Sarcopenia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

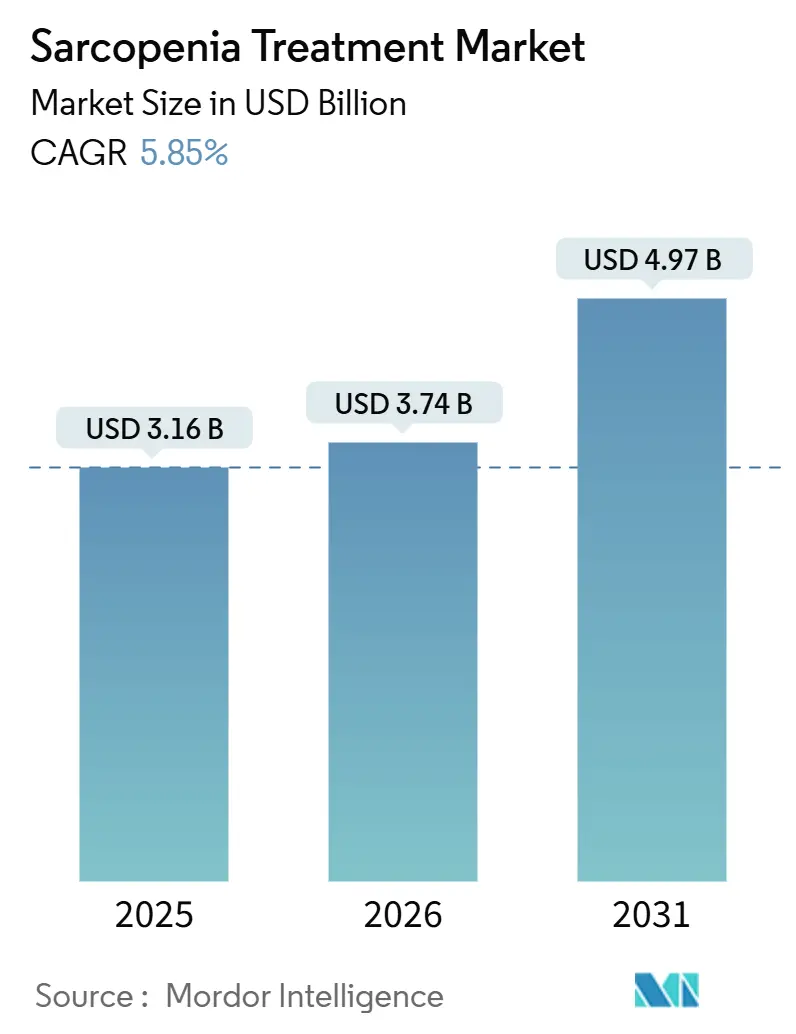

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

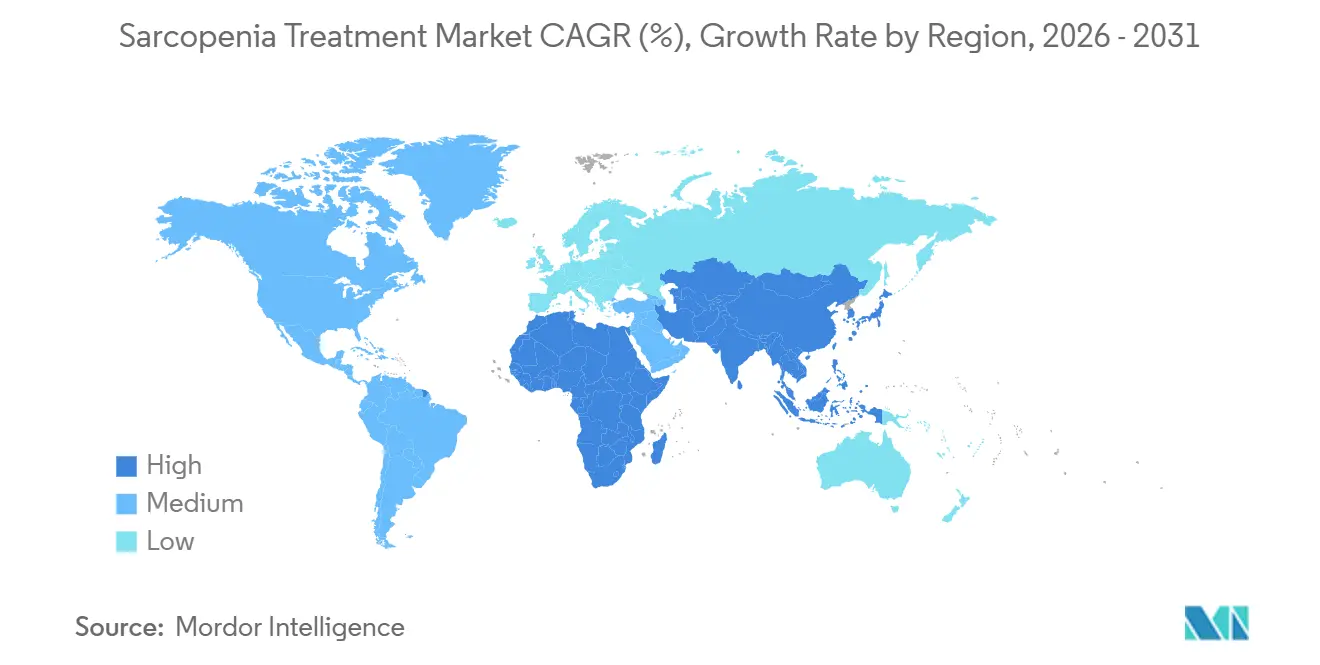

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

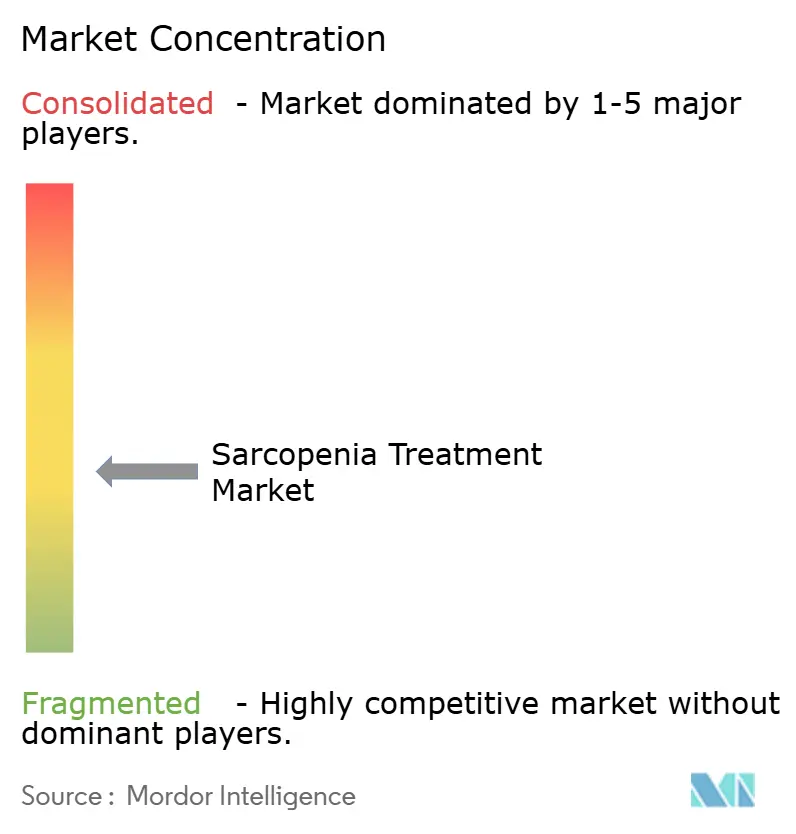

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sarcopenia Treatment Market Analysis by Mordor Intelligence

The Sarcopenia Treatment Market size was valued at USD 3.16 billion in 2025 and is estimated to grow from USD 3.74 billion in 2026 to reach USD 4.97 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031).

Rapid population aging, the sharp rise in prescriptions for GLP-1 receptor agonists, and the first regulatory filings for myostatin antibodies are converging to lift demand for both nutritional and pharmacologic interventions. Asia-Pacific grows at the fastest pace, helped by Japan’s and South Korea’s reimbursement of ICD-10-CM code M62.84 services, while North America’s payers experiment with step-therapy that begins with low-cost protein and moves up to biologics. Investor capital is flowing into biotech pipelines targeting the ActRII pathway, and digital platforms that screen CT scans for low muscle mass are widening the diagnosed population. These forces, alongside government healthy-aging programs, anchor a medium-term growth runway that keeps the sarcopenia treatment market on a steady upward trajectory.

Key Report Takeaways

- By treatment type, protein supplements commanded 55.27% of sarcopenia treatment market share in 2025, whereas myostatin & ActRII inhibitors are projected to post a 9.34% CAGR through 2031, the fastest within the segmentation.

- By route of administration, oral delivery retained 84.78% of the sarcopenia treatment market size in 2025; parenteral products, however, are advancing at an 8.46% CAGR as ERAS protocols gain traction.

- By distribution channel, hospital pharmacies led with 43.79% sarcopenia treatment market share in 2025, while online pharmacies are expanding at a 9.68% CAGR on the back of subscription-based, direct-to-consumer models.

- By end user, hospitals held 42.89% of revenue in 2025, yet home-care settings are the fastest riser with an 8.22% CAGR, reflecting payer and patient preference for aging-in-place.

- By geography, Asia-Pacific accounted for 36.89% of the global sarcopenia treatment market size in 2025 and is on course for a 6.83% CAGR to 2031, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sarcopenia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating global aging and fall-related costs | +1.2% | Japan, South Korea, Germany, Italy, United States | Long term (≥ 4 years) |

| Rising adoption of protein, vitamin D, and calcium | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Surging R&D funding for first-in-class pharmacologics | +1.4% | North America, Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Government healthy-aging and malnutrition programs | +0.8% | Japan, China, South Korea, select EU markets | Long term (≥ 4 years) |

| GLP-1-induced muscle wasting creates adjunct demand | +1.1% | United States, Canada, United Kingdom, Germany | Short term (≤ 2 years) |

| AI-powered early-diagnosis platforms unlock new pools | +0.7% | United States, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Global Aging and Fall-Related Healthcare Costs

Japan’s over-65 cohort reached 29.1% in 2023 and will likely touch 35% by 2040.[1] Statistics Bureau of Japan, “Population Estimates,” STAT.GO.JPChina already counts 280 million people over 60, a figure expected to reach 400 million by 2035.[2]National Bureau of Statistics of China, “Population Data,” STATS.GOV.CN In the United States, falls among older adults cost Medicare USD 50 billion each year, and sarcopenia is implicated in up to half of those incidents. The Society of Actuaries calculated that a 10% cut in sarcopenia prevalence could save USD 6.7 billion over five years. These facts underpin payer pilots that reimburse nutritional counseling and resistance training for patients documented with low muscle mass, directly boosting the sarcopenia treatment market.

Rising Adoption of Protein, Vitamin D, and Calcium Supplements

Protein supplementation has moved from sports aisles into geriatric wards. Whey isolates enriched with leucine are standard in post-fracture discharge packs, and vitamin D co-supplementation trims fall risk by 12% in institutional settings, according to a 2024 Cochrane review. Retail sales of combination protein-vitamin D-calcium formulas climbed 18% year-over-year in North America and Europe during 2024. Abbott and Nestlé have repositioned Ensure and Boost as medical foods, reinforcing physician trust and keeping protein at the center of the sarcopenia treatment market.

Surging R&D Funding for First-in-Class Pharmacologics

Scholar Rock filed apitegromab, the first myostatin antibody, with the FDA in February 2025. Regeneron began a Phase 1 study of a dual GDF8-activin A antibody the same year.[3]Scholar Rock Therapeutics, “Apitegromab FDA Submission,” IR.SCHOLARROCK.COM Venture and public investors have committed more than USD 1.2 billion to such programs since 2023, reflecting strong belief that the sarcopenia treatment industry is on the verge of its first drug approvals. Regulatory momentum is primed to shift revenue from commodity supplements toward high-margin biologics and lift the overall sarcopenia treatment market size.

Government Healthy-Aging and Malnutrition Programs

Japan’s 2024 policy update now reimburses dietitians who craft personalized protein plans for older citizens. China earmarked CNY 50 billion (USD 7 billion) for elderly-nutrition initiatives under Healthy China 2030. South Korea and the European Union are embedding muscle-health targets into national insurance and Horizon Europe research calls. These measures directly lower out-of-pocket costs, expanding access and stimulating the sarcopenia treatment market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of FDA-approved drugs and diagnostic fragmentation | -0.6% | United States, Europe, Asia-Pacific | Medium term (2-4 years) |

| High retail prices of premium protein supplements | -0.3% | South America, Southeast Asia, sub-Saharan Africa | Short term (≤ 2 years) |

| Long-term safety concerns for anabolic and myostatin blockers | -0.4% | United States, Europe | Long term (≥ 4 years) |

| Digital divide limits tele-rehabilitation reach | -0.2% | South Asia, rural Latin America, sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of FDA-Approved Drugs and Fragmented Diagnostic Criteria

Neither EWGSOP2 nor AWGS has won FDA endorsement, forcing U.S. trials to negotiate bespoke endpoints that delay filings and muddy cross-study comparisons. Scholar Rock’s submission slipped 18 months while endpoints were finalized. Payers echo the uncertainty, with Medicare contractors differing on whether bioelectrical impedance or DXA is reimbursable. Regulatory clarity, expected in draft guidance by late 2026, remains a gating item for the sarcopenia treatment industry.

High Retail Prices of Premium Protein Supplements

Leucine-fortified whey powders cost USD 50-80 per month in high-income markets, pricing out seniors in countries where per-capita income is below USD 300. Soy and pea alternatives are 30% cheaper but carry lower leucine density, undercutting clinical effectiveness. Budget local brands often lack third-party testing, dampening physician confidence. Until subsidies widen, price remains a drag on sarcopenia treatment market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Myostatin Inhibitors Outpace Commodity Supplements

Protein supplements secured 55.27% of sarcopenia treatment market share in 2025, cementing their role in discharge bundles and retail aisles. However, myostatin and ActRII inhibitors are poised to grow 9.34% per year through 2031, propelled by late-stage trials and supportive cost-offset analyses. The sarcopenia treatment market size for these biologics is projected to reach USD 1.1 billion by 2031, underscoring payer willingness to fund muscle preservation that averts fall-related admissions.

Commodity vitamins hold mid-teens share but face saturation in developed economies. SARM candidates such as enobosarm could double their sliver of the market if 2026 approvals materialize. Combination sachets that fold protein, leucine, HMB, vitamin D, and calcium into single servings simplify adherence and sustain premium pricing, offering nutrition conglomerates a hedge as prescription entrants arrive.

By Route of Administration: Parenteral Gains as Hospital Protocols Evolve

Oral products represented 84.78% of the sarcopenia treatment market size in 2025, yet parenteral formats are climbing at an 8.46% CAGR as ERAS pathways embed intravenous amino acids before and after orthopedic surgery. A meta-analysis across 18 trials found perioperative parenteral nutrition reduced length of stay by 1.2 days, saving USD 3,000 per hip-fracture case.

Future approvals of subcutaneous biologics such as apitegromab would redistribute revenue toward parenteral channels and hospital pharmacies. Oral supplements remain convenient for community-dwelling seniors, but severe cases diagnosed in inpatient settings are gravitating to higher-bioavailability injections that deliver faster functional gains.

By Distribution Channel: Online Pharmacies Disrupt Traditional Retail

Hospital pharmacies retained 43.79% of sarcopenia treatment market share in 2025, courtesy of discharge prescriptions and formulary control. Still, online pharmacies are advancing at a 9.68% CAGR as seniors adopt auto-replenishment models that bundle AI coaching and body-composition tracking.

Retail drug stores face margin compression but are innovating with in-store muscle-mass kiosks piloted by CVS Health. Regulatory liberalization in the EU is smoothing cross-border e-pharmacy standards, paving the way for continued e-commerce gains.

By End User: Home-Care Settings Gain as Age-In-Place Preferences Intensify

Hospitals accounted for 42.89% of 2025 revenue, yet home-care settings are expanding at an 8.22% CAGR, reflecting both payer economics and patient preference. Portable impedance devices and tele-dietitian consultations lower clinical-oversight barriers, while long-term-care insurance in Japan now reimburses in-home nutrition services.

Specialized rehab centers provide superior lean-mass gains but struggle with visit caps in insurance plans. The trend toward decentralized care positions home-based delivery as the long-term growth engine of the sarcopenia treatment market.

By Patient Type: Post-Acute Sarcopenia Emerges as High-Value Niche

Primary age-related sarcopenia comprised 64.37% of patient volume in 2025, yet post-acute episodes following hospitalization are rising 7.46% annually. Payers view pre-habilitation and post-discharge nutrition as cost-effective levers to cut readmissions, elevating the sarcopenia treatment market size tied to post-surgical care pathways.

Sarcopenic obesity remains an under-served phenotype but could unlock combination drug-plus-exercise regimens, especially as GLP-1 agents paradoxically improve body composition when paired with resistance training. Secondary sarcopenia linked to chronic disease sits in the mid-teens share, opening partnership possibilities between cardio-renal drug makers and muscle-health innovators.

Geography Analysis

Asia-Pacific captured 36.89% of global sarcopenia treatment market share in 2025 and is pacing for a 6.83% CAGR through 2031. Japan, South Korea, and China are adding screening and nutritional benefits to national insurance, while India and Southeast Asia see urban middle-class uptake of premium supplements. Australia’s Pharmaceutical Benefits Scheme started reimbursing sarcopenia nutritional products in 2024, reinforcing regional momentum.

North America held a mid-20s share, constrained by supplement saturation and the absence of FDA-approved drugs. Falls cost Medicare USD 50 billion each year, yet only one-third of at-risk seniors receive muscle-strength assessments. Approvals of apitegromab or enobosarm could reignite growth by shifting spending toward reimbursed biologics.

Europe accounted for the low-20s share in 2025. Germany and the UK now reimburse screening under statutory and NHS schemes. Southern Europe battles affordability issues, but Horizon Europe funding is catalyzing multicountry trials, keeping regional R&D robust.

Competitive Landscape

The field is moderately fragmented. Abbott and Nestlé Health Science dominate the commodity protein market through medical nutrition portfolios and retail reach. Scholar Rock, Keros, Veru, and TNF Pharmaceuticals sit at the forefront of prescription innovation, with patents that protect exclusivity well into the 2030s.

White space emerges in sarcopenic obesity, post-surgical muscle loss, and digital therapeutics. Hinge Health and peers embed AI into tele-rehab, but reimbursement lags. Transparent Labs and other direct-to-consumer startups siphon online share by coupling subscription supplements with mobile apps. Technology integration is becoming a key differentiator as the sarcopenia treatment market evolves toward a bifurcated supplement-plus-biologic paradigm.

Sarcopenia Treatment Industry Leaders

Nestle Health Science

Biophytis SA

Bayer AG

Pfizer Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Biophytis signed an MoU with investors to finance the first global Phase 3 trial of BIO101 in sarcopenia.

- August 2025: Duke-NUS launched MAGNET, a SGD 10 million program to develop Singapore’s first precision sarcopenia therapies.

- July 2025: Epirium Bio completed dosing in a Phase 1 study of MF-300, an oral 15-PGDH inhibitor for sarcopenia.

- January 2025: TNF Pharmaceuticals reported positive safety data and plans a larger Phase 2b trial of isomyosamine, including a cohort of GLP-1 users.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the sarcopenia treatment market as all prescription or over-the-counter nutritional supplements, emerging pharmacological candidates, and medically guided exercise or device-aided regimens that are prescribed or dispensed to manage primary or secondary age-related muscle loss in humans. The size quoted by Mordor Intelligence for 2025 is USD 3.16 billion.

Scope Exclusion: sports-nutrition tonics aimed at athletic performance and any veterinary muscle-loss therapies are excluded.

Segmentation Overview

- By Treatment Type

- Protein Supplements

- Vitamin D & Calcium Supplements

- Vitamin B12 Supplements

- Anabolic Agents (SARMs & Hormonal Therapies)

- Myostatin & ActRII Pathway Inhibitors

- Ghrelin Receptor Agonists

- Anti-inflammatory / Metabolic Modulators

- Combination / Multi-nutrient Formulations

- By Route of Administration

- Oral

- Parenteral

- Enteral

- By Distribution Channel

- Hospital Pharmacies

- Retail & Drug Stores

- Online Pharmacies

- By End User

- Hospitals

- Specialized Clinics & Rehabilitation Centers

- Homecare Settings

- By Patient Type

- Primary (Age-related) Sarcopenia

- Secondary Sarcopenia ? Chronic-disease

- Sarcopenic Obesity

- Post-Acute / Post-Surgical Sarcopenia

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed geriatricians, hospital pharmacists, supplement formulators, and biotech executives across North America, Europe, and Asia-Pacific. Conversations centered on real-world prescribing splits, emerging myostatin-inhibitor pricing intentions, and regional reimbursement triggers, which let us temper secondary-data optimism and fine-tune baseline prevalence and ASP inputs.

Desk Research

We began with aging-population data from sources such as the UN World Population Prospects, WHO Global Health Observatory, and Eurostat to size the at-risk cohort. Prevalence and hospitalization costs were drawn from peer-reviewed outputs in the Journal of Cachexia, Sarcopenia and Muscle and CDC NHANES releases, which clarify diagnosis rates and treatment uptake. Trade bodies, including the International Alliance of Dietary/Food Supplement Associations, guided supplement penetration assumptions, while regulatory notes from the FDA and EMA informed pipeline attrition probabilities. Company financials accessed through D&B Hoovers added average selling price (ASP) reference points. (The list is illustrative; many other public and subscription sources were reviewed for confirmation and gap closure.)

Market-Sizing & Forecasting

A top-down framework starts with 60+ population counts, applies regional sarcopenia prevalence, and then layers medical-seeking rates to derive treated-patient pools, which are further refined through reimbursement coverage ratios. Select bottom-up checks, sampled supplement sales, pipeline drug revenue targets, and pharmacy channel audits ensure patient-pool realism. Key variables tracked include: 1) geriatric population growth, 2) clinically diagnosed prevalence trends, 3) mean daily protein-supplement spend, 4) number of active late-stage drug candidates, and 5) share of public insurance scripts. Multivariate regression, validated by expert consensus, projects each variable to 2030; scenario analysis adjusts for drug-approval timing shifts. Where bottom-up data were thin, we bridged gaps with proxy indicators such as protein-powder import volumes and survey-derived adherence rates before re-aligning totals to the top-down anchor.

Data Validation & Update Cycle

Outputs pass three-level analyst review, variance checks against fresh quarterly supplement shipment data, and rerun prevalence models when new clinical guidelines alter diagnostic thresholds. Reports refresh annually, and material events, such as FDA approvals or major pricing shifts, trigger interim recalibration so clients always receive the latest vetted view.

Why Mordor's Sarcopenia Treatment Baseline Numbers Command Reliability

Published estimates vary because publishers pick different patient universes, mix consumer wellness products with medical therapies, or freeze currency exchange at older baselines. By anchoring on treated-patient pools, refreshing inputs yearly, and cross-checking with channel ASPs, Mordor delivers a figure that decision-makers can confidently track.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.16 B (2025) | Mordor Intelligence | - |

| USD 3.03 B (2024) | Global Consultancy A | excludes pipeline drugs and counts only vitamin supplements |

| USD 3.00 B (2024) | Industry Association B | uses static prevalence from 2018, no reimbursement adjustment |

| USD 6.14 B (2024) | Regional Consultancy C | bundles sports-nutrition powders and wellness beverages |

In short, our disciplined scope selection, annually refreshed variables, and dual-angle validation give Mordor Intelligence a balanced, transparent baseline that clients repeatedly cite as the dependable starting point for strategic planning.

Key Questions Answered in the Report

What is the present and projected value of the sarcopenia treatment market in 2031?

The sarcopenia treatment market size is 3.74 billion in 2026 forecast to reach USD 4.97 billion by 2031 at a 5.85% CAGR.

Which treatment category is expanding fastest?

Myostatin & ActRII pathway inhibitors are expected to grow at about 9.3% per year through 2031, the highest among all categories.

Why is Asia-Pacific considered the most attractive region?

National insurance coverage for screening and nutrition, coupled with rapid demographic aging, gives Asia-Pacific 36.89% market share and the fastest regional CAGR.

How are GLP-1 drugs influencing demand?

GLP-1–induced muscle loss is driving adjunct prescriptions of protein supplements and creating trial cohorts for new anabolic agents, lifting short-term market growth.

When might the first FDA-approved drug for sarcopenia arrive?

If current timelines hold, biologics such as apitegromab or enobosarm could secure approval between 2026 and 2027, opening the prescription segment.

Which distribution channel is gaining share fastest?

Online pharmacies are advancing at nearly 9.68% CAGR as seniors adopt subscription models and tele-health bundles.

Page last updated on: