Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The Canada Renewable Energy Market Report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

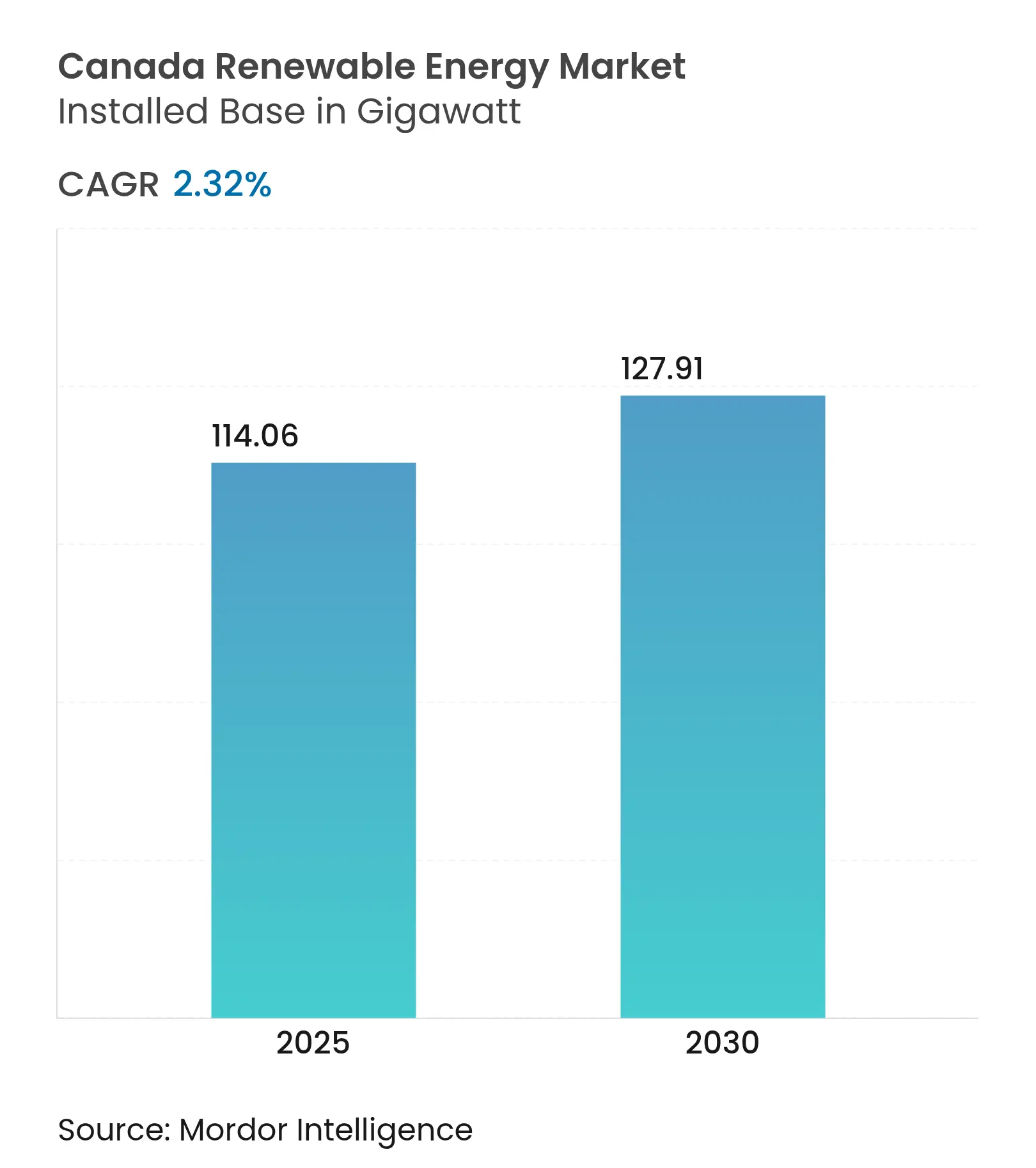

| Market Volume (2025) | 114.06 gigawatt |

| Market Volume (2030) | 127.91 gigawatt |

| CAGR | 2.32 % |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hydro assets continue to underpin generation, yet wind and solar additions outpace legacy growth as carbon-pricing moves above CAD 170 per tonne. Falling levelized costs and an expanding pool of corporate power-purchase agreements bolster project bankability, while Indigenous equity structures lower financing hurdles for installations in remote regions. Green hydrogen export corridors widen the demand base beyond domestic electricity needs, and federal clean-technology incentives improve residential economics, nudging households toward distributed solar-plus-storage solutions.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Federal carbon-pricing escalation Federal carbon-pricing escalation | +0.60% | National, with strongest effect in Alberta and Saskatchewan | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.60% | Geographic Relevance:National, with strongest effect in Alberta and Saskatchewan | Impact Timeline:Medium term (2-4 years) |

Accelerated coal-to-renewables displacement mandate Accelerated coal-to-renewables displacement mandate | +0.50% | Alberta, Saskatchewan, Nova Scotia | Short term (≤ 2 years) | |||

Declining LCOE of onshore wind & utility-scale PV Declining LCOE of onshore wind & utility-scale PV | +0.40% | National, with early gains in Ontario, Alberta, Quebec | Medium term (2-4 years) | |||

Surge in corporate PPAs from data-centre & mining sectors Surge in corporate PPAs from data-centre & mining sectors | +0.30% | Ontario, Quebec, British Columbia | Medium term (2-4 years) | |||

Indigenous equity-ownership frameworks unlocking capital Indigenous equity-ownership frameworks unlocking capital | +0.20% | British Columbia, Prairies, Northern territories | Long term (≥ 4 years) | |||

Green-hydrogen export corridor initiatives Green-hydrogen export corridor initiatives | +0.20% | Atlantic provinces, with spill-over to Quebec | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Federal Carbon-Pricing Escalation

Escalating carbon fees lift fossil-fuel generation costs and sharpen the competitiveness of renewables, particularly as rates climb toward CAD 170 per tonne by 2030.[1]CBC News, “Federal Carbon Price Escalation,” cbc.ca Clean Electricity Regulations adopted in 2024 require zero-emission electricity by mid-century, compelling utilities to fast-track renewable capacity.[2]Canada Gazette, “Clean Electricity Regulations 2024,” canadagazette.gc.ca Provinces diverge in compliance pace, but the price signal improves long-term revenue certainty for wind and solar developers, supporting merchant projects and lengthening contract tenors sought by institutional investors.

Indigenous Equity-Ownership Frameworks Unlocking Capital

The inaugural CAD 108.3 million equity loan from the Canada Infrastructure Bank to the Mesgi'g Ugju's'n 2 wind farm illustrates how Indigenous participation unlocks financing while honoring stewardship rights.[3]Yahoo Finance, “Canada Infrastructure Bank Funds Indigenous Wind,” finance.yahoo.com Subsequent BC Hydro procurement awarded nine majority-Indigenous projects worth CAD 6 billion, demonstrating policy alignment between reconciliation goals and energy expansion. Equity involvement accelerates permitting, lessens social-license risk, and channels revenue into local economies, creating a durable model for growth in remote resource corridors.

Green-Hydrogen Export Corridor Initiatives

A CAD 8 billion Newfoundland scheme aimed at German off-takers showcases Canada’s bid to supply renewable-based hydrogen to Europe. Brookfield’s 20 MW electrolyzer for Gazifère pairs hydrogen production with existing gas networks, proving a hybrid infrastructure that broadens decarbonization pathways. Export corridors demand fresh wind and solar build-outs, absorb excess generation and trigger transmission upgrades, extending growth beyond the electricity sector.

Surge in Corporate PPAs from Data-Centre & Mining Sectors

Microsoft’s 10.5 GW global renewables arrangement with Brookfield underscores hyperscale appetite for clean power that circumvents utility procurement timelines. Alberta’s roadmap for AI data-centre interconnections targets 1,200 MW of new load by 2028, embedding long-term PPAs into project pipelines. Mining firms echo the trend, contracting wind and solar to cut energy costs and satisfy investor ESG mandates, further diversifying demand.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Transmission congestion & curtailment risks Transmission congestion & curtailment risks | -0.40% | Alberta, Ontario, with emerging issues in Saskatchewan | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.40% | Geographic Relevance:Alberta, Ontario, with emerging issues in Saskatchewan | Impact Timeline:Short term (≤ 2 years) |

Lengthy provincial site-permitting timelines Lengthy provincial site-permitting timelines | -0.30% | National, with acute delays in British Columbia and Quebec | Medium term (2-4 years) | |||

Critical-minerals supply-chain tightness for PV & storage Critical-minerals supply-chain tightness for PV & storage | -0.20% | National, affecting all provinces | Medium term (2-4 years) | |||

Indigenous land-rights disputes delaying projects Indigenous land-rights disputes delaying projects | -0.20% | British Columbia, Northern Ontario, Prairies | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Transmission Congestion & Curtailment Risks

Rapid build-out has outpaced grid capacity in several corridors, prompting curtailment warnings from the Alberta Electric System Operator and driving Hydro-Québec to earmark CAD 50 billion for 5,000 km of new lines. Bottlenecks raise project financing costs and shave revenues until upgrades materialize, tempering near-term expansion in high-resource zones.

Critical-Minerals Supply-Chain Tightness for PV & Storage

Canada mines lithium, nickel, and cobalt, yet limited domestic processing exposes solar and battery projects to global supply disruptions.[4]Natural Resources Canada, “Critical Minerals Strategy,” nrcan.gc.ca A CAD 4 billion federal strategy seeks to localize refining, but facilities will take years to scale, leaving projects vulnerable to import price swings during the forecast horizon.

By Technology: Hydropower Anchors, Ocean Energy Surges

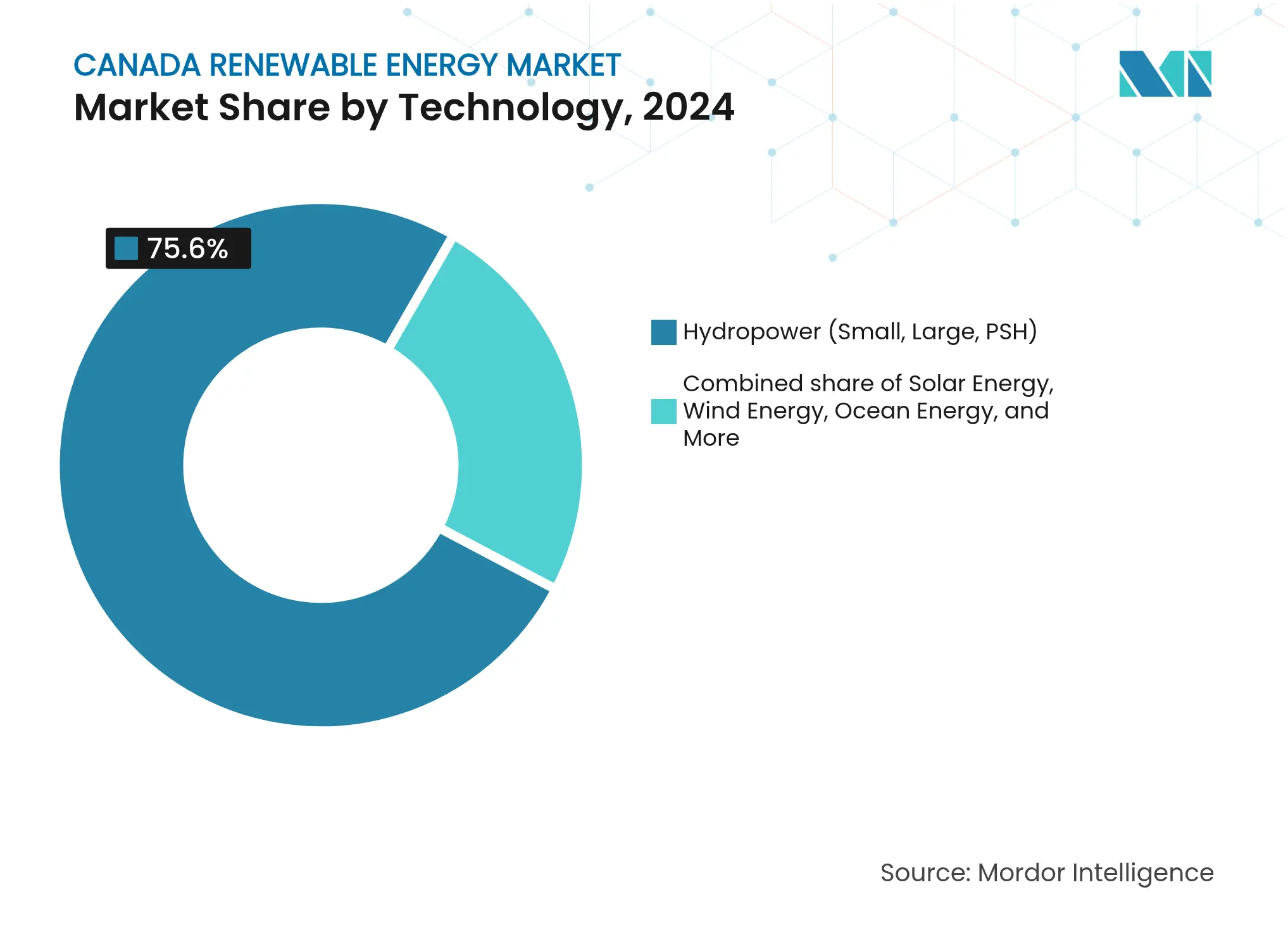

Hydropower dominated the Canadian renewable energy market with 75.6% of installed capacity in 2024 as mega-projects such as La Grande (16 GW) and Site C (1.1 GW) continued to supply baseload electricity. Ocean energy, though starting from a small base, is projected to scale at a 58.5% CAGR on the strength of tidal arrays in the Bay of Fundy and wave pilots off Vancouver Island, supported by federal Emerging Renewable Power Program funding. Wind added 1.8 GW in 2024, concentrated in Alberta’s Palliser and Cypress wind belts where capacity factors top 40%, land leases remain cheap, and developers pair projects with batteries to qualify for capacity payments. Solar added 1.2 GW in 2024, leveraging bifacial modules with single-axis trackers in Ontario and Alberta for annual capacity factors near 20%.

Bioenergy and geothermal combined accounted for less than 3% of capacity in 2024, yet both technologies gained renewed interest for their baseload attributes. Bioenergy plants in British Columbia and Quebec tapped forest residues to add 150 MW last year under provincial renewable standards. Alberta’s oil patch is repurposing depleted wells; Eavor’s 5 MW closed-loop geothermal system offers a template for heat extraction without hydraulic fracturing. Pumped-storage hydropower is resurging as grid operators seek multi-hour storage; Ontario Power Generation broke ground on the 400 MW Marmora project that will soak up curtailment and discharge during nightly peaks. Collectively, these shifts illustrate how the Canada renewable energy market is diversifying away from its hydropower-centric legacy toward a multi-technology portfolio.

Note: Segment shares of all individual segments available upon report purchase

By End User: Utility Control Shifts Toward Distributed Models

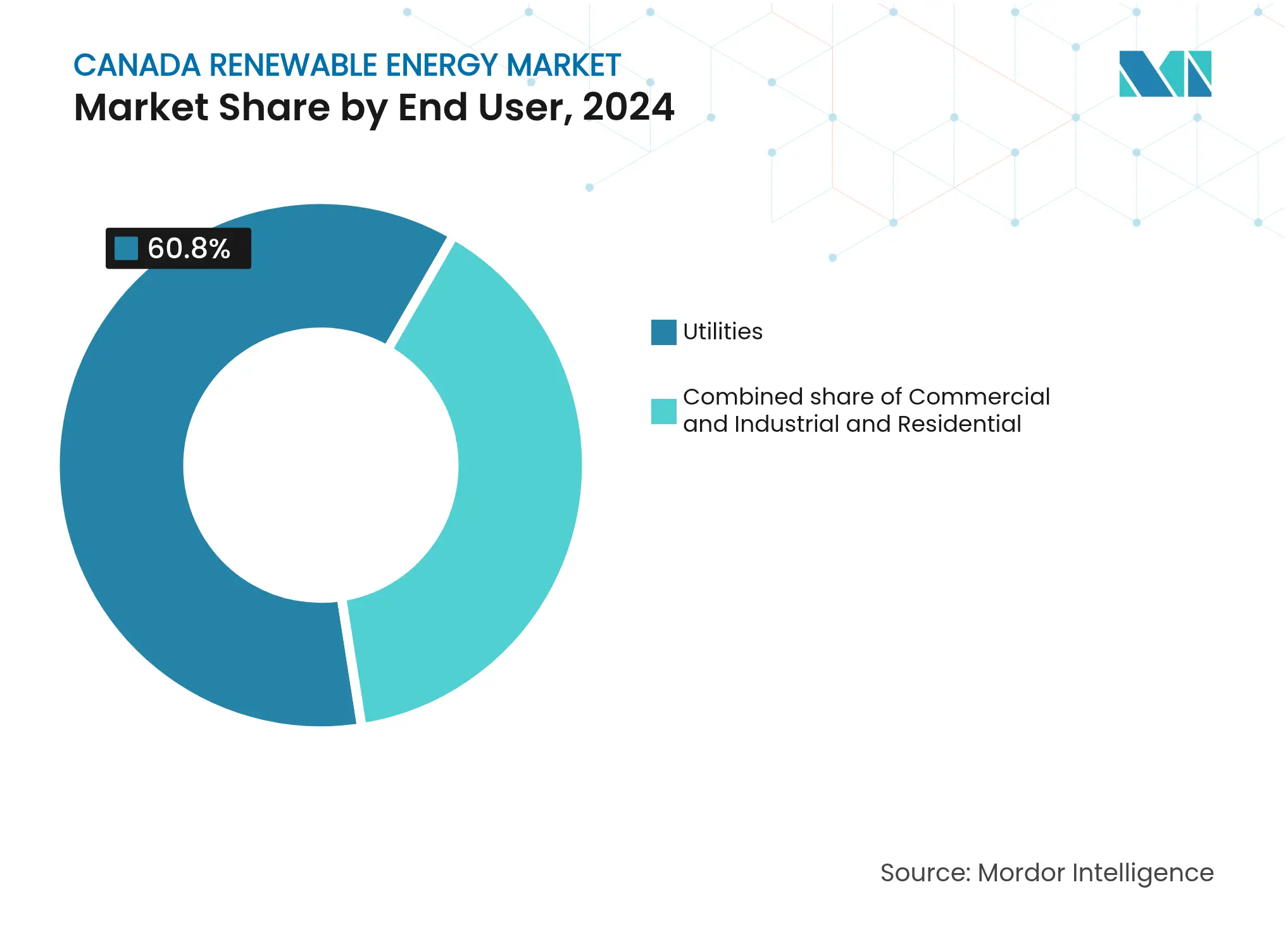

Utility-owned producers met 61% of end-user demand in 2024, leveraging scale and long-term contracts to finance large hydro and wind parks. The residential segment grows 8% annually as households install rooftop arrays and lithium-ion batteries that qualify for the federal clean-tech investment credit, eroding retail sales volumes for incumbents. Commercial buyers ink direct PPAs to hedge future power costs and satisfy sustainability mandates, while miners and data-centre operators anchor utility-scale solar in energy-rich Alberta.

Distributed resources necessitate two-way power flows, pushing regulators to revamp interconnection rules and time-of-use tariffs. Aggregated behind-the-meter assets begin to participate in capacity markets, offering demand response and ancillary services. Utilities respond by investing in distribution automation and customer-sited storage, pivoting toward platform service models that monetize grid reliability rather than volumetric sales alone.

Note: Segment shares of all individual segments available upon report purchase

Quebec commands the largest provincial footprint due to legacy hydro capacity and a CAD 185 billion strategy to triple wind installation, modernize transmission, and export surplus power to the northeastern United States. Its 2024 tender procured 1,550 MW of wind at 7.8 cents per kilowatt-hour, maintaining cost competitiveness despite inflationary pressure. Indigenous partnerships underpin most new projects, granting communities equity stakes and revenue sharing that streamline permitting.

British Columbia accelerates procurement to meet a projected 15% load rise by 2030. BC Hydro’s recent award of nine Indigenous-majority wind contracts totaling nearly 5,000 GWh annually reflects reconciliation priorities and favorable coastal wind regimes. The province exempts wind farms from environmental assessments under defined thresholds, shortening lead times while maintaining robust First Nations consultation protocols.

Alberta hosts 75% of recent renewable investment, yet grapples with policy turbulence. A six-month moratorium was lifted in early 2024, but land-use restrictions on agricultural parcels and scenic zones lengthen development cycles. Grid stability concerns spur market redesign, and transmission build-out lags generation additions. Still, superior solar irradiance and robust wind resources suggest large-scale potential once regulatory clarity improves.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

Market structure remains moderately consolidated. Hydro-Québec, BC Hydro, and Ontario Power Generation dominate their home jurisdictions by owning hydroelectric fleets and integrated transmission assets. Independent power producers such as Brookfield Renewable Partners, Northland Power, and Innergex Renewable Energy expand through offshore wind, utility-scale batteries, and global diversification. Indigenous joint ventures increasingly win provincial tenders, altering competitive hierarchies and embedding community ownership into project finance.

Consolidation gains momentum. CDPQ’s CAD 10 billion acquisition of Innergex elevates pension-fund influence over project pipelines, while LS Power’s CAD 2.5 billion purchase of Algonquin’s renewables arm signals inbound US capital seeking exposure to long-dated Canadian contracts. Developers hedge regulatory risk by blending merchant exposure with contracted revenues and assembling multi-technology portfolios that capture ancillary-service revenues from storage.

Strategic themes include vertical integration into green hydrogen, co-location of renewables with data-centre load, and deployment of long-duration storage. Companies leverage Canada’s critical minerals endowment to explore domestic battery supply chains, though processing scarcity keeps immediate focus on imported cells. Competitive pressures spur innovation in financing structures, with revenue-based securitization and synthetic PPAs gaining traction among institutional investors.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Renewable energy is derived from natural sources that replenish faster than they are consumed, such as sunlight, wind, water, geothermal heat, and biomass. These resources are considered inexhaustible and are used to generate electricity, heat, and fuel, typically resulting in a lower carbon footprint and reduced environmental impact compared to fossil fuels.

The Canadian Renewable Energy Market is segmented by technology and end-user. By technology, the market is segmented by Solar Energy (PV and CSP), Wind Energy (Onshore and Offshore), Hydropower (Small, Large, PSH), Bioenergy, Geothermal, Ocean Energy (Tidal and Wave). By end user, the market is segmented into Utilities, Commercial and Industrial, and Residential. The report also covers the market size and forecasts for Canada.

For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

Unlocking Market Potential for Solid-State Transformers

3 Min Read

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.