Kaposi Sarcoma Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 150.41 Million |

| Market Size (2031) | USD 183.34 Million |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

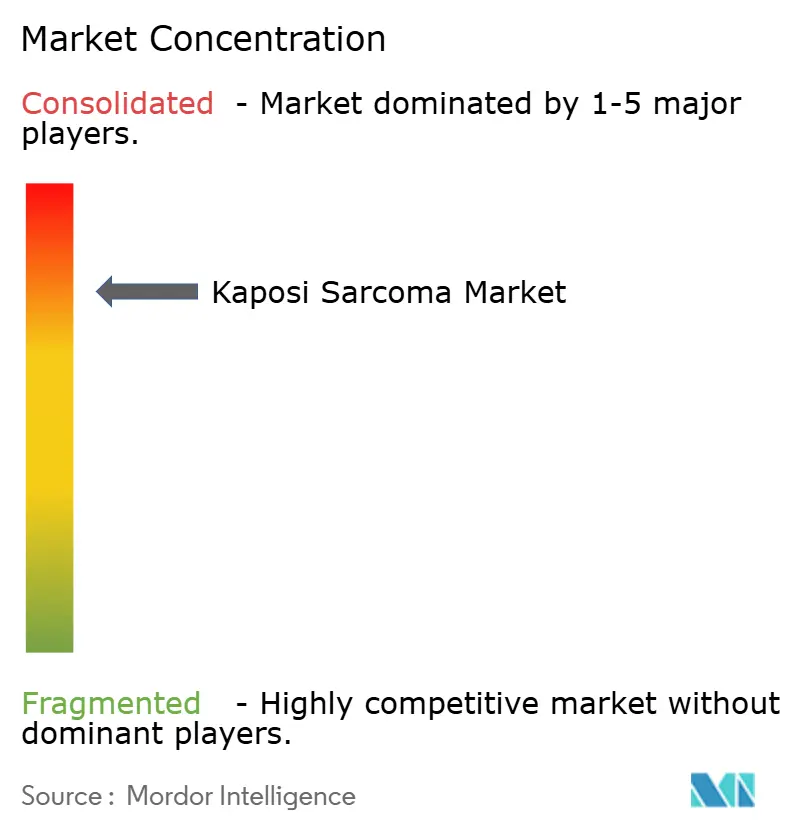

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kaposi Sarcoma Market Analysis by Mordor Intelligence

Kaposi's Sarcoma market size in 2026 is estimated at USD 150.41 million, growing from 2025 value of USD 144.57 million with 2031 projections showing USD 183.34 million, growing at 4.04% CAGR over 2026-2031. Demand is guided more by precision-medicine advances than by sheer patient volume, so growth remains steady rather than explosive. Rising incidence among immuno-compromised populations, wider use of pegylated liposomal anthracyclines, and pipeline immune-checkpoint inhibitors together reinforce this upward trajectory, while cold-chain gaps and reimbursement headwinds temper the pace. Consolidation among leading oncology businesses is intensifying, with big-ticket acquisitions exceeding USD 10 billion in 2024 alone. Simultaneously, cell-based gene therapies and AI-driven pathology platforms are shortening diagnostic lead-times, unlocking earlier intervention opportunities that further expand the addressable patient pool.

Key Report Takeaways

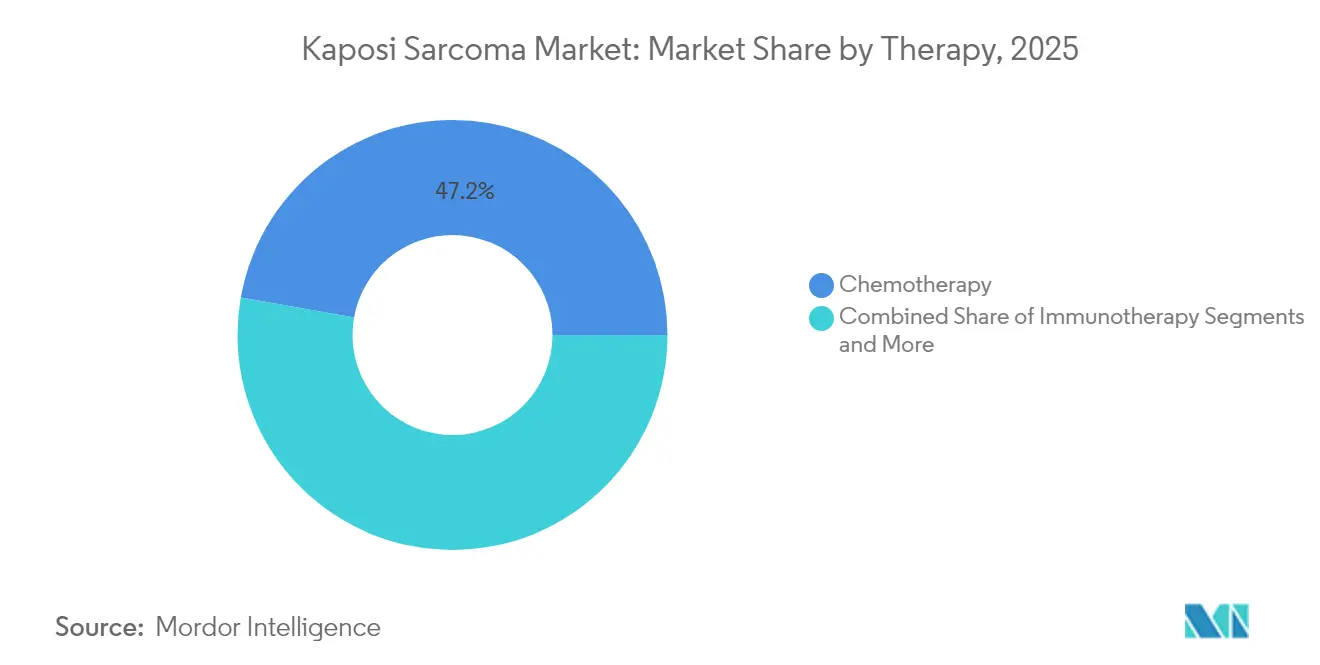

- By therapy, chemotherapy led with 47.21% of Kaposi's Sarcoma market share in 2025, while immunotherapy shows the fastest 5.26% CAGR through 2031.

- By route, intravenous products accounted for 61.55% of the Kaposi's Sarcoma market size in 2025; oral formulations are rising at a 5.64% CAGR to 2031.

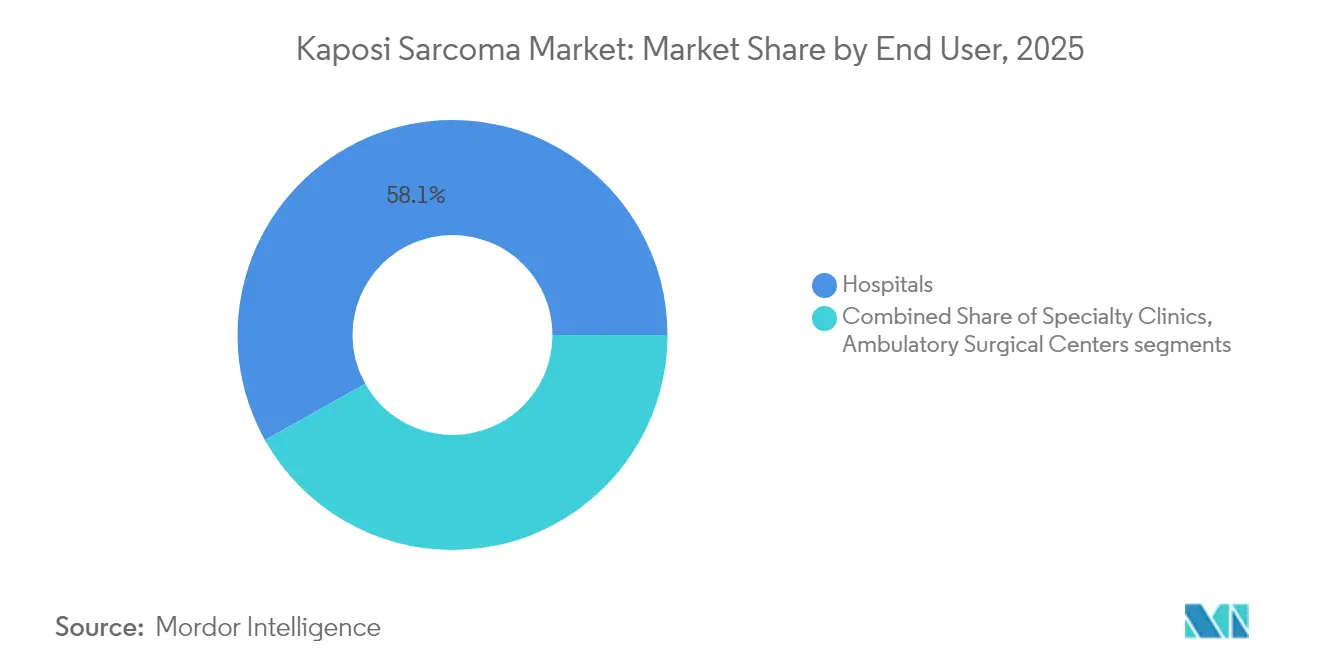

- By end user, hospitals held 58.12% revenue share in 2025; ambulatory surgical centers post the highest 5.97% CAGR through 2031.

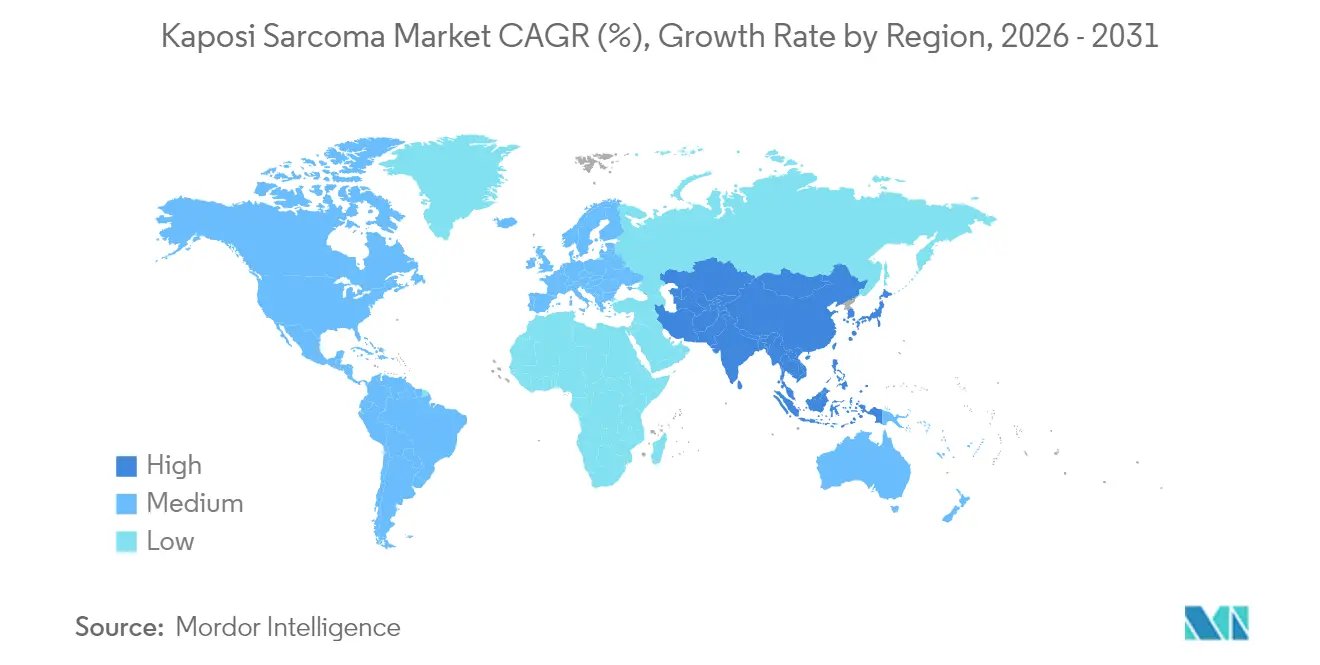

- By region, North America commanded 39.25% share in 2025; Asia-Pacific is set to expand at a 6.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kaposi Sarcoma Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence among immuno-compromised populations | +1.2% | Global, concentrated in sub-Saharan Africa and urban centers | Medium term (2-4 years) |

| Wider uptake of liposomal anthracyclines in first-line therapy | +0.8% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing access to antiretroviral therapy in LMICs | +0.7% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Pipeline of immune-checkpoint inhibitors targeting HHV-8 | +0.6% | Global, early gains in North America and Europe | Long term (≥ 4 years) |

| AI-driven histopathology workflows shortening diagnostic lead-time | +0.4% | Developed markets, gradual LMIC adoption | Medium term (2-4 years) |

| Cell-based gene therapies entering early-phase trials | +0.3% | North America, EU, select Asia-Pacific centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Among Immuno-Compromised Populations

Escalating numbers of immune-compromised patients—kidney transplant recipients, individuals on biologic immunosuppressants, and long-COVID sufferers—are broadening the Kaposi's Sarcoma market beyond the historical HIV cohort. Kidney transplant recipients face added complexity because standard antirejection drugs dampen tumor immunity, creating demand for regimens that balance graft protection with oncologic control. Emergent data on post-viral immune dysregulation following COVID-19 further enlarges the patient universe, prompting oncologists to adapt treatment pathways.

Wider Uptake of Liposomal Anthracyclines in First-Line Therapy

Pegylated liposomal doxorubicin has become the preferred first-line agent because it decreases cardiotoxicity while sustaining antitumor potency. Three-decade follow-up confirms durable efficacy, and multiple European approvals such as Celdoxome and Myocet have fostered competition that is nudging prices downward. Expanded formulary availability in Asia-Pacific hospitals is accelerating uptake, and U.S. payers increasingly authorize outpatient administration, trimming facility overheads.

Growing Access to Antiretroviral Therapy in LMICs

Rapid ART rollout has dropped HIV-related Kaposi’s incidence, yet the larger pool of virally suppressed survivors needs lifelong cancer surveillance. Viral resistance rates up to 19.6% for dolutegravir threaten rebound risk, keeping Kaposi’s vigilance high. Zimbabwe’s attainment of WHO maturity level 3 exemplifies regulatory capacity gains that enable broader oncology drug importation[1]Source: World Health Organization, “HIV Drug Resistance – Brief Report 2024,” who.int .

Pipeline of Immune-Checkpoint Inhibitors Targeting HHV-8

Nivolumab plus pomalidomide trials show early tumor regression in virus-associated sarcomas, signaling a breakaway from chemotherapy dependence. The National Cancer Institute has earmarked USD 3 million for HHV-8 vaccine investigation, underscoring government resolve to shift toward prophylaxis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High toxicity profile of existing chemotherapies | -0.9% | Global, particularly affecting elderly populations | Short term (≤ 2 years) |

| Scarcity of validated surrogate endpoints for rare-tumor trials | -0.6% | Global, regulatory impact in all major markets | Medium term (2-4 years) |

| Limited reimbursement outside HIV-associated cases | -0.5% | North America, EU, select Asia-Pacific markets | Medium term (2-4 years) |

| Cold-chain gaps in endemic African regions | -0.4% | Sub-Saharan Africa, rural areas in LMICs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Toxicity Profile of Existing Chemotherapies

Cumulative doxorubicin exposure above 450 mg/m² elevates congestive-heart-failure risk to 11%, forcing shorter regimens or cardioprotective measures that raise treatment cost. Pegylated formulations reduce exposure yet hand-foot syndrome causes dose interruptions in up to 40% of recipients, curbing real-world effectiveness. Such toxicity concerns push oncologists toward immunotherapies, but access remains uneven.

Limited Reimbursement Outside HIV-Associated Cases

Coverage gaps for classic Kaposi’s cases complicate therapy initiation. Payer tactics such as white-bagging cut physician margins by more than USD 2,000 per infusion and inflate patient copays, discouraging use of premium agents. Medicare’s pending G2211 removal exemplifies shrinking reimbursement windows for complex oncology visits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: Immunotherapy Gains Ground Despite Chemotherapy Dominance

Chemotherapy anchored almost half of 2025 revenue, yet its growth has slowed as clinicians seek safer long-term strategies. Liposomal anthracyclines continue to dominate first-line use because of strong data and broad formulary coverage, keeping the Kaposi's Sarcoma market firmly grounded in cytotoxic approaches. Even so, immune-checkpoint drugs, especially PD-1 inhibitors, are demonstrating durable responses in refractory disease, elevating their share in trial enrollment lists. Bioscience investors have responded by directing capital toward antibody engineering and T-cell activation platforms, suggesting a structural tilt toward immunotherapy over the forecast window.

Immunotherapy’s 5.26% CAGR reflects both scientific progress and practical convenience. Subcutaneous nivolumab, cleared in December 2024, trims chair time from hours to minutes, allowing outpatient centers to treat additional patients per day. These operational efficiencies resonate with health systems pivoting from inpatient infusions. Consequently, immunotherapy’s contribution to the Kaposi's Sarcoma market size is expected to swell from the mid-teens today to more than one-quarter by 2031, accelerating overall revenue momentum without materially lifting patient counts.

By Route of Administration: Oral Formulations Challenge IV Dominance

Intravenous delivery still governs 61.55% of the Kaposi's Sarcoma market size in 2025 thanks to entrenched hospital protocols and payer familiarity. Pegylated liposomal doxorubicin and paclitaxel rely on controlled infusion rates to mitigate acute side-effects, locking huge volumes into infusion suites. Yet, oral molecules—particularly thalidomide analogues and next-generation antivirals—are coming on strong, growing 5.64% annually until 2031. Telehealth monitoring and digital adherence tools cut the perceived risk of outpatient dosing, encouraging physicians to switch stable patients. With Medicare requiring National Drug Code submission for oral oncologics from 2025, compliance is expected to standardize billing practices, further easing uptake .

Despite convenience gains, IV formulations are unlikely to collapse quickly; many late-stage candidates, including cell-based therapies, still necessitate controlled administration. Nonetheless, every incremental shift toward tablets erodes infusion-center volume, signaling gradual realignment of ancillary service revenues across the Kaposi's Sarcoma industry.

By End User: Ambulatory Centers Capitalize on Outpatient Trend

Hospitals retained 58.12% share in 2025 because complex cases often demand multidisciplinary oversight and intensive supportive care. However, payer pressure to subdue facility fees is pushing lower-acuity infusions into ambulatory surgical centers, where streamlined staffing and shorter stays reduce cost per episode. This migration supports a 5.97% CAGR for ambulatory facilities, making them the fastest-growing channel within the Kaposi's Sarcoma market. Specialty oncology clinics occupy a strategic niche, leveraging deep disease-area expertise without the overhead of tertiary hospitals. Tele-oncology check-ins, adopted widely during the COVID-19 pandemic, are now standard for routine follow-up, allowing high-risk patients to avoid unnecessary in-person visits.

Long term, payer reimbursement algorithms may steer more care toward bundled outpatient packages, but hospitals are evolving too. Many academic centers are spinning off satellite infusion units and partnering with home-care firms to retain patient flows, demonstrating that competition for site-of-care share is dynamic rather than zero-sum.

Geography Analysis

North America generated 39.25% of 2025 revenue, supported by mature insurance coverage, sophisticated clinical trial infrastructure, and early approval of novel agents . Yet, cost containment policies are hardening. Medicare drug-price negotiations under the Inflation Reduction Act, while easing patient out-of-pocket burdens, cloud manufacturers’ pricing power, nudging some firms to delay launches until clearer guidance emerges.

Asia-Pacific posts the leading 6.49% CAGR through 2031 thanks to improved HIV outreach, upgraded regulatory regimes, and aggressive hospital build-outs. China’s rising oncology budget under the 14th Five-Year Plan and India’s expansion of National AIDS Control Programme facilities are catalyzing demand. However, rural-urban disparities persist: cold-chain networks struggle in remote provinces, limiting high-value biologic penetration. Innovative value-based agreements, already piloted in Singapore and South Korea, may mitigate affordability gaps as regional payers experiment with outcome-linked pricing.

Europe maintains steady, mid-single-digit growth, underpinned by compulsory insurance systems that guarantee broad access but also enforce strict cost-effectiveness thresholds. Uptake of biosimilar pegylated liposomal doxorubicin has delivered double-digit savings for national health funds, freeing resources for immune-checkpoint therapies. Post-Brexit regulatory adjustments require parallel submissions to both EMA and MHRA, adding administrative cost that smaller biotech firms sometimes struggle to absorb, subtly consolidating launch activity among larger multinationals.

Competitive Landscape

The Kaposi's Sarcoma market is moderately consolidated, with the top companies accounting for roughly half of global revenue. Bristol Myers Squibb’s USD 4.8 billion Mirati purchase and AstraZeneca’s USD 2 billion Fusion buyout underline industry appetite for differentiated oncology assets. Merck’s latest deal for an anti-PD-1/VEGF bispecific antibody positions it to challenge Bristol in combination immunotherapy, while Gilead is leveraging its antiviral heritage to develop dual-pathway agents that both suppress HHV-8 replication and stimulate T-cell function.

Technology adoption differentiates leaders. AI-enhanced digital pathology networks at institutions partnered with Johnson & Johnson reduce biopsy-to-report cycles by 50%, accelerating time to first treatment and effectively boosting drug volume per patient year. Sanofi’s EUR 300 million radioligand collaboration with Orano Med targets rare HHV-8-positive tumors, positioning the company in a subsegment with limited competition.

Emerging challengers like Nuvation Bio and Regeneron are advancing precision biologics that hit viral epitopes unique to Kaposi’s Sarcoma. Although these firms currently lack the commercial muscle of incumbents, partnership deal flow suggests incumbents may license or acquire promising candidates, tightening consolidation further.

Kaposi Sarcoma Industry Leaders

Bristol-Myers Squibb

Merck & Co., Inc

Pfizer Inc.

Navidea Biopharmaceuticals, Inc.

Baxter Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA cleared fam-trastuzumab deruxtecan-nxki for HER2-low breast cancer, underscoring continued progress in antibody-drug conjugate platforms relevant for Kaposi’s Sarcoma innovation.

- November 2024: Merck signed an exclusive global license with LaNova Medicines for LM-299, an anti-PD-1/VEGF bispecific antibody aimed at solid tumors including Kaposi’s Sarcoma applications.

- May 2024: UNC Lineberger Comprehensive Cancer Center unveiled a mouse model for Kaposi sarcoma, a breakthrough poised to accelerate the development of new treatments for the disease

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Kaposi sarcoma market as the yearly revenue from branded and generic drugs, radiotherapy fractions, and curative surgical procedures used to treat epidemic, classic, endemic, and iatrogenic Kaposi sarcoma across 17 tracked economies.

Scope exclusion: routine HIV antiretroviral therapy prescribed only for viral control, along with palliative wound-care consumables, is left outside the model.

Segmentation Overview

- By Therapy

- Chemotherapy

- Immunotherapy

- Antiviral Therapy (HAART)

- Targeted/Precision Therapies

- By Route of Administration

- Intravenous

- Oral

- Topical

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Oncologists, transplant clinicians, and hospital pharmacy managers from North America, Europe, Sub-Saharan Africa, and Asia-Pacific were interviewed. Their insights refined incidence multipliers, line-of-therapy switching rates, and typical course pricing, closing gaps left by secondary data.

Desk Research

Mordor analysts first mapped the treated-patient pool with open data sets such as WHO Global Cancer Observatory, UNAIDS country sheets, SEER, Eurostat cancer registries, and key PubMed meta-analyses. We layered import-export filings, US FDA orphan-drug approvals, hospital charge-master data, and company filings drawn through D&B Hoovers, plus news feeds from Dow Jones Factiva to benchmark regimen costs and regional therapy mix. The sources listed are illustrative; many additional records supported data collection and verification.

Market-Sizing & Forecasting

A top-down patient-volume reconstruction begins with country-level KS incidence, HIV prevalence, and post-transplant numbers, which are then linked to therapy uptake and average selling prices to yield 2025 revenue. Supplier roll-ups and sampled invoice checks act as a bottom-up sanity filter. Key variables include HAART coverage, annual organ transplants, liposomal doxorubicin pricing, checkpoint-inhibitor adoption, and regional reimbursement intensity. Five-year forecasts apply multivariate regression with ARIMA smoothing, and assumptions are stress-tested with our expert panel before sign-off.

Data Validation & Update Cycle

Outputs pass variance checks, peer review, and management approval. Reports refresh annually; interim updates trigger on guideline shifts, major launches, or reimbursement changes, ensuring buyers receive the latest view.

Why Mordor's Kaposi Sarcoma Baseline Commands Reliability

Published estimates often diverge because firms use unequal scopes, vintage years, and validation depth.

By anchoring estimates in current epidemiology, clearly defined therapy bundles, and dual-path modeling, Mordor Intelligence provides a balanced baseline clients can trust. External studies quote USD 110.48 million for 2022, USD 140.2 million for 2023, and USD 145.55 million for 2024; each applies narrower scopes or older data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 144.57 million (2025) | Mordor Intelligence | - |

| USD 110.48 million (2022) | Regional Consultancy A | Limited geography; therapy-only scope |

| USD 140.2 million (2023) | Global Consultancy A | Excludes radiation and surgery spend; sparse primary checks |

| USD 145.55 million (2024) | Trade Journal B | Hospital-billing only model; biennial refresh |

In short, our disciplined mix of fresh epidemiological baselines, dual-path modeling, and continuous peer review makes Mordor's numbers the most transparent and reproducible reference available today.

Key Questions Answered in the Report

Q1. What factors chiefly propel the Kaposi's Sarcoma market?

Most momentum stems from rising immuno-compromised patient numbers, increasing adoption of liposomal anthracyclines, and broadening access to ART in low- and middle-income nations. Additional lift comes from checkpoint-inhibitor pipelines and AI-enabled diagnostics that shorten time to treatment.

Q2. Which therapy category is expanding fastest?

Immunotherapy grows at 5.26% annually through 2031 as PD-1 inhibitors and novel bispecific antibodies deliver durable responses with milder side-effect profiles than chemotherapy.

Q3. Where do reimbursement barriers most hinder uptake?

Coverage remains restricted for non-HIV-associated Kaposi’s cases in the United States and parts of Europe, while insurer practices such as white-bagging further squeeze provider economics.

Q4. How is site-of-care shifting?

Ambulatory surgical centers record the highest 5.97% CAGR because payers prefer lower facility costs and patients value shorter visits; hospitals, however, retain complex case management.

Q5. Which region leads future growth?

Asia-Pacific is forecast to climb 6.49% annually, driven by improved HIV programs, regulatory modernization, and expanding oncology infrastructure.

Page last updated on: