Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

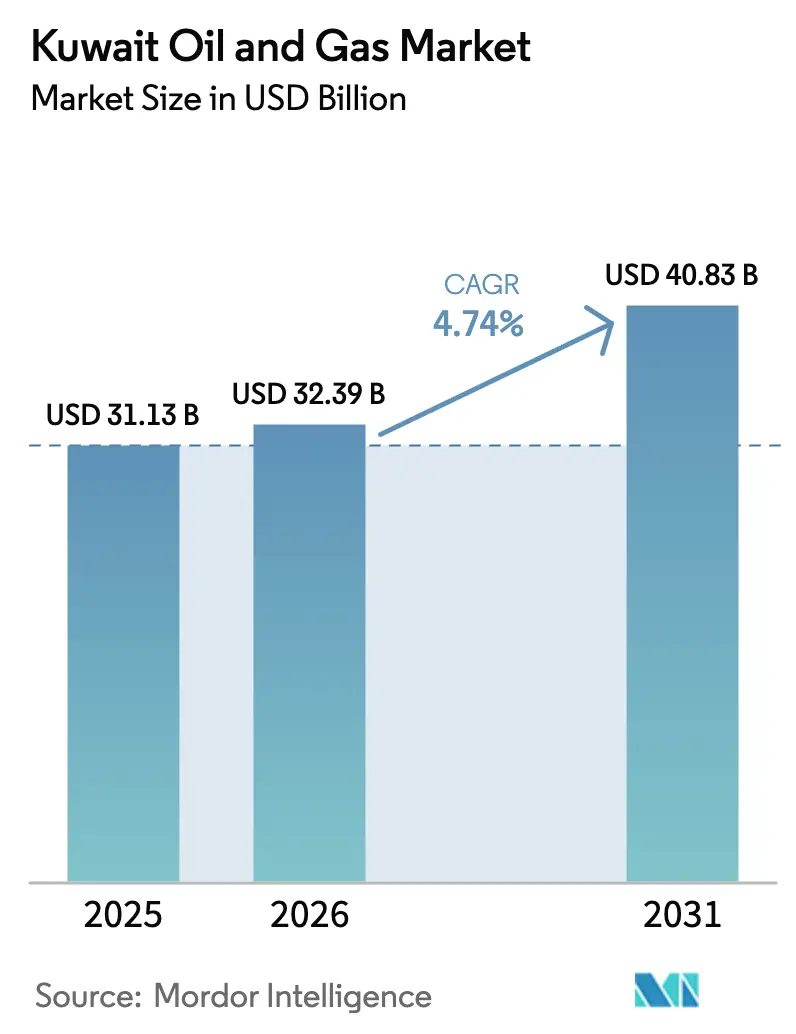

| Base Year Market Size (2025) | USD 31.13 Billion |

| Market Size (2026) | USD 32.39 Billion |

| Market Size (2031) | USD 40.83 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

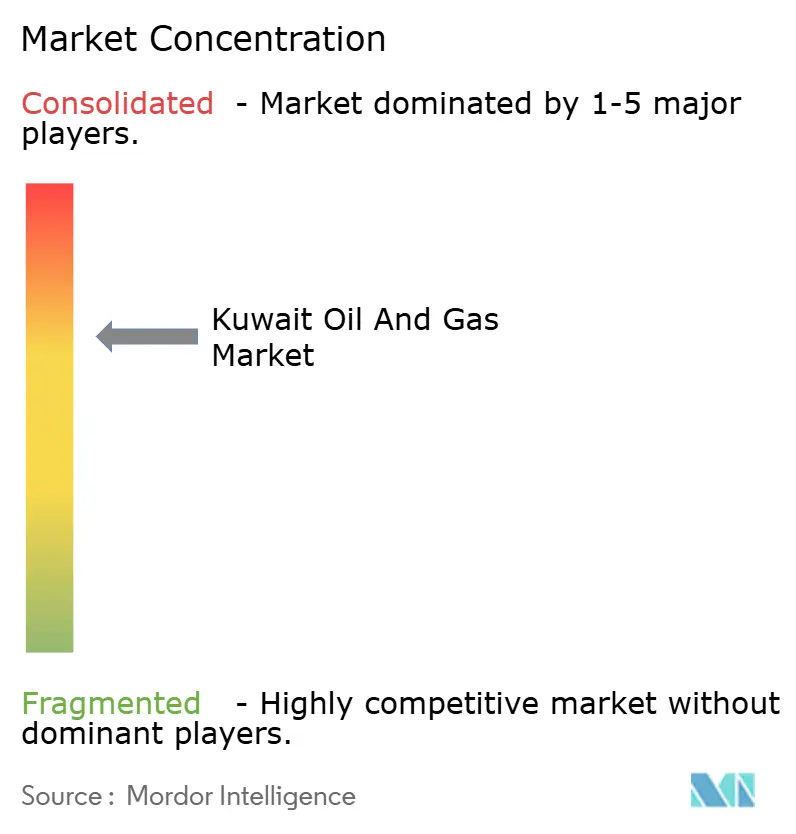

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait Oil And Gas Market Analysis by Mordor Intelligence

The Kuwait Oil And Gas Market size was valued at USD 31.13 billion in 2025 and is estimated to grow from USD 32.39 billion in 2026 to reach USD 40.83 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031).

OPEC+ quota discipline is capping headline crude volumes, yet state-led investment of USD 9 billion to USD 10 billion per year is pushing offshore frontier acreage into development and slowing decline rates in mature onshore fields.[1]Kuwait Oil Company, “Kuwait Integrated Digital Field Platform Operational Across 1,200 Wells,” kockw.com Downstream profitability is rising as the 615,000-barrel-per-day Al-Zour refinery approaches nameplate throughput and captures IMO-compliant bunker-fuel premiums.[2]Kuwait Integrated Petroleum Industries Company, “KIPIC Annual Report 2024-25,” kipic.com Domestic gas demand for power and desalination is expanding faster than supply, sustaining LNG imports and spurring midstream expansion.[3]Kuwait Ministry of Electricity and Water, "Kuwait Ministry of Electricity and Water: Installed Capacity and Peak Demand Analysis," mew.gov.kw Meanwhile, digital-oilfield roll-outs across 1,200 wells are lowering non-productive time and reallocating capital toward predictive maintenance and production optimization.

Key Report Takeaways

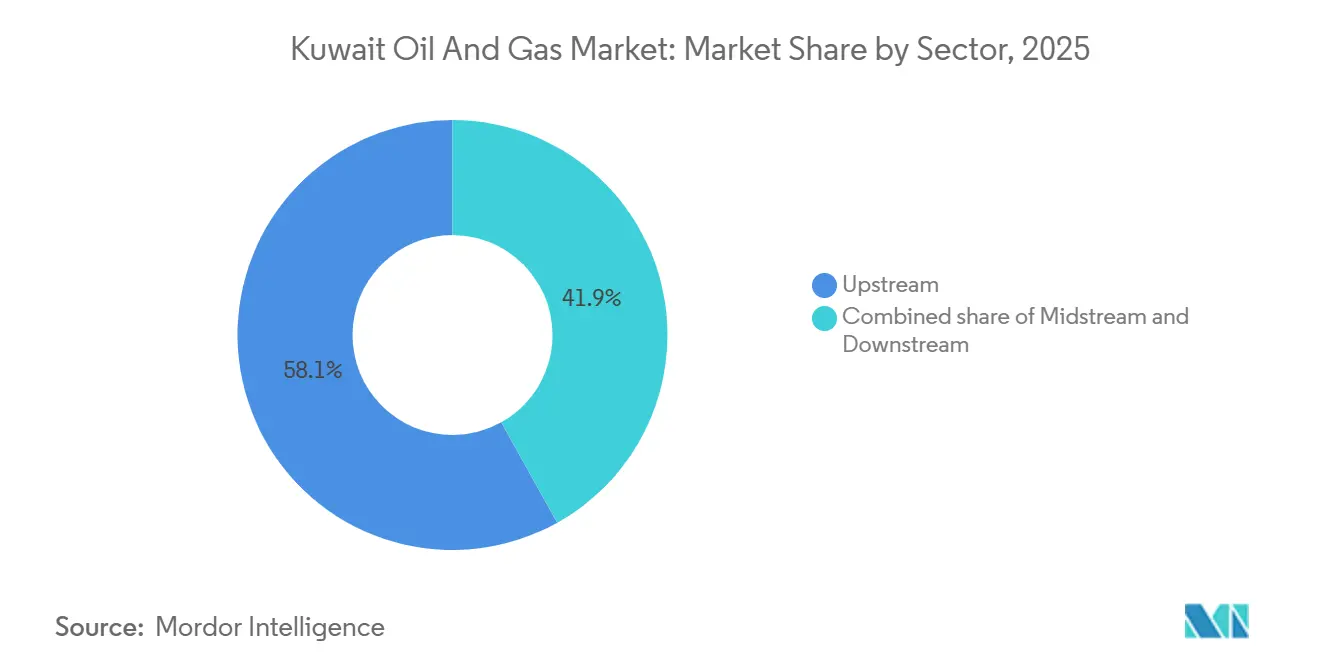

- By sector, upstream captured 58.14% of Kuwait's oil and gas market share in 2025, while downstream is advancing at a 6.18% CAGR through 2031.

- By location, onshore assets held 91.5% of the Kuwait oil and gas market size in 2025; offshore activity is growing at a 7.1% CAGR on the strength of three major discoveries.

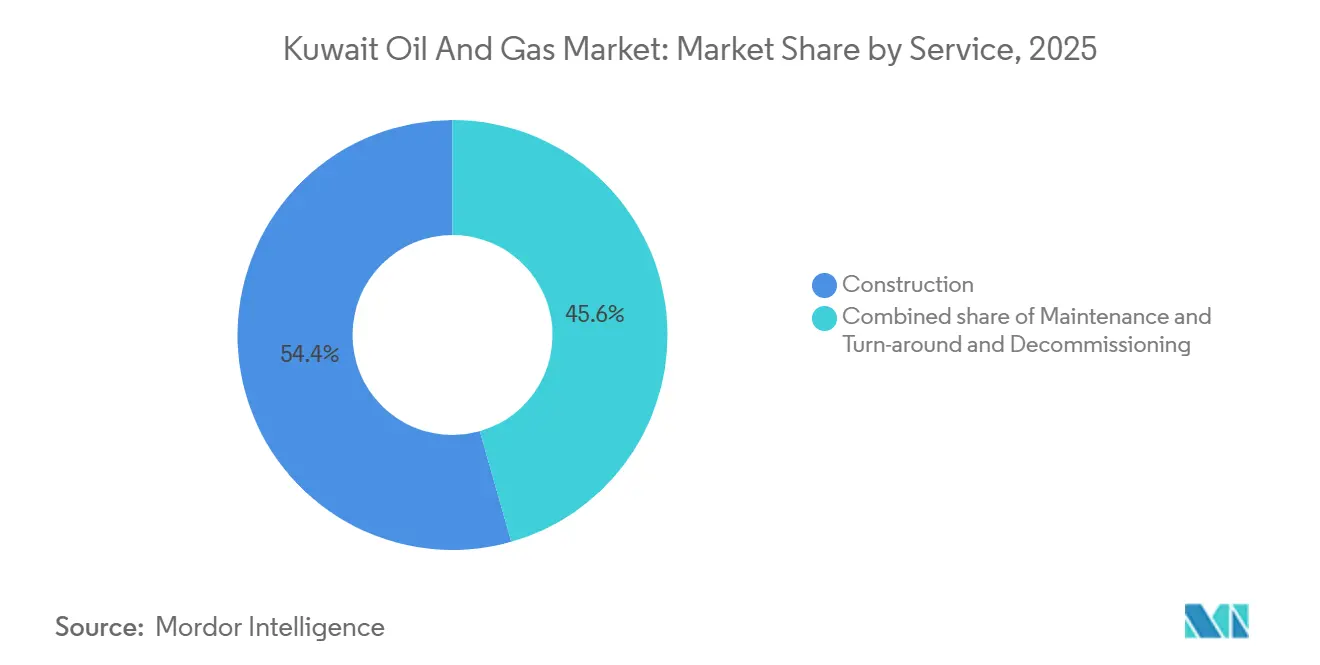

- By service, construction services led with 54.4% of the Kuwait oil and gas market share in 2025, whereas decommissioning is set to expand at a 6.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 30 billion Five-Year Upstream Expansion Plan (2024-29) | +1.2% | Greater Burgan, West Kuwait, Neutral Zone offshore blocks | Medium term (2-4 years) |

| Al-Zour Refinery Ramp-up Elevating Downstream Margins | +0.9% | National; export spillover to Asia and East Africa | Short term (≤ 2 years) |

| Neutral-Zone Development Revitalising Offshore Output | +0.7% | Partitioned Zone Wafra, Khafji and new offshore finds | Medium term (2-4 years) |

| Rising Domestic Gas Demand for Power & Desalination | +0.6% | Coastal desalination hubs and urban grids | Long term (≥ 4 years) |

| Digital Oilfield Roll-outs | +0.4% | North Kuwait, Greater Burgan | Medium term (2-4 years) |

| In-country Pipeline / Equipment Manufacturing | +0.3% | Shuaiba and Ahmadi industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

USD 30 billion Five-Year Upstream Expansion Plan (2024-29)

Kuwait Petroleum Corporation is allocating USD 9 billion to USD 10 billion each year through 2030 to offset 4%-6% natural decline in mature reservoirs and advance new offshore acreage.[4]Staff writers, “Kuwait Upstream Capex to Reach $9-10 bn Annually Through 2030,” Middle East Economic Survey, mees.com The capital program centers on sustaining the 1.7 million-barrel-per-day Burgan plateau, restarting Neutral-Zone capacity toward 600,000 barrels per day, and drilling high-pressure Jurassic wells that require horizontal completions and multi-stage fracturing. Execution risk pivots on procuring subsea trees, sour-service pipe, and high-temperature separators within global supply-chain bottlenecks that can extend fabrication by 6-12 months. KBR’s July 2025 FEED award for the South Ratqa Heavy Oil Program underlines a push into viscous crudes needing thermal recovery at USD 15-USD 20 per-barrel incremental cost. Field work windows restricted to October-April add seasonal schedule pressure, making real-time logistics coordination critical for on-time delivery.

Al-Zour Refinery Ramp-up Elevating Downstream Margins

Al-Zour reached 507,458 barrels per day average throughput in fiscal 2024-25, or 82% of its 615,000-barrel-per-day design, after achieving mechanical completion in July 2023. January 2026 exports exceeded 1 million tonnes of very-low-sulfur fuel oil, capturing a USD 8-USD 12 per-tonne premium in Asian bunker hubs and widening downstream margins by USD 4-USD 6 per barrel relative to legacy refineries. Hydrocracking and delayed-coking units deliver a 95% distillate yield versus 70%-75% at older plants, while integration with a 22-million-tonne-per-year LNG terminal substitutes cheaper gas for refinery fuel and trims costs by USD 0.30 per barrel. The KNPC–KIPIC merger, launched in April 2025, targets USD 2 billion annual synergies by unifying procurement and storage, signaling deeper value-chain integration. Rising domestic fuel sales, forecast to hit 17 billion liters within three years, will further anchor refinery utilization.

Neutral-Zone Development Revitalising Offshore Output

Partitioned Neutral-Zone production rebounded to about 341,000 barrels per day by early 2025 after prior shutdowns, and bilateral plans aim for 600,000 barrels per day through facility upgrades and infill drilling. The May 2025 Wara-Burgan-1 test flowed more than 500 barrels per day of 26°-27° API crude, validating deeper Cretaceous targets and sparking a six-well appraisal program. Kuwait Gulf Oil Company is fast-tracking subsea manifolds, flowlines, and a central processing platform to connect new finds to export networks by late 2027, contingent on 18-24-month equipment lead times. Joint-approval requirements between Kuwait and Saudi Arabia continue to add 12-24 months to final investment decisions whenever cost-recovery terms diverge. High H₂S content in recent offshore gas discoveries obliges acid-gas injection or sulfur-recovery units that raise development costs by USD 1.50-USD 2.00 per thousand cubic feet.

Rising Domestic Gas Demand for Power & Desalination

Natural-gas output hit a record 2.07 billion cubic feet per day in June 2025, yet peak-summer power and desalination loads outstrip supply, compelling LNG imports through Al-Zour’s 22-million-tonne-per-year terminal. Installed generation capacity stands at 21 GW, but aging turbines reduce reliable output to roughly 17 GW, prompting electricity imports from Saudi Arabia and accelerating oil-fired unit retirements. The 2040 gas strategy seeks 4 billion cubic feet per day, with Jurassic non-associated gas providing half that volume if reservoir performance meets expectations. Desalination already consumes 15% of the national gas supply, and each 10-million-gallon-per-day capacity addition requires around 35 million cubic feet per day of fuel gas, locking in long-term demand. HEISCO’s 2024 pipeline upgrade removed bottlenecks in the south, yet further midstream debottlenecking is essential to avoid winter supply shortfalls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OPEC+ Quota Volatility & Compliance Cuts | -0.8% | National; spillover to global prices and fiscal revenue | Short term (≤ 2 years) |

| High Flaring-to-Zero Emissions Mandate Costs | -0.5% | New gathering centers and offshore platforms | Medium term (2-4 years) |

| Chronic Ministerial Turnover Slowing Project Sanctions | -0.3% | Upstream and downstream FIDs | Medium term (2-4 years) |

| Water Scarcity Pressures on Enhanced Oil Recovery | -0.2% | Inland fields using polymer flood or steam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OPEC+ Quota Volatility & Compliance Cuts

Kuwait’s February 2026 quota of 2.58 million barrels per day sits 620,000 barrels per day below sustainable capacity and 1.42 million barrels per day under the 2035 target, translating into USD 1.3 billion annual revenue loss for every 100,000-barrel-per-day cut at USD 75 Brent. Repeated shut-ins in high-productivity Burgan wells raise well-restart costs by USD 200,000-USD 500,000 each. Quarterly OPEC+ meetings rarely specify baseline clarifications, forcing the Kuwait Oil Company to model multiple production scenarios that inflate planning budgets by up to 8% OPEC.ORG. Contracting uncertainty also strands drilling rigs and hydraulic-fracturing spreads booked 18-24 months ahead, leaving day-rate obligations outstanding when quotas tighten. Long-lead projects face discounted net-present-value assessments because unlocked volumes may not be monetizable under future allocations.

High Flaring-to-Zero Emissions Mandate Costs

The Kuwait Environment Public Authority now obliges zero routine flaring on all new assets, adding USD 80 million-USD 150 million to each major gathering-center budget for compressors, dehydration units, and sulfur-recovery trains. Offshore compliance is more expensive because space and weight limits drive the need for subsea gas export lines priced at USD 2 million-USD 3 million per kilometer in shallow Gulf waters. Non-compliant flare stacks face USD 10,000 daily fines, accelerating the adoption of continuous emissions monitoring and satellite-based methane detection that cost USD 5 million-USD 10 million per asset plus annual software subscriptions. Sour-gas streams with >10% H₂S require additional sulfur handling that raises operating expense by USD 0.40-USD 0.60 per barrel in fields like the new Neutral-Zone discoveries. While the policy enables Kuwait to market low-carbon barrels, it pressures near-term cash flows and extends breakeven timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Anchors Revenue, Downstream Drives Growth

Upstream contributed 58.14% of Kuwait's oil and gas market revenue in 2025, reflecting the dominance of the Burgan complex and the Neutral-Zone restart. Yet OPEC+ limits and natural decline temper growth, keeping segment value almost flat through 2028. Downstream is advancing at a 6.18% CAGR to 2031 as Al-Zour's 95% distillate yield lifts margins and boosts export competitiveness. Midstream investments trail domestic gas demand that hit 2.07 billion cubic feet per day in 2025 and could double by 2040. Schlumberger's USD 1.5 billion Mutriba contract shows operators outsourcing complexity to speed first oil and stretch plateau rates.

Upstream capital intensity is rising as operators move into deeper, hotter, and sourer reservoirs requiring corrosion-resistant alloys and high-pressure completion systems, pushing average well costs toward USD 8 million-USD 12 million. The Kuwait oil and gas market size linked to the downstream has more headroom because every 1 percentage-point increase in Al-Zour utilization adds around USD 160 million in annual gross margin at current cracks. Integration via the KNPC–KIPIC merger pools 1.42 million barrels per day of refining and 3.12 million barrels per day of gas processing capacity, creating purchasing leverage and unlocking USD 2 billion in cost savings. Heavy-oil development at South Ratqa will diversify the crude slate but carries steam-generation costs of USD 15-USD 20 per produced barrel. As downstream captures higher returns, future allocations may tilt toward petrochemical integration, implying a gradual shift in Kuwait's oil and gas market share toward midstream-to-downstream assets over the next decade.

By Location: Onshore Heritage, Offshore Momentum

Onshore fields delivered 91.5% of 2025 output and retained the dominant revenue position inside the Kuwait oil and gas market in the same year, thanks to the well-developed Burgan, North Kuwait, and West Kuwait clusters that keep drilling costs near USD 3 million-USD 5 million per well and sustain plateau rates despite 4%-6% natural decline. Offshore prospects are rising at a 7.1% CAGR to 2031 as three discoveries announced between July 2024 and October 2025, Al-Nokhatha, Al-Jlaiaa, and Jazah-1, collectively added 4.5 billion barrels of oil equivalent, shifting capital to subsea platforms, manifolds, and flowlines.

The Neutral-Zone revival is the centerpiece of offshore spending, targeting 600,000 barrels per day by 2028 once joint Kuwaiti–Saudi facilities reach full throughput. Offshore wells cost USD 25 million-USD 40 million each, yet reservoir quality is higher, with 26°-28° API gravity crudes that trade near Brent and improve the Kuwait oil and gas market size, attached to export revenues. Onshore assets face produced-water disposal costs that add USD 0.50-USD 0.80 per barrel, while offshore campaigns contend with 18-24-month equipment lead times that can delay first oil by a full budget cycle. Digital real-time surveillance now covers 1,200 Burgan wells, cutting non-productive time and freeing crews for offshore tasks that push the future Kuwait oil and gas market growth profile toward deeper water.

By Service: Construction Rules, Decommissioning Accelerates

Construction services commanded 54.4% of the Kuwait oil and gas market share in 2025 on the back of four gathering-center awards, GC-29, GC-30, GC-31, and GC-32, which together add 1.2 million barrels per day of crude-handling capacity, all executed under zero-flare specifications. Decommissioning is the fastest growing service line at 6.6% CAGR through 2031, steered by tighter bonding rules from the Environment Public Authority that oblige operators to plug and abandon legacy wells before license expiry.

Maintenance and turn-around work sits between those extremes, with integrated condition-based monitoring trimming scheduled shutdown frequency at Al-Zour and Mina Abdullah refineries by up to 12%. Baker Hughes embedded a 25,000-square-meter workshop under a multi-year electric-submersible-pump contract that ties payment to uptime, underscoring the shift from equipment sales toward outcome-based fees within the Kuwait oil and gas industry. Looking ahead, the Kuwait oil and gas market will pivot toward decommissioning scale after 2029 once gathering-center installations plateau and brownfield abandonment widens, offering margin resilience to service firms with remediation credentials.

Geography Analysis

The Greater Burgan area delivered about 1.7 million barrels per day in 2025, anchoring national volumes and hosting the Kuwait Integrated Digital Field platform that covers more than 1,200 wells. North Kuwait produced 400,000-500,000 barrels per day, while West Kuwait added up to 250,000 barrels per day, yet all three onshore clusters require 200 infill wells annually to offset 4%-6% decline, keeping the Kuwait oil and gas market investment bias toward drilling fluids, rigs, and artificial-lift upgrades.

Offshore acreage inside Kuwaiti territorial waters now represents the most important growth lever, with the Al-Nokhatha, Al-Jlaiaa, and Jazah-1 finds proving commercial hydrocarbons and pushing the Kuwait oil and gas market share of offshore capex above 20% for the first time. Kuwait Gulf Oil Company is fast-tracking subsea tie-backs to existing Neutral-Zone pipelines, but every procurement decision must pass bilateral review, extending approval cycles by up to two years.

The coastal industrial corridor houses Al-Zour refinery, the LNG import terminal, and two legacy refineries that together consume roughly 1.5 billion cubic feet per day of gas, concentrating supply-chain logistics but increasing single-point-of-failure exposure during regional tension. Arid inland fields rely on desalinated seawater or produced-water recycling for enhanced-oil-recovery pilots, which adds 8%-12% to lifting costs and limits polymer-flood scaling, a structural headwind inside the Kuwait oil and gas market value model.

Competitive Landscape

Kuwait Petroleum Corporation and its five core subsidiaries control all acreage, refining barrels, and LNG intake, creating a tightly held Kuwait oil and gas market where international firms compete for service contracts rather than equity. The April 2025 KNPC-KIPIC merger consolidates 1.42 million barrels per day of refining with 3.12 million barrels per day of gas processing, aiming for USD 2 billion annual synergy once integration completes, and further narrows the room for independent downstream players.

Technology partnerships are becoming the primary route for foreign participation. Schlumberger secured a USD 1.5 billion integrated Mutriba contract in February 2026 that links payment to production uptime, while Baker Hughes locked in an outcome-based electric-submersible-pump agreement in December 2025 that includes local manufacturing capacity. Local fabricators benefit from the USD 6.6 billion in-country-value program that targets 40% localization of midstream capex by 2030, pressuring import margins for foreign suppliers but shortening project delivery.

Emerging opportunities exist in subsea equipment for offshore blocks, thermal recovery for heavy oil, and integrated digital platforms that bundle subsurface modeling, surface automation, and carbon dashboards, with operators awarding multi-year extensions to vendors that deliver measurable cost or recovery gains. Decommissioning specialists with environmental remediation credentials gain share as the Burgan field approaches eight decades of production and abandonment liabilities rise.

Kuwait Oil And Gas Industry Leaders

-

Kuwait Petroleum Corporation

-

Chevron Corporation

-

BP PLC

-

Schlumberger NV

-

Petrofac Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: KPC is in preliminary discussions to sell a USD 7 billion stake in its crude oil pipelines. Prominent investors, including BlackRock, Brookfield, and EIG, have expressed interest in the deal. This transaction would follow similar infrastructure deals in the Gulf region, aiding Kuwait’s financing requirements and supporting its long-term energy investment objectives.

- January 2026: Kuwait is preparing to sell a USD 7 billion stake in its pipeline network to attract foreign investment amidst declining oil revenues. Kuwait Petroleum Corporation (KPC) has engaged global investors and advisors to initiate the process. This move aligns with a broader Gulf trend of monetizing energy infrastructure to support economic diversification and fiscal stability. [energynow.com

- November 2025: KPC is expediting major subsidiary mergers and initiating a recruitment drive targeting Kuwaiti engineers to improve operational efficiency. The restructuring efforts aim to reduce costs, streamline operations, and support long-term production goals, reinforcing Kuwait’s strategy to strengthen its oil and gas sector.

- October 2025: Kuwait has announced a significant offshore gas discovery at the Jazah-1 well, with production exceeding 29 million cubic feet per day (mcf/d) and low impurity levels. The estimated reserves of 1 trillion cubic feet (tcf) align with KPC’s 2040 energy strategy, enhancing future gas capacity and bolstering national energy security through accelerated offshore development.

Kuwait Oil And Gas Market Report Scope

Oil and gas are defined as petroleum, natural gas, hydrocarbons, minerals, or any combination of them, and all substances developed from them. In the production and distribution of oil and gas, a number of complex processes and systems are employed, which require advanced technology and a large amount of capital. The Kuwait oil and gas market report scope includes:

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

How large is the Kuwait oil and gas market in 2026?

It is valued at USD 32.39 billion and is on course to reach USD 40.83 billion by 2031, reflecting a 4.74% CAGR.

Which segment grows fastest up to 2031?

Downstream, led by the Al-Zour refinery, is expanding at 6.18% CAGR as very-low-sulfur fuel oil exports widen margins.

What drives offshore investment?

Three frontier discoveries since 2024 and the Neutral-Zone redevelopment are pushing offshore capex higher at 7.1% CAGR.

How does OPEC+ policy affect Kuwait?

The 2.58 million-barrel-per-day quota limits output below sustainable capacity and costs roughly USD 1.3 billion in annual revenue for every 100,000 barrels curtailed.

What technology trends are shaping the sector?

Digital oilfields, AI-enabled well optimization, and outcome-based service contracts are cutting downtime and aligning vendor fees with production gains.

Where are new service opportunities emerging?

Decommissioning work, heavy-oil thermal projects, and localized midstream fabrication are the leading white-space segments through 2031.

Page last updated on: