Land Drilling Rig Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 62.03 Billion |

| Market Size (2031) | USD 63.38 Billion |

| Growth Rate (2026 - 2031) | 0.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Land Drilling Rig Market Analysis by Mordor Intelligence

The Land Drilling Rig Market size is estimated at USD 62.03 billion in 2026, and is expected to reach USD 63.38 billion by 2031, at a CAGR of 0.43% during the forecast period (2026-2031).

Demand stability masks an ongoing shift toward super-spec technology, stricter emissions rules, and divergent regional capital-spending patterns that collectively reshape contractor economics. North American operators continue to retire legacy mechanical fleets in favor of high-horsepower AC rigs that shorten spud-to-TD cycles and cut fuel burn, while Middle Eastern national oil companies (NOCs) expand government-backed fleets to secure unconventional gas supply. Corporate net-zero targets are nudging dayrate premiums for rigs equipped with dual-fuel engines, selective catalytic reduction, and automated pipe-handling systems. Meanwhile, geothermal and natural-hydrogen pilot wells are opening nascent but fast-growing avenues for land drilling contractors willing to tailor equipment to corrosive fluids and hard-rock environments. Competitive intensity remains pronounced as super-spec supply is concentrated among a handful of North American contractors, yet regional fragmentation persists where NOCs favor domestic providers.

Key Report Takeaways

- By rig type, mobile and wheel-mounted platforms captured 40.8% of 2025 revenue, whereas walking super-spec rigs are advancing at a 0.8% CAGR through 2031.

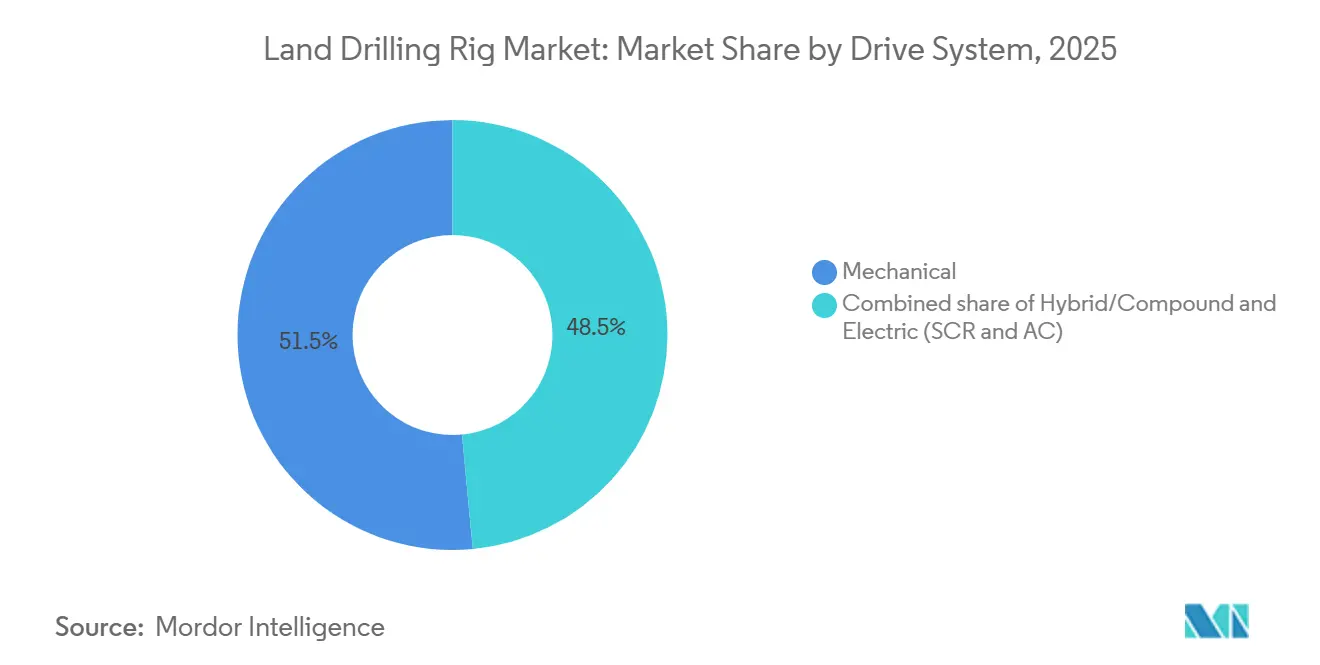

- By drive system, mechanical rigs held 51.5% of the 2025 value, while electric SCR and AC architectures are posting the segment’s fastest 0.7% CAGR as emissions scrutiny intensifies.

- By horsepower, 1,000-1,499 HP units accounted for 60.7% of deployments in 2025; however, rigs above 1,500 HP lead growth with a 1.0% CAGR on the strength of deeper Permian and Middle Eastern wells.

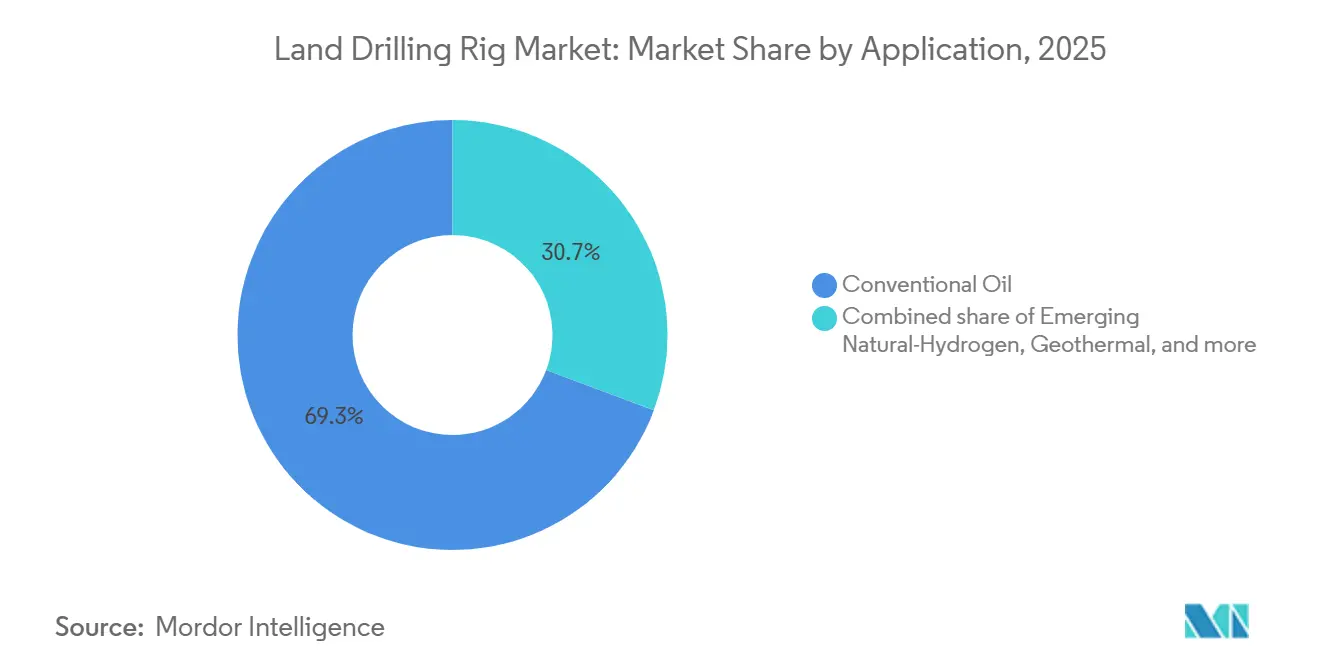

- By application, conventional oil drilling maintained 69.3% of 2025 activity, yet natural-hydrogen programs are rising at a 15.5% CAGR from a small base.

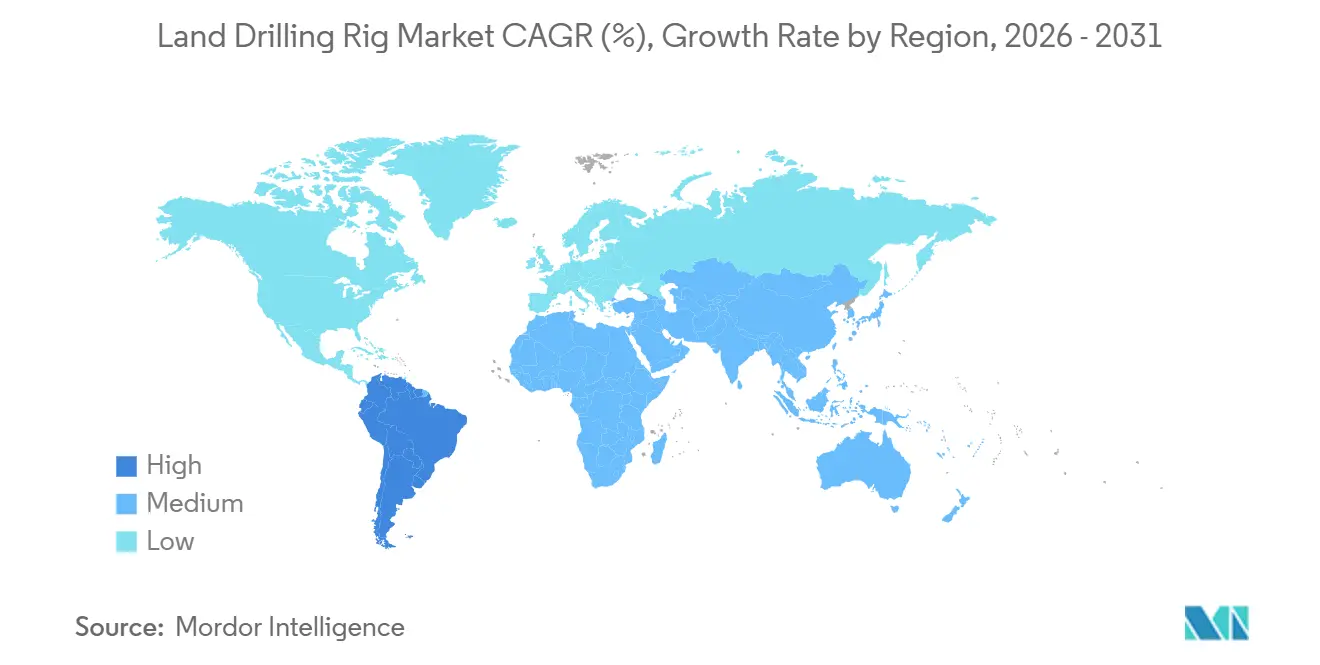

- By geography, North America generated 49.9% of the 2025 market value, but Asia-Pacific is the fastest-growing region at a 1.3% CAGR, fueled by India’s geothermal push and Australia’s tight-gas projects.

- The five largest contractors, Nabors Industries, Helmerich & Payne, Patterson-UTI Energy, Precision Drilling, and ADNOC Drilling, collectively controlled roughly 45% of global active rigs in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Land Drilling Rig Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ≥1,500 HP super-spec adoption | +0.20% | North America, Middle East | Medium term (2-4 years) |

| Shale and other unconventional reserves | +0.10% | North America, Argentina, Australia | Long term (≥ 4 years) |

| Revival of MENA onshore CAPEX | +0.15% | Middle East, North Africa | Short term (≤ 2 years) |

| Low-emission gas/LNG-powered rig engines | +0.05% | Global, early adoption in North America | Medium term (2-4 years) |

| Fully automated digital rigs | +0.10% | North America, Middle East, Asia-Pacific | Medium term (2-4 years) |

| Geothermal & natural-hydrogen programs | +0.08% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

≥1,500 HP super-spec adoption

Super-spec platforms above 1,500 HP now dominate complex unconventionals, enabling laterals beyond 15,000 feet and trimming total-depth times by up to 30% versus legacy units.[1]Helmerich & Payne, “Q4 2024 Earnings Call,” helmerichpayne.com FlexRig fleets in the United States logged average day rates of USD 28,500 in 2025, a USD 3,000 premium justified by 7,500-psi pumps and 750-ton top drives. About 60% of U.S. deployments went to the Permian Basin, where deeper Wolfcamp zones require higher torque. ADNOC Drilling mirrored the trend, adding 12 super-spec rigs for the high-pressure Jafurah gas play. High upfront capex, often above USD 25 million per rig, continues to limit ownership to well-capitalized operators.

Shale and other unconventional reserves

Unconventional drilling has switched from appraisal to factory mode, reinforcing baseline demand for the land drilling rigs market.[2]International Energy Agency, “World Energy Investment 2025,” iea.org Argentina’s Vaca Muerta delivered 500,000 barrels per day by late 2025, up 56% in two years, as YPF and partners drilled deeper liquids-rich sections using 1,200-1,500 HP rigs. The United States still accounted for 40% of global unconventional activity, benefiting from takeaway capacity and pro-drilling infrastructure. Australia is emerging as a tight-gas frontier, where Santos is deploying automated rigs in the Cooper Basin to curb labor exposure. Regulatory incentives such as Argentina’s RIGI tax-stability regime are accelerating foreign participation, whereas U.S. federal lease issuance faces legal headwinds.

Revival of MENA onshore CAPEX

Middle Eastern NOCs scheduled USD 130 billion in upstream spend through 2026, dedicating roughly one-third to onshore drilling. Saudi Aramco alone committed USD 7 billion to Jafurah gas, deploying high-spec rigs built for 10,000-psi reservoirs.[3]Saudi Aramco, “Annual Review 2024,” aramco.com ADNOC Drilling grew its fleet to 118 units in 2024 and secured multiyear contracts in the Rub’ al Khali, where ambient desert heat demands enhanced cooling systems. Kuwait’s 5-year Burgan contract with KCA Deutag embedded performance clauses tied to rate-of-penetration metrics. Low breakeven prices below USD 30 per barrel help shield the region from oil-price volatility.

Low-emission gas/LNG-powered rig engines

Dual-fuel and field-gas powertrains are gaining momentum as methane regulations tighten. Caterpillar shipped 85 Tier 4 Final engines to North American contractors in 2025.[4]Caterpillar, “Investor Day 2024,” caterpillar.com Permian operators slash daily fuel costs by USD 1,500-2,000 when substituting flared gas for diesel, cutting flaring volumes by 20%. Nabors retrofitted 12 rigs for seamless diesel-gas switching, while pilot LNG-powered units entered service in Argentina and Australia to address remote-fuel logistics. Upcoming U.S. methane rules create further incentives, though enforcement timelines remain subject to litigation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shift to renewables | -0.15% | Global, pronounced in Europe and North America | Long term (≥ 4 years) |

| Oil-price volatility & capital discipline | -0.12% | Global, most acute in North America | Short term (≤ 2 years) |

| ESG financing & insurance hurdles | -0.08% | North America, Europe | Medium term (2-4 years) |

| Expanding no-drill buffer zones | -0.05% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global shift to renewables

Renewables attracted USD 623 billion in investment during 2024, overtaking upstream hydrocarbon spend for a third straight year. The IEA’s Net-Zero scenario sees oil demand peaking in 2025 and sliding 25% by 2035, implying structural pressure on drilling programs. TotalEnergies now directs 40% of its capex toward power and renewables, retreating from North Sea wildcats. Investor activism deepened in 2024 as BlackRock and Vanguard voted against drilling expansions, citing climate risk. Middle Eastern NOCs remain insulated, but North American independents are repurposing rigs toward geothermal, where commercial scale is still years away.

Oil-price volatility & capital discipline

WTI traded between USD 70 and USD 85 during 2024-2025, levels that fund maintenance drilling yet seldom justify fleet additions. Mega-mergers, including ExxonMobil-Pioneer, prioritize inventory depth over incremental rigs, signaling a strategic shift to manufacturing efficiency. U.S. Lower 48 rig counts slipped to 588 in late 2025 even as production rose 3%, evidencing productivity-led growth. Companies such as ConocoPhillips returned USD 14 billion to shareholders in 2024, diverting cash from exploration. Declining drilled-but-uncompleted (DUC) inventories underscore the new capital-discipline paradigm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rig Type: Mobility Versus Automation Economics

Walking super-spec rigs lifted the land drilling rigs market share for high-tech platforms by adding 0.8% CAGR, even though mobile and wheel-mounted units still generated 40.8% of 2025 revenue. Walking systems cut move times from three days to eight hours, saving up to USD 200,000 per relocation and boosting pad-drilling economics. These benefits appeal most to Permian operators completing 6-12 wells per pad. Capital intensity above USD 28 million per unit limits their spread in emerging regions, where dayrate premiums must offset financing costs.

At the other end, conventional truck-mounted fleets persist in Argentina, Colombia, and parts of Africa, where dispersed wells, shallow targets, and lower safety standards favor minimal capex. California’s new Tier 4 engine rules effectively ban diesel-only mechanical rigs for new programs, accelerating retirements in the San Joaquin Basin. The Middle East is importing the walking concept; ADNOC moved four units into Jafurah in 2024, validating international demand beyond North America. As super-spec supply tightens, contractors with mixed fleets retain pricing power in conventional work.

By Drive System: Electric Transition Accelerates

Mechanical rigs represented 51.5% of the 2025 land drilling rigs market size, but electric SCR and AC drives are expanding at a 0.7% clip under regulatory and fuel-savings pressure. Electric platforms cut diesel usage by roughly 15% per foot drilled, translating to USD 2,000-3,000 in daily savings at current fuel prices. They also enable regenerative braking during tripping, lowering operating costs further.

Adoption patterns vary by geography. Canada, with challenging winters and shorter drilling windows, is converting slowly; only 55% of Precision Drilling’s 181-rig fleet is electric. China still runs 70% mechanical rigs, though COSL has pilots underway in the Tarim Basin to meet PetroChina methane goals. Lifecycle economics favor full electrification because maintenance expenses fall 18-22% thanks to fewer moving parts, according to an SPE 2024 study. Hybrid diesel-electric setups are bridging the gap where grid or field gas is patchy.

By Horsepower Rating: Super-Spec Premium Persists

Rigs in the 1,000-1,499 HP window captured 60.7% of the 2025 land drilling rigs market share, servicing mid-depth horizontals across global shale and tight-oil plays. Yet units exceeding 1,500 HP are rising fastest, growing at 1.0% CAGR as deeper laterals and higher mud weights become common in Wolfcamp, Bone Spring, and Jafurah wells. Nabors achieved USD 32,000-35,000 day rates for high-HP rigs in 2025, a USD 6,000-8,000 uplift over mid-range machines.

Sub-1,000 HP rigs are sliding toward workover niches as horizontal drilling becomes the norm. The super-spec segment’s USD 25-30 million build cost deters speculative orders, sustaining supply tightness even when overall market growth is sluggish. Geothermal pilots such as Fervo’s Nevada project, which used 1,500 HP rigs to punch through 4,000-meter granite, illustrate crossover demand that further supports premium day rates.

By Application: Hydrogen Disrupts Conventional Dominance

Conventional oil maintained 69.3% of the 2025 land drilling rigs market size, underpinning mature fields in the Middle East and the Americas. Unconventional shale and tight plays added nearly 25% of volume, but the stand-out growth story is natural-hydrogen drilling, advancing at 15.5% CAGR from a tiny base. HyTerra’s Kansas wells measured 96% H₂, prompting a USD 25 million appraisal program that could create the first commercial hydrogen wells in North America.

Geothermal remains secondary but rising; enhanced systems and closed-loop concepts together accounted for fewer than 1% of wells in 2025, yet planned licensing in India and Australia hints at a larger 2030 opportunity. Conventional oil’s share is forecast to ease toward 65% by 2031 as hydrogen and geothermal scale, although absolute barrel replacement needs keep the segment numerically large.

Geography Analysis

North America produced 49.9% of the 2025 value and is forecast at a modest 0.4% CAGR to 2031. Rig counts eased to 588 in late 2025, but output still climbed 3% thanks to longer laterals and faster cycle times. ExxonMobil’s USD 60 billion Pioneer acquisition unlocked larger contiguous pads, enhancing capital efficiency. Canada’s seasonal fleet reached 181 rigs, yet spring breakup still sidelines equipment for up to two months each year, tempering utilization swings. Natural-hydrogen spuds in Kansas and Colorado, plus geothermal wells in Nevada, provide emerging diversification, though volumes remain modest relative to oil.

The Middle East and Africa posted the steadiest outlook with a 0.6% CAGR, aided by state funding and sub-USD 30 breakevens. ADNOC Drilling scaled to 118 rigs, entering Kuwait and Saudi Arabia under multiyear contracts backed by performance tariffs. Saudi Aramco’s USD 7 billion onshore program targets 200 TCF of Jafurah gas, requiring high-torque rigs tailored for 10,000-psi formations. Libya plans 20 land rigs to restore 1.5 million barrels per day, although progress depends on political stability. Algeria’s 120-well plan for 2026 signals renewed Saharan gas drilling after years of underinvestment.

Asia-Pacific is the fastest-growing region at 1.3% CAGR, yet from a smaller base. India issued 13 geothermal blocks targeting the Cambay and Godavari basins with temperatures above 200 °C. Australia’s Cooper Basin tight-gas projects employ automated rigs to mitigate labor scarcity. Indonesia’s frontier exploration faces permitting delays, while China’s COSL trials electric rigs in the Tarim Basin as part of methane-cutting goals. South America’s 0.5% CAGR hinges on Vaca Muerta, whose 500,000 barrels per day output lifted regional demand despite Brazil focusing offshore. Europe remains constrained by fracturing bans, though Turkey and Romania sustain modest drilling in mature onshore licenses.

Competitive Landscape

Moderate concentration characterizes the land drilling rigs market, with the top five players controlling roughly 45% of active rigs. Patterson-UTI’s merger with NexTier in November 2024 created the second-largest North American land driller, combining 370 rigs and 300,000 hydraulic horsepower, and retiring 40 aging units to tighten super-spec supply. Helmerich & Payne maintains a homogeneous 219-rig FlexRig fleet that lowers training and maintenance spend by 10-15% versus mixed fleets, underpinning consistently high utilization. Nabors increasingly monetizes its SmartROS automation platform, booking USD 45 million in 2024 software revenue as it licenses technology to third-party contractors.

White-space opportunities emerge in geothermal, where Fervo’s 400-well Nevada project showcased scalability using conventional rigs, pointing to a USD 2-3 billion addressable segment by 2030 if additional capacity materializes. ADNOC Drilling earmarked USD 1.5 billion for 20 new super-spec rigs destined for Saudi Arabia and Iraq, signaling that regional consolidation could mirror North America’s scale economics. Smaller U.S. contractors pivot either to shallow workover services or exit entirely as super-spec capex hurdles mount. Technology adoption remains the main differentiator: rigs with automation and Tier 4 dual-fuel engines command USD 3,000-5,000 dayrate premiums, while mechanical fleets face erosion under tightening emissions regimes.

Land Drilling Rig Industry Leaders

Nabors Industries

Helmerich & Payne

Patterson-UTI

Precision Drilling

China Oilfield Services (COSL)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Helmerich & Payne signed a three-year deal with ExxonMobil for 25 FlexRigs in the Delaware Basin at USD 30,000 day rates plus performance bonuses.

- May 2025: ADNOC Drilling unveiled a USD 1.5 billion program to add 20 super-spec rigs by 2026 for the Jafurah and Rumaila projects.

- November 2024: HyTerra confirmed 96% hydrogen in Kansas basement wells, triggering a USD 25 million, 10-well appraisal campaign.

- February 2024: Nabors Industries launched SmartROS Edge and licensed it to three contractors for 18 Middle East and Latin America rigs, securing USD 12 million in upfront software revenue.

Global Land Drilling Rig Market Report Scope

A drilling rig is machinery used to drill a wellbore. The mud tanks and pumps, the derrick, the draw works, the rotary table, the drill string, the power generation equipment, and the auxiliary equipment are all a drilling rig.

The land drilling rig market is segmented by rig type, drive system, horsepower rating, application, and geography. By rig type, the market is segmented into conventional, mobile, and walking super-spec. The market is segmented by drive system into mechanical, electric SCR, and compound. By horsepower rating, the market is segmented into Up to 1,000 HP, 1,000 to 1,499 HP, and Above 1,500 HP. By application, the market is divided among conventional oil, unconventional/tight and shale, geothermal, and emerging natural hydrogen. The report also covers the market size and forecasts for the land drilling rig market across major regions. The market sizing and forecasts have been done for each segment based on revenue (USD).

| Conventional |

| Mobile/Wheel-Mounted |

| Walking Super-Spec |

| Mechanical |

| Electric (SCR and AC) |

| Hybrid/Compound |

| Up to 1,000 HP |

| 1,000 to 1,499 HP |

| Above 1,500 HP |

| Conventional Oil |

| Unconventional/Tight and Shale |

| Geothermal |

| Emerging Natural-Hydrogen |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Turkey |

| Romania | |

| Ukraine | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| Australia | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Oman | |

| Kuwait | |

| Iraq | |

| Algeria | |

| Libya | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Rig Type | Conventional | |

| Mobile/Wheel-Mounted | ||

| Walking Super-Spec | ||

| By Drive System | Mechanical | |

| Electric (SCR and AC) | ||

| Hybrid/Compound | ||

| By Horsepower Rating | Up to 1,000 HP | |

| 1,000 to 1,499 HP | ||

| Above 1,500 HP | ||

| By Application | Conventional Oil | |

| Unconventional/Tight and Shale | ||

| Geothermal | ||

| Emerging Natural-Hydrogen | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Turkey | |

| Romania | ||

| Ukraine | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| Australia | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Oman | ||

| Kuwait | ||

| Iraq | ||

| Algeria | ||

| Libya | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the land drilling rigs market in 2026?

The land drilling rigs market size is estimated at USD 62.03 billion for 2026.

What is the projected CAGR for land drilling rigs through 2031?

The market is forecast to expand at a 0.43% CAGR between 2026 and 2031.

Which rig type is growing fastest?

Walking super-spec platforms are the fastest, advancing at a 0.8% CAGR due to pad-drilling efficiencies.

Which region shows the highest growth rate?

Asia-Pacific leads with a 1.3% CAGR, propelled by geothermal and unconventional gas initiatives.

What technology trends shape future rig demand?

High-horsepower electric rigs with automation and dual-fuel engines are commanding dayrate premiums and driving fleet upgrades.

How is natural hydrogen influencing drilling activity?

Natural-hydrogen programs, although nascent, are expanding at 15.5% CAGR as explorers validate high-purity reservoirs in Kansas, Mali, and Australia.

Page last updated on: