Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

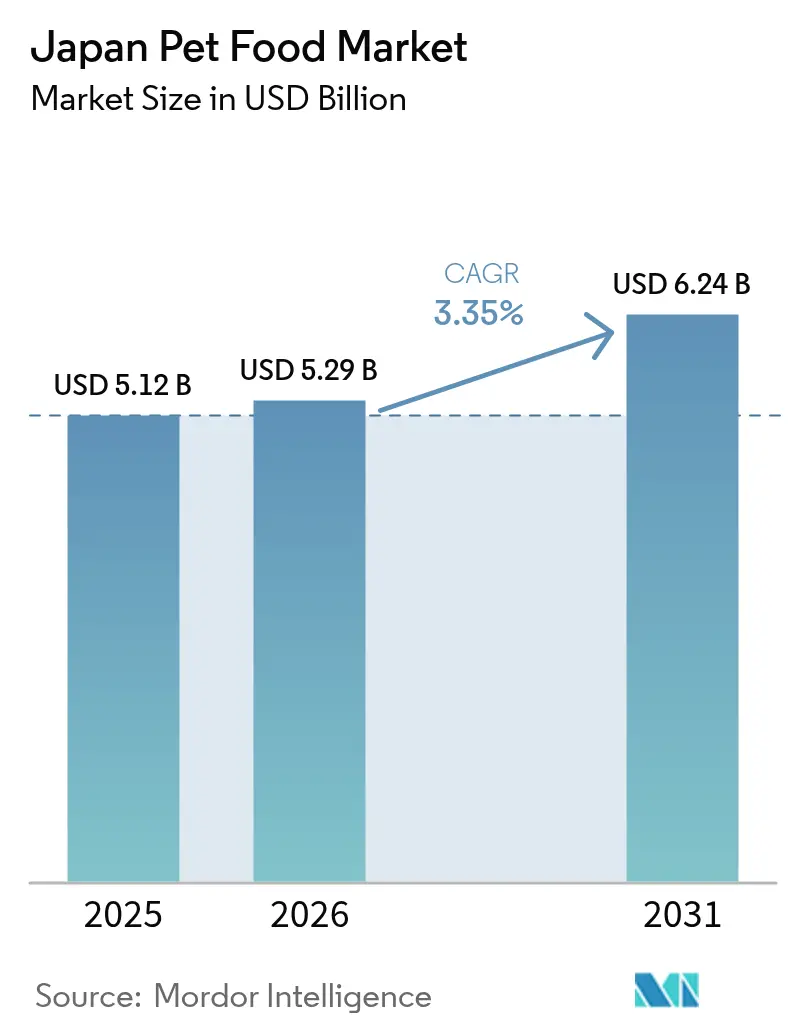

| Base Year Market Size (2025) | USD 5.12 Billion |

| Market Size (2026) | USD 5.29 Billion |

| Market Size (2031) | USD 6.24 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Pet Food Market Analysis by Mordor Intelligence

Japan pet food market size in 2026 is estimated at USD 5.29 billion, growing from 2025 value of USD 5.12 billion with 2031 projections showing USD 6.24 billion, growing at 3.35% CAGR over 2026-2031. This growth is driven by a mature pet ownership base, with 38.1% of households being single-person units increasingly relying on pets for companionship. Premiumization remains a key factor, as pet owners prioritize functional ingredients, organic formulations, and veterinary-prescribed therapeutic diets to ensure the health and well-being of their pets. Additional growth drivers include the rise of digital commerce, which provides convenience and access to a wider range of products, disaster-preparedness stockpiling due to Japan's vulnerability to natural disasters, and a shift toward smaller pets that are better suited for urban apartments with limited space. However, trends such as home-cooked pet meals, which appeal to owners seeking greater control over their pets' diets, and periodic import restrictions, which can disrupt supply chains, slightly constrain volume growth. The market remains fragmented, enabling competition among global leaders and domestic players based on quality, safety, and brand trust, with companies focusing on innovation and tailored offerings to meet evolving consumer preferences.

Key Report Takeaways

- By product category, food products held 73.55% of Japan pet food market share in 2025, and pet treats are projected to grow at a 5.86% CAGR through 2031.

- By pets, dogs accounted for a 48.35% share of the Japan pet food market size in 2025, and are set to expand at a 3.78% CAGR to 2031.

- By distribution channel, specialty stores captured 34.20% revenue share in 2025, while online channels are poised for a 4.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization of Pets Driving Premiumization | +1.2% | National, strongest in Tokyo and Osaka | Medium term (2-4 years) |

| Aging Pet Population Requiring Functional Diets | +0.8% | Nationwide, higher in rural prefectures | Long term (≥ 4 years) |

| E-commerce Penetration Expanding Accessibility | +0.6% | Urban centers first, now national | Short term (≤ 2 years) |

| Rise in Single-Person Households Boosting Ownership | +0.5% | Major cities Tokyo, Kanagawa, and Osaka | Long term (≥ 4 years) |

| Government Disaster-Prep Policies Spurring Stockpiling | +0.2% | Shizuoka, Kanagawa, and Tokyo | Short term (≤ 2 years) |

| Pet-Friendly Offices Increasing Weekday Treat Demand | +0.1% | Tokyo business districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Humanization of Pets Driving Premiumization

Japanese owners increasingly treat pets as family members, pushing demand for human-grade nutrition. Organic and natural formulations are rising rapidly, far outpacing the broader Japan pet food market. Clean-label requirements, single-protein recipes, and transparent sourcing dominate new product launches, while revised additive standards tighten compliance [1]Consumer Affairs Agency, “Food Additive Standards Revision 2024,” caa.go.jp. Brands that offer human-grade processing and traceable ingredients command 20-30% price premiums without deterring purchase intent. Growing veterinary endorsement of functional ingredients and the rise of pet cafés featuring organic menus further accelerate this trend, signaling a structural shift toward wellness-oriented pet diets in Japan.

Aging Pet Population Requiring Functional Diets

Senior pets now mirror Japan’s aging human demographic, prompting owners to prioritize therapeutic nutrition over reactive care. Veterinary diets are expanding rapidly, with standard formulations now featuring omega-3s, probiotics, and joint-support nutrients. Companies investing in age-specific research, clinical validation, and collaborations with veterinary clinics are capturing stronger brand loyalty among health-conscious households. Rising awareness of preventive health, coupled with increased veterinary visits and insurance adoption, is reinforcing the long-term shift toward specialized senior pet nutrition in Japan.

E-commerce Penetration Expanding Accessibility

Digital platforms bridge geographic access gaps by offering a far wider product range than traditional brick-and-mortar stores [2]Japan E-commerce Association, “E-commerce Market Survey 2024,” ecommerce.or.jp. Subscription models ensure a consistent supply, while improved cold-chain logistics maintain product freshness and safety. Direct-to-consumer brands bypass retail markups, enhancing affordability and strengthening customer loyalty. Growing smartphone penetration and E-commerce literacy further accelerate pet food adoption through online channels, especially in Tier-2 and Tier-3 cities.

Rise in Single-Person Households Boosting Ownership

Single-person households represent 38.1% of all homes and exhibit high per-person spending due to emotional attachment. Urban zoning reforms permitting pets in apartments amplify adoption rates. Premium food ranges benefit most, as owners prioritize quality over quantity. This demographic shift also fuels demand for convenient, portion-controlled packaging and ready-to-serve wet foods. Brands offering functional nutrition and personalized diet plans increasingly capture this segment, reflecting Japan’s trend toward individualized pet care and lifestyle integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Birthrate Limiting Long-Term Pet Additions | -0.4% | Nationwide, sharpest in rural areas | Long term (≥ 4 years) |

| Stringent Ingredient Regulations Raising Costs | -0.3% | All manufacturing sites | Medium term (2-4 years) |

| Home-Cooked Pet Meals Cannibalizing Packaged Sales | -0.2% | Social-media-savvy urban households | Short term (≤ 2 years) |

| Zoonotic-Scare Import Bans Causing Supply Shocks | -0.1% | Import-dependent categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Birthrate Limiting Long-Term Pet Additions

Japan’s fertility rate fell to 1.26 births per woman in 2024, shrinking the pool of first-time pet owners typically aged 25-35 [3]Ministry of Health, Labour and Welfare, “Vital Statistics 2024,” mhlw.go.jp. Rural depopulation accelerates the trend, tightening the future customer base even as existing owners spend more per pet. Long-term growth, therefore, rests on premiumization, not headcount expansion. The demographic imbalance shifts the Japan pet food market toward high-value, low-volume dynamics.

Stringent Ingredient Regulations Raising Costs

The Ministry of Agriculture, Forestry, and Fisheries's (MAFF’s) feed-safety standards and Consumer Affairs Agency's (CAA’s) additive lists require constant formulation reviews [4]Ministry of Agriculture, Forestry and Fisheries, “Pet Food Safety Law Implementation Guidelines,” maff.go.jp. Compliance drives up quality-control and testing expenses, squeezing margins for smaller brands. Larger companies absorb the costs through scale, reinforcing their competitive moat. This stringent regulatory environment acts as a structural restraint on market entry and innovation speed within the Japan pet food market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Food Dominance Drives Market Stability

Food accounted for 73.55% of Japan pet food market share in 2025, far ahead of treats, supplements, and veterinary diets. Dry kibble remains the volume anchor, while wet food gains share among premium brands emphasizing palatability and hydration. Treats rank second in revenue and show the fastest expansion due to indulgence trends. Nutraceuticals and veterinary diets remain smaller but premium-priced niches supported by professional endorsement and insurance coverage.

Pet treats are projected to post the highest 5.86% CAGR through 2031, outpacing the 3.35% baseline for the overall Japan pet food market. Veterinary diets represent a specialized but growing segment, benefiting from increased veterinary recommendations and pet insurance coverage that reduces cost barriers for therapeutic nutrition. The segment's growth reflects Japan's sophisticated veterinary care infrastructure and pet owners' willingness to invest in medically prescribed solutions.

By Pets: Dogs Lead Despite Market Maturation

Dogs captured 48.35% of Japan pet food market share in 2025, followed by cats and other small animals. Higher per-animal consumption and intensive premium spending place dogs atop revenue rankings. Cats exhibit steadier but lower volume growth, and niche species such as rabbits and birds remain small yet profitable through specialty diets.

The dog segment is forecast to expand at a 3.78% CAGR through 2031, followed by cats, while other pets grow steadily as urban apartment living modestly enlarges the exotic companion base. Breed-specific and life-stage formulas, especially for senior dogs, drive incremental sales. Other pets, including rabbits, birds, and small mammals, constitute a niche but growing segment driven by urban apartment living constraints that favor smaller companion animals. This segment's growth potential lies in specialized nutrition solutions for exotic pets and premium positioning that commands higher margins despite lower volume sales.

By Distribution Channel: Specialty Stores Face Digital Disruption

Specialty stores held 34.20% revenue share in 2025, followed by supermarkets and hypermarkets, with online channels and convenience outlets contributing smaller portions. Expertise, curated assortments, and bundled services keep specialty stores dominant in premium spend. Supermarkets compete on price and reach, while online channels match or exceed specialty selections and add subscription convenience.

Online channels are projected to deliver a 4.37% CAGR through 2031, the highest among channels, benefiting the overall Japan pet food market size. Specialty stores will grow steadily, while supermarkets and convenience outlets see slower expansion as foot traffic migrates to e-commerce. Omnichannel strategies, therefore, remain critical to defend market share across all touchpoints. The distribution landscape increasingly favors omnichannel strategies that combine physical touchpoints for product education with digital fulfillment for convenience and competitive pricing. Regulatory compliance factors create advantages for established distribution networks with temperature-controlled logistics and inventory tracking systems that ensure product integrity throughout the supply chain.

Geography Analysis

Japan's pet food market operates within a geographically concentrated demand structure where metropolitan areas drive premium consumption while rural regions maintain traditional purchasing patterns. The Tokyo-Osaka corridor accounts for approximately 60% of national pet food spending, reflecting higher household incomes, greater pet ownership rates, and stronger adoption of premium and functional nutrition products. Urban pet owners demonstrate willingness to pay 20-30% premiums for organic, natural, and veterinary-recommended formulations, creating market opportunities for companies positioning products at the intersection of health and convenience. Regional variations in pet ownership patterns reflect housing constraints, with apartment-dwelling urban residents favoring smaller pets requiring specialized nutrition solutions.

Rural prefectures face demographic headwinds that constrain long-term market growth, as aging populations and youth outmigration reduce both pet adoption rates and discretionary spending capacity. However, these regions maintain higher dog ownership rates per household, supporting demand for larger package sizes and value-oriented product positioning. The geographic distribution of specialty retail channels favors urban areas, while rural regions rely more heavily on agricultural cooperatives and general merchandise stores for pet food access. E-commerce penetration helps bridge this distribution gap, with rural customers increasingly adopting online purchasing for product variety and competitive pricing unavailable through local retail channels.

Disaster preparedness policies create regional demand variations based on seismic risk assessments and local government emergency planning requirements. High-risk prefectures including Shizuoka, Kanagawa, and Tokyo experience periodic stockpiling behavior that temporarily boosts sales volumes, particularly for shelf-stable dry food products. This geographic risk factor influences inventory management strategies and creates opportunities for companies offering emergency preparedness product bundles that combine nutrition with extended shelf life capabilities.

Competitive Landscape

Japan's pet food market exhibits moderate fragmentation with the major companies controlling a significant market share, creating a competitive environment that balances scale advantages with innovation opportunities for specialized players. Unicharm Corporation leads the domestic market share, leveraging its consumer goods expertise and distribution relationships to maintain premium positioning across multiple pet categories. Global players, including Mars Incorporated and Nestlé Purina, compete through established brand portfolios and international supply chain capabilities, while domestic specialists like Inaba-Petfood Co., Ltd. capture market share through category-specific innovation and local consumer insight.

The competitive landscape increasingly favors companies that combine regulatory compliance capabilities with innovation in functional nutrition and premium positioning. Recent M&A activity demonstrates industry consolidation trends, exemplified by General Mills' USD 1.45 billion acquisition of Whitebridge Pet Brands in November 2024, signaling continued strategic interest in premium pet nutrition platforms.

Technology adoption patterns focus on supply chain optimization, direct-to-consumer capabilities, and data-driven product development rather than disruptive innovation, reflecting the market's emphasis on quality and safety over technological novelty. Regulatory influence from the Ministry of Agriculture, Fisheries and Food (MAFF) Pet Food Safety Law creates competitive advantages for companies with established quality management systems and compliance infrastructure, while creating barriers for new market entrants lacking regulatory expertise.

Japan Pet Food Industry Leaders

Unicharm Corporation

Mars, Incorporated

Inaba-Petfood Co., Ltd.

Nestle (Purina)

Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nestlé (Purina) expanded its pyramid-shaped wet cat food range globally, including Japan, under the Gourmet Revelations and Fancy Feast Gems brands, strengthening premium positioning in the wet cat food segment and accounting for 30% of Purina's sales through distinctive packaging innovation.

- January 2025: Hill's Pet Nutrition announced new products in its Prescription Diet line, including low-fat options for dogs and stress management products for cats, designed to enhance taste preferences while meeting nutritional needs.

- December 2024: General Mills, Inc. finalized its USD 1.45 billion acquisition of Whitebridge Pet Brands’ premium cat food and pet treats portfolio, which includes Tiki Pets and Cloud Star. This move enhances its presence in the Asia-Pacific market. The growth of these premium, human-grade brands is anticipated to support the pet food market in Japan.

- November 2023: Unicharm has expanded its domestic pet-care production by establishing a new Peparlet factory in Shizuoka Prefecture. This investment reinforces its position in Japan's pet ecosystem, aligns with premiumization trends, and supports future growth in high-quality, locally produced pet food and related products.

Japan Pet Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel.Pet Food Product

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary Tract Disease | ||||

| Other Veterinary Diets |

Pets

| Cats |

| Dogs |

| Other Pets |

Distribution Channel

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft and Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary Tract Disease | |||||

| Other Veterinary Diets | |||||

| Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms