Market Overview

| Study Period | 2021 - 2031 |

|---|---|

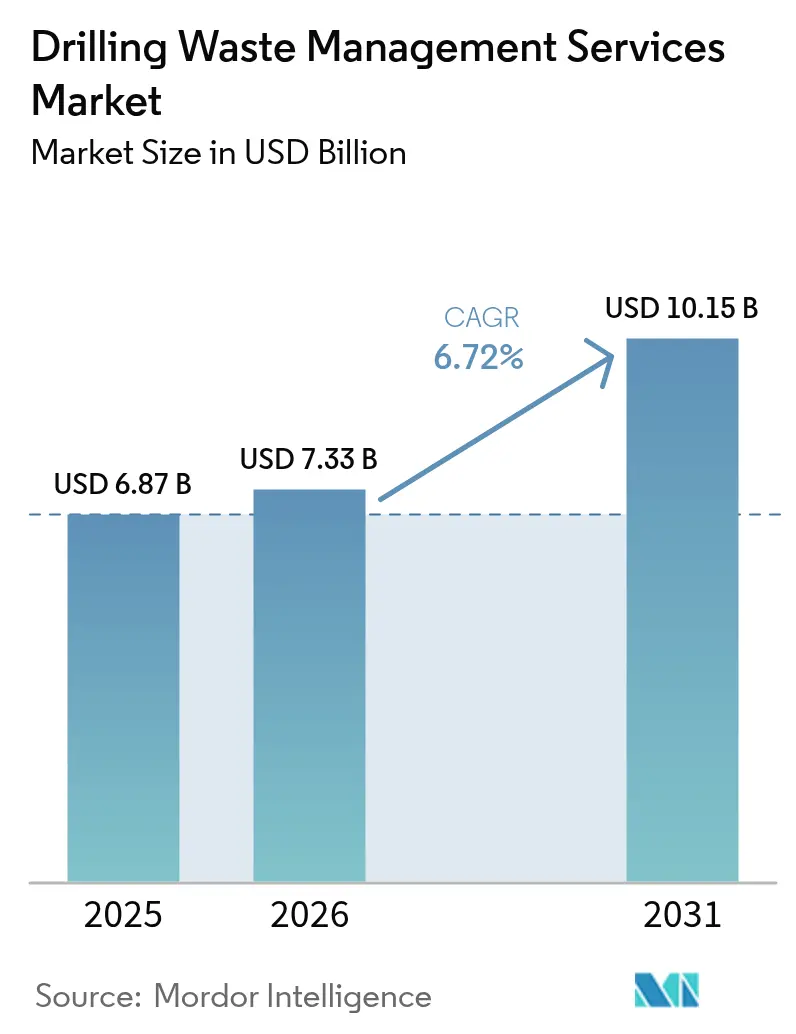

| Market Size (2026) | USD 7.33 Billion |

| Market Size (2031) | USD 10.15 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

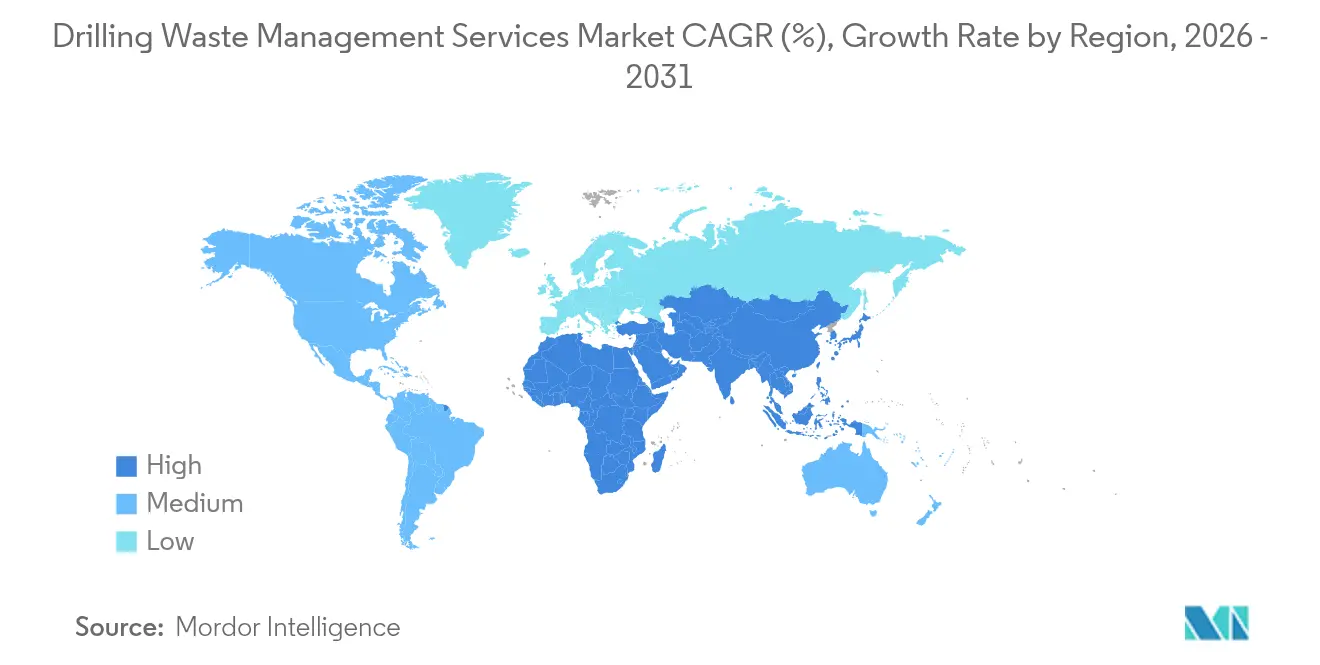

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drilling Waste Management Services Market Analysis by Mordor Intelligence

The Drilling Waste Management Services Market size in 2026 is estimated at USD 7.33 billion, growing from 2025 value of USD 6.87 billion with 2031 projections showing USD 10.15 billion, growing at 6.72% CAGR over 2026-2031.

Rising enforcement of zero-discharge rules, rapid growth in deep-water wells, and ESG-linked financing that rewards environmentally compliant projects underpin steady demand. North America leads on the back of soaring produced-water volumes in the Permian Basin, while Saudi Arabia’s 90% landfill-diversion target propels the Middle East and Africa’s expansion.[1]RBN Energy, “Permian Basin Produced-Water Outlook,” rbnenergy.com Technology adoption is shifting from basic containment to sophisticated treatment and recovery platforms, with modular thermal desorption and cuttings reinjection gaining momentum. Consolidation among service providers is accelerating as operators prefer integrated offerings that combine solids control, treatment, and digital tracking for full-cycle compliance.

Key Report Takeaways

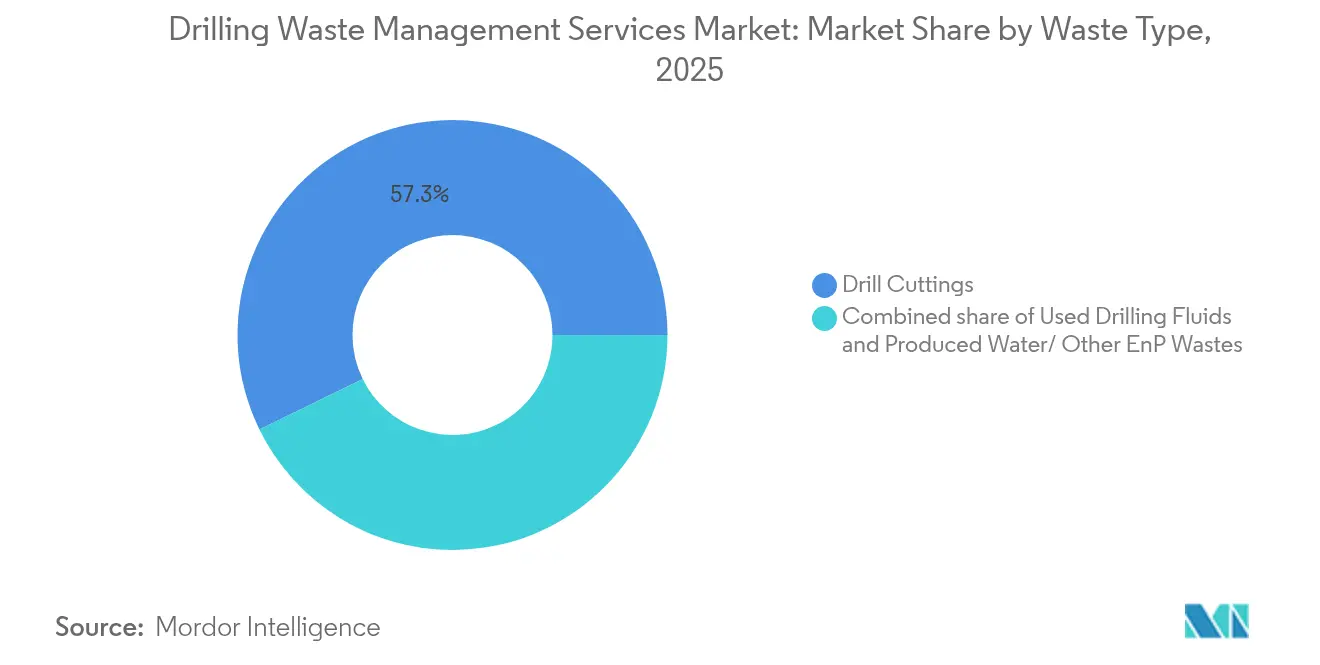

- By waste type, drill cuttings accounted for 57.25% revenue share in 2025; produced water and other E&P wastes are projected to grow at a 7.67% CAGR through 2031.

- By service, solids control held 41.35% of the drilling waste management services market share in 2025, while treatment and disposal are forecast to expand at an 8.28% CAGR between 2026 and 2031.

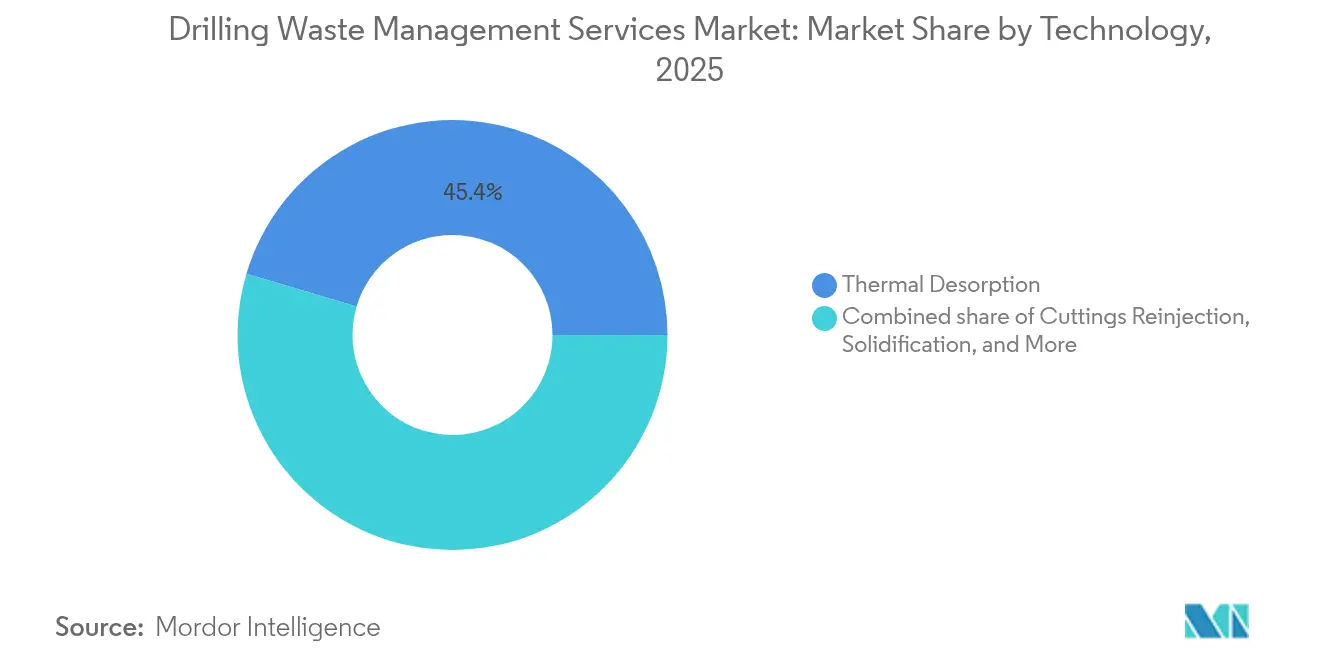

- By technology, thermal desorption captured 45.40% share of the drilling waste management market size in 2025; cuttings reinjection is advancing at a 9.05% CAGR to 2031.

- By deployment location, onshore commanded a 70.20% share of the drilling waste management market size in 2025, whereas offshore is expected to grow at a 7.56% CAGR over the forecast period.

- By geography, North America led the drilling waste management services market with a 37.65% share in 2025; the Middle East and Africa recorded the highest regional CAGR of 8.34% for the period 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drilling Waste Management Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global discharge regulations | +1.8% | Global, with early enforcement in North America & EU | Short term (≤ 2 years) |

| Growth in deep-water & ultra-deep-water drilling activity | +1.5% | Global offshore regions, concentrated in Gulf of Mexico, North Sea, Brazil | Medium term (2-4 years) |

| Shale boom driving high-volume cuttings in North America | +1.2% | North America, primarily Permian Basin, Eagle Ford, Bakken | Medium term (2-4 years) |

| ESG-linked financing favouring "zero-waste" projects | +1.0% | Global, with stronger adoption in Europe and North America | Long term (≥ 4 years) |

| Rapid adoption of modular thermal desorption units in MENA | +0.8% | Middle East and Africa, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Digital waste-tracking mandates by hydrocarbons regulators | +0.5% | UK, Canada, expanding to EU and select US states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Global Discharge Regulations

Worldwide discharge limits are intensifying as Texas implements its first overhaul of oilfield waste in four decades and the UK mandates a digital tracking system from April 2025. EPA offshore rules now prohibit the discharge of oil-based fluids within 3 miles of shore and impose strict toxicity ratios for non-aqueous fluids. Offshore operators, therefore, turn to onboard treatment and cuttings reinjection to achieve zero discharge. Regulators’ wider use of real-time monitoring systems forces investment in advanced processing rather than truck-and-dump disposal. As these rules take hold, demand rises sharply for compact thermal desorption units that meet stringent oil-on-cuttings thresholds.[2]U.S. Environmental Protection Agency, “Effluent Guidelines for Oil & Gas Extraction,” epa.gov

Growth in Deep-Water & Ultra-Deep-Water Drilling Activity

Projects such as Chevron’s 20,000 psi Anchor field in the Gulf of Mexico demonstrate how complex wells multiply waste volumes. Ultra-deep campaigns rely on high-performance fluids, generating more contaminated cuttings that shore-based landfills cannot accept. Operators retrofit drillships with thermomechanical cleaners to process thousands of tonnes of oil and gas offshore, minimizing non-productive time. Integrated waste platforms that couple desorption with slurry-handling reduce logistics costs and meet zero-discharge standards. As Brazil, Norway, and the US Gulf sanction new deep-water fields, service providers with portable offshore systems secure premium contracts.[3]SPE International, “Total E&P Angola Offshore Cuttings Cleaners Performance,” spe.org

Shale Boom Driving High-Volume Cuttings in North America

Permian output is forecast to hit 13.7 million bpd in 2025, producing large water and cuttings streams that overwhelm saltwater-disposal well capacity. Regulators warn that over-injection elevates formation pressure, risking production curtailment. Operators respond by recycling produced water for completions, blending AI-driven analytics to balance disposal and reuse. Modular treatment plants capable of processing 50,000 bpd of brine are being deployed near drill pads to cut trucking mileage. These shifts prompt a shift from simple containment to integrated treatment and recycling services across leading shale basins.

ESG-Linked Financing Favouring “Zero-Waste” Projects

Banks are increasingly conditioning lending on ESG metrics, making robust waste management essential for accessing capital. Baker Hughes reduced its greenhouse-gas intensity by 39.5% from 2019 and highlighted closed-loop drilling in its investor briefs. Operators that eliminate reserve pits and reclaim base oil typically exhibit lower remediation liabilities and attract more affordable financing. Conversely, companies reliant on disposal wells face higher borrowing costs and stricter covenant terms. This financial differentiation accelerates the uptake of zero-discharge systems and integrated digital reporting solutions that demonstrate compliance to investors.[4]Baker Hughes, “2025 Sustainability Report,” bakerhughes.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile rig-count and capex cycles | -1.5% | Global, with higher volatility in North America shale regions | Short term (≤ 2 years) |

| High capital cost of onsite treatment technologies | -1.2% | Global, particularly affecting smaller operators and remote locations | Medium term (2-4 years) |

| Closed-loop drilling fluid systems reducing third-party volumes | -0.8% | North America and Europe, with gradual adoption in other regions | Medium term (2-4 years) |

| Uncertain permitting for onshore cuttings reinjection in Europe | -0.4% | Europe, with potential regulatory spillover to other developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Rig-Count and Capex Cycles

Demand for drilling waste services swings with rig activity. Saudi Aramco’s cancellation of 20 jack-up charters in 2024 reduced Middle East rig demand growth to 1% from 4% and forced contractors to idle modular desorption fleets. Service providers must maintain expensive thermal units even during downturns, straining cash flows. Large firms hedge by deploying skid-mounted systems that can relocate quickly between basins; however, logistics costs rise when utilization falls below 60%. Financing new equipment becomes challenging when day-rate visibility declines, thereby prolonging replacement cycles. This cyclical pressure reduces near-term investment in advanced technologies and tempers the drilling waste management services market.

High Capital Cost of Onsite Treatment Technologies

Thermal desorption packages exceed USD 10 million per 20 t/h unit, while CRI systems involve directional drilling spreads and microseismic monitoring that elevate well costs. Smaller independents prefer lower-capex skip-and-ship models, despite higher lifetime spend, which delays the large-scale adoption of zero-discharge platforms. Vendors answer by offering lease-operated models and multi-client “hub” sites, but payback still depends on steady well counts. Remote frontier operations in Africa and Asia incur additional freight and customs fees that can add 25% to equipment costs, keeping conventional pits in use. The budget barrier, therefore, slows the penetration of cutting-edge solutions outside of super-major projects, constraining the upside in price-sensitive regions for the drilling waste management services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Drill Cuttings Hold Volume Leadership While Produced Water Surges

Drill cuttings commanded 57.25% of the drilling waste management services market share in 2025, thanks to their ubiquity across well designs and the complex oil-on-cuttings treatment requirements that prohibit direct discharge. Extended-reach horizontals generate longer footage and heavier cuttings logistics, sustaining demand for shakers, dryers, and thermal cleaners. The produced-water stream, meanwhile, is scaling faster at a 7.67% CAGR to 2031 as shale developments pump brine volumes that dwarf solid waste. Services now bundle cutting handling with water recycling contracts, reflecting operators’ search for single-point accountability. Closed-loop mud systems reduce fluid losses but increase the need to process recovered slops, thereby boosting the drilling waste management services market size allocated to liquid treatment platforms. Over the forecast window, integrated contracts covering cuttings plus water are expected to capture a larger wallet share as operators favor vendors who optimize both waste categories.

The produced-water surge encourages investment in mobile evaporation and crystallizer units that reduce trucking miles. In the Permian, pads trial electro-coagulation rigs paired with thermal concentrators, cutting disposal volumes by 80% and reclaiming fresh water for completions. Similar pilots in Saudi Arabia target irrigation reuse, aligning with its circular economy vision. Although drill cutting remains dominant by tonnage value, the density of produced water is expected to rise as regulators scrutinize injection wells, positioning fluid-treatment specialists for premium growth within the drilling waste management services market.

By Service: Treatment and Disposal Overtake Traditional Control for Growth

Solids control remained the largest segment at 41.35% in 2025, reflecting the mandatory inclusion of shaker and centrifuge packages on every rig. Yet treatment and disposal are advancing fastest at an 8.28% CAGR to 2031 as ESG-focused operators favor solutions that transform waste into reusable resources. Vendors now integrate vertical cuttings dryers with thermal desorption to recover up to 95% of base oil, cutting new-mud purchases by USD 40-60 per barrel. The drilling waste management services market size allocated to treatment is therefore expanding more quickly than containment spending. Service companies provide disposal certainty through strategic landfill or injection well capacity, offering “cradle-to-grave” compliance certificates that meet the demands of lenders.

Containment and handling retain relevance where well clusters share central treatment hubs. Drill-cuttings reinjection services appeal to offshore operators constrained by deck space, driving niche demand for high-pressure slurry pumps and permanent isolation packers. Digital waste-tracking SaaS is emerging as an “overlay” service that stitches together control, treatment, and disposal data, enabling operators to audit carbon intensity and prepare sustainability reports. This convergence signals a structural migration from piecemeal offerings toward end-to-end platforms in the drilling waste management services industry.

By Technology: Thermal Desorption Dominates; Reinjection Becomes Zero-Discharge Flagship

Thermal desorption retained a 45.40% share in 2025, valued for its 1% oil-on-cuttings output that meets North Sea and Gulf of Mexico discharge norms. Skid-mounted indirect-fired units process 10-15 t/h and recover base oil for reuse, improving well economics by USD 200,000 per pad. Cuttings reinjection’s 9.05% CAGR through 2031 reflects the rising deep-water activity, where operators prefer to sequester waste below the cap rock rather than shuttle barges to shore. CRI also eliminates liability associated with landfill cells that may require post-closure monitoring for 30 years, thereby strengthening its business case.

Bioremediation and stabilization serve land operations with benign climates and loose regulatory frameworks. Vacuum transfer and dewatering serve as enablers for all advanced methods by conditioning waste streams before final treatment. Suppliers are increasingly offering hybrid plants that combine desorption with low-temperature oxidation or bio-augmentation to meet varying disposal standards in multi-country campaigns. This integrated approach cements technology as a key battleground for market share in the drilling waste management services market.

By Location of Deployment: Offshore Complexity Commands Premium Growth

Onshore accounted for 70.20% of the drilling waste management market size in 2025, mirroring global rig splits. However, offshore revenues are scaling at 7.56% CAGR as deep-water projects specify onboard thermal processing and CRI packages. Day rates for offshore treatment spreads average 25-30% above those of comparable onshore units, primarily due to space constraints and the need for hazardous-area certifications. Operators accept the premium because overboard discharge bans leave no alternative but to ship waste to shore at USD 150-200 per tonne. New modular desorption units weighing under 60 t fit supply-boat cranes, broadening adoption on mid-water rigs and FPSOs.

Onshore operations still benefit from lower-cost pit closure and landfarming in jurisdictions with lenient rules, but groundwater-protection statutes are closing this gap as regulators tighten pit designs and mandate synthetic liners; cost parity with thermal or solidification treatment improves, nudging land operators toward more advanced methods. This trend underpins the steady expansion of integrated offerings that traverse on- and offshore theaters within the drilling waste management services market.

Geography Analysis

North America led the drilling waste management services market in 2025, with a 37.65% share, driven by the region's prolific shale activity. Texas’s overhaul of oilfield-waste statutes introduces first-time limits on saltwater-injection volumes and new liner requirements for pits. These rules amplify demand for high-capacity water-recycling hubs and mobile desorption fleets. Produced-water logistics in the Permian already consume more energy than five US states, prompting the development of electrified pipeline networks and solar-powered treatment plants. The region’s willingness to pilot AI-driven fluid-handling software further catalyzes market innovation.

Europe retains significant influence despite fewer rigs. Norway’s offshore waste-monitoring regime remains the gold standard for compliance, driving adoption of closed-loop mud systems and thermal desorption on every North Sea jack-up. The United Kingdom’s digital waste-tracking mandate, effective 2025, requires cradle-to-grave documentation, thereby extending the revenue for data-centric service models. Germany promotes dual-use waste-to-energy plants that accept oil-based cuttings for co-combustion, highlighting a circular economy within the drilling waste management services market.

Middle East and Africa represent the fastest-growing region, with an 8.34% CAGR through 2031. Saudi Arabia targets 90% landfill diversion and funds modular desorption pilots that reclaim synthetic muds. Oman extends the model to desert cluster drilling where trucking distances exceed 300 km, providing a cost case for onsite treatment. Africa’s frontier plays in Namibia and Kenya create fresh demand for portable containment and stabilization units compatible with limited infrastructure. These dynamics establish a robust pipeline for the drilling waste management services industry across the MENA region.

Asia-Pacific, led by China and India, accelerates onshore exploration and tightens provincial well-closure rules; however, dispersed rig counts and capital constraints slow the deployment of premium technologies. South America’s growth centers on Brazil, where Petrobras’ deep-water pre-salt developments specify integrated fluids, cement, and waste contracts that reward major service houses with desorption and CRI capabilities. Across geographies, regulatory harmonization and ESG finance push the market toward standardized zero-discharge benchmarks.

Competitive Landscape

The drilling waste management services market remains moderately fragmented. Schlumberger, Halliburton, and Baker Hughes leverage integrated portfolios to secure multi-year bundles that combine drilling, fluids, and waste services under a single invoice. Specialists such as TWMA Group, Thermtech, AS, and Secure Waste Infrastructure Corp. differentiate themselves through proprietary desorption systems and regional landfill networks. Waste Connections’ CAD 1.075 billion purchase of Secure Energy’s western-Canada assets in February 2024 underscores a consolidation wave aimed at assembling hub-and-spoke treatment infrastructures.

Digital capabilities now tip bids. TWMA’s RotoMill platform pairs thermal desorption with live emissions dashboards, winning a three-year contract with TotalEnergies UK. Baker Hughes embeds lifecycle-analysis modules into its AutoTrak rotary steerable service, offering customers carbon-unit tracking downhole. Halliburton’s BaraSolve cloud suite integrates shaker performance data with waste-tracking manifests, reducing invisible lost time by 8%. Such innovations elevate switching costs and justify premium day rates across the drilling waste management services market.

Strategic alliances flourish where majors lack local permits. Schlumberger partners with Saudi-owned Taqa to co-own a 25,000 t/y desorption plant in Dammam, ensuring compliance with in-Kingdom total value mandates. Thermtech licenses its TCC technology to Chinese fabricators, accelerating Asia roll-outs while collecting royalties. Competitive intensity is therefore shifting from simple price wars to technology licensing, regional compliance mastery, and digital-asset ecosystems that embed service providers deeply within client workflows.

Drilling Waste Management Services Industry Leaders

Baker Hughes Co.

Halliburton Company

Schlumberger Limited

Weatherford International PLC

National Oilwell Varco Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The UK Government implemented mandatory digital waste-tracking service requirements, mandating detailed documentation of waste movements from production to disposal, with enforcement actions planned for non-compliance starting April 2025.

- December 2024: SLB secured an approximately USD 800 million integrated services contract with Petrobras, covering 100 deep-water wells and advanced waste management technologies.

- April 2024: Deep Well Services and CNX Resources have launched AutoSep Technologies, introducing an automated flowback system that cuts methane emissions and enables remote operation.

- February 2024: Waste Connections completed the CAD 1.075 billion acquisition of Secure Energy Services' portfolio of 30 western-Canada energy-waste facilities.

Global Drilling Waste Management Services Market Report Scope

The drilling waste management services market report include:

By Waste Type

| Drill Cuttings |

| Used Drilling Fluids |

| Produced Water/Other E&P Wastes |

By Service

| Solids Control |

| Containment and Handling |

| Treatment and Disposal |

| Drill-Cuttings Reinjection |

| Others |

By Technology

| Thermal Desorption |

| Bioremediation and Composting |

| Stabilisation/Solidification |

| Cuttings Reinjection (CRI) |

| Dewatering and Vacuum Transfer |

By Location of Deployment

| Onshore |

| Offshore |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Rest of Middle East and Africa |

| By Waste Type | Drill Cuttings | |

| Used Drilling Fluids | ||

| Produced Water/Other E&P Wastes | ||

| By Service | Solids Control | |

| Containment and Handling | ||

| Treatment and Disposal | ||

| Drill-Cuttings Reinjection | ||

| Others | ||

| By Technology | Thermal Desorption | |

| Bioremediation and Composting | ||

| Stabilisation/Solidification | ||

| Cuttings Reinjection (CRI) | ||

| Dewatering and Vacuum Transfer | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the drilling waste management services market in 2026?

The market stands at USD 7.33 billion in 2026 and is projected to reach USD 10.15 billion by 2031.

Which region holds the largest share of the drilling waste management services market?

North America leads with 37.65% share in 2025 owing to high shale activity and strict waste rules.

Which segment is growing fastest within the drilling waste management services market?

Cuttings reinjection technology is expanding at a 9.05% CAGR between 2026-2031 due to zero-discharge mandates.

Why are treatment and disposal services outpacing solids control growth?

ESG-linked financing and tighter discharge regulations drive operators toward comprehensive treatment that recovers valuable fluids and assures full compliance.

How do digital waste-tracking mandates affect service providers?

Mandatory electronic manifests in the UK, Canada and select US states create demand for SaaS platforms that log volumes, routes and certificates, adding a new analytics revenue stream.

What factors constrain adoption of onsite thermal desorption?

High capital costs—often exceeding USD 10 million per unit—are a barrier for small operators and remote fields, although lease-operated models are emerging to spread expenses.

Page last updated on: