Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

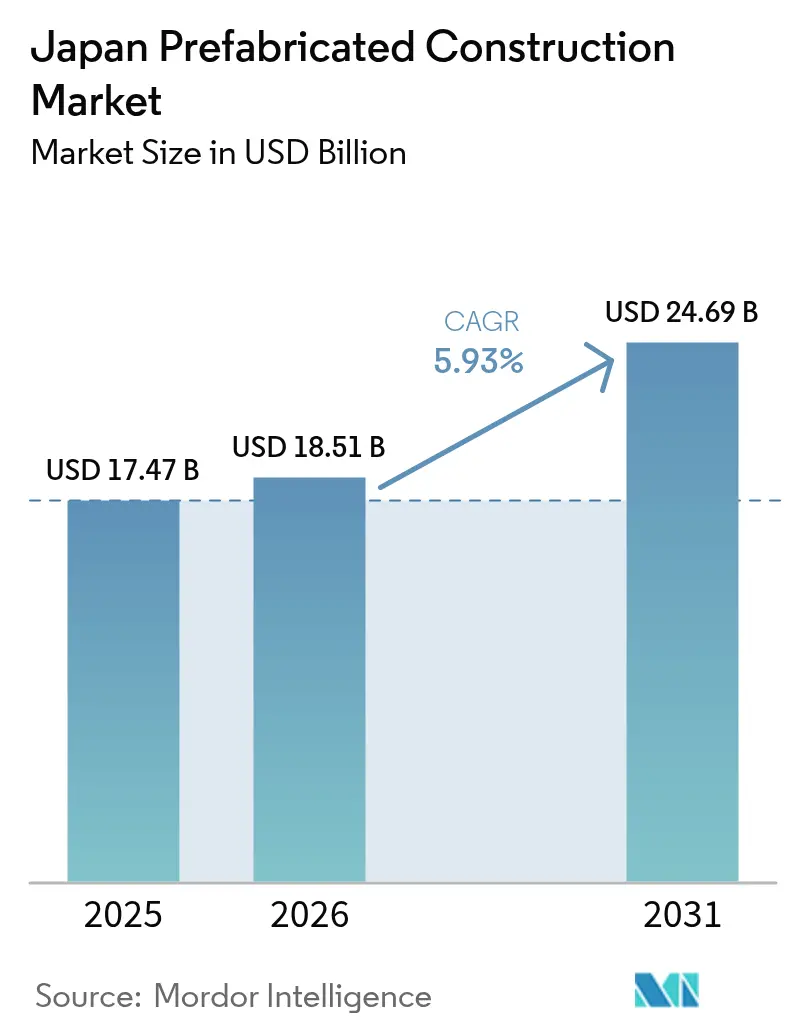

| Base Year Market Size (2025) | USD 17.47 Billion |

| Market Size (2026) | USD 18.51 Billion |

| Market Size (2031) | USD 24.69 Billion |

| Growth Rate (2026 - 2031) | 5.93% CAGR |

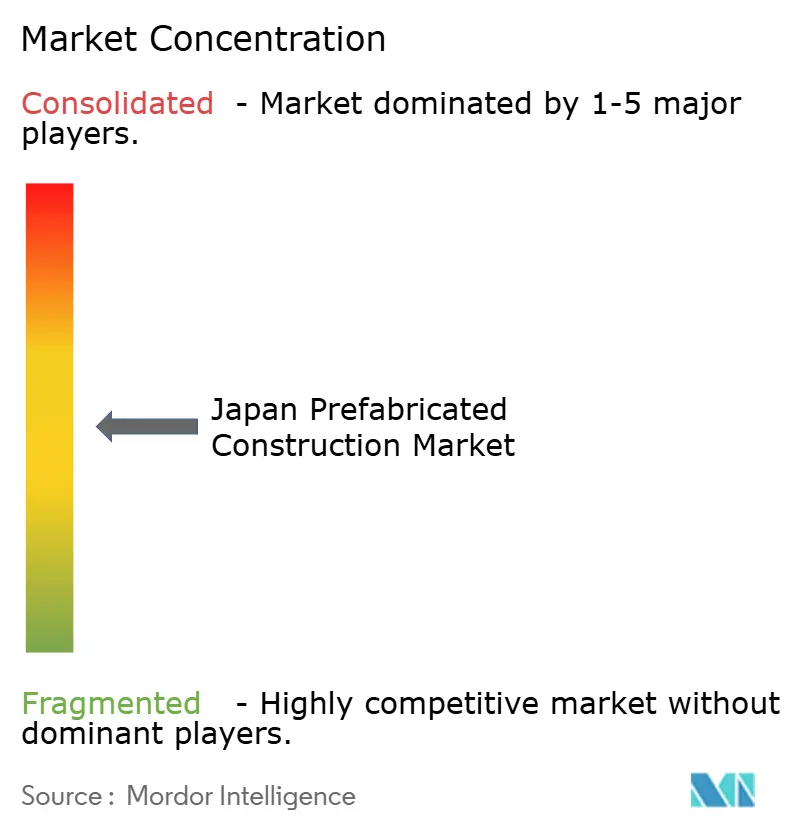

| Market Concentration | Medium |

Major Players_-_Copy.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Prefabricated Construction Market Analysis by Mordor Intelligence

The Japan Prefabricated Construction Market size was valued at USD 17.47 billion in 2025 and estimated to grow from USD 18.51 billion in 2026 to reach USD 24.69 billion by 2031, at a CAGR of 5.93% during the forecast period (2026-2031). This momentum reflects a structural pivot away from site-intensive construction toward factory-built precision as the sector confronts chronic labor shortages, stricter overtime rules, and tighter seismic and energy-efficiency codes. Volumetric modules that leave the factory with mechanical, electrical, and plumbing (MEP) systems already installed are shortening project schedules, and timber innovations—including cross-laminated timber (CLT)—are unlocking mid-rise opportunities once dominated by concrete and steel. Municipalities are accelerating school and clinic retrofits, developers are racing to deliver e-commerce fulfillment centers ahead of demand, and investors are rewarding companies that embed carbon-reduction and circular-economy principles into production workflows. Against this backdrop, the Japan prefabricated construction market offers an operational hedge against workforce attrition, regulatory headwinds, and material-cost volatility while positioning manufacturers to capture value in disaster recovery and decarbonization programs[1]Foundation for Promoting Personal Mobility and Ecological Transportation, “Labor Shortages and Prefab Adoption,” ecomo.or.jp.

Key Report Takeaways

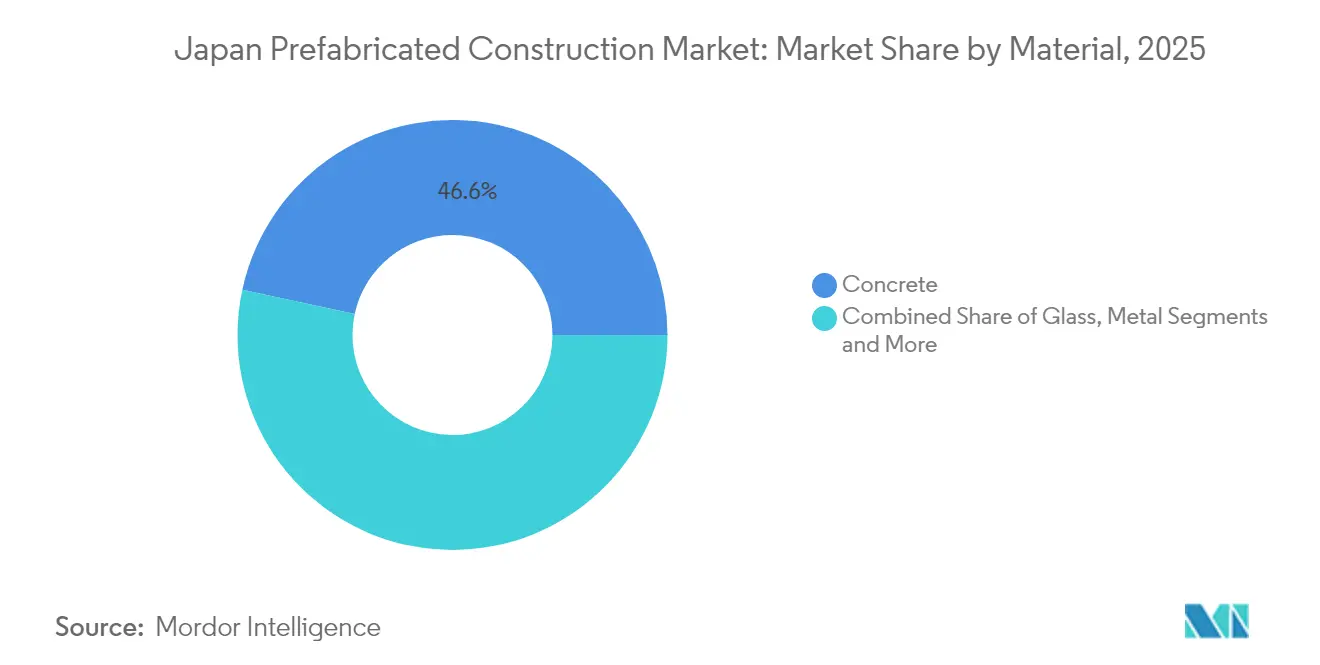

- By material, concrete led with 46.62% of the Japan prefabricated construction market share in 2025; engineered wood is forecast to expand at a 6.54% CAGR to 2031, the fastest among all materials.

- By application, residential accounted for 58.74% of the Japan prefabricated construction market size in 2025, while commercial buildings are advancing at a 6.73% CAGR through 2031.

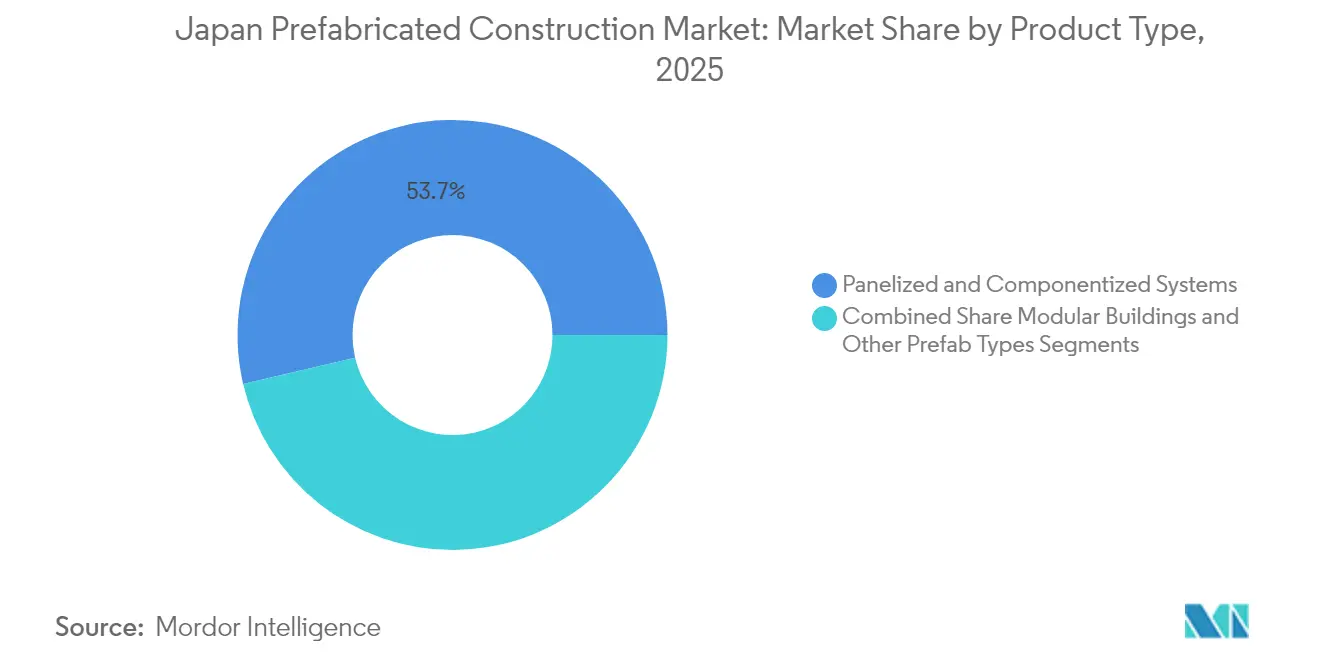

- By product type, panelized and componentized systems captured 53.65% of 2025 revenue; modular buildings are projected to grow at a 6.88% CAGR between 2026 and 2031.

- By city, Tokyo commanded 35.24% of 2025 demand, whereas Osaka is set to record the fastest expansion at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe skilled-labor shortages and aging workforce favor factory-built, labor-efficient solutions | +1.8% | National, with acute pressure in Tokyo, Osaka, Nagoya metropolitan areas | Long term (≥ 4 years) |

| Demand for rapid, high-quality rebuilds/retrofits of aging housing, schools, and clinics | +1.2% | National, with early gains in Tokyo, Osaka, and disaster-affected prefectures | Medium term (2-4 years) |

| Stringent seismic/quality standards align with precision prefab (steel/wood modular, panelized) | +1.0% | National, particularly in seismic zones (Kanto, Kansai, Tohoku) | Long term (≥ 4 years) |

| Energy-efficiency and decarbonization retrofits (insulation, airtight envelopes) boost prefab envelopes | +0.9% | National, with leadership in Tokyo and Osaka for ZEH/ZEB adoption | Medium term (2-4 years) |

| Disaster recovery and temporary-to-permanent modular needs after earthquakes/typhoons | +0.6% | Regional, concentrated in Noto Peninsula, Tohoku, and typhoon-prone coastal areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Severe Skilled-Labor Shortages and an Aging Workforce

Japan’s construction labor force continues to shrink, and workers aged 60 and above already represent 25% of the total, while those under 29 stand at just 12%. The Ministry of Land, Infrastructure, Transport and Tourism foresees a 667,000-worker gap by 2040, a deficit that conventional job-site methods cannot bridge. April 2024 overtime caps now limit on-site work hours, making factory environments that deliver predictable shifts far more attractive to contractors. Prefabrication trims 30%–40% of on-site labor hours, helping developers hit completion milestones even as wage inflation accelerates. With immigration policy in flux, capital-intensive automated lines offer a safer productivity path than labor-dependent site work[2]Sekisui House Co., Ltd., “Foundation Direct Joint Method,” sekisuihouse.co.jp.

Demand for Rapid, High-Quality Rebuilds and Retrofits

Roughly 29% of detached houses predate the 1981 seismic code, and an added 17% still fail to satisfy current capacity thresholds, creating a national backlog of retrofit needs. Schools, clinics, and municipal buildings erected during the 1960s boom are simultaneously reaching the end of their life, forcing local governments to seek solutions that minimize downtime. Prefabrication can pre-install HVAC and life-safety systems off-site while meeting millimeter-level tolerances verified through factory quality checks. Disaster-response programs illustrate the speed advantage: 6,882 prefab housing units were delivered within 11 months after the January 2024 Noto Peninsula earthquake. These precedents are guiding municipal tenders that now prioritize modular options for both temporary and permanent rebuilds.

Stringent Seismic and Quality Standards

Revisions to seismic evaluation criteria in 2017 raised allowable drift ratios and introduced device-certification mandates that elevate structural precision requirements. Factory-controlled welding, anchor-bolt placement, and concrete curing eliminate variables that plague site pours and carpentry. Sekisui House’s Foundation Direct Joint construction method, for example, removes sill plates and fastens posts directly to foundations, lowering weak-joint risk and earning full-scale cyclic-loading validation at the Building Research Institute. Large-panel ALC frames endured 0.04 radian story drifts without damage during official tests, reinforcing confidence among code officials and insurers that prefab meets or surpasses seismic mandates.

Energy-Efficiency and Decarbonization Mandates

From 2025, every new structure must meet Building Energy Conservation Act standards, while Zero Energy House (ZEH) and Zero Energy Building (ZEB) targets start in 2030. Prefab manufacturers have standardized grade-6 insulation and C-value airtightness of ≤ 1.0 cm²/m² across detached-home lines. Asahi Kasei Homes became Japan’s first RE100-certified housemaker in 2023, illustrating the ease of integrating renewable power at centralized factories. Advanced envelopes ship with triple-glazed windows, heat-recovery ventilation, and rooftop photovoltaic wiring pre-installed. These package solutions help builders and owners satisfy municipal carbon roadmaps without lengthy on-site retrofits.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront costs vs traditional builds and conservative procurement norms slow adoption | -0.8% | National, with stronger resistance in rural municipalities and smaller-scale projects | Medium term (2-4 years) |

| Site constraints, transport limits, and crane logistics for large modules in dense cities | -0.5% | Urban cores (Tokyo, Osaka, Nagoya) and mountainous regions with narrow access roads | Short term (≤ 2 years) |

| Fragmented codes/approvals across municipalities and limited standardization across suppliers | -0.4% | National, with greater complexity in regions with supplementary local building requirements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Costs and Conservative Procurement Norms

Prefabricated buildings still command a 10%–15% premium over conventional builds in select segments, reflecting factory overhead and automation capital costs. Japan’s lowest-bid procurement culture undervalues lifecycle savings such as lower maintenance and faster occupancy, keeping some municipal buyers anchored to traditional methods. Material-price swings complicate tender pricing; the Bank of Japan recorded a 4.0% year-on-year rise in cement prices in April 2025, while steel fell 4.2%, creating hedging challenges. Smaller city officials often request extra documentation for modular assemblies, extending approval timelines and eroding schedule gains.

Site Constraints, Transport Limits, and Crane Logistics

Road widths, overhead lines, and turning radii in Tokyo, Osaka, and Nagoya cap module dimensions at roughly 3 m × 12 m, forcing factories to ship more pieces and increasing crane time on tight lots. Night-time road closures and police escorts can add USD 5,000–10,000 per delivery. Mountainous regions have winding access roads and bridge weight limits that rule out heavy precast panels, pushing suppliers toward lighter timber or steel systems. Japan’s 1,724 municipalities apply supplemental code clauses that limit design standardization, diluting economies of scale. Although joint-delivery pacts among major housemakers emerged in 2024, last-mile logistics remain a challenging cost center.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Timber Challenges Concrete’s Dominance

Concrete captured 46.62% of the Japan prefabricated construction market in 2025, thanks to its fire resistance and acoustic mass, especially in multi-story housing and commercial towers. Yet timber’s footprint is expanding as domestic CLT capacity scales and engineered-wood innovations such as Sumitomo Forestry’s PRIMEWOOD validate mid-rise viability. The Forestry Agency’s promotion incentives and the high-profile W350 timber skyscraper concept have pushed architects to consider carbon-sequestering frames. Timber is forecast to grow at a 6.54% CAGR through 2031, outpacing the overall Japan prefabricated construction market and narrowing the cost gap with concrete as domestic mills achieve higher output efficiencies.

In parallel, steel-frame modular offerings from Sekisui House and Daiwa House continue to serve detached homes and low-rise rentals, leveraging robotic welding lines that pare labor inputs. Composite panels marrying fiber-reinforced polymers with lightweight concrete are gaining niche traction in seismic isolation retrofits. Haseko’s new precast plant, slated to supply interior-floor components for 4,000 units annually from October 2025, underscores confidence that concrete will retain a crucial role in dense urban housing even as wood accelerates.

By Application: Commercial Surge Offsets Cooling Housing Starts

Residential projects held 58.74% of the Japan prefabricated construction market size in 2025, with brand-name detached offerings such as Asahi Kasei’s Hebel Haus anchoring demand. Mortgage-rate hikes and material inflation tempered new-build volumes in 2024, yet renovation and rebuild pipelines remained active as owners pursued seismic upgrades. Commercial and institutional builds—schools, clinics, offices, and logistics centers—are expanding at a 6.73% CAGR toward 2031, reflecting municipal urgency to overhaul aging stock while minimizing operational downtime.

Full-scale fire and seismic tests at the Building Research Institute have given city planners confidence that modular classrooms and hospital wings meet stringent codes without sacrificing design flexibility. Prefab solutions also accelerate e-commerce logistics hubs: Osaka’s distribution boom has sparked rapid deployment of single-story, large-bay facilities that need quick commissioning. Disaster-recovery shelters and temporary workforce housing, while small in volume, offer high-visibility showcases for prefab versatility and speed.

By Product Type: Modular Units Gain as BIM Integration Deepens

Panelized and componentized systems accounted for 53.65% of revenue in 2025, prized for adaptability to irregular urban lots and renovation inserts. However, modular buildings—fully finished volumetric units—are projected to post the fastest 6.88% CAGR through 2031, supported by Ministry-led BIM permit workflows that reward digital-twinned production lines. Sekisui House’s skeleton-infill (SI) collaboration lets regional contractors combine centrally made structural shells with localized finishes, scaling output without replicating entire factories.

Hybrid approaches that ship bathroom and kitchen pods inside panelized envelopes offer a cost-performance middle ground. Asahi Kasei’s Hebel Maison rental range pairs panelized exteriors with factory-fitted ZEH-M packages, winning the Good Design Award 2024 for aesthetics and livability. Panasonic’s uptick in domestic electrical-material sales points to growing demand for factory-integrated power, data, and energy-storage systems within volumetric modules.

Geography Analysis

Tokyo accounted for 35.24% of the Japan prefabricated construction market in 2025, buoyed by landmark mixed-use towers like Toranomon Hills Station Tower that marry transit, office, and luxury residential functions. Land prices exceeding USD 10,000 per m² and narrow streets elevate the value of factory precision and tight staging. Retrofits of 1960s-era schools and clinics, combined with the metropolitan government’s ZEH-M drive, keep panelized envelopes in steady demand even as new-build volumes level off.

Osaka is projected to be the fastest-growing city segment at a 7.11% CAGR through 2031, catalyzed by post-Expo infrastructure, plentiful industrial plots, and rising e-commerce fulfillment needs. The completion of the Osaka Station West Elevated Area in June 2024 demonstrated how prefab minimizes disruption to live rail operations, reinforcing the method’s appeal for transit-adjacent commercial builds. Logistics developers value one-story panelized sheds that can be commissioned within months, turning landholdings into revenue earners faster than conventional builds.

Nagoya remains an automotive manufacturing powerhouse, with battery assembly and clean-room requirements driving precision-built industrial shells. Growth here trails Osaka, yet Panasonic’s USD 2.5 billion capex push for battery facilities signals health in specialized industrial prefab demand. Beyond the megacities, regional prefectures leverage disaster-recovery subsidies to install quake-resilient housing and clinics. The rapid erection of nearly 7,200 units after the Noto Peninsula quake shows how prefab supplies lifelines in remote areas where transporting skilled trades would be prohibitive.

Competitive Landscape

Moderate fragmentation defines the Japan prefabricated construction industry: the top five firms—Sekisui House, Daiwa House, Panasonic Homes, Asahi Kasei Homes, and Sumitomo Forestry—jointly hold about significant share of revenue, but leadership shifts by material and client segment. Steel-frame specialists dominate multi-story housing, while timber innovators champion carbon-sequestration messaging in detached homes. Market niches remain for regional subcontractors that license proprietary systems via programs such as Sekisui’s SI collaboration, gaining access to seismic-strengthening technology without large capital outlays.

Strategic moves signal aggressive positioning. Sekisui House’s USD 5 billion buyout of U.S. builder MDC Holdings in January 2024 vaulted it into the top five American homebuilders and created a knowledge loop for multiskilled construction methods that could migrate back to Japan. Asahi Kasei Homes posted record revenue of USD 6.8 billion in FY 2024, buoyed by resource-circulation product lines that earned Ministry recognition and attracted eco-conscious buyers. Daiwa House leans on its logistics-facility portfolio to lock in long-term leases with e-commerce operators, while Panasonic Homes bundles energy-storage offerings with volumetric units to differentiate on resilience and operating cost.

Digitalization separates front-runners from laggards. Sumitomo Forestry ranks among the highest for social-media engagement, using LINE and Instagram to convert leads at a lower cost than showroom visits. BIM-to-factory workflows enable real-time clash detection, improve first-time-right ratios, and reduce municipal approval cycles once BIM-based permits become mandatory in 2025. Full-scale seismic, fire, and durability tests at government institutes remain a capital barrier for new entrants, preserving incumbent share even as demand accelerates.

Japan Prefabricated Construction Industry Leaders

Sekisui House

Daiwa House Group

Panasonic Homes

Toyota Housing Corporation

Misawa Homes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Haseko Corporation and partners announced an 8,810 m² precast factory in Kasumigaura City, targeting full operation from Oct 2025 and annual output for 4,000 apartment units, expandable to 5,000.

- May 2025: Toyota broke ground on a new Tokyo headquarters in Shinagawa, aiming for a FY 2030 opening and underscoring sustained corporate appetite for large-scale prefab commercial space.

- January 2025: Sekisui House confirmed its rise to fifth-largest U.S. homebuilder post-MDC acquisition and plans to train 20 U.S. crews in multiskilled prefab methods.

- December 2024: Prefab suppliers delivered 6,882 emergency housing units after the Noto Peninsula earthquake, plus 286 units for heavy-rain victims by March 2025.

Japan Prefabricated Construction Market Report Scope

The Japan Prefabricated Construction Market covers the growing trends and projects in prefab building markets, like commercial construction, residential construction, and industrial construction. The report also covers the industry along with the type of material used, like concrete, timber, glass, metal, and other types. Along with the scope of the report, it also analyzes the key players and the competitive landscape in the Japan Prefabricated Buildings Market. The impact of Geopolitics and the Pandemic on the Market has also been incorporated and considered during the study.

Japan's Prefabricated Construction Industry is segmented by Material Type (Concrete, Glass, Metal, Timber, and Other Material Types) and Application (Residential, Commercial, and Other Applications (Infrastructure and Industrial). The report offers market size and forecast for all the above segments in value (USD).

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By City

| Tokyo |

| Osaka |

| Nagoya |

| Rest of Japan |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By City | Tokyo |

| Osaka | |

| Nagoya | |

| Rest of Japan |

Key Questions Answered in the Report

What is the current value of the Japan prefabricated construction market?

The market stands at USD 18.51 billion in 2026 and is forecast to reach USD 24.69 billion by 2031.

Which material leads prefab demand in Japan?

Concrete commands 46.62% of 2025 revenue, but engineered wood is growing fastest at a 6.54% CAGR through 2031.

Why are modular buildings gaining popularity?

Volumetric modules leave the factory with MEP systems installed, cut on-site labor by up to 40%, and are projected to grow at a 6.88% CAGR.

Which city is expanding prefab use most rapidly?

Osaka is the fastest-growing metropolitan market, set for a 7.11% CAGR from 2026 to 2031 due to logistics and Expo-related projects.

How do seismic and energy codes influence prefab adoption?

Factory precision helps meet tighter seismic drift limits and 2025 energy-conservation mandates, making prefab a compliance-friendly choice.

What limits prefab uptake despite its advantages?

Upfront premiums of 10%–15% and urban transport restrictions for large modules still temper adoption in some projects.

Page last updated on: