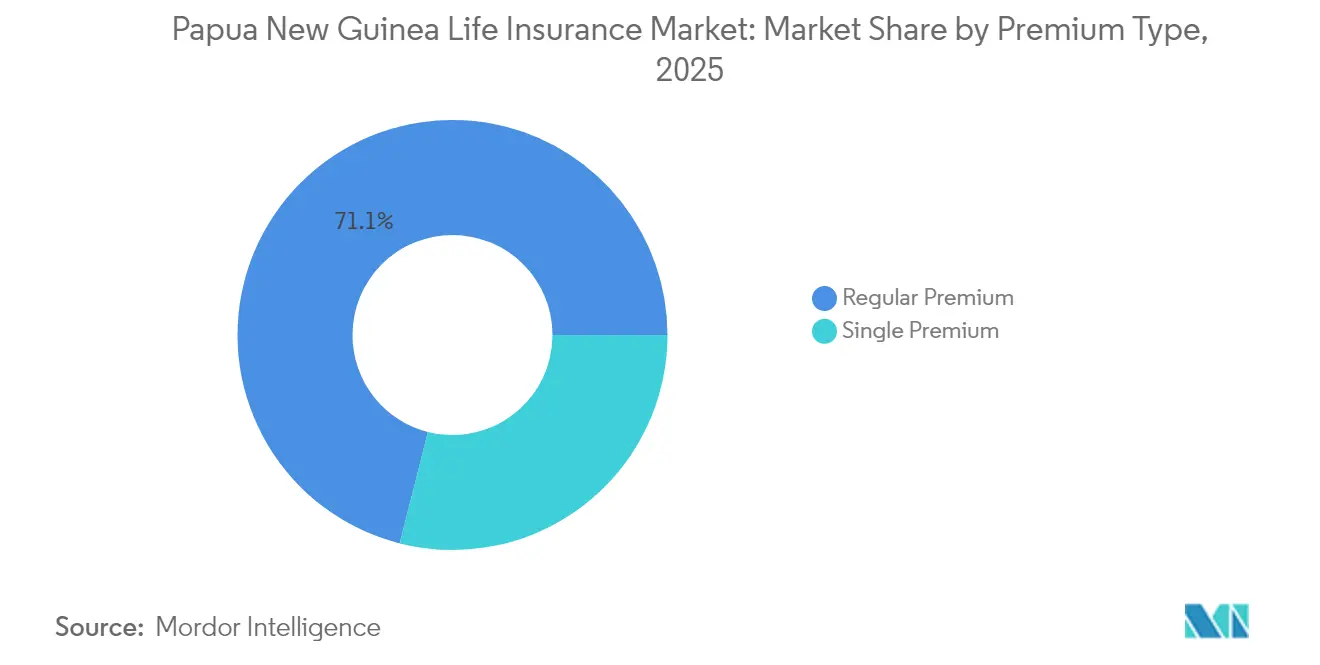

- By premium structure, regular-premium contracts dominated with a 71.05% share of Papua New Guinea's life insurance market size in 2025, yet single-premium business is set to expand at a 7.29% CAGR to 2031.

- By customer age group, the 25-44 cohort captured 48.75% of Papua New Guinea's life insurance market share in 2025, while the 45-64 segment is expected to grow fastest at 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Papua New Guinea Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory employer-superannuation contributions spur group-life uptake | +1.8% | National, concentrated in formal employment centers | Medium term (2-4 years) |

| Mobile & agent-led micro-insurance expansion | +1.5% | National, strongest in urban and peri-urban areas | Short term (≤ 2 years) |

| Growing urban middle class and formal employment | +1.2% | Port Moresby, Lae, Mount Hagen, regional centers | Long term (≥ 4 years) |

| Strengthening prudential & solvency supervision by BPNG | + 0.9% | National regulatory framework | Medium term (2-4 years) |

| Climate-risk financing pilots bundling life & catastrophe cover | +0.7% | Coastal and disaster-prone provinces | Long term (≥ 4 years) |

| Remittance-linked life-savings products for PNG diaspora | +0.6% | International corridors, domestic recipient communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Employer-Superannuation Contributions Spur Group-Life Uptake

Nasfund managed PGK 8.92 billion (USD 2.4 billion) in member funds across more than 724,680 accounts in 2025, and compulsory payroll deductions automatically bundle death and disability coverage that lifts group penetration[1]Bank of Papua New Guinea, “Quarterly Economic Bulletin Q1 2025,” bankpng.gov.pg. Predictable premium flows reduce underwriting costs, enabling lower group rates and broader coverage for mining, government, and banking workers. Prudential rules enforced by the Bank of Papua New Guinea safeguard reserves, which sustain insurer appetite for long-duration liabilities. Integrating insurance into workplace benefits offsets low retail awareness, particularly for high-risk industries that confront income-protection gaps. Employers exceeding minimum contribution thresholds further enlarge the overall Papua New Guinea life insurance market as voluntary top-ups translate into higher sum-assured levels.

Mobile & Agent-Led Micro-Insurance Expansion

BIMA reached 282,289 customers by partnering with Digicel to allow premium deductions from airtime, overcoming branch scarcity and language barriers[2]UNCDF, “Pacific Insurance and Climate Adaptation Programme Update 2025,” uncdf.org. Agent networks explain simple K2.70 monthly covers in local dialects, unlocking sales among cocoa farmers, market vendors, and seasonal laborers. The Digizen digital ID pilot with 2,500 rural enrollees simplifies KYC and instant policy issuance. Scalable commissions keep agents active in remote posts, while mobile penetration of 42% provides a ready platform for policy alerts and claims filing. Regulatory sandboxes let carriers test parametric models that pay via mobile wallets, a format suited to low-ticket risks and disaster compensation.

Growing Urban Middle Class and Formal Employment

GDP rebounded 4.3% in 2024 on Porgera mine reopening and LNG expansion, lifting disposable income in Port Moresby, Lae, and Mount Hagen. Skilled workers seek unit-linked contracts that combine protection with equity participation in resource-sector recovery. Urban customers favor riders for education funding, mortgage protection, and retirement planning aligned with aspirational lifestyles. Improved foreign-exchange liquidity lets insurers denominate certain policies in AUD or USD for expatriates. Nevertheless, commodity price swings and political instability can stall payroll growth, challenging premium persistency.

Strengthening Prudential & Solvency Supervision by BPNG

Draft Financial Consumer Protection legislation expands quarterly disclosure and establishes a complaints unit under the central bank, enhancing transparency and policyholder confidence[3]International Monetary Fund, “Papua New Guinea Financial Sector Stability Review 2024,” imf.org. Alignment with IAIS capital standards attracts reinsurers looking for robust governance. Quarterly financial inclusion reporting creates granular data that guides product design. Fintech sandboxes encourage pay-as-you-go covers piloted with telcos, while solvency monitoring dissuades under-capitalized entrants and supports consolidation among the five licensed life insurers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low financial literacy & limited awareness of insurance | -1.4% | National, most pronounced in rural areas | Long term (≥ 4 years) |

| Geographic dispersion and poor infrastructure drive costs | -1.1% | Remote provinces and island communities | Long term (≥ 4 years) |

| High communicable-disease mortality pushes premiums up | -0.8% | National, concentrated in urban informal settlements | Medium term (2-4 years) |

| Punitive taxation of non-resident insurers curbs reinsurance appetite | -0.6% | International reinsurance markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Financial Literacy & Limited Awareness of Insurance

Surveys cite “don’t know what insurance is” as the leading barrier, and traditional wantok systems reduce perceived need for formal cover[4]United Nations Development Programme, “Financial Inclusion Diagnostic for Papua New Guinea 2024,” undp.org. Traditional wantok systems, which emphasize communal support, further reduce the need for formal insurance coverage in the eyes of many. The absence of insurance-related topics in school curricula prevents knowledge about insurance from being passed down to younger generations. With over 600 islands, media campaigns struggle to reach all areas, limiting efforts to raise awareness. Additionally, only 36% of women use digital financial services, which widens the gap between genders in accessing financial tools. Community workshops conducted in Tok Pisin have shown positive results in educating people, but the high costs of scaling these workshops to cover 800 different languages make widespread implementation challenging.

Geographic Dispersion and Poor Infrastructure Drive Costs

Mountainous terrain and island chains raise distribution and claims-servicing expenses, inflating premiums for villagers who often need to travel by boat or plane to lodge claims. January 2024 civil unrest in Port Moresby disrupted logistics and highlighted the vulnerability of urban infrastructure. Climate events frequently cut off road and telecom links, delaying payouts and hurting customer trust. Partnerships with micro-banks and churches ease last-mile delivery but lack economies of scale needed for actuarial sustainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Investment-Oriented Policies Lead Customer Preference

Unit-linked contracts captured 37.85% of Papua New Guinea's life insurance market share in 2025 as resource-sector bonuses funneled into wealth-building vehicles. The segment benefits from transparent fund values and the prospect of capital appreciation tied to LNG and mining equities. Annuity business is projected to compound at 6.87% through 2031, favored by aging workers seeking guaranteed post-retirement income in the absence of state pensions. Whole-life remains relevant for conservative savers wanting definite death benefits, while term assurance attracts young families needing affordable mortgage risk cover. Endowment plans support education savings as private school enrollment rises. Hybrid covers that bundle outpatient health benefits broaden protection scope and help carriers defend margins in a competitive field.

Steady growth within unit-linked accounts underscores rising financial sophistication among urban professionals, and it boosts asset-management revenues for carriers with in-house fund arms. The annuity line, though still niche in absolute volume, gains momentum as superannuation members approaching 55 convert lump-sum withdrawals into life-contingent streams. Endowments and other blended products remain important for diversifying insurer balance sheets and catering to parents wary of tuition inflation. Collectively, the product mix shows a shift from pure protection to solutions combining protection and savings, a trend that sustains the broader Papua New Guinea life insurance market.

By Distribution Channel: Trusted Intermediaries Hold Sway

Agents generated 44.15% of premiums in 2025 because relationship-based selling aligns with communal culture and local-language needs. They guide paperwork, facilitate claims, and meet customers in markets or villages, cementing trust. Telco-hosted platforms, however, are set to grow 7.72% annually through 2031 as Digicel Financial Services cross-sells life covers through 1.1 million mobile money accounts. Banks, notably BSP, leverage branch footprints and payroll relationships to push bundled covers during loan origination. Brokers handle corporate risk portfolios, and direct digital sales remain low due to limited literacy, but offer potential for straight-through processing of micro policies.

The channel landscape will diversify as open-API frameworks allow insurers to plug products into ride-hailing or agri-e-commerce apps, widening reach without duplicative infrastructure. Yet, high agent productivity and cultural proximity suggest that face-to-face will keep primacy for complex products. The evolving mix underpins resilient premium inflows for carriers while enhancing consumer choice, sustaining overall expansion of the Papua New Guinea life insurance market.

By Premium Type: Regular Payments Dominate Household Budgets

In 2025, regular-premium contracts made up 71.05% of written premiums, mirroring the salary cycles of both government and corporate employees. Monthly deductions not only ensure persistency but also create a steady cash flow for policyholders and insurers alike. These contracts are particularly appealing to salaried individuals, as they align with their income patterns and provide a manageable way to maintain insurance coverage. The single-premium segment is projected to grow annually by 7.29%. This growth is fueled by mine dividends, remittances, and land lease windfalls, which are driving lump-sum investments, especially in savings plans linked to the diaspora. Such plans cater to individuals seeking to maximize returns on one-time financial windfalls while securing their financial future.

Periodic payments are gaining traction, highlighting the need for affordability in a nation where merely 15% of adults possess formal bank accounts. These payment structures make insurance accessible to a broader demographic, particularly those with limited financial resources. For insurers, these predictable inflows pave the way for investments in long-dated government bonds and real estate, aligning with their liability profiles. Such investments ensure financial stability and contribute to the development of the broader economy. While spikes in single-premium business are infrequent, they present prime opportunities for asset accumulation and diversification of liquidity sources for insurers. These lump-sum payments allow insurers to strengthen their financial position and explore new investment avenues. Collectively, these two structures not only complement each other but also showcase the evolving customer stratification within Papua New Guinea's life insurance landscape. The coexistence of regular and single-premium contracts reflects the diverse financial needs and capabilities of the population, enabling insurers to cater to a wide range of customers effectively.

By Customer Age Group: Working-Age Adults Sustain Momentum

In 2025, individuals aged 25-44, who often finance households, mortgages, and schooling, represented 48.75% of insurance premiums. This group tends to favor term and unit-linked covers, often opting for added loan protection or education riders. Their preference for such policies is driven by the need to secure their financial obligations and provide stability for their families. Additionally, insurers are increasingly targeting this demographic with tailored products and digital platforms to enhance accessibility and convenience. Meanwhile, the 45-64 age bracket is set to expand at a rate of 6.56% annually. This growth is primarily attributed to automatic group-life enrollment through superannuation schemes and a growing emphasis on retirement planning. As this cohort approaches retirement, their demand for life insurance products that offer long-term financial security is expected to rise. Insurers are responding by introducing flexible policies and retirement-focused riders to cater to this segment's evolving needs.

Younger adults below 25 remain underserved due to limited disposable income. However, student micro-covers priced at K1 per month are emerging as a promising solution to address this gap. These affordable policies are designed to provide basic coverage while fostering early adoption of insurance among the youth. Insurers are also leveraging digital channels and educational campaigns to raise awareness and drive penetration in this segment. Seniors over 65 face challenges related to affordability and underwriting requirements. Despite these hurdles, improving life expectancy is expected to drive demand for simplified-issue covers, which offer easier access and reduced complexity. Insurers are exploring innovative product designs and partnerships to better serve this demographic, ensuring that their needs are met without compromising affordability. Age segmentation highlights a market poised for expansion as literacy rates, digital access, and retirement awareness continue to improve. These factors are expected to support the sustained growth of the Papua New Guinea life insurance market, creating opportunities for insurers to develop targeted strategies and capture untapped potential across various age groups.

Geography Analysis

In Port Moresby, Lae, and Mount Hagen, premium generation thrives, bolstered by a confluence of formal employment, bank branches, and agent density. These urban centers serve as the primary hubs for life insurance activities, driven by higher disposable incomes and a growing awareness of financial protection. Resource projects and public-sector payrolls in the National Capital District and Morobe Province create a consistent demand for group schemes, further strengthening the market. Meanwhile, secondary centers like Madang, Kokopo, and Wewak are witnessing a surge in uptake due to the expansion of mobile agents and micro-bank kiosks. These developments are enlarging the Papua New Guinea life insurance market size by reaching previously underserved areas and fostering financial inclusion.

Coastal provinces face significant cyclone and flood risks, which heighten the need for protection products. Parametric micro-covers, piloted under the 2024 UNCDF-Lloyd’s Global Disaster Resilience Vehicle, offer swift payouts through mobile wallets, enhancing resilience in regions such as East New Britain, Milne Bay, and Bougainville. These innovative solutions address the unique challenges posed by climate risks, ensuring faster recovery for affected communities. Additionally, the Pacific Insurance and Climate Adaptation Programme is conducting feasibility studies to develop more climate-linked life insurance products. These products are expected to leverage telecommunications channels for distribution, further expanding market penetration and accessibility.

Highland provinces face challenges with road access, which limits traditional distribution channels. However, resource enclaves like Porgera and Hela generate high-income workers who demand sophisticated insurance products. EU-supported Women’s Micro Bank outlets demonstrate the viability of agent-assisted banking in regions like East Sepik and Sandaun. These outlets are paving the way for bundled life-and-savings plans, which cater to the specific needs of local populations. Geography-specific strategies, such as combining digital payments, community agents, and disaster parametrics, are expected to drive future growth in the Papua New Guinea life insurance market. These tailored approaches ensure that the market continues to evolve and adapt to the diverse needs of the country’s population.

Competitive Landscape

Five licensed carriers once vied for dominance, but with Workers Mutual Insurance now liquidated, only four remain, underscoring a moderate market concentration. Leveraging its parent bank's clout, BSP Life launched in 2018, swiftly securing payroll deduction deals with corporate clients. The company has since expanded its product portfolio to include tailored life insurance solutions for small and medium enterprises (SMEs), further strengthening its market position. Capital Life, with its bancassurance alliances and investment-linked offerings, appeals to urban professionals. It has also introduced flexible premium payment options to attract younger demographics and first-time policyholders. Niugini Lifecare, in collaboration with telecoms, delves into micro-insurance, targeting underserved rural populations with affordable and accessible coverage. Additionally, the company has partnered with community organizations to enhance financial literacy and promote insurance awareness.

Pacific MMI, bolstered by ties to the regional Pacific group, works to maintain its premium volumes. The company has also diversified its product offerings to include niche insurance products, such as travel and expatriate insurance, catering to a broader customer base. Insurers are racing to digitize claims, employing chatbots fluent in Tok Pisin, and adopting mobile wallets for premium collections. Noteworthy strategies include BSP Life's introduction of a self-service policy portal in 2025, which aims to streamline customer interactions and improve policy management efficiency. Capital Life's acquisition of an analytics suite to enhance medical underwriting is expected to reduce claim processing times and improve risk assessment accuracy. Pacific MMI's collaboration with a global reinsurer for climate-centric covers positions the company to address emerging risks associated with climate change, such as natural disasters and extreme weather events.

While the Bank of Papua New Guinea promotes innovation via a sandbox initiative, it simultaneously imposes solvency thresholds, creating hurdles for new entrants. These thresholds ensure market stability but also limit competition, favoring established players. In summary, the life insurance landscape in Papua New Guinea is tilted in favor of established players, due to their capital strength, expansive distribution networks, and technological prowess. The market's evolution is driven by a combination of innovation, regulatory oversight, and strategic partnerships, which collectively shape its competitive dynamics.

Papua New Guinea Life Insurance Industry Leaders

BSP Life (PNG) Ltd

Capital Life Insurance Co Ltd

Life Insurance Corporation (PNG) Ltd

Pacific MMI Insurance Ltd

Kwila Insurance Corp Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Securities Commission introduced an Investment Scam Alert Reporting Form to curb fraud in financial markets.

- January 2025: The Internal Revenue Service suffered a cyberattack that disrupted core tax systems, spotlighting data-security gaps across financial ecosystems.

- October 2024: UNCDF and Lloyd’s launched the Global Disaster Resilience Vehicle, providing parametric cyclone, earthquake, tsunami, and flood cover in Papua New Guinea, Fiji, and Samoa.

- September 2024: Bank of Papua New Guinea Governor Elizabeth Genia championed fintech-driven micro-insurance and micro-pension solutions for the informal sector at a national roundtable co-hosted by UNCDF and industry bodies.

Papua New Guinea Life Insurance Market Report Scope

A complete background analysis of the Papua New Guinea Life and Annuity Insurance Market, which includes an assessment of the parental market, emerging trends by segments, significant changes in market dynamics and market overview, is covered in the report. The market is segmented by Insurance Type.

By Product Type (Value)

| Term Life Insurance |

| Whole Life Insurance |

| Endowment Insurance |

| Unit-Linked / Investment-Linked |

| Annuity Insurance |

| Other Types |

By Distribution Channel (Value)

| Agents |

| Brokers |

| Banks |

| Direct to Consumer |

| Online Marketplaces |

By Premium Type (Value)

| Regular Premium |

| Single Premium |

By Customer Age Group (Value)

| 0–24 Years |

| 25–44 Years |

| 45–64 Years |

| 65 Years & Above |

| By Product Type (Value) | Term Life Insurance |

| Whole Life Insurance | |

| Endowment Insurance | |

| Unit-Linked / Investment-Linked | |

| Annuity Insurance | |

| Other Types | |

| By Distribution Channel (Value) | Agents |

| Brokers | |

| Banks | |

| Direct to Consumer | |

| Online Marketplaces | |

| By Premium Type (Value) | Regular Premium |

| Single Premium | |

| By Customer Age Group (Value) | 0–24 Years |

| 25–44 Years | |

| 45–64 Years | |

| 65 Years & Above |

Key Questions Answered in the Report

How large is Papua New Guinea’s life insurance market in 2026?

It is valued at USD 672.9 million and is projected to climb to USD 899.64 million by 2031.

What is the expected growth rate through 2031?

The market is forecast to expand at a 5.98% CAGR during the forecast period (2026-2031), supported by superannuation mandates and mobile micro-insurance.

Which product category currently holds the largest share?

Unit-linked policies lead with 37.85% of written premiums due to middle-class demand for wealth accumulation.

Which distribution channel is growing fastest?

Online marketplaces tied to mobile money are rising at a 7.72% CAGR, though agents remain dominant.

What are the main challenges to wider insurance uptake?

Low financial literacy, high distribution costs in remote areas, and cybersecurity risks hinder broader penetration.

Who is the leading insurer?

BSP Life leverages its parent bank’s reach and bancassurance capabilities to command a significant share of group and retail business.

Page last updated on: