Container Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

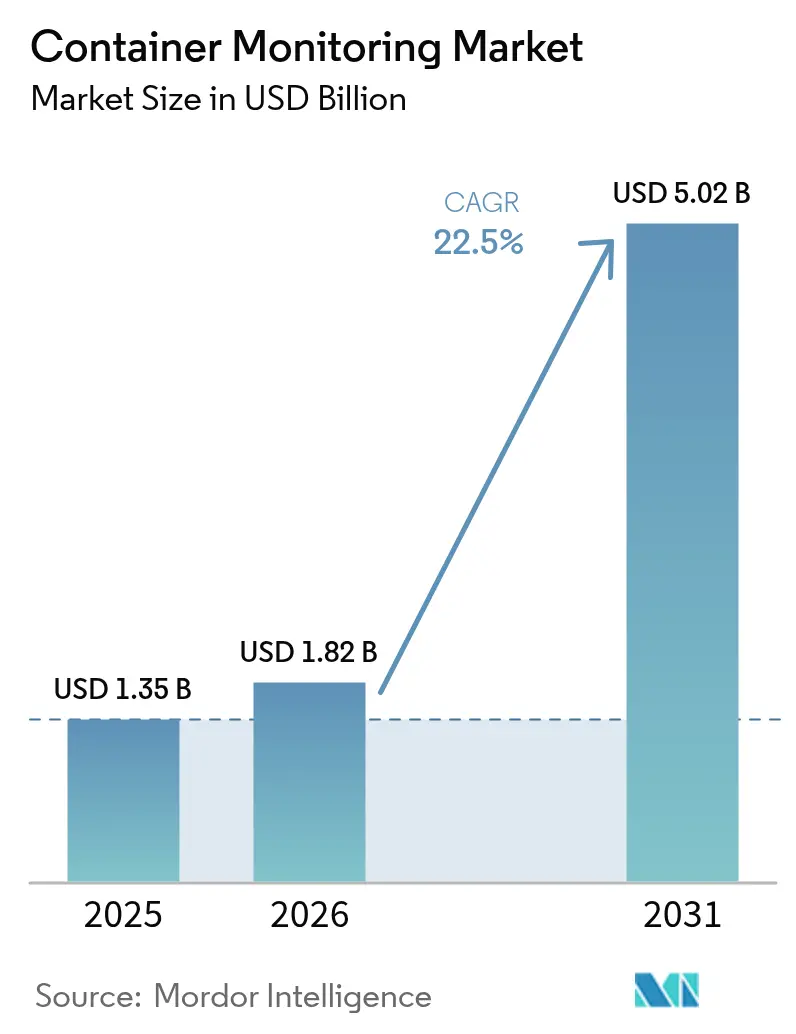

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 22.50% CAGR |

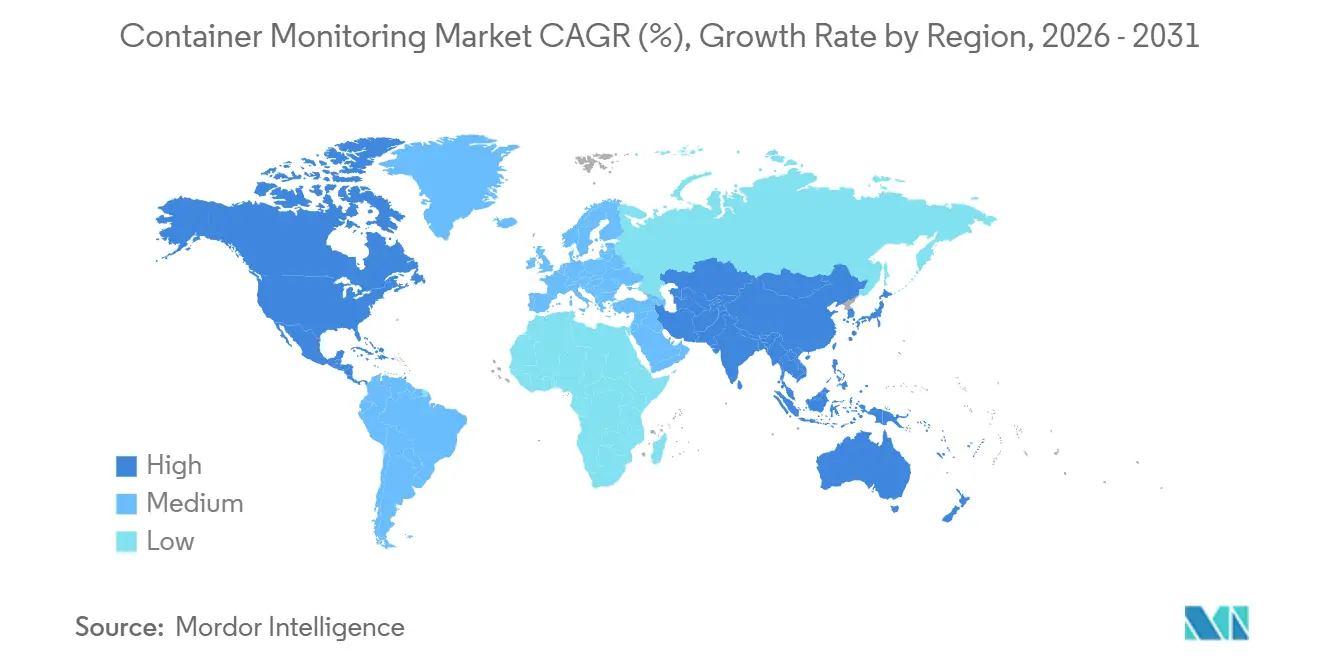

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

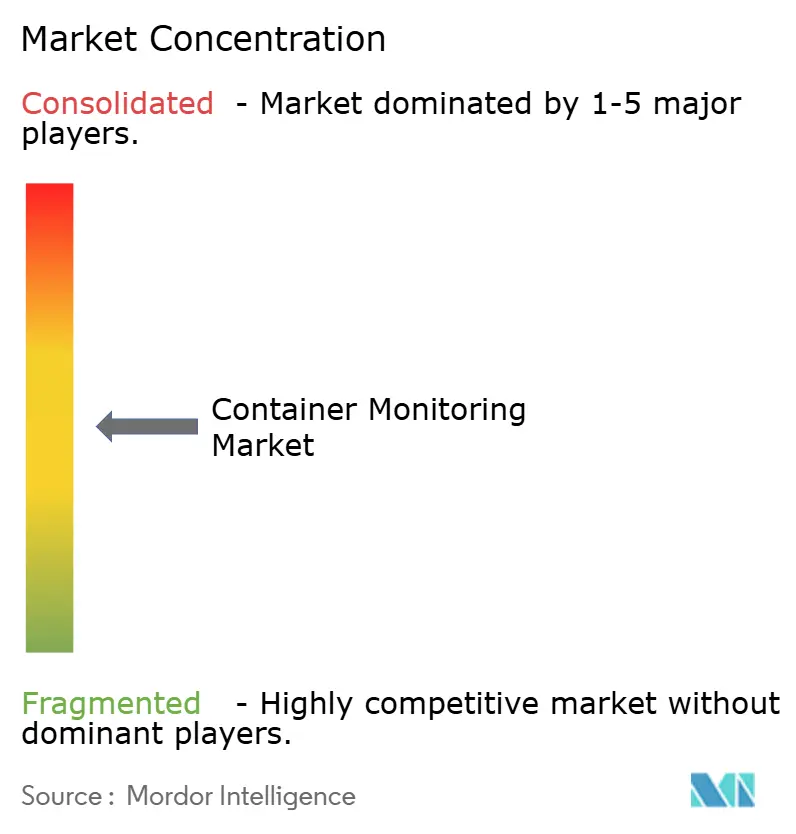

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Container Monitoring Market Analysis by Mordor Intelligence

The container monitoring market size is projected to expand from USD 1.35 billion in 2025 and USD 1.82 billion in 2026 to USD 5.02 billion by 2031, registering a CAGR of 22.5% between 2026 and 2031. Rapid migration from virtual machines to containerized microservices is amplifying the volume, velocity, and variety of telemetry, creating urgent demand for platforms that correlate metrics, logs, and traces in near-real time. eBPF-powered instrumentation now captures kernel-level events with negligible CPU overhead, enabling sub-second latency visibility across short-lived pods while lowering data-ingest bills. FinOps teams increasingly tag cost metrics at the container layer, uncovering stranded resources and driving automated rightsizing. Compliance frameworks such as the Digital Operational Resilience Act and HIPAA have begun to require continuous workload monitoring, further accelerating tool adoption. Competition centers on AI-assisted root-cause analysis, open-standards telemetry pipelines, and pricing models that align vendor revenue to customer consumption.

Key Report Takeaways

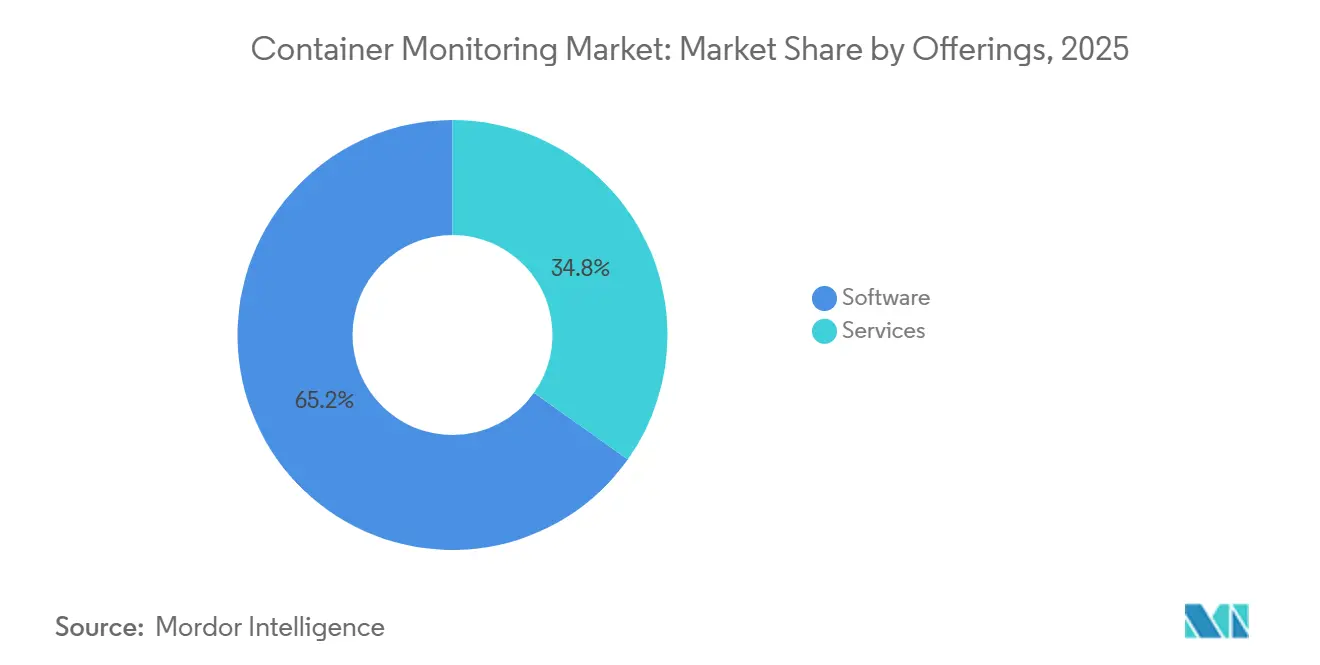

- By offerings, software captured 65.18% of container monitoring market share in 2025, services are forecast to outpace all other offerings at a 22.83% CAGR through 2031.

- By deployment model, cloud-based solutions held 57.83% of the container monitoring market size in 2025, whereas hybrid architectures are advancing at a 22.58% CAGR over 2026-2031.

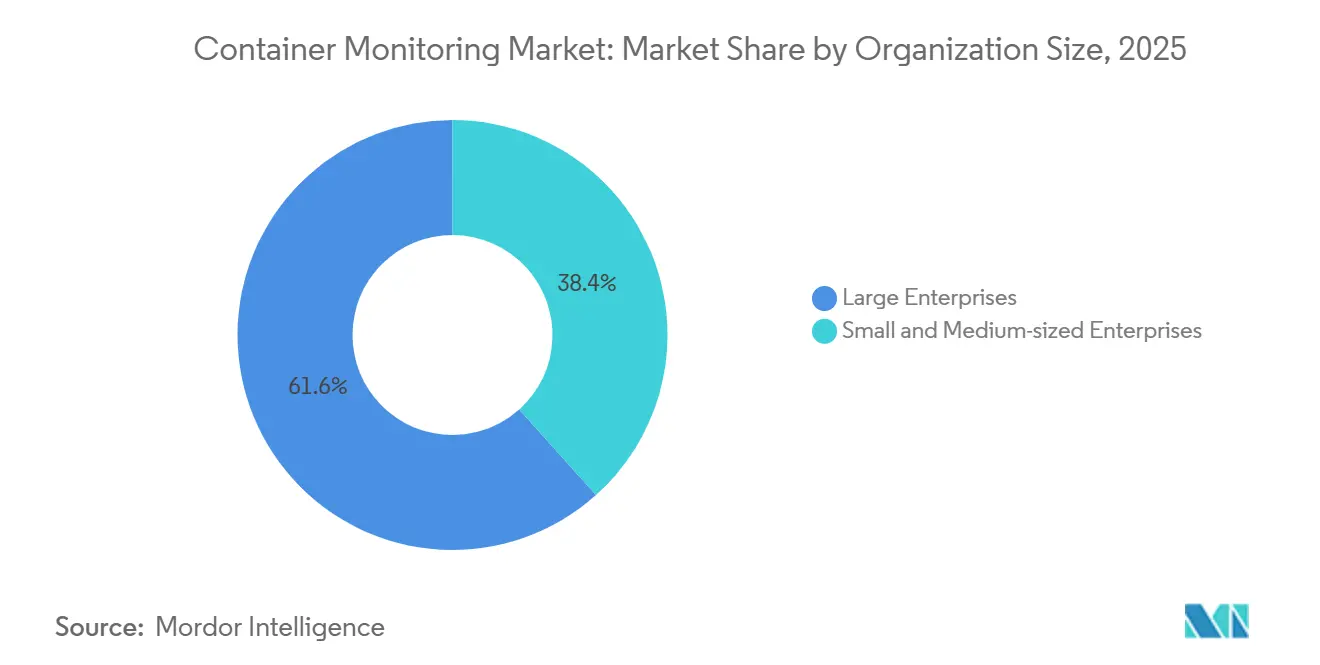

- By organization size, large enterprises accounted for 61.64% of 2025 spend, while small and medium-sized enterprises are expanding at 22.91% during the forecast window.

- By container platform, Kubernetes led with 72.93% container monitoring market share in 2025, yet HashiCorp Nomad is projected to grow at 22.52% CAGR through 2031.

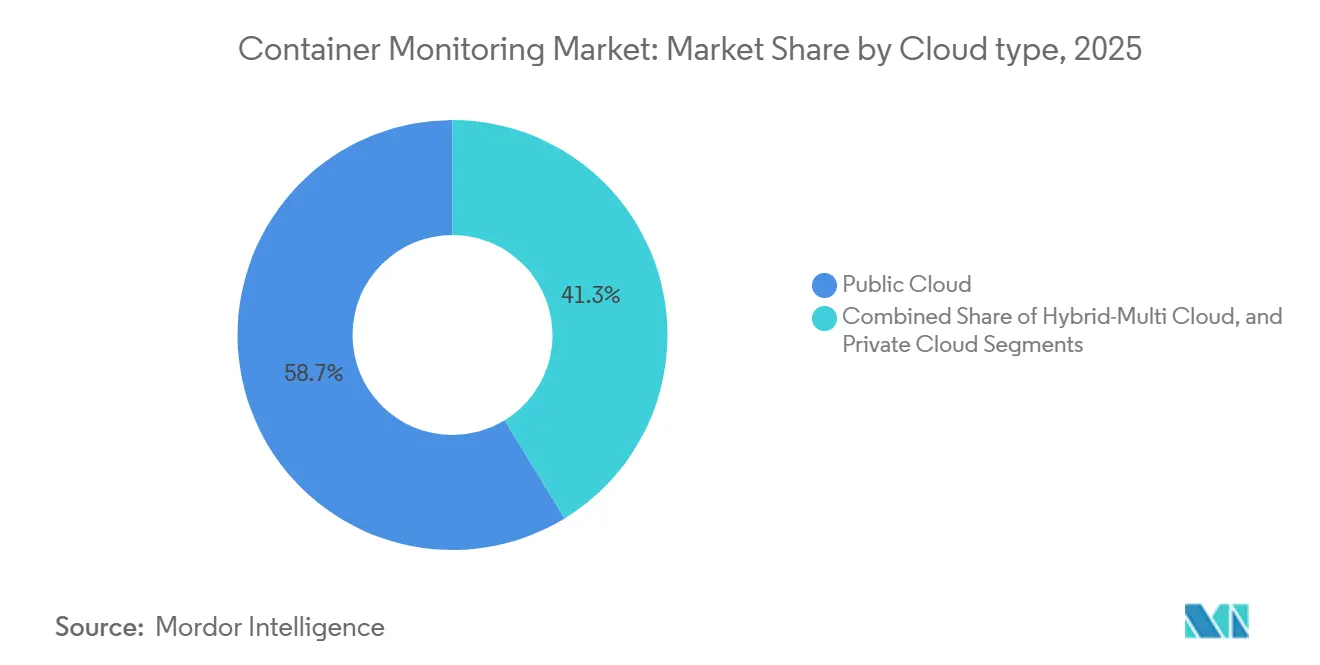

- By cloud type, public cloud deployments represented 58.74% of revenue in 2025; hybrid multi-cloud is the fastest sub-segment at 23.02% CAGR to 2031.

- By end-user industry, IT and telecom delivered 31.68% of 2025 revenue, whereas healthcare and life sciences is poised for the highest 23.16% CAGR through 2031.

- By geography, North America commanded 31.94% of the 2025 container monitoring market; Asia-Pacific is forecast to advance at a 23.61% CAGR across the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Container Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Based Services | +4.2% | North America, Asia-Pacific | Medium term (2-4 years) |

| Proliferation of Micro-Services Architecture | +3.8% | Global (IT and telecom, retail) | Medium term (2-4 years) |

| DevOps Shift-Left Culture Driving Continuous Monitoring | +3.5% | North America, Europe | Short term (≤ 2 years) |

| Rising Compliance and Container-Security Mandates | +3.1% | Europe, North America | Long term (≥ 4 years) |

| eBPF-Enabled Deep, Low-Overhead Observability | +2.9% | Global (early U.S. adoption) | Short term (≤ 2 years) |

| FinOps Cost-Optimization Pressures at Container Level | +2.7% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud-Based Services

Managed Kubernetes services—Amazon EKS, Azure AKS, and Google GKE—eliminate control-plane upkeep yet introduce highly ephemeral workloads that traditional agents cannot follow. Cloud-native collectors based on OpenTelemetry discover pods automatically and attach trace context without recompilation, giving teams end-to-end visibility even as clusters autoscale. Multi-cloud deployment spreads risk and bargaining power but splinters telemetry formats, prompting demand for unified dashboards with schema-normalization layers. Consumption-based pricing further lowers entry barriers, letting organizations meter observability spend in lockstep with actual resource usage.

Proliferation of Micro-Services Architecture

Breaking monoliths into dozens of loosely coupled services multiplies network hops and failure points. A single e-commerce checkout can now traverse inventory, payments, shipping, and notification microservices, all orchestrated in separate pods. Distributed tracing injects unique identifiers into every request, while service-mesh sidecars such as Istio propagate that context across languages. The Cloud Native Computing Foundation recorded that 61% of enterprises run containers in production, up from 49% two years earlier, underscoring the irreversible march toward microservices.[1] Cloud Native Computing Foundation, “CNCF Annual Survey 2024,” cncf.io

DevOps Shift-Left Culture Driving Continuous Monitoring

Continuous integration pipelines now gate production deployments on performance budgets as strictly as on functional tests. Synthetic traffic replay in staging flags telemetry regressions early, cutting mean time to resolution. NIST SP 800-190 recommended embedding vulnerability scans and runtime policy enforcement into build workflows, leading DevOps teams to treat observability configurations as version-controlled code.[2]National Institute of Standards and Technology, “SP 800-190: Application Container Security Guide,” nist.gov The approach trims post-production firefighting and elevates monitoring from reactive insurance to proactive quality control.

eBPF-Enabled Deep, Low-Overhead Observability

Extended Berkeley Packet Filter programs run inside the Linux kernel, capturing syscalls, network packets, and file I/O with <1% CPU overhead. Vendors such as Grafana Labs and Datadog employ eBPF to auto-instrument even closed-source binaries, slashing rollout friction.[3]Grafana Labs, “Introducing Grafana Beyla,” grafana.com Security teams leverage the same hooks to enforce zero-trust egress policies at the socket layer without decrypting payloads, satisfying privacy rules in finance and healthcare. Kernel-level insight marries infrastructure and application telemetry on a unified clock, sharpening root-cause correlation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tool-Chain Complexity and Skills Gap | –2.8% | Global (acute in emerging markets) | Medium term (2-4 years) |

| Escalating Telemetry Storage and Licensing Costs | –2.3% | Global (SMEs hardest hit) | Short term (≤ 2 years) |

| Shortage of Container-Observability Talent | –1.9% | North America, Europe | Long term (≥ 4 years) |

| Data-Sovereignty Limits on Cross-Border Telemetry Flows | –1.6% | Europe, Middle East, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tool-Chain Complexity and Skills Gap

Many enterprises juggle Prometheus metrics, Elasticsearch logs, and Jaeger traces in bespoke pipelines that break whenever an API version shifts. Kubernetes itself imposes a steep learning curve—network policies, persistent volumes, sidecar proxies—so few engineers can also fine-tune high-cardinality dashboards. Reliance on multiple user interfaces fragments incident response, prolonging outages and dampening enthusiasm for broader rollouts.

Escalating Telemetry Storage and Licensing Costs

High-cardinality labels such as pod_name, customer_id, or git_sha explode time-series cardinality, generating terabytes per day in large clusters. ISPs charge egress fees, vendors meter ingest bytes, and auditors demand multi-year retention, pushing observability bills beyond infrastructure budgets. Downsampling alleviates cost but loses granularity precisely when root-cause clues hide in outlier traces. The tension forces teams to prioritize mission-critical workloads, leaving blind spots in less visible services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offerings: Services Scale as Complexity Outpaces DIY Skills

Services are projected to expand at 22.83% CAGR through 2031, edging above the overall container monitoring market size trajectory despite software’s 65.18% revenue lead in 2025. Organizations increasingly outsource deployment, tune anomaly-detection models, and manage alert fatigue, freeing developers to focus on feature velocity. eBPF-based agents cut software footprint, but the know-how to operationalize them still commands premium consulting rates.

Annual renewals reveal that customers stick with managed engagements once service-level objectives improve; churn falls sharply when vendors own 24/7 runbooks. Integrators bundle observability-as-code templates in Git, aligning dashboard changes with the same peer-review gates that govern application releases. This governance best practice, initially seeded by service partners, often becomes institutionalized, widening the moat for providers.

By Deployment Model: Hybrid Bridges Compliance and Cloud Economics

Hybrid environments are advancing at 22.58% CAGR, closing the gap with cloud-native modes that held 57.83% share in 2025. Financial firms governed by the Digital Operational Resilience Act keep raw payment traces on-premise but burst aggregated metrics into cloud AI engines for predictive scaling. Edge proxies perform local downsampling to meet air-gap rules in defense and critical infrastructure.

Public cloud dominates greenfield projects thanks to zero-maintenance control planes and granular cost tagging. Yet rising egress charges and sovereignty laws nudge even start-ups toward hybrid setups, especially once monthly cloud bills surface line items for telemetry storage that rival compute spend. Vendors respond with tiered storage—hot data in-memory, warm data on object stores, cold data compressed on cheaper archival layers.

By Organization Size: SMEs Leverage Managed Kubernetes to Level the Field

Small and medium-sized enterprises are tracking a 22.91% CAGR, slightly eclipsing large-enterprise growth despite controlling only 38.36% of 2025 spend. Turnkey Kubernetes clusters, provisioned via web console and billed per-node-hour, let lean teams deploy without hiring platform engineers. Consumption-priced observability pairs seamlessly, offering entry tiers that include 10,000 span-per-minute quotas at no charge.

Large enterprises, however, still drive absolute dollars, stitching multiple clusters across regions for disaster recovery. They demand single-pane role-based access control and integration with ticketing systems, features that skew R&D roadmaps toward enterprise SKUs. Vendors thus segment their catalogues—SME SaaS plans with click-to-connect wizards, and enterprise on-premise offerings with Hardware Security Module support.

By Container Platform: Kubernetes Hegemony Faces Edge-Centric Nomad Surge

Kubernetes owned 72.93% of 2025 workloads, cementing its role as the default orchestrator. Yet HashiCorp Nomad’s lightweight binary and Consul/Vault integration fuel 22.52% CAGR at the edge, where air-gapped oil rigs or retail kiosks lack the resources for a multi-component control plane. Docker Swarm continues a gentle decline as organizations rewrite legacy stacks for Helm chart portability.

Monitoring vendors prioritize Kubernetes operators—custom resource definitions that deploy DaemonSets for collectors and manage automatic upgrades—thereby deepening lock-in. Nomad-first providers carve a niche with compact binaries and offline-friendly license servers. Apache Mesos remains a specialist option for mixed big-data and container scheduling but shows little incremental net-new adoption.

By Cloud Type: Hybrid Multi-Cloud Complexity Elevates Single-View Dashboards

Public clouds retained 58.74% of 2025 spend, driven by managed services and global network reach. Hybrid multi-cloud is the bright spot, advancing at 23.02% as firms split workloads across Amazon, Microsoft, and Google to curb vendor power and meet jurisdictional rules. Private clouds persist in defense and national-critical sectors, yet most roadmap discussions now assume eventual cloud adjacency for analytics layers.

Unified observability renders cloud heterogeneity invisible. OpenTelemetry collectors normalize Amazon CloudWatch logs, Google Cloud Operations metrics, and Azure Monitor traces before forwarding them to a central lake. This abstraction cushions provider switches and clarifies cost attribution, feeding FinOps dashboards that rebalance workloads according to spot-instance arbitrage.

By End-User Industry: Compliance-Driven Healthcare Outpaces High-Tech Pioneers

Healthcare and life sciences top the growth chart at 23.16% CAGR, spurred by HIPAA mandates for immutable audit trails on patient-data flows. Containerized Electronic Health Record modules now emit structured traces, writing protected health information hashes rather than plaintext identifiers, which satisfy privacy audits while enabling root-cause triage.

IT and telecom dominated 2025 revenue at 31.68%, reflecting streaming-media carbohydrate spikes and SaaS platform ubiquity. Financial institutions embed latency Service Level Objectives in payment gateways—sub-100 ms end-to-end times are no longer aspirational but published regulatory thresholds. Retail-e-commerce leans on auto-scaling to weather Black Friday bursts; observability drives capacity rightsizing that saves millions in over-provisioned nodes. Manufacturing deploys ruggedized clusters on factory floors, marrying OT sensor feeds with IT analytics to predict equipment failure in seconds, not hours.

Geography Analysis

North America held 31.94% of 2025 revenue, anchored by Silicon Valley cloud natives and Wall-Street fintechs that run thousands of clusters across availability zones. United States federal agencies adopted Kubernetes Security Benchmarks in 2025, compelling prime contractors to include real-time monitoring in project bids. Canada’s major banks mirror these controls, while Mexico’s automotive plants implement edge collectors that buffer traces during intermittent connectivity, uploading once bandwidth frees overnight.

Asia-Pacific is racing ahead at a 23.61% CAGR to 2031. China’s sovereign-cloud edicts propelled domestic providers to embed observability agents as default add-ons, turning monitoring into a bundled utility rather than an upsell. India’s Digital Personal Data Protection Act limits metric egress, so hyperscalers opened regional zones with in-country storage tiers, immediately lifting container monitoring market size in Bangalore and Hyderabad. Japan’s Industry 4.0 factory retrofits require latency dashboards for robotic cells; South Korea’s telcos bake monitoring SLAs into 5G slicing contracts.

Europe’s trajectory aligns more with regulatory cadence than pure tech enthusiasm. The Digital Operational Resilience Act, live since January 2025, obligates financial entities to stress-test IT systems under live-production loads, creating a hard mandate for granular telemetry. Germany’s auto giants monitor over-the-air software updates for millions of vehicles, pushing petabyte-scale trace stores. France and the United Kingdom emphasize data residency, turning to regional cloud resellers certified under ISO 27001 to host telemetry lakes. The Middle East and Africa lag on absolute spend but post double-digit growth where sovereign-funded hyperscale builds in Riyadh and Abu Dhabi demand certified observability stacks.

Mordor Intelligence provides coverage of the container monitoring market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Container monitoring adoption is increasingly shaped by security and resilience rules that call for continuous visibility into containerized workloads. In the United States, NIST SP 800-190 (Application Container Security Guide) is widely used as a baseline for container security practices, including centralized monitoring of image compliance and runtime controls in DevSecOps pipelines. In Europe, the EU Cyber Resilience Act (Regulation 2024/2847) sets horizontal cybersecurity requirements for products with digital elements and introduces vulnerability reporting obligations starting September 11, 2026, with full enforcement on December 11, 2027. That timetable increases the importance of automated detection, evidence capture, and auditable response workflows in container environments.

Compliance requirements also influence how telemetry is collected, stored, and shared across borders and regulated sectors. ETSI EN 304 635 provides a voluntary conformity standard aligned to the CRA for virtualization and container execution stacks, while organizations operating under data residency and sovereignty constraints tend to rely on in-region storage and controlled telemetry pipelines. Globally recognized standards such as ISO/TS 18625:2017 for container tracking and monitoring systems reinforce a broader shift toward standardized monitoring data models, supporting open schemas and repeatable controls across distributed environments.

Value Chain Analysis

The value chain begins with data generation across orchestrators and runtimes (notably Kubernetes), application frameworks, service meshes, and the Linux kernel, then moves into collection and normalization layers that increasingly standardize on OpenTelemetry and Prometheus conventions. Instrumentation can include agents, eBPF-based sensors, sidecars, and managed collectors, while telemetry pipelines handle filtering, sampling, enrichment (tags, cost attributes, ownership), and routing to storage and analytics. Storage and query layers span metrics (time series), logs (indexed and searchable), and traces (distributed tracing), with cost controls implemented via tiered retention, aggregation, and downsampling to manage high-cardinality data.

Downstream, analytics and workflow integration turns telemetry into operational outcomes through alerting, SLO management, incident response, and remediation automation integrated into DevOps toolchains and cloud consoles. Hyperscaler marketplaces and managed Kubernetes services function as key distribution channels, reducing procurement friction and supporting cloud-based deployments, while systems integrators and managed service providers deliver implementation, tuning, and 24/7 operations that help offset skills gaps. Recent platform moves, such as AWS adding OpenTelemetry-based Container Insights for Amazon EKS (June 2026) and real-time deployment observability in the Amazon ECS Management Console (July 2026), show cloud providers pulling observability deeper into their control planes, reshaping how third-party vendors differentiate through advanced analytics, unified views across hybrid multi-cloud, and AI-assisted investigation.

Competitive Landscape

Incumbent APM vendors, cloud-native disrupters, and open-source guardians share the battlefield. Datadog, Dynatrace, Splunk, New Relic, and Cisco’s AppDynamics bundle AI assistants that surface anomalous golden signals—latency, traffic, errors, saturation—without custom queries. Grafana Labs and Elastic steward communities around open dashboards and query languages, monetizing through hosted SaaS tiers with enterprise support. Sysdig and Aqua pivot from container security to runtime visibility, offering single agents that stream both security and performance events.

Partner ecosystems matter as much as feature checklists. Hyperscalers list third-party collectors in their marketplaces, enabling click-through procurement that bypasses lengthy vendor-risk reviews. OpenTelemetry breaks data-format lock-in, forcing vendors to differentiate on analytics sophistication and workflow integration rather than proprietary protocols. Price—for-value trends downward as entrant startups court cost-sensitive SMEs with “always-free” ingestion thresholds and per-span billing.

Consolidation is inevitable: heavyweights acquire niche compression engines or edge-collector start-ups to close multi-cloud gaps. Yet open source remains a potent counterweight, with CNCF incubating projects that commoditize yesterday’s premium features. Talent scarcity keeps managed-service revenue buoyant; enterprises gladly offload 24/7 telemetry plumbing to specialists, especially when every minute of SRE time saved translates into new customer-facing releases.

Container Monitoring Industry Leaders

Datadog, Inc.

Dynatrace, LLC

Splunk Inc.

New Relic, Inc.

Sysdig, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is consolidation of fragmented observability stacks into unified, standards-based deployments, since many organizations still run multiple parallel toolchains across metrics, logs, and traces. CNCF noted this operational reality in 2026 with practitioner survey data showing 46.7% of organizations operate two to three observability stacks, while only 7.4% report a unified experience. That fragmentation supports opportunities for vendors and service partners that can deliver OpenTelemetry-native pipelines, schema normalization, and governance patterns (observability-as-code, RBAC, auditability) across Kubernetes-heavy and hybrid multi-cloud estates.

Standards maturity and compliance drivers are also shifting buyer requirements toward portable telemetry and auditable security controls. OpenTelemetry reached CNCF graduation in July 2026, reinforcing it as a de facto interoperability layer for container monitoring across AWS, Azure, and Google Cloud and supporting broader adoption of vendor-neutral collection with differentiated downstream analytics. In parallel, regulations such as the EU Cyber Resilience Act introduce time-bound vulnerability reporting obligations beginning September 11, 2026, which pushes demand for monitoring that links runtime signals to vulnerability management evidence and incident workflows. Together, these forces increase interest in investigation features, eBPF-based low-overhead collection for ephemeral workloads, and FinOps-aligned telemetry that ties cost and performance attribution to container and namespace levels for day-to-day engineering decisions.

Recent Industry Developments

- July 2026: AWS added real-time deployment observability capabilities to the Amazon ECS Management Console to track deployment health, failures, and task status. By embedding deployment telemetry into a primary operations surface, the move reduces reliance on separate tooling for first-level triage and tightens the feedback loop for teams running containerized services at scale.

- April 2026: Dynatrace acquired Bindplane to strengthen open-standards telemetry pipeline capabilities across logs and metrics. The addition supports OpenTelemetry-centric data routing and control, helping enterprises manage ingest costs and normalize container telemetry across hybrid and multi-cloud environments.

- November 2025: Grafana Labs unveiled Grafana Cloud Kubernetes Monitoring, a managed Prometheus-compatible offering with pre-built dashboards for common failure modes. The release expanded managed options for Kubernetes observability and reinforced the shift toward hosted monitoring bundles that reduce operational overhead for platform teams.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the container monitoring market covers software and related services that track the health, performance, and availability of containerized applications and their supporting layers (such as clusters, nodes, and container runtimes) across cloud, on-premises, and hybrid environments.

Scope exclusions: Container security, CI/CD build tools, and generic infrastructure monitoring that does not provide container-level visibility are excluded from the scope.

Segmentation Overview

- By Offerings

- Software

- Services

- By Deployment Model

- Cloud-based

- On-Premise

- Hybrid

- By Organization Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By Container Platform

- Kubernetes

- Docker Swarm

- Apache Mesos

- HashiCorp Nomad

- Other Runtimes

- By Cloud Type

- Public Cloud

- Private Cloud

- Hybrid Multi-Cloud

- By End-User Industry

- IT and Telecom

- BFSI

- Retail and E-commerce

- Manufacturing and Industrial

- Healthcare and Life Sciences

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for containerized workloads and cloud-native adoption, then mapping that demand to what organizations actually purchase as container monitoring software and services. We refer to public and official sources such as the US Bureau of Labor Statistics, US Census Bureau, Eurostat, OECD ICT indicators, and ITU statistics to anchor macro and digitalization signals that influence enterprise software spend.

To keep assumptions grounded, we also review company filings, earnings transcripts, investor presentations, and reputable press coverage to understand packaging changes, service attach patterns, and regional demand differences. When needed, we use paid subscriptions for company financials and intelligence, patent databases, and news and financials to check product positioning and pricing direction without relying on any single narrative. These sources are not exhaustive, and other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what desk sources cannot show clearly, including typical contract structures, adoption timing, and how budgets are split between platform engineering and central IT. We spoke with a mix of solution providers, channel partners, system integrators, and enterprise users across APAC, EMEA, and the Americas, then rechecked key assumptions when responses differed by industry or deployment preference.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 50% |

| Mid tier: 58% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 16% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing uses a top-down model where enterprise software and cloud spend signals are filtered into an addressable container monitoring pool using adoption and usage indicators. Inputs we track include Kubernetes and other runtime adoption, the share of applications deployed in containers, the cloud versus on-premises mix, typical monitoring tool penetration by organization size, and how spending shifts between software subscriptions and services.

Those totals are then checked using selective bottom-up approximations, such as sampled vendor revenue cues, channel checks, and an ASP-times-deployed-workload logic where data is available. When the bottom-up view is incomplete for smaller regions or newer use cases, we scale from verified deployment ratios and revalidate with interview feedback so gaps do not inflate the outcome.

For forecasting, we use scenario analysis because adoption rates, pricing, and cloud migration speed can change quickly. Scenarios are linked to practical drivers like container workload growth, platform standardization cycles, and managed services expansion, and the final forecast follows the scenario set that experts say best matches current buying behavior.

Data Validation & Update Cycle

Validation is done by comparing outputs against independent signals, including software spend trends, cloud adoption indicators, and observed shifts in platform tooling priorities. Outliers are flagged at the region and offering level, then assumptions are revisited until the variance can be explained by a real market driver rather than a modeling artifact.

Before sign-off, the model and the story go through a multi-step internal review, where key calculations are checked and the logic is challenged for edge cases. If new information materially changes pricing, adoption, or regulation-related spending, experts are re-contacted and the impacted parts are recalculated. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Container Monitoring Market Size Compared With Other Published Estimates

Published market values for container monitoring often differ because the scope is not always consistent, and base year and currency timing can change the starting point. Variance also comes from how firms treat services, how they count hybrid deployments, and whether they model demand from container workload growth or from broader observability spending.

Container security and broader application performance monitoring suites that are not container-specific sit outside Mordor Intelligence's container monitoring scope, which can pull its number away from studies that blend adjacent observability categories. Differences also show up when a publisher uses a more aggressive scenario for Kubernetes-led adoption, applies a faster ASP progression, or does not separate software from services cleanly in the build-up.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.35 B (2025) | |

| Global Consultancy A | USD 0.89 B (2024) | Uses an earlier base year and appears to treat parts of the market as a narrower tooling category, which can undercount service revenue and multi-cloud hybrid deployments. |

| Industry Publisher B | USD 0.33 B (2025) | Runs a longer forecast window with a tighter definition and fewer counted buying groups, which typically reduces the starting market size even if the growth rate looks healthy. |

The table indicates that most of the spread comes from scope and starting year, followed by how software and services are counted in hybrid environments. By anchoring the size to observable workload adoption inputs and then cross-checking with practical spend signals from interviews, the final estimate stays explainable and repeatable for decision-making.

Key Questions Answered in the Report

How large will the container monitoring market be by 2031?

The container monitoring market size is forecast to reach USD 5.02 billion by 2031.

Which segment is growing fastest within container observability?

Services are projected to expand at a 22.83% CAGR, the highest among all offerings.

Why are healthcare companies investing heavily in container monitoring?

HIPAA audit-trail mandates require immutable, real-time visibility into patient-data flows, driving a forecast 23.16% CAGR for healthcare and life sciences workloads.

What role does eBPF play in modern observability?

EBPF runs inside the Linux kernel, capturing low-level events with <1% CPU overhead, enabling deep yet efficient container visibility.

How are hybrid multi-cloud strategies influencing monitoring tool choice?

Hybrid multi-cloud’s 23.02% CAGR fuels demand for platforms that normalize telemetry across AWS, Azure, and Google Cloud while keeping regulated data in-region.

Page last updated on: