KSA Satellite Communications Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

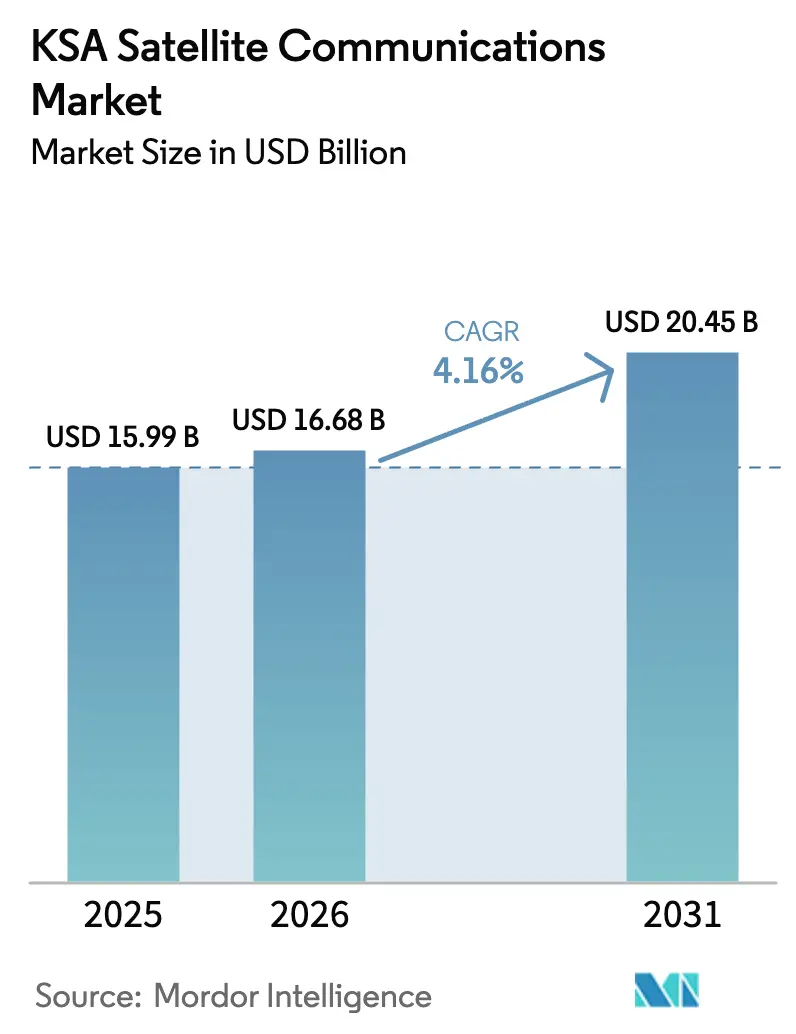

| Base Year Market Size (2025) | USD 15.99 Billion |

| Market Size (2026) | USD 16.68 Billion |

| Market Size (2031) | USD 20.45 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

KSA Satellite Communications Market Analysis by Mordor Intelligence

The KSA satellite communications market size is projected to expand from USD 15.99 million in 2025 and USD 16.68 million in 2026 to USD 20.45 million by 2031, registering a CAGR of 4.16% between 2026 and 2031. Sturdy government spending on space capabilities, heightened cybersecurity standards, and the search for resilient connectivity in offshore and border regions keep demand growing even as fiber-to-the-home and 5G fixed-wireless networks blanket most urban centers. Enterprises with remote operations now treat satellite capacity as an operational necessity rather than a last-resort back-up, while hybrid non-terrestrial architectures begin to emerge as an accepted extension of cellular coverage. Incumbent geostationary operators are refreshing fleets with Ka-band payloads to defend broadcast and enterprise contracts, whereas low-earth-orbit entrants court mobile-backhaul and defense users that value low latency. Together, these shifts give the KSA satellite communications market room to expand at a measured but durable pace through 2031.

Key Report Takeaways

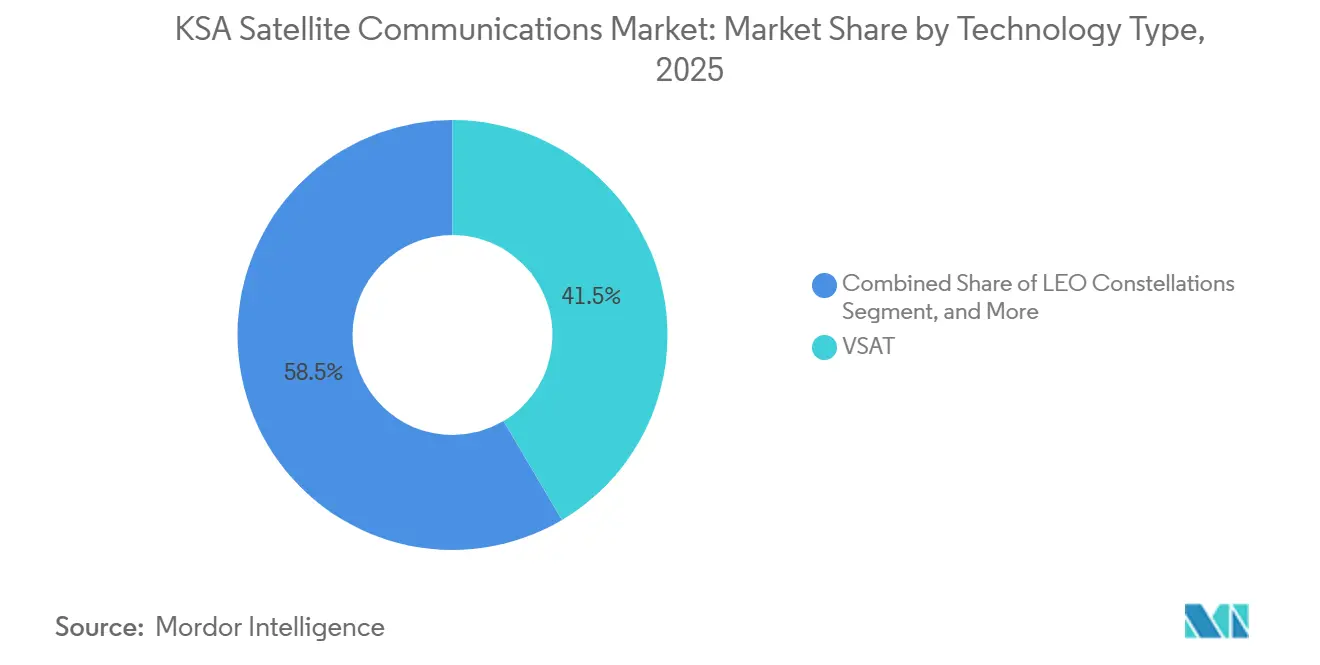

- By technology type, VSAT systems held 41.49% of the KSA satellite communications market share in 2025, while low-earth-orbit constellations are forecast to post the fastest 4.89% CAGR through 2031.

- By frequency band, Ku-band led with 45.56% revenue share in 2025; Ka-band adoption is advancing at a 4.56% CAGR to 2031.

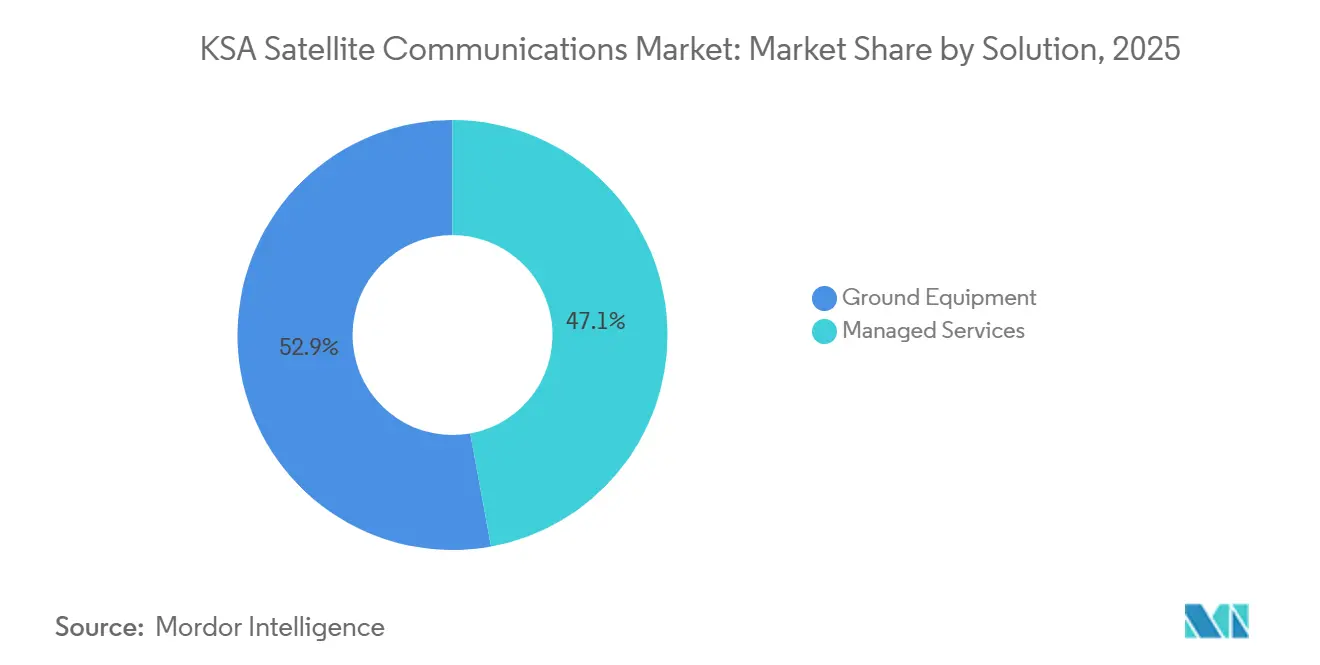

- By solution, managed services captured 52.86% revenue in 2025 and are projected to maintain 4.94% annual growth through 2031.

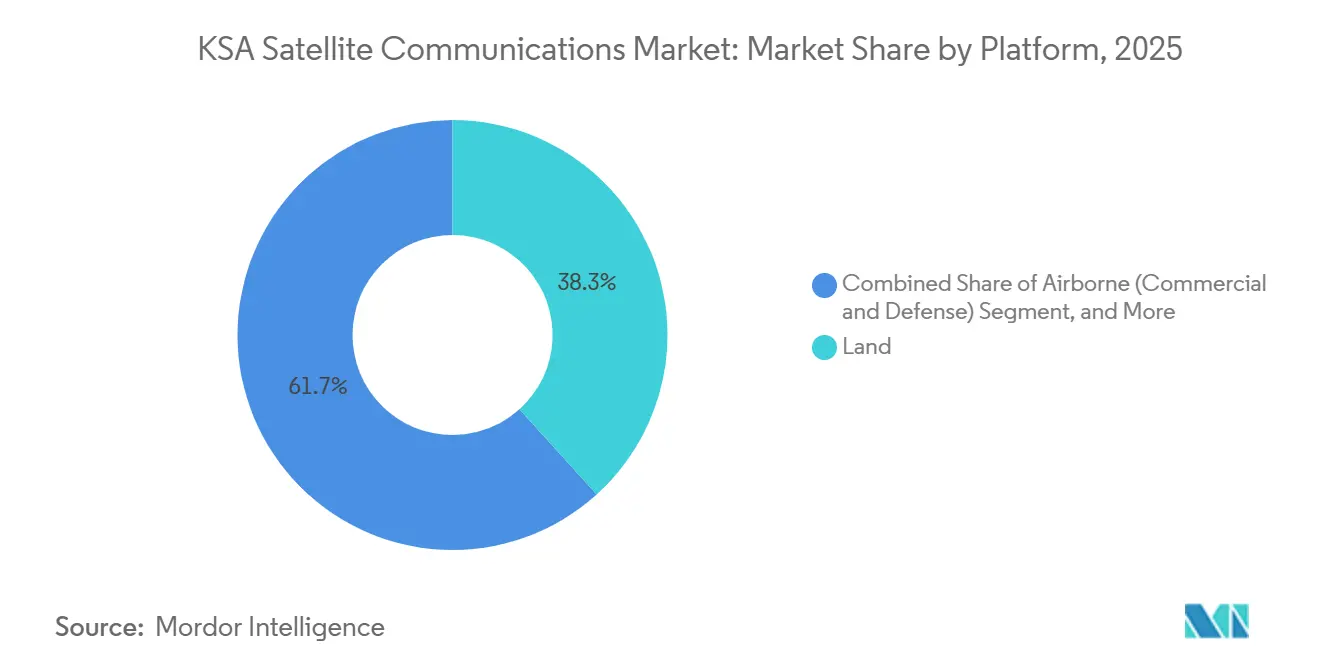

- By platform, land installations accounted for 38.29% of 2025 deployments, whereas airborne systems are set to record the highest 5.13% CAGR over 2026-2031.

- By end-user vertical, maritime applications held 30.74% share in 2025, yet defense and government demand is rising fastest at a 5.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

KSA Satellite Communications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Demand for Ubiquitous Broadband Connectivity | +1.20% | National, with concentration in Eastern Province oil fields, Red Sea maritime corridors, and Northern Border regions | Medium term (2-4 years) |

| Government Investment Under Vision 2030 and KSA Space Strategy | +1.00% | National, anchored by Riyadh PIF investments and Saudi Space Authority programs | Long term (≥ 4 years) |

| Digital-First Shift in Oil and Maritime IoT Back-Haul | +0.80% | Eastern Province (Aramco operations), Red Sea offshore platforms, Suez Canal approaches | Medium term (2-4 years) |

| Planned Saudi Sovereign LEO Constellation (Neo Space Group) | +0.60% | National, with early commercial focus on government and enterprise segments | Long term (≥ 4 years) |

| Mandatory Redundancy After 2021 Gulf Cable Outages | +0.40% | National, with acute demand in Jeddah, Dammam, and maritime operators | Short term (≤ 2 years) |

| HAPS Integration Requiring Satellite Gateway Backhaul | +0.20% | Pilot zones in Western and Central regions (Riyadh, Jeddah corridors) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Demand for Ubiquitous Broadband Connectivity

Mobile data consumption reached 48 gigabytes per subscriber each month in 2025, triple the global average, underscoring the limits of terrestrial coverage in offshore fields, shipping lanes, and desert borders.[1]SAMENA Council, “CST Issues the Saudi Internet Report 2024,” samenacouncil.org The Communications, Space and Technology Commission now emphasizes technology-neutral licensing, allowing operators to stitch together cellular, fixed-wireless, and satellite links within a single network framework.[2]GSMA, “Roadmaps for Awarding 5G Spectrum,” gsma.com Oil platforms located beyond 50 kilometers from shore, Red Sea vessels transiting the Suez Canal, and surveillance posts along 4,000 kilometers of frontier all require connectivity that fiber economics cannot justify, so multi-orbit satellite solutions are filling the gap. The World Bank notes that digital services already contribute 15% of the Kingdom’s non-oil GDP, making any data outage commercially painful.[3]World Bank, “Gulf Economic Update: The Gulf’s Digital Transformation,” worldbank.org As a result, enterprises willingly pay a premium for resilient bandwidth that meets strict service-level targets, keeping satellite demand healthy even where terrestrial density rises.

Government Investment Under Vision 2030 And KSA Space Strategy

Neo Space Group’s formation in 2024 and its inaugural LEO launch expanded the domestic space economy to USD 8.7 billion that year, and public forecasts suggest USD 31.6 billion by 2035.[4]Space in Africa, “Saudi Arabia’s Neo Space Group Successfully Launches First Satellite,” spaceinafrica.com Royal decrees empower the Saudi Space Authority to execute international cooperation and ensure sovereignty over critical communications channels. Vision 2030 earmarks satellite links for the hardest-to-serve 10% of the population while funnelling capital into secure ground segments that meet National Cybersecurity Authority standards. National AI and data center programs, funded at USD 10 billion, replicate datasets across distant clusters and thus lean on high-throughput satellite backhaul for redundancy. Collectively, these policies guarantee a steady pipeline of long-term government and enterprise contracts for compliant operators.

Digital-First Shift in Oil and Maritime IoT Back-Haul

Saudi Aramco operated roughly 400 VSAT links across its offshore network by 2025 and began trailing OneWeb LEO capacity for latency-sensitive sensor traffic. GHGSat collaboration adds real-time methane monitoring, blending earth-observation payloads with Ka-band gateways for rapid data relay. In shipping, multiple Red Sea cable cuts during 2024-2025 forced operators to install satellite redundancy as insurers began requiring dual-path connectivity. Economic losses from a single offshore production outage can exceed USD 1 million daily, dwarfing the annual service fee for a dedicated Ka-band link, so CFOs increasingly treat satellite contracts as risk-mitigation tools. KAUST labs are meanwhile prototyping phased-array terminals that can operate across 7-24 gigahertz, a step toward local manufacturing that may reduce import tariffs over time.

Planned Saudi Sovereign LEO Constellation

The sovereign constellation under Neo Space Group aims to mesh directly with terrestrial 5G cores using non-terrestrial network protocols now under CST review, enabling seamless handoffs along 4,000 kilometres of sparsely populated borders. Early design targets call for at least 24 polar-orbit satellites and inter-satellite laser links to guarantee national coverage, with KAUST research supporting sub-terahertz phased-array ground stations. Exclusive government and defense contracts will insulate the program from consumer pricing pressures and provide immediate anchor tenancy. Diplomatic channels opened by Royal Decree M/24 help negotiate cross-border spectrum entries, reducing collision risk with neighbouring filings. If launch cadence holds, the constellation could deliver sovereign secure links by late 2027, boosting long-term momentum for the KSA satellite communications market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and Spectrum-Allocation Delays | -0.50% | National, with bottlenecks in CST spectrum-coordination processes | Medium term (2-4 years) |

| Competition From Fiber and 5G Terrestrial Roll-Outs | -0.70% | Urban centers (Riyadh, Jeddah, Dammam) and Vision 2030 fiber-priority zones | Short term (≤ 2 years) |

| Import Duties on Satellite Ground-Equipment Components | -0.30% | National, affecting all operators sourcing non-GCC equipment | Short term (≤ 2 years) |

| Shortage of Ka/Ku-Band RF Installation Talent | -0.20% | National, acute in Eastern Province and remote project sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory And Spectrum-Allocation Delays

CST licensing still trails operator application by 18-24 months, a lag mismatched to LEO production cycles and high-altitude platform schedules. Mid-band reorganization to favour 5G imposed exclusion zones within 50 kilometres of major cities, constraining earth-station siting. Operators contemplating USD 50-200 million gateway hubs hesitate without multiyear spectrum certainty. Absent formal redundancy mandates for critical infrastructure, uptake remains driven by voluntary risk assessments. This policy ambiguity subtracts 0.5 percentage points from forecast CAGR, tempering near-term enthusiasm in the KSA satellite communications market.

Competition From Fiber And 5G Terrestrial Rollouts

Fixed-broadband penetration is on track for a 12.9% CAGR to 2030 as fiber and 5G FWA blanket urban zones. Operators collectively invested more than USD 746 million during the first nine months of 2025 to extend terrestrial reach, effectively reserving satellite links for the residual 10% of households plus niche industrial sites. Residential customers view fiber as the default, forcing satellite providers to compete on total cost of ownership through bundled managed services. Because CST favours efficient spectrum use for terrestrial networks, satellite offerings must prove unique mobility or sovereignty benefits to secure long-term contracts. These factors shave 0.7 percentage points off the growth trajectory for the KSA satellite communications market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type – Sovereign LEO Ambitions Challenge VSAT Incumbency

VSAT terminals generated 41.49% of revenue in 2025, reflecting legacy Ku-band infrastructure across offshore rigs and government teleports. Although this base remains sticky, the KSA satellite communications market size tied to low-earth-orbit constellations is projected to expand at a 4.89% CAGR through 2031 as Neo Space Group launches additional spacecraft and as stc prepays USD 175 million for AST SpaceMobile direct-to-device links. Medium-earth-orbit services, led by SES O3b mPOWER, occupy a latency niche beneath 150 milliseconds attractive to fintech and defense missions. Direct-to-home broadcasting, once dominant, now contracts as IPTV substitutes grow in urban households.

Operators that pair GEO broadcast efficiency with LEO latency through intelligent traffic steering already win renewed enterprise contracts. ARABSAT’s BADR-8 Ka-band payload demonstrates this hybrid push while retaining GEO economics. Over the forecast period, VSAT vendors must pivot toward Ka-band and offer upgrade paths into multi-orbit packages or risk erosion of their installed base. In parallel, LEO providers require dense ground-station footprints, favouring telecom incumbents with existing tower and fiber assets. This competitive shuffle ensures the KSA satellite communications market keeps technology diversity even as LEO growth accelerates.

By Frequency Band – Ka-Band Ascendance Driven by Throughput Economics

Ku-band still commanded 45.56% revenue during 2025, underpinned by mature VSAT fleets across Aramco, maritime, and governmental users. Yet Ka-band contributes the strongest incremental dollar growth, rising at 4.56% annually as operators chase tenfold capacity per satellite and smaller 0.75-meter user terminals that face lower import duty. L-band preserves a narrowband niche for handheld safety services, whereas emergent Q/V-band appears in experimental backhaul links and inter-satellite lasers.

The mid-band spectrum clean-up that relieved 3.5 gigahertz for 5G already forced some satellite earth stations into power-flux density limits, signalling similar trade-offs ahead for Ka-band allocations. Operators thus race to lock gateways before tighter regulations bite. ARABSAT’s Ka-band migration for 5G backhaul shows how GEO incumbents protect share, while KAUST research on 7-24 gigahertz phased arrays tackles the skills gap that slows large-scale rollouts.

By Solution – Managed Services Dominate for Complexity Mitigation

Managed offerings represented 52.86% of 2025 revenue and are forecast to grow 4.94% yearly as enterprises convert capex into predictable opex through capacity leasing, remote monitoring, and SLA-wrapped maintenance. This shift aligns with KPMG findings that 94% of Saudi organizations favour as-a-service procurements. The KSA satellite communications market size is tied to ground-equipment sales, therefore grows more slowly, and suppliers face lumpy demand cycles.

Import levies of 5% duty and 15% VAT plus SASO certification add roughly 20-25% to antenna and modem costs, lengthening procurement by up to 90 days. Operators that absorb these hurdles and deliver turnkey service tap latent demand among oil and maritime players who prefer not to carry inventory. As domestic assembly emerges, especially through KAUST-backed phased-array initiatives, hardware lead times may compress, but managed services are expected to retain the majority share in the KSA satellite communications market.

By Platform – Airborne Systems Rise on Defense Modernization

Land installations contributed 38.29% of active sites in 2025, spanning gateway teleports, fixed enterprise dishes, and data-center uplinks. Maritime users followed, buoyed by compulsory redundancy after high-profile Red Sea cable cuts. Airborne platforms, though smaller in base, will post the quickest 5.13% CAGR through 2031 as business jets, surveillance drones, and fast-jet fleets install low-profile antennas for beyond-line-of-sight data.

Starlink’s May 2025 regulatory green light for aviation and maritime connectivity positions SpaceX to capture early airborne share. Stratospheric platforms trailed by Airbus and Salam also rely on satellite backhaul and could create fresh demand for Ka-band gateways. Meanwhile, a shortage of certified RF technicians in remote oil fields constrains land-platform upgrades, nudging enterprise customers toward managed fleets with remotely steered antennas.

By End-User Vertical – Defense Surges Beyond Maritime Growth

Maritime operators accounted for 30.74% of 2025 spend, sustained by shipping lines that cross the Kingdom’s Red Sea corridor and by offshore rigs that need continuous telemetry. Yet defense and government verticals are forecast to add revenue fastest, expanding 5.24% annually through 2031 as sovereign LEO capacity and SATCOM-on-the-move systems become budget priorities. Oil, gas, and energy customers keep baseline demand steady through VSAT refreshes and emissions monitoring. Media and entertainment continues to decline in absolute revenue as IPTV substitutes advance, though live-event news gathering sustains niche purchases.

High-throughput, low-latency links let border forces stream video from drones in real time, a capability impossible on legacy GEO circuits. Maritime insurers increasingly request dual-path proof, reinforcing subscription renewals. Corporate CIOs still procure satellite for disaster recovery because 66% reported chronic IT disruptions in KPMG’s 2025 poll. Collectively, these patterns keep the KSA satellite communications market balanced between steady maritime revenue and accelerating defense contracts.

Geography Analysis

Eastern Province anchors the highest site density because Saudi Aramco’s headquarters in Dhahran and hundreds of offshore platforms require resilient links for production control and methane analytics. Oil majors layer LEO back-haul on legacy Ku-band VSAT to cut latency for edge computing at wellheads. CST spectrum rules restrict high power emissions near Dammam and Jubail, encouraging operators to deploy low-profile Ka-band terminals on floating installations where terrestrial reach ends.

Red Sea coastal cities such as Jeddah and Yanbu form the second-largest demand cluster. Shipping companies, port authorities, and the NEOM construction program rely on satellite redundancy after repeated cable outages in 2024-2025 severed AAE-1 and EIG segments. High-altitude platform trials over these corridors also depend on satellite gateways to relay wide-area imagery, boosting regional bandwidth sales. Hybrid terrestrial-satellite handoff models, including stc’s direct-to-device roadmap, promise seamless coverage across mountainous terrain and archipelagos that fiber cannot economically reach.

Riyadh and central provinces generate specialized demand from government ministries and large data centers. HUMAIN’s AI compute clusters replicate datasets over multi-gigabit satellite trunks as part of disaster-resilient architecture. Northern Border regions with Iraq, Jordan, and Yemen rely almost entirely on satellite for real-time surveillance since 5G tower spacing exceeds 30 kilometers in desert terrain. Collectively, these geographic pockets keep the KSA satellite communications market diversified, lowering revenue concentration risk for operators.

Competitive Landscape

Regional incumbents ARABSAT and stc together hold the largest public sector and broadcast contracts, yet their combined share leaves ample room for aggressive international rivals. ARABSAT added Ka-band capacity through BADR-8 to defend enterprise accounts, while stc leveraged its tower network to sign a decade-long USD 175 million prepayment with AST SpaceMobile that couples satellite reach with existing mobile subscribers. International GEO giants SES, Intelsat, and Eutelsat promote multi-orbit portfolios that offload high-value, low-latency traffic onto LEO and keep bulk video on GEO, aiming to undercut pure-play LEO competitors on total cost of ownership.

Starlink entered the KSA satellite communications market in May 2025 with aviation and maritime licenses, immediately targeting oilfield helicopters and commercial shipping. Neo Space Group, backed by the Public Investment Fund, secures defense and sovereign traffic that foreign operators cannot handle due to data-sovereignty rules. Thuraya’s merger with Yahsat creates a combined L-band and Ka-band service set that challenges Inmarsat in handheld and activity-tracking niches.

Regulatory pressure favours terrestrial use of mid-band spectrum, compelling satellite players to refine interference mitigation and accept geographic exclusions. KAUST-driven efforts to localize phased-array manufacturing could lower ground-segment costs and help domestic integrators such as Mawarid Electronics and Detasad gain share. Operators offering turnkey managed services, embedded encryption, and quick-risk audits appeal to Saudi ICT managers who value third-party guidance, a trend that increasingly shapes contract awards.

KSA Satellite Communications Industry Leaders

Arab Satellite Communications Organization

Saudi Telecom Company (STC)

Thales Group

Salam (Integrated Telecom Company)

Thuraya Telecommunications Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SES closed a USD 3.1 billion deal to acquire Intelsat, creating a global multi-orbit platform.

- May 2025: Starlink secured aviation and maritime licenses to operate in the Kingdom.

- April 2025: Riyadh Air picked Viasat for gate-to-gate Ka-band IFC on its 787 fleet.

- March 2025: Arabsat debuted neXat managed services, moving beyond pure capacity leasing.

KSA Satellite Communications Market Report Scope

The KSA Satellite Communications Market Report is Segmented by Technology Type (VSAT, High-Throughput Satellites, LEO Constellations, MEO Constellations, Direct-to-Home Broadcasting), Frequency Band (L-Band, C-Band, Ku-Band, Ka-Band, Q/V and Optical), Solution (Ground Equipment, Managed Services), Platform (Portable/Man-Pack, Land, Maritime, Airborne), and End-User Vertical (Maritime, Defense and Government, Oil/Gas/Energy, Media/Entertainment, Financial/Corporate, Other). Market Forecasts are Provided in Terms of Value (USD).

| VSAT (Very Small Aperture Terminal) |

| High-Throughput Satellites (HTS) |

| Low-Earth-Orbit (LEO) Constellations |

| Medium-Earth-Orbit (MEO) Constellations |

| Direct-to-Home (DTH) Broadcasting |

| L-Band |

| C-Band |

| Ku-Band |

| Ka-Band |

| Q/V and Optical (Others) |

| Ground Equipment | Antennas and Terminals |

| Gateways and Hubs | |

| Modems and Routers | |

| Managed Services | Capacity Leasing |

| Support and Maintenance |

| Portable / Man-Pack |

| Land |

| Maritime |

| Airborne (Commercial and Defense) |

| Maritime |

| Defense and Government |

| Oil, Gas and Energy Enterprises |

| Media and Entertainment |

| Financial and Corporate Enterprises |

| Other End-User Vertical |

| By Technology Type | VSAT (Very Small Aperture Terminal) | |

| High-Throughput Satellites (HTS) | ||

| Low-Earth-Orbit (LEO) Constellations | ||

| Medium-Earth-Orbit (MEO) Constellations | ||

| Direct-to-Home (DTH) Broadcasting | ||

| By Frequency Band | L-Band | |

| C-Band | ||

| Ku-Band | ||

| Ka-Band | ||

| Q/V and Optical (Others) | ||

| By Solution | Ground Equipment | Antennas and Terminals |

| Gateways and Hubs | ||

| Modems and Routers | ||

| Managed Services | Capacity Leasing | |

| Support and Maintenance | ||

| By Platform | Portable / Man-Pack | |

| Land | ||

| Maritime | ||

| Airborne (Commercial and Defense) | ||

| By End-User Vertical | Maritime | |

| Defense and Government | ||

| Oil, Gas and Energy Enterprises | ||

| Media and Entertainment | ||

| Financial and Corporate Enterprises | ||

| Other End-User Vertical | ||

Key Questions Answered in the Report

How fast will the KSA satellite communications market grow through 2031?

Value is projected to reach USD 20.45 million by 2031, reflecting a 4.16% CAGR over 2026-2031.

Which segment expands quickest in the KSA satellite communications market?

Low-earth-orbit constellation services register the highest 4.89% CAGR due to sovereign launches and direct-to-device plans.

What drives enterprise demand for satellite links in Saudi Arabia?

Mandatory redundancy after cable outages, oil-field IoT, and government cybersecurity standards keep satellite bandwidth essential for risk mitigation.

Why is Ka-band gaining share?

Tenfold capacity per satellite, smaller antennas that lower import cost, and alignment with emerging LEO networks accelerate Ka-band uptake.

How do import duties impact ground-equipment pricing?

A 5% customs duty, 15% VAT, and SASO certification add roughly 20-25% to landed antenna and modem costs, encouraging managed-service adoption.

What role does Vision 2030 play?

Vision 2030 funds sovereign constellation programs and reserves satellite capacity for hard-to-serve regions, ensuring steady public-sector demand.

Page last updated on: