Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

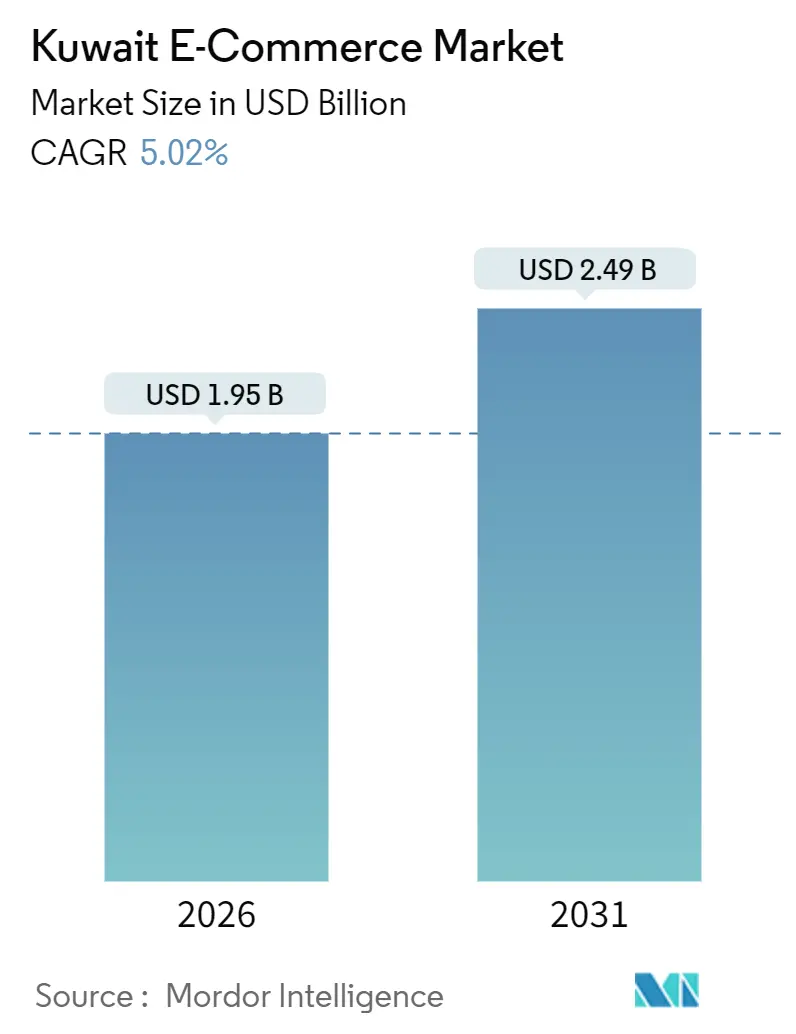

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

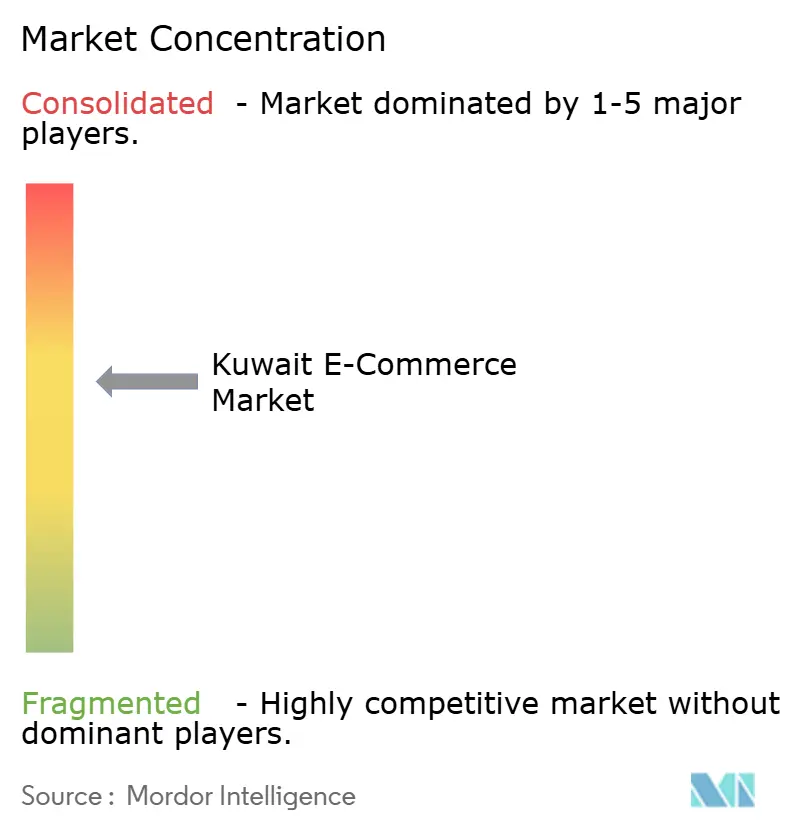

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait E-commerce Market Analysis by Mordor Intelligence

The Kuwait E-commerce Market size stood at USD 1.95 billion in 2026 and is projected to reach USD 2.49 billion by 2031, reflecting a 5.02% CAGR over the forecast period. A maturing digital retail environment now hinges on infrastructure upgrades, tighter regulation, and platform consolidation rather than first-wave adoption gains. Government mandates for e-invoicing, the cloud-first policy, and a comprehensive digital commerce law have formalized online transactions, lowering compliance risk for merchants and consumers alike. Domestic wallets tied to Kuwait Pay are scaling rapidly, while extensive 5G coverage enables live-stream shopping and augmented-reality product testing. Competitive strategies revolve around micro-fulfillment robotics, subscription monetization, and ad-tech revenue streams, which together sharpen unit economics and open fresh opportunities in underserved suburbs.

Key Report Takeaways

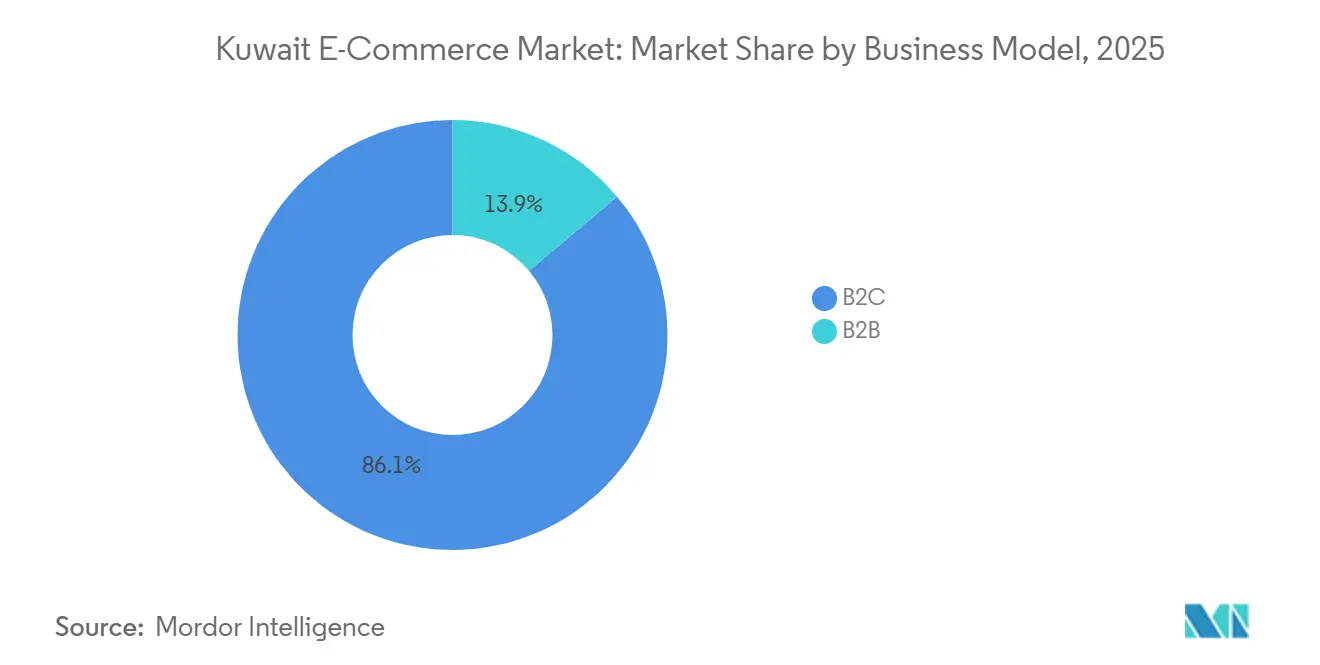

- By business model, business-to-consumer transactions led with an 86.12% share of the Kuwait E-commerce Market in 2025, while the B2B segment is forecast to expand at a 7.89% CAGR through 2031.

- By device type, smartphones captured 70.89% of the Kuwait E-commerce Market in 2025, and other connected devices are forecast to grow at an 8.17% CAGR to 2031.

- By payment method, cards held 50.23% of the Kuwait E-commerce Market in 2025, whereas digital wallets are set to climb at a 9.03% CAGR through 2031.

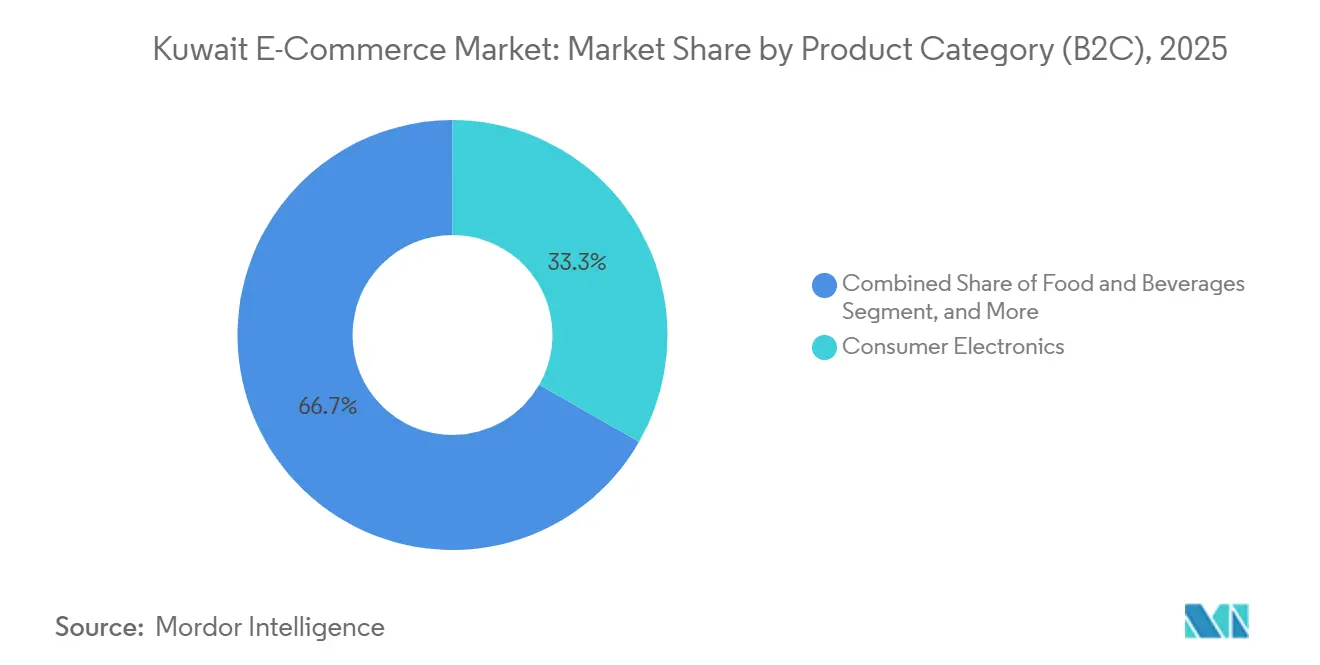

- By product category, consumer electronics accounted for 33.27% of the Kuwait E-commerce Market in 2025, yet food and beverages are projected to advance at a 9.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kuwait E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic digital-wallet surge | +1.2% | Al Asimah and Hawalli | Short term (≤ 2 years) |

| Quick-commerce dark-store expansion | +0.9% | Al Asimah, Hawalli, spillover to Al Farwaniyah | Medium term (2–4 years) |

| 2024 e-invoicing mandate | +0.7% | Nationwide, strongest in B2B segments | Medium term (2–4 years) |

| Nationwide 5G rollout | +0.6% | Urban governorates | Long term (≥ 4 years) |

| AI-driven Arabic personalization | +0.5% | Platform-dependent adoption | Long term (≥ 4 years) |

| Influencer live-stream commerce integration | +0.4% | Youth clusters in Al Asimah and Hawalli | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Domestic Digital-Wallet Surge Driven by Kuwait Pay

Instant interbank transfers via Kuwait Pay remove card-network fees, prompting merchants to promote wallet checkout aggressively. Digital-wallet payment value is rising annually as Tabby and Tamara embed buy-now-pay-later installments into checkout flows, capturing younger shoppers who favor interest-free plans.[1]Tabby, “Tabby Product Overview,” tabby.ai Regulatory updates by the Central Bank standardized authentication and liability, boosting merchant confidence.[2]Central Bank of Kuwait, “Regulations for Electronic Payment Transactions,” kuna.net.kw Cash on delivery has fallen to 20%, freeing working capital that merchants can redirect to inventory and marketing. High smartphone penetration in Al Asimah and Hawalli accelerates wallet adoption, and integration with the Sahel Business app normalizes digital payments for taxes, licenses, and fees, feeding a virtuous adoption loop.

Quick-Commerce Dark-Store Expansion in Kuwait City

Talabat’s grocery vertical grew significantly after integrating InstaShop, validating the multi-category playbook. Automated picking at Raha’s AutoStore site doubled order throughput and mitigated rising labor costs.[3]Swisslog, “AutoStore Robotics in Kuwait,” swisslog.com Operators are now piloting hybrid models that merge dark-store inventory with partner retail assortments to smooth demand swings. Early success in urban cores is encouraging expansion into Al Farwaniyah, where route density is lower, but real estate is cheaper, helping balance cost and coverage.

Mandated 2024 E-Invoicing Accelerates SME Onboarding

The Central Agency for Information Technology requires electronic invoices for all government suppliers, forcing thousands of SMEs to digitize accounting and payments. Platforms such as Z-HUB bundle e-invoicing, catalog listings, and procurement tools, cutting onboarding friction for wholesale sellers. Digitized invoices create audit trails that appeal to institutional buyers, reduce information asymmetry, and lay the groundwork for data-driven credit scoring. As B2B sellers comply, many also list goods on public portals, enlarging assortment and spurring price competition. Over the medium term, this formality is expected to narrow Kuwait’s SME productivity gap and raise the ceiling for digital-procurement volumes.

5G Rollout Enables Live Commerce and AR Shopping

Nationwide 5G coverage with sub-20 millisecond latency supports live-stream events where influencers demonstrate products and viewers purchase instantly. Chalhoub Group recorded a significant engagement from shoppable video among Gen Z beauty buyers. Retailers like H&M and IKEA Kuwait have piloted mobile augmented reality for virtual try-ons and room renders, cutting return rates. Edge computing on user devices allows recommendation models to run locally, aligning with Kuwait’s 2024 Personal Data Protection Law. In the long term, 5G unlocks bandwidth-intensive formats such as volumetric video and holographic product demos, further blurring the line between physical and digital retail.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile costs in low-density areas | -0.8% | Al Jahra, Al Ahmadi, Mubarak Al Kabeer | Medium term (2–4 years) |

| Cultural preference for cash on delivery | -0.5% | Nationwide, acute in Al Jahra and Al Farwaniyah | Short term (≤ 2 years) |

| Limited temperature-controlled warehousing | -0.4% | Nationwide, affects grocery and pharma | Long term (≥ 4 years) |

| Shortage of Arabic UX and CX specialists | -0.3% | Nationwide, platform-level | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Costs in Low-Density Governorates

Sparse street naming in outlying governorates forces couriers to rely on landmarks and phone calls, adding 5-10 minutes per stop and squeezing driver capacity. Platforms either raise fees or set high minimum-order thresholds, curbing demand in price-sensitive neighborhoods. Experiments with geo-fenced zones and dynamic pricing risk excluding fringe areas, sustaining a digital divide. Vision 2035 pledges standardized postal codes, yet timelines remain uncertain, so firms trial pickup lockers at petrol stations to offset routing inefficiencies. Until systemic fixes arrive, elevated last-mile costs will cap penetration outside urban cores.

Cultural Preference for Cash on Delivery

Though cash on delivery fell in 2023, many shoppers still prefer physical inspection before payment, especially in Al Jahra and Al Farwaniyah. Cash handling inflates logistics overhead, prolongs merchant settlement cycles, and fuels cancellation risk. Central Bank liability guarantees enhance trust in wallet payments, but behavioral inertia slows conversion. Platforms are testing partial deposits and post-delivery invoicing to hedge risk, while education campaigns highlight refund protection and one-tap re-ordering convenience. The shift away from cash will likely be gradual rather than abrupt.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Procurement Digitization Gains Momentum

The B2C segment controlled 86.12% of the Kuwait E-commerce Market in 2025, anchored by platforms that spent a decade honing logistics and brand equity. However, B2B sales are projected to grow 7.89% annually through 2031, lifted by mandatory e-invoicing and rising SME participation.[4]Zain Kuwait, “Z-HUB Business Solutions,” kw.zain.com This growth should expand the Kuwait E-commerce Market size for wholesale categories, as procurement departments embrace catalog automation and electronic payments. Platforms targeting industrial supplies leverage bulk-pricing engines and ERP integrations to shorten sourcing cycles, although longer sales funnels and credit-term negotiations remain hurdles.

Higher average order values, lower return rates, and data-rich transactions bolster B2B platform margins. Kuwait National Petroleum Company’s adoption of JAGGAER for refinery projects illustrates enterprise appetite for digital sourcing.[5]JAGGAER, “KNPC Procurement Success,” jaggaer.com Conversely, B2C platforms seek stickier economics via paid memberships like Talabat Pro and cross-category bundling, with advertising now contributing half of Talabat’s EBITDA. As platform competition intensifies, user segmentation and first-party data analytics will decide who wins incremental share.

By Device Type (B2C): Mobile Dominance with Emerging Interfaces

Smartphones accounted for 70.89% of consumer spending in 2025, reflecting ubiquitous 4G and 5G access. They also generated the most first-time conversions, underscoring the Kuwait E-commerce Market share lead for mobile channels. Yet tablets, smart TVs, and voice assistants are forecast to post an 8.17% CAGR as shoppable live streams and connected-home commands catch on. These interfaces will gradually expand the Kuwait E-commerce Market size as households buy through multiple screens.

Second-screen behavior is commonplace: customers discover products on smart-TV streams, save them on mobile wishlists, then finalize payment on desktops to apply corporate discounts. Seamless session syncing and biometric single-tap checkout are therefore critical. Platforms circumvent app-store fees by nudging users to the mobile web for final payment, while augmented-reality previews reduce return rates. Voice commerce in Arabic is nascent but benefits from investments in natural-language processing and local payment rails.

By Payment Method (B2C): Cards Still Rule but Wallets Surge

Cards retained 50.23% of payment value in 2025, benefiting from decades-old trust in K-Net as well as global Visa and Mastercard rails. Digital wallets, however, are scaling fastest and will likely account for a growing slice of the Kuwait E-commerce Market size as BNPL services mitigate affordability barriers. Wallet growth hinges on real-time transfers, fee savings, and buyer protections that mirror card-scheme chargebacks.

Cash on delivery’s share continues to slide, but its persistence complicates dynamic pricing and personalization, which rely on instant payment confirmation. Closed-loop balances such as Talabat Credit encourage prepaid spending and capture float. For platforms, maximized payment optionality is vital; Checkout.com data show frequency lifts when customers save credentials for one-tap reorders, reinforcing loyalty and repeat purchase rates.

By Product Category (B2C): Electronics Lead while Groceries Accelerate

Electronics held a 33.27% revenue share in 2025, driven by smartphone upgrades and smart-home adoption. In turn, food and beverages are forecast to rise at a 9.47% CAGR, the fastest among major categories, expanding the Kuwait E-commerce Market size for high-frequency purchases. Quick-commerce dark stores and integrated grocery tabs inside food-delivery apps compress delivery times and increase basket stickiness.

Fashion, beauty, and furniture occupy mid-tier shares yet present unique logistics and return-rate challenges. Boutiqaat’s content-commerce model, featuring 650 influencers, boosts engagement and conversion for beauty SKUs. Furniture sellers offset bulky-item friction with AR previews and BNPL plans. The category mix will keep evolving as platforms extend into high-frequency essentials to lift lifetime value.

Geography Analysis

Al Asimah and Hawalli, where smartphone penetration is high, anchor most platform innovation, including 15-minute grocery service and live-stream shopping. Route density and real estate economics justify dense micro-fulfillment networks, which in turn enlarge the Kuwait E-commerce Market size in these governorates. Al Farwaniyah shows rising adoption as operators balance delivery times against lower fees, aided by shared logistics across adjacent districts.

Al Ahmadi, with its oil-sector camps and expatriate enclaves, exhibits mixed adoption: affluent compounds spend heavily online, while outer zones face navigation issues that inflate last-mile costs. Al Jahra’s vast area but low density curbs quick-commerce viability; pickup points at petrol stations help maintain service coverage without prohibitive per-order costs. Mubarak Al Kabeer mirrors Farwaniyah’s trajectory with steady gains tied to broader payment acceptance.

The International Telecommunication Union ranks Kuwait in its Advanced tier for digital development, ensuring that all six governorates benefit from robust network infrastructure. Yet socio-demographic gaps in digital skills leave lower-income, older, and non-national citizens under-represented online, limiting the addressable base. Public-private initiatives targeting affordable broadband and digital literacy can unlock latent demand and expand the Kuwait E-commerce Market share beyond affluent urban cores.

Competitive Landscape

The market is moderately concentrated. Talabat leads food delivery, broadened by its USD 360 million InstaShop acquisition that increased grocery penetration. Amazon and Noon contest general merchandise with cross-border fulfillment, while local players such as Boutiqaat and Raha carve niches in beauty and micro-fulfillment. Talabat’s December 2024 IPO, which sold a 15% stake, financed ad-tech and robotics, enabling half of adjusted EBITDA to come from advertising rather than commissions.

Delivery Hero absorbed Carriage, illustrating consolidation pressure on mid-tier specialists. Fresh white-space remains in B2B procurement, cold-chain logistics, and Arabic AI personalization, areas where scale platforms hold capital but nimble entrants can differentiate. Regulatory tightening around data protection and cybersecurity favors well-funded firms able to shoulder compliance costs, raising the barrier for smaller startups. Strategic emphasis now lies on subscription monetization, multi-vertical bundling, and infrastructure automation to widen margins and extend geographic reach.

Kuwait E-commerce Industry Leaders

Apparel Group FZ-LLC – 6thStreet.com

Namshi General Trading LLC

H&M Hennes and Mauritz AB

Ubuy Inc.

Noon AD Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deliveroo began onboarding former Cari users after the competing app’s exit, expanding both merchant roster and customer base in Kuwait.

- November 2025: Kuwait enacted a comprehensive digital commerce law that clarified consumer rights, merchant duties, and dispute mechanisms, encouraging cross-border sellers.

- November 2025: The Kuwait Skills program launched with Microsoft and the Central Agency for Information Technology, aiming to train 30,000 employees in AI and cloud competencies.

- October 2025: DoorDash completed its takeover of Deliveroo’s international units, bringing new logistics algorithms and capital to Kuwait.

Kuwait E-commerce Market Report Scope

The Kuwait E-commerce Market is segmented into B2B E-commerce and B2C E-commerce. By B2C E-commerce, the market studied is further subdivided into beauty and personal care, consumer electronics, fashion and apparel, food and beverage, and furniture and home. The study also tracks important market metrics, underlying growth influencers, and significant industry vendors, providing support for Kuwait's market estimates and growth rates throughout the anticipated period.

The Kuwait E-commerce Market Report is Segmented by Business Model (B2C, B2B), Device Type (Smartphone/Mobile, Desktop and Laptop, Other Device Types), Payment Method (Credit and Debit Cards, Digital Wallets, Buy Now Pay Later, Other Payment Methods), Product Category (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, Toys DIY and Media, Other Product Categories), and Geography (Al Asimah, Hawalli, Al Farwaniyah, Al Ahmadi, Al Jahra, Mubarak Al Kabeer). The Market Forecasts are Provided in Terms of Value (USD).

By Business Model

| B2C |

| B2B |

By Device Type (B2C)

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method (B2C)

| Credit and Debit Cards |

| Digital Wallets |

| Buy Now Pay Later (BNPL) |

| Other Payment Methods |

By Product Category (B2C)

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

| By Business Model | B2C |

| B2B | |

| By Device Type (B2C) | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method (B2C) | Credit and Debit Cards |

| Digital Wallets | |

| Buy Now Pay Later (BNPL) | |

| Other Payment Methods | |

| By Product Category (B2C) | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

Key Questions Answered in the Report

What is the 2026 revenue of the Kuwait e-commerce sector?

The Kuwait E-commerce Market size reached USD 1.95 billion in 2026.

How fast is online grocery growing in Kuwait?

Food and beverage sales are projected to expand at a 9.47% CAGR through 2031, the fastest among major categories.

Which payment method is gaining most rapidly in Kuwait’s digital retail?

Digital wallets tied to Kuwait Pay are rising at a 9.03% CAGR, outpacing cards and cash.

Why are dark stores important for Kuwait’s quick-commerce model?

They allow 15- to 30-minute fulfillment in dense districts while lowering real-estate costs compared with high-street frontage.

What regulatory change most affects B2B e-commerce adoption?

The 2024 e-invoicing mandate compels SMEs to digitize invoices and payments, driving platform onboarding.

Which governorates show the strongest online shopping activity?

Al Asimah and Hawalli lead due to dense populations, high smartphone penetration, and extensive 5G coverage.

Page last updated on: