Leadless Cardiac Pacemaker Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

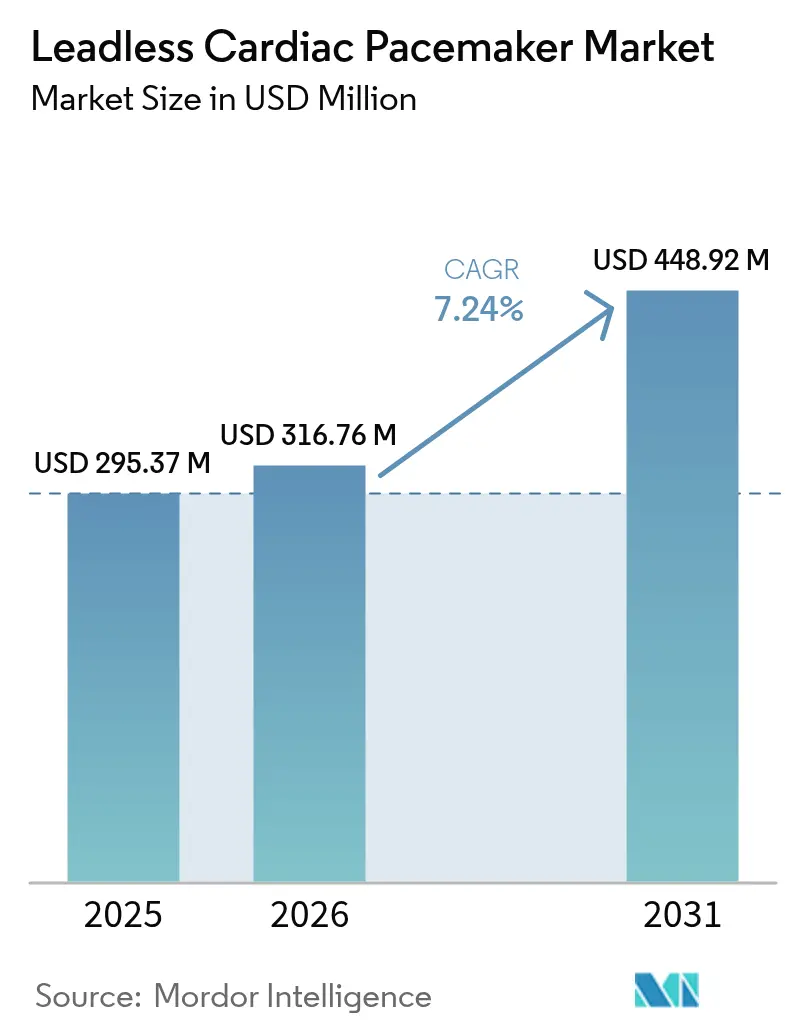

| Market Size (2026) | USD 316.76 Million |

| Market Size (2031) | USD 448.92 Million |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leadless Cardiac Pacemaker Market Analysis by Mordor Intelligence

The Leadless Cardiac Pacemaker Market size was valued at USD 295.37 million in 2025 and is estimated to grow from USD 316.76 million in 2026 to reach USD 448.92 million by 2031, at a CAGR of 7.24% during the forecast period (2026-2031).

Demand momentum rests on the rapid shift from single-chamber ventricular pacing toward dual-chamber and forthcoming conduction-system solutions that promise physiologic synchrony without transvenous leads. North American reimbursement clarity, expanding MRI-conditional labeling, and aging demographics continue to anchor volume growth. Competitive intensity is high because Abbott and Medtronic defend entrenched positions through differentiated technology and deep clinical trial pipelines, yet Boston Scientific’s modular platform illustrates how new architectures can disrupt the established order. Market opportunities widen in Asia-Pacific where streamlined approvals and hospital investments offset persistent pricing barriers.

Key Report Takeaways

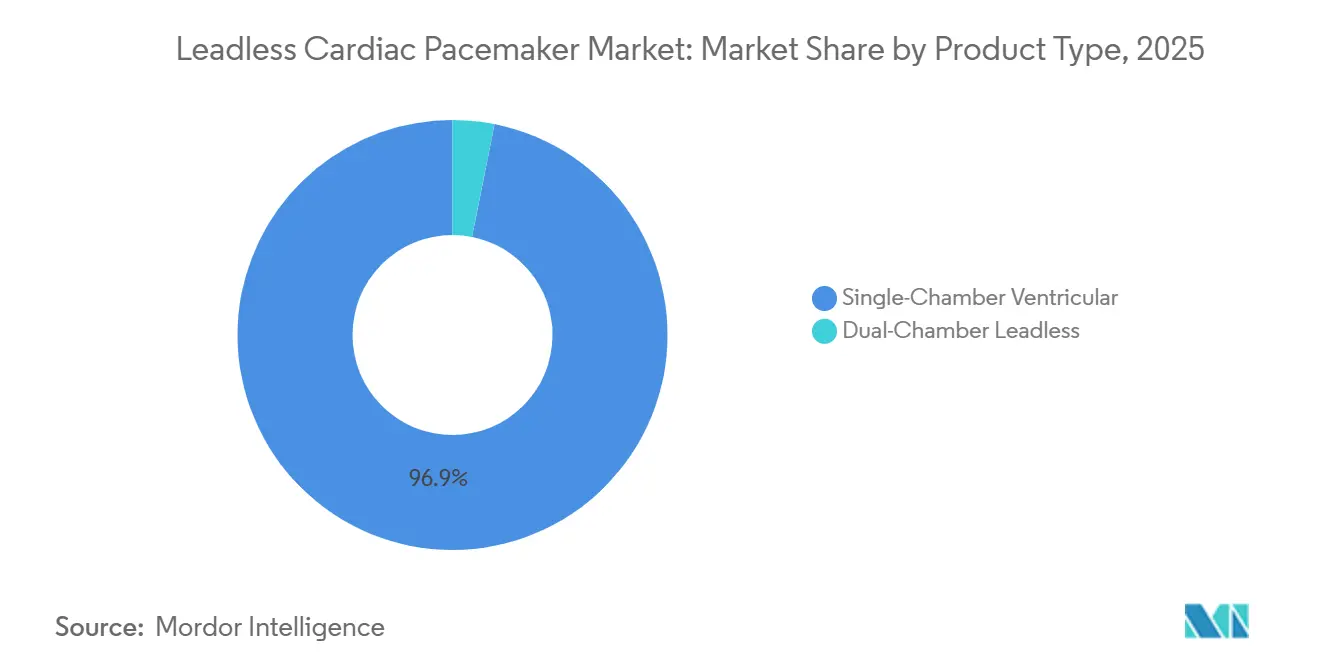

- By product type, single-chamber systems carried a 96.88% share of the leadless pacemaker market in 2025, while dual-chamber platforms are projected to expand at 7.82% CAGR to 2031.

- By indication, bradyarrhythmia accounted for 60.71% of the 2025 leadless pacemaker market size, whereas atrial fibrillation applications record the fastest trajectory at 8.09% CAGR through 2031 .

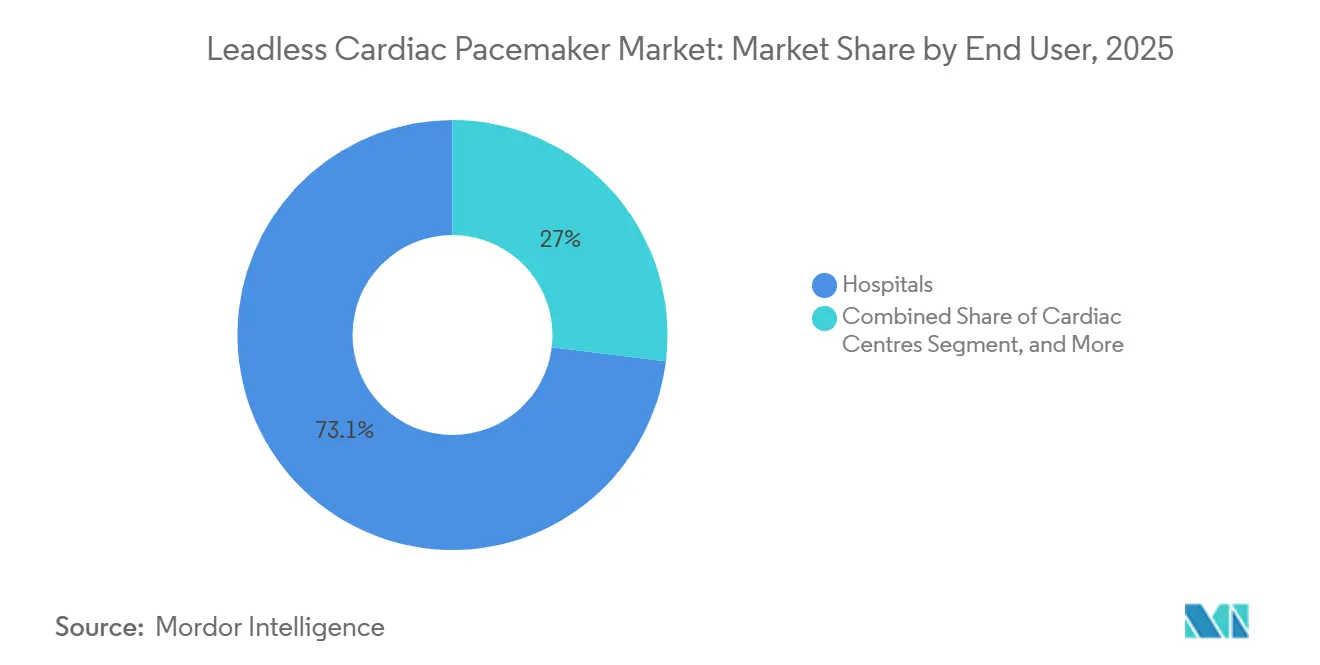

- By end user, hospitals held 73.05% of 2025 revenue yet cardiac centers exhibit the highest forecast CAGR at 8.23% through 2031.

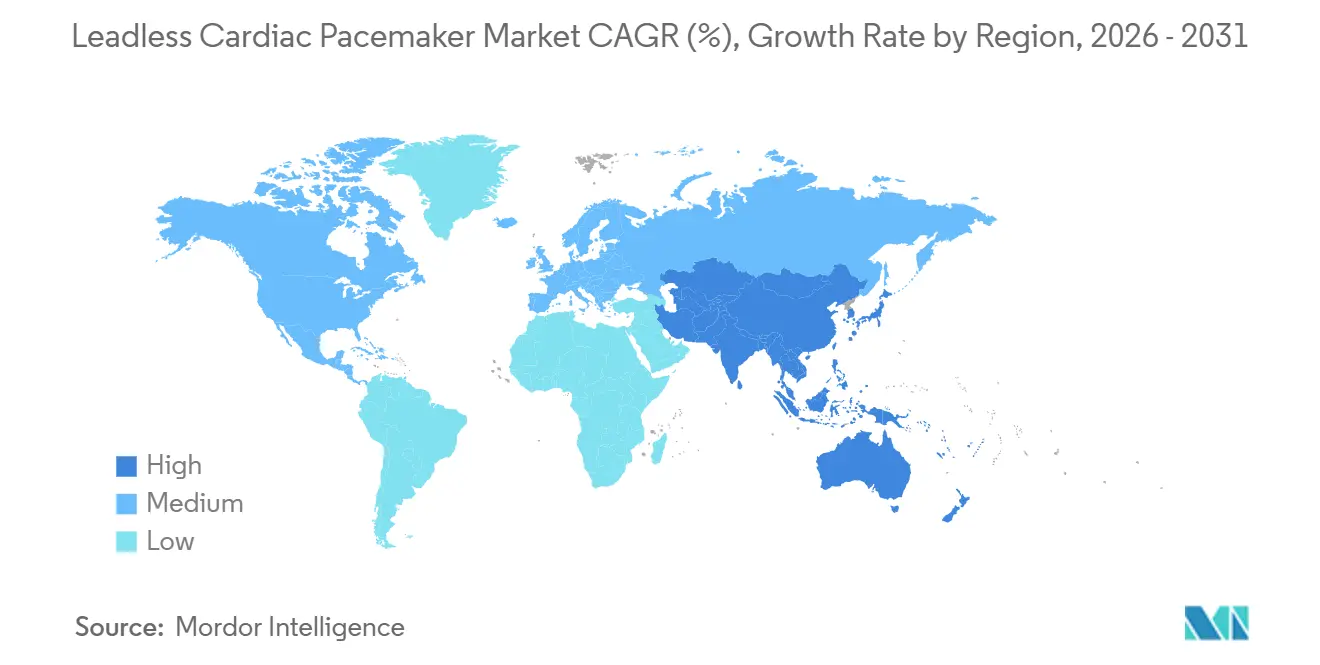

- By geography, North America maintained 41.88% leadless pacemaker market share in 2025, while Asia-Pacific is set to deliver a 8.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Leadless Cardiac Pacemaker Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapidly ageing population base | +1.8% | Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Superior safety profile versus trans-venous | +1.5% | Global, acute in high-infection markets | Medium term (2-4 years) |

| MRI-conditional labeling expanding cohorts | +1.2% | North America, Europe, Australia | Short term (≤ 2 years) |

| Day-case reimbursement models | +1.0% | United States, United Kingdom, Germany, Australia | Medium term (2-4 years) |

| Capitated-risk cardiac bundles | +0.9% | United States | Medium term (2-4 years) |

| Synergy with conduction-system pacing | +0.7% | North America, Western Europe, select Asia-Pacific centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Ageing Population Base

In 2024, the global population aged 65 and older surpassed 761 million, a figure projected to reach 1.6 billion by 2050.[1]World Health Organization, “Ageing and Health,” who.int Japan, with 29.1% of its residents aged 65 and above, reported a 14% increase in cardiac device implants from 2020 to 2024.[2]Ministry of Health, Labour and Welfare Japan, “Medical Fee Schedule 2024,” mhlw.go.jp Elderly patients frequently face venous stenosis, complicating the use of transvenous leads and making leadless options more appealing. In 2025, South Korea broadened its national reimbursement for leadless systems, resulting in a 40% reduction in hospital stays. Following suit, Germany introduced equal reimbursement for patients over 75, leading to a 22% increase in uptake at university centers.

Superior Safety Profile Versus Transvenous Leads

Registry evidence shows Micra recipients experienced 63% fewer major complications than comparable transvenous cohorts at five years. The abolition of leads and pockets effectively removes the principal nidus for device infection, an advantage magnified in dialysis and immunocompromised populations. Cardiac perforation risk remains salient at roughly 1.5% of cases, yet real-world data confirm overall safety parity with conventional systems once operator proficiency matures.

MRI-Conditional Labeling Expanding Eligible Cohort

In 2024, the FDA granted clearance for full-body 1.5 T and 3 T scanning for Micra AV2/VR2, eliminating a diagnostic hurdle for 50-75% of pacemaker recipients.[3]U.S. Food and Drug Administration, “Pacemakers – Cardiovascular Devices,” fda.gov Following this, ESC imaging guidelines shifted to endorse leadless options, particularly for oncology and neurology patients who may require an MRI. In 2025, the CE-marked Aveir DR received similar labeling, distinguishing it from dual-chamber devices. An August 2025 Europace registry reported a 12-15 point improvement in quality-of-life scores on the SF-36 following label expansion.

Capitated-Risk Cardiac Bundles in U.S. Health Systems

In 2024, BPCI-Advanced incorporated cardiac devices, linking 90-day costs directly to patient outcomes. By replacing traditional units with leadless ones, networks reduced total episode spending by 12-16%, successfully avoiding lead-related complications. Meanwhile, Kaiser Permanente, under its bundled protocol, increased the adoption of leadless devices by 28% through 2025, achieving a notable 19% reduction in 90-day costs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Device Price in Cost-Sensitive Regions | -1.3% | Asia-Pacific (ex-Japan/Australia), Latin America, Middle East & Africa | Medium term (2-4 years) |

| Limited Retrieval / Battery Exchange | -0.9% | Global, pronounced where long device life is critical | Long term (≥ 4 years) |

| Electrophysiologist Training Gap | -0.8% | India, Southeast Asia, Latin America, Sub-Saharan Africa | Medium term (2-4 years) |

| Lithium-Cell Supply-Chain Volatility | -0.6% | Global, manufacturing centered in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Price in Cost-Sensitive Regions

List prices exceed USD 15,000 for transvenous systems, while those below USD 5,000 are priced below GDP growth, constraining uptake where reimbursement lags GDP growth. Economic analyses place cost-effectiveness thresholds at AUD 47,379 per QALY in Australia, an acceptable range for mature markets but a hurdle for emerging payers. Specialized training and imaging overhead further inflate total procedural cost in low-resource settings.

Limited Retrieval / Battery-Exchange Protocols

Percutaneous retrieval success wanes with implant duration as endothelialization deepens, creating uncertainty for younger individuals expected to outlive first-generation battery cycles. Coexistence of multiple intracardiac capsules raises thrombogenicity questions, and guidelines lack consensus on chronic explant timing. Dual-chamber upgrades compound the dilemma because atrial modules must be anchored alongside ventricular devices, making future extraction more complex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-Chamber Systems Gain Despite Technical Hurdles

2025 data show the leadless pacemaker market size for single-chamber systems at 96.88% share, yet dual-chamber devices exhibit an 7.82% CAGR outlook through 2031 as Abbott’s AVEIR DR secures 98.1% atrioventricular synchrony in trials. Single-chamber models remain clinically indispensable for permanent atrial fibrillation and end-of-life scenarios where procedural simplicity overrides physiologic pacing benefits.

Continued miniaturization and implant-to-implant communication propel dual-chamber platforms toward standard of care, elevating revenue mix toward premium-priced configurations. Manufacturers also explore conduction-system pacing capsules that deliver native bundle activation without transvenous leads, a step anticipated to compress heart-failure admissions linked with RV septal pacing. Patent landscaping indicates more than 25 active filings covering wireless energy transfer and retrieval tooling, underscoring sustained R&D investment.

By Indication: Bradyarrhythmia Core Expands into Atrial Fibrillation

Bradyarrhythmia dominated the 2025 leadless pacemaker market share at 60.71%, serving sinus node dysfunction and atrioventricular block cohorts where infection prevention carries high clinical value. Atrial fibrillation pacing needs, once constrained by single-chamber limitations, now grow at 8.09% CAGR to 2031 as dual-chamber solutions re-establish AV synchrony.

Post-cardiac surgery conduction disease and TAVR-related AV block further diversify the indication canvas. Real-world evidence files document safe deployment in congenital and post-ablation scenarios, although diversity in anatomy demands individualized implant planning.

By End User: Specialized Cardiac Centers Gain Momentum

Hospitals accounted for 73.05% of 2025 revenue, driven by integrated surgical backup and reimbursement familiarity, yet cardiac centers generate the top-line growth at 8.23% CAGR by concentrating procedural volume and electrophysiology talent.

Dedicated centers cut fluoroscopy times through experienced operators, support day-case pathways to unlock payer savings, and embed rigorous post-implant surveillance. Ambulatory surgical centers enter select U.S. markets on the back of catheter-based techniques, though adoption scales slowly because device retrieval capabilities and rapid surgical conversion are regulatory prerequisites.

Geography Analysis

North America led with 41.88% share in 2025 on the strength of Medicare Coverage with Evidence Development that reimburses while capturing outcomes data. Hospital networks integrate leadless pacemakers into value-based bundles that reward reduced infection readmissions.

Europe sustains robust volume through CE-marked evidence programs and pan-regional registries that refine practice guidelines, although MDR compliance adds incremental certification cost. Asia-Pacific posts the fastest 8.74% CAGR as India cleared AVEIR VR in 2024 and major Chinese centers ramp local clinical trials to support National Reimbursement Drug List petitions. Rising middle-class coverage and infrastructure builds accelerate procedure counts despite lingering affordability challenges.

Latin America and Middle East & Africa remain opportunity pockets where private insurance penetration and public tender cycles dictate slower diffusion trajectories.

Competitive Landscape

Abbott and Medtronic dominate with cumulative majority share, reflecting deep patent estates, long-running registry datasets, and captive delivery tool ecosystems. Abbott leverages i2i communication to offer true dual-chamber pacing, while Medtronic’s accelerometer-based AV algorithm sustains broad U.S. payer coverage. Boston Scientific’s Empower MPS aims to integrate subcutaneous ICD therapy with leadless pacing, a modular concept that could expand addressable arrhythmia indications and pressure incumbent pricing.

Emerging entrants such as EBR Systems pursue wireless left-ventricular pacing capsules, and Chinese firms Lepu Medical and MicroPort seek domestic volume advantage. Strategic moves pivot on securing breakthrough designations, executing multicenter trials, and negotiating DRG-aligned reimbursement that balances premium device cost with infection avoidance savings.

Leadless Cardiac Pacemaker Industry Leaders

Abbott Laboratories

Medtronic PLC

EBR Systems Inc.

Boston Scientific Corporation

MicroPort Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BIOTRONIK has kicked off a global pivotal study to assess its LivIQ leadless pacemaker system. This state-of-the-art device aims to provide atrioventricular (AV) synchrony, leveraging cutting-edge electrical far-field sensing technology.

- January 2026: Biotronik performed first-in-human LivIQ leadless pacemaker implants under the BIO|CONCEPT.LivIQ study in Australia.

- October 2025: Abbott introduced Aveir DR in India at INR 1,450,000 and partnered with AIIMS Delhi, Apollo Hospitals, and Fortis Healthcare for training.

Global Leadless Cardiac Pacemaker Market Report Scope

As per the scope of this report, a leadless cardiac pacemaker is a small, self-contained electrode system and generator that is implanted in the right ventricle. The device is placed via a femoral vein transcatheter technique.

The leadless cardiac pacemaker market is segmented by product type, indication, end user, and geography. By product type, the market is segmented into single-chamber ventricular leadless pacemakers and dual-chamber leadless pacemakers. By indication, the market is segmented into bradyarrhythmia, atrioventricular block, atrial fibrillation, and other indications. By end user, the market is segmented into hospitals, cardiac centers, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Single-Chamber Ventricular Leadless Pacemaker |

| Dual-Chamber Leadless Pacemaker |

| Bradyarrhythmia |

| Atrioventricular Block |

| Atrial Fibrillation |

| Others |

| Hospitals |

| Cardiac Centres |

| Ambulatory Surgical Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-Chamber Ventricular Leadless Pacemaker | |

| Dual-Chamber Leadless Pacemaker | ||

| By Indication | Bradyarrhythmia | |

| Atrioventricular Block | ||

| Atrial Fibrillation | ||

| Others | ||

| By End User | Hospitals | |

| Cardiac Centres | ||

| Ambulatory Surgical Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the leadless pacemaker market in 2026?

The market stands at USD 316.76 million and is projected to reach USD 448.92 million by 2031 at a 7.24% CAGR.

Which product type is growing fastest?

Dual-chamber leadless systems deliver the highest growth at 7.82% CAGR through 2031 due to superior AV synchrony.

What clinical advantage drives adoption?

Eliminating transvenous leads lowers major complication risk by 63% compared with conventional pacemakers.

Which region shows the strongest growth outlook?

Asia-Pacific records a 8.74% CAGR owing to streamlined approvals and expanding electrophysiology capacity.

What is the core pricing challenge?

Device costs above USD 15,000 remain a barrier in cost-sensitive markets where transvenous systems are far cheaper.

How long is current battery longevity?

First-generation devices show a projected median battery life of 6.8 years based on five-year follow-up data.

Page last updated on: